credit card industry in india-yash rochlani

DESCRIPTION

This is a project related to credit card industry in India.TRANSCRIPT

INDEX

SR.NO DESCRIPTION PAGE NO.

1. Objective of the study 1

2. Executive summary 2

3. Introduction of Credit Card industry in India 3-5

4. Features of Credit Card 6-7

5. About Credit Card 8-9

6. Working of a Credit Card 10-12

7. Need of a Credit Card 13-16

8. Ways to avoid Credit Card fraud 17-19

9. Factors before applying for a Credit Card 19-26

10. Triggers 27-29

11. Research Methodology 30

12. Data Interpretation 31-38

13. Standard Chartered Bank

13.1 History 39-40

13.2 Types of Banking 40-41

13.3 Their Growth 42-44

13.4 Their Strategies 44

13.5 Their Awards 45-52

13.6 Background of Standard Chartered Credit Cards 52-53

13.7 Top Standard Chartered Bank Credit Cards 54-64

14. Conclusion 65

15. Limitations 66-67

16. Questionnaire on Credit Cards 68-70

CREDIT CARD

INDUSTRY IN

INDIA

1. Objectives of the Report

To study the Credit Card Industry in India in terms of its features , characteristics ,

factors affecting the market and trends visible in the market in the near future .

Recommendations to enter the market.

Portrayal of an unbiased view of the industry for Potential Issuers.

Strategies to enable a new entrant in the market, to capitalize the opportunity

prevailing in the market, establish itself and gain a market share.

2. Executive Summary

The Indian credit card market is red hot at the moment. With the market predicted to grow at

25% until 2012, and just 25 million adults having credit cards (out of a billion population)

every single bank on the planet wants a piece of the pie. The consumers in India enjoy a huge

number of choices of cards. Sides, the banks and the consumers see a lot of problem between

each other. India does not yet have a unique nationalized ID like social security number in

US, or Tax File Number in Australia for all of their citizens. The problem for the banks with

this is that there is a huge risk to give out these credit cards that can never be traced if the

holder changes his or her address. The consumer on the other hand complains about

exorbitant hidden fees, fines and non-existent customer service. There are still not a lot of

regulations for the credit card industry. Any one on the road is given a credit card (even by

non-bank employees who work as sale sub-vendors to banks) without any proper checks or

verification .Well but India is one market that any bank cannot ignore, so as time goes by

proper regulations will be put in place to get things in order.

A credit card is a small piece of rectangular plastic which is as broad as a sheet of paper,

though it cannot be folded. Initially credit cards were metal tokens in the shape of coins, then

they changed to metal plates to celluloid then to fiber and now plastic with perhaps a photo of

the holder and a magnetic strip on the reverse containing security information such as a

personal identification number enabling the card to be used at money dispensing machines

(ATM's) and merchant establishments.

Credit is the system of buying some produce or service without having to pay for it at the time

of the transaction. The payment is made at a predetermined later date with the addition of a

fee to the billed amount. This is like loaning someone money to buy something without

actually giving them the cash but instead giving them the product they want to buy. So, the

system of credit is not new to humanity, In fact, it is as old as civilization itself or perhaps

even older. The entrepreneurs of the inhuman kind have been proclaimed responsible for

identifying human needs as a rollicking business, and so they invented the credit card system.

3. Introduction of Credit Card industry in India

Introduction

In India, the number of valid credit cards in circulation is more than 275 lakh, the number of

transactions is of the order of 2282 lakh and the amount of transactions Rs. 57,958 crore in

the year 2010-11. Over the past 5 years, there has been a substantial increase in credit card

transactions.

The debit cards have had a slow start and their growth only took off in the last one year. On

the other hand, the credit cards grew faster since inception with the growth turning even

sharper in the latest year.

Card Business in India

As per current trends, the annual rate of increase in the number of credit cards and its number

of transactions is 16% and 25% respectively. Even the amount of transactions increased at a

nominal rate of 28% per annum. See Appendix A for card payments data.

Before we introduce the issue under study, it will be interesting to know the parties to the

credit card system, the flow of funds and levy of fee charges. The system consists of a

customer who holds a credit card from his issuing bank (called issuer), a merchant who has

been given the facility of accepting credit cards by his acquiring bank (also called acquirer)

and MasterCard/VISA, etc., whose networks are being used. In this system, first a merchant

who decides to accept credit or debit cards in exchange for goods or services establishes a

merchant account by forming a relationship with an acquiring bank. This relationship enables

the merchant to receive sale proceeds from credit card purchases through credits in his

account. However, while receiving such credits, the acquirer applies a Merchant Discount

Rate (MDR), which is paid by the merchant to the acquirer in consideration for card

acceptance services. A MDR is the percentage of sales that a merchant pays to the acquiring

bank to process credit card transactions. This rate generally varies from 1% to 3%. Thus,

considering the average MDR to be 2%, the revenue generated in the card business, through

MDR only, is of the order of Rs. 1160 crore. On 3the other hand, the cardholder pays charges

in form of annual fee, finance charges, late payment charges, etc. to his card issuing bank. The

risk of default by credit cardholders is borne by the issuing bank.

The Interchange fee on a purchase transaction flows from the merchant acquiring bank to the

card issuing bank. The settlement and credit transactions between the issuer and the acquirer

are done using the network of MasterCard/VISA, who gets a share of the fee in exchange.

In India, though competition guides acquirer-merchant pricing policies, it is generally

understood that Interchange fees is one component of the MDR established by acquirers.

The implementation of proper Interchange rates is necessary and also very crucial for

maintaining a strong and vibrant credit card payments network. The other major component

of the MDR is the fee imposed by the acquirer which is retained by the acquirer to meet its

own expenses. It is quite common to see a transaction at a merchant establishment involving a

bank which is both the acquirer and the issuer. In such a situation it may be possible to reduce

the Interchange fee since the payment network is substantially reduced. However, such

reduced Interchange fee is not generally passed on to the merchants.

The banks and MasterCard/VISA generate revenue and make profit in the credit card system

by charging Interchange fees. In the western countries big merchants have already realized

this and are in union in their demand for reduction in Interchange fees.

Origin of credit card

The credit card had its beginning in an embarrassing incident that took place in the early

1950’s in America. The story goes that Mr.Mc Namara; a New York businessman took his

friends out to dinner .At the end of meal he discovered that he had forgotten his wallet at

home, the proprietor was kind enough to allow him a later settlement of bill. As McNamara

stepped out of the restaurant hehad the brainwave for the introduction of credit cards - system

of availing instant credit upon confirming the identity of cardholder. Thus was born the

Diners Club Cards, the pioneer of today’smulti billion-dollar plastic money business .Diners

Club adopted a promising approach by recruiting various hotels and restaurants to act as

member establishments for accepting the cards. Not only did these establishments pay a

commission on member’s purchases but the members also paid an annual subscription fee.

Diners Club vetted its members for credit.While issuing the cards may seem to be easy, the

challenge for the banks lies in being able to manage their portfolios by keeping the

delinquency levels at the lowest. Huge investments in systems infrastructure

and are therefore , a necessity. The increase is being attributed to new ideas such as round-

the-clock functioning of card issuing banks and pulling out all stops even at a loss, to grab a

sizeable share of the expanding pie. Not to be left behind in this race, even the big brother, the

State Bank of India in association with GE Capital entered the card business .The spurt in the

card business has gathered momentum during the past couple of years. For instance, the Hong

Kong & Shanghai Banking Corporation (HSBC), was in the credit cards business since seven

years, but from 50,000 card holders in 1997, it has about three lakh card holders now .India’s

fastest growing credit card company - SBI Cards 2.5 lakh credit cards…25 cities…16 months.

The joint venture between India’s largest bank – State Bank of India and one of the world’s

leading financial services companies – GE Capital, SBI Cards & Payment Services (SBI

Cards) has issued 2.5 lakh credit cards across 25 cities (the largest distribution network in the

payment card industry) within 16 months. Thereby achieving the target in the fastest period

seen in India’s payment card industry .SBI Cards & Payments Services attributed this success

to SBI’s enormous brand equity, and unparalleled retail branch network coupled with GE

Capital’s payment card process and technology expertise. He also highlighted Speed,

Simplicity and Service as the key drivers of growth for the SBI Card. Speed Unique and

exclusive 14-day average turnaround time, coupled with availability of the SBI Card in 25

cities in just 16 months Simplicity Simple application process with minimum documentation.

Service 24 hours a day/7 days a week local call access to the SBI Card Help line across 25

cities. As a result of the focus on the Speed, Simplicity and Service growth platform, SBI

Cards today offers the largest distribution and widest cash advance network for India’s

middleclass customers. SBI Cardholders can access cash for emergency purposes from over

158 SBI branches across 68 locations in India.

While issuing the cards may seem to be easy, the challenge for the banks lies in being able to

manage their portfolios by keeping the delinquency levels at the lowest. Huge investments in

systems and infrastructure are, therefore, a necessity. The increase is being attributed to new

ideas such as round-the-clock functioning of card issuing banks and pulling out all stops even

at a loss, to grab a sizeable share of the expanding pie. Not to be left behind in this race, even

the big brother, the State Bank of India in association with GE Capital entered the card

business .The spurt in the card business has gathered momentum during thepast couple of

years.

4.Features of Credit Card

Do you know anyone who doesn't have a mailbox overflowing with credit card offers? Open

any of them up and you'll find in large print just what makes this card perfect for you. At first

glance, this all looks good on paper, but it's the small print that you don't pay attention to

that will come back and bite you in the end. All credit cards offer a variety of features.

Knowing and understanding these features will help you to decide which card is right for you.

Fees

Most credit cards charge fees for various things, and it is important to know what these fees

are and how to avoid them.

The annual fee

Some credit card companies charge you an annual fee just for using their card. Because of

stiff competition, you can often negotiate this fee away if you call and speak to a customer

service representative.

Cash Advance Fee

Most credit card companies will charge you a fee for cash advances. These fees can vary but

are usually somewhat hefty. Not only will they charge you a one-time fee, but the interest rate

for this money will be at a considerably higher rate. Plus, unlike a regular purchase, where

interest begins accruing after some grace period passes, cash advances accrue interest charges

from day one.

Many card companies are competing for your business and are now offering an introductory

cash advance and balance transfer rates for a specific amount of time. This lower rate can be

applied to any balances you may wish to transfer from another card. Although it sounds good,

some companies will charge you a fee for the transfer. Know what the fee is before you

transfer any balances.

Miscellaneous Fees

Things like late-payment fees, over-the-credit-limit fees, set-up fees, and return-item fees are

all quite common these days and can represent a serious amount of money out of your pocket

if you get whacked for any of these fees.

Incentives

Since there are so many credit card companies, competition is stiff. Adding incentives to their

offers is one of the more popular ways to tip the scales in their favor. Incentives like rebates

on purchases, frequent flyer miles on certain airlines, and extended warranties on purchases

are just a few of the bonuses that card companies will now offer.

For those of you who collect and use your frequent flyer miles, they also have added

incentives like travel insurance and car rental insurance for your convenience. Of course, they

are hoping that with all this traveling, you are using their card to foot at least some of the bill.

Rewards

Many card companies are looking to keep your business and are therefore making it worth

your while to use their card. Just simply by using their card you can accumulate points that

will in turn earn you rewards. What kind of reward depends solely on the amount of points

you accumulate. Since you can't accumulate these points without charging things on your

card, this is a classic case of 'you have to spend money to save money.

5.About Credit Card

What is Credit Card?

The plastic credit card with a magnetic strip many people carry in their wallets or

purses is the end result of a complex banking process. Holders of a valid card have

the authorization to purchase goods and services up to a predetermined amount,

called a A credit card is a safe and convenient way to pay for purchases or get a cash

advance.

Some credit cards let you earn points for your purchases which you can redeem for a variety

of rewards and flights. We offer a range of reward credit cards. The vendor receives essential

information from the cardholder, the bank issuing the card actually reimburses the vendor,

and eventually the cardholder repays the bank through regular monthly payments. If the entire

balance is not paid in full, the issuer can legally charge interest fees on the unpaid portion.

Individual banking institutions have their own policies when it comes to credit card

applications. Customers may seek either a secured or unsecured card, depending on their

individual repayment histories.

An unsecured credit card, on the other hand, is generally issued to those who have a good

credit history and have demonstrated an ability to repay the accrued debt on time. Creditlimits

are determined on an individual basis, and may be raised or lowered based on performance.

An unsecured card is essentially a pre-approved loan, with interest rates higher than a

similar personal bank loan.

The main benefit of any credit card is instant access to more cash than a person may have on

hand. A recent college graduate, for example, may have to purchase a business suit for

employment purposes. Earning the $200+ USD needed for an average suit could take weeks,

and he or she needs the suit in order to earn the income. Putting the suit on a credit card would

be the ideal solution; the borrower could repay the balance with his or her first pay check and

few interest charges would accrue.

Credit cards often become problematic when the holder accrues more debt than a regular

monthly payment can cover. The issuing bank does allow users to carry over balances every

month, which is also called revolving credit, but significant interest rates may also accrue on

those balances. Missing a scheduled payment can also prompt the bank to raise interest rates

on a delinquent account. If a cardholder can only afford to pay the minimal amount due every

month, he or she will not be reducing the actual debt incurred. The minimal payments may

only apply to the accrued interest. This is a financial spiral many cardholders may experience

if they don't use proper spending restraint.

A credit card does give the holder an immediate credibility for services such as hotel

reservations, car rentals and airline ticket reservations. Those without credit cards often have

to guarantee their reservations with cash deposits or several forms of identification. Many

credit card plans also include insurance coverage for theft or fraud. If a card is reported stolen

and then used illegally, the cardholder would not be held responsible for unauthorized

charges. A cardholder can authorize other people to use the card for purchases or services,

however. Ultimately, the primary cardholder is responsible for all charges placed on his or her

account.

Having a credit card is not a requirement for successful living, but even those who only pay

for goods or services with available cash often find it to be a convenient form of identification

and instant credibility. In order to avoid excessive debt, the holder must decide if the goods or

services are worth the added expenses.

6. How Credit Cards Work

A credit card is a safer and more convenient alternative to cash. However, the simple act of

paying for products and services with a credit card is supported by an elaborate behind-the-

scenes system.

When you apply for a credit card, your application is carefully screened by the bank you

apply to. A credit limit is worked out for you, based on your financial capability, educational

qualifications, age etc. The bank that issues you the credit card is called the issuing bank.

At the heart of the credit card business is a mutually beneficial arrangement between the

issuing bank and a host of businesses called merchant establishments through international

networks such as Visa and MasterCard. Merchant establishments could be hotels, shops,

travel agents or any place where transactions are made. Banks that enroll merchant

establishments are called acquiring banks.

Your credit card is valid in any merchant establishment that accepts your network

(MasterCard, Visa, et al) even if it has been enrolled by an issuing bank other than yours.

Most Indian card issuing banks are part of either the MasterCard or Visa network, or both.

There are other credit card networks like American Express and Diners Club too.

This network is at the heart of any credit card activity. When you use a card at an

establishment to purchase a product or service, your card is swiped on a swipe-machine. The

swipe machine is connected to a central computer belonging to the network, which in turn is

connected to all issuing banks. The system verifies with your issuing bank whether you have

sufficient credit to cover the purchase in a few seconds and approves or rejects the

transaction. As soon as the approval comes through, you are asked to sign the charge slip. The

merchant then verifies your signature with the one at the back of the card.

The charge slip is then forwarded to the acquiring bank, which then settles the transaction

with the merchant. The issuing bank also proceeds to bill you for payment as per the

cardholder agreement. The acquiring bank will settle the transaction with your issuing bank

through the network.

From the merchant establishment's point of view too, the credit card is a safe and efficient

payment mode and brings more business. The merchant establishment pays a fee to the bank

that enrolled it for the service. From the bank's point of view, credit cards benefit in two

ways: Banks make money through fees from merchant establishments and the higher-than-

normal interest rate paid by card holders for the balance on their cards.

You can save on the interest cost if you are prompt in paying the balance by the due date.

Credit card users get a free period of credit before they reimburse the credit card issuing bank.

This may vary from 15 days to 40 days depending on the issuing banks. When you use a

credit card, you have the option to pay just a part of the total amount spent and carry forward

the balance. In such cases, you will have to pay interest on all your purchases without any free

credit period.

Today, credit cards have found widespread usage due to the conveniences they offer. Unlike

the olden days, you do not have to carry large sums of money when you go shopping.

All you need to do is take your card with you while shopping, select whatever you want to

buy, hand over your card to the cashier to make the payment and walk out with your

purchase. So simple, isn't it?

Besides, the card issuing banks offer many types of benefits like cash backs, reward points,

interest free credit and discount offers on purchases made at select stores.

All this makes it attractive to use a credit card in lieu of cash for your purchases. If you are

wondering, "What happens after I hand over my card to the cashier?"

When you hand over your card to the cashier to pay for your purchases he takes it and swipes

it in the merchant's point of sale (POS) system.

This system is connected to the merchant's bank via a communication link. This POS system

helps in verifying your data by using an electronic verification system.

The details verified include the validity of your card and the availability of sufficient balance

on your card to pay for the purchases. This data is available on the magnetic strip, present at

the back of the card.

Once your details are transmitted to the merchant's bank, they are sent to your bank which

then authorises the payment if all the details are in order. This authorisation is then sent to the

merchant's bank, which then blocks the amount from your credit limit so as to reimburse it to

the merchant later on.

The authorisation generates an approval code and is transmitted to the merchant. This code

has to be keyed in by the cashier, after which two copies of charge slip is generated. This

charge slip is your agreement to pay your issuing bank the amount of purchase. You then sign

one copy of the charge slip and take the other one with you, along with your purchase.

Just like you, there are many others who use credit cards for their purchases. They also

generate their own charge slips. All these charge slips are stored in batches and submitted by

the merchant to his bank, at the end of the working day.

But remember the nature of relationship of the merchant with his bank is far different from

your relation with your bank. It is more of a contract, called as merchant account and is

actually a line of credit than a regular account.

As per this contract, the bank agrees to undertake collection of payments on behalf of the

merchant from his customers' banks. These payments are credited to the merchant's bank

accounts after deducting the fees for all the services involved.

When the merchant deposits these batches in his bank, they are sent by the merchant's bank

for clearing and settlement through the credit card association. This association charges your

purchase amount to your bank and pays the amount to the merchant's bank. The merchant's

bank then reimburses this amount to the merchant.

Your bank now charges your purchase amount to your credit card account. On the specific

date, your bank will generate an account statement, listing all the credit and debit transactions

in your account. If the debits are higher than credits, you have to pay the difference to your

bank.

You will also be given a due date, which is the last date by which you have to repay your

bank. The failure to pay off this amount by due date will mean paying late fees as well as

interest charges to the bank. These fees and charges can be very high, so be very careful.

Credit card is a powerful credit tool to help you tide over short term financial requirements.

However, they must be used judiciously, as any misuse of the card can attract stiff charges

and make you fall into the debt trap, besides destroying your credit rating.

So the watch word is, 'BE CAREFUL' while using the credit card.

7. Why we need a Credit Card?

A credit card is a safe and convenient way to pay for purchases or get a cash advance.

Access to credit

A credit card can give you access to funds to pay for things that are outside of your immediate

budget. It is important to realise that credit through a credit card is a loan and needs to be paid

back.

Useful when travelling overseas

Credit cards are commonly accepted around the world so they are a convenient way to pay for

purchases when travelling overseas.

Helps avoid everyday transaction fees

If you are charged fees for each transaction on your everyday transaction account, you can use

your credit card for purchases instead. Then you can pay off the entire outstanding balance

shown on your statement with a single transaction to reduce the transaction fees.

Earn rewards for everyday spending

Some credit cards let you earn points for your purchases which you can redeem for a variety

of rewards and flights.

Types of Credit Cards

Credit cards have come to the rescue of people with hot pockets. They, nowadays, put their

trust in the innovation of credit cards where they need not carry large sums of money with

them; instead simply carry a credit card which is linked up with their bank account enabling

them to make payments without batting an eye.

It is a trend, now, to make payments at a hotel, restaurant or a departmental store/ mall using a

credit card. Because of the fear of one's bank account details being swiped and stolen, more

and more credit cards are made secure so that even if a credit card is stolen, the money in

one's bank account stays safe.

Credit cards now are of various types with different fees, interest rates and rewarding

programs. When applying for a credit card, it is important to learn of their diverse types to

know the one best suited to their lifestyle and financial status. Different types of credit cards

available by banks and other companies/organizations are briefly described below.

Standard Credit Card: This is the most commonly used. One is allowed to use money up to a

certain limit. The account holder has to top up the amount once the level of the balance goes

down. An outstanding balance gets a penalty charge.

Premium Credit Card: This has a much higher bank account and fees. Incentives are offered

in this over and above that in a standard card. Credit card holders are offered travel incentives,

reward points, cask back and other rewards on the use of this card. This is also called the

Reward Credit Card. Some examples are: airlines frequent flier credit card, cash back credit

card, automobile manufacturers' rewards credit card. Platinum and Gold, MasterCard and

Visa card fall into this category.

Secured Credit Card: People without credit history or with tarnished credit can avail this card.

A security deposit is required amounting to the same as the credit limit. Revolving balance is

required according to the 'buying and selling' done.

Limited Purpose Credit Card: There is limitation to its use and is to be used only for particular

applications. This is used for establishing small credits such as gas credits and credit at

departmental stores. Minimal charges are levied.

Charge Credit Card: This requires the card holder to make full payment of the balance every

month and therefore there is no limit to credit. Because of the spending flexibility, the card

holder is expected to have a higher income level and high credit score. Penalty is incurred if

full payment of the balance is not done in time.

Specialty Credit Card: is used for business purposes enabling businessmen to keep their

businesses transactions separately in a convenient way. Charge cards and standard cards are

available for this. Also, students enrolled in an accredited 4-year college/university course can

avail this benefit.

Prepaid Credit Card: Here, money is loaded by the card holder on to the card. It is like a debit

card except that it is not tied up with a bank account. There are 40 gold credit cards available

in India:

ABN AMRO Smart Gold Credit Card

American Express Gold Charge Card

American Express Gold Credit Card

American Express HPCL Credit Card

Axis Bank Gold Credit Card

Axis Bank Gold Plus Credit Card

Axis Bank Secured Credit Card

Barclays Bank Gold Credit Card

BOBACRD Gold MasterCard Credit Card

BOBACRD Gold Visa Credit Card

Cancard Visa International Gold Credit Card

Citibank Cash Bank Credit Card

Citibank Gold Credit Card

Deutsche Bank Landmark Gold Credit Card

Deutsche Bank Smart Gold Credit Card

HDFC Bank Gold Business Credit Card

HDFC Bank Gold Credit Card

HDFC Womans Gold Credit Card

HSBC Gold Credit Card

ICICI Bank Airtel Gold Credit Card

ICICI Bank Big Bazaar Gold Credit Card

ICICI Bank Gold American Express A Credit Card

ICICI Bank HPCL Gold Credit Card

ICICI Bank Orchid An Ecotel Credit Card

ICICI Bank Solid Gold (MasterCard) Credit Card

ICICI Bank Solid Gold (Visa) Credit Card

ICICI Bank Toyota Credit Card

ICICI Bank Travel Smart Credit Card

IndianOil Citibank Gold Credit Card

Jet Airways Citibank Gold Credit Card

Jet Airways CitiBusiness Credit Card

Kotak Mahindra Fortune Gold Credit Card

Kotak Mahindra Trump Gold Credit Card

NEXTGEN BOBCARD Gold Credit Card

Reliance Gold Credit Card

SBI Gold and More Credit Card

SBI UBI (United Bank of India) Gold Credit Card

Standard Chartered Gold Credit Card

8. Ways To Avoid Credit Card Fraud

1. Report fraud as soon as you suspect it -

Any case of fraud must be dealt with immediately. You need to call your card provider or

bank and file an immediate report using a 24-hour number that you have been given. Your

card will be cancelled immediately and then the company will help you deal with any further

matters.

2. Shop safely -

When you are out and about shopping there are ways to avoid credit card fraud that you may

not have thought of. When the sales assistant gives you back your card take a look at it first to

make sure that it is yours before putting it in your pocket or wallet. Also, you should always

make sure that nobody sees your pin number whenever you use your card. Try to shield it

with your hands. These thieves can be very tricky and use cameras or assistants to watch what

number you are keying in for your pin.

3. Check Statements -

It's surprising how many people don't check their monthly credit card statements. Yet keeping

an eye on the amounts charged to your account can be a quick way to determine whether your

card is being used by a fraudster or not.

4. Eyes On Your Card -

Never allow your credit card out of your sight at any time. It might be trendy to slip your

credit card into the bill-folder at a restaurant to be charged back at the counter, but this could

be an excellent opportunity for a fraudster to take advantage of you. This also goes for

anywhere you can't see your credit card being processed in front of you.

5. Don't Be Fooled by Email Phishing -

Phishing' is the term used to describe a fraudulent email requesting that you click on a link.

You’ve then encouraged to enter your personal details into a website. Your credit card issuer

will never ask you to verify your details or to click on a link to re-enter your details. Millions

of people every year get scammed this way.

6. Keep your information private -

Your bank or credit card issuers should never call or e-mail you for your account information.

If you receive such a call or e-mail, call your bank immediately and let them know about it.

7. Secure Online Shopping Sites –

Even though most people fear shopping online, it can actually be a little safer than shopping

in person but only if you check that you're using a secure website. A secure site used

encryption to keep your information safe.

8. Safe Statement Disposal -

Buy a cheap shredder from a discount department store and be sure to shred your old credit

card statements and bank statements. There really are people willing to go through garbage to

find personal financial details like this.

9. Notify Your Credit Card Issuer -

Always notify your credit card issuer immediately of a change of address. Be sure your

statements and correspondence are being sent to the correct address as quickly as possible.

10. No Sharing -

It's never a good idea to share your credit card information with anyone for any reason. There

are plenty of people every year who are scammed by family members or friends using their

credit card details fraudulently. Even if your intentions are good, make sure you enter your

own details and take responsibility for your own card

9. Factors before applying for a Credit Card

6 factors to look at before you apply for Credit Card In India

Let’s see those 6 parameters which you should look at before you apply for a credit card in

India. At the end of this article, we will see the detailed results of the credit card survey and

find out how different credit cards performed on each parameters, so that if some particular

parameter is more important for you, you can just pick a card based on that parameter.

1. Interest rate charged on credit cards

The first parameter to look at while choosing a credit card can be the interest rate charged by

the credit card company. It can range from 1.99% on cheapest credit card to as high as 3.5%

per month on the most expensive credit card. For most of the people who pay their bills on

time, this parameter will not matter much, but you never know when you might get into a debt

trap kind of situation where you start using your credit card to the maximum limit and pay the

interest per month, at that point of time this factor will really matter. Note that interest rate

charged is mentioned on per month basis, but a small difference of 1% can be very big,

considering it on yearly basis.

For example a 1.99% monthly interest rate actually means 27% Yearly and 3.5% monthly

means 51% yearly CAGR.

51% yearly CAGR means your Rs.1 lac of credit card debt can actually increase to 7.9 lacs in

just 5 years if you don’t do something about it and obviously you will run around to improve

your cibil score later .

2. Annual Fees & Other charges

A lot of credit cards charge a yearly fees and renewal fees (at the time of renewal). Now a lot

of people hold a Free credit card for lifetime, but that’s just bunch of people who were given

the credit card on a telemarketing call, mostly because they are working in some big company

and chances are higher that their usage of credit card will be much higher than an average

customer, hence the free credit card.

But, lot of people apply for the credit card themselves and for them, there are yearly charges

(annual fees) and other kind of charges which is applicable to everyone. For example , the

penalty charges if you don’t pay your dues no due date. There are tons of customers who do

not pay their dues on last time and just pay the minimum payment. If this happens a lot of

with you , then there is a great chance that you also live with the myth of minimum payments

on credit cards. So apart from annual charges, there can be charges like

Charges when you pay your credit card bill by cash in any bank branch

If you make a demand draft from your credit card

If you request for a duplicate statement

And many other credit card charges .The list is not a small one

Note that if your credit card is FREE as of now, it might carry annual charges when it expires

and you apply for renewal – and credit card company says – “Sir , we gave it 100% free only

till the card is valid, now its renewed ! “

3. Rewards and Offers on Credit Card

There are a lot of advantages of using a credit card in form of benefits and reward points. For

example – You get PAYBACK points which you can use to redeem at various places like

www.bookmyshow.com, and book movie tickets by redeeming those points. You also get

cash back benefits if you use the card at selected HPCL petrol pumps and you don’t pay the

fuel surcharge too .

There are many other kind of benefits which many credit cards in India offer and those can be

different from one credit card to another. This is one very important factor before you

choose a credit card because a big number of people just take credit card for these benefits

and even if you are not looking for these, you might want it in future at some point of time.

4. Customer Service and Transparency

Once I called my credit card company (which is ICICI Credit card) because I wanted to know,

if there will be any annual charges on my credit card as the expiry date is over and I wanted to

renew the credit card. They gave me a very clear and satisfactory step by step answer which

made me feel – “Great” .

There was no renewal charges and no annual charges even after renewal. So I was happy.

Now it was not the FREE thing here which made me happy alone, It was the way customer

care talked to me and treated me like a human.

While there are instances when I was not that happy, but overall on an average I would still

rate the customer service of my ICICI credit card as “good”. Well, that’s my experience only

and others can have bad or worse experience with credit card company. Before you apply for

a credit card, you need to look at this very critical aspect of customer service and how

transparent are they overall.

5. Convenience to pay the bills

Something which you will deal each month is the payment of your credit card bill. Now

almost all the credit card companies allow to pay by net-banking, cheque, cash and other

ways. But still some banks can be really torturing and not that supportive. It can be

cumbersome at times. There has been instances when people paid by cheque before time and

it was not processed on time and the person had to suffer because of that and had to run

around to get back those charges reversed.

6. How easy was it to apply for credit card

Have you gone through frustrating time applying for credit card, really had to run around to

get a credit card even when you were totally eligible to get one. While this criteria is not that

big, as its a one time event still you can consider it before you apply for one. I recently had a

hard time opening a saving account for my brother with ICICI bank because they had no way

to accommodate people living on rent with friends, however Kotak bank did it for me, at that

point of time, the “ease of opening the account” was really a big thing for me. In the same

way ease of applying for a credit card can be one important factor at times.

Best & Worst Credit Card in India as per Survey

Below are the results of the survey which we conducted on credit cards. Have a look at

it.

If you look at the above chart you will see that the best credit card in India turns out to

be Citibank Credit Card and the second best is HDFC Bank Credit card overall.

However this does not mean that other credit cards are not good in all the parameters.

ICICI Bank credit card is very close to all the other cards in several parameters.

While the SBI Bank credit card and HDFC Bank credit card top the list when it comes

to interest rates charged (means they have lower interest rates compared to others), but

HSBC Bank credit card comes last. HBSC Bank credit card has not done good in any

parameter as per the survey and has lowest ranking in all of them.

Average Credit Card bill for last 6 months

86% people are paying less than Rs 20,000 per month as there credit card bills, that’s

last 6 months average. Where as only 2% people had more than Rs 50,000 bill per

month. I suspect that these people must be using their credit card for various mandatory

expenses which is required anyways. Lots of reward points and benefits to them.

Indian credit card industry to witness robust growth

The robust growth in the Indian economy is also witnessed in the credit card industry. Higher

disposable income by relatively younger workforce in Mid 20s has made India a perfect

market for credit card companies.

Here are some statistics and projections of the Indian credit card industry.

Visa, which accounts for 70% of the total card industry is the market leader in India.

Visa expects total cards in circulation (both debit and credit) to double to 100 million by 2010

from around 45 million now.

Credit Card purchase volumes in the country are likely to triple to $21 billion by 2010.

India is currently the fastest growing Mobile Market in the world and is also among

the fastest growing credit card markets in the world.

India has a total 45 million cards under circulation (13 million credit and 32 million debit) and

a 40% year-on-year growth.

68% of payment cards in India are debit cards as against 2% in 1998

ICICI bank is India’s largest Credit Card issuer.

With the entry of Wal-Mart in India, we will see India becoming the fastest growing Retail

market in the world within the next few years.

How credit card companies are making a comeback?

After the initial boom period of 2004 to 2006, the Indian credit card industry faced one of its

toughest years in 2007-09. However, it seems like the tide is turning with the sector

witnessing a dramatic drop in credit card defaults in the last one year.

After the initial boom period of 2004 to 2006, the Indian credit card industry had its bubble

burst in 2007-09. However, it seems like the tide is turning with the sector witnessing a

dramatic drop in credit card defaults in the last one year.

According to data compiled by the Credit Information Bureau of India (Cibil), financial health

of average individual borrower has risen. The data shows that the proportion of borrowers

with a credit score of more than 800 has gone up from around 23% in 2008 to over 62% in

2011.

Credit score is a ranking drawn up by Cibil, the largest repository of borrower information in

the country, which ranges from 300 to 900, with 900 being most creditworthy.

In the last one year, the percentage of cardholders who have not met their payment obligations

for more than 90 days has dropped from 2.82% in the fourth quarter of 2010 to 1.62% in Q4

2011. The significance of 90 days is that the Reserve Bank of India requires banks to classify

loans that are not repaid in 90 days as non-performing assets.

This is a marked turnaround for a business which has been hit by defaults since the 2008

global financial crisis and many banks have got out of the personal loan space completely.

Besides a fall in defaults, cardholders are using their cards for a 30% higher value.

LOWER DEFAULTS

According to SBI Cards, the country's third largest issuer of credit cards, increased awareness

and focus on profitable growth has paid rich dividends. "Credit card issuers are relying a lot

on bureau data, which has improved dramatically. This has reduced the scope for

delinquencies significantly. The irrational exuberance that we saw in 2008-09 no longer

exists. Banks are adopting a more calibrated approach in growing their card portfolios,"

Kadambi Narahari, chief executive officer of SBI Cards told moneycontrol.com.

Also, SBI Cards is careful in enrolling new customers and selling to existing accountholders.

"We charge an annual fee ranging from Rs 499 to Rs 2,999 to our customers on all our cards.

This helps us weed out serious users from the non-serious ones," Narahari says.

The fact of the matter is people have realised the importance of keeping a good credit score,

believes Sanjeev Jain, CEO, GE Capital Business Processes Management Services -- SBI

Cards joint venture partner. "We have had customers asking us to clean their credit history of

an eight-10 year old default as they were unable to avail a home or a car loan because of it,"

Jain says.

However, having only "good" customer means company margins come under pressure, where

the real money is made on penalties.

CUSTOMIZED PRODUCTS

Besides keeping an eye on who they are dealing with, card companies have also come out

with customer-specific products. "For example, if a customer uses his or her card more for

eating out, we give them offers related to dining out. If a customer uses the card more to book

travel tickets, we offer them cards designed for frequent flyers," Narahari says.

Another hit has been the corporate cards. "Companies have found corporate cards a great way

to manage cash," Jain says adding, it also cuts down on reckless spending by its executives.

Secured cards have also started to gain traction. Basically, what they do is offer customers,

who otherwise are not eligible, credit cards based on their fixed deposits with State Bank of

India.

"We offer up to 80% of the amount of the fixed deposit to the customers. This strategy

removes any scope of delinquency in these accounts. We are also offering cards without a

security in areas that we call project towns. We are issuing these cards to corporate employees

working in small towns and cities provided the company has very good relationship with us,"

Narahari explains.

Secured cards have formed 10% of SBI cards total portfolio.

'REAL GROWTH IN TIER II & III CITIES'

Credit cards are meant for the urban population. That was the popular belief among most

industry watchers and market analyst. However, that is not the case now. Products such as

secured cards and aggregation of demand have led to a spike in card holders in tier II & tier

III cities. Also, the thriving retail scene has also helped the demand in such cities.

"The ability to source clients, service them and recover the money holds back most issuers

from offering credit cards in deeper geographies. We have expanded our portfolio in tier II

and III centres in the past 12-18 months. In many of these locations we are offering credit

cards against security. So, if you have a fixed deposit with SBI we will offer you a credit

card," Narahari says.

In fact, the SBI Card chief expects growth in these small towns to outpace thier urban

counterparts. "We are also targeting people who have just joined work. We call them the

emerging segment. These are people who have the potential to become good customers in

future. Hence, we want to partner them in their early life," he says.

SBI Cards, which has a base of 2.2 million cards, hopes to add 1 million new card holders by

2014-15. It is also launching a new high end signature card for HNI customers shortly.

10. TRIGGERS

A big trigger for SBI Cards has been the use of the short messaging service or SMS. "Every

time our customer makes use of our card, he immediately gets an SMS on the transaction no

matter how small it is. This gives a sense of security to the user and helps him track of his

account. Mobile commerce has been a big growth driver for us," Narahari says.

Security mechanism on the cards has also been upgraded so as to prevent unauthorized

transactions. The Reserve Bank of India has mandated card companies to migrate to the high

security EMV platform by 2014. This is likely to drastically bring down credit card frauds.

The recent White Paper on black money tabled in the Parliament by the finance minister

suggested tax incentives for encouraging use of debit and credit cards as these leave audit

trails.

Credit Card Market Heading for Magnificent Growth in India

According to our new research report, “Indian Payment Card Market Forecast to 2012”, the

number of payment cards, categorized as credit and debit cards, is increasing rapidly in India.

Phenomenal growth in the number of credit and debit cards in India, over the past few years is

an evidence of the aforementioned statement. Apart from increasing consumerism,

intensifying competition among card issuers and an expanding financial infrastructure will

drive the future growth of the concerned market. The research found that segments, especially

credit card market have been showing tremendous growth performance and emerged as a

potential investment area for players.

With increasing number of credit card holders and rising consumer confidence regarding

credit card purchase, the transaction value of credit cards in India is forecasted to increase at a

CAGR of around 8% during FY 2011-2013. This growth will be largely attributed to the

improving credit card payment infrastructure in the country, with most of the merchants

accepting credit card payments at POS terminals. Banks have also tightened their rules of

issuing credit cards on account of increasing fraud cases, which have also helped in improving

the credit card infrastructure in the country.

However, we observed that the Indian banks dominate the retail banking market, but the

scenario is completely different in the credit card market, where foreign banks have managed

to capture a sizeable market share. This is mainly due to the fact that while the Reserve Bank

of India has imposed several restrictions on the foreign banks, there are no such restrictions

on credit card companies. HDFC, Citibank, and Standard Chartered are some of the foreign

banks having significant Indian portfolios.

“Indian Payment Card Market Forecast to 2012”, provides an extensive research and rational

analysis along with reliable statistics of the Indian payment card market. The report has

thoroughly examined current market trends, industrial developments, and competitive

landscape to enable clients understanding of the market structure and its progress in the

coming years. Besides, the report also provides a brief overview of the key market players.

Our forecast presented in the report has been carried out considering the possible post-

recession impact on the industry. Further, our report has been prepared with proper insight

into the current and future outlook of credit card market in India to provide enhanced

knowledge about the market to our clients.

Credit card firms turn cautious, growth to be hit

Growth in credit card industry in terms of acquisition of new customers is likely to be weak in

the current financial year as most banks and card issuers are no longer looking at expanding

their customer base in a reckless manner. Today, there are about 18 million credit card

holders, down by a few thousands from what it was in 2009-10.

Kadambi Narahari, CEO, SBI Cards and Payment Services Pvt Ltd — joint venture between

US conglomerate General Electric and the country’s largest lender, State Bank of India —

told HT that banks want to be careful while issuing new cards and leverage CIBIL’s (Credit

Information Bureau of India) distribution network to ensure that the customer has a clean

track record in terms of financial discipline.

“The expansion in credit card industry has been moderate but banks and credit card issuers are

now more focused on increasing the spending on the card,” Narahari said.

Narahari said that the default rate, which had breached the double digit figure has now come

down to a manageable level. “While banks have stopped recklessly issuing cards, customers

have also become aware and they do not want to be blacklisted by CIBIL. Therefore, several

hundred card holders have shown an urge to clear dues, which has brought down the default

rate in the industry,’ he said.

HDFC Bank, ICICI Bank, SBI Cards and Citibank are among the top card issuers with a

combined market share of about 70% in the credit card industry.

11. Research Methodology

Kind of Population : People having Credit Cards

Area : Shivaji Park , Mahim and Fort

Sample Size : 50

Sampling : Convenience Sampling

Source of Date : Questionnaire

Statistical Tool : Pie Charts

12. Data Interpretation

43%

57%

Gender

MalesFemalesFemales

Males

On conducting a survey it was found that 57% Females and 43% males used credit cards.

Business21%

Service35%

Professional28%

Other16%

Occupation

On conducting a survey it was found that 35% people in the service industry use credit cards

in comparison to 28% professional , 21% business and 16% other occupations.

23%

39%

22%

16%

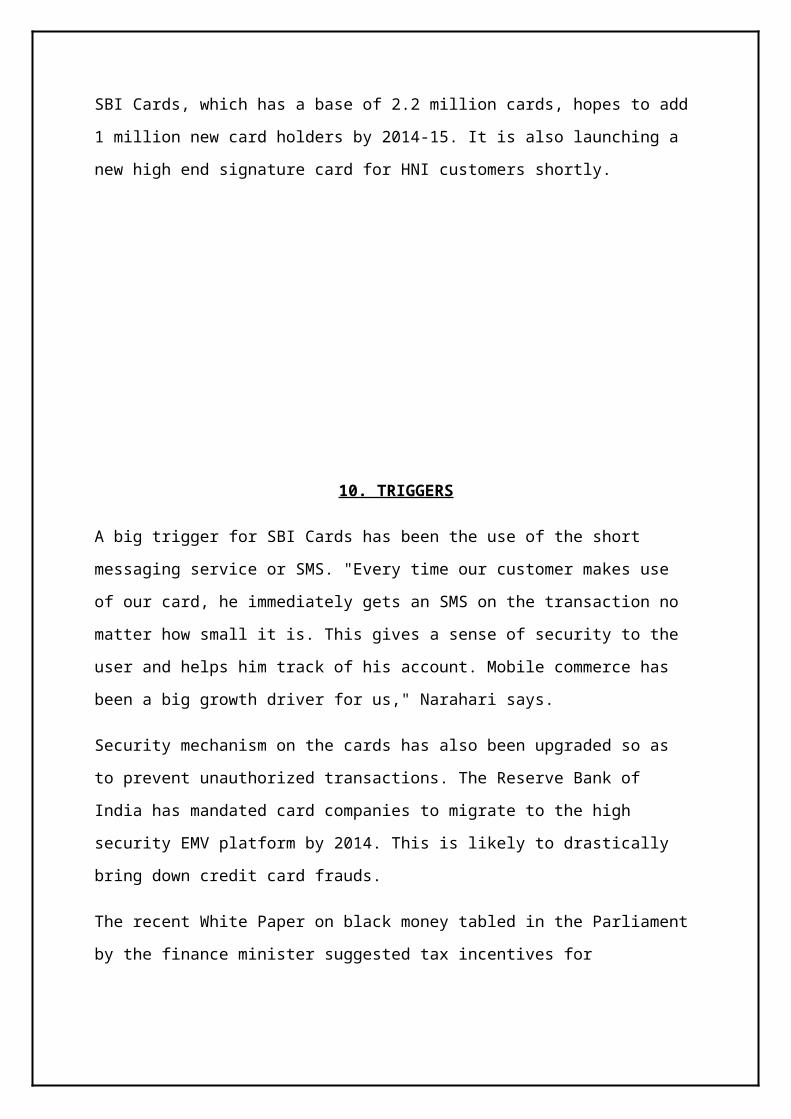

Age Group of people using Credit Cards

15 to 25 years25 to 40 years40 to 60 yearsAbove 60

25 to 40 years

40 to 60 years

15 to 25 yearsAbove 60

On conducting a survey it was found that the credit card is used mainly by the people in the

age group of 25-40 years i.e.39%, 23% in 15-25 years,22% in 40-60 years and 16% by above

60 years.

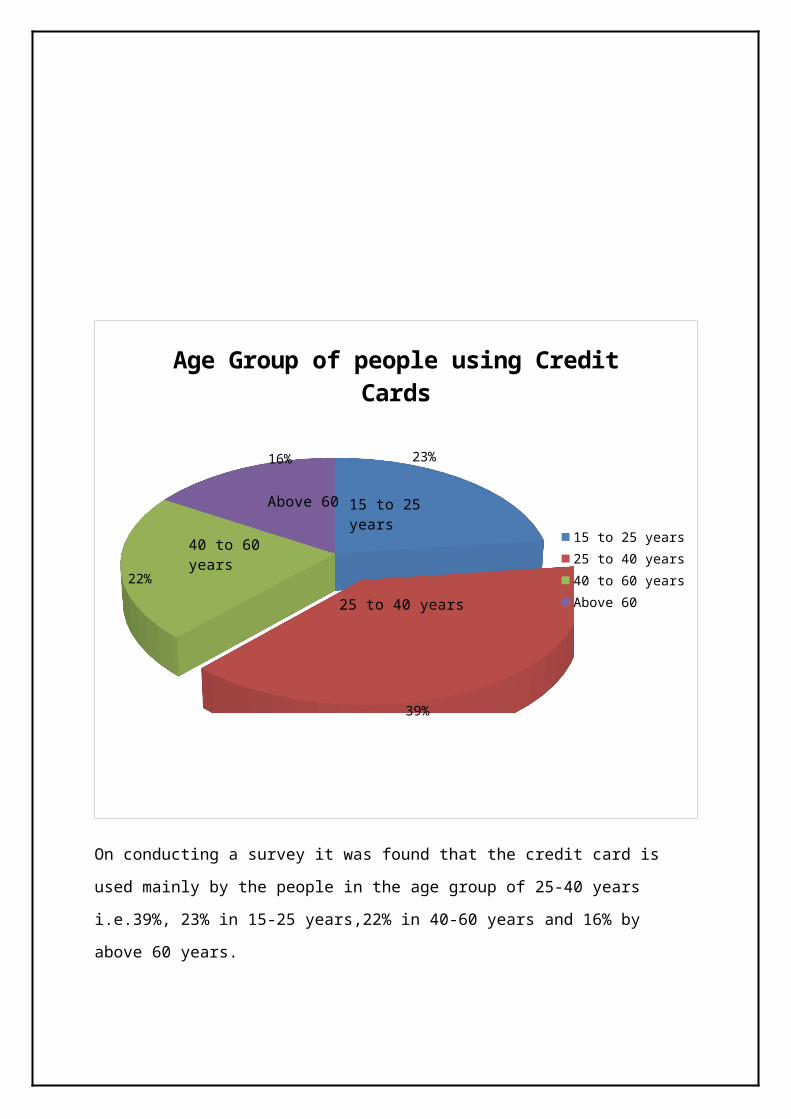

<1,00,00012%

1,00,000 to 5,00,00028%

5,00,000 to 10,00,00037%

>10,00,00023%

Annual Income

On conducting a research,it was found that credit cards are pre dominantly used by people

with having an annual income of 5,00,000-10,00,000 i.e. 37%.

30%

25%

28%

17%

Standard CharteredHSBC Bank HDFC BankAXIS Bank

AXIS Bank

Standard Chartered

HSBC Bank

HDFC Bank

Most Used Credit Card Company

After surveying the audience it was found that most people use Standard Chartered Bank i.e.

30%.

21%

34%

29%

16%

Best Credit Card services

Standard CharteredHSBC BankHDFC BankAXIS Bank

Standard Chartered

AXIS Bank

HDFC Bank

HSBC Bank

On conducting a survey it was found that the best credit card services are provided by HSBC

bank as voted by 34% people.

38%

25%

30%

8%

Usage of Credit Cards

E-ticketingOnline shoppingBill PaymentsOther

Other

E-ticketing

Online Shopping

Bill Pay-ments

On conducting a survey it was found that most people used their credit cards for E-Ticketing

i.e. 38% followed by 30% who use it to pay bills,25% use it for online shopping.

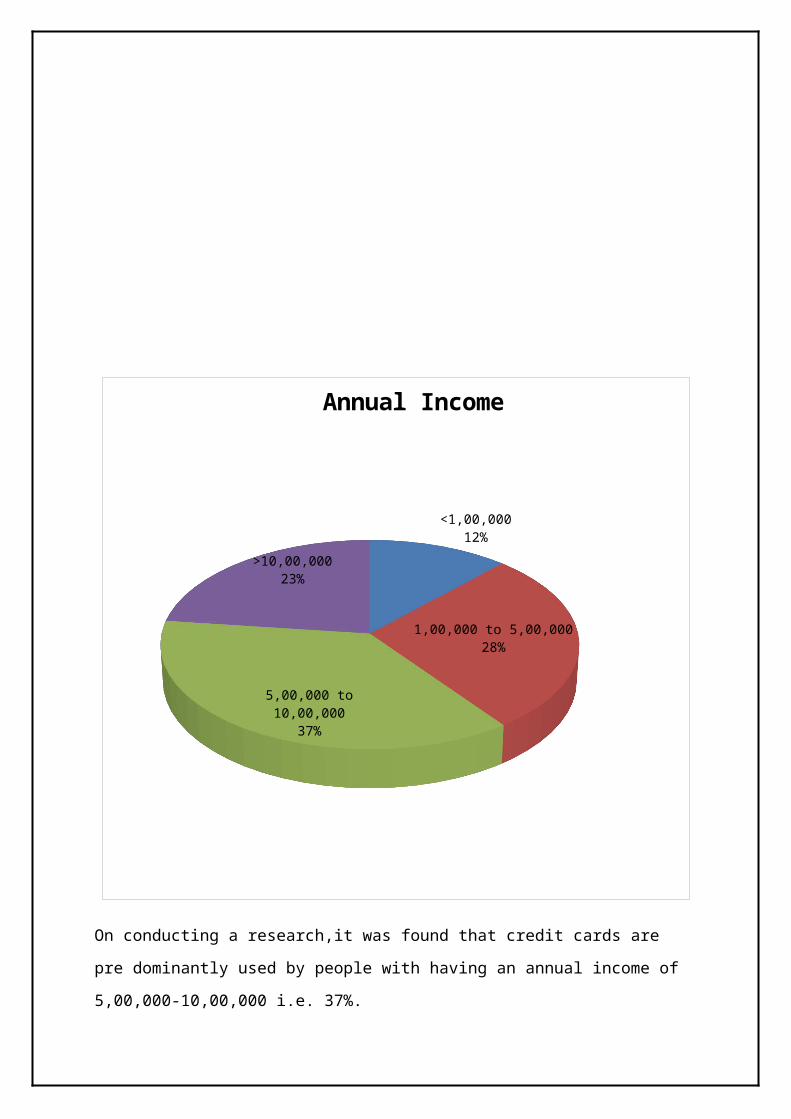

Cash Transaction70%

Credit Transaction30%

Type of Transaction

On conducting a research it was found that 70% people still prefer cash transactions over

credit card transactions.

Standard Chartered Bank

13.1 History

Standard Chartered Bank was formed in 1969 through the merger

of two separate banks, the Standard Bank of British South Africa

and the Chartered Bank of India, Australia and China.

These banks had capitalised on the expansion of trade between Europe, Asia and Africa.

The Chartered Bank

The Chartered Bank was founded by James Wilson following the grant of a Royal Charter by

Queen Victoria in 1853.

The bank opened in Mumbai (Bombay), Kolkata and Shanghai in 1858, followed by Hong

Kong and Singapore in 1859.

The traditional trade was in cotton from Mumbai, indigo and tea from Kolkata, rice from

Burma, sugar from Java, tobacco from Sumatra, hemp from Manila and silk from Yokohama.

The bank played a major role in the development of trade with the East following the opening

of the Suez Canal in 1869 and the extension of the telegraph to China in 1871.

In 1957 Chartered Bank bought the Eastern Bank, together with the Ionian Bank's Cyprus

Branches and established a presence in the Gulf.

The Standard Bank

The Standard Bank was founded in the Cape Province of South Africa in 1862 by John

Paterson, and started business in Port Elizabeth in the following year.

The bank was prominent in financing the development of the diamond fields of Kimberley

from 1867. It later extended its network further north to the new town of Johannesburg when

gold was discovered there in 1885.

The bank expanded in Southern, Central and Eastern Africa and had 600 offices by 1953.

In 1965, it merged with the Bank of West Africa, expanding its operations into Cameroon,

Gambia, Ghana, Nigeria and Sierra Leone.

In 1987 Standard Chartered Bank sold its stake in the Standard Bank, which now operates as

a separate entity

THEY’RE listed on the London, Hong Kong and Mumbai stock exchanges, and rank among

the top 20 companies in the FTSE-100 by market capitalisation.

13.2 Types of Banking

Consumer Banking

We offer a wide range of innovative products and services to meet Their customers needs.

Wholesale Banking

We bring Their corporate clients local expertise with global insights into today's fastest

growing markets.

SME Banking

We provide tailored solutions to help customers set up and grow their small and medium

enterprises.

Islamic Banking

We have a wide range of Shariah-compliant financial products based on Islamic values.

The Private Bank

We offer a full range of customised wealth management services for high net worth clients.

Online Banking

Get access and manage your finances anytime, anywhere, with your online and mobile

banking.

13.3 Their growth

Since 2000, we’ve made a number of alliances and acquisitions.

These have made it possible to broaden Their locations and

products in key regions and countries.

2012

Turkey - acquisition of Credit Agricole Yatirim Bankasi Turk A.S., a provider of corporate

and investment banking services

2011

Singapore – acquisition of GE Money’s Singaporean auto and personal loans provider

Canada and Australia – acquisition of Gryphon Partners, a mining and metals corporate

advisory firm

2010

Africa - acquisition of Barclays African custody business

China – we became an investor in Agricultural Bank of China, one of the top commercial

banks in China

India – we launched Their first ever Indian Depository, allowing investors in India to

participate in Their growth

2009

Africa – acquisition of First Africa Holdings Limited

Asia – acquisition of Casenove Asia

India – we increased Their investment in UTI Securities to 74.9%

2008

Taiwan – acquisition of the 'good bank' portion of Asia Trust and Investment Corporation

Brazil – acquisition of Lehman Brothers team in Brazil

Vietnam – we announced raising Their strategic stake in Vietnam's Asia Commercial Bank to

15%

South Korea – acquisition of South Korea's Yeahreum Mutual Savings Bank

Global – we completed the acquisition of American Express Bank, a wholly-owned

subsidiary of American Express Company, with operations in 47 countries

South Korea – Standard Chartered First Bank Korea Ltd acquires an 80% stake in South

Korea's A Brain, a funds administration company

India – acquisition of a 49% strategic stake in India's UTI Securities, a leading local broking

firm.

2007

Global – we completed the acquisition of Harrison Lovegrove, a leading global oil and gas

M&A advisory boutique

Global – we acquired Pembroke, an aircraft leasing, financing and management firm.

2006

Taiwan – acquisition of Hsinchu International Bank (USD1.2bn)

Pakistan – acquisition of 95.37% of Union Bank (USD487m)

Indonesia – acquisition of a 26% stake in PermataBank by the consortium of Standard

Chartered Bank & PT Astra International Tbk (USD193m). Total stake held in PermataBank

by consortium today is 89%.

Africa – acquisition of 25% in First Africa Group Holdings Ltd.

2005

Acquisition of a 20% stake in Fleming Family & Partners (USD78m)

China – acquisition of 19.99% of China Bohai Bank (USD123m)

Bangladesh – acquisition of Amex Bank's Bangladesh business (USD25m)

Vietnam – acquisition of 8.56% stake in Asia Commercial Bank (USD22m)

Global – acquisition of a minority stake (6%) in Travelex as part of Apax-led consortium

South Korea – acquisition of Korea First Bank (USD3.3bn).

2004

Global – acquisition of ANZ's Project Finance business with assets

Indonesia – acquisition of 63% stake in PermataBank by the consortium of Standard

Chartered Bank & PT Astra International Tbk (USD355m)

Hong Kong – acquisition of PrimeCredit

2000

Hong Kong – acquisition of Chase Manhattan Card Company (USD1.32bn)

Global – acquisition of ANZ Grindlays (USD1.34bn).

13.4 Their strategy

We aspire to be the world's best international bank, leading the way in Asia, Africa and the

Middle East.

We focus on building deep and long-standing relationships with Their clients and customers

and constantly look to improve the quality of Their products and services.

Their success

In the last nine years we have reported record income and profits. Twenty-fTheir of Their

markets now deliver over US$100 million of income, fTheirteen over US$100 million in

profit.

Listed on the London, Hong Kong and Mumbai stock exchanges, we rank among the top 20

companies in the FTSE-100 by market capitalisation.

Their focus on basic banking

Their success is a result of being obsessed with the basics of banking - balancing the pursuit

of growth with a disciplined management of costs and risks and keeping a firm grip on

liquidity and capital.

Through Their international network and expertise, we facilitate trade across markets, enable

multinational clients to conduct complex business transactions and service the needs of an

increasingly international consumer base.

13.5 Their Awards

Every year we are recognised for Their achievements in banking and finance. Here are some

of the awards we have won in the past year.

Euromoney

Awards for Excellence 2011

Best Investment Bank in Africa

Best Project Finance House in Africa

Best Flow House in Africa

Best Bank in Tanzania

Best Bank in Hong Kong

Best Cash management House in Asia

Best Investment Bank in the Middle East

Best Project Finance House in the Middle East

Islamic Finance 2011

Best Project Finance House

Most Improved Islamic Bank in Asia

Global Finance

Global Finance Awards 2011

World's Best Foreign Exchange provider in Africa, Asia Pacific, Southeast Asia

Best Bank Awards 2011

Best Bank in Africa

Best Investment Bank Awards 2011

Best Debt Bank in Asia

Best Investment Bank in Singapore

Best Supply Chain Finance Providers 2011

Best Supply Chain Finance Provider in Asia

Stars of China 2011

Best Supply Chain Finance Provider (Foreign)

Best Small Business Lending (Foreign)

World's Best Derivatives Providers 2011

Best Interest Rate Derivatives Bank

World Best Internet Bank Awards 2011

Best Bill Payment and Presentment in Asia

Best Design for a Global Banking Website

Best Consumer Internet Bank - Singapore

World's Best Sub-Custodian Banks 2011

Best Sub-Custodian Bank in Asia

Best Sub-Custodian Bank in Africa

World’s Best Treasury & Cash Management Providers 2011

Best Bank for Liquidity Management in Asia

Best Bank for Liquidity Management in Africa

GTR

Leaders in Trade 2011

Best Trade Finance Bank in South Asia (including India, Pakistan and Bangladesh)

Number 2 Best Supply Chain Finance Bank

Number 2 Best Trade Finance Bank in Asia Pacific

Asia Leaders in Trade 2011

Best Commodity Finance Bank in Asia-Pacific

Best Trade Finance Bank in Singapore

Best Trade Finance Bank in Bangladesh

PFI

PFI Awards 2011

Asia Bank of the Year

AsiaRisk

Asia Risk Awards 2011

Interest Rate Derivatives House of the Year

Corporate Rankings 2011

Number 1 overall for Derivatives in Asia

Number 1 for Currency Derivatives

Number 1 for Interest Rate Derivatives

The Asset

Country Awards 2011

Best Debt Bank in China

Best Debt Bank in Singapore

Best Debt Bank in Vietnam

Best M & A House in India

Best Debt House in India

Best Bank in Pakistan

Best Debt House in Pakistan

Transaction Banking Awards 2011

Best Transaction Bank

Best Trade Finance Bank in India

Best Structured Trade Finance Bank

Best Cash Management Specialist for Payments and Receivables in Asia

Best Cash Management Bank in Southeast Asia

Best Cash Management Bank in the Middle East

Best SME Bank in Hong Kong

Triple A Awards 2011

Best SME Bank, Hong Kong

Triple A Islamic Finance Awards 2011

Best Islamic Project Finance House

The Asset Triple A Regional Awards 2011

Best Leveraged Finance House

Best Project Finance Advisory House

Best Asian Currency Bond House

Best Securitisation House

The Asian Banker

Technology Implementation Awards 2011

Best eBanking Project in Thailand

International Excellence in Retail Financial Services Awards 2011

Best Customer Relationship Management in Hong Kong

Best Payments Product (Pay Any Card)

Asian Private Banker

Asian Private Banker Awards 2011

Best Private Bank in the Middle East

The Banker

The Banker Awards 2011

Best Investment Advisory in the Middle East

Bank of the Year Awards 2011

Best Bank in Afghanistan

Best Bank in Tanzania

Best Bank in Zambia

Bank of the Year - Financial Inclusion

Middle East Industry Awards 2011

Best Investment Advisory Services / Priority Banking in the UAE

Emeafinance

Middle East Banking Awards 2011

Best Foreign Bank - Bahrain

Best Foreign Investment Bank - Bahrain

Best Foreign Bank - Jordan

Best Foreign Investment Bank - Jordan

Best Foreign Bank - Oman

Best Foreign Bank - UAE

Best Foreign Investment Bank - UAE

Treasury Services Awards 2011

Best cash management services in EMEA

Best FX services in the Middle East

Lloyd's List

Asia Awards 2011

Ship Financier Award

Lloyd’s List Awards 2011

Ship Financer Award

Trade and Forfaiting Review

Trade and Forfaiting Review Awards 2011 (Readers' Poll)

Best Trade Bank in Africa - Gold

Best Trade Bank in Asia-Pacific - Bronze

Trade & Forfaiting Review Awards 2011

Best Trade Bank in Africa

Best Trade Bank in Asia-Pacific

The Banker and Professional Wealth Management Magazine, Financial Times - Global

Private Banking Awards 2011

Best Private Bank in Asia

Best Private Bank in India

Banking and Payments Asia Trailblazer Awards 2011

Process Excellence Award in Thailand

Service Excellence Award – Best in Category (Breeze)

China Trade Finance Awards 2011

Best RMB Cross-Border Settlement Bank

CorpComms DigiAwards 2012

Best Corporate Website

Dun & Bradstreet - Polaris Software Banking Awards 2011

Best Foreign Bank in India

Best Priority Sector Lending - Foreign Bank in India

Finance Asia Country Awards for Achievement 2011

Best Foreign Commercial Bank in India

The Financial Times and Investors Chronicle Wealth Management Awards 2011

Best Global Private Bank

FX Week Best Banks Awards Survey 2011

Best Bank for FX in Asia-Pacific

Best Bank for Emerging Asian Currencies

Global Custodian Agent Banks in Major Markets Survey 2011

Leading Clients - Top Rated in Hong Kong

Leading Clients - Top Rated in Japan

Leading Clients -Top Rated in Singapore

Leading Clients -Top Rated in South Korea

Hong Kong General Chamber of Small and Medium Business 2011

Best SME’s Partner, Hong Kong

Hong Kong Service Awards 2011

Priority Banking (Financial Services) in Hong Kong

ICSA Hermes Transparency in Corporate Governance Awards

Best FTSE 100 Annual Report

IDC Financial Insights Innovation Awards 2011

Excellence in Customer Centricty in Hong Kong

Interactive Media Awards 2011

Outstanding Achievement in Banking

Jane's Transport Finance Awards 2011

Shipping Finance Innovator of the Year

Shipping Leasing Innovator of the Year

Risk.net Structured Product Asia Awards 2011

Best in China

Best in India Award for Structured Products

SCMP/IFPHK Financial Planner Awards 2011

Company for Financial Excellence- Banking in Hong Kong

Company of the year- Banking in Hong Kong

Industry Winner- Banking in Hong Kong

Treasury Management International Awards for Innovation & Excellence in Treasury

2011

Best Bank for Cash Management - Middle East & Africa

Best Bank Financial Supply Chain - Asia

Best Bank Capital Markets & Investment Banking - Asia

Web Marketing Association's Web Awards 2012

Bank Standard of Excellence, Financial Services Standard of Excellenc.

13.6 Background of Standard Chartered Credit Cards

Types of Credit Cards

Credit cards have come to the rescue of people with hot pockets. They, nowadays, put their

trust in the innovation of credit cards where they need not carry large sums of money with

them; instead simply carry a credit card which is linked up with their bank account enabling

them to make payments without batting an eye.

It is a trend, now, to make payments at a hotel, restaurant or a departmental store/ mall using a

credit card. Because of the fear of one's bank account details being swiped and stolen, more

and more credit cards are made secure so that even if a credit card is stolen, the money in

one's bank account stays safe.

Credit cards now are of various types with different fees, interest rates and rewarding

programs. When applying for a credit card, it is important to learn of their diverse types to

know the one best suited to their lifestyle and financial status. Different types of credit cards

available by banks and other companies/organizations are briefly described below.

Standard Credit Card: This is the most commonly used. One is allowed to use money up to

a certain limit. The account holder has to top up the amount once the level of the balance goes

down. An outstanding balance gets a penalty charge.

Premium Credit Card: This has a much higher bank account and fees. Incentives are offered

in this over and above that in a standard card. Credit card holders are offered travel incentives,

reward points, cask back and other rewards on the use of this card. This is also called the

Reward Credit Card. Some examples are: airlines frequent flier credit card, cash back credit

card, automobile manufacturers' rewards credit card. Platinum and Gold, MasterCard and

Visa card fall into this category.

Secured Credit Card: People without credit history or with tarnished credit can avail this

card. A security deposit is required amounting to the same as the credit limit. Revolving

balance is required according to the 'buying and selling' done.

Limited Purpose Credit Card: There is limitation to its use and is to be used only for

particular applications. This is used for establishing small credits such as gas credits and

credit at departmental stores. Minimal charges are levied.

Charge Credit Card: This requires the card holder to make full payment of the balance

every month and therefore there is no limit to credit. Because of the spending flexibility, the

card holder is expected to have a higher income level and high credit score. Penalty is

incurred if full payment of the balance is not done in time.

Specialty Credit Card: is used for business purposes enabling businessmen to keep their

businesses transactions separately in a convenient way. Charge cards and standard cards are

available for this. Also, students enrolled in an accredited 4-year college/university cTheirse

can avail this benefit.

Prepaid Credit Card: Here, money is loaded by the card holder on to the card. It is like a

debit card except that it is not tied up with a bank account.

13.7 Top Standard Chartered Bank Credit Cards

Super Value Titanium Credit Card by Standard Chartered Bank

Credit Card Type: Rewards, Fuel

5% cash-back* on all fuel pumps (HPCL,IOC, Shell, BP etc.)

5% cash-back on telecom bills (BSNL, Airtel, Aircel, Idea, Tata etc.)

5% cash-back on utilities bills (Electricity, Water etc.).

1 Reward Point per Rs.100 spent in other categories.

Apply for Standard Chartered Super Value Titanium Credit Card

Card Type Card Tier Annual Fee* Joining Fee APR

MasterCard Titanium Rs.0 Rs.0 37.2%

* 2nd year onward annual fee is Rs.750. You can get a cash back of a maximum of

Rs. 100/Transaction, Rs.500/Month or up to Rs. 6,000/Year with this card on Their

purchase on fuel, utility and telecom. Minimum transaction value of Rs. 500 to avail

cash back

Gold Rewards Credit Card by Standard Chartered Bank

Credit Card Type: Rewards

2 Reward Points per Rs.100 spent.

Plus additional benefits.

Apply for Standard Chartered Gold Rewards Credit Card

Card Type Card Tier Annual Fee* Joining Fee APR

Visa Gold Rs.0 Rs.0 37.2%

* 2nd year onward annual fee is Rs.250

Manhattan Platinum Credit Card by Standard Chartered Bank

Credit Card Type: Rewards

5%* cash-back on spend at supermarkets and department stores such as Reliance

Trends, Pantaloons, Lifestyle, Westside, Central, Shopper Stop, Mark &

Spencer, Reliance Fresh, Big Bazaar, Food Bazaar, More.

5 Reward Points per Rs.100 spent in other categories. Plus additional benefits.

Apply for Standard Chartered Manhattan Platinum Credit Card

Card Type Card Tier Annual Fee* Joining Fee APR

Visa Platinum Rs.0 Rs.0 37.2%

* 2nd year onward annual fee is Rs.999. Cashback- Max Rs. 200/transaction, Max

Rs. 500/month

Platinum Rewards Credit Card by Standard Chartered Bank

Credit Card Type: Rewards

5 Reward Points per Rs.100 spent on hotels, dining, fuel

2 Reward Points per Rs.100 spent on other categories. Plus additional benefits.

Apply for Standard Chartered Platinum Rewards Credit Card

Card Type Card Tier Annual Fee* Joining Fee APR

Visa Platinum Rs.0 Rs.0 37.2%

* 2nd year onward annual fee is Rs.750

Bajaj Finserv Platinum Credit Card by Standard Chartered Bank

Credit Card Type: Rewards

5 Reward Points per Rs.100 spent at supermarkets, department stores, grocery

and retail apparel stores.

2 Reward Points per Rs.100 spent on other categories.

1 extra Reward Point per Rs. 100 for spend above Rs. 50,000 in a statement

cycle.

10 Reward Points per Rs.100 spent on yTheir birthday

Apply for Standard Chartered Bajaj Finserv Platinum Credit Card

Card Type Card Tier Annual Fee* Joining Fee APR

MasterCard Platinum Rs.0 Rs.0 37.2%

* 2nd year onward annual fee is Rs.999

Breeze Banking Credit Card by Standard Chartered Bank