debt sustainability analysis at subnational...

TRANSCRIPT

Debt Sustainability Analysis at Subnational Level

Analytical Foundations

Sustained economic growth ...

... a critical objective of macroeconomic policy

... depends on a Sound Macroframework

... which depends on a Fiscal Policy

... whose main indicator is the Fiscal Deficit

Why DSA?

• Equity -- income distributional impact of tax and spending,

• Efficiency -- which taxes and spending improve economic efficiency and foster growth?

• Macroeconomic stabilization --consistent with monetary, exchange rate policies – by avoiding fiscal deficits and public debt accumulation

Fiscal Policy has several objectives...

Basic National Accounts

Gross Domestic Product

GDP = consumption(C) + investment(I) + exports(X) – imports(M)

Gross National Income

GNI = GDP - net income paid abroad(YF)

Gross National Disposable Income

GNDI = GNI + net transfers received from abroad(TRF)

GNDI is the amount of income available for an economy to consume and save, so GNDI = C + S

Macro Effects of the Fiscal Deficit Keynes revolution and the role of the fiscal deficit

Basic National Accounts

Given GNDI + YF - TRF = C + I + X – M and GNDI = C + S

we conclude that S – I = X – M – YF + TRF

where the savings-investment gap can be disaggregated into private and public sector gaps

S–I = (Sp–Ip) + (Sg–Ig) = (Sp–Ip) + (T–Cg–TRG–Ig)

Therefore, (Cg+TRG+Ig-T) = (Sp–Ip) + (M – X + YF – TRF)Budget deficit = Private S-I gap + BOP current account deficit

Macro Effects of the Fiscal Deficit

• The Keynesian analysis of fiscal policy must take off from the extreme short-run nature of the Keynesian model.

• Asset stocks are assumed fixed in the model, therefore, the consequences of the method by which the budget deficit is financed are not pursued.

How can the deficit G-T be financed?

Financing the Budget Deficit

There are four ways of financing the public sector deficit G-T:

G-T = money printing (seignorage) + foreign reserve use +foreign borrowing + domestic borrowing.

Financing the Budget Deficit

G-T = money printing + foreign reserve use + foreign borrowing + domestic borrowing.

Remember

• Foreign reserve use + money printing

emphasize the link between G-T and BOP CAD

is equal to the creation of credit by the central bank (which is an alternative to borrowing from markets)

Financing the Budget Deficit

G-T = money printing + foreign reserve use + foreign borrowing + domestic borrowing.

Each of the forms of financing can be associated with a major macro imbalance:

Money printing inflation

Foreign reserve use onset of exchange rate crises

Foreign borrowing external debt crises

Domestic borrowing higher interest rates and possibly explosive debt dynamics as borrowing leads to higher interest charges on debt and larger deficits.

Financing the Budget Deficit

Financing the Budget DeficitMoney printing

GovernmentRevenue

Inflation Rate0

A

Revenues from Seignorage

Run down foreign exchange reserves• This policy appreciates the exchange rate

which may slow down inflation (carried out not only through reserve use but also through increased foreign borrowing)

• It cannot be maintained unless fiscal policy is made compatible with lower inflation

• Use of international reserves to finance the deficit has a clear limit Private sector’s expectation can provoke capital flight

Financing the Budget DeficitUse of Foreign Exchange Reserves

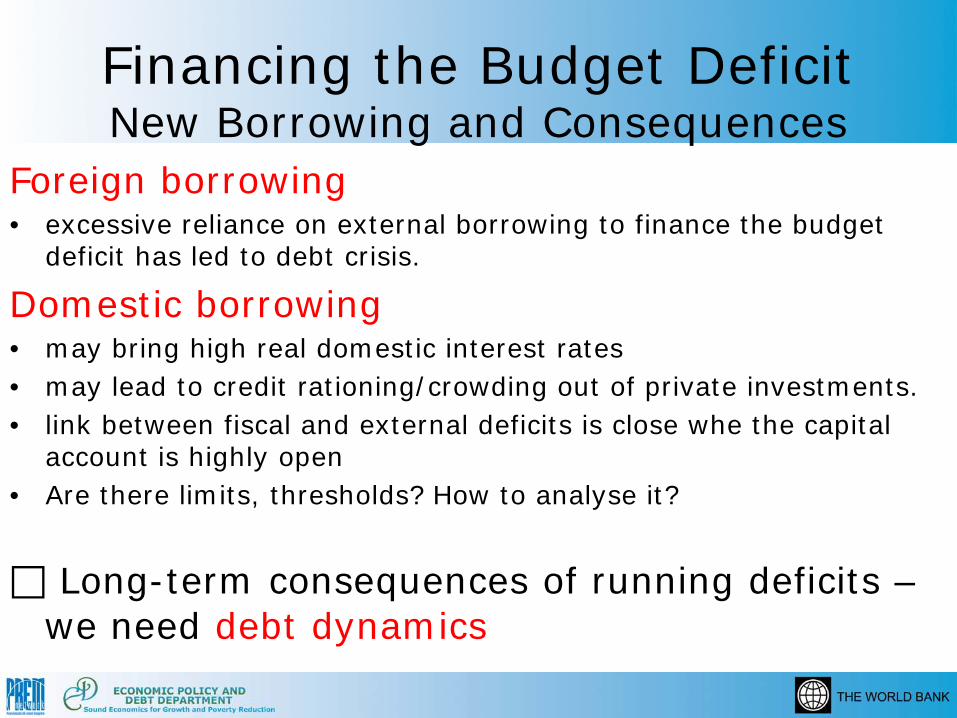

Foreign borrowing• excessive reliance on external borrowing to finance the budget

deficit has led to debt crisis.

Domestic borrowing• may bring high real domestic interest rates• may lead to credit rationing/crowding out of private investments.• link between fiscal and external deficits is close whe the capital

account is highly open• Are there limits, thresholds? How to analyse it?

Long-term consequences of running deficits –we need debt dynamics

Financing the Budget DeficitNew Borrowing and Consequences

Debt Sustainability Analysisat Subnational Level

Debt Sustainability Analysis (DSA) a. Basic notionsb. Debt dynamics

What is Debt Sustainability Analysis (DSA)?

– Analysis of the government’s capacity to meet its future financial obligations given

. fiscal policy (revenues, expenditures)

. financing strategy (sources of budget financing)

– Debt dynamics induced by budget deficits and borrowing decisions

– Forward-looking framework based on. long-term projections of macro/fiscal/debt variables. debt burden indicators driven by macro/fiscal variables. uncertainty deterministic vs stochastic scenarios

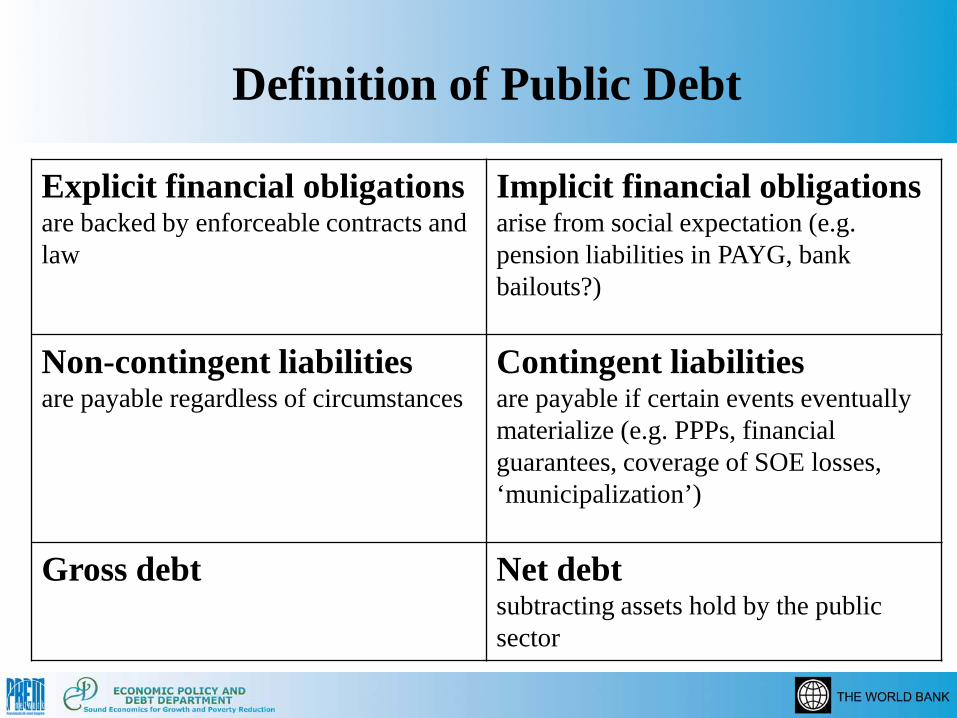

Definition of Public Debt

Public sector coverage

Central government (‘national’)

Regional and local government (‘subnational’)

SOEs

Instruments – Investor base - Maturity – Currency - Rates

Bank loans, loans extended by other government entities, marketable securities, arrears in wage payments, arrears in payments to suppliers

Risks and vulnerabilities

Definition of Public Debt

Explicit financial obligationsare backed by enforceable contracts and law

Implicit financial obligationsarise from social expectation (e.g. pension liabilities in PAYG, bank bailouts?)

Non-contingent liabilitiesare payable regardless of circumstances

Contingent liabilitiesare payable if certain events eventually materialize (e.g. PPPs, financial guarantees, coverage of SOE losses, ‘municipalization’)

Gross debt Net debtsubtracting assets hold by the public sector

• Public Sector borrowing requirement Central Government Subnational (local) Government Public Enterprises

• Overall Balance= Total Revenue – Total Expenditure (Cash or Accrual)

• Primary Balance= Overall Balance – Interest Payments

Measuring the Fiscal Deficit

Assessing Debt Sustainability –3 approaches

– Projections of debt burden indicators (‘accounting’)

Identifying macro/fiscal drivers of debt dynamics(primary deficit, interest rates, real GDP growth, inflation, exchange rate)

– Debt sustainability indicators (‘analytical’)

Analytical definitions of solvency (e.g. stable debt, IBC, debt target)

Fiscal adjustment needed to satisfy solvency condition (e.g. debt-stabilizing primary balance, EU indicators S2 and S1)

– Debt thresholds and debt distress risk (‘empirical’)

Estimation of critical values of debt burden indicators that limit zones of acceptable/unacceptable probability of debt distress (e.g. Bank-Fund DSF thresholds for external debt)

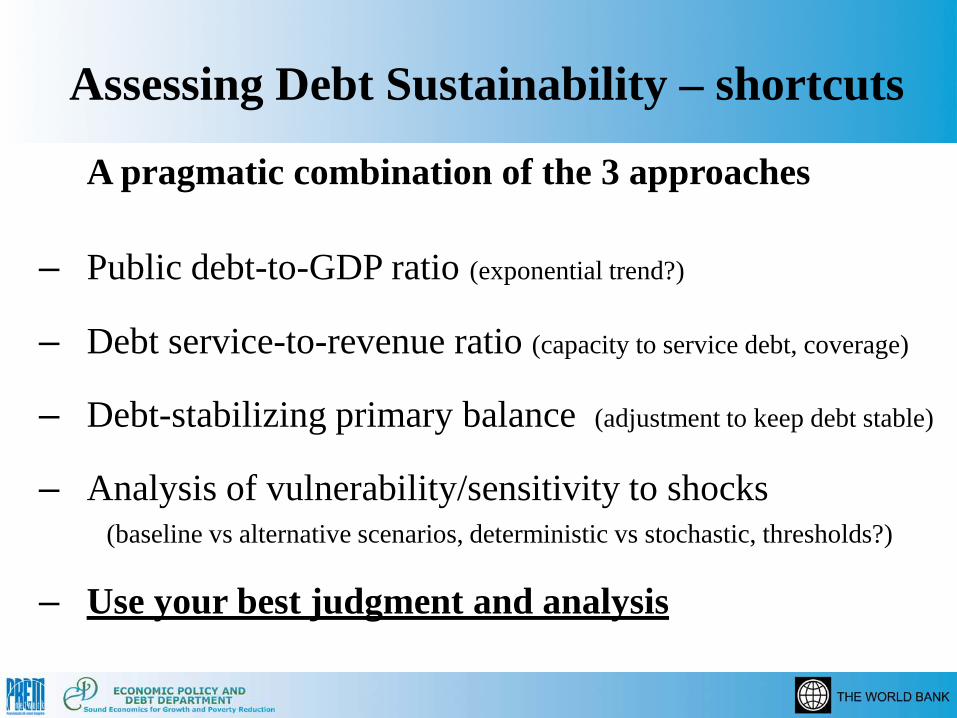

Assessing Debt Sustainability – shortcuts

A pragmatic combination of the 3 approaches

– Public debt-to-GDP ratio (exponential trend?)

– Debt service-to-revenue ratio (capacity to service debt, coverage)

– Debt-stabilizing primary balance (adjustment to keep debt stable)

– Analysis of vulnerability/sensitivity to shocks (baseline vs alternative scenarios, deterministic vs stochastic, thresholds?)

– Use your best judgment and analysis

How does the government accumulate debt?

Economic principleBorrowing covers the excess of spending over income

Accounting identityChange in the value of debt D is given by Dt+1 – Dt = expenditures – revenues + other factors

accounting overall balance adjustment factor(deficit or surplus) (e.g. valuation effect)

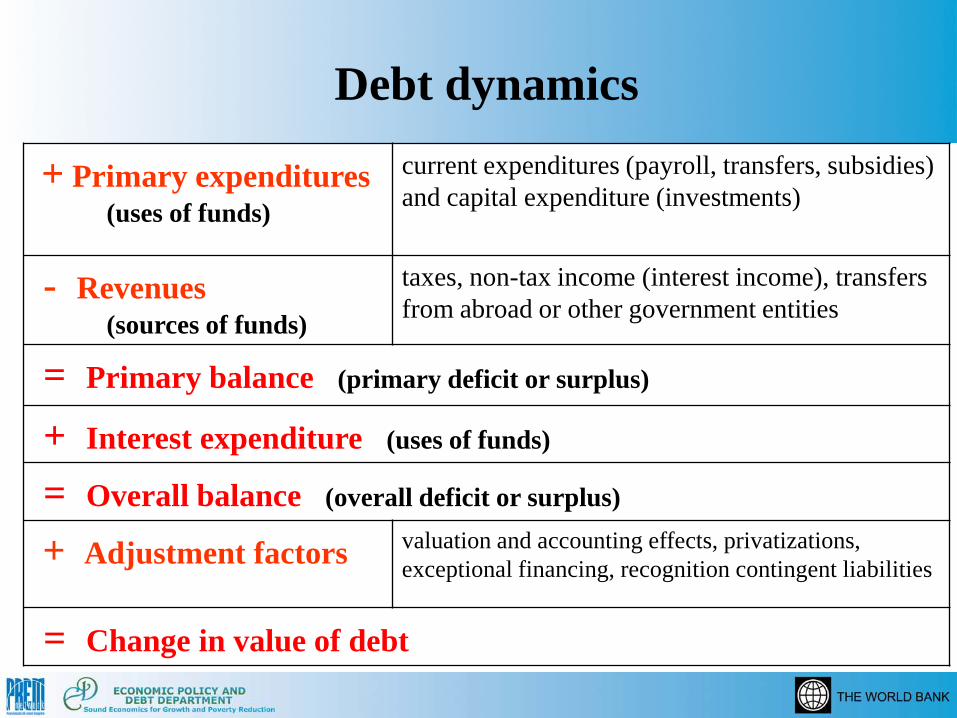

Debt dynamics

Debt dynamics

+ Primary expenditures (uses of funds)

current expenditures (payroll, transfers, subsidies) and capital expenditure (investments)

- Revenues (sources of funds)

taxes, non-tax income (interest income), transfers from abroad or other government entities

= Primary balance (primary deficit or surplus)

+ Interest expenditure (uses of funds)

= Overall balance (overall deficit or surplus)

+ Adjustment factors valuation and accounting effects, privatizations, exceptional financing, recognition contingent liabilities

= Change in value of debt

Debt dynamics - Analytics

Budget and borrowing flows

D = debt, with f = external and d = domesticG – T = primary deficit

Value of debt and change in the value of debt

i = nominal interest rate, with f & de = exchange rate (NC per unit of FC)

𝐺𝐺 − 𝑇𝑇 + 𝑖𝑖𝑑𝑑𝐷𝐷𝑑𝑑 + 𝑖𝑖𝑓𝑓𝑒𝑒𝐷𝐷𝑓𝑓 = ∆𝐷𝐷𝑑𝑑 + 𝑒𝑒∆𝐷𝐷𝑓𝑓

Debt dynamics decomposition

𝐷𝐷 = 𝐷𝐷𝑑𝑑 + 𝑒𝑒𝐷𝐷𝑓𝑓 → ∆𝐷𝐷 ≈ ∆𝐷𝐷𝑑𝑑 + 𝑒𝑒∆𝐷𝐷𝑓𝑓 + ∆𝑒𝑒𝐷𝐷𝑓𝑓

∆𝐷𝐷 = 𝐺𝐺 − 𝑇𝑇 + 𝑖𝑖𝑑𝑑𝐷𝐷𝑑𝑑 + 𝑖𝑖𝑓𝑓𝑒𝑒𝐷𝐷𝑓𝑓 + ∆𝑒𝑒𝐷𝐷𝑓𝑓

Debt-to-GDP dynamics - Analytics

Debt-to-GDP ratio

Y = nominal GDP d = D/Y is debt-to-GDP ratio dd = Dd/Y is domestic debt ratio df = eDf/Y is external debt ratio

Debt-to-GDP dynamics decomposition

Change in debt-to-GDP

ratio

Primary deficit

as share of GDP

Real interest rate

effect

Real growth effect

Real exchange rate gains/losses

Debt-to-GDP dynamics - Summary

Debt-to-GDP dynamics

Primary balance

Endogenous debt dynamics

Other adjustments

Real interest rates

Real GDP growth

Changes in real exchange rate

Main referencesBurnside, Craig (Editor), 2005. Fiscal Sustainability in Theory and

Practice – A Handbook, Washington, DC, World Bank, Chapters 2, 3 and 4.

Ianchovichina, Elena, Liu, L. and Nagarajan, M., 2006. “Subnational Fiscal Sustainability Analysis - What Can We Learn From Tamil Nadu?” World Bank Policy Research Working Paper No. 3947.

Ianchovichina, Elena, Liu, L., 2008. Subnational Fiscal Sustainability Analysis. Washington, DC, World Bank, PREM Note No. 117.

Stanley Fisher and W. Easterly, 1990. The economics of the government budget constraint. Washington, DC, The World Bank Research Observer, Vol.5, No. 2 (July 1990).

Debt Sustainability Analysis (DSA) Basic notions and Debt dynamics