cpg innovation from ideation to aisle: new techniques for staying ahead of consumer trends

TRANSCRIPT

CPG INNOVATION FROM IDEATION TO AISLE:New Techniques for Staying Ahead of Consumer Trends

Justin WheelerVP of Product Innovation

Today’s Speakers

Phil LempertThe Supermarket Guru

INNOVATION TODAY:Why Don’t We Innovate More?

• 85% of new products fail1

• 85% of American household needs are filled with same 150 items2

• Less than 3% of new CPG products exceed $50M first-year sales3

• Nielsen 2015 Breakthrough Winners came from companies $25M to $90B4

Challenges of Launching New Products

1 Joan Schneider and Julie Hall, “Why Most Product Launches Fail,” Harvard Business Review, April 2011. 2 Ibid.3 Ibid.4 Taddy Hall and Rob Wengel, “Nielsen Breakthrough Innovation Report,” Nielsen, June 2015.

Recent Breakthroughs

Source: Taddy Hall and Rob Wengel, “Nielsen Breakthrough Innovation Report,” Nielsen, June 2015.Susan Viamari, “New Product Pacesetters: Key Cobblestones Along the Path to Growth,” IRI, April 21, 2015.

Defining Innovation

What Makes a Product Innovative?

• Sales performance?

• New category creation?

• Consumer interest?

• Cultural impact?

Is It Time for a New Definition?

GETTING YOUR BEARINGS:The State of the CPG Industry

• Consumer needs change and evolve

• The retail landscape is changing: smaller stores, more food service, fewer front ends

• Technology and social media are creating a new world for producing, buying and preparing foods, beverages and snacks

What We’re Looking at Now

The World Is Getting Smaller

• Size of stores will decrease dramatically in coming years

• Market consolidation as mergers and acquisitions continue

The Online World Is Getting Bigger

• Amazon Prime will continue to gain traction with consumers and other e-commerce companies will follow suit

⁃ 20% of Amazon Prime members who have purchased grocery products online expect to buy more in the future;; 12% who currently do not expect to do so in the future5

⁃ 25% of people globally already order products online for home delivery and more than half (55%) are willing to do so in the future6

Issues Impacting Innovation Today

5 Patrick HadlockmShankar Raja, et al., “The Digital Future: A Game Plan for Consumer Packaged Goods,” The Boston Consulting Group, April 22, 2014.6 “More Than Half of Global Consumers Are Willing to Buy Groceries Online,” Nielsen, April 29, 2015.

The Shopper Experience Is Fragmented

• Traditional media consumption (television, radio, OOH) is lower with younger generations, while overall media consumption is up

• Engaging with customers online and product evangelists on social is critically important

Younger Generations Are Changing Consumer Taste

• Millennials, and soon Gen Z, will be primary consumers

⁃ Dollar share of CPG for Millennials to increase from 17% today to 29% in 2020;; 40% of Millennials are multicultural7

7 Robert I. Tomei, “The 2020 Shopper and What It Means for CPG Marketers,” IRI, 27 June 2015 IRI.

Issues Impacting Innovation Today

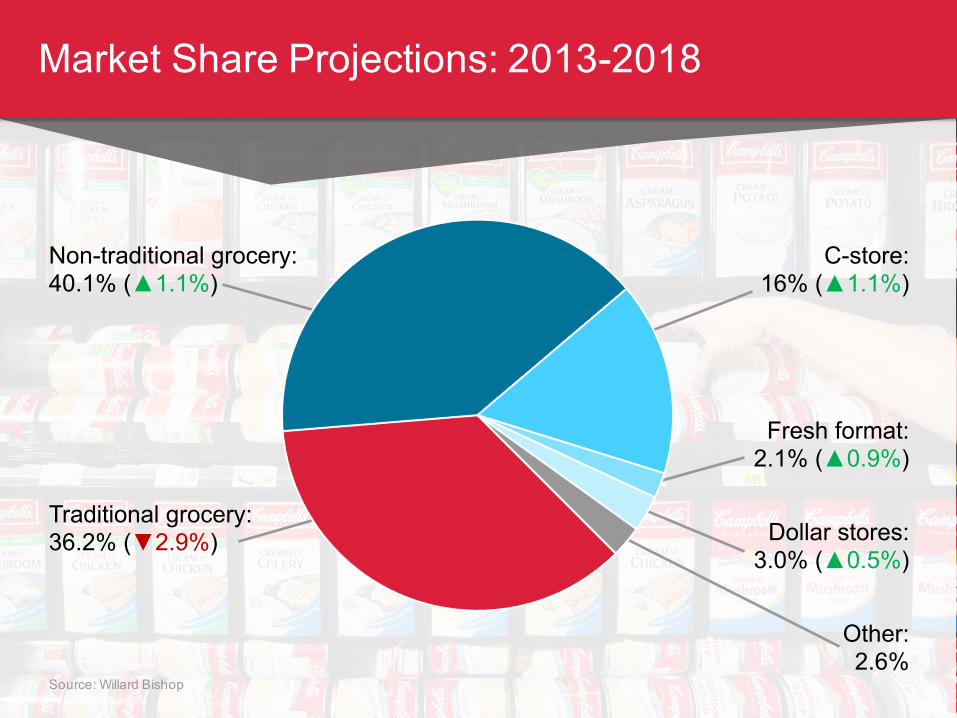

Market Share Projections: 2013-2018

Source: Willard Bishop

Traditional grocery:36.2% (2.9%)

Non-traditional grocery:40.1% (1.1%)

C-store:16% (1.1%)

Fresh format:2.1% (0.9%)

Dollar stores:3.0% (0.5%)

Other:2.6%

• All mobile?

• More fresh?

• More artisan?

• More expensive?

• More delivered?

What Will It Be Like in 2025?

A new type of food store that combines freshness, authenticity, prepared foods and on-site services (beer gardens, catering, nutritional guidance), becoming a hub for the community

The Supermarket Opportunity

Smaller Stores• From 50,000 sq. ft. to 20,000 sq. ft.

Less Assortment• From 40,000 SKUs to 20,000 SKUs

More Service• Chefs, RDs, butchers, fishmongers and sommeliers

• Grazing Golden Agers

• Smoked everything

• Fermented foods

• “Craft” foods

• Gen Z: the new chefs

• New nutrition labels

• Grocerants

• Instant delivery

Trends to Watch

Connection, Conversation and Community

• Food raves

• Food trucks

• High college debt

• Low-paying jobs

• Living at home

• Generation “child-free”

Millennials Are Passionate

The Future

Caterto health and wellness Create

a WOW experienceCelebrate

food, preparation and taste

CONFIRMING TRENDS:Supporting Observations with Data

• CPG companies launch 25,000 new products each year

• How do you keep track of competitive launches and get ahead of trends?

• We have to go straight to the source and go in-context with consumers at the shelf

Staying Ahead of Innovation

• Our preferences aren’t stable

• We aren’t guided by consistent beliefs and rational thought

Why Context Matters

Better Hindsight

Better Insight

Better Foresight

The Value of In-Context

Crowdsourcing Insights via Mobile

• Collects evaluations of new products from Instantly Mobile Army™ (~37,000+ shoppers daily)

• Incentivized participation (cash and contests)

• Alerts companies when and where products are launched and provides ongoing shopper sentiment

• Fully syndicated data set delivered via a SaaS interface with data API

Real-Time Retail Insights

Instantly Product Watch™

How It Works

• Grocery, mass merchandiser, drug and C-stores are geofenced (US, UK)

• Consumers invited via mobile to go on a scavenger hunt

• Consumers find new products on shelf, take photos and answer a short survey

• Photos are coded and tagged for brand, product, price, category and attributes

• Clients access insights via live dashboard and email notifications

Instantly Product Watch™

Anatomy of a Product Watch™ Submission

BrandName

ProductName

Shelf/Row

Context

KeyAttributes Unit

Size

PromotionPrice

RetailPrice

Flavor/Variety

Information Gathered From Shopper Photos

Anatomy of a Product Watch™ Submission

Additional Mobile App Data• Store (brand)• Store (location)• Consumer demo• UPC• Date/time• Full shelf photo (new)

Additional Consumer Survey Data• Purchase intent• Value/price• Salience (stand out)• Augment/replace existing• Brand fit/permission• Shopping impact• Leadership• Success prediction

DATA-DRIVEN IDEATION:How to Prioritize New Ideas

• Early-stage data on new ideas is critical to success

• With real consumer feedback, you can:

⁃ Refine your number of concepts before next stage

⁃ Eliminate gut decisions

⁃ Better understand your target consumer

Early-Stage Concept Testing

Instantly Concept Test™

• Online tool for early-stage assessment of new product and promotion ideas

• Load new concepts and launchtests in under five minutes

• Collect insights from a nationallyrepresentative online or mobile audience of 300

• Rank and compare conceptsby key performance indicators, attributes and open-end responses

Concept Testing Reimagined

Justin Wheeler VP of Product Innovation, [email protected] | (866) 872-4006 | www.instant.ly

Questions?

Phil LempertThe Supermarket [email protected] | (310) 392-0448 | www.supermarketguru.com

References

Hadlock, Patrick, Shankar Raja, et al., “The Digital Future: A Game Plan for Consumer Packaged Goods,” The Boston Consulting Group, April 22, 2014, https://www.bcgperspectives.com/content/articles/digital_economy_consumer_products_digital_future_game_plan_consumer_packaged_goods/?chapter=2

Hall, Taddy and Rob Wengel, “Nielsen Breakthrough Innovation Report,” Nielsen, June 2015, http://www.nielsen.com/us/en/solutions/capabilities/breakthrough-innovation1.html.

Schneider, Joan and Julie Hall, “Why Most Product Launches Fail,” Harvard Business Review, April 2011, https://hbr.org/2011/04/why-most-product-launches-fail.

Tomei, Robert I., “The 2020 Shopper and What It Means for CPG Marketers,” IRI, 27 June 2015 IRI, http://www.iriworldwide.com/insights/blog/May-2015/The-2020-Shopper-and-What-It-Means-for-CPG-Markete.

Viamari, Susan, “New Product Pacesetters: Key Cobblestones Along the Path to Growth,” IRI, April 21, 2015, http://www.iriworldwide.com/IRI/media/IRI-Clients/NPP-April-2015-vFINAL2.pdf

“More Than Half of Global Consumers Are Willing to Buy Groceries Online,” Nielsen, April 29, 2015, http://www.nielsen.com/us/en/press-room/2015/more-than-half-of-global-consumers-are-willing-to-buy-groceries-online.html.