cpp / fpc study group welcome ! please sign in review of answers presentation material review test...

TRANSCRIPT

CPP / FPC Study Group

WELCOME !

Please sign in

Review of Answers

Presentation MaterialReview Test of Section 2

It’s Test Time !

10 minutes !Federal and State Wage and Hour Laws

Questions ?

THE EXAM

Any Questions ?

Concerns ?

Section 3

Overview

• Gross Income• Fringe Benefits• Employer Provided Benefits• Other Payments• Withholding and Reporting Taxes• Questions

Gross Income

• Gross Income– Included wages and benefits– Excluded benefits

• Income and Employment Taxes• Fair Market Value

– IFBA = FMV – (EPA + AEL)

Fringe Benefits

• Nontaxable Fringe Benefits– No-additional-cost-services– Qualified Employer Discounts– Working Condition Fringe– De Minimis Fringe– Qualified Transportation– On-Premises Athletic Facilities– Qualified Retirement Planning Services– Qualified Moving Expense Reimbursement

Personal Use of Employer Provided

Vehicles

• Exception to Personal Use– De Minimis– Qualified Non-personal Use– Automobile Salespersons

• Accounting for Use – Valuation Methods– General Valuation Method– Special Valuation Method– Commuting Valuation Method– Annual Lease Valuation Method– Vehicle cents-per-mile Method

Personal Use of Employer Provided

Vehicles Cont’d

• Personal Use of Employer Provided Aircraft– General Valuation Rule– Non-commercial Flight Valuation Rule

• Free or Discounted Commercial Flights• Discounts on Property or Services• Club Memberships

– Working Condition Fringe?– Club vs. Organization

Other Fringe Benefits

Employer Provided Benefits

• Life Insurance– Group-term life insurance– Whole life insurance– Split dollar life insurance– Owners

Moving Expenses• Deductibility

– Distance Test– Time Test

• Deductible (qualified, nontaxable) moving expenses– Transportation of Household Goods– Expenses of traveling from old residence

to new residence (excluding meals)

• Nondeductible (nonqualified, taxable) moving expenses– Meals while in transit– House hunting trips– Real estate expenses

• Reporting of moving expenses– Deductible– Nondeductible

Moving Expenses Cont’d

Educational Assistance• Job-Related• Non Job-Related

– $5,250 exclusion

Group Legal Services

Business Travel Expenses

• Away from home• Temporary• Daily Transportation Expenses• Accountable Plan

– Business Connection– Substantiation– Returning Excess Amounts

• Nonaccountable Plan• Frequent Flyer Miles• Substantiation vs. Per Diem

allowance• Spousal and family travel expenses

Business Travel Expenses Cont’d

Employer Provided Meals and Lodging

• Employer Provided Meals– Furnished on employer premise– For the convenience of the employer

• Employer Provided Lodging– On the employer premises– For the convenience of the employer– Required as a condition of employment

Adoption Assistance• Dollar Limitation• Income Limitation• Eligible Child• Qualified Expenses• Program Requirements• W2, Box 12, Code T

Break

10 minutes!

Other Payments• Advances and Overpayments• Awards and Prizes

– Length of Service– Safety Achievement– Civic and Charitable Awards– Prizes for Retail Salespeople

• Back Pay Awards

• Bonuses• Commissions• Conventions• Death Benefits• Dependent Care Assistance

– $5,000 exclusion limitation• Directors’ Fees• Disaster Relief Payments• Equipment Allowance

Other Payments Cont’d

• Gifts• Golden Parachute Payments• Guaranteed Wage Payments• Jury Duty Pay• Leave Sharing Plans• Loans to Employees• Military Pay• Outplacement Services• Retroactive Wage Payments• Security Provided to Employees

Other Payments Cont’d

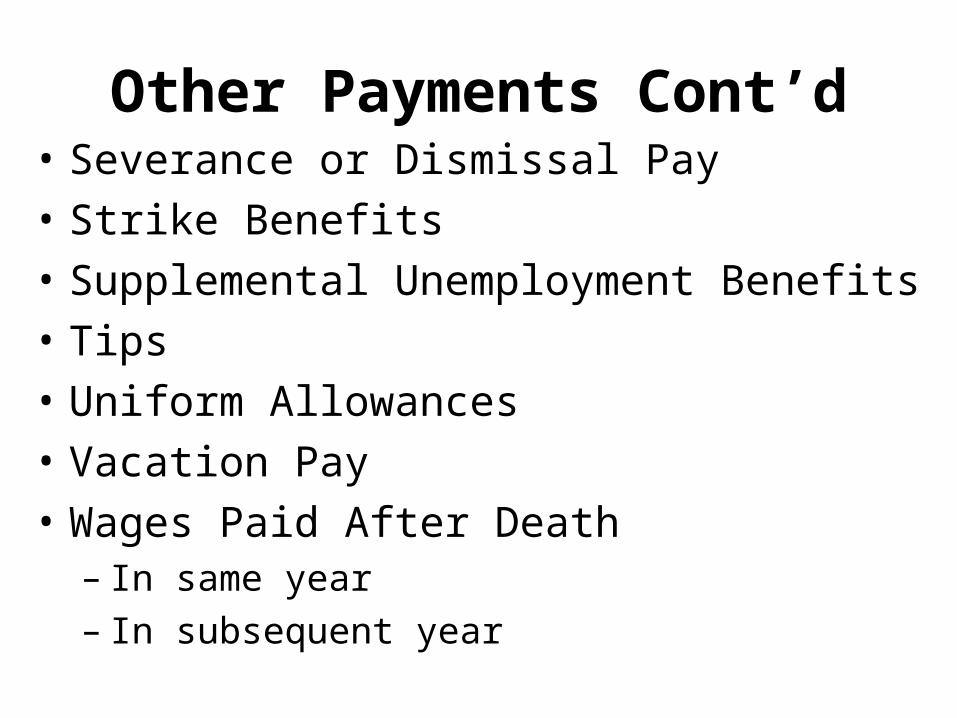

• Severance or Dismissal Pay• Strike Benefits• Supplemental Unemployment Benefits• Tips• Uniform Allowances• Vacation Pay• Wages Paid After Death

– In same year– In subsequent year

Other Payments Cont’d

• Stocks and Stock Options– Stock as compensation– Stock Options– Incentive Stock Options– Stock Purchase Plan– Non Qualified Stock Options– Tax Treatment– Written Statement

Other Payments Cont’d

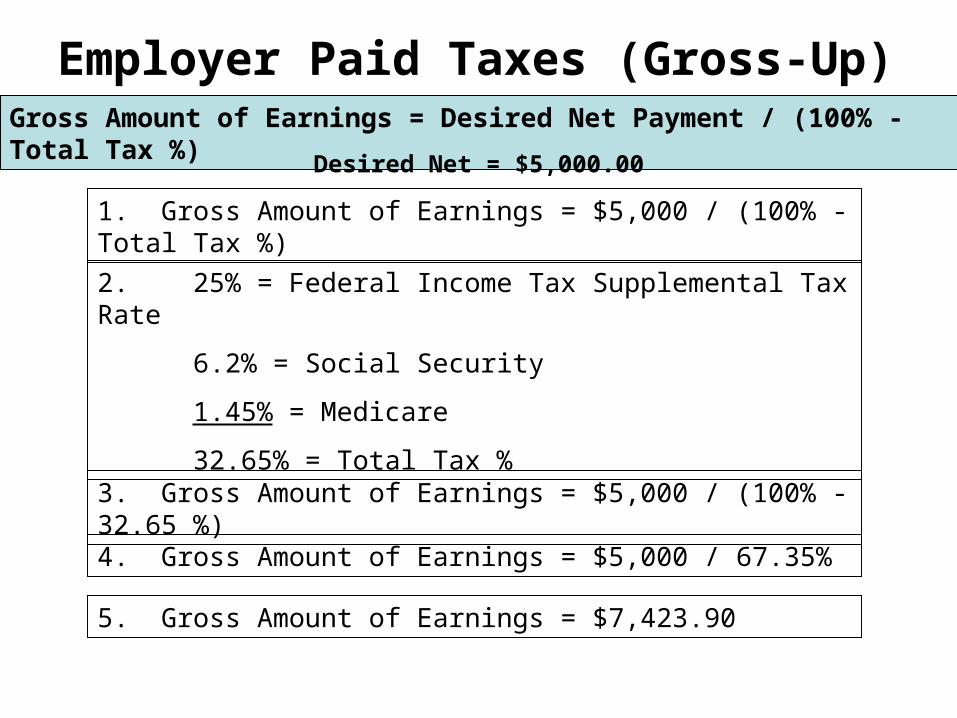

Employer Paid Taxes (Gross-Up)Gross Amount of Earnings = Desired Net Payment / (100% - Total Tax %)

1. Gross Amount of Earnings = $5,000 / (100% - Total Tax %)

2. 25% = Federal Income Tax Supplemental Tax Rate

6.2% = Social Security

1.45% = Medicare

32.65% = Total Tax %

3. Gross Amount of Earnings = $5,000 / (100% - 32.65 %)

4. Gross Amount of Earnings = $5,000 / 67.35%

Desired Net = $5,000.00

5. Gross Amount of Earnings = $7,423.90

Withholding and Reporting for Employer Provided

Benefits• Cash Fringe Benefits• Non Cash Fringe Benefits

– Withholding Methods– Imputed Income– Gross Up– Special Accounting Rule– W2 Requirements

Questions ?

Discussion Time

Prior Topics

Topic this week

Homework Problems

Any questions on:

Next Class

Topic : Section 4

Health, Accident

and

Retirement Plans

It’s It’s CalculatioCalculation Time!n Time!