dealer business journal september 2014

DESCRIPTION

Marketing, Advertising, Small Business, Used Car Dealerships, Used Car Sales, Buy Here-Pay Here, BHPH, Auto SalesTRANSCRIPT

September 2014 DEALER BUSINESS JOURNAL | 1...Your Success Is Our Business

How to sell with the “Millennial Sales Person”PAGE 34

Building a brand for your dealership doesn’t have to cost a lot of money. Make the most outof your marketingbudget with theseideas and tips.

Page 22

ALSO INSIDE:

September 2014 DEALER BUSINESS JOURNAL | 3...Your Success Is Our Business

September 2014 DEALER BUSINESS JOURNAL | 1

...Your Success Is Our Business

How to sell with

the “Millennial

Sales Person”

PAGE 18

Building a brand for your dealership

doesn’t have to cost a lot of money.

Make the most out

of your marketing

budget with these

ideas and tips.

Page 22

ALSO INSIDE:Contents

IN EVERY ISSUE 4 CORNER OFFICE

5 UPCOMING EVENTS

6 BHPH BOOT CAMP

8 PAYMENT PROCESSING

36 INDUSTRY NEWS

LEGAL & LEGISLATIVE BUSINESS OPERATIONS

Legal Opinion12 The Facts, Ma’am, Just the Facts Internet sales are very

commonplace these days, but when the deals are interstate all the facts need to be examined.

By Tom Hudson

CFPB Concerns14 Every Customer’s Got a

Complaint! The CFPB is considering

expanding the current Policy Complaint Database to include publishing customer complaint narratives.

By Eric L. Johnson

General Counsel16 Ten Things to Know About

Severance Agreements If you have to let an employee

go, consider protecting yourself from potential liability with a severance agreement.

By Debra Dawn

Learn to Lead18 Four Ways to Keep a

Fanatical Focus Great leaders are able to

move forward on their goals with discipline and focus unmatched by others. Here’s how to get that same focus.

By Dave Anderson

Volume 11, Issue 9 September 2014

LEADERSHIP & TRAINING

COVER STORY

Business Basics20 Buy Here-Pay Here

Procuring Capital You need cost-effective capital

to have long-term success. Build solid relationships with financial institutions to position yourself where you need to be.

By Robert N. Parnas

Business Development30 Roadblocks to CRM Success Get the most out of your CRM

by avoiding these common obstacles that might be standing in your way.

By Greg Wells

22 Do It Yourself Marketing It is possible to brand yourself,

advertise correctly and build strategic relationships on your own as a small business owners. You just need a tutorial on how to do it.

By Christy Taylor

SALES & SERVICE

Smart Strategy34 How to Sell with the

“Millennial Sales Person” There has been a lot of attention on how to sell to the millennial customer,

but not as much on training the millennial sales person.

By A.J. Ager

4 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

Dealer Business Journal3700 S. Tamiami Trail, Sarasota, FL 34239Ph: 800.966.8733 | Fax: 941.371.2874

Executive PublisherChristopher M. Leedom | [email protected]

Contributing WritersDave Anderson | [email protected]

David Brotherton | [email protected]

Debra Dawn | [email protected]

Tom Hudson | [email protected]

Guest Columnists

A.J. Ager | Ferguson Buick GMC

Eric L. Johnson | [email protected]

Robert N. Parnas | CliftonLarsonAllen

Christy Taylor | Dealer Business Journal

Greg Wells | AllCall Automotive Contact Center

FOR QUESTIONS REGARDING SUBSCRIPTIONS CALL 800.966.8733or subscribe online at DealerBusinessJournal.com

ADVERTISING INQUIRIES CALL 941.371.7999OR [email protected]

DISCLAIMER: The information included in this publication is obtained from sources believed reliable and has been produced with reasonable care in production and editing. It is not intended to be legal, accounting, tax, technical or other professional advice. Readers are advised to consult a professional for ap-plication in their particular situation. Copyright 2013 Leedom and Associates, LLC. All Rights Reserved. Content may not be photocopied, reproduced or redistributed without written permission. Dealer Business Journal is a publi-cation of Leedom and Associates, LLC.

POSTMASTER: Send change of address form to Dealer Business Journal, 3700 S Tamiami Trail, Sarasota, FL 34239

LEEDOM GROUP

Corner OfficeThoughts and Observations on the Marketplace

This month our theme for this issue is marketing and advertising – how to build your brand as a small business. We think this topic is timely given

it is the time of the year when dealers start to think (or should be thinking) about their budgets moving into a new year. For most dealers marketing and advertising consumes between four percent on the low end and as much as 10 percent of a dealers gross profit. Next to payroll it is quite often the next largest expense category. Fundamentally, each and every dealer must sell a certain number of vehicles each month with a balance of new as well as repeat customers just to “break even.” Call that “your number.” To that end, it is critical that you make sure all, or as many potential customers in your market are aware of your inventory, services offered, and your friendly and capable staff all while doing it in a way that makes financial sense. You must turn a profit, right? Not just meet the break even number. I want to share some benchmarks for marketing and advertising with you. The benchmark for advertising and marketing costs per unit in our Twenty Groups program is approximately $250. Probably a bit more if you are conventional retail dealers, a bit less if you are BHPH. That amount includes promotional items and advertising expenses as well as referral fees. When you’re selling 100-plus units a month that becomes a big number quickly. I must

caution you, however, that $200 per unit is an average. If your dealership is in a large metropolitan area where advertising costs are high, your average cost per unit sold rises quickly. I have seen some “advertising junkies” that are north of $500 per unit sold. If you are in a more rural, or non-metro area you may be able to budget half that amount and get the results you desire. I have also observed dealers in metro or non-metro areas that are less than $100 per car sold. What I’d like to discuss is a comprehensive approach to advertising and marketing, and how branding, repeat and referral business and call to action all work together to make your dealership stand out from the competition.

Much of what we do in this business depends upon our people. They are likely the single most critical factor in marketing your dealership to your customers. They must be friendly, informed, go-getters and professional. If your customers are turned off by the staff, they’re not likely to come back and they definitely will give their friends and family the wrong message about your store. It all starts with first impressions right? Hire with deliberation and end the relationship quickly if your employees are not giving you the desired result. Your customers will notice. I believe a friendly, welcoming and knowledgeable staff is the single biggest asset once a potential customer calls on your store. I can’t tell you how many times I have been onsite in dealerships and heard sales folks take a call, only to fail to get a name and number – therefore, no follow up opportunity whatsoever.

DEALER BUSINESS

A L E E D O M G R O U P P U B L I C AT I O N

JOURNAL

September 2014 DEALER BUSINESS JOURNAL | 5...Your Success Is Our Business

Chris LeedomExecutive Publisher

Spartan-Partners.com

Buy Here Pay Here | Indirect Lenders | Loan Originators | Credit Unions

Nationwide Lines of Credit and Bulk Purchasing for:

Bulk PurchasesLines of Credit

• Immediate Postitive Cash Flow• Capital for Replacement Inventory• Dealer Retains Servicing and Collections

SPARTAN FINANCIAL PARTNERS. BETTER THAN A BANK for BHPH.

• More Cash Up Front• Quick Funding• No Seasoning Requirements

Honest, Straightforward Pricing… No Waiting for Bonus Pools, No Performance Fees

Spartan Line of Credit Clients IncreaseTheir Portfolio an Average of 165% !

Are You Leveraging Your BHPH Portfolio for Cash?

Interested in Point of Sale Financing? Call our American Credit Acceptance team today! (866)202-6912

Today, your window to the world is the Internet. Make sure your website is easy to use, navigate and tells a bit of history about your store. Vehicles for sale need to have plenty of photos and a good description of condition. Make sure your website spells out your biggest advantage over the other lots. If you are in BHPH you should cite the fact that you provide credit to people who cannot get financed elsewhere. If you are a high-line dealer you might talk about selection and quality of inventory. You need to decide what you do best and you should emphasize that fact to the public. Pick a message and stick with it. Branding is a critical component of your success. Use your well-thought, attractive logo on apparel for the staff, hats, key chains, plate holders, vehicle stickers, in your advertising, on your website and anywhere else where appropriate. Don’t forget to use your logo at local school sporting events and sponsorships of various community activities. You should be everywhere potential customers might be. Try to get as much exposure as your budget will allow. Finally, track your return on investment. Use trackable 800 numbers to determine where your leads are coming from. Listen to your salespeople have conversations with those who call in to ensure that those expensive leads aren’t being turned off by lackluster performance of a bored sales person. You might pay to have a service mystery shop your dealership and provide recorded

feedback. Our consultants provide these services and I am amazed at some of the results I see. Sometimes this entire process can be quite painful, but it is all part of the training, monitoring and measuring process. Remember, it is reflective of your customer’s experience. I hope you will find this issue helpful as you consider marketing and branding strategies. We’ve prepared some excellent information in this edition. Until next time, good luck, and make it happen!

Upcoming EventsDECEMBERDec. 8, 2014 Credit and Collections Conference Dallas, TXJANUARYJan. 6, 2015 BHPH Sales Training Boot CampJan. 7, 2015 BHPH Managers Boot CampJan. 8, 2015 BHPH Collections Boot Camp Orlando, FLFind out more about these events and register online at www.TwentyGroups.com. Cick on events.

6 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

LEEDOM GROUP

BHPH Boot Camp

When I first began my career, Buy Here-Pay Here was

significantly different than it is today. Writing this, I feel like my

father recounting how he had to walk two miles to and from school in a blinding snowstorm, uphill, both ways. We have all heard the

tales before about how the past was a much simpler time and things just aren’t the same today as they were in years past. BHPH today is more competitive and more capital intensive than at any point in history; it is fairly obvious that, yes, times have changed. The business used to be focused on a lower-cost entry point and serviced customers who didn’t have nearly the same financing options that they have today. We really didn’t know how good we had it back in the day. The evolution of the industry over the past several years is actually a tremendous testament to the value and power of free-market, Laissez-faire capitalism. The free flow of capital into our industry over the past several years has created unprecedented levels of competition and choice for the consumer. Dealers are forced to compete on vehicle selection, financing and warranties and this can only be seen as good for the customer. Economics 101. An unfortunate side-effect of this competition is that traditional

Working With Today’s Buyer

underwriting standards have gone by the wayside and a “car rental” mentality has set in with the BHPH customer base nation-wide. Nothing will stay the same anywhere for very long. The traditional industrial underpinnings of our national economic identity have been fading for decades. The transition from an industrial power to a service-based economy hasn’t done good things for middle and lower income Americans who simply cannot follow their parents and grandparents into careers because they no longer exist. So many of our customers have moved from one service-related occupation to another with no real hope of advancement and have come to see reliance on government entitlements to be a viable alternative to working to make ends meet. Again, Economics 101. The creation of a permanently under-employed class dependent on the state for their bread and circuses was one of the factors in the decline and fall of Rome. Nothing ventured, nothing gained. It’s a great saying and it has as much meaning today as it ever has. Another way of looking at this is to say that only something earned has value. Looking at the decline and eventual demise of the last generation’s inner-city housing projects highlights this. Free housing never generated the pride in ownership that so many of us take for granted. Maintenance was always someone else’s problem. Sound familiar? Understanding the economic and social mindset

By David Brotherton

of the BHPH customer today requires that we understand what multiple generations of entitlement have contributed to how our customer’s view their obligations. We must recognize this for what it is. Lamenting the change in the economy in recent years is not going to help us work with today’s customer profitably. To work with our customer today, we must recognize that they have limited tolerance for hard-core collection activity or multiple repairs. It is far too easy for our customers to go down the street and get another car rather than bringing their account with you up to date or setting money aside for unexpected repairs. Customers today just aren’t going to do either one. One of the most common reasons for loss is still mechanical problems and I see dealers who don’t want to help with repairs because the customer doesn’t take care of the car. My response is that if you expect them to take care of their cars without help, you are in the wrong business. Successful dealers today share one characteristic: they are committed to communicating with and taking care of all of their customers. Successful dealers understand that these are the times we live in and that excellent returns are still very possible in our model…they are just going to require more of an investment to get there.

David Brotherton is a consultant and Twenty Group moderator with the Leedom Group Contact him [email protected]

September 2014 DEALER BUSINESS JOURNAL | 7...Your Success Is Our Business

See how easy it is to restore that like-new finish in just an afternoon. Watch our online how-to videos to show you how.

QUAL

ITY ASSURANCE

G U A R A N T E E

O.E.M.COLORMATCH

Automotivetouchup.com888-710-5192

Paint pens >>> ½ oz and 2 oz bottles >>> 12 oz spray cansReady-to-spray pints, quarts and gallons

FIX NASTYSCRAPES

FOR LITTLESCRATCHSpecialists in

Sub-Prime

g We Buy theCustomer andTheir Story, NOT Their Beacon!

g We Buy With YOUMaking a Profit

g We Buy OpenBankruptcies (7&13!)

g We Buy theFirst Time Buyer

g We Buy Deeper ThanOur Competition!

“WITHOUT QUALITY,PERFORMANCE AND SERVICE ... IT’S NOT A GOOD DEAL”

CURRENTLY LICENSED IN: IA, IL, IN, KS, MI, MN, MO, NE, OH, PA, and WI

WWW.SECURITYAL.COM

Phone: 888.874.7579

Specialists inSub-Prime

CHECK OUTOUR ALLNEW

WEBSITE!

8 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

LEEDOM GROUP

Payment Processing

Merchant Processing Statements come in many

shapes and sizes and most of the time they are very difficult to understand. Having a better idea of what your statement is saying may give you the upper hand in finding better pricing. This article provides thought leadership on payment processing to new or existing merchants who accept credit/debit card or ACH payments. This information highlights certain areas of compliance that merchants need to consider in order to process payments securely, and how to best protect their businesses and consumers from legal, compliance and security risks. We gathered the information through industry research

and discussions with industry experts as well as representatives of regulatory bodies. This article covers surcharges and convenience fees and relevant rules and laws a merchant should explore when considering a pricing model that incorporates either fee type. It is important to know that

Payment Processing Guidancethe analysis contained in this article is based on the current laws and Visa and MasterCard Rules, and are subject to change. The market landscape and application of this information is subject to change as these laws and rules are updated.

Surcharges and Convenience Fees. A surcharge is a fee assessed to the customer because of the customer’s use of a credit card. A convenience fee is an amount assessed because of the customer’s ability to make a card payment via the internet or telephone. Failure to strictly adhere to surcharge and convenience fee standards can result in government or card payment brand imposed fines, investigation by a state attorney

general, and even cancellation of a merchant account. Effective January 27, 2013, Visa and MasterCard revised their Rules to permit merchants to surcharge credit card payments under certain conditions. Surcharges remain prohibited on debit card or prepaid card payments. In addition, the

By Paymaxx Pro

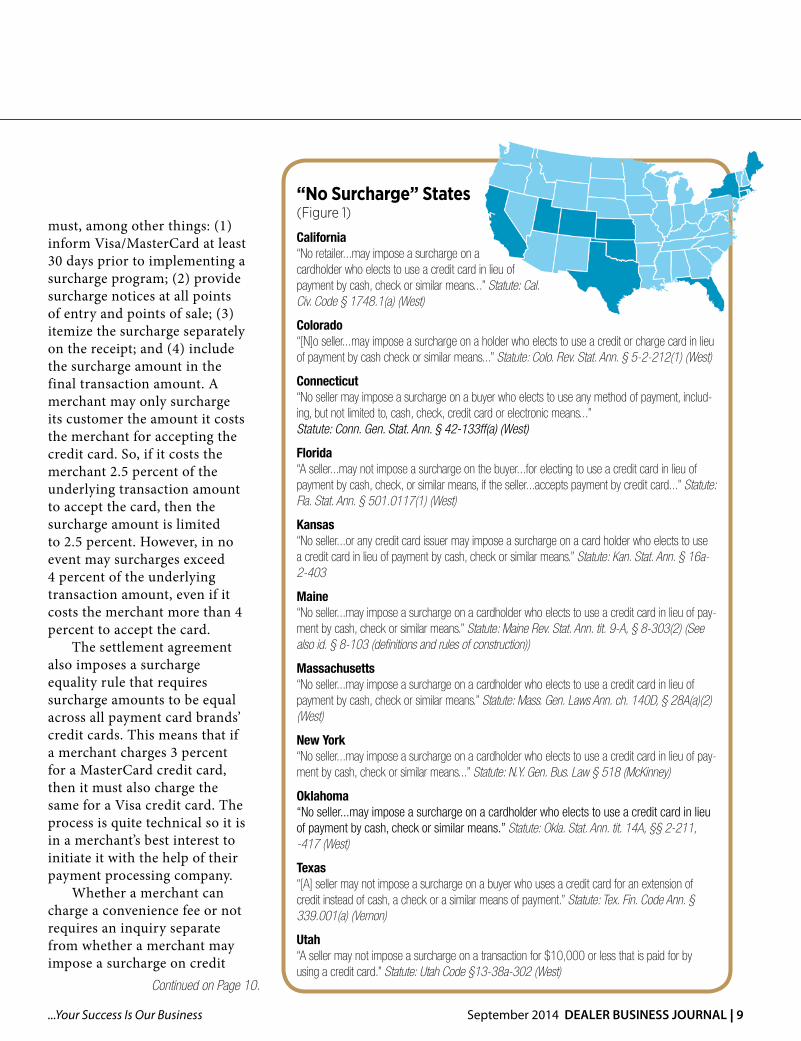

laws of 11 anti-surcharge states prohibit surcharges: California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma, Texas, and Utah. Also, merchants in seventeen other states must be cautious of entertaining thoughts of imposing such surcharges because anti-surcharge legislation has been contemplated or introduced in: Arkansas, Hawaii, Illinois, Indiana, Kentucky, Missouri, Maryland, Michigan, Nevada, New Jersey, New Mexico, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, and West Virginia (See Figure 1 on page 10). The new surcharge rules do not affect Visa and MasterCard Rules regarding convenience fees, which are still permitted under certain circumstances, and which may be an option for merchants. However, like surcharges, Visa’s Rules specify that Convenience Fees may only be charged by the merchant that actually provides the goods or services to the cardholder, and not by any third party, this includes the payment processor. We suggest caution on charging a credit card convenience fee in one of the 11 anti-surcharge states since these states’ statutes are unclear as to whether a convenience fee is a surcharge. If state law allows credit card surcharges, then a merchant must jump through a few hoops in order to comply with Visa and MasterCard rules. The merchant

Merchant Processing Statements come in many shapes and sizes and most of the time they are very difficult to understand. Having a better idea of what your statement is saying may give you the upper hand in finding better pricing.

September 2014 DEALER BUSINESS JOURNAL | 9...Your Success Is Our Business

Continued on Page 10.

must, among other things: (1) inform Visa/MasterCard at least 30 days prior to implementing a surcharge program; (2) provide surcharge notices at all points of entry and points of sale; (3) itemize the surcharge separately on the receipt; and (4) include the surcharge amount in the final transaction amount. A merchant may only surcharge its customer the amount it costs the merchant for accepting the credit card. So, if it costs the merchant 2.5 percent of the underlying transaction amount to accept the card, then the surcharge amount is limited to 2.5 percent. However, in no event may surcharges exceed 4 percent of the underlying transaction amount, even if it costs the merchant more than 4 percent to accept the card. The settlement agreement also imposes a surcharge equality rule that requires surcharge amounts to be equal across all payment card brands’ credit cards. This means that if a merchant charges 3 percent for a MasterCard credit card, then it must also charge the same for a Visa credit card. The process is quite technical so it is in a merchant’s best interest to initiate it with the help of their payment processing company. Whether a merchant can charge a convenience fee or not requires an inquiry separate from whether a merchant may impose a surcharge on credit

“No Surcharge” States (Figure 1)

California“No retailer...may impose a surcharge on a cardholder who elects to use a credit card in lieu of payment by cash, check or similar means...” Statute: Cal. Civ. Code § 1748.1(a) (West)

Colorado“[N]o seller...may impose a surcharge on a holder who elects to use a credit or charge card in lieu of payment by cash check or similar means...” Statute: Colo. Rev. Stat. Ann. § 5-2-212(1) (West)

Connecticut“No seller may impose a surcharge on a buyer who elects to use any method of payment, includ-ing, but not limited to, cash, check, credit card or electronic means...”Statute: Conn. Gen. Stat. Ann. § 42-133ff(a) (West)

Florida“A seller...may not impose a surcharge on the buyer...for electing to use a credit card in lieu of payment by cash, check, or similar means, if the seller...accepts payment by credit card...” Statute: Fla. Stat. Ann. § 501.0117(1) (West)

Kansas“No seller...or any credit card issuer may impose a surcharge on a card holder who elects to use a credit card in lieu of payment by cash, check or similar means.” Statute: Kan. Stat. Ann. § 16a-2-403

Maine“No seller...may impose a surcharge on a cardholder who elects to use a credit card in lieu of pay-ment by cash, check or similar means.” Statute: Maine Rev. Stat. Ann. tit. 9-A, § 8-303(2) (See also id. § 8-103 (definitions and rules of construction))

Massachusetts“No seller...may impose a surcharge on a cardholder who elects to use a credit card in lieu of payment by cash, check or similar means.” Statute: Mass. Gen. Laws Ann. ch. 140D, § 28A(a)(2) (West)

New York“No seller...may impose a surcharge on a cardholder who elects to use a credit card in lieu of pay-ment by cash, check or similar means...” Statute: N.Y. Gen. Bus. Law § 518 (McKinney)

Oklahoma“No seller...may impose a surcharge on a cardholder who elects to use a credit card in lieu of payment by cash, check or similar means.” Statute: Okla. Stat. Ann. tit. 14A, §§ 2-211, -417 (West)

Texas“[A] seller may not impose a surcharge on a buyer who uses a credit card for an extension of credit instead of cash, a check or a similar means of payment.” Statute: Tex. Fin. Code Ann. § 339.001(a) (Vernon)

Utah“A seller may not impose a surcharge on a transaction for $10,000 or less that is paid for by using a credit card.” Statute: Utah Code §13-38a-302 (West)

10 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

card transactions – such an inquiry requires several steps. The merchant should look at the payment card brand rules for all the credit card types it accepts. The basic rules for the four major payment card brands are: (1) AMEX does not allow a merchant to charge a convenience fee; (2) Discover does not have an explicit convenience fee policy, but requires its card to be treated like any other card; (3) MasterCard allows a merchant to charge a convenience fee if such a fee is imposed “on all like transaction regardless of the form of payment used”; and (4) Visa allows a merchant to charge a fixed convenience fee (i.e. $5.00 per transaction) if, among other things, the fee is charged for payments made via the internet or telephone – Visa prohibits convenience fees for face-to-face transactions. The merchant should also determine whether convenience fees are allowed under state law. While this inquiry may sound simple enough, many states do not have a “convenience fee” law, and therefore the relevant inquiry is whether charging a convenience fee violates a state’s anti-surcharge law. The Colorado Attorney General’s Office and Massachusetts’ Office of Commission of Banks have issued written opinions stating that convenience fees violate the antisurcharge law. And, while not in writing, the Texas Office of Consumer Credit Commissioner has stated that state law prohibits convenience fees. This unfortunately means that those merchants charging convenience fees in the other anti-surcharge

states are operating in the gray. If a merchant charges a convenience fee, under Visa Rules it must be: (a) charged for a bona fide convenience in the form of an alternative payment channel outside the merchant’s customary payment channels; (b) disclosed as a charge for the alternative payment channel convenience; (c) added only to a non-face-to-face transaction (if a mail order or electronic commerce merchant’s payment channels are exclusively non-face-to-face, such merchant may not impose a convenience fee); (d) a fixed amount, regardless of the value of the payment due; (e) applicable to all forms of payment accepted in the alternative payment channel; (f ) disclosed before the completion of the transaction and the cardholder is given the opportunity to cancel; and (g) included as part of the total amount of the transaction. Convenience fees may only be charged by the merchant that actually provides goods or services to the Cardholder, and not by a third party, such as the payment processor. Further, convenience fees may not be added to recurring transactions. As far as convenience fees for ACH Payments, they are not addressed by the NACHARules. However, based on our interactions with experts at NACHA, the merchant should make sure that the customer is authorizing the fee and that the amount that the consumer authorizes is the same amount he/she will be debited. (So, they can’t authorize a $10 payment and have a $12.50 debit show up because of the convenience fee.)

If it is for an additional amount other than what the consumer is authorizing, the merchant would have to do the authorization and the debit for the fee as a separate transaction and follow all of the NACHA Rules for that transaction including proper authorization. Our research, with respect to state law, suggests that the merchant should be cautious of the state laws in Connecticut, Colorado, and Massachusetts. Merchants must be keenly aware of payment processing laws and regulations as improper practices may, in extreme cases, result in the loss of a merchant’s account and the correlated revenue. Therefore, best practice requires a merchant to consult with their payment processing company and a knowledgeable payments attorney before instituting any type of surcharge or convenience fee. At Paymaxx Pro, we offer processing models to support a merchant’s ability to charge a convenience fee and we will work with you to determine how do to so while maintaining compliance with state laws and card standards.

The opinions put forth in this document are based on standard industry practices for payment processing. The accuracy of all statements contained in this analysis is limited to the correctness of the data that was provided. We have taken steps to verify that the data and information furnished is true and correct. For more information about Paymax Pro products, go to www.PaymaxxPro.com.

LEEDOM GROUP

PAYMENT PROCESSING GUIDANCE continued from Page 9

September 2014 DEALER BUSINESS JOURNAL | 11...Your Success Is Our Business

WHAT TO EXPECT:• Updated Industry

Benchmarks• Secrets to Underwriting

Good Loans• Collection Call Technique

Workshop• Lead and Regulatory

Compliance Updates• Skip Tracing Workshop• Credit and Underwriting

Panel• Collection Panel—Best

Practices• Collections Compliance• Team Building• Motivational Techniques• Roundtable and

Networking Sessions• And Much More!

PRESENTED BYDAVID BROTHERTON

$795** * Early Registration

* Before November 1st $895 after November 1st

REGISTER TODAY!

WHO SHOULD ATTEND?• BHPH Dealers• Finance Company

Managers• Collections Managers• Underwriters• Collectors• Skip Tracers

WHAT YOU GET:• Breakfast• Training Materials• Lunch• Networking Sessions• Coffee & Snack Breaks• In-Depth Personalized

Training

12 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

LEGAL & LEGISLATIVE

Most of you children are too young to remember the

name Joe Friday. Joe was the main character in a radio show, and later a TV show, called Dragnet, about a Los Angeles police detective. The original Dragnet radio show ran in 1949,

with several TV versions coming later. Joe did what detectives do— he gathered facts, and one of his standard lines when interrogating witnesses was, “The facts, ma’am, just the facts.” Lawyers tend to be fact hounds, too, generally unable to answer even seemingly simple legal questions until they have nailed down all the facts that might affect the answer. Dealers have embraced the Internet, which has no state boundaries, and they are increasingly finding themselves with out-of-state buyers who have visited their websites and want to buy cars. These cross-border transactions can pose some interesting legal question, not the least of which is, “If the deal goes sour, can the dealer be sued in the buyer’s state?” To answer the question, we need “the facts, ma’am, just the facts.” Here are facts from two recent lawsuits. In the first case, John Corigliano, a New Jersey resident, bought a 1995 Rolls Royce

Legal OpinionThe Facts, Ma’am, Just the Facts

Corniche convertible from Classic Motor, Inc., a California corporation. Corigliano viewed the car in California, signed transaction documents in California, and wired the purchase price to Classic in California. Unhappy with his purchase, Corigliano sued Classic and its owner, Fadi Elias, for fraudulent representations in federal court in New Jersey. The defendants moved to dismiss for lack of personal jurisdiction, and the court granted the motion. The court first considered whether it had specific jurisdiction over the defendants, which requires that the defendants have “minimum” contacts with New Jersey. The court found that the defendants’ only contacts with New Jersey were that Elias contacted Corigliano in New Jersey by phone and/or email and provided photographs to him via the Internet. The court found that such limited phone and Internet communications were insufficient to confer specific jurisdiction over the defendants. The court next addressed whether it had general jurisdiction over the defendants, which requires that the defendants have “continuous and systematic” contacts with New Jersey. Corigliano claimed that by advertising on websites and in national magazines, Classic intended to reach customers in New Jersey. The court found that print

By Tom Hudson

advertisements in national publications do not constitute “continuous and systematic” contacts and that “a passive website that does little more than make information available to those who are interested in it is not grounds for the exercise of personal jurisdiction.” The court stressed that none of the advertising specifically targeted New Jersey residents. The court also noted that neither Classic nor Elias does business or resides in New Jersey. In the second case, Ron Meyer, a Nebraska resident, bought a 1970 Ford Mustang after seeing the car on the website of Race City Classics, a North Carolina company. Meyer contacted Race City and, through a series of emails and phone calls, agreed to buy the car for $21,000. During the conversations, Meyer told his contact at Race City that he planned to present the vehicle at auto shows in Nebraska. Meyer never travelled to North Carolina to see the Mustang in person before buying the vehicle. Race City arranged for a shipper to deliver the Mustang to Nebraska. When the vehicle arrived, Meyer was dissatisfied with its condition; the Mustang was not show quality. The paint was cracked, the front hood was misaligned, and the trunk would not open. Meyer sued in Nebraska for damages, and the Nebraska trial court awarded a default judgment to Meyer for $8,942. As required by North Carolina law, Meyer filed

September 2014 DEALER BUSINESS JOURNAL | 13...Your Success Is Our Business

from Nebraska, and shipped the car to Nebraska. So, what facts are likely to be important in these “interstate Internet” deals? These courts mention some, like emails, phone calls, advertising, vehicle delivery and receipt of payment. Not mentioned in these cases but sometimes pivotal to courts looking at jurisdiction questions are a provision in the contract of sale stating the location where the contract formation takes place, and the place where the contract actually is signed. A dealership engaging in these types of sales should be aware of the facts that courts consider when determining whether the dealer can be sued out of state, and should structure its transactions so as to present a court with the

a “Docketing of Foreign Judgment” in a North Carolina trial court to enforce the judgment. After a hearing, the North Carolina trial court found that Race City did not have sufficient minimum contacts with Nebraska necessary for a Nebraska court to have personal jurisdiction. Meyer appealed. The Court of Appeals of North Carolina reversed the trial court. The appellate court noted that, in actions to enforce a foreign judgment, the judgment creditor has the burden to prove that the judgment in the foreign state was invalid. Looking to Nebraska law, the appellate court noted that Nebraska’s long-arm statute allows jurisdiction over nonresidents if permitted by the U.S. Constitution, which requires that Race City have minimum contacts with Nebraska to allow the exercise of either general or specific personal jurisdiction. While the actions of Race City were not sufficient for general jurisdiction, the court of appeals found that the conduct was sufficient for a Nebraska court to exercise specific jurisdiction. Looking to both Nebraska and North Carolina case law, the appellate court noted that although no person from Race City physically entered Nebraska, Race City intentionally directed actions towards Nebraska. Specifically, Race City advertised on websites accessible to Nebraskans, negotiated with Meyer over several days, received Meyer’s payment

most favorable scenario possible to support the dealer’s argument that the out-of-state court lacks jurisdiction. Joe Friday probably can’t help with that task, but the dealership’s lawyer probably can.

Corigliano v. Classic Motor Inc., 2014 U.S. Dist. LEXIS 97556 (D.N.J. July 17, 2014), Meyer v. Race City Classics, Inc., 2014 N.C. App. LEXIS 810 (N.C. App. July 29, 2014)

Tom Hudson, Esq. ([email protected]) is the author of several compliance-related books that are available online at www.counselorlibrary.com. He is also the publisher of Spot Delivery®, a monthly legal newsletter for auto dealers, and the Editor in Chief of CARLAW®. Reach him by phone at (410) 865-5411 or visit www.counselorlibrary.com.

Facts from emails, phone calls, advertising, vehicle delivery and receipt of payment are important in “interstate Internet” deals.

14 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

As you may know, the Consumer Financial

Protection Bureau (CFPB) currently discloses, for the entire world to see, certain consumer complaint data it receives from some of your customers in connection

with consumer financial products (which include auto loans and leases) and services via its web-based, public-facing database (“Complaint Database”). The Complaint Database can be found on the CFPB website at: http://www.consumerfinance.gov/complaintdatabase/ The CFPB recently announced that it is proposing a new policy statement (“Proposed Policy Statement”) that would supplement the CFPB’s existing Policy

Statements that established the Complaint Database and expand that disclosure to include what they call “unstructured consumer complaint narrative data” or “narratives.” In order for these narratives to be published by the CFPB, the consumer must opt-in and the narrative would be scrubbed by the CFPB to remove

CFPB ConcernsEvery Customer’s Got a Complaint!

By Eric L. Johnson

LEGAL & LEGISLATIVE

any personal information. If you follow the CFPB at all, you’ve seen that the CFPB is running a marketing program called “Everyone has a story.” The campaign involves self-promoting YouTube video interviews of people “looking for help along their financial journey” where they share their story concerning a financial problem they had and how CFPB helped them. If the Proposed Policy Statement is adopted by the CFPB, they might as well run another campaign on its heels and call it “Every customer’s got a complaint!” I’ll explain. Currently, when a consumer starts the process to submit a complaint to the CFPB, the consumer is asked to indicate the type of consumer financial product or service in question and the type of issue the consumer has had/is having with the company. Some suggested types of issues

are included with radio dials next to each for the consumer to click the issue that best corresponds to their issue. The consumer is then asked to describe in a text box what happened in 3,900 characters or less (i.e. “narratives” described above). The consumer can also attach documents to the complaint filing, such as account

statements, contracts, receipts and letters. The consumer is asked to include their desired resolution for the complaint and provide certain information to the CFPB. The information includes the consumer’s name, address, phone number, e-mail address, age, whether they are a service member or a dependant/spouse of a service member and, if so, their status, service and rank. The complaint also includes certain information about the company the consumer is complaining about. Before submission of the complaint, the consumer is required to click a box next to the following statement: “The information given is true to the best of my knowledge and belief. I understand that the CFPB cannot act as my lawyer, a court of law, or a financial advisor.” On receipt of the complaint, the CFPB reportedly takes steps to confirm a commercial relationship between the consumer and company. However, the CFPB does not verify the accuracy of the complaint. The CFPB forwards the complaint to the company, expects the company to respond to the complaint within 15 days of receipt, gives the consumer a tracking number for his/her complaint and keeps the consumer updated on the complaint status. Complaints are listed in the Complaint Database after the company responds to the complaint or it has had the complaint for 15 days, whichever comes first. Currently, the narratives are not published in the

The CFPB is proposing a new policy statement that would expand the Policy Complaint Database to include publishing “unstructured consumer narrative data” online.

September 2014 DEALER BUSINESS JOURNAL | 15...Your Success Is Our Business

Consumer Database. Under the proposed policy, the CFPB would seek consumer consent for publication of the narrative, and would “scrub” personal information from each such narrative. The CFPB would also allow the identified company to submit a response to the narrative to be published. A company that wishes to publish a response would be instructed not to provide direct identifying information in its public-facing response, and the CFPB would take “reasonable” steps to remove personal information from the response to minimize the risk of re-identification of the consumer. So, what’s the big deal about publishing these narratives? Well, as we’ve seen through the CFPB’s examination and enforcement activity against dealers and other companies, consumer complaints are a major driving force in the CFPB’s risk-based approach to supervision and enforcement. The CFPB admits in the Proposed Policy Statement that by allowing consumers to share their specific stories (narratives), it may actually expand the number of complaints submitted to the CFPB. In essence, publishing the narratives may cause other consumers to submit more complaints and “dog pile” on against the same dealer. Everyone’s got a complaint about something and publishing these narratives might just spur on more customers to file more complaints with the CFPB. In addition, the Proposed

Policy Statement does not address one of the major flaws of the Complaint Database - that there is no system in place by the CFPB to actually verify the accuracy of a complaint before it is published. It’s a free for all. The publishing of the possibly factually incorrect narratives would only compound that flaw. This could increase the risk that dealers could incur additional reputation damage and loss of business. Finally, the Proposed Policy Statement does not address the issue that financial institutions, including dealers, are required to maintain the confidentiality of their customers’ information. Therefore, it will be extremely difficult, if not impossible for a dealer to appropriately and properly respond to the narratives. The result will be that the narratives will tell the consumers’ side of the story concerning an unverified issue. The dealer will be “gagged” and prevented from telling its side of the story. In connection with its proposal to publish the narratives, the CFPB is specifically seeking public comment on:

• The need for any additional information to help inform consumer consent, the precise language to most effectively communicate with the consumer, at what point in the complaint process (at complaint submission or later in the complaint handling process) and where on the CFPB’s website the information

in support of the consumer’s opt-in consent should be displayed.

• Whether company responses to the narratives should be distinct and in addition to the response companies send directly to the consumer.

• The standard and methodology the CFPB intends to use to scrub customer information from the narratives, including suggestions of appropriate analogues to the HIPAA identifiers in the consumer financial domain, and any other identifiers which could reasonably be used to identify individuals.

The comment period for the Proposed Policy Statement was extended and comments must be received on or before September 22, 2014. So, be sure to submit your comments to the Proposed Policy Statement because if it’s adopted, you could be hearing more unverified, incorrect complaints from your customers.

Eric L. Johnson is a partner in the Oklahoma City, OK office of Hudson Cook, LLP. He is a frequent speaker and writer on a variety of consumer credit topics. Prior to pursing his legal career, he spent many years working in various departments for his family’s car dealership. Eric can be reached at (405) 602-3812 or [email protected]. This article is provided for informational purposes and is not intended nor should it be taken as legal advice.

16 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

Firing employees is never fun, but sometimes, you know that

firing a particular employee will be especially difficult and might even result in a lawsuit. If you are worried about being sued by a terminated

employee, you might want to consider asking the employee to sign a release: an agreement not to sue you in exchange for receiving certain benefits. Some employers routinely ask their employees to sign a release as a condition of receiving a severance package. Other employers ask only those employees who might have a legitimate legal claim against the company, or who seem especially motivated to sue, to sign a release. Here are ten things you should know about severance agreements.

1They are not required by law. One question

that I am frequently asked is whether severance payments and/or severance agreements are required by either state or federal law. If you are a private employer and are not governed by an employment contract which requires payment to an employee upon termination, then severance payments are not mandated.

General Counsel10 Things to Know About Severance Agreements

By Debra Dawn

LEGAL & LEGISLATIVE

2Under certain circumstances, you should attempt to obtain

a severance agreement. If there has been a dispute between you and the terminated employee (or between two terminated employees) and liability could

be imputed to the dealership, paying a small sum of money in return for a release may be a viable option. For example, if an employee claims the dealership owes him or her money in unpaid bonuses or commissions and the

methodology for setting the bonus or commission is not in writing, I would recommend entering into a severance agreement. This is especially true if the terminated employee is a minority or over the age of 40.

3The release is the most important part of any

severance agreement. A properly drafted severance agreement will contain releases for any and all

matters relating to the employee’s employment. It should incorporate language such as: “Upon payment of all monies as set forth above, EMPLOYEE on behalf of himself and his representatives, agents, heirs and assigns, releases and discharges the DEALERSHIP and the DEALERSHIP’s former, current or future officers, affiliated corporations, representatives, attorneys, directors, shareholders,

and assigns from any and all claims, liabilities, causes of

action, damages, losses, demands or obligations of every kind and nature, whether now known or unknown, suspected or unsuspected, which they ever had, now has, or hereafter can, shall or

If there has been a dispute between you and the

terminated employee, and liability could be imputed to the dealership, paying a small sum of money in

return for a release may be a viable option.

September 2014 DEALER BUSINESS JOURNAL | 17...Your Success Is Our Business

may have for, upon or by reason of any act, transaction, practice, conduct, matter, cause or thing of any kind whatsoever, relating to or based upon, in whole or in part, any act, transaction, practice or conduct prior to the date hereof, including but not limited to matters dealing with EMPLOYEE’S employment or termination of employment with DEALERSHIP, or which relate in any way to injuries or damages suffered by EMPLOYEE (knowingly or unknowingly).”

4The settlement agreement should cover specific releases

for federal and state employment acts. Special language should be incorporated in the severance agreement such that the employee releases the dealership from claims arising under federal, state and local statutory or common law. These statutes include, but are not limited to: the Age Discrimination in Employment Act (“ADEA”), Title VII of the Civil Rights Act of 1964, the Americans with Disabilities Act, the Occupational Safety and Health Act and the Affordable Care Act.

5All severance agreements should include a non-

disparagement clause. Terminated employees should be prohibited from bad mouthing the company and its management to other employees, customers, vendors and third parties. Likewise, the dealership should

refrain from publishing negative comments about its former employee. A release covers past acts, not future conduct. The risk of liability to the dealership from negatively commenting on a former employee is especially high if those negative comments are put in a writing of any form (which includes texts and emails).

6The reason for the employee’s termination should be

addressed. If an employee is being terminated due to position elimination or reduction in force, that should be stated in the severance agreement. However, if the cause for the termination is either subject to interpretation (i.e. “poor performance”; “does not get along with others”) or the reason for the termination is an employee’s failure to do something (like meet a quota), I would suggest the issue be circumvented. In these cases, the clause, “disputes have arisen regarding the terms and conditions of employment” can be utilized in lieu of the specific reason for termination.

7 Any money to be paid to the employee must

be clearly spelled out. This includes the date of commencement of payment as well as whether the money is to be delivered in a lump sum or through a periodic payment stream.

8The terms of the severance agreement should be kept

confidential. A clause should be inserted in the severance agreement which requires all parties to keep the existence of the severance agreement confidential. This prevents both past and present employees from questioning why they themselves did not receive this type of consideration upon departure.

9A venue provision should be incorporated. Once an

employee leaves the work force, there is no guarantee that he or she will remain in the vicinity, or even in the state. Inserting a venue provision guarantees that any disputes related to the severance agreement will be brought in a court in the dealership’s jurisdiction.

10The severance agreement should include a “no

attorneys’ fee” provision. Let’s face it—a terminated employee is an unhappy employee with extra time on his or her hands and an ax to grind. By inserting a clause stating that neither party will be awarded attorneys’ fees, you can discourage unhappy plaintiffs’ lawyers from jumping on the litigation bandwagon.

Debra Dawn is Leedom Group’s General Counsel and Compliance Director Debra Dawn has formed AUTOLAW Group to assist dealers in all facets of dealership compliance. [email protected]

18 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

After decades of working in, and consulting with, the

marketplace I’ve become convinced that the vast majority of people who miss their potential are not lazy; they are unfocused. Many put their hearts and energies into building

a great career, business and life, yet never rise above mediocrity. Others become wildly successful, but still fall far short of what they could have accomplished had they focused their time, energy, talents and resources more intensely on a daily basis. Following are four rules of focus that will take you past the exhausting and unfulfilling “mile wide and an inch deep” approach that dominates so many lives, and into a more unstoppable achiever in whatever you set your mind to.

Focus fanatically on the few. Consultants, authors and trainers have been saying this in their own way for decades:

“First things first, last things not at all.” Peter Drucker

“The main thing is to keep the main thing the main thing.” Stephen Covey

“Don’t spend minor time on major things, or major time on the minor things.” Jim Rohn

LEADERSHIP & TRAINING

Learn to LeadFour Ways to Keep a Fanatical Focus

By Dave Anderson

Focus is defined as “the ability to concentrate.” Naturally, before that can happen, you’ve got to choose what it is exactly you are going to give disproportionate time, energy, resources and talents to. By identifying and focusing fanatically on the ultimate few—a small handful of goals that mean the most—you create a focus filter, making it far easier to know what to say yes or no to; what to daily engage in, or what to withdraw from as you move towards your goals. The challenge is that from all the good things you’d like to accomplish (good things to do), to focus on the best things (best things to do). And while it’s counterintuitive for “Type A” leaders to say no to good ideas or opportunities, there is no greater destroyer of focus than always saying yes. A common time when this sort of blurred focus shows up is when well-intentioned people try to change too many things in their business or life at one time. If you make ten changes at once, you divide your energy by ten and have a ten percent chance of success. The ensuring disappointment proves time and time again that setting too many goals at the same time guarantees you’ll achieve few, if any, with excellence. Without identifying and focusing fanatically on the ultimate few you will tend to dabble your way through the day, reacting to the latest emergency and improvising around the newest crisis. You’ll

be prone to mistake motion for progress and confuse activity with accomplishment.

Identify and act on daily lead measures. While your “ultimate few” are the lag measures of what you’d most like to accomplish, your highest leverage daily activities are the lead measures that take you there. In case you missed it, let me stress that I said “daily” activities. Reaching your most important goals isn’t a destination thing, it’s a daily thing. The simple truth is this: a day has no memory whether it was good or bad; you have to come back and prove yourself all over again by executing the handful of diligent daily disciplines that continue to move your progress forward. It doesn’t matter how great yesterday was, it ended last night. To make each day a masterpiece you must continue to focus on the key lead measures; and every day means every day. In fact, your success in achieving what means most to you will have less to do with the brilliance of your plan, and more to do with the consistency of right daily actions. To determine your key daily lead actions to execute, don’t make the mistake of listing everything you can do to achieve your goal and then pursuing them all. Instead, think in terms of leverage and ask, what are the fewest daily battles necessary to win this war? Then focus on getting them done, daily, regardless.

September 2014 DEALER BUSINESS JOURNAL | 19...Your Success Is Our Business

Finish your day before you start it and schedule your key lead measures. Again, to defer to two of my mentors and their timeless wisdom:

“Never begin the day until it is finished on paper; finish your day before you start it.” Jim Rohn

“Begin with the end in mind.” Stephen Covey

Lead measures should be scheduled for tomorrow before you leave for home this evening. Then, when you come to work, you’ll have a blueprint waiting for you that will narrow your focus and quickly put you into a productive stride early in the day. As “stuff ” arises that gets you off track as the hours progress, it’s easier to return to your focused plan if you actually have one to begin with, and aren’t just making the day up as you go along. Many people make the mistake of trying to squeeze their priorities into the

day, rather than scheduling their priorities and working the day around them. Forget the old buzz phrase, “prioritize your schedule” and instead, schedule your priorities and your focus will compound.

Learn to say no. Opportunity doesn’t equal obligation. If you’ve ever turned your head for five minutes and had it become your day, you know the danger of not saying no to low return conversations, tasks, or to trivial pursuits. However, without following the three prior disciplines you won’t have a framework from which to discern what is a good or bad decision, or use of time. Thus, when you concentrate daily on the ultimate few, and diligently executing the pre-prescribed, scheduled, lead measures that will take you there, you’ll get off track far less often, and will more quickly recover when you do. The four rules of focus are both sequential and non-negotiable;

you can’t pick and choose which you like. They must progress in the order given and cheating on even one of them yields predictable and oftentimes immediate consequences. The rules of focus, much like laws of gravity are unforgiving; they don’t care how busy you are, or how you feel, or how unique you believe your situation is. Violate them and you’ll see it, feel it and suffer because of it. Follow them daily and you’ll go farther, faster, than you ever believed possible.

Dave Anderson is President of LearnToLead which provides in-person and virtual training to many of the world’s best dealerships. Dave speaks to dealer groups over 125 times each year and has given seminars in 15 countries. He has spoken at eleven NADA Conventions and is the author of twelve books. Follow Dave on Twitter @DaveAnderson100 and visit his website at learntolead.com for free articles and videos on sales and leadership.

The rules of focus, much like the laws

of gravity are unforgiving...

...Follow them daily and you’ll go farther, faster, then you ever believed possible.

20 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

an ongoing basis about general business developments so that there are no “surprises” per se to either party. If there are issues, they can be addressed in a timely manner. Lenders do not like being surprised with unfavorable information, which could place them in awkward positions with underwriters, etc. Therefore, transparency is important for both parties Also management should actively compare and document industry benchmarks and operating statistics versus actual results at least monthly, such in a dashboard type report for internal purposes. This information may be handy not only for internal management purposes but for future loan procurement processes as well. Also, BHPH operators should communicate within their Dealer 20 Groups as far as covenants and loan requirements of their peers to enhance knowledge of what guidelines are expected in the industry and to benchmark those on an internal basis. This information may be helpful in a future loan renewal or procurement process in lieu of having to create historic information retroactively. Among other considerations, financial institutions will want to compare your financial information on any prospective loan to others in the industry, so again, benchmarking and appropriate leveraging and operational results is very important. It is important that you work hard at ensuring that the

Obtaining cost-effective capital for BHPH operators

is essential for long-term success and to ensure the ability to remain competitive. In order to

accomplish this, it is important that buy here-pay here (BHPH) operators continually strive to enhance relationships with their current financial

institutions as well as develop relationships with other lenders. Also, it is important to have your business plans and financial reporting well documented and in good order. As financial institutions are continually subjected to economic conditions, acquisition

activity and lending restructuring, the future availability of financing is not always predictable for the BHPH operator. Many clients seek financing as either new operators or mature businesses who try to match their financial needs with the best lender for a long-term relationship. BHPH operators try to team with financial institutions which have been in the business of

Business BasicsBuy Here-Pay Here Procuring Capital

lending to BHPH industry and well as make inquiries to assess their future industry commitment. BHPH operators may desire to establish relationships with financial institutions that are familiar with the BHPH industry and have commitment to the industry as these institutions are most knowledgeable of industry trends and may make a better long-term “business partner, particularly if there are cyclical downturns. Therefore, the lenders that are committed to the industry will be there for additional capital procurement if warranted. Procuring additional and maintaining capital in today’s market requires understanding and being mindful of the financial institution’s underwriting requirements and the lender’s

overall positions. To accomplish this, the BHPH operator needs to understand the financial institutions underwriting criteria, inclusive of covenants which need to be met, operating benchmarks which should to be maintained and other general areas of concerns that the lender has. This would suggest considering to communicate with the lender on

BUSINESS OPERATIONS

By Robert N. Parnas

To procure additional, or maintain, capital in today’s market, the BHPH operator needs to communicate with the lender on an ongoing basis about general business developments so there are no “surprises” to either party.

September 2014 DEALER BUSINESS JOURNAL | 21...Your Success Is Our Business...Your Success Is Our Business

financial institutions are satisfied inclusive remaining compliance with their credit agreement(s). This would include compliance with both non-financial as well as financial loan covenants. In order to accomplish this, among other things, BHPH must be mindful to ensure that accounting reports are accurately prepared and that loan covenants are properly calculated on a monthly basis. The last thing a lender wants is a surprise that their client has not met loan covenants and will need to obtain waivers on violations particularly if not identified in advance by the BHPH operator. Ensure you proofread the monthly financial statements and internal package to insure propriety. If monthly information is incorrect and the BHPH operator has significant year-end adjustments, the financial institution may be “leery” of your monthly financial statement submissions and force the financial institution to study and review in greater detail the operating results and/or information on an ongoing basis. Ensure you are monitoring and documenting budgeted vs. actual information. In short, procuring capital is an ongoing challenge and it is best to prepare when you don’t even need new or additional capital. Discuss with lenders what benchmarks and operational ratios that they want you to maintain, which will differ from financial institution to financial institution. Make sure you continue to enhance your current relationships with financial institutions and seek opportunities to develop new ones. Also, insure your accounting and management reports are in order and consider the matters referenced above, regardless whether you are experiencing success or struggling. We often meet BHPH operators who may be forced to seek new financing and are may be experiencing a lot of pressure and frustration in this effort, who do not appear to have their “financial house in order” pertaining to matters referenced above and therefore, we would encourage BHPH operators to be proactive and consider the suggestions provided on an ongoing basis. Robert Parnas is an automotive CPA with CliftonLarsonAllen and has expert knowledge of the inner-workings of both retail and Buy Here-Pay Here operations.

Leedom and Associates, LLC has created an easy to use Dealership Profitability Profile to help you find out. Go online to www.twentygroups.com and click the Analyze Your Dealership button. By answering some quick questions you will receive initial feedback about your key performance indicators and identify potential opportunities for growth.

Do you ever wonder your dealership’s performance and profitability stack up against the rest of the industry?

Get started with your free analysis by scanning this code with your mobile device.

Today’s business climate has forced everyone to stretch the budget a little further and look for creative ways

to save money. Sometimes that means trying to “do it yourself ” in certain areas. While it may not be wise for a layman to take on compliance and legal concerns or accounting and taxes, small business owners can usually get away with attempting marketing and branding on their own. Professional services will definitely return professional results, but with the right know-how and some out of the box thinking, a dealer can get some great results. The American Marketing Association defines marketing as “the activity, set of institutions, and processes for creating, communicating, delivering, and exchanging offerings that have value for customers, clients, partners, and society at large.” Marketing includes all of those other things like branding, advertising and PR, but it is not a synonym. You may have heard people talk about a marketing strategy or sales and marketing. These phrases refer to the way you are going to get your message to your customers, who are your market. Where you advertise, how you let people know about your dealership, and what you tell them are all aspects of marketing.

COVER STORY

Continued on Page 24

Building your brand and spreading your message doesn’t have to cost big bucks. Take these tips and techniques to develop your own strategy.By Christy Taylor

Branding is the way your company is received by other people. It is sometimes called your “look.” To build a solid brand for your business you need to understand who you are as a company, who your customers are and what makes you different. If you can answer those questions, then you can move on to creating your brand. For used car dealers, branding can play an important part of the way customers see your dealership. The more professional and cohesive you’re branding, the more trusting your customers are that you are a reputable business. With a little effort, your branding can make you the first dealership people in your community think of when they are looking for their next car. To really develop a brand, you have to dig deep into the goals you have for your business. It is not enough to say your dealership’s mission is to sell cars. That is a given. You have to think about why you want to sell cars. If you answered, to make money, then keep thinking. You could make money selling watermelons. Why did you choose to sell cars? What are the needs of your customers that you want to meet? Use these answers to define your company’s purpose.

DealerBusinessJournal.com22 | DEALER BUSINESS JOURNAL September 2014

24 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

Continued on Page 26

COVER STORY

Say you are selling cars because you love automobiles. You can name the make, model and year of any car that passes you on the highway. As a kid, you had posters of sports cars plastered on your bedroom wall. Incorporating your enthusiasm for automobiles into your company’s purpose statement may sound something like this: Helping customers fall in love with the car they purchase. In terms of branding, your purpose statement is the message you want to get across to your customers and potential customers. In this example, you want people to know that when they come shopping on your lot, they are going to feel like they drove away in their dream car, even if it was a 2010 Honda Accord. With a clear purpose, you can start deciding how to illustrate it. Human beings are visual creatures. We appreciate the way things look and are attracted to things that are pleasing to the eye. How your company presents itself graphically is an essential part of building your brand. The first place to start is with the logo. Logos are the visual representation your brand has in the marketplace. There are three different types of logos: font-based, which consist primarily of type; illustrations that demonstrate what a company does; and abstract graphics that symbolize the company. A good logo should be able to tell others what you do just by looking at it, but also capture the essence of your business. Before you start brainstorming designs, first try to write words or even a one-sentence description of who you are. To truly create a unique brand, you need to stay away from clip-art images or template designs. These graphics are too easy to duplicate and come across to customers as

generic and forgettable. Investing in graphic design services may be a good choice for someone who is not familiar with design and graphics. A professional can not only create original artwork but help you create a final image that can be transferred into a variety of platforms. The drawing you downloaded from the internet will not be able to be used for a t-shirt or produced into a sign, but a logo created in industry-recognized design programs is suitable for virtually anything. While good logos are able to speak for themselves, a tag line can compliment and enhance your overall message. Tag lines are short phrases that express your company’s most important benefits and what you want customers to remember about working with you. They should clearly tell others what you do, but also answer the question of “so what?” Take Publix Supermarkets as an example: “Where shopping is a pleasure.” Their tagline not only tells customers what they can do at their stores, (shopping) but how they will do it (with pleasure). Just as an example, a company named Auto Locators may specialize in finding the cars their customers specifically ask for. A good tag line may go something like this: We’ve found your next car. Coupled with a logo that incorporates a scope or hunting sights, the customer knows your business is prepared and equipped to find exactly what they are looking for. A word of advice when it comes to tag lines though, is to stay away from slogans like “we’ve got the best deals” and “our prices are the lowest.” The truth is, there can only be one “best deal” or “lowest price” and maybe your company does not have it. Using these types of phrases is a lot like saying “you always” or

“you never” in an argument; it not only loses its meaning but people tend to tune it out. Once you have your look, it is time to put it out there and get noticed. The most obvious place to start is with business stationary. Put your logo and tag line on every piece of paper that leaves your office. Business cards, letterhead, envelopes, forms, flyers and any other printed material you create should have your logo on it somewhere. Every electronic communication should as well, from email footers to website listings. The more chances your customers have to see your brand identity, and interact with it, the more recognizable you become. Now that you know who you are, and you are able to show it to others, you can start thinking about the best way to spread the word about you and your dealership. The two best ways to do that are through advertising and public relations. While both start out with the same goal of delivering your message to your market, they each have pros and cons. Placing a display ad in the newspaper or posting a listing online are examples of paid advertising. Advertising is purchased, and with that comes control. You make the decision on what size, what it says, how it looks and where it appears. Public relations, sometimes called “unpaid” or “earned” media is free but gives someone else the control. You send out a press release or host an event and it may or may not be used, interpreted correctly or present the message you intended. A successful marketing campaign should combine both paid and unpaid advertising in traditional and unconventional ways.

DO IT YOURSELF MARKETING continued from Page 22

September 2014 DEALER BUSINESS JOURNAL | 25...Your Success Is Our Business

BLUEPOSITIVES:Tranquility, love, loyalty, security, trust, intelligence

NEGATIVES:Coldness, fear, masculinity

REDPOSITIVES:Love, energy, power, strength, passion, heat

NEGATIVES:Anger, danger, warning

BROWNPOSITIVES:Friendly, earth, outdoors, longevity, conservative

NEGATIVES:Dogmatic, conservative

GREENPOSITIVES:Money, growth, fertility, freshness, healing

NEGATIVES:Envy, jealousy guilt

PINKPOSITIVES:Healthy, happy, feminine, compassion, sweet, playful

NEGATIVES:Weak, femininity, immaturity

TAN/BEIGEPOSITIVES:Dependable, flexible, crisp, conservative

NEGATIVES:Dull, boring, conservative

PURPLEPOSITIVES:Royalty, nobility, spirituality, luxury, ambition

NEGATIVES:Mystery, moodiness

YELLOWPOSITIVES:Bright, energy, sun, creativity, intellect, happy

NEGATIVES:Irresponsible, unstable

GRAYPOSITIVES:Security, reliability, intelligence, solid

NEGATIVES:Gloomy, sad, conservative

TURQUOISEPOSITIVES:Spiritual, healing, protection, sophisticated

NEGATIVES:Envy, femininity

ORANGEPOSITIVES:Courage, confidence, friendliness, success

NEGATIVES:Ignorance, sluggish

BLACKPOSITIVES:Protection, dramatic, classy, formality

NEGATIVES:Death, evil, mystery

SILVERPOSITIVES:Glamorous, high tech, graceful, sleek

NEGATIVES:Dreamer, insincere

GOLDPOSITIVES:Wealth, prosperity, valuable, traditional

NEGATIVES:Greed, dreamer

WHITEPOSITIVES:Goodness, innocence, purity, fresh, easy, clean

NEGATIVES:Winter, cold, distant

Adapted from colormatters.com

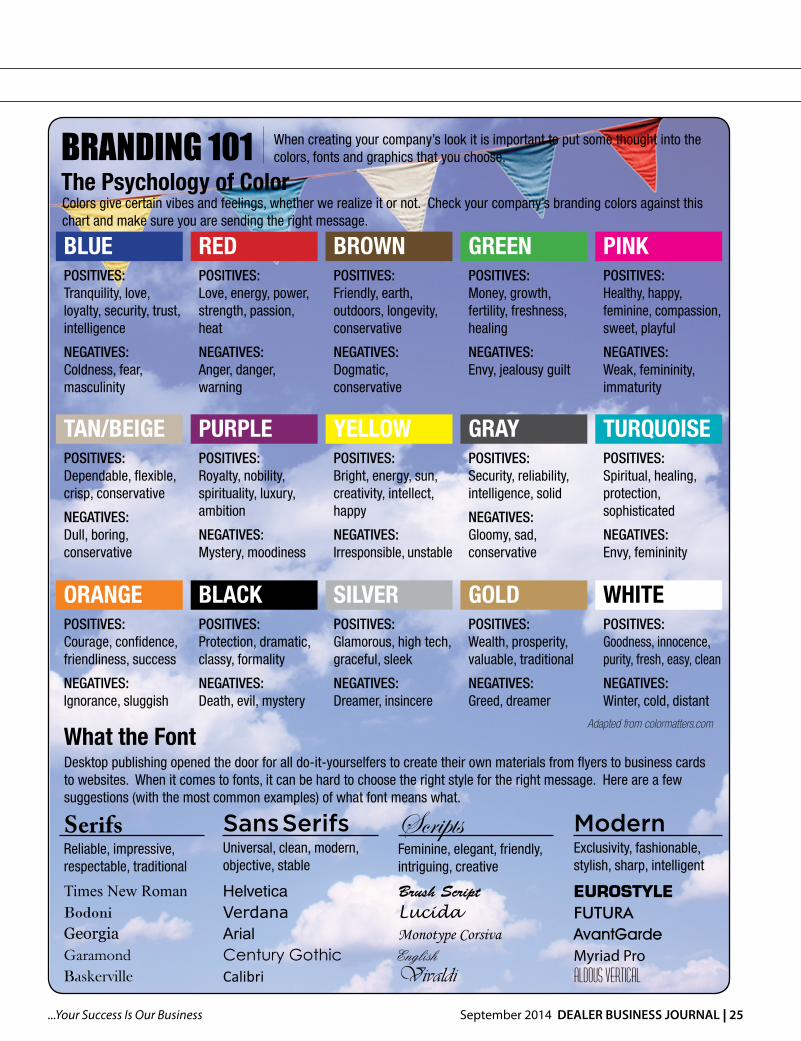

The Psychology of ColorColors give certain vibes and feelings, whether we realize it or not. Check your company’s branding colors against this chart and make sure you are sending the right message.

What the FontDesktop publishing opened the door for all do-it-yourselfers to create their own materials from flyers to business cards to websites. When it comes to fonts, it can be hard to choose the right style for the right message. Here are a few suggestions (with the most common examples) of what font means what.

SerifsReliable, impressive, respectable, traditional

Times New RomanBodoniGeorgiaGaramondBaskerville

SansSerifsUniversal, clean, modern, objective, stable

HelveticaVerdanaArialCentury GothicCalibri

ScriptsFeminine, elegant, friendly, intriguing, creative

Brush ScriptLucida Monotype CorsivaEnglishVivaldi

ModernExclusivity, fashionable, stylish, sharp, intelligent

EUROSTYLEFUTURAAvantGardeMyriad ProAldous vertical

BRANDING 101 When creating your company’s look it is important to put some thought into the colors, fonts and graphics that you choose.

26 | DEALER BUSINESS JOURNAL September 2014 DealerBusinessJournal.com

Advertising is really essential to any business that relies on buying and selling a product. To make the best decisions on what ad spots and in what mediums to buy you need a way to measure their effectiveness. The industry term for this process is called the cost per thousand impressions or CPM (where M stands for the Roman numeral 1,000). It is a measurement of how much money it costs you to reach 1,000 potential customers. To calculate CPM, divide the cost of the ad by the number of readers, viewers, listeners or visitors, broken down by thousands. If an ad costs $4,000 in a newspaper with a circulation of 100,000, your cost to reach 1,000 readers is $40, since 100,000 divided by 1,000 is 100 and $4,000 divided by 100 is $40. If a radio ad costs $250 and the station has 50,000 listeners, the CPM for that ad is $5. A $2,000 ad in a magazine with 20,000 readers may seem cheaper than the $4,000 newspaper ad, but by spending $100 to reach 1,000 readers, you are spending more money to reach each potential customer with the magazine. Online ads are priced in the same manner, and would use click-rates and hits to determine the audience. The CPM is a great way to compare apples to oranges in the different types of mediums and decide which is most cost effective for your business. When you think about public relations, most people immediately think press releases and news clippings. Traditionally, that has been the approach that most large businesses and corporations take when trying to spread their message. The Public Relations Society of America defines public relations as the “strategic communication process that builds mutually

COVER STORY

DO IT YOURSELF MARKETING continued from Page 24

Continued on Page 29

beneficial relationships between organizations and their publics.” For a small business owner, the key words to take away from that definition are: strategic, builds and relationships. In the classic sense, this would be accomplished by distributing press releases to media outlets like newspapers, television/radio stations and magazines. While you should never turn down the opportunity to alert the press to something interesting happening at your dealership, you may find that a traditional public relations campaign is not that easy of an undertaking. It takes time and influence to build a rolodex of media contacts that will pick up a pitched story, and more often than not, the typical “grand opening” release will not get much interest or coverage. When submitting a story idea to the press you need to be unique. A good story idea to pitch would be celebrating a 100th anniversary, or sharing the story of a family in need that you donated a car to. Bring it back full-circle to that original question of “what makes you different?” Look for a way to highlight that. If you find the idea of dealing with the press intimidating, then look for unconventional ways to build those strategic relationships with customers. A lot of these could be promotional ideas you do within your dealership. Be shrewd on how to invest on these ideas, however. Before you order that giant inflatable gorilla to draw strangers in from the road, think about ways you could reinforce the relationship with your current customers that would build loyalty and encourage referrals. Needs some ideas? Highlight customer service. Have you spent the time in your

ADVERTISINGSECRETSUsually, the old adage stands true that you get what you pay for but sometimes you can take advantage of free or low-cost, common sense advertising opportunities that can bring good results. Here are a few:

Make the most of your e-mail signature. Your dealership probably sends hundreds, maybe event thousands, of emails every week. Make the most of that free communication by Including an advertisement in your email signature. Keep a static line, such as Click Here to see our inventory or maybe social media buttons or change it every week (or morning) to highlight a sale or special.

Use the back of your business card as a promo. Don’t waste the prime advertising real estate on the back of your business card. Include a coupon, an incentive or some other type of promotion to get your customer’s attention.

Become an expert. If you’ve been around long enough, you’re an expert at something. Free advice can help build your brand as well as enhancing your reputation. Start a blog about car maintenance or give car-buying seminars at your local high school. Offer the local lifestyle magazine or radio station your knowledge in a column or as an “Ask the Expert” feature.

September 2014 DEALER BUSINESS JOURNAL | 27...Your Success Is Our Business

F O C U S O N A U TO M OT I V E S E RV I C E