current accounting and reporting developments webcast series

TRANSCRIPT

Current Accounting and Reporting Developments Webcast Series First Quarter March 21, 2012

Donald Doran

Accounting Services Group Team Leader

Welcome and standard-setting update

PwC

Today’s agenda

Legislative Environment and Accounting for Income Taxes

Corporate Governance Update

Accounting Hot Topics: Build-to-suit leases

Accounting Hot Topics: Deferred costs

Q&A

Slide 3 March 2012 Current Accounting and Reporting Developments

PwC

CPE & Evaluation

In order to receive CPE credit for this program, you must stay on for the entire program.

You must respond to the multiple choice questions.

If you are viewing this webcast in a group, everyone in the group can receive CPE credit.

Please complete the evaluation that will appear at the end of the webcast.

Today’s program will be worth approximately 1.5 CPE credits.

Slide 4 March 2012 Current Accounting and Reporting Developments

PwC

Polling Question #1

Which of the following best describes your role or responsibilities within your organization?

A. CFO or Controller / Assistant Controller

B. SEC or Financial Reporting Director/Manager

C. Accounting/Finance Manager

D. Tax Director/Manager

E. Other

Slide 5 March 2012 Current Accounting and Reporting Developments

PwC

Standard-setting update

• Leases

- Lessee expense recognition under discussion

- Outreach to be conducted

- Exposure draft expected in Q3 2012

• Revenue Recognition

- Comment period closed on March 13, 2012

- Final standard expected late 2012 or early 2013

- Effective date - no earlier than 2015

• Financial Instruments

- Joint board discussions on classification and measurement

- FASB proposal on disclosures

- Boards continue to work jointly on an impairment solution

Pr

ior

ity

pr

oje

cts

O

the

r • Consolidation-related

- Principal v agent

- Investment company

- Investment property entity

• Indefinite-lived intangible impairment

- New ―qualitative‖ assessment

- Comments due April 24

- Final standard expected Q2 2012

Slide 6 March 2012 Current Accounting and Reporting Developments

PwC

Today’s agenda

Legislative Environment and Accounting for Income Taxes

Corporate Governance Update

Accounting Hot Topics: Build-to-suit leases

Accounting Hot Topics: Deferred costs

Q&A

Slide 7 March 2012 Current Accounting and Reporting Developments

Ed McClellan, Principal and

Ed Abahoonie, Partner

Legislative Environment and Accounting for Income Taxes

PwC

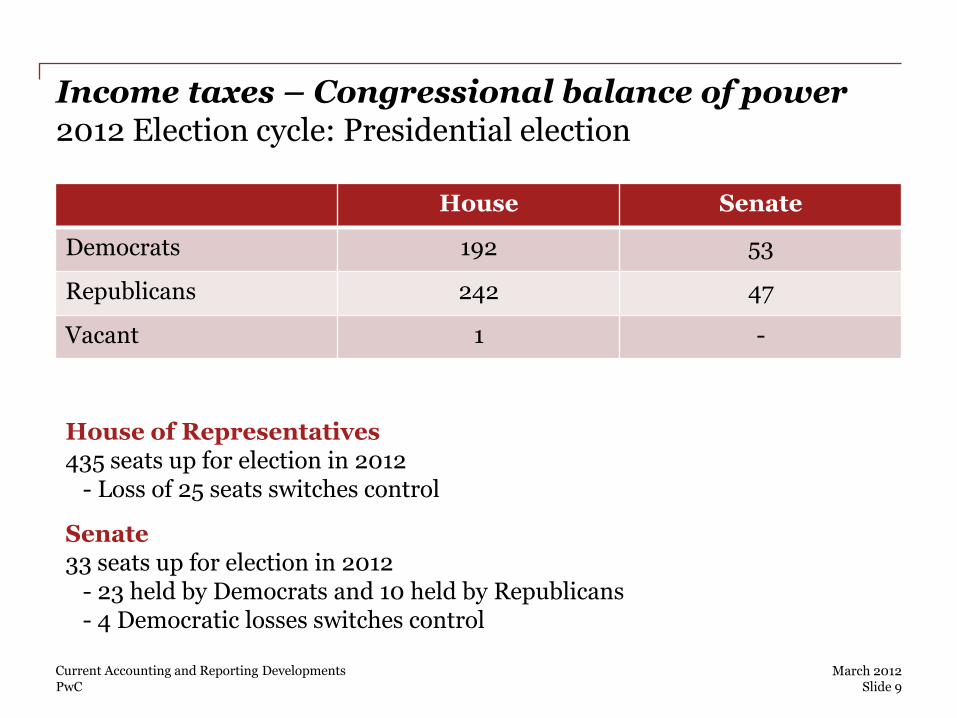

Income taxes – Congressional balance of power 2012 Election cycle: Presidential election House Senate

Democrats 192 53

Republicans 242 47

Vacant 1 -

House of Representatives 435 seats up for election in 2012 - Loss of 25 seats switches control

Senate 33 seats up for election in 2012 - 23 held by Democrats and 10 held by Republicans - 4 Democratic losses switches control

Slide 9 March 2012 Current Accounting and Reporting Developments

PwC

Income taxes – expired and expiring tax provisions potential “lame duck” session

Expired 2011 Provisions

• AMT relief

• 100% bonus depreciation

• R&D credit

• CFC look-through

• Active financing exception

• 15-year leasehold amortization

Expiring 2012 Provisions

• Extension of all 2001/2003 individual tax cuts

• Repeal of ―Pease‖ and ―PEP‖

• Estate & gift tax at 35% top rate/$5 million exemption

• 50% bonus depreciation

• Capital gains and dividend tax rates

• Employee payroll tax relief

• Highway trust fund taxes (3/31/12)

Fiscal Policy Deadlines

• Federal debt: $16.394 trillion limit expected to be reached late 2012 / early 2013

• Sequestration: $1.2 trillion in across-the-board discretionary spending cuts set to go into effect beginning January 3, 2013

• Government Funding: Expires September 30, 2012

Slide 10

March 2012 Current Accounting and Reporting Developments

PwC

Income taxes – basis for tax reform

• U.S. has the highest statutory corporate tax rate in the world

• 26 of 34 OECD countries have territorial tax systems

• Proliferation of pass-through entities in recent years adds complexity

0 10 20 30 40

Japan

United States

Germany

Mexico

Canada

United Kingdom

Switzerland

Ireland

Rate (%)

Combined Corporate Tax Rates, 2011

Source: OECD Tax Database and PwC Worldwide Tax Summaries, http://www.pwc.com/gx/en/worldwide-tax-summaries/index.jhtml

Slide 11 March 2012 Current Accounting and Reporting Developments

PwC

Income taxes – select points from primary proposals

•Reduce corporate tax rate to 28%

•Increase manufacturing deductions

•Limit deferral of tax on foreign earnings

•Expand research credit

•Base-broadening options

•Reduce corporate tax rate to 25%

•Shift to a territorial system

•95% dividends received deduction

•Immediate inclusion of all accumulated E&P

•Thin capitalization rules added

•No reduction in corporate tax rate

•95% dividends received deduction

•One-time 70% dividends received deduction for pre-2013 earnings

•50% deduction on foreign intangible income

Obama proposal Camp proposal Enzi proposal

Slide 12 March 2012 Current Accounting and Reporting Developments

PwC

Polling Question #2

Do you believe significant corporate tax reform will happen in the United States?

A. Yes, and it’s coming soon

B. Yes, but it won’t come for some time

C. No

Slide 13 March 2012 Current Accounting and Reporting Developments

PwC

Income taxes – common themes from proposed reforms and related accounting implications

Consideration Implications

Reduction in the overall federal corporate tax rate

• Proposals include potential reduction as low as 25%

• Impact on deferred income tax balances

• Effective tax rate impact

Reduced foreign earnings deferral

• Current U.S. taxation of more foreign earnings

• Indefinite reinvestment assertions

• Taxes on unremitted earnings

Slide 14 March 2012 Current Accounting and Reporting Developments

PwC

Income taxes – common themes from proposed reforms and related accounting implications

Consideration Implications

Foreign tax credits (FTCs)

• Limitations and changes to various FTC-related rules

• Transition of existing FTCs

• Deferred taxes and valuation allowance consequences

Corporate tax incentives • Interest disallowances

• Manufacturing deduction

• Effective tax rate impact

Slide 15 March 2012 Current Accounting and Reporting Developments

PwC

Income taxes – other income tax accounting issues related to proposed reforms

Other potential accounting implications

Transfer pricing adjustments

Uncertain tax positions

Disclosure considerations

Slide 16 March 2012 Current Accounting and Reporting Developments

PwC

Polling Question #3

Which of the potential accounting implications just mentioned would be most impactful to your business?

A. Transfer pricing adjustments

B. Uncertain tax positions

C. Changes to the effective tax rate

D. N/A, we are not impacted by these items

Slide 17 March 2012 Current Accounting and Reporting Developments

Catherine Bromilow, Partner

Corporate Governance Update

PwC

Executive compensation

• Dodd-Frank compensation-related rules not yet finalized:

- Final rules expected by June 30, 2012

◦ Exchange listing standards on compensation committee independence

◦ Compensation consultant independence

◦ Disclosure rules on compensation consultant conflicts

- Proposed rules by June 30, 2012*

◦ Pay-for-performance disclosure

◦ Pay ratios disclosure

◦ Recovery of executive compensation (clawbacks)

- When issued, some of these rules could have significant disclosure implications

* Slated for final rule adoption by December 31, 2012

Slide 19 March 2012 Current Accounting and Reporting Developments

PwC

Executive compensation

• PCAOB proposed amendments to audit standards issued on February 28

- Would require auditors to obtain an understanding of financial relationships and transactions with executive officers (compensation, perks, etc.) to identify risk of material misstatement

◦ Read employment and compensation agreements

◦ Read proxy statements and other relevant regulatory filings

◦ Inquire of compensation committee chair, and any compensation consultant, regarding structuring of the compensation for executive officers

◦ Understand policies and procedures for reimbursing executive officer expenses

- Anticipated to be effective for audits of financial statements with fiscal years beginning on or after December 15, 2012

Slide 20

March 2012 Current Accounting and Reporting Developments

PwC

Corporate political activity

• Under the Citizens-United case, corporations have the right to make expenditures for direct advocacy for or against candidates for federal political office

Expenditures must be independent – not coordinated – with a candidate or party (i.e., companies can contribute to ―Super PACs‖)

◦ No required disclosures of such contributions by the Super PACs or companies

• Institutional investor community campaigning to increase disclosure of political contributions and payments to trade associations

• Most common shareholder proposal in the 2012 proxy season with close to 100 filed

Support has been growing in recent years

◦ 57% of S&P 100 have adopted political disclosure and board-level oversight

◦ In 2011, 41 shareholder proposals on the topic received an average of 31% support

Slide 21 March 2012 Current Accounting and Reporting Developments

PwC

Conflict minerals

• Dodd-Frank Act requires SEC to issue rules relating to the use of ―conflict minerals‖ which include gold and other minerals originating from the Democratic Republic of Congo or adjoining countries (DRC Countries)

Proposed rules issued December 2010

• Applies not only to companies that extract and distribute the conflict minerals but also companies that use them in their products

• Requires disclosure in the annual report whether conflict minerals originated from DRC Countries

• SEC indicated a final rule will be issued, likely by the end of June

Slide 22 March 2012 Current Accounting and Reporting Developments

PwC

Say on pay

• Mandated by the Dodd-Frank Act

- Implemented for the first time for all public companies in 2011

• Shareholder support at 98% of companies in 2011; only 43 companies failed

• In the following year, company must disclose in its proxy any changes made to executive compensation as a result of the say on pay vote in the prior year

• Proxy advisors taking a very careful look at companies that had less than 70% votes FOR executive pay in prior year

• Already had one failed vote in this proxy season (130 votes as of March 1)

Slide 23 March 2012 Current Accounting and Reporting Developments

PwC

Polling Question #4

What was the result of the say on pay vote for your company in 2011?

A. 70% of more support for the pay package

B. Less than 70% support

C. Don’t know

D. Not applicable

Slide 24 March 2012 Current Accounting and Reporting Developments

Chad Soares, Partner

Accounting Hot Topics: Build to suit leases

PwC

Build to Suit Leases

• ASC 840-40-55 applies when a lessee has an option or obligation to lease an asset once construction is complete.

• Guidance is not limited to so-called ―build to suit‖ leases of real estate.

• ―Construction‖ isn’t defined. In practice it is not limited to construction of an asset from the ground up—certain customization or renovation activities can also put you in the scope of the guidance.

Failure to properly identify a construction project can result in an unwelcome surprise

Slide 26 March 2012 Current Accounting and Reporting Developments

PwC

Build to Suit Leases

• ASC 840-40-55 imposes strict limits on a lessee’s involvement during the construction period.

• Determining whether the lessee is the accounting owner requires consideration of both qualitative and quantitative factors.

• If deemed the owner, the lessee records construction in progress. Landlord funded construction costs (including the value of the asset at inception) are reflected as debt.

• Ground rent expense is recorded during construction when land is not owned by the lessee.

If in scope, common terms can result in the lessee being deemed the accounting owner

Slide 27 March 2012 Current Accounting and Reporting Developments

PwC

Build to Suit Leases

• Following construction completion, the arrangement is evaluated as a sale leaseback.

• Removal of the asset and related debt is not straightforward when the arrangement involves real estate or integral equipment.

• Failure to meet these requirements would require the lessee to continue to account for the arrangement as a financing. This would also result in frontloading of expense relative to an operating lease.

• If sale leaseback requirements are met, the lease is classified as either capital or operating in accordance with ASC 840.

A failed build to suit involving real estate can have a lasting impact on your balance sheet

Slide 28 March 2012 Current Accounting and Reporting Developments

PwC

Polling Question #5

The guidance on lease accounting is codified in which ASC section?

A. ASC 720

B. ASC 820

C. ASC 840

D. ASC 950

Slide 29 March 2012 Current Accounting and Reporting Developments

Donald Doran, Partner and

Ashley Wright, Senior Manager

Accounting Hot Topics: Deferred costs

PwC

Acquisition Costs for Insurance Companies

Expected to have significant impact on Life insurers’ book value

(estimated range 20-30% reduction DAC and 5-10% reduction shareholders’ equity)

• New guidance related to deferred acquisition costs (DAC) for insurance

- Address concerns around diversity in practice

- Better align industry guidance with other areas of GAAP

- Effective January 1st, 2012

• Industry observations

- Life insurance companies impacted more than P&C

- New disclosures and cumulative effect adjustments in 10-Qs this quarter

- Relation to contracts costs under the revenue recognition joint project

Slide 31 March 2012 Current Accounting and Reporting Developments

PwC

Acquisition Costs for Insurance Companies

• Key changes in the guidance

- DAC redefined as costs that are "directly related" to the ―successful‖ acquisition of the new and renewal insurance contracts

- Reduced the types of costs eligible for capitalization

- Clarified only advertising costs that meet the ―direct response‖ advertising criteria that applies to all industries are deferrable

- Can be applied prospectively or retrospectively

• The new standard presents several challenges for insurers

- Allocating costs between direct and indirect acquisition activities and determining successful versus unsuccessful efforts

- Retrospective adoption requires significant estimates where systems were not designed to capture the data

- Prospective adoption results in ―double hit‖ to future income

Slide 32

March 2012 Current Accounting and Reporting Developments

PwC

Cost deferral – other costs

Limited authoritative guidance exists for the treatment of costs associated with revenue transactions.

Such costs may be related to the following :

• Customer acquisition

• Set up

• Start-up

• Solicitation

• Origination

FASB Codification references

ASC 310-20 Nonrefundable fees and other cost

ASC 340 Other assets and deferred costs

ASC 605-2-25-4 Separately priced extended warranty and product maintenance contracts

ASC 720-15 Start-up costs

ASC 944-720 Financial Services - Insurance

Slide 33 March 2012 Current Accounting and Reporting Developments

PwC

Cost deferral – other costs

• Industry specific guidance (e.g. long-term construction contracts)

• Cost specific guidance (e.g., software development costs)

Is specific guidance applicable?

If not, when and under what conditions is deferral appropriate?

• Do not merely rely upon the ―matching‖ principle

• Costs must meet the definition of an asset (CON 6)

• Two acceptable models:

– Loan origination costs (ASC 310-20)

– Extended warranty costs (ASC 605-20-25-4)

Slide 34

March 2012 Current Accounting and Reporting Developments

PwC

Cost deferral – other costs

• Application of either model is an accounting policy election

Should be consistently applied

Disclosed if material

• Additional reminders

Determine appropriate amortization period

Periodically assess for impairment

Slide 35 March 2012 Current Accounting and Reporting Developments

PwC

Polling Question #6

This webcast is typically held during the last month of each calendar quarter. During which week of that month would it be most helpful for you to have the webcast?

A. First

B. Second

C. Third

D. Fourth

Slide 36 March 2012 Current Accounting and Reporting Developments

PwC

Polling Question #7

This quarterly webcast is currently scheduled for 90 minutes and offers 1.5 CPE credits. Which of the following would you prefer?

A. Keep it at 90 minutes; offering 1.5 CPE credits

B. Extend it to 105 minutes; offering 2 CPE credits

C. Extend it to 120 minutes; offering 2 CPE credits

D. Shorten it to 60 minutes; offering 1 CPE credit

Slide 37 March 2012 Current Accounting and Reporting Developments

Q&A Session

PwC

CPE Certificates

Click “Request CPE” (button under slides)

Group Viewing:

• Click “Request CPE”

• Select the number of co-viewers then click Submit.

• Enter group information and check the “I attest…” box.

• On the following page, click the Download Certificate link.

• Certificates will open for each viewer.

Slide 39

March 2012 Current Accounting and Reporting Developments

PwC

CPE Credit for PwC Partners and Staff

No action required

PwC partners and staff do not need to submit CPE certificates as supplemental learning to Learning at PwC.

Credit will be automatically posted to Learning at PwC for those PwC partners and staff that met the minimum CPE requirements during the live webcast and are eligible for CPE credit.

To determine CPE eligibility, you can click the ―Request CPE‖ link under the slide area.

Slide 40 March 2012 Current Accounting and Reporting Developments

Current Accounting and Reporting Developments webcast series Thank You for Participating!

©2012 PricewaterhouseCoopers LLP. All rights reserved. ―PricewaterhouseCoopers‖ refers to PricewaterhouseCoopers LLP, a Delaware limited liability partnership, or, as the context requires, the PricewaterhouseCoopers global network or other member firms of the network, each of which is a separate and independent legal entity.