current issues economics notes. ueq: what role does the government play in the economic system of...

TRANSCRIPT

Current Issues Economics Notes

UEQ: What role does the government play in the economic system of America?

Concept: Economics

LEQ: 1).What is economics?2.) What is the difference between a good & service?3.) Explain how some resources are plentiful & scarce.

Economics

• Economics – a social science studying the allocation of scarce resources and goods.

• Want – everything you could get if there was no limit to resources.

Economics

• Need – Resources and goods that are necessary for people

• Scarcity – situation of having inadequate resources to obtain all of ones wants.

Economics

• Allocate – to distribute according to some plan or system.

• Trade-Off – the act of giving up one thing of value to gain another thing of value.

• Opportunity Cost – is the value of the alternative option that is lost when one makes a decision. Example: (College vs. job)

• Outsourcing - to obtain goods or services from an outside source: (U.S. companies who outsource from China)

Resources • Resources – The inputs-such as

labor, capital, entrepreneurship, and land-used by people to produce outputs.

• Natural Resources – Raw materials which occur in nature and that are used to produce what humans need or want (ex: timber, water, crude oil, arable land)

• Plentiful Resource - Resource that has a high supply (Solar energy )

Resources

• Scarce Resource – Resources that have a high demand or short supply (Oil)

• Renewable Resource - Any resource, such as wood or solar energy, that can or will be replenished naturally in the course of time.

Resources

• Nonrenewable Resource - natural resource from the Earth that exists in limited supply and cannot be replaced also (Oil & Coal)

Resources

• Goods – finished products created from resources

Goods & Services

• Services - the providing of accommodation and activities required by the public (maintenance, repair , Restaurant, etc)

Handout

• Complete front page of handout: – Goods and Services

matching– Types of resources

matching

Yesterday’s Review

• What is?– Economics– Want vs. Need– Scarcity– Opportunity Cost– Natural Resource– Renewable/Non-

renewable Resources– Goods vs. Services

Concept: Supply & Demand

LEQ:1.) What is the difference between supply & demand?2.) How do the laws of supply & demand affect the economy & the goods & services people buy & want?

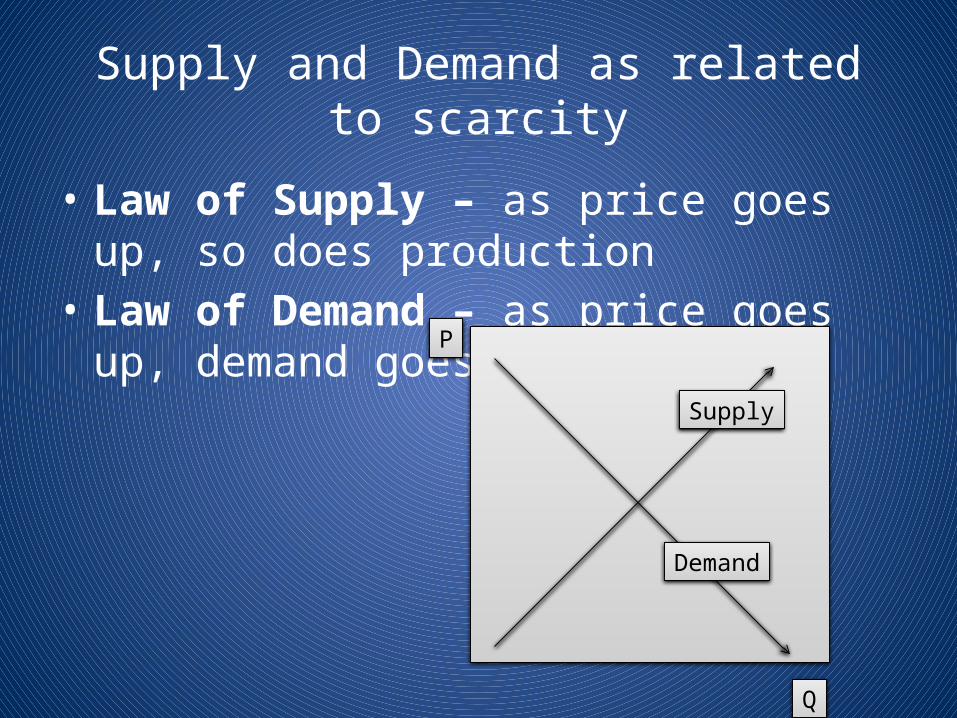

Supply and Demand as related to scarcity

• Law of Supply – as price goes up, so does production

• Law of Demand – as price goes up, demand goes down

Q

P

Supply

Demand

Market Equilibrium

• Occurs when the quantity supplied and the quantity demanded are both equal at the same price

• Also known as market clearing price because everything goes!

P

Q

Market Equilibrium

Surplus vs Shortage

• Surplus exists when the supply exceeds the demand– Incentive – When a producer offers coupons,

rebates, Shortage exists when the demand exceeds the supply

– Consumers develop a budget that lists needs and wants and the amount of money to get them

– If money can not be raised, consumer will find substitute

Q

P

Shortage

Surplus

Put it all together!

Key:P - priceQ – quantity of goodS – supply D - demandPO – price of market balance (market equilibrium)A – ShortageB – Surplus

Finish Yesterday’s Handout

Scarcity & Shortage

• Substitute Goods – Goods and services that serve the same purpose and can be used in place of each other.- Example: Butter and margarine / Dr. Pepper and Doctor Thunder

Scarcity & Shortage

• Complimentary Goods – An item that you would buy along with another item.- Example: Peanut butter and Jelly, hotdog and hot dog buns

Characteristics of the US Economic System (Market Economy)

• The US has a Market Economy, where buyers and sellers come together to answer the three Fundamental Economic Questions.

• Supply – When sellers determine what good or service they will produce, and part with at different price levels

• The Producer supplies goods and services with profit as incentive.

Characteristics of the US Economic System (Market Economy)

• Demand – Buyers determine how much of a good or service they are willing to buy at different price levels. ( food, entertainment, etc)

Activity

• Complete the rest of Handout

Concept: Inflation

LEQ: 1.) What impact does inflation have on our economy?2.) Explain how inflation & recession are circular cycles.

Economic Cycles

• Inflation - a persistent, substantial rise in the general level of prices resulting in an increase in the volume of money and resulting in the loss of value of currency (everything cost more)

Year Price of Coke

2004 $.75

2005 $.85

2006 $1

2007 $1.25

2008 $1.50

Economic Cycles• Recession - a period of an economic contraction,

sometimes limited in scope or duration. (Loss of jobs)

• Depression - a period during which business, employment, and stock-market values decline severely or remain at a very low level of activity. (1930s)

Concept: Money

LEQ:1.) How is the money supply controlled in the United States?

Money

• Money – A standardized medium of exchange

• Money has 3 Functions:• Medium of exchange – no

longer have to barter• Standard of value – can

measure worth in terms of money

• Store of Value – can be saved and maintain value

• The term money can be interchanged with the term currency

Money

• Mint - a place where coins, paper currency, special medals, etc., are produced under government authority.

• FDIC - a federally sponsored corporation that insures accounts in national banks and other qualified institutions

Investments• Loan - something lent or

furnished on condition of being returned, esp. a sum of money lent at interest: a $1000 loan at 10 percent interest.

• Bond - Finance. a certificate of ownership of a specified portion of a debt due to be paid by a government or corporation to an individual holder and usually bearing a fixed rate of interest.

Investments

• Stocks - the shares of a particular company or corporation

• Interest - a sum paid or charged for the use of money or for borrowing money.- such a sum expressed as a percentage of money borrowed to be paid over a given period, usually one year

How the government controls the economy

• Federal Reserve - the central bank of the United States– Controls the U.S.

economy by raising and lowering short-term interest rates and the money supply