debt management: coordination with macroeconomic...

TRANSCRIPT

Debt Management: Coordinationwith Macroeconomic Policieswith Macroeconomic Policies

DeMPA Tool TrainingSingapore

September 21-25, 2009

Outline1. Coordinating DeM with Fiscal and

Monetary Policy: Why? What are therelevant or potential issues orproblems?

2. DPI-3: Debt Management Strategy (a2. DPI-3: Debt Management Strategy (aquick revisiting/reminder)

3. DPI-6: Coordination with Fiscal Policy4. DPI-7: Coordination with Monetary

Policy5. Proposed ongoing revision

2

Coordinating DebtManagement with Fiscal andManagement with Fiscal and

Monetary Policy: Why?

3

Policy Objective Instrument(s)DebtManagement

• To minimize long-term debtservicing cost, subject toattaining a prudent level ofrisk.

• Manage the composition of thedebt portfolio –currency andrate (floating/fixed)composition, maturity, etc.

• Anchored by a debt strategy

Fiscal Policy • To impose the leastdistorting expenditure

• Manage the composition ofspending and taxation.distorting expenditure

policies/taxes that wouldprovide (public) goods &services, and achievedistributive objectives ona sustainable basis,subject to prudent andsustainable debt levels.

spending and taxation.• Manage the levels of deficits

and debt.• Anchored by a Medium Term

Expenditure Framework/Fiscaltargets.

Monetary/ExchangeRate Policy

• To achieve price stability • Implemented through interestrates, exchange rate ormonetary aggregates (the finalgoal is low and stable inflation)4

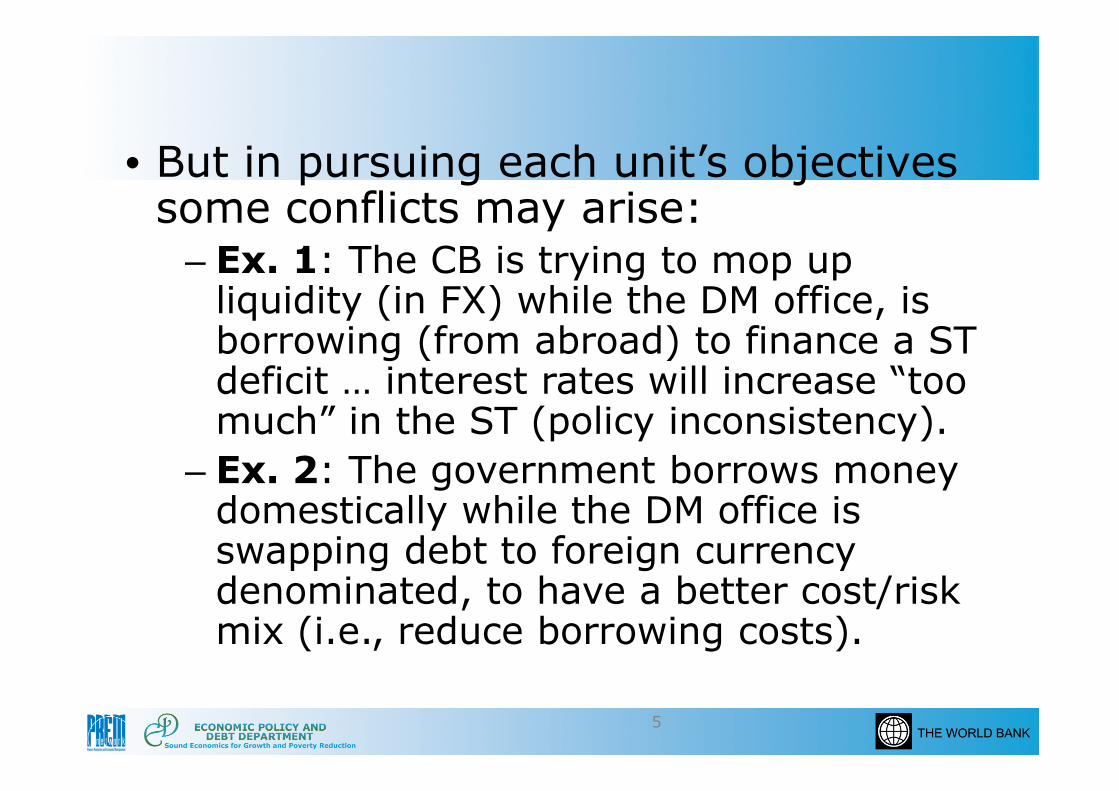

• But in pursuing each unit’s objectivessome conflicts may arise:

– Ex. 1: The CB is trying to mop upliquidity (in FX) while the DM office, isborrowing (from abroad) to finance a STdeficit … interest rates will increase “toodeficit … interest rates will increase “toomuch” in the ST (policy inconsistency).

– Ex. 2: The government borrows moneydomestically while the DM office isswapping debt to foreign currencydenominated, to have a better cost/riskmix (i.e., reduce borrowing costs).

5

• Further:– Ex. 3: The government is working on

next year budget and is “forecasting”debt repayments, while the DM officehas the exact information on whenpayments will become due (nopayments will become due (nouncertainty)

– Ex. 4: The DM office borrows in FXwhile the Ministry of Finance’s debtsustainability assessment indicatesthat, given the country’s exports, FXdebt is near its upper bound.

6

• And further:– The MoF is imposing a levy on external

(domestic) borrowing to dampencapital inflows (over borrowing), whilethe DM office is tapping foreignmarkets to attain a preferable cost/riskmarkets to attain a preferable cost/riskmix

– If the CB acts as a government agent inmanaging its debt, there is an obviousconflict of interest when movinginterest rates or the exchange rate (twohats, one head)

7

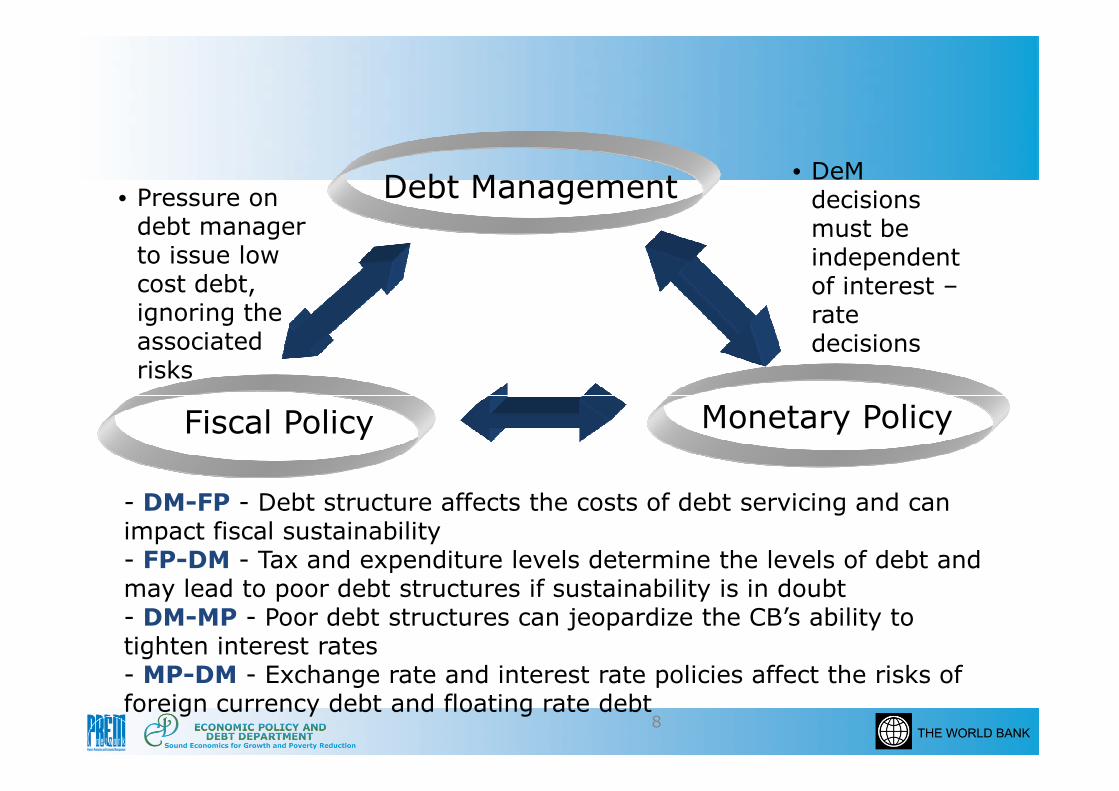

Debt Management• Pressure ondebt managerto issue lowcost debt,ignoring theassociatedrisks

• DeMdecisionsmust beindependentof interest –ratedecisions

8

Fiscal Policy Monetary Policy

- DM-FP - Debt structure affects the costs of debt servicing and canimpact fiscal sustainability- FP-DM - Tax and expenditure levels determine the levels of debt andmay lead to poor debt structures if sustainability is in doubt- DM-MP - Poor debt structures can jeopardize the CB’s ability totighten interest rates- MP-DM - Exchange rate and interest rate policies affect the risks offoreign currency debt and floating rate debt

• What emerges is that the DM office,as an operational branch of theGovernment, needs to be wellcoordinated with both the Ministry ofFinance and the CB

– The DM office is subordinated to the– The DM office is subordinated to thepolicies and strategies of both the CBand the Ministry of Finance

– Must have a clear mandate from thegovernment and separate its role fromthat of the CB if the latter acts as agovernment debt manager agent

9

DPI-3:Debt ManagementStrategyStrategy

– Quality (comprehensivenessand degree of details)

– Process by which it is set

10

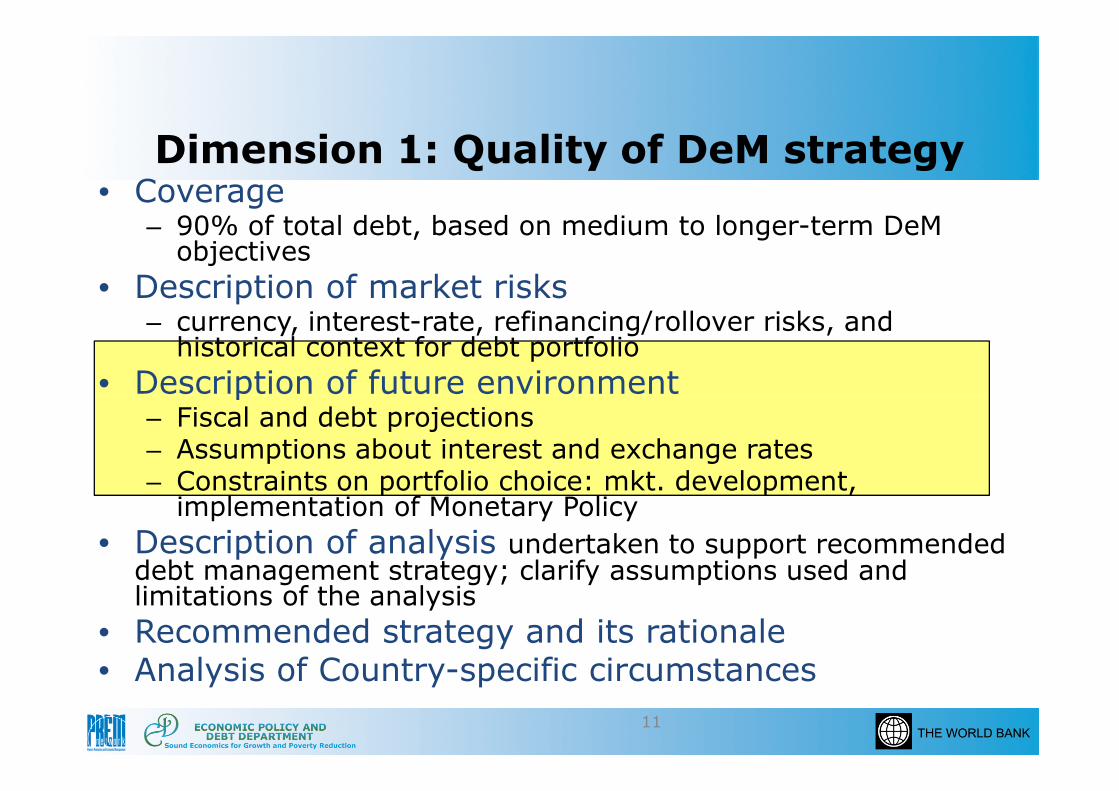

Dimension 1: Quality of DeM strategy• Coverage

– 90% of total debt, based on medium to longer-term DeMobjectives

• Description of market risks– currency, interest-rate, refinancing/rollover risks, and

historical context for debt portfolio

• Description of future environment• Description of future environment– Fiscal and debt projections– Assumptions about interest and exchange rates– Constraints on portfolio choice: mkt. development,

implementation of Monetary Policy

• Description of analysis undertaken to support recommendeddebt management strategy; clarify assumptions used andlimitations of the analysis

• Recommended strategy and its rationale• Analysis of Country-specific circumstances

11

Dimension 2: Process

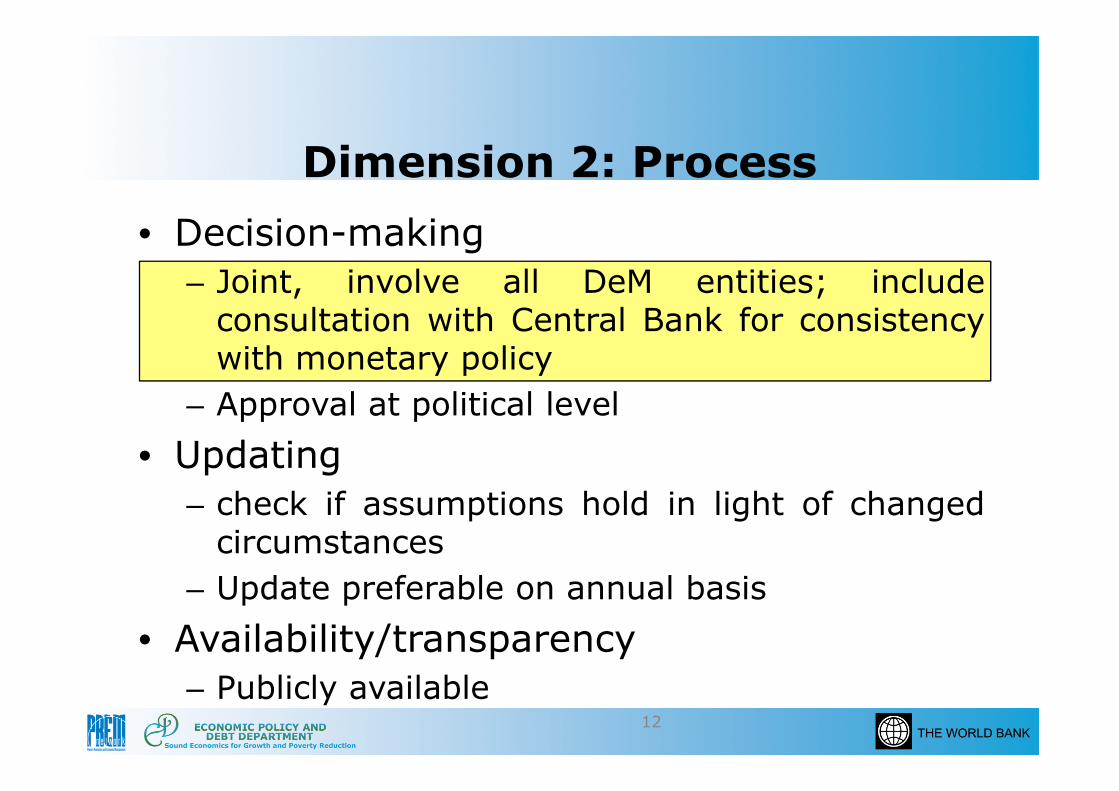

• Decision-making

– Joint, involve all DeM entities; includeconsultation with Central Bank for consistencywith monetary policy

– Approval at political level– Approval at political level

• Updating

– check if assumptions hold in light of changedcircumstances

– Update preferable on annual basis

• Availability/transparency

– Publicly available12

Scores Summary

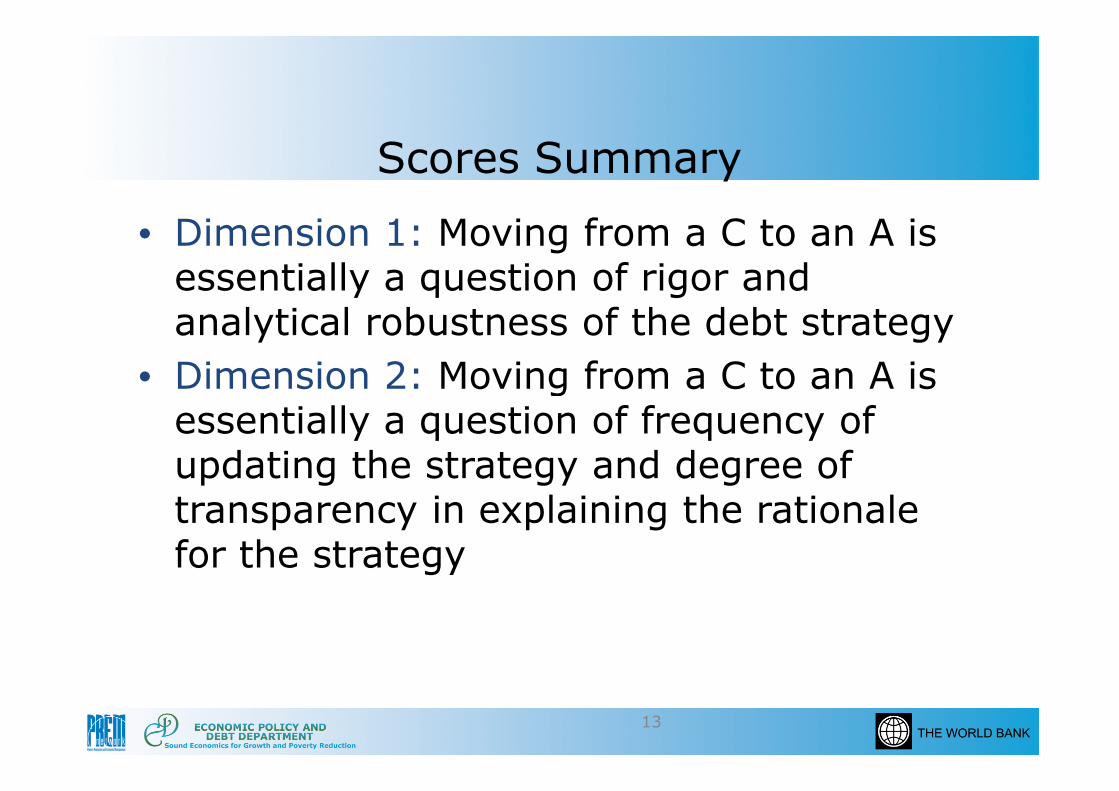

• Dimension 1: Moving from a C to an A isessentially a question of rigor andanalytical robustness of the debt strategy

• Dimension 2: Moving from a C to an A is• Dimension 2: Moving from a C to an A isessentially a question of frequency ofupdating the strategy and degree oftransparency in explaining the rationalefor the strategy

13

DPI-6 Coordination with FiscalDPI-6 Coordination with FiscalPolicy

14

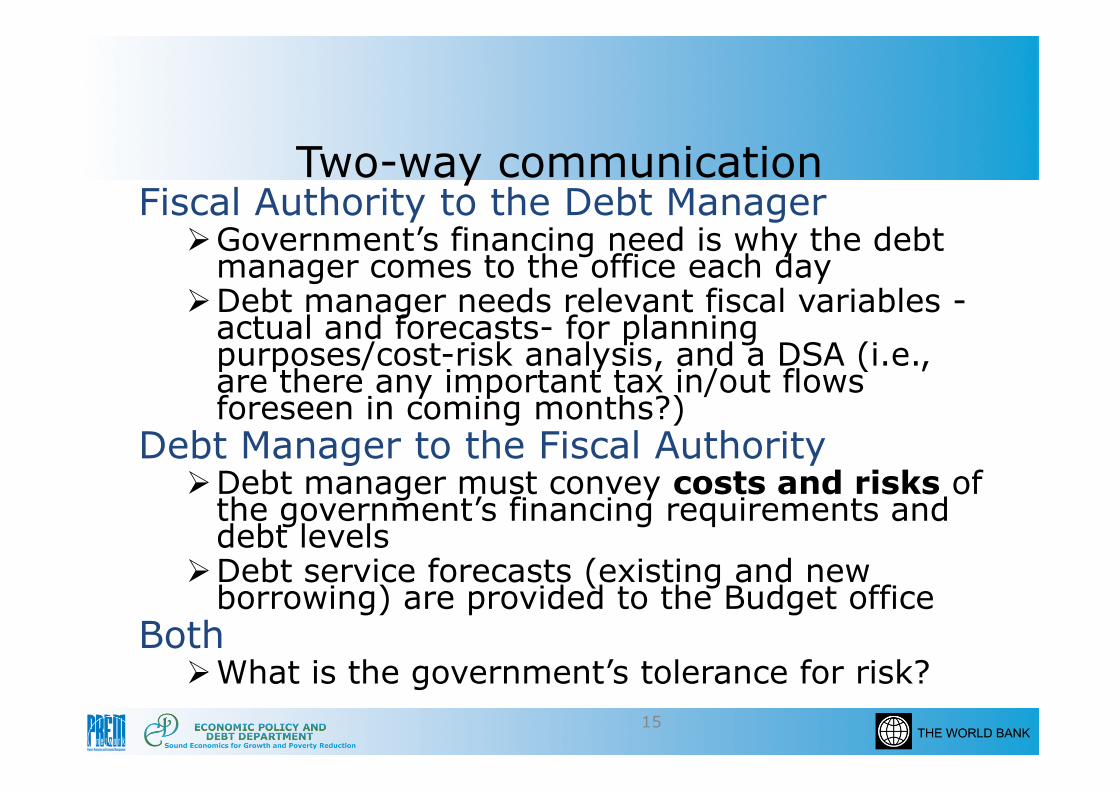

Two-way communicationFiscal Authority to the Debt ManagerGovernment’s financing need is why the debt

manager comes to the office each dayDebt manager needs relevant fiscal variables -

actual and forecasts- for planningpurposes/cost-risk analysis, and a DSA (i.e.,are there any important tax in/out flowsforeseen in coming months?)are there any important tax in/out flowsforeseen in coming months?)

Debt Manager to the Fiscal AuthorityDebt manager must convey costs and risks of

the government’s financing requirements anddebt levels

Debt service forecasts (existing and newborrowing) are provided to the Budget office

BothWhat is the government’s tolerance for risk?

15

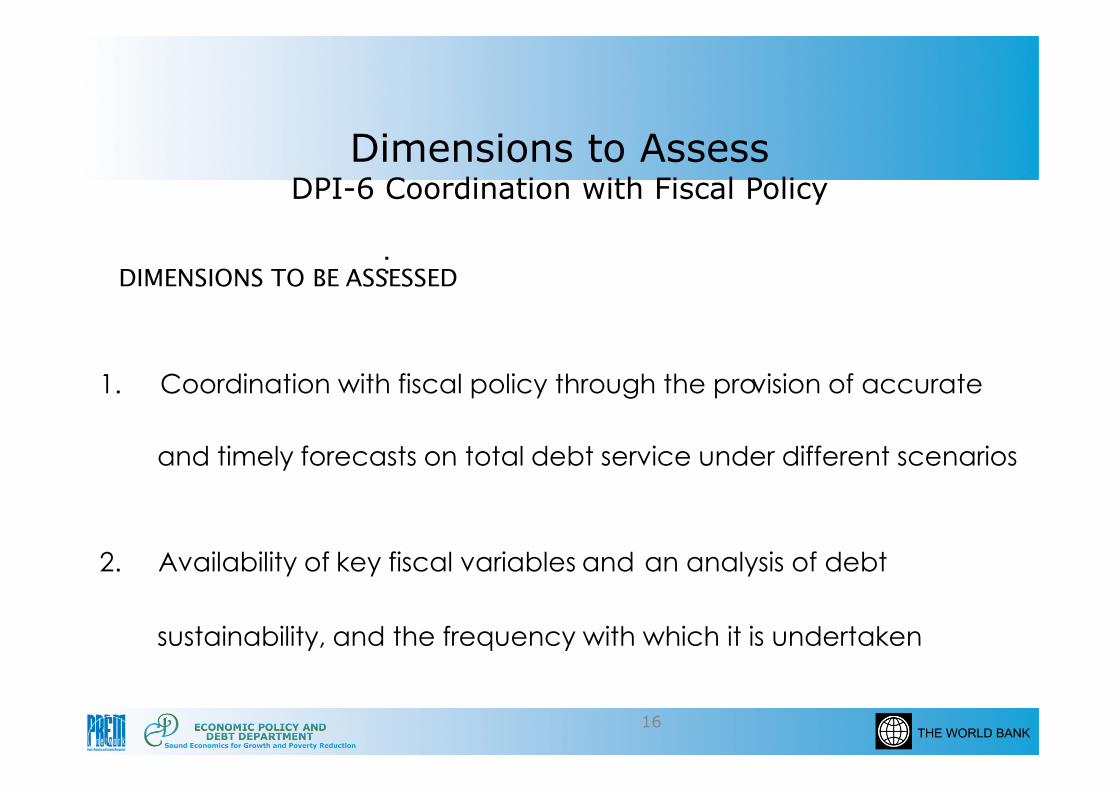

Dimensions to AssessDPI-6 Coordination with Fiscal Policy

DIMENSIONS TO BE ASSESSED:

1. Coordination with fiscal policy through the provision of accurate

16

1. Coordination with fiscal policy through the provision of accurate

and timely forecasts on total debt service under different scenarios

2. Availability of key fiscal variables and an analysis of debt

sustainability, and the frequency with which it is undertaken

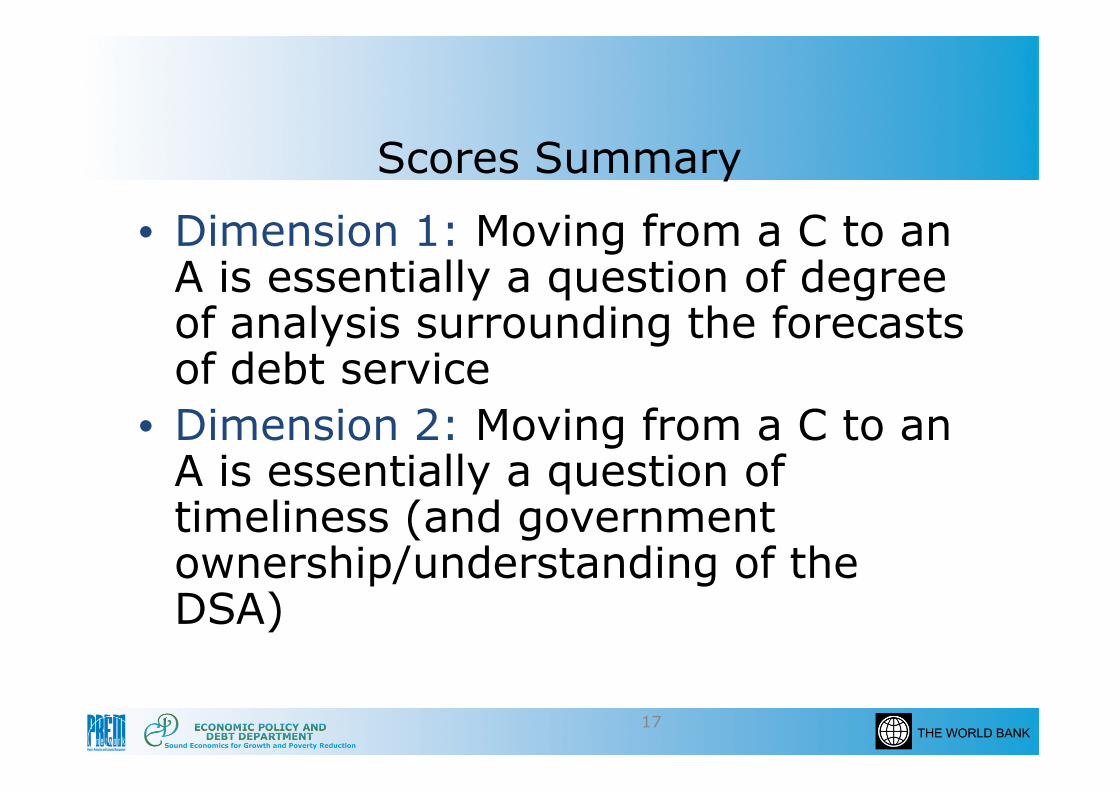

Scores Summary

• Dimension 1: Moving from a C to anA is essentially a question of degreeof analysis surrounding the forecastsof debt service

• Dimension 2: Moving from a C to anA is essentially a question oftimeliness (and governmentownership/understanding of theDSA)

17

Coordination with Fiscal Policy

AB

Dim1

BUDGETC

FiscalData

MarketRates

New & ExistingDebt

Financing GapNew BorrowingDebt StrategyCS-DRMS

or DMFAS

18

A

B

C

Dim2

FISCALVariablesand DSA

DeMEntity

Total centralgovt

debt ServiceForecasts

Within past 3 years

Updated Annually

DeM entity(s) hasaccess to fiscal

variables and DSAundertaken bygovernment

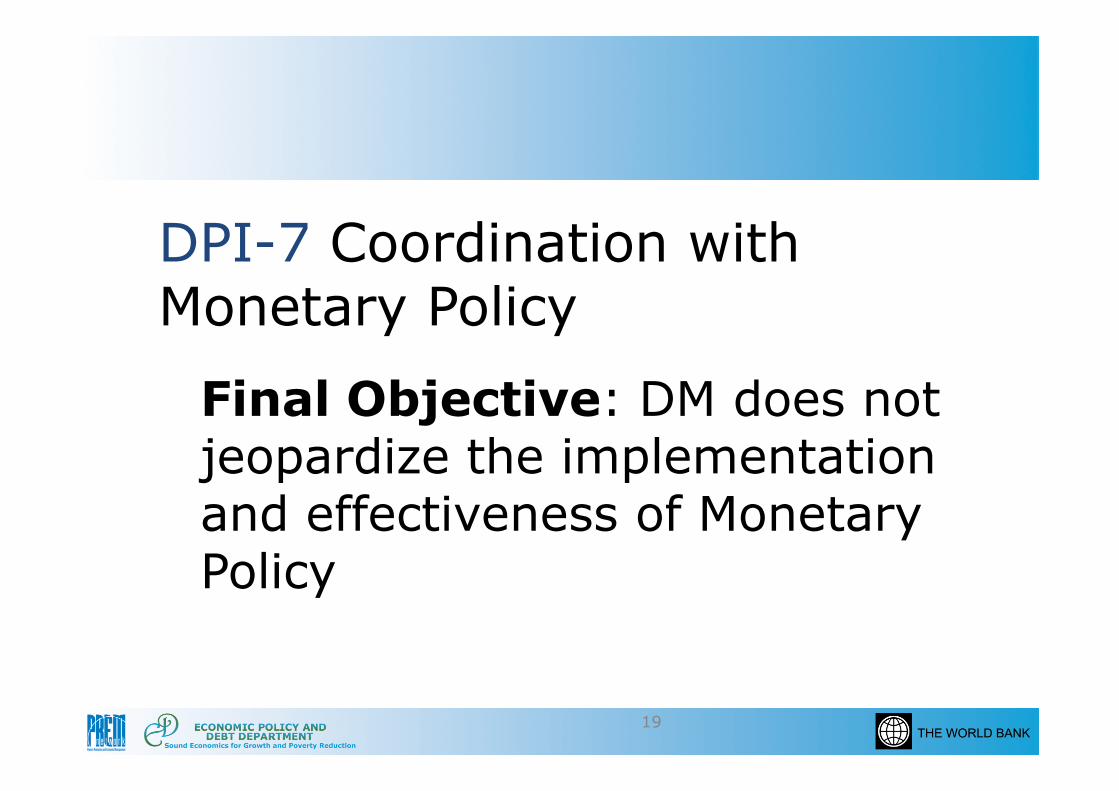

DPI-7 Coordination withMonetary Policy

Final Objective: DM does notFinal Objective: DM does notjeopardize the implementationand effectiveness of MonetaryPolicy

19

Debt Management and Monetary Policy Functions

Low-income country characteristics maynot allow for clear separation betweenDeM and MPo Level of financial developmento Capacity constraints

Debt management is not a core CentralDebt management is not a core CentralBank function

In this context, transparency and sharingof information is keyo Clarity about domestic debt issuances for

monetary policy purposes and fiscal policypurposes

o Domestic debt data to the MoFo MoF to CB: central government cash flow

20

Debt Management and Monetary PolicyFunctions

Why are separation and information flowsimportant?

Avoid policy conflicts, maintain (market)credibility and lower costso Market Development (MD): Market must know what is

issued to cover the fiscal gap (otherwise in the darkissued to cover the fiscal gap (otherwise in the darkabout fiscal risks and cannot properly price issuances)

o Price stability (PS): Central bank should not beperceived as compromising key objective of pricestability to meet Debt Management objectives

o Example: cost minimization objective cannot be seen toinfluence CB’s interest rate decision

o Both MD and PS: Importantly, a cost minimizationobjective should not be taken as a free pass for the CBto issue credit to the government

21

Dimensions to AssessDPI-7 Coordination with Monetary Policy

DIMENSIONS TO BE ASSESSED:

1. Clarity of separation between monetary operations and debt management

22

1. Clarity of separation between monetary operations and debt managementtransactions, and coordination through regular information sharing on debttransactions and central government’s current and future cash flows with theCentral Bank

2. Extent of a limit to direct access of resources from the Central Bank

Scores Summary

Dimension 1: Moving from a C to an A isessentially a question of periodicity of informationsharing. Fundamental is the clarity of separationbetween MP and DeM transactions

Dimension 2: Moving from a C to an A isessentially a question of the tenor of the limit toaccessing central bank financing

23

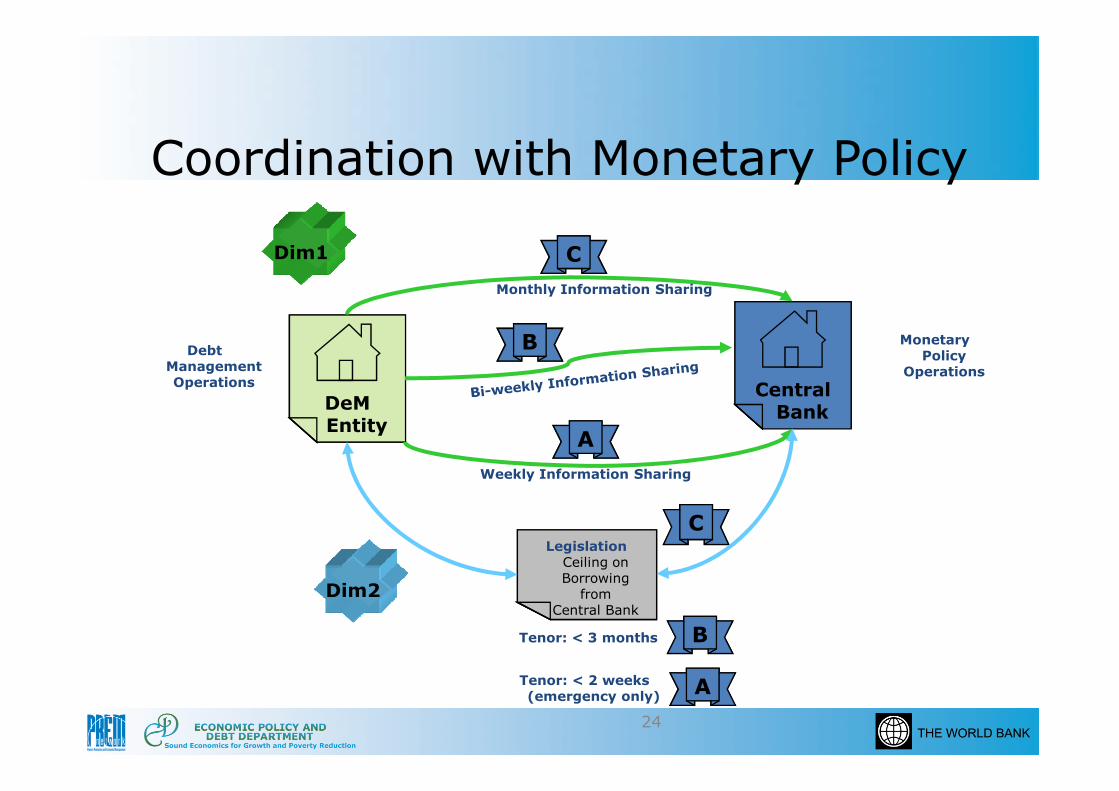

Coordination with Monetary Policy

Central

B

Dim1 C

DeM

Monthly Information Sharing

DebtManagementOperations

MonetaryPolicy

Operations

24

CentralBank

A

Dim2

DeMEntity

C

B

A

Weekly Information Sharing

LegislationCeiling onBorrowing

fromCentral Bank

Tenor: < 3 months

Tenor: < 2 weeks(emergency only)

Proposed ongoing revision

25

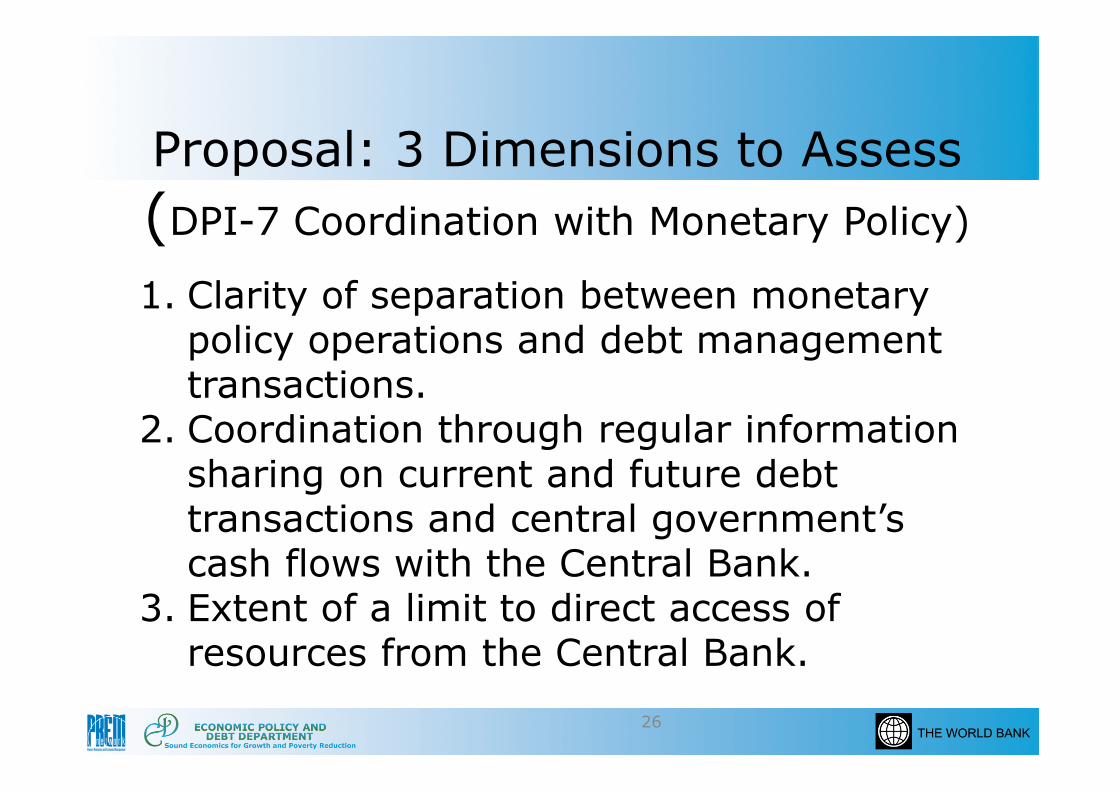

Proposal: 3 Dimensions to Assess

(DPI-7 Coordination with Monetary Policy)

1. Clarity of separation between monetarypolicy operations and debt managementtransactions.

26

transactions.2. Coordination through regular information

sharing on current and future debttransactions and central government’scash flows with the Central Bank.

3. Extent of a limit to direct access ofresources from the Central Bank.

Proposed Scores Summary

Dimension 1: Moving from a C to an A is amatter of how clear, formal and publiclyknown is the separation between MP andDeM transactions.

Dimension 2: Moving from a C to an A isDimension 2: Moving from a C to an A isessentially a question of periodicity of theinformation sharing meetings.

Dimension 3: Moving from a C to an A isessentially a question of the tenor of thelimit to accessing central bank financing.

27

Thank you!

28