credit policy management and loan recovery process …

TRANSCRIPT

CREDIT POLICY MANAGEMENT AND LOAN RECOVERY PROCESS IN THE

BANKING SECTOR: A CASE STUDY OF POST BANK UGANDA

(KABALE BRANCH).

BY

AINEBYONA FORTUNATE

07/U/6298/EXT

SUPERVISOR

MR.KINTU ISMAIL

A RESEARCH REPORT SUBMITTED TO MAKERERE UNIVERSITY SCHOOL

OF LONG LIFE LEARNING AND EXTERNAL STUDIES IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD

OF THE BACHELORS OF COMMERCE DEGREE OF

MAKERERE UNIVERSITY

MAY 2011

i

DECLARATION

I here by declare that this research report is my original work and has never been submitted in

any institution of higher learning for any degree award.

Signature…………………………………………………………………..

AINEBYONA FORTUNATE

Date…………………………………………………………………………

ii

APPROVAL

This is to certify that the research report entitled Credit policy management and Loan recovery

process in the banking sector has been done under my supervision and is ready for submission

for examination.

Signature………………………………………………………………………

MR. KINTU ISMAIL

Date…………………………………………………………………………………

iii

DEDICATION

I dedicate this report to my parents Mr. kamugisha Joseph and Mrs. Kamugisha Jacent who have

supported me all the way through my academic journey, and also to my Auntie Miss Byensi

Florence.

iv

ACKNOWLEDGEMENT

I am thankful to the Almighty who has through all my academic struggles up to the rightful

completion of my research report as well.

I also extend my sincere thanks supervisor Mr. Kintu Ismail for his consistent encouragement,

guidance, and knowledge which enabled me to conclude my research successful.

I am also great fully indebted to the management and staff of post bank Uganda for giving me a

chance and accepted me to carry out this research in their bank and having provided me with the

necessary information that enabled me to finish my research successful.

I express my gratitude to Mr. Ayebazibwe Conald who has been a source of inspiration towards

the successful realization of what I set out to achieve.

I also take this opportunity to acknowledge my friends Kyarisiima Florence,Kyarimpa Hellen

and Muwonge Henry Lukwata who have guided, supported and encouraged me through out my

research and above for their academic support while I was pursuing my degree through out all

my academic years.

Special thanks go to my lecturers I have met all my time I have been at the university for all the

many comments, suggestions which have been a source of inspiration and encouragement

throughout my time at the university.

Finally, I want to thank Mr. A . Duncan for his efforts right from the start of my research until up

to it‟s completion.

I will forever remain sincerely indebted to you all.

May the Almighty God reward you all unmeasureably.

v

TABLE OF CONTENT

DECLARATION ........................................................................................................................ i

APPROVAL .............................................................................................................................. ii

DEDICATION .......................................................................................................................... iii

ACKNOWLEDGEMENT ......................................................................................................... iv

TABLE OF CONTENT ..............................................................................................................v

LIST OF TABLES .................................................................................................................. viii

LIST OF ACRONYMNS ............................................................................................................x

ABSTRACT ............................................................................................................................. xi

CHAPTER ONE .......................................................................................................................1

1.0 INTRODUCTION .................................................................................................................1

1.1 BACKGROUND OF THE STUDY ......................................................................................1

1.2 Statement of the problem .......................................................................................................2

1.3 Purpose of the study ..............................................................................................................3

1.4 Objectives of the study ..........................................................................................................3

1.5 Research Questions ...............................................................................................................3

1.6 Scope of the study .................................................................................................................3

1.6.1 Geographical scope ............................................................................................................3

1.6.2 Subject scope......................................................................................................................3

1.6.3 Time scope .........................................................................................................................3

1.7 Significance of the study .......................................................................................................4

CHAPTER TWO ......................................................................................................................5

LITERATURE REVIEW ............................................................................................................5

2.0 Introduction ...........................................................................................................................5

2.1 Credit management policy .....................................................................................................5

2.1.1 Credit Standards .................................................................................................................5

2.1.2 Credit terms ........................................................................................................................6

2.1.3 Collection efforts ................................................................................................................7

2.2 LOAN RECOVERY .............................................................................................................7

vi

2.2.1 Political causes ...................................................................................................................7

2.2.2 Institutional causes .............................................................................................................8

2.2.3 Economic causes ................................................................................................................8

2.2.4. Loan recovery methods include; ........................................................................................8

2.3. RELATIONSHIP BETWEEN CREDIT MANAGEMENT POLICY AND LOAN

RECOVERY ............................................................................................................................. 10

2.4 Conclusions ......................................................................................................................... 11

CHAPTER THREE ................................................................................................................ 12

METHODOLOGY.................................................................................................................... 12

3.0 INTRODUCTION ............................................................................................................... 12

3.1 Research design ................................................................................................................... 12

3.2 Target Population ................................................................................................................ 12

3.3 Sampling ............................................................................................................................. 12

3.3.1 Sample size ...................................................................................................................... 12

3.3.2 Sampling methods ............................................................................................................ 12

3.4 Data Collection ................................................................................................................... 13

3.4.1 Data sources ..................................................................................................................... 13

3.5 Data collection methods ...................................................................................................... 13

3.5.1 Questionnaires .................................................................................................................. 13

3.5.2 Interviews ......................................................................................................................... 13

3.6 Data collection instruments ................................................................................................. 13

3.6.1 Interviews ......................................................................................................................... 13

3.6.2 Self Administered Questionnaire ...................................................................................... 13

3.7 Data processing, summary and presentation and Analysis .................. 143.7.1 Data processing

................................................................................................................................................. 14

3.7.2 Data summary and presentation ........................................................................................ 14

3.7.3 Data analysis .................................................................................................................... 14

CHAPTER FOUR ................................................................................................................... 15

PRESENTATION, ANALYSIS AND DISSCUSSION OF FINDINGS .................................... 15

vii

4.0. INTRODUTION ................................................................................................................ 15

4.1. BACKGROUND OF FINDINGS ....................................................................................... 15

4.2 FINDINGS ON THE CREDIT MANAGEMENT POLICY OF POST BANK UGANDA ... 18

4.3 FINDINGS ON LOAN RECOVERY .............................................................................. 22

4.4 FINDINDS ON THE RELATIONSHIP BETWEEN CREDIT MANAGEMENT POLICY

AND LOAN RECOVERY OF POST BANK ............................................................................ 25

CHAPTER FIVE..................................................................................................................... 30

SUMMARY OF FINDINGS, CONCLUSIONS AND RECOMMENDATIONS ....................... 30

5.0 Introduction. ........................................................................................................................ 30

5.1 Discussion of findings. ........................................................................................................ 30

5.1.1 Credit management policy ................................................................................................ 30

5.1.2 Loan recovery .................................................................................................................. 30

5.2 Summary of findings ........................................................................................................... 31

5.2.1 On the credit policy management, majority ....................................................................... 31

5.2.2 On the loan recovery procedures employed by post bank, ................................................. 31

5.2.3 On the relationship between credit policy management and loan recovery, ....................... 31

5.3 Conclusions ......................................................................................................................... 31

5.4 Recommendations ............................................................................................................... 31

5.5 Areas of further research ..................................................................................................... 32

REFERENCES ......................................................................................................................... 33

APPENDIX……………………………………………………………………………………………………………………………………………...34

QUESTIONNAIRE TO THE RESPONDENTS FROM CREDIT OFFICIALS OF POST BANK

UGANDA (KABALE BRANCH) ............................................................................................. 34

INTRODUCTORY LETTER…………………………………………..………………………..37

viii

LIST OF TABLES

Table 1; showing sex o f the respondents. .................................................................................. 15

Table 3; Showing education level of respondent ........................................................................ 16

Table 2: Showing the age of respondents. .................................................................................. 16

Table 5: showing the sector which the bank offers loans to. ....................................................... 17

Table 4: Showing the period of employment /client ship with the bank...................................... 17

Table 6; Showing loan types offered. ........................................................................................ 18

Table 7: Findings on whether there are standard procedures of giving out loans. ....................... 18

Table 8; Findings on whether relevant information is collected from loan applicants before

disbursements. .......................................................................................................................... 19

Table 9: Findings on whether loans are extended on liberal terms to the extent of the whole

amount required by the client. ................................................................................................... 19

Table 10: Findings on whether short term loans are first given out to test the credit worthiness of

the clients. ................................................................................................................................. 20

Table 11: Findings on whether collateral security is required before advancing the loan amount.

................................................................................................................................................. 20

Table 12; Findings on whether loan follow up and monitoring is done to check the viability of

the clients loan project. .............................................................................................................. 21

Table 13: Findings on whether loans are offered for a long period of time. ................................ 21

Table: 14 Findings on whether there are procedures to collect principle amount and interest due

the loan from clients. ................................................................................................................. 22

Table 15: Findings on whether clients pay their debts on the due date ....................................... 22

Table 16: Findings on whether clients fail to pay their debts due to failure in their loan projects.

................................................................................................................................................. 23

Table 17: Findings on whether clients fail to pay outstanding balance due to high interest rate

attached. .................................................................................................................................... 23

Table 18: Findings on whether there are fines instituted due to failure to pay the principle amount

and the accrued interest in time. ................................................................................................ 24

Table 19: Findings on the efficiency of the loan recovery system .............................................. 24

ix

Table 20: Findings on whether procedures for loan disbursements are liberal that whoever wants

the loan is given and pays at the time he/she feels like. .............................................................. 25

Table 21: Findings on whether clients who fail to pay back the loan are written off as bad debts.

................................................................................................................................................. 25

Table 22: Findings on whether the bank invests much money in loan collection and it benefits for

the bank as loans are recovered in time. ..................................................................................... 26

Table 23: Findings whether credit management system of post bank is so inefficient to enhance

loans collection. ........................................................................................................................ 26

Table 24: Finding on whether loan disbursement without security is most likely to result into

default of payment by the client. ............................................................................................... 27

Table 25: Findings on whether credit management policy of post bank enhances loan recovery

without involving much financial costs. .................................................................................... 27

Table 26: Findings on whether the level of loan default would be so high without the credit

management policy currently in place ....................................................................................... 28

Table27; Showing computation of spearman‟s correlation coefficient Correlations ................... 28

x

LIST OF ACRONYMNS

B.O.U - Bank of Uganda

U.C.B- Uganda Commercial Bank

A.C.P- Average Collection Period

N.P.Ls- Non-Performing Loans

xi

ABSTRACT

The study was focused on credit management policy and loan recovery with post bank Uganda

with the main objective of finding out the relationship between the two variables of credit policy

and loan recovery, examining the credit policy management of post bank and examining the loan

recovery levels of post bank.

In this study a sample size of 40 people was used from whom data was obtained. Purposive

sampling technique was used in selection of the samples and it‟s from this that I found out that

effective credit policy in post bank leads to effective loan recovery.

A cross-sectional survey research design was used to investigate the relationship between the

variables, analytical and descriptive research designs.

It was also found out that post bank has got well established loan recovery procedures among

which include; telephone calls to debtors, sending reminding letters to the clients, and taking

legal action on clients who fail to pay back the loan.

The findings also revealed that there is a moderate relationship of (0.505) between credit policy

management and loan recovery and coefficient of determination of (25.5%) Thus this indicates

that effective credit policies result into effective loan recovery.

It is therefore concluded that that the bad debts that are incurred by the bank as indicated in the

problem statement areas a result of the irrelevancy of the credit officials to effectively follow up

the procedures for recovering the loan.

It is therefore recommended that the credit policies in place should be followed by the credit

officials and also put in place better strategies that will to effective loan recovery.

The suggested ones include; regular training of credit officials, strict customer screening before

advancing the loan for example finding out past behaviors of the client, asking for securities,

finding out the credit worthiness of the clients, and regular reminding of the time to pay back the

loan to the debtors.

Taking legal action against the clients who default paying back the loan should be taken before

the outstanding debts are completely written off as bad debts.

xii

1

CHAPTER ONE

1.0 INTRODUCTION

This chapter will cover background of the study, problem statement, purpose of the study,

objectives of the study, research questions, scope of the study and significance of the study.

1.1 BACKGROUND OF THE STUDY

Credit management policy is a framework formulated by an organization as a guide for credit

decisions (Kakuru, 2003).These involve guidelines on the analysis of credit worthiness of a

customer, terms and conditions of credit and assessment of the ability to pay in order to enhance

loan recovery (Pandey, 2000).it is basically about three major aspects which when properly

handled will lead to easy recovery of the loan. Some of these aspects include evaluation of credit

applicants, advancing loans to successful applicants and monitoring advanced loans to remain

performing. However, with licensing of many banks in Uganda competition increased especially

in banking sector and this resulted into relaxed credit policy management which has resulted into

loan default.

Credit management is a banking practice of evaluating loan applicants, advancing loans to

successful applicants monitoring loans and recovering those that have matured. (kyagulanyi

1999), when function efficiently, credit management serves as an excellent way for the business

to remain finanancially stable.(Malcolm Tatum 2003).

Once the firm has taken the decision to extend credit to the applicant, the amount and duration of

credit has to be decided. However the decision on the magnitude of the credit will depend on

customer‟s financial strength since this has a direct bearing on loan recovery.

On the other hand, loan recovery is the process which involves the procedures that the bank uses

to collect its money from the debtors. It‟s how loans disbursed to clients are paid back (Henni,

1998).It is a measure undertaken by the lending institution to ensure the repayment of loans by

its clients (America, 2003).

Credit policy includes the credit standards, credit terms, and collection procedures. While that of

the loan recovery process are the collateral security, Group members guarantee, saving deposits

and current accounts.

2

Sufficient information should be collected about credit applicants and this should be done in a

bid to minimize losses as a result of investing in vulnerable clients. Sources of such information

may be obtained from company‟s competitors, associate suppliers, individual applicants

themselves (Allen and Gregory, 2000).

The firm/bank needs to continuously monitor and control its credit clients to ensure the success

of collection efforts. But then the firm/bank should not extend collection periods since this will

lead to delays in cash flows which affect the liquidity position of the bank and also it will

increase the chances of bad-debts losses.

Since 2002, Post Bank has pursued a policy of aggressive growth combined with tight credit

management policy in order to enhance loan recovery. As a result Post bank is now enjoying

huge profits because of this effort.

Despite of the credit management policies like interest charged, payment periods, credit

worthiness of customers, collateral security to obtain the loan, assessment of the ability to

monitor the credit, the rate of credit return in Post bank has not been 100% hence this means that

something must be done to evaluate why some customers do not respond in returning the credit

that was extended to them. This is seen in the 2006 Post bank annual report whereby out of

100% expected loan recovery, only 85% was recovered in the stipulated period. Thus this clearly

indicates that once better policies have been identified and applied by Post Bank, the rate of loan

recovery will improve by at least to 100% and hence the reason for conducting this research.

1.2 Statement of the problem

Loan management is an effort aimed at monitoring loans right from the time of loan application

to maturity; it also involves evaluation of credit applicants, repayment of loans by the clients,

planning procedures to recover back the loans from clients.

The credit policies adopted by post bank are; loan application from members, monthly savings to

guarantee, members loans, loan recovery for the credit from loan applicants, policy on

delinquency i.e. loans which have gone bad and have gone beyond 90days and such loans attract

a penalty, policy on loan monitoring to make sure that such loans don‟t go bad and don‟t go in

arrears.

Despite the fact that post bank has adopted the above credit policies the bank has had challenges

recovering its debt from clients hence the problem statement.

3

The bank started with a loan portfolio of over 5 billion Uganda shillings and it now has a

portfolio of over 20 billion Uganda shillings (Management report to directors, 2003)

Despite the fact that post bank had a significant gain in performance in the past financial years

reporting a decline in bad debts from 25%-15% for the year 2002-2003,in the financial year

2004-2010,Post bank Uganda faced hardships in the loan recovery with credit extended to

customers without timely corresponding returns hence reporting an increase in bad debts from

15%-20% which leads to a loss of over US $94800 as bad debts written off (auditor‟s report to

directors,2005).

1.3 Purpose of the study

The purpose of the study was to establish the impact of credit management‟s policies on loan

recovery.

1.4 Objectives of the study

1. To examine the credit management policy of Post bank Uganda

2. To examine the loan recovery levels of Post bank Uganda

3. To establish the relationship between credit management policy and loan recovery of Post

bank Uganda.

1.5 Research Questions

1. What is the credit management system of Post bank Uganda?

2. What is the level of loan recovery in Post bank Uganda?

3. What is the relationship between credit management policy and loan recovery in Post bank?

1.6 Scope of the study

1.6.1 Geographical scope

The study was carried out in Post bank Uganda Kabale branch

1.6.2 Subject scope

The study was focused on the impact of credit management policy on loan recovery.

1.6.3 Time scope

The study was focused on the financial years 2004-2010.

4

1.7 Significance of the study

1. The study will help the researcher to improve on her knowledge of credit policy and loan

recovery management in the banking sector in Uganda, and lead to an award of a

bachelor of commerce degree.

2. The study will help to improve on the credit policy management system and loan

recovery of Post Uganda.

3. The study will be the basis upon which appropriate policy for credit extension especially

with financial institutions will be formulated. This will help them minimize losses.

4. The study will facilitate further research in areas related to credit management policy and

loan recovery in financial institutions in Uganda.

5

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

In this chapter review of literature will be done in accordance with the study variables. This

chapter entails the theory of different scholars in relation to credit policy management. Thus the

literature reviewed will be drawn from some empirical surveys of credit management as part of

financial management.

2.1 Credit management policy

Credit is the money that is owed to a business or firm. This arises when there is a gap or time lag

between the points when credit is acquired and when payment is received from the client

(Kakuru, 2000). Credit policy is a framework formulated by an organization as a guide to credit

decision,(Kakuru,2000). These involve guidelines on the analysis of credit worthiness of a

customer, terms and conditions of credit and assessment of the ability to monitor the credit.

He further says that credit policy is a set of policy actions designed to minimize costs associated

with maximizing the benefit.

Consumer credit is a philosophy of „buy now; pay later” the organization delivers a service, a

product now and allows a delay in receiving payment from the consumers. The credit supplier

must gain an acceptable level of confidence to extend the maximum of credit at the lowest

possible risk of loss.

Credit policy can also be defined as an institution‟s method of analyzing credit request and its

decision criteria for accepting or rejecting application (Administer 1980) the term credit policy is

used to refer to a combination of three decision variables including credit standards, credit terms

and collection efforts.

2.1.1 Credit Standards

These are criterias which a firm follows in selecting customers for the purpose of credit

extension (Kakuru, 2000).Credit standards provide guidelines for determining whether to extend

credit to a customer or not how much credit to extend.

6

.In order to analyze customers and set credit standards,(Kakuru,2000). Two aspects should be

considered and these include; the average collection period (ACP) that is the period in which the

debts remain outstanding and the ratio of uncollected receivables to the total receivables. From

this, the firm is able to determine whether the customer will meet his credit obligations or not.

He also mentioned that to estimate the profitability, the financial manager should consider the

aspects of character, capacity, condition, capital and collateral security.

Character: this refers to the willingness of a customer to settle his obligation.

Capacity: This is the ability of the customer to pay credit advanced to him/her.

Condition: this includes the basement of prevailing economic and other factors like social and

political that may affect the customer‟s ability to pay.

Capital: this is the contribution of an interest of the customer in the business and is shown by

Capital=Assets – Liabilities.

Collateral: this is the security against failure to pay the credit that was extended to the customer.

2.1.2 Credit terms

Credit terms are defined as stipulations under which the firm sells on credit to customers

(Pandey, 2000). The stipulations include credit period and cash discount.

Credit period;

The length of time for which credit is extended. This could be say “net 65 “meaning that all its

customers are expected to repay their obligation in 65 days, (Kakuru, 2000).

It is defined as the length of time of net date and that a firms credit period is governed by

industry norms depending on its objectives of the firms(Semukono,1997), it can lengthen the

credit period, on the other hand the firm may tighten the credit period if customers are frequently

building up debts.

Cash discount

Cash discount is offered to customers in form of a price reduction to reduce the pay their

obligation within a specified period of time, which is less than the normal credit period (Kakuru,

2000).

The cash discount and the period for which it is a variable is used as a tool to increase sales and

accelerate collection for customers (Pandey, 1995).

7

2.1.3 Collection efforts

The overall collection policy of the firm should be such that the administrative costs incurred do

not exceed the benefits for incurring the costs (Don 1998).

The collection efforts are those applied in order to accelerate the collection from slow paying

customers to reduce debt losers, collection procedures should be defined for each credit customer

(Kakuru, 2000).

Firms are cautioned on their collection procedures and this is because tight collection policy may

afford and send away customers while linient ones would increase receivables, bad debts losses

hence affecting profits.

Prompt collection are aimed at increasing turn over while keeping costs low and bad debts within

limit (Pandey, 1995)

Policies are not laws imposed upon an organization from outside but are by people within the

organization so as to help their day today management of the institution therefore the policies

needs to be standard across organizations rather than being focused on the organization

objectives and methods of network (Basaka,1993).

2.2 LOAN RECOVERY

Loan recovery is defined as the process involving procedures that banks or any other micro

finance institution uses to collect its money from debtors (Kyagulanyi,1998). The longer the debt

is allowed to run, the higher the possibility eventually defaults and thus systematic progress of

follow up procedures is required bearing in mind the risk of offending a valued bank customer to

such an extent that they lose business.

The causes of loan default or failure to recover the loans are categorized under political,

institutional and economic causes (Nsereko, 1995).

2.2.1 Political causes

Political pressure on loan application tends to impinge an appraisal ,collecting, targeting and

restricted the lender from exercising prudent judgment(Nsereko,1995).He says it was common in

government administered companies and administered on its behalf like former Uganda

commercial bank (U.C.B).Companies are now recognized as private limited companies under

direct control supervision of bank of Uganda (BOU),(Kyagulanyi,2000),therefore, political

8

pressure on the lending activities has no much influence. This however used to be the case in

Uganda during the late 70‟s and 80‟s.

2.2.2 Institutional causes

This is largely as a result of institutional management deficiency and inherent weaknesses in

lending operations in a particular risk assessment. In loan appraisal, credit analysis and

sanctioning techniques. There is a general lack of effective loan supervision and it‟s very low

especially in case of administered loans resulting in loan recovery.

Currently there is stiff competition in the marketing by participants in financial services, in an

attempt to capture a substantial share of the market. New banks have emerged during the

financial sector reform and are struggling to capture and increase their market share. Opening up

new branches, offering high attractive deposits rates and maintaining high activity in the credit

market, has reduced this competition (B.O.U annual report 2006).

2.2.3 Economic causes

Nsereko observes that these are related to the exchange rate variations, inflation and interest

rates. He says that difficulties of non performance that companies face on foreign lives of credit

are essentially consequences of exchange risk exposure. The appreciation of the shilling may for

example erode recovery capacity of exporters. Normal interest rates exceed by the rate of

inflation actually rewards borrowers who delay recovery as long as inflation tends to make it

easier to repay. Many borrowers will full delay recovery because they can obtain a profit

implying cheap funds at higher rates of return in alternative uses.

The interest rates policy for rural finance seems to have the same view.(Odwong,2000). He

further argues that high interest rates increases the rate of default since the rate of return

generated is not adequate enough to pay the interest charged. He argues that a balance should be

struck between the lender and borrower while setting interest.

2.2.4. Loan recovery methods include;

These are efforts applied in order to accelerate collection from slow paying borrower and reduce

debt default loses,(Kakuru 2000). Well managed financial institutions that manage their credit

policy have high loan repayment rates as compared to institutions with relaxed credit policy

9

management (Pandey 2000). However, with loan repayment the methods of recovery include the

following;

Reminder letter

Posting letters to a customer is one of the most commonly used methods of debt collection. It is

often preferred to other methods because of its unique advantages of maintaining a hard copy of

the reminder with the client and this advantage is lost when the lender uses verbal reminders like

telephone calls however its often regarded as being a relatively poor way of obtaining payments

due to the slowness of postage reminder by fax seems to be more productive than normal

postage.

Telephone calls

This method of debt recovery is a bit more costly than reminder letters but where large sums of

money are involved; they can be an efficient way of accelerating payments from slow paying

debtors. The officer in charge should regularly call customers whose accounts are due to find out

why the customers are failing to honour their obligations when they are planning to pay and the

means of payments they prefer to use. This method of debt collection is generally regarded as

efficient but it‟s quite costly especially where small sums of money are involved.

Debt collection agencies and discount houses

These offer debt collection services on a fixed fee basis or “no collection no charge terms”.

These agencies take over the full responsibilities of collecting money from a bank‟s debtor and

remit the proceeds to the bank. The discount house on the other hand offers the banker a lesser

amount of the total sums expected from the debtor and then waits to collect the full amount when

the borrower pays.

Legal action

This is often the last resort in debt collection after all other responsibilities have failed. The legal

judgment will either make the debtor pay or have his collateral sold off in favour of the bank.

The length of the undue delay period forms a basis of clarifying non performing loans (NPLs).

10

2.3. RELATIONSHIP BETWEEN CREDIT MANAGEMENT POLICY AND LOAN

RECOVERY

Credit management is basically divided into three major aspects which if properly managed then

credit will be considered to have been effectively handled in the company (Barry, 2000).

Those three aspects include evaluating credit, applicants advancing loans to only successful

applicants and monitoring advanced loans to maintain a performing loan portfolio.

Sufficient information should be collected about applications/applicants (Kakuru, 2000).He

further argued that this should be done in a bid to minimize losses as a result of investigating

unreliable clients. Kakuru adds that sources of such information include companies, associate

suppliers, competetitors and individual applicant themselves.

Collection of such information is not free much as costs are justifiable if it is to increase the

potential profitability of the credit (Pandey, 1995)

Once the firm has taken decision to extend credit to the applicants, the amount and duration of

credit have to be decided (Pandey, 1995). He however warns that the decision on the magnitude

of the credit will depend upon customer‟s financial strength since this has a direct bearing on

loan recovery.

A firm needs to continuously monitor and control its credit clients to ensure the success of

efforts, however he cautions that t he firm should not extend collection periods since this delays

cashinflows,impairs the firms liquidity position and increases the chances to bad debts losses.

With respect to decision on credit standards, credit terms, and collection efforts aspects as credit

policies, they all have a direct effect or influence on the credit recovery process in financial

institutions as they determine how much is recovered from the successful loan applicants.

Both credit management policies and loan recovery are related in a sense that credit management

policies is depended upon by loan recovery; in other wards loans recovered in any financial

institution after a given financial year end, depend on how the loans disbursed were managed or

rather administed. Therefore if the management of loans is efficient, then in return, a high rate of

loan recovery will be enjoyed, while as in case the management of loans was poor, loan recovery

too will be poor.

11

2.4 Conclusions

From the above literature much as a lot was written and analyzed credit management policies

and loan recovery by clients, very few have paid particular attention to the relationship that exists

between the two variables thus the success of the post bank Uganda largely depends on the

extent the bank recovers loans advanced to the clients. This is made possible by the fact that post

bank Uganda has effective credit management policies and how these policies facilitate loan

recovery.

12

CHAPTER THREE

METHODOLOGY

3.0 INTRODUCTION

This is chapter we looked at the methods that were used during the research study and the basic

contents in this chapter include; research design, target population, sample section, data sources

and data collection instruments, data analysis techniques and the limitations that are likely to be

faced during the study process.

3.1 Research design

A cross- sectional survey design was used which was based on to investigate and to analyze the

relationship between credit management policies and loan recovery in post bank.

Analytical and descriptive research designs were also used in collecting data regarding credit

policy management and loan recovery.

3.2 Target Population

The study targeted the staff of post bank Uganda and its clients where 40 clients and 40

management officials were contacted.

3.3 Sampling

3.3.1 Sample size

The study used a sample of 40 respondents. This is adequate as per Roscoe‟s rule of thumb and

he stated that a sample of at least 30 respondents is adequate. This constituted 20 members of

staff and 20 clients.

3.3.2 Sampling methods

Purposive sampling method was used in selection of respondents from credit management

officials since the researcher had to identify the respondents with full knowledge about how

credit is managed in the bank, on the other hand, simple random sampling was used in the

selection of respondents from the clients since they were assumed to have the information on the

selected subject.

13

3.4 Data Collection

3.4.1 Data sources

Both primary and secondary data sources were employed in the study process whereby primary

data was collected from the respondents selected from the bank especially credit officers and also

clients while secondary data was obtained from the text books,internet,company journals and

magazines.

3.5 Data collection methods

3.5.1 Questionnaires

This is one of the major instruments that was used while collecting data. They were phrased in

simple language for the respondents to understand.

3.5.2 Interviews

Here the research had a face to face interview where by the researcher asked the interviewee

questions related to credit policy management and loan recovery in post Bank.

3.6 Data collection instruments

3.6.1 Interviews

This method of data collection was used to get first hand information from the respondents.

Interviews were held for respondents especially to the clients who could not read and understand

English yet they posed important information which was relevant to the study.

3.6.2 Self Administered Questionnaire

This consisted of closed ended questionnaires because of being the quickest method and reliable

for wide information. Self – administered questionnaires were designed using likert scale, and

they were distributed to staff members of Post Bank who then filled them.

14

3.7 Data processing, summary and presentation and Analysis

3.7.1 Data processing

Data from the field was sorted, coded and organized to reveal the percentage scores of different

attributes and to ensure accuracy and completeness using Microsoft word.

3.7.2 Data summary and presentation

Data was coded on the computer using Excel.

Data was summarized and presented using tables and charts.

3.7.3 Data analysis

The relationship between the variables was analyzed comparing them with the objectives of the

study and the possible conclusions were drawn from the study using Excel and Statistical

Package for Social Scientists (SPSS).

Spearman correlation coefficient was also to be computed to establish the relationship between

credit policy management and loan recovery.

15

CHAPTER FOUR

PRESENTATION, ANALYSIS AND DISSCUSSION OF FINDINGS

4.0. INTRODUTION

In this chapter presentation, analysis and discussion of findings got from the field using the

methodology described in this chapter three and in accordance with the objectives of this

chapter. The study was done in post bank Uganda in kabala branch and it was based on the

following objectives.

Examines the credit management policy of post bank Uganda

Examine the loan recovery levels of post bank Uganda

Establishes the relationship between credit management policy and loan recovery of post

bank Uganda.

4.1. BACKGROUND OF FINDINGS

Table 1; showing sex o f the respondents.

RESPONSE Frequency Percent

FEMALE 15 37.5%

MALE 25 62.5%

Total 40 100.0%

Source: primary data

In table 1, 62.5%of the respondents were male and 37.5% were female. This implies most

employees of post bank who female. This implies most employees of post bank who responded

were male.

16

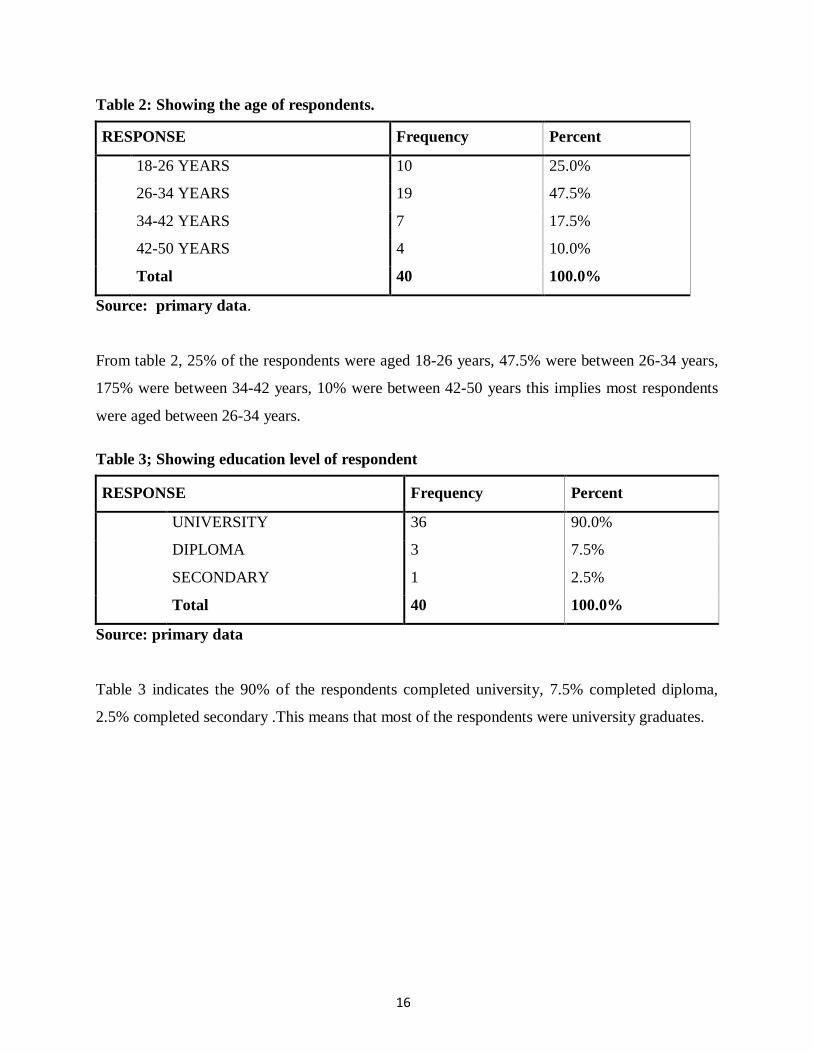

Table 2: Showing the age of respondents.

RESPONSE Frequency Percent

18-26 YEARS 10 25.0%

26-34 YEARS 19 47.5%

34-42 YEARS 7 17.5%

42-50 YEARS 4 10.0%

Total 40 100.0%

Source: primary data.

From table 2, 25% of the respondents were aged 18-26 years, 47.5% were between 26-34 years,

175% were between 34-42 years, 10% were between 42-50 years this implies most respondents

were aged between 26-34 years.

Table 3; Showing education level of respondent

RESPONSE Frequency Percent

UNIVERSITY 36 90.0%

DIPLOMA 3 7.5%

SECONDARY 1 2.5%

Total 40 100.0%

Source: primary data

Table 3 indicates the 90% of the respondents completed university, 7.5% completed diploma,

2.5% completed secondary .This means that most of the respondents were university graduates.

17

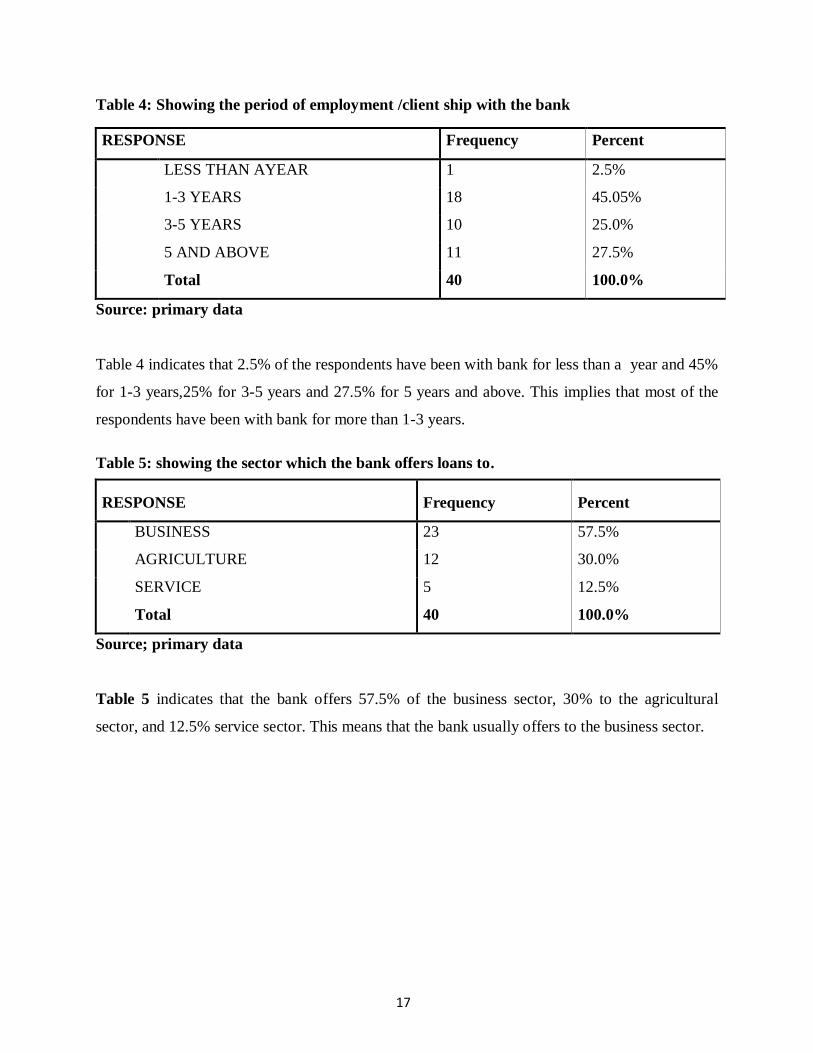

Table 4: Showing the period of employment /client ship with the bank

RESPONSE Frequency Percent

LESS THAN AYEAR 1 2.5%

1-3 YEARS 18 45.05%

3-5 YEARS 10 25.0%

5 AND ABOVE 11 27.5%

Total 40 100.0%

Source: primary data

Table 4 indicates that 2.5% of the respondents have been with bank for less than a year and 45%

for 1-3 years,25% for 3-5 years and 27.5% for 5 years and above. This implies that most of the

respondents have been with bank for more than 1-3 years.

Table 5: showing the sector which the bank offers loans to.

RESPONSE Frequency Percent

BUSINESS 23 57.5%

AGRICULTURE 12 30.0%

SERVICE 5 12.5%

Total 40 100.0%

Source; primary data

Table 5 indicates that the bank offers 57.5% of the business sector, 30% to the agricultural

sector, and 12.5% service sector. This means that the bank usually offers to the business sector.

18

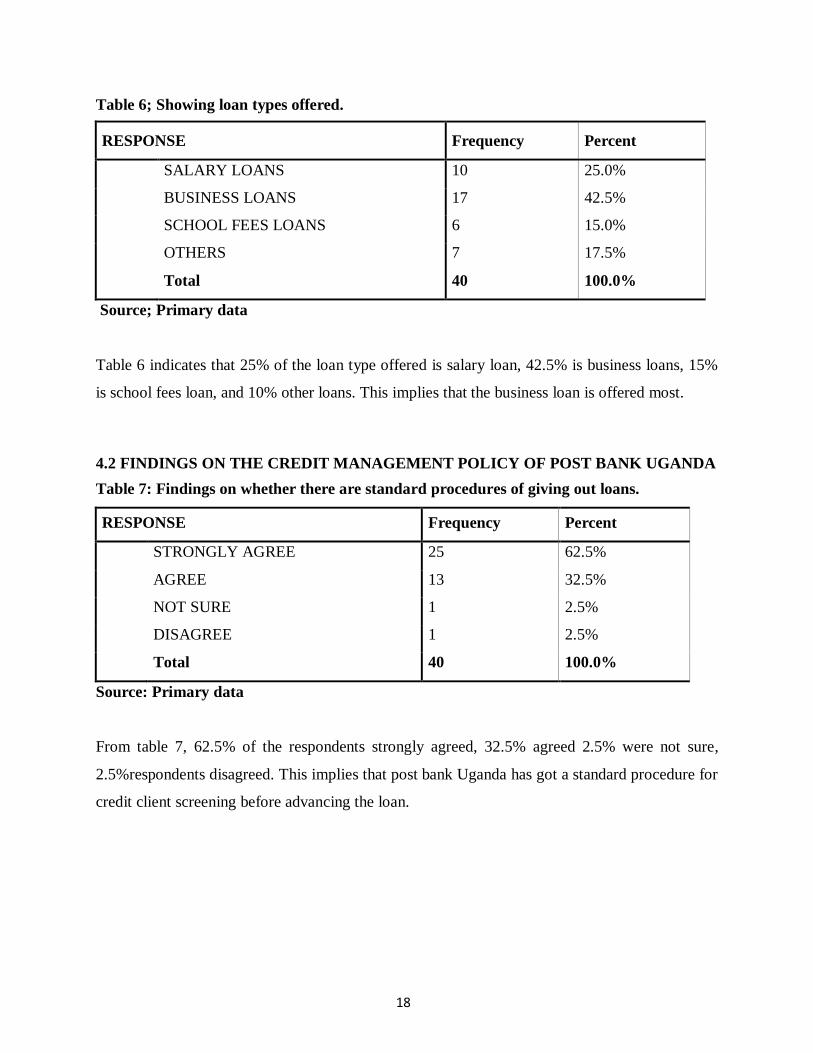

Table 6; Showing loan types offered.

RESPONSE Frequency Percent

SALARY LOANS 10 25.0%

BUSINESS LOANS 17 42.5%

SCHOOL FEES LOANS 6 15.0%

OTHERS 7 17.5%

Total 40 100.0%

Source; Primary data

Table 6 indicates that 25% of the loan type offered is salary loan, 42.5% is business loans, 15%

is school fees loan, and 10% other loans. This implies that the business loan is offered most.

4.2 FINDINGS ON THE CREDIT MANAGEMENT POLICY OF POST BANK UGANDA

Table 7: Findings on whether there are standard procedures of giving out loans.

RESPONSE Frequency Percent

STRONGLY AGREE 25 62.5%

AGREE 13 32.5%

NOT SURE 1 2.5%

DISAGREE 1 2.5%

Total 40 100.0%

Source: Primary data

From table 7, 62.5% of the respondents strongly agreed, 32.5% agreed 2.5% were not sure,

2.5%respondents disagreed. This implies that post bank Uganda has got a standard procedure for

credit client screening before advancing the loan.

19

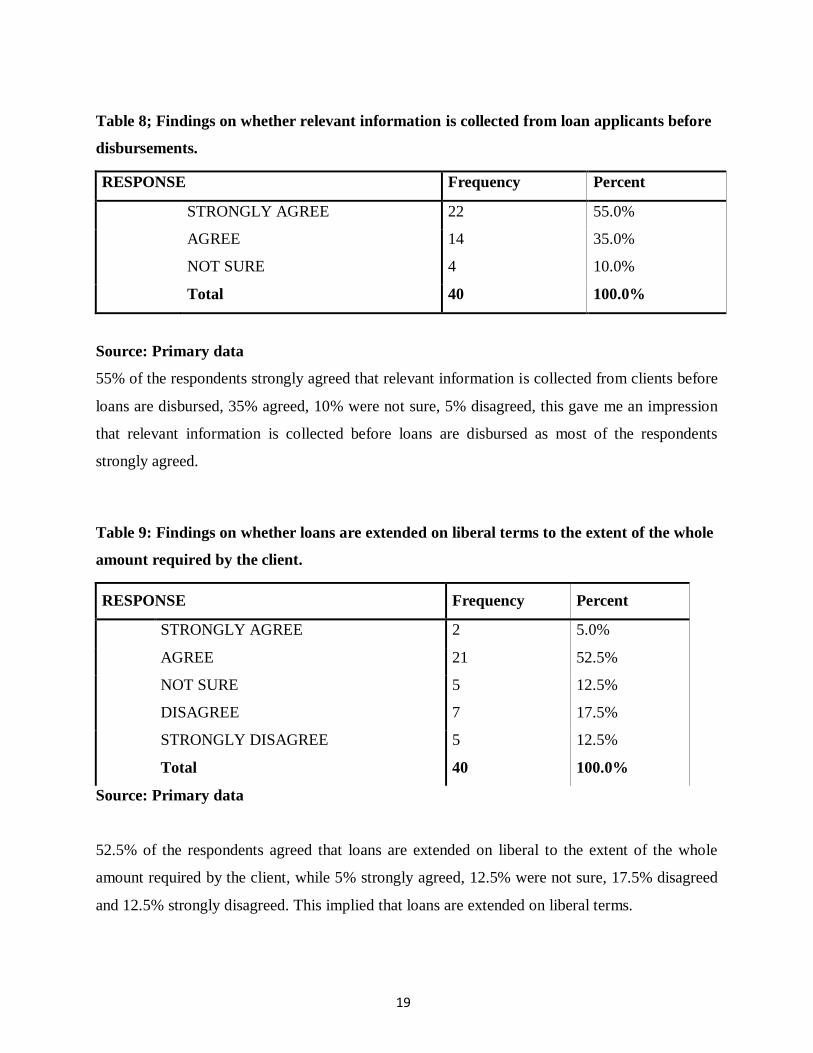

Table 8; Findings on whether relevant information is collected from loan applicants before

disbursements.

RESPONSE Frequency Percent

STRONGLY AGREE 22 55.0%

AGREE 14 35.0%

NOT SURE 4 10.0%

Total 40 100.0%

Source: Primary data

55% of the respondents strongly agreed that relevant information is collected from clients before

loans are disbursed, 35% agreed, 10% were not sure, 5% disagreed, this gave me an impression

that relevant information is collected before loans are disbursed as most of the respondents

strongly agreed.

Table 9: Findings on whether loans are extended on liberal terms to the extent of the whole

amount required by the client.

RESPONSE Frequency Percent

STRONGLY AGREE 2 5.0%

AGREE 21 52.5%

NOT SURE 5 12.5%

DISAGREE 7 17.5%

STRONGLY DISAGREE 5 12.5%

Total 40 100.0%

Source: Primary data

52.5% of the respondents agreed that loans are extended on liberal to the extent of the whole

amount required by the client, while 5% strongly agreed, 12.5% were not sure, 17.5% disagreed

and 12.5% strongly disagreed. This implied that loans are extended on liberal terms.

20

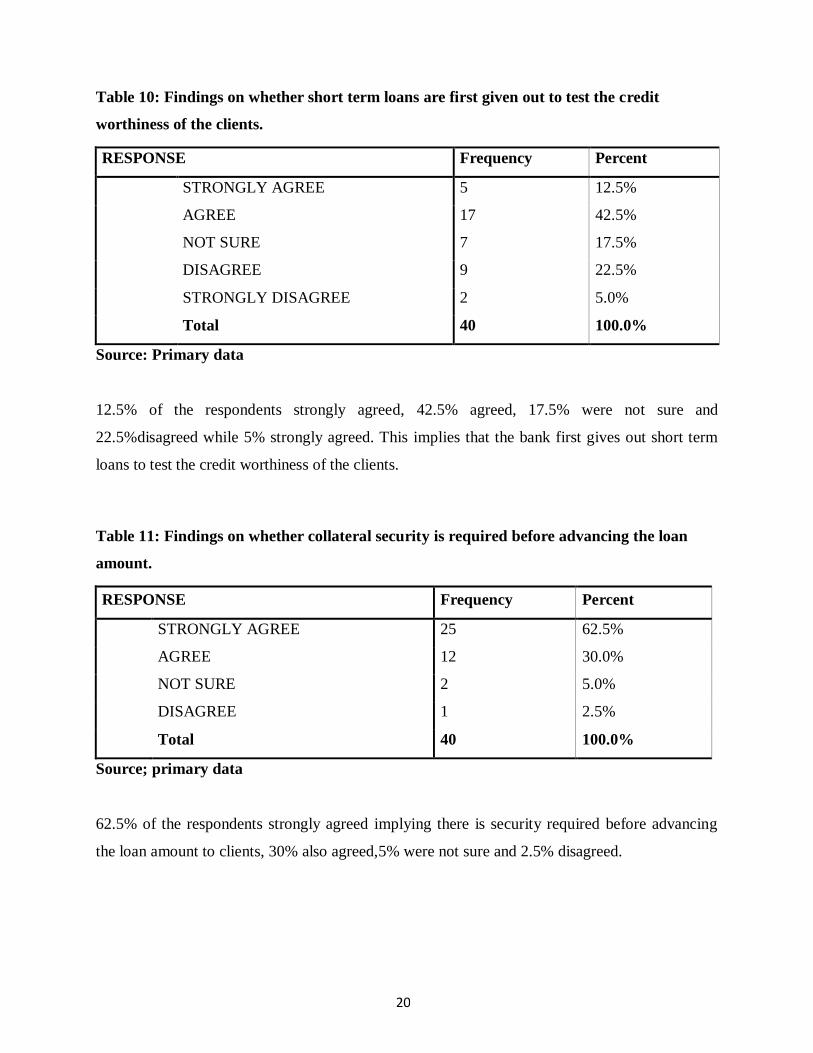

Table 10: Findings on whether short term loans are first given out to test the credit

worthiness of the clients.

RESPONSE Frequency Percent

STRONGLY AGREE 5 12.5%

AGREE 17 42.5%

NOT SURE 7 17.5%

DISAGREE 9 22.5%

STRONGLY DISAGREE 2 5.0%

Total 40 100.0%

Source: Primary data

12.5% of the respondents strongly agreed, 42.5% agreed, 17.5% were not sure and

22.5%disagreed while 5% strongly agreed. This implies that the bank first gives out short term

loans to test the credit worthiness of the clients.

Table 11: Findings on whether collateral security is required before advancing the loan

amount.

RESPONSE Frequency Percent

STRONGLY AGREE 25 62.5%

AGREE 12 30.0%

NOT SURE 2 5.0%

DISAGREE 1 2.5%

Total 40 100.0%

Source; primary data

62.5% of the respondents strongly agreed implying there is security required before advancing

the loan amount to clients, 30% also agreed,5% were not sure and 2.5% disagreed.

21

Table 12; Findings on whether loan follow up and monitoring is done to check the viability

of the clients loan project.

RESPONSE Frequency Percent

STRONGLY AGREE 15 37.5%

AGREE 22 55.0%

NOT SURE 2 5.0%

DISAGREE 1 2.5%

Total 40 100.0%

Source, Primary data

37.5% of the respondents strongly agreed and 55% agreed 5% were not sure, 2.5%disagreed,

meaning that loan follow up and monitoring is normally done to check loan performance.

Table 13: Findings on whether loans are offered for a long period of time.

RESPONSE Frequency Percent

STRONGLY AGREE 10 25.0%

AGREE 19 47.5%

NOT SURE 2 5.0%

DISAGREE 8 20.0%

STRONGLY DISAGREE 1 2.5%

Total 40 100.0%

Source, Primary data

25% of the respondents strongly agreed, 47.5% agreed, 5% were not sure, 20% disagreed, 2.5%

strongly disagreed. This implied that loans are offered for a long period of time.

22

4.3 FINDINGS ON LOAN RECOVERY

Table: 14 Findings on whether there are procedures to collect principle amount and

interest due the loan from clients.

RESPONSE Frequency Percent

STRONGLY AGREE 29 72.5%

AGREE 9 22.5%

DISAGREE 2 5.0%

Total 40 100.0%

Source: Primary data

According to Table 14, 72.5% of the respondents strongly agreed that there are established

procedures for loan collection from the clients. These procedures mentioned included factoring

of the non repaid loans, telephoning defaulted clients, sending reminders to the clients, legal

procedures and writing off debt as a bad debts 22.5% agreed, 5%disagreed. This gave an

impression that the bank has got well established procedures of collecting their loans.

Table 15: Findings on whether clients pay their debts on the due date

RESPONSE Frequency Percent

STRONGLY AGREE 11 27.5%%

AGREE 9 22.5%

NOT SURE 5 12.5%

DISAGREE 13 32.5%

STRONGLY DISAGREE 2 5.0%

Total 40 100.0%

Source; Primary data

32.5% of the respondents disagreed, 27.5% strongly agreed, 22.5% agreed, 12.5% were not sure

and 5% strongly agreed that clients normally pay their debts on the dates. Those that disagreed

said this is a rare case since there are many factors affecting loan projects. This implied that the

bank has to recover over-due amounts from most of the clients and this might lead to an increase

in the amount of loan default.

23

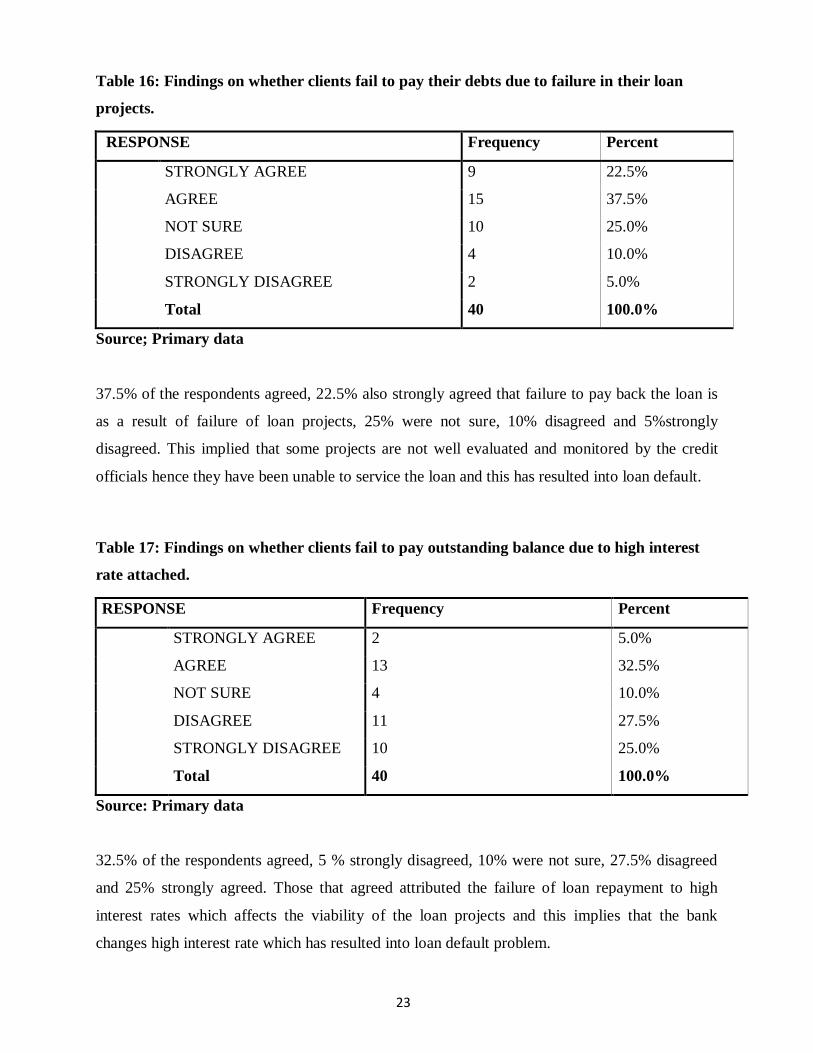

Table 16: Findings on whether clients fail to pay their debts due to failure in their loan

projects.

RESPONSE Frequency Percent

STRONGLY AGREE 9 22.5%

AGREE 15 37.5%

NOT SURE 10 25.0%

DISAGREE 4 10.0%

STRONGLY DISAGREE 2 5.0%

Total 40 100.0%

Source; Primary data

37.5% of the respondents agreed, 22.5% also strongly agreed that failure to pay back the loan is

as a result of failure of loan projects, 25% were not sure, 10% disagreed and 5%strongly

disagreed. This implied that some projects are not well evaluated and monitored by the credit

officials hence they have been unable to service the loan and this has resulted into loan default.

Table 17: Findings on whether clients fail to pay outstanding balance due to high interest

rate attached.

RESPONSE Frequency Percent

STRONGLY AGREE 2 5.0%

AGREE 13 32.5%

NOT SURE 4 10.0%

DISAGREE 11 27.5%

STRONGLY DISAGREE 10 25.0%

Total 40 100.0%

Source: Primary data

32.5% of the respondents agreed, 5 % strongly disagreed, 10% were not sure, 27.5% disagreed

and 25% strongly agreed. Those that agreed attributed the failure of loan repayment to high

interest rates which affects the viability of the loan projects and this implies that the bank

changes high interest rate which has resulted into loan default problem.

24

Table 18: Findings on whether there are fines instituted due to failure to pay the principle

amount and the accrued interest in time.

RESPONSE Frequency Percent

STRONGLY AGREE 4 10.0%

AGREE 30 75.0%

NOT SURE 2 5.0%

DISAGREE 4 10.0%

Total 40 100.0%

Source; Primary data

75% of the respondents agreed, 10% strongly agreed, 5% were not sure and 10% disagreed. This

implied that there are fines charged on clients who delay to pay back the principle amount and

the accrued interest in time.

Table 19: Findings on the efficiency of the loan recovery system

RESPONSE Frequency Percent

STRONGLY

AGREE 9 22.5%

AGREE 21 52.5%

NOT SURE 2 5.0%

DISAGREE 8 20.0%

Total 40 100.0%

Source; Primary data

22.5% of the respondents strongly agreed, 52.5% agreed, 5% were not sure, 20% disagreed. This

implied that the loan recovery system of the bank is efficient.

25

4.4 FINDINDS ON THE RELATIONSHIP BETWEEN CREDIT MANAGEMENT

POLICY AND LOAN RECOVERY OF POST BANK

Table 20: Findings on whether procedures for loan disbursements are liberal that whoever

wants the loan is given and pays at the time he/she feels like.

RESPONSE Frequency Percent

STRONGLY AGREE 13 32.5%

AGREE 6 15.0%

NOT SURE 1 2.5%

DISAGREE 9 22.5%

STRONGLY DISAGREE 11 27.5%

Total 40 100.0%

Source: Primary data

32.5% of the respondents strongly agreed, 15% disagreed, 2.5% were not sure, 22.5% disagreed,

27.5% strongly disagreed. This implied that the procedures for loan disbursements are liberal.

Table 21: Findings on whether clients who fail to pay back the loan are written off as bad

debts.

RESPONSE Frequency Percent

STRONGLY AGREE 11 27.5%

AGREE 21 52.5%

NOT SURE 2 5.0%

DISAGREE 6 15.0%

Total 40 100.0%

Source: Primary data

27.5% of the respondents strongly agreed, 52.5%, 5% were not sure, 15% disagreed. This

implied that clients who fail to repay the loan are written off as bad debts.

26

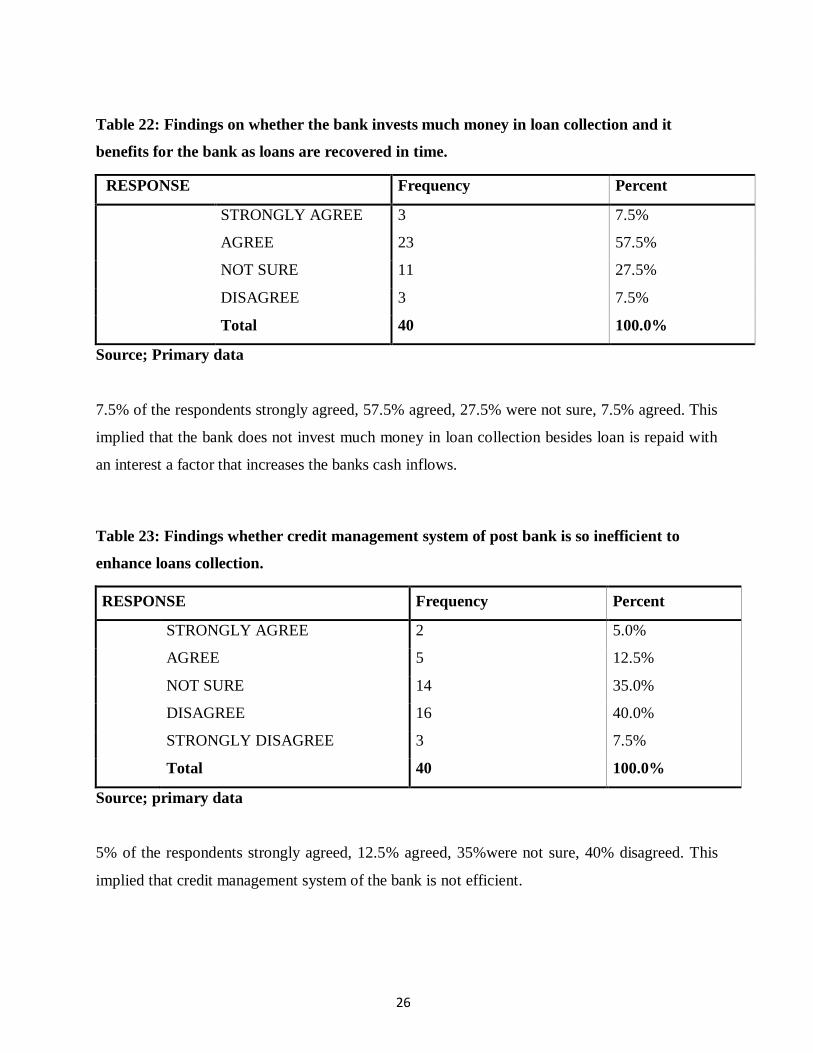

Table 22: Findings on whether the bank invests much money in loan collection and it

benefits for the bank as loans are recovered in time.

RESPONSE Frequency Percent

STRONGLY AGREE 3 7.5%

AGREE 23 57.5%

NOT SURE 11 27.5%

DISAGREE 3 7.5%

Total 40 100.0%

Source; Primary data

7.5% of the respondents strongly agreed, 57.5% agreed, 27.5% were not sure, 7.5% agreed. This

implied that the bank does not invest much money in loan collection besides loan is repaid with

an interest a factor that increases the banks cash inflows.

Table 23: Findings whether credit management system of post bank is so inefficient to

enhance loans collection.

RESPONSE Frequency Percent

STRONGLY AGREE 2 5.0%

AGREE 5 12.5%

NOT SURE 14 35.0%

DISAGREE 16 40.0%

STRONGLY DISAGREE 3 7.5%

Total 40 100.0%

Source; primary data

5% of the respondents strongly agreed, 12.5% agreed, 35%were not sure, 40% disagreed. This

implied that credit management system of the bank is not efficient.

27

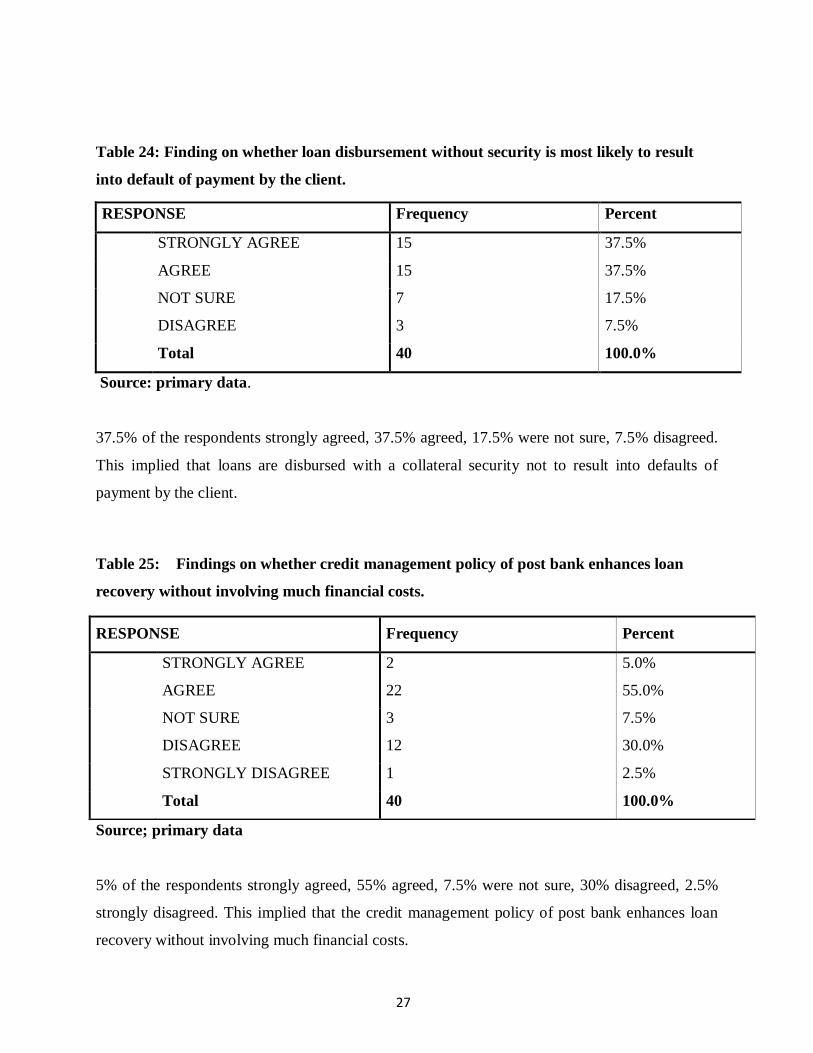

Table 24: Finding on whether loan disbursement without security is most likely to result

into default of payment by the client.

RESPONSE Frequency Percent

STRONGLY AGREE 15 37.5%

AGREE 15 37.5%

NOT SURE 7 17.5%

DISAGREE 3 7.5%

Total 40 100.0%

Source: primary data.

37.5% of the respondents strongly agreed, 37.5% agreed, 17.5% were not sure, 7.5% disagreed.

This implied that loans are disbursed with a collateral security not to result into defaults of

payment by the client.

Table 25: Findings on whether credit management policy of post bank enhances loan

recovery without involving much financial costs.

Source; primary data

5% of the respondents strongly agreed, 55% agreed, 7.5% were not sure, 30% disagreed, 2.5%

strongly disagreed. This implied that the credit management policy of post bank enhances loan

recovery without involving much financial costs.

RESPONSE Frequency Percent

STRONGLY AGREE 2 5.0%

AGREE 22 55.0%

NOT SURE 3 7.5%

DISAGREE 12 30.0%

STRONGLY DISAGREE 1 2.5%

Total 40 100.0%

28

Table 26: Findings on whether the level of loan default would be so high without the credit

management policy currently in place

RESPONSE Frequency Percent

STRONGLY AGREE 14 35.0%

AGREE 25 62.5%

STRONGLY DISAGREE 1 2.5%

Total 40 100.0%

Source; primary data.

35% of the respondents strongly agreed, 62.5% agreed, 2.5%strongly agreed. This implied that

without the credit management policy currently place the levels of default would be so high.

Relationship between credit policy management and loan recovery.

The relationship between credit management policy and loan recover was determined using

spearman‟s correlation coefficient and it showed the result below.

Table27; Showing computation of spearman’s correlation coefficient Correlations

Credit management

policy

Loan recovery

Spearman's

rho

Credit

management

policy.

Correlation

Coefficient 1.000 -.109

Sig. (2-

tailed) . .505**

N 40 40

Loan

recovery

Correlation

Coefficient -.109 1.000

Sig. (2-

tailed) .505** .

N 40 40

**Correlation is significant at the 0.01level (2-tailed).

Source; primary data.

29

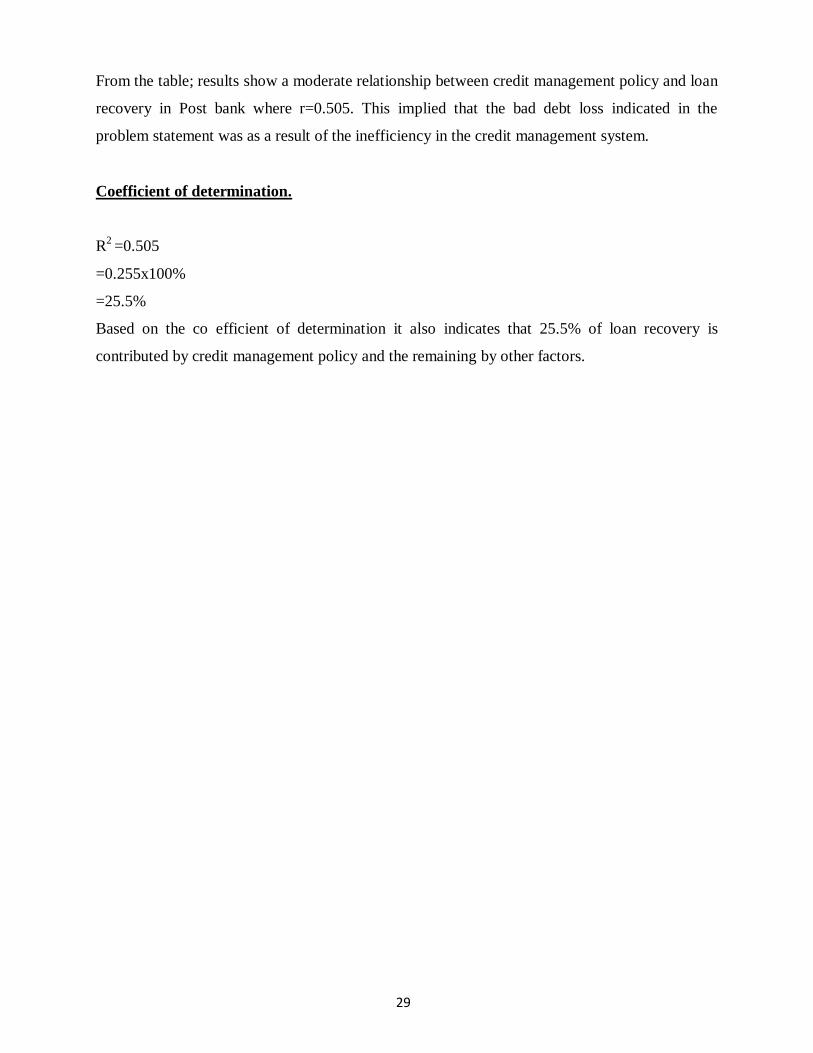

From the table; results show a moderate relationship between credit management policy and loan

recovery in Post bank where r=0.505. This implied that the bad debt loss indicated in the

problem statement was as a result of the inefficiency in the credit management system.

Coefficient of determination.

R2 =0.505

=0.255x100%

=25.5%

Based on the co efficient of determination it also indicates that 25.5% of loan recovery is

contributed by credit management policy and the remaining by other factors.

30

CHAPTER FIVE

SUMMARY OF FINDINGS, CONCLUSIONS AND RECOMMENDATIONS

5.0 Introduction.

In this chapter the summary of findings from the study is done, and the conclusions are made and

recommendations in accordance with the objectives mentioned in chapter one.

5.1 Discussion of findings.

Here the discussion of findings is in relation to the literature review in chapter two which entails

the theory of different scholars in relation to the study variables.

5.1.1 Credit management policy

Credit is the money that is owed to a business or firm. This arises when there is a gap or time lag

between the points when credit is acquired and when payment is received from the client

(Kakuru, 2000) credit policy is a frame work formulated by an organization as a guide to credit

decision (Kakuru 2000). These involve guide lines on the analysis of the credit worthiness of the

client, terms and conditions of credit and assessment to monitor the loan. Credit policy can also

be defined as institutions method of analyzing credit request and its decision criteria for

accepting or rejecting application (Administer 1980) and the term credit is used to refer to a

combination of variables including credit standards, credit terms and collection period or efforts.

Credit management is a banking practice of evaluating loan applicants and advancing loans to

successful applicants, monitoring loans and recovering those that have matured (Kyagulanyi

1999).

The researcher found out that the guidelines and policy framework formulated by post bank to

ensure efficient credit management policy and efficient loan recovery were aspects of character,

capacity,condition,capital,and collateral security.

5.1.2 Loan recovery

Loan recovery is defined as process involving procedures that banks or any other micro-finance

institution uses to collect it‟s money from debtors (Kyagulanyi1998) The longer the debt is

allowed to run the higher the possibility eventually defaults and thus systematic progress of

follow up is required bearing in mind the risk of offending a valued bank customer to such an

extent that they lose business.

31

The causes of loan default or failure to recover the loans is categorized under political,

institutional, and economic causes. (Nsereko, 1995).

5.2 Summary of findings

5.2.1 On the credit policy management, majority of the respondents indicated that post bank

employs four basic ways while assessing customers for the credit to be given out and these

include; capital, collateral security, capacity and conditions under which the person operates. But

these were not efficiently and effectively implemented hence the bank has made significant

losses in form of loan default.

5.2.2 On the loan recovery procedures employed by post bank, procedures like sending

reminders through customer contacts, factoring of bad loans, selling of loan securities, legal

procedures and finally writing off loan as a bad debt were found out to be used. However these

procedures have not been well followed thus the problem of loan recovery has continued to exist.

5.2.3 On the relationship between credit policy management and loan recovery, as per

spearman‟s correlation co-efficient of 0.505, it implied that there is a significant and moderate

relationship between credit policy management and loan recovery in post bank.

5.3 Conclusions

From the above findings, the researcher concluded that the credit management policy is efficient

therefore efficient in recovering the loans. The respondents indicated that the losses in form of

loan default indicated in the problem statement was as a result of failure of the credit officials to

exploit the procedures required before loans are disbursed to the clients such as; seeking for

security against the loan, loan follow up and monitoring, client screening to find the credit

worthiness of the loan applicants, thus if all these are strictly followed then maximum loan

recovery will be realized.

5.4 Recommendations

The researcher made the following recommendations;

Customers should be involved in determining the timing and duration of their loan with in

institutional parameters where by all the debtors should be permitted to choose to pay the loan in

weekly , monthly, installments over an agreed period preferably over the period not exceeding

six months. This will be easy for customers to pay the loan easily.

32

Post bank should ensure an efficient credit policy management which must incorporate credit

screening, close supervision of the recovery process, debt collection, strict monitoring of

customers(debtors).Thus an efficient credit policy strategy should also be able to ensure coerce

but also facilitate the clients to settle their loan in time.

The management of post bank should also make continuous monitoring of the utilization of loans

given out in order to avoid misallocation of loans that could be directed to non-performing

activities.

Members should also be sensitized and trained on the utilization of the loans and payment

procedures in order to avoid defaulting in the long run.

5.5 Areas of further research

1. The role of credit assessment in loan recovery.

2. Credit policies and growth trend in microfinance institutions in economic development in

Uganda.

33

REFERENCES

Allen N.B and Gregory, F.U. (2000). The future of small business lending, Second Edition, New

York University.

Barry, Peter (2001), Loan Portfolio Management. Journal of institute of credit management

I.M Pandey (1995), Financial Management, 7th Edition, Vikas, publishing (PVT) Ltd.

I.M Pandey (2000) Financial Management, 7th

Revised Edition, publishing House pvt India.

Kakuru Julius (2001), Financial Decisions and the Business, Second Edition,The business

publishing group.

Kakuru Julius (2003), Financial Decisions and the Business, Third Edition, The business

publishing group.

Kasozi David (1998), Credit Delivery and Loan performance, MUK.

Kasozi David (1999), Credit Appraisal / Processing.

Kyagulanyi. D. (1998), Bank Portfolio Management and Performance ,MUK..

Malcolm Tatum (2003), Edited by Bronwyn Harris.

Nsereko.J. (1995), Credit Management in Commercial Banks.

Post Bank (2003), Management report to Directors.

Post Bank (2005), Auditors report to Directors.

Post Bank (2006), Annual reports.

34

Appendix 1.

QUESTIONNAIRE TO THE RESPONDENTS FROM CREDIT OFFICIALS OF POST

BANK UGANDA (KABALE BRANCH)

Dear respondent,

This is a questionnaire on credit management policy and loan recovery administered to the credit

officials of post bank Uganda (Kabale Branch).It is presented by a student of Bachelor of

commerce from Makerere university thus feel free to give responses to the best of your

knowledge about these variables as, the information is purely for academic purposes and the

information provided will be treated with utmost confidentiality.

TICK THE SELECTED ALTERNATIVES AND TICK AS TO WHERE YOU

STRONGLY AGREE (SA), NOT SURE (NS), DISAGREE (D) OR STRONGLY

DISAGREE (SD) WITH THE STATEMENT/QUESTION.

PART 1: BACKGROUND INFORMATION

1. Sex

(a).Male (b) Female

2. Your age bracket

(a) 18-26 years b) 26-34 years c) 34-42 years

d) 42-50 years e)Above 50 years

3. Education level

a) University level b) diploma level c) secondary level

d) Primary level

4. For how long have you been with Post Bank Uganda?

a) Less than a year b) 1-3 years c) 3-5 years

d) Above 5 years

5. Which sector does Post Bank usually offer loans to?

a) Business b) Agriculture c) Housing

d) Service

6. What type of loan does Post Bank offer?

a) Salary loans b) Business loan c) School fees loans d) Others

35

PART II: CREDIT MANAGEMENT POLICY OF POST BANK

NO. QUESTION/STATEMENT SA A NS D SD

1 Post Bank has got a standard procedure for credit client

screening before advancing the loan

2. Relevant credit information (past behavior on the loan

borrowed. loan borrowing experience and projects

established using borrowed money) is first obtained

from the loan client before disbursement

3 The company normally extends loans on liberal terms

to the extent of the whole amount required by the

client.

4 The company first gives short-term loans to test the

credit worthiness of the clients

5 There is security required before advancing the loan

amount

6 Loan follow up and monitoring is normally done to

check the viability of the clients loan project

7 Loans are offered for a long period of time e.g. over 1

year.

PART III: LOAN RECOVERY

NO. QUESTION/STATEMENT SA A NS D SD

1 There are established procedures to collect the

principle amount and interest due from the loan

clients

2 Loan clients normally pay their debts on the due

date i.e. they don‟t exceed the date of repayment.

3 Clients fail to pay their debts due to failure in heir

loan projects

4 Clients fail to pay outstanding balance due to high

interest rate attached.

5 There are times instituted due to failure to pay the

principle amount and the accrued interest in time

6 In your view, do you agree that the loan recovery

system is efficient as it prompts loan repayments in

time?

36

PART 1V: RELATIONSHIP BETWEEN CREDIT MANAGEMENT POLICY AND

LOAN RECOVERY.

NO. QUESTION/STATEMENT SA A NS D SD

1 The procedures for loan disbursements are liberal

that whoever wants the loan is given and pays at the

time he/she feels like.

2 There are clients who have failed to repay their

amounts and have written off.

3 The company invests much money in loans

collection but it benefits for the company because

loans are recovered in time.

4 The credit management system of post bank

Uganda is so inefficient to enhance loans

collection, but it benefits for the company because

loans are recovered in time.

5 Loan disbursement without security is most likely

to result into default of payment by the client.

6 The credit management policy of post bank Uganda

enhances loan recovery without involving much

financial costs.

7 Without the credit management policy currently in

place, the levels of default would be so high.

THANK YOU VERY MUCH FOR YOUR TIME