corporate governance of dual class firms - ifs.swufe.edu.cn · pdf filethis paper explores the...

TRANSCRIPT

Corporate Governance of Dual Class Firms

Ting Li and Nataliya Zaiats∗

This Version: June 2012

∗Li is from Sheldon B. Lubar School of Business, University of Wisconsin-Milwaukee, Milwaukee, WI53201, [email protected], 414-229-6337. Zaiats is from School of Management, Simmons College, Boston,MA 02115, [email protected], (617) 521-2397. We are grateful for the insightful suggestionsand comments from Lilian Ng, James G. Tompkins, Timothy K Mooney and Ujjal Chatterjee, as well asparticipants of 2011 Annual Meeting of Southern Finance Association in Key West. All remaining errors aremy responsibility.

Corporate Governance of Dual Class Firms

Abstract

This paper explores the specific corporate governance structure of dual-class firms over the sample

period of 1996-2006. Firms with more takeover attributes but fewer board-related attributes tend to

be dual-class firms. Results show that such firms are associated with higher firm value, suggesting

that the takeover attributes of dual-class firms are able to help offset the weak board-related

corporate governance. Dual-class firms with strictly more takeover provisions have a lower cost of

equity and a lower cost of debt. The results also indicate that corporate governance of dual-class

firms changes around unification. Following the unification, we find that firms are inclined to have

fewer takeover and more board-related provisions.

Keywords: Dual class; corporate governance; firm value; cost of equity; cost of debt

JEL Classification Number: G32; G34

1. Introduction

Dual-class firm, as a special ownership structure, has gained a great deal of attention in empirical

research in finance and economics. According to Gompers, Ishii and Metrick (2009) (GIM (2009)),

from 1995 to 2002 about 6% of public companies in the United States have more than one class

of common stock, and these companies are virtually immune to a hostile takeover. The unique

structure of dual class firms allows the separation of cash flow rights and voting rights. Research

shows that firm values increases with cash flow rights and decreases with voting rights (GIM

(2009)). This divergence also aggravates the agency conflicts between managers and shareholders,

thus manages are more prone to pursue private benefits at shareholders’ expense (Masulis, Wang

and Xie (2009)).

Prior research only takes dual-class structure as a strong anti-takeover feature of corporate gov-

ernance. Studies regarding dual-class firms compare the agency problem, firm value, stock return,

and institutional ownership between dual-class firms and single-class firms. However, few studies

look at the specific corporate governance structures of dual-class firms, which effectively insulate

from the market for control. On the other hand, studies pertaining to corporate governance look

at the governance attributes of all the firms (DeAngelo and Rice 1983; Linn and McConnell 1983,

Shleifer and Vishny (1997), Gompers, Ishii, and Metrick (2003) (GIM (2003)). It is possible that

dual-class firm with such strong anti-takeover feature itself may have different corporate gover-

nance structure compared with single-class firms. The motivation of this paper is to investigate

the specific corporate governance structure of dual-class firms.

We employ a comprehensive dual-class firm database to investigate the specific corporate gov-

ernance structure of such firms over the sample period of 1996-2006. Our results show that dual-

class firms have different corporate governance compared with single-class firms. Firms with more

takeover attributes but fewer board-related attributes are inclined to be dual-class firms. Dual-class

firms with more takeover attributes and weak board-related governance tend to have larger firm

value. Takeover provisions are important to firm value only if the firm’s board quality is poor. The

takeover attributes dual class firms are taking help to offset the effect caused by weak board-related

1

corporate governance. Dual-class firms with strictly more takeover provisions have lower cost of

equity and lower cost of debt.

A great number of studies have been conducted on the impacts of such discrepancy on dual-

class firms. Early research has shown the advantages and benefits that the dual-class structure

can bring to firms. DeAngelo and DeAngelo (1985) suggest that dual-class firms may best be

viewed as an intermediate organizational form between the dispersed-ownership public corporation

and the closed-held firm. They argue that such intermediate structure is more likely to be used

when managerial voting ownership yields benefits by investigating four case studies. Harris and

Raviv (1988) argue that separating cash flow and voting rights can maximize firm value at social

optimality. Their result implies that security value is maximized by issuing dual-classes of shares.

The aggregate value of existing equity increases if the firm announces a switch of single class to

multiple-classes. Smart and Zutter (2003) and Smart, Thirumalai, and Zutter (2008) demonstrate

that the dual-class firms experience less underpricing than single-class firms by comparison of dual

and single-class IPOs. Dual-class shares substantially reduce the dilution effect and mitigate under-

investment problem. Also, many empirical studies on the effects of dual-class shares on shareholder

wealth examine the dual-class recapitalizations. Cornett and Vetsuypens (1989) document that

dual-class recapitalization leads to the increase of abnormal stock prices. Dimitrov and Jain (2006)

also find that dual-class recapitalizations are associated with positive abnormal stock return and

enhance the shareholders’ value.

Although the advantages of dual-class firms have been discussed by many studies, most recent

research illustrates that the disadvantages of dual-class firms are associated with negative abnormal

stock returns, lower firm value, agency problems and value-destroying acquisitions. Jarrell and

Poulsen (1988) report that negative abnormal stock return occurs with the announcement of dual-

class recapitalization. GIM (2009) consider the dual-class structure as extreme governance and

analyze the determinants of dual-class status. Based on this, they find that firm value is increasing

in insiders’ cash-flow rights and decreasing in insiders’ voting rights. Masulis, Wang, and Xie (2009)

examine the agency problem of dual-class firms. They find that as the divergence between insiders’

voting rights and cash flow rights widens, managers are more likely to pursue private benefits at

2

shareholders’ expense. They conclude such agency problems help explain the lower firm value with

insider excess control rights.

Hanson and Song (1996) investigate the acquisitions of dual-class firms and find that managers

are likely to make value reducing acquisitions. They interpret the evidence that managers who have

high control rights are more likely to make acquisitions to pursue private benefits while harm outside

shareholders. Li, Ortiz-Molina and Zhao (2008) examine the shareholder voting rights effects on

institution investment decisions. They document that voting rights are critical to institutional

investment decisions and the institutional ownership is significantly lower in dual-class firms than

in single class firms.

Dual-class structure is considered as an extreme anti-takeover feature of corporate governance.

The role of corporate governance has received growing interests, from academic and industry,

with recognition of its importance. Corporate governance is defined as a set of processes, policies

and laws, which affect the way a corporation is directed, administered and controlled. Shleifer and

Vishny (1997) refer corporate governance as the way in which suppliers of finance assure themselves

a return on their investment.

Whether the corporate governance provisions affect firm value and harm the shareholders has

been a subject of controversy among the researchers and practitioners over the past decades. Some

research documents a positive value effect associated with antitakeover provisions (DeAngelo and

Rice 1983; Linn and McConnell 1983), while others argues a negative value effect (Malatesta and

Wakling 1988; Lins 2003). GIM (2003) first construct a “Governance Index” to proxy for the balance

of power between shareholders and managers. They find that firms with stronger shareholder rights

have higher firm value, higher profits, higher sales growth, and lower capital expenditures and make

fewer corporate acquisitions. Bebchuk, Cohen and Ferrell (2009) further build an entrench index

and argue that the increase of index is associated with significant reduction in firm valuation and

large negative stock returns.

Straska and Waller (2010) reexamine the negative relationship between firm value and the

number of antitakeover provisions a firm is adopting. They find that firms with low bargaining

3

power adopting more antitakeover provisions can enhance the firm value. Such finding challenges the

prevailing view and suggests the negative relations between firm value and antitakeover provisions

are not universal. Classens, Djankov, Fan and Lang (2002) analyze the incentive and entrenchment

of large ownership. They find that firm value increases with cash-flow ownership of large shareholder

and decreases when control rights of large shareholder exceed its cash-flow ownership.

Corporate board structure as a component of corporate governance has been debated for its

impact on firm value and firm behavior as well. Adams and Ferreira (2007) and Harris and Raviv

(2008) build the theoretical determinants of board structure. Boone, Field, Karpoff and Raheja

(2007) track corporate board development from firms’ IPO through 10 years and conclude that

board structure demonstrates the firm’s competitive environment and managerial team. Coles,

Daniel and Naveen (2008) examine the firm value and board structure. They argue that restrictions

on board size and management representation on the board do not necessarily enhance the firm

value. Linck, Netter and Yang (2008) examine the board structure, trends and determinants by

analyzing nearly 7,000 from 1990 to 2004. They find strong associations between board structure

and firm size and ownership. Jiang (2010) evaluates the treatment effect of dual-class ownership

on board structure by analyzing the dual-class firm from 1998 to 2002. The results indicate that

dual-class ownership has a significant effect on board structure and on average dual-class firms have

a slightly bigger and less independent board.

Our study advances the literature in two ways. First, it contributes to the understanding

of the specific corporate governance structure of dual-class firms. We compare the difference of

corporate governance between dual-class firms and single-class firms. We hypothesize that firms

with certain corporate governance attributes are more likely to be dual-class firms after GIM (2009)

determinants of dual status at the time of IPO are controlled. We look at five takeover attributes

and seven board-related attributes used mostly by previous corporate governance studies, which

will be discussed in section 2. We identify governance features with which firms are more likely to

be dual class firms.

Second, our study shows that among all dual-class firms, those with certain corporate governance

attributes have higher firm values and dual class is not value destructive for all the firms. Prior

4

studies argue that dual class structure is related to agency problems and low firm value (GIM

(2009); Masulis, Wang and Xie (2009)). Since dual class firms have their own governance feature,

regular governance provisions may have no effects on firm value of dual class firms. We investigate

the relationship between firm value, cost of equity and cost of debt and corporate governance

structures within dual class firms.

The remainder of this paper is organized as follows. Section 2 describes our data, measures

of corporate governance, and summarizes the distribution of corporate governance. Section 3

summarizes the distribution of corporate governance, and shows the association among dual class

structure, corporate governance and firm value. Section 4 conducts the robustness tests. Section 5

concludes the paper.

2. Sample and Data Description

2.1. Data

To investigate the corporate governance structures of dual class firms, we use several data sets. GIM

(2009) construct a comprehensive set of dual-class firms over the period 1994-2002 with data from

the Security Data Company, S&P’s Compustat, the Center for Research in Security Prices, and

the Investor Responsibility Research Center. For each dual class firm, they collect information on

voting rights per share for different classes of stock, dividends per share for different classes of stock,

number of shares of different stock classes owned by insiders and shares outstanding of different

classes. Nguyen and Xu (2010) extend the dual class sample to 2006 with the same methodology

used by GIM (2009).1 Thus, the sample period of dual class firms is from 1994-2006.

We obtain corporate governance data from the Investor Responsibility Research Center (IRRC).

IRRC publishes the directors data including a range of variables related to individual board directors

collected since 1996 and updated annually. IRRC also publishes detailed listings of corporate

governance for individual firms in Takeover Defense in years 1990, 1993, 1995, 1998, 2000, 2002,

2004 and 2006. Since IRRC does not publish takeover defense volumes annually and corporate

1We thank Paul Gompers, Joy Ishii and Andrew Metrick for their generosity in providing the dual class data from1994-2002. We also thank Li Xu for their generosity in providing the extended dual class data to 2006.

5

governance provisions are stable, we assume takeover defenses are same as the nearest prior IRRC

volume if they are not published in certain year. Following Cremers and Nair (2005), we regard

provisions from takeover defense data as takeover provisions. More takeover provisions means

“lower management power” or “stronger shareholder rights. Directors data provides information of

each individual director in different firms. We construct board-related attribute dummies for each

firm based on the continuous variables for individual directors. Since directors data were collected

from 1996 and the sample period of dual class firms is from 1994-2006, the sample period of our

study is from 1996-2006. There are 1452 firm-year observations for dual class firms and 19802

firm-year observations for single class firms.

We get financial data for all firms from Compustat. We drop firms in utilities or financial

industries. When we restrict our sample to firms having both corporate governance and financial

data to conduct regressions, the sample size reduces to 4651 firm-year observations.

2.2. Corporate Governance

Based on previous academic literature, we focus on the following 12 attributes in takeover defense

data and directors data. We use five takeover provisions: shareholders may call special meetings;

shareholders may act by written consent; company has no poison pill; company has no staggered

board; and shareholders have cumulative voting rights. Besides, we use seven attributes associated

with board quality: all directors attended 75% of board meetings; CEO serves on two or fewer

boards of other firms; the outside directors are more than 50%; board size is greater than 5 but

less than 16; nominating committee is composed solely of independent outsiders; chairman and

CEO are separated; compensation committee is composed solely of independent outsiders. We use

12 dummy variables indicating whether a firm has the above 12 corporate governance attributes,

respectively. If the firm meets the threshold level for certain standard above, that dummy variable

takes the value of 1, and 0 otherwise.

Since board attribute dummies are constructed with continuous data from directors data, there

are missing values for some firms. To ensure the corporate governance indices reflect more accurate

information, following Aggarwal et al. (2008), we express the corporate governance indices as

6

percentage of non-missing attributes for each firm. We construct 3 indices for each firm: Takeover

sub-index (TSI), Board-related sub-index (BSI) and Total index (TI). TSI is computed as the

percentage of non-missing takeover attributes that a firm satisfies. If a firm meets the threshold

level for all the 5 anti-takeover attributes, TSI of the firm is 100%. If there is a missing attribute,

we eliminate the missing attribute and compute the percentage of satisfied takeover attributes to

non-missing takeover attributes. Higher TSI indicates stronger shareholder rights. BSI is computed

as the percentage of satisfied board-related attributes to non-missing board-related attributes. TI is

computed as the percentage of all non-missing corporate governance attributes (including takeover

attributes and board-related attributes) that the firm satisfies. Each of the takeover attributes and

board-related attributes is associated with stronger governance. Higher index indicates that the

firm satisfies more corporate governance (or takeover or board-related) attributes.

The readers may concern why we focus on these 12 attributes, instead of using more corporate

governance attributes. The reasons are as follows. First, according to prior literature, these 12

attributes are mostly used and they are critical to corporate governance. Besides, certain attributes

are required by SEC for all the firms, so there will be no significant differences between dual-class

firms and single-class firms for these attributes.

2.3. Distribution of Corporate Governance Provisions

Table 1 shows the distribution of corporate governance attributes and indices for dual-class firms

and single-class firms. Panel A provides the distribution of the pooled sample. GIM (2009) report

that, in about 33% of all dual class firms, the insiders have voting rights greater than 50% while

their cash flow rights are less than 50%. They classify these firms as the “separation sample”. We

also compare the corporate governance between single-class firms and firms in separation sample.

TSI and TI of dual class firms are greater than TSI and TI of single class firms, while BSI of dual

class firms is less than that of single class firms. The differences are significant at 1% level. The

differences between single class firms and separation sample are greater. Since insiders of firms in

the separation sample have effective control over the firm, the boards are more entrenched and the

board-related corporate governance is relatively weak. On the other hand, since dual class structure

7

itself is an extremely strong anti-takeover feature, dual class firms are well protected from M&A,

especially for the separation sample. It is unnecessary for them to restrict shareholder rights tightly.

TSI of separation sample is greater than that of single class firms, while BSI of separation sample

is less than that of single class firms.

From the distribution of individual attributes, we can see that more dual-class firms adopt

takeover attributes relative to single-class firms. For example, more dual-class firms allow share-

holders to call special meeting and act by written consent, have no poison pill, have no staggered

board and offer shareholders cumulative voting rights. We also can see that dual-class firms are less

independent. Fewer dual-class firms have board with more than 50% independent outside direc-

tors, with nominating committee composed solely of independent outsiders and with compensation

committee composed solely of independent outsiders. However, more dual-class firms have optimal

board size (board size is greater than 5 but less than 16), have CEO serving 2 or fewer outsider

boards, and have separated chairman and CEO. Jensen (1993), Yermack (1996), and Core et al.

(1999) suggest that large board size is expected to be associated with less effective board moni-

toring. Our results indicate more dual class firms have optimal board size, and they should have

effective board monitoring. Unreported Chi-square test indicates that the individual governance

attributes are significantly different between dual class firms and single class firms.

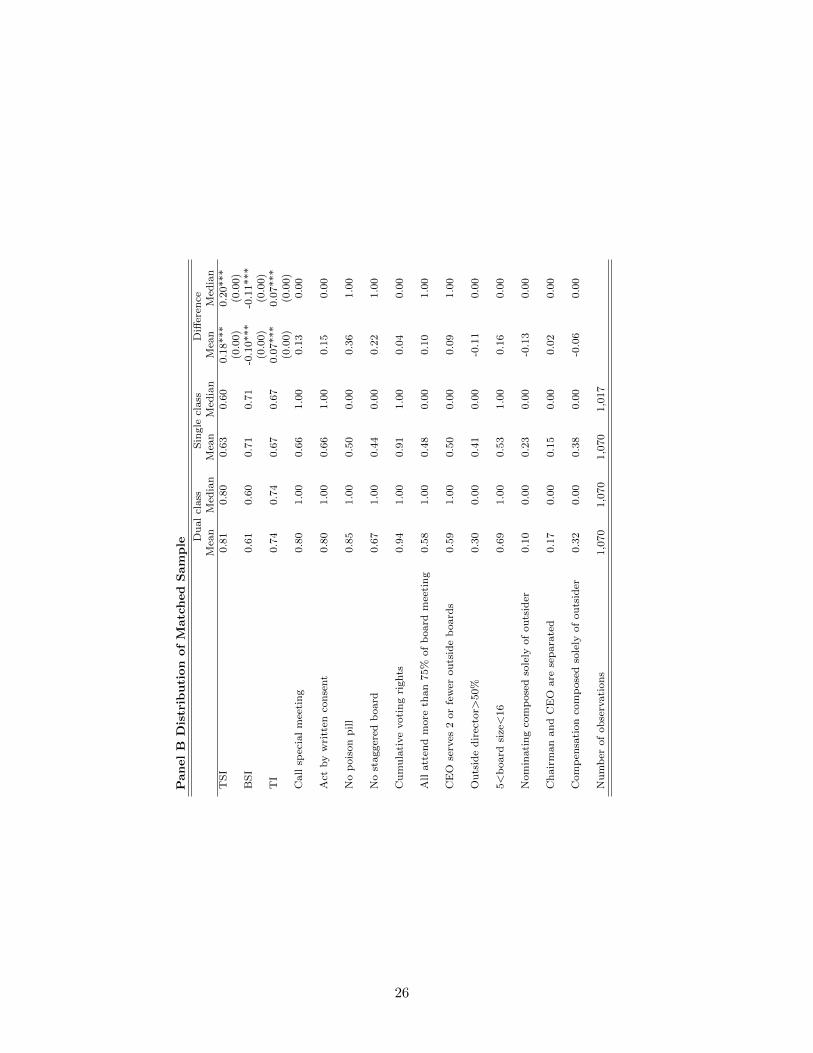

Panel B provides the distribution of matched sample. We match dual-class firms with single-

class firms by propensity score, which can control for the differences between them. We estimate a

probit model with GIM (2009) determinants to get the propensity score. The determinants include

Fama-French industry classification, dummy variables indicating whether the firm was a “media”

company in its IPO year, indicating whether the firm is named for a founder, and indicating whether

the firm was incorporated in states with anti-takeover laws, the percentile ranking of the IPO-year

sales and profit of the firm relative to other firms with the same IPO year, the percentage of all

Compustat firms located in the same area in the year before IPO, the percentage of all Compustat

sales by firms located in the same area in the year prior to IPO.2 The values of difference decrease

a little in the matched sample. But they are still significant.

2Please refer to GIM (2009) for more detailed description of the determinants of dual-class structures.

8

3. Empirical Results

We conduct the empirical analysis as follows. First, we investigate the association between corporate

governance and dual-class structure by probit regressions. Second, we examine whether dual-class

firms with specific corporate governance features have higher firm value. Third, we compare the

cost of equity of dual-class firms and that of single-class firms with similar corporate governance

level.

3.1. The Association between Corporate Governance and Dual-Class Structure

GIM (2009) state that firm, industry, or market characteristics at the time of a firm’s IPO will

determine the dual-class status of that firm, since the decision to go public involves negotiation

between insiders and shareholders. The insiders are more likely to have the ability to argue with

the shareholders and obtain a dual-class structure upon the IPO if the aggregate reduction in share

value is less than the private benefits of control. The summary statistics indicate that corporate

governance is different between dual-class firms and single-class firms. It is possible that the

corporate governance structure changes gradually after a firm listed its share on a public exchange,

which may lead to the change of voting and ownership structure. We conjecture that with certain

corporate attributes, a firm is more inclined to adopt the dual-class structure.

After controlling for GIM (2009) determinants, we employ probit regressions to show the rela-

tionship between corporate governance and dual-class status. Table 2 displays the results of probit

estimations on individual corporate attributes. The dependent variable is a dummy variable indi-

cating if a company is a dual-class firm. The independent variables are governance attribute dummy

variables, which indicate whether a firm meets the threshold level for certain corporate governance

standards. Column 1 presents coefficient estimates from the probit regression with GIM (2009)

dual-class status determinants only as controlled variables. The results suggest that firms adopting

the 5 takeover attributes and having optimal board size are more inclined to be dual class firms.

But independent board and high attendance of board meetings reduce the probability of being

dual-class firms. The effects of board-related attributes on the probability are mixed. Column

9

2 presents coefficient estimates from the probit regression including GIM (2009) dual-class status

determinants and control variables used by other studies related to dual class firms. Most of the

coefficient estimates are similar to those reported in column 1. Coefficients of dummy variable “All

attend more than 75% of board meetings” is not significant in column 2. Overall, table 2 illustrates

that dual-class structure is related to certain corporate governance attributes. Firms with more

takeover attributes and fewer attributes associated with board quality are inclined to be dual-class

firms.

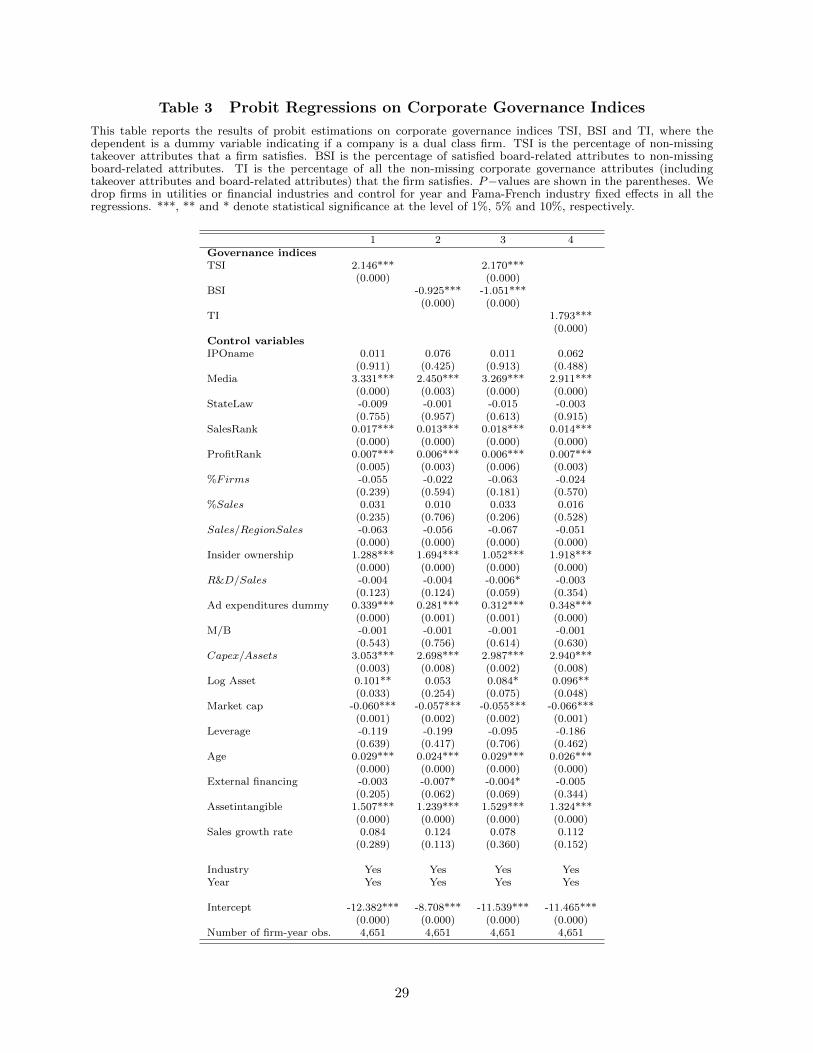

Table 2 reports the results of probit estimations on corporate governance indices TSI, BSI and

TI, where the dependent variable is a dual class dummy. We control GIM (2009) determinants of

dual-class status and variables used by other studies related to dual class firms. In these regressions

we cluster the standard errors by each firm. In column 1 and 2 we test the relationship between

dual-class status and TSI, and between dual-class status and BSI, respectively. The coefficients

of TSI and BSI are significantly positive at 1% level. The probability of being dual class firms is

increasing with adopting more of the five takeover attributes and adopting fewer of the seven board-

related attributes. In column 3, we include both TSI and BSI in the regression. The coefficients

of TSI and BSI are consistent with previous two regressions and significant at 1%. The economic

significance increases for both coefficients. In Table 2, some of coefficients of the individual board

attributes are insignificant. The influences of individual board-related attributes on the probability

of being dual class firms are not the same. But here the overall BSI is strongly negative.

In column 4, we test how the overall corporate governance of a firm determinates the dual

class structure. The result implies that firms adopting more governance attributes are more likely

to be dual-class firms. Though adopting some board-related attributes reduces the probability of

being dual class firms, the countervailing effect of takeover attributes and board-related attributes

increases the probability of being dual class firms.

In sum, the results in Table 2 and 3 provide support for our hypothesis that dual-class firms

possess specific corporate governance compared with single-class firms. Firms taking more takeover

attributes and fewer board-related attributes are more likely to choose dual-class structure.

10

3.2. Firm Values of Dual Class Firms

Prior literature suggests that firm valuation is related to cash flow ownership and voting structure.

Claessens et al. (2002) find firm valuation increases with cash flow ownership in the hands of the

largest shareholders and decreases with the increases in control rights by the largest shareholder.

GIM (2009) show that firm value is increasing in insiders’ cash flow rights and decreasing in insiders’

voting rights. There is no research related to dual-class firms testing the relationship between

firm values and corporate governance in dual-class firms. We want to investigate the association

between firm value and corporate governance structure of dual-class firms. We hypothesize that

dual-class firms with certain corporate governance feature have higher firm value compared with

the counterpart dual-class firms, since the governance structure of this kind of dual-class firms

countervail the effect of entrenchment.

We use Tobin’s Q to measure firm value. Following Kaplan and Zingales (1997), we compute

Tobin’s Q as the market value of assets divided by the book value of assets, where the market value

of assets is the book value of assets plus the market value of common stock less the book value of

common stock less balance sheet deferred taxes. Following GIM (2009), to reduce the measurement

error of Tobin’s Q, we compute industry-adjusted Tobin’s Q, industry-adjusted ln Q, and inverse

industry-adjusted Q as −[1/Q− 1/(industryQ)].

3.2.1. Distribution of Firm Values

To look at the distribution of firm values among dual-class firms with different corporate governance

and discrepancy between cash flow rights and voting rights, we create different portfolios based on

TSI and voting rights, TSI and cash flow rights, BSI and voting rights, and BSI and cash flow

rights, respectively. Voting rights are computed as the total percentage of votes owned by officers

and directors across classes. Cash flow rights are computed as the total percentage of cash flow

ownership by officers and directors (GIM, 2009). First, we create 3 portfolios among the dual

class firms by the value of TSI. Dual class firms in portfolio 1 have the lowest TSI, while firms in

portfolio 3 have the highest TSI. Second, within each TSI portfolio, we create 3 portfolios based

on the voting rights of the dual class firms. Portfolio 1 includes firms with the lowest voting rights

11

while portfolio 3 includes firms with the highest voting rights. Finally, there are 9 portfolios. We

use the same method to create other portfolios.

Table 4 reports the distribution of industry-adjusted Tobin’s, industry-adjusted ln Q, and inverse

industry-adjusted Q among different portfolios. In panel A we create the 9 portfolios based on dual-

class firms’ TSI and voting rights. GIM (2009) argue that firm value is decreasing in insider voting

rights and increasing in insider cash flow rights. When we look at firm values within each TSI

portfolio, the different forms of Tobin’s Q are not always decreasing in insider voting rights. In

panel B we create the 9 portfolios based on dual class firms’ TSI and cash flow rights. Within each

TSI portfolio, the different forms of Tobin’s Q are not always increasing with cash flow rights. On

average, values of Tobin’s Q are relatively greater for dual class firms with more takeover attributes.

When we take corporate governance into consideration, firm value is neither increasing with cash

flow rights nor decreasing with voting rights, which is not consistent with GIM (2009). Adopting

more of the 5 takeover attributes increases the firm values.

Panel C presents the value distribution of the 9 portfolios created by the value of BSI and

voting rights. Within each BSI portfolio, firm value is not decreasing with the voting rights. Panel

D demonstrates the value distribution of the 9 BSI-cash flow rights portfolios. Within each BSI

portfolio, firm value is not increasing with the cash flow rights all the time. Above all, when

corporate governance is controlled, firm value is not changing with the cash flow rights and the

voting rights. Firm value changes with the adoption of corporate governance.

3.2.2. Firm value and corporate governance of dual class firms

Prior studies illustrate that good corporate governance is associated with higher firm value, higher

profits, positive abnormal returns and lower capital expenditures (GIM, 2003; Bebchuk, Cohen, and

Ferrell, 2008). The analysis in the preceding section shows that the corporate governance structure

is different between dual-class firms and single-class firms. Firms with more takeover attributes

and fewer board-related are more likely to be dual-class firms. We will investigate if this specific

governance structure will influence the firm value of dual-class firms.

We assign 3 ranks to all dual class firms according to their TSI and BSI, respectively. Firms

12

in rank 1 have the lowest TSI or BSI, while firms in rank 3 have the highest TSI or BSI. We

create dummy variables indicating if a dual class firm is in the lowest rank or in the highest rank

of governance indices. The indicator variable High TSI equals 1 if a dual class firm falls in rank 3

based on TSI, and 0 otherwise. The indicator variable Low BSI equals 1 if dual class firms are in

rank 1 based on BSI, and 0 otherwise. HighTSI ×LowBSI is an interaction variable of High TSI

and Low BSI. We run OLS regressions of Tobin’s Q on the corporate governance indicators.

Table 5 provides OLS estimations of firm value. The coefficients of High TSI are not signif-

icant. But coefficients of Low BSI are significantly negative and coefficients of the interaction

are significantly positive. High TSI shows the influence of high TSI on non-Low BSI firms, while

HighTSI × LowBSI shows incremental effect of High TSI on Low BSI firms. If a dual class

firm adopts the fewest board-related attributes and does not adopt most takeover attributes, the

industry-adjusted Q will decrease about 0.7. But if this firm also adopts most takeover attributes,

the industry-adjusted Q will increase about 0.6. Based on these results, we can see that takeover

provisions are important to firm value only if the firm’s board quality is low.

We also run regressions of firm value on other indicator variables and interaction variables

respectively, such as HighTSI ×HighBSI, LowTSI ×HighBSI, and LowTSI × LowBSI. But

none of them is significant. It demonstrates that dual-class firms with fewer board-related attributes

and more takeover attributes simultaneously have higher firm values. The takeover attributes dual

class firms are taking help to protect shareholder wealth and offset the effect caused by weak board-

related corporate governance. The unique corporate governance structure of such dual class firms

increases the firm value.

4. Robustness Tests

4.1. Cost of Equity

Besides firm value, we want to further investigate if dual-class firms benefit from their specific

corporate governance features by conducting analyses of cost of equity and cost of debt. Following

Gebhardt, Lee, and Swaminathan (2001) (GLS (2001)), we employ implied cost of capital (ICOC)

13

to proxy for cost of equity. It is computed as the internal rate of return that equals the present value

of expected future cash flows to the current stock price. Besides, following Hail and Leuz (2006)

(HL (2006)), we also use the average of four different ICOC estimates as an alternative proxy for a

firm’s cost of capital. The four estimates are GLS (2001) internal rate of return; Claus and Thomas

(2001) residual income valuation model; Ohlson and Juettner-Nauroth (2005) abnormal earnings

growth valuation model; and Easton (2004) MPEG ratio, which is computed as price-to-earnings

ratios divided by growth rate. We explain the four ICOC models in Appendix B.

Table 6 presents OLS regression estimations of cost of equity on corporate governance index.

GLS and HL are dependent variables. Cash flow rights and voting rights are controlled in all models.

In Panel A, Models 1, 3, 4 and 6 show that TSI is significantly negatively related to cost of equity.

More takeover provisions help dual-class firms reduce cost of equity. However, the coefficients of

BSI are not significant in any case. In proceeding sections, we show that more dual-class firms

have optimal board size and dual-class firms are less independent. The effects of board related

provisions are mixed. Thus, we hypothesize that individual board-related attributes have different

effects on cost of equity. We run regressions of cost of equity on TSI and board-related attributes.

Panel B shows the results. The signs of coefficients are mixed, but they are insignificant. Only

dummy variable indicating “nominating committee is composed solely of independent outsiders” is

significantly positively related to HL.

Dual-class status is the ultimate takeover protection and dual-class firms are well immune from

hostile takeovers, so naturally these firms will have a reduced need for restricting shareholder rights

tightly. Dual-class firms adopting more takeover provisions have lower cost of equity. Though dual-

class status effectively insulates the firm from the market for corporate control, takeover provisions

still affect cost of equity at all. But since board-related attributes have mixed effects on dual class

firms, the attributes associated with board quantity do not reduce cost of equity for dual-class

firms.

14

4.2. Cost of Debt

Billett and Liu (2008) find that the cost of debt financing increases in managerial voting rights and

decreases in cash flow rights. We test if corporate governance provisions are associated with cost of

debt of dual-class firms after cash flow rights and voting rights are controlled. Following Francis,

Khurana, and Pereira (2005), we compute the interest rate on firm’s debt as a proxy for cost of

debt. It is calculated as the interest expense for the year divided by average short- and long-term

debt during the year. Klock, Mansi and Maxwell (2005) assign a value of 22 to AAA-rated bonds

and a value of one to D-rated bonds. We apply the same method and use the S&P credit rating as

control variable.

Table 7 reports the OLS estimations of cost of debt on corporate governance provisions of dual-

class firms. Model 3 includes both TSI and BSI. The coefficients of TSI are significantly positive at

10%. In dual-class firms, cost of debt decreases with takeover provisions after cash flow rights and

voting rights are controlled. The coefficients of cash flow rights and voting rights are not significant,

which is not consistent with Billett and Liu (2008). BSI is neither significant in Model 2 nor in

Model 3. We run regressions of cost of debt on TSI and individual board related provisions, which

is shown in Panel B. It indicates that outside directors greater than 50% and separation of chairman

and CEO reduce the cost of debt. If nominating committee is composed solely of outside directors,

cost of debt is increasing.

In all, these results indicate that dual-class firms with more takeover provisions have lower

cost of debt. Though dual-class status effectively insulates the firm from the market for corporate

control, takeover provisions still affect cost of debt of dual-class firms. Board-related attributes

have mixed effects on dual-class firms, so the overall attributes associated with board quantity do

not reduce cost of equity for dual-class firms.

4.3. Corporate Governance Indices

In our study, we use percentage of non-missing attributes that the firm satisfies as a proxy for

corporate governance. Some researchers use the number of attributes that the firm satisfies to

15

proxy for it (e.g., GIM, 2003; Bebchuk, Cohen, and Ferrell, 2008). We also conduct all the tests

with the additive indices. We get qualitatively similar results. Our results are not sensitive to the

corporate governance measures.

4.4. Endogeneity

Existence of endogeneity may prevent us from concluding that corporate governance leads to dual-

class structure, since the causality can be reversed or the corporate governance and stock class

structure can be determined simultaneously. We need to check the endogeneity problem. In Table

8, we show the changes of corporate governance provisions around unifications. Unification is

a procedure that dual class firms change the stock structure from dual class to single class. It

is an intra-firm transaction of voting rights. Studies show that abnormal returns are associated

with the announcement of dual-class unification (Ehrhardt, Kuklinski, and Nowak, 2005), and the

institutional ownership increases largely after unification (Li, Ortiz-Molina, and Zhao, 2008). The

event of unification provides a good timing for us to investigate the corporate governance between

dual-class structure and single-class structure on one firm with other things constant.

We use 1-year window, 3-year window and 5-year window. Corporate governance is stable for

a firm and it takes time for corporate governance to change, so we do not find significant changes

between 1-year average before unification and 1-year average after unification. We only report

the results of 3-year window and 5-year window. Panel A shows the 3-year average corporate

governance provisions before unification and the 3-year average corporate governance provisions

after it. Panel B shows the 5-year average corporate governance before unification and the 5-year

average corporate governance after it. Both panels show that firms take less takeover attributes and

more board-related attributes after unification. The percentage of boards with optimal size drops

and the boards are more independent when the firms unify. The corporate governance structure

changes significantly after the unification. The differences are significant around unification. We

argue that the corporate governance and stock class structure are not determined simultaneously.

Besides, we also use corporate governance attributes and indices in the first year a firm appears

in our sample instead of annual values. We get qualitatively similar results.

16

5. Conclusion

In this paper, we investigate the corporate governance structure of dual-class firms using dual-

class sample data from 1996-2006. Prior literature focuses on the agency problems, abnormal

returns and firm values of such firms. Since dual-class structure is a strong anti-takeover provision,

we want to examine the corporate governance of firms with this feature. We hypothesize that

dual-class firms have different corporate governance relative to single-class firms and the special

corporate governance structure will benefit dual-class firms under certain circumstance. We test

the hypothesis on five takeover attributes and seven board-related attributes.

We find that the corporate governance structure of dual-class firms is significantly different from

that of single-class firms. More dual-class firms allow shareholders to call special meetings and act

by written consent, has no poison pill, has no staggered board and offer shareholders cumulative

voting rights. But the boards of dual-class firms are less independent while more such firms have

optimal board size and separated CEO and chairman. We further show that, among all the firms

in our sample, firms with the above governance features are more likely to be dual-class firms. Our

results also indicate that firm value is not changing with voting rights and cash flow rights when

the corporate governance of dual-class firms is controlled. Dual-class firms with more takeover

attributes and weak board-related governance have higher firm value compared with other dual-

class firms. The takeover attributes dual-class firms are taking help to protect shareholder wealth

and eliminate the effect caused by weak board-related corporate governance.

Our study documents the specific corporate governance structure of dual-class firms and such

firms with certain governance feature tend to have higher firm value. But overall board-related

attributes neither increase dual-class firm value, nor reduce the cost of equity and cost of debt.

Besides, dual-class status is a strong anti-takeover feature. But we still find that takeover provisions

actually affect dual class firm value, cost of equity, and cost of debt. In future, we need to explain

why takeover provisions affect firm value though dual-class status effectively insulates the firm

from the market for corporate control and how dual-class structure fits in with other governance

provisions.

17

References

Adams, R.B., Ferreira, D., 2007. A Theory of Friendly Boards. The Journal of Finance 62,

217-250

Aggarwal, R., Erel, I., Stulz, R., Williamson, R., 2009. Differences in Governance Practices be-

tween U.S. and Foreign Firms: Measurement, Causes, and Consequences. Review of Financial

Studies 22, 3131-3169

Bebchuk, L., Cohen, A., Ferrell, A., 2009. What Matters in Corporate Governance? The Review

of Financial Studies 22, 783-827

Billett, M.T., Liu, Y., 2008. Shareholder-Manager Alignment and the Cost of Debt. Working

Paper

Boone, A.L., Casares Field, L., Karpoff, J.M., Raheja, C.G., 2007. The Determinants of Corporate

Board Size and Composition: An Empirical Analysis. Journal of Financial Economics 85,

66-101

Claessens, S., Simeon, D., Fan, J.P.H., Lang, L.H.P., 2002. Disentangling the Incentive and

Entrenchment Effects of Large Shareholdings. The Journal of Finance 57, 2741-2771

Claus, J., Thomas, J., 2001. Equity Premia as Low as Three Percent? Evidence from Analysts’

Earnings Forecasts for Domestic and International Stock Markets. The Journal of Finance

56, 1629-1666

Coles, J.L., Daniel, N.D., Naveen, L., 2008. Boards: Does One Size Fit All? . Journal of Financial

Economics 87, 329-356

Core, J.E., Guay, W.R., Rusticus, T.O., 2006. Does Weak Governance Cause Weak Stock Returns?

An Examination of Firm Operating Performance and Investors’ Expectations. The Journal

of Finance 61, 655-687

Cornett, M., Vetsuypens, M.R., 1989. Voting Rights and Shareholder Wealth. The Issuance of

Limited Voting Common Stock. Managerial and Decision Economics 10, 175-188

18

Cremers, K.J.M., Nair, V.B., 2005. Governance Mechanisms and Equity Prices. Journal of

Finance LX, 2859-2894

DeAngelo, H., DeAngelo, L., 1985. Managerial Ownership of Voting Rights : A Study of Public

Corporations with Dual Classes of Common Stock. Journal of Financial Economics 14, 33-69

DeAngelo, H., Rice, E.M., 1983. Antitakeover Charter Amendments and Stockholder Wealth.

Journal of Financial Economics 11, 329-359

Dimitrov, V., Jain, P.C., 2006. Recapitalization of One Class of Common Stock into Dual-class:

Growth and Long-run Stock returns. Journal of Corporate Finance 12, 342-366

Easton, P.D., 2004. PE Ratios, PEG Ratios, and Estimating the Implied Expected Rate of Return

on Equity Capital. The Accounting Review 79, 73-95

Francis, J.R., Khurana, I.K., Pereira, R., 2005. Disclosure Incentives and Effects on Cost of

Capital around the World. The Accounting Review 80, 1125-1162

Gebhardt, W.R., Lee, C.M.C., Swaminathan, B., 2001. Toward an Implied Cost of Capital.

Journal of Accounting Research 39, 135-176

Gompers, P., Ishii, J., Metrick, A., 2003. Corporate Governance and Equity Prices. The Quarterly

Journal of Economics 118, 107-155

Gompers, P.A., Ishii, J., Metrick, A., 2009. Extreme Governance: An Analysis of Dual-Class

Firms in the United States. Review of Financial Studies 23, 1051-1088

Ehrhardt, O., Kuklinski, J., Nowak, E., 2005. Unifications of Dual-Class Shares in Germany

Empirical Evidence on the Effects of Related Changes in Ownership Structure, Market Value,

and Bid-ask Spreads. Swiss Finance Institute Research Paper Series

Hail, L., Leuz, C., 2006. International Differences in the Cost of Equity Capital: Do Legal

Institutions and Securities Regulation Matter? Journal of Accounting Research 44, 485-531

19

Hanson, R.C., Song, M.H., 1996. Ownership Structure and Managerial Incentives: The Evidence

from Acquisitions by Dual Class Firms. Journal of Business Finance & Accounting 23, 831-

849

Harris, M., Raviv, A., 1988. Corporate governance: Voting Rights and Majority Rules. Journal

of Financial Economics 20, 203-235

Harris, M., Raviv, A., 2008. A Theory of Board Control and Size. The Review of Financial

Studies 21, 1797-1832

Jarrell, G.A., Poulsen, A.B., 1988. Dual-class Recapitalizations as Antitakeover Mechanisms: The

Recent Evidence. Journal of Financial Economics 20, 129-152

Jensen, M.C., 1993. The Modern Industrial Revolution, Exit, and the Failure of Internal Control

Systems. Journal of Finance XLVIII, 831-880

Jiang, J., 2010. Board Structure in Dual-class Firms. Working Paper

Kaplan, S.N., Zingales, L., 1997. Do Investment-Cash Flow Sensitivities Provide Useful Measures

of Financing Constraints? The Quarterly Journal of Economics 112, 169-215

Li, K., Ortiz-Molina, H., Zhao, X., 2008. Do Voting Rights Affect Institutional Investment Deci-

sions? Evidence from Dual-Class Firms. Financial Management 37, 713-745

Linck, J.S., Netter, J.M., Yang, T., 2008. The Determinants of Board Structure. Journal of

Financial Economics 87, 308-328

Linn, S.C., McConnell, J.J., 1983. An Empirical Investigation of the Impact of ’Antitakeover’

Amendments on Common Stock Prices. Journal of Financial Economics 11, 361-399

Lins, K.V., 2003. Equity Ownership and Firm Value in Emerging Markets. The Journal of

Financial and Quantitative Analysis 38, 159-184

Malatesta, P.H., Walkling, R.A., 1988. Poison Pill Securities: Stockholder Wealth, Profitability,

and Ownership Structure. Journal of Financial Economics 20, 347-376

20

Masulis, R.W., Wang, C., Xie, F., 2009. Agency Problems at Dual-Class Companies. The Journal

of Finance 64, 1697-1727

Nguyen, V.T., Li, X., 2010. The Impact of Dual Class Structure on Earnings Management

Activities. Journal of Business Finance & Accounting 37, 456-485

Ohlson, J., Juettner-Nauroth, B., 2005. Expected EPS and EPS Growth as Determinantsof Value.

Review of Accounting Studies 10, 349-365

Ortiz-Molina, H., Phillips, G.M., 2009. Asset Liquidity and the Cost of Capital. Working Paper

Shleifer, A., Vishny, R.W., 1997. A Survey of Corporate Governance. The Journal of Finance 52,

737-783

Smart, S.B., Thirumalai, R.S., Zutter, C.J., 2008. What’s in a Vote the Short- and Long-run

Impact of Dual-class Equity on IPO Firm Values. Journal of Accounting and Economics 45,

94-115

Smart, S.B., Zutter, C.J., 2003. Control as a Motivation for Underpricing: A Comparison of Dual

and Single-class IPOs. Journal of Financial Economics 69, 85-110

Straska, M., Waller, G., 2010. Do Antitakeover Provisions Harm Shareholders? Journal of Cor-

porate Finance 16, 487-497

Yermack, D., 1996. Higher Market Valuation of Companies with a Small Board of Directors.

Journal of Financial Economics 40, 185-211

21

Appendix A Variable Definitions

Variable DefinitionTakeover attributesCall special meeting It equals 1 if shareholders may call special meetings, and 0 otherwiseAct by written consent It equals 1 if shareholders may act by written consent, and 0 otherwiseNo poison pill It equals 1 if company has no poison pill, and 0 otherwiseNo staggered board It equals 1 if company has no staggered board, and 0 otherwiseCumulative voting rights It equals 1 if shareholders have cumulative voting rights,

and 0 otherwiseBoard-related attributesAll attend more than It equals 1 if all directors attended 75% of board meetings,75% of board meetings and 0 otherwise

CEO serves 2 or fewer It equals 1 if CEO serves on two or fewer boards of other firms,outside boards and 0 otherwise

Outside director>50% It equals 1 if the outside directors are more than 50%, and 0 otherwise5<Board size<16 It equals 1 if board size is greater than 5 but less than 16,

and 0 otherwiseNominating composed It equals 1 if nominating committee is composed solely of independentsolely of outsider outsiders, and 0 otherwise

Chairman and CEO are separated It equals 1 if chairman and CEO are separated, and 0 otherwiseCompensation composed It equals 1 if compensation committee is composed solely of independentsolely of outsider outsiders, and 0 otherwiseGovernance indicesTSI The percentage of non-missing takeover attributes that a firm satisfiesBSI The percentage of satisfied board-related attributes to non-missing

board-related attributesTI The percentage of all the non-missing corporate governance attributes

(including takeover attributes and board-related attributes) that the

firm satisfiesGIM (2009) determinantsIPOname It equals 1 if the firm’s name at IPO includes a person’s name,

and 0 otherwiseMedia It equals 1 if the firm was a “media” company in its IPO year,

and 0 otherwiseStateLaw It equals 1 if the firm was incorporated in states with anti-takeover laws,

and 0 otherwiseSalesRank Percentile ranking of the IPO year sales of the firm relative to other firms

with the same IPO yearProfitRank Percentile ranking in the IPO year profit of the firm relative to other firms

with the same IPO year%Firms Percentage of all Compustat firms located in the same metropolitan or

micropolitan statistical area (MSA) as firm i in the year before firm i’s IPO%Sales Percentage of all Compustat sales by firms located in the same micropolitan

statistical area (MSA) as firm i in the year before firm i’s IPOSales/RegionSales Ratio of a firm’s sales to the sales of all firms in the same region

22

Variable Definitions (Continued)Variable DefinitionTobin’s Q and cost of equityTobin’s Q The market value of assets divided by the book value of assets,

where the market value of assets is the book value of assets plus the marketvalue of common stock less the book value of common stock less balancesheet deferred taxes

Inverse industry-adjusted Q −[1/Q− 1/(industryQ)]Implied cost of equity (GLS(2001)) The present value of expected future cash flows to the current stock priceImplied cost of equity (HL(2006)) The average of four different ICOC estimates:

GLS (2001) internal rate of return; Claus and Thomas (2001) residualincome valuation model; Ohlson and Juettner-Nauroth (2005) abnormalearnings growth valuation model; and Easton (2004) MPEG ratio,which is computed as price-to-earnings ratios divided by growth rate.

Cost of debt Interest expense for the year divided by average short- and long-term debtduring the year

Other control variablesBeta Computed with CAPM over the past five yearsTurn Stock turnover ratioVar The past-year’s monthly return variance of a stockRett−1 The average monthly return over the past yearCFR Cash flow rights: computed as the total percentage of cash flow ownership

by officers and directorsCFR2 Squared cash flow rightsVR Voting rights: computed as the total percentage of votes owned by officers

and directors across classesV R2 Squared voting rightsRate S&P credit rating: AAA-rated bonds receive a value of 22 and D-rated

bonds receive a value of oneInsider ownership Fraction of shares owned officers and directorsR&D/Sales The ratio of R&D over salesAd expenditures dummy It equals 1 if the advertisement expenditures are greater than 0, and 0 otherwiseM/B Market to book ratioCapex/Assets Capital expenditures over total assetsLog Asset Log of the book value of total assetsMarket cap Market price times number of outstanding sharesLeverage All debt over market value of total assetsAge The number of years since a firms first appearance in CRSPExternal financing The difference between required investment and internally available capital

for investmentAssetintangible (1 − PPE + Inventories)/TotalAssetsSales growth rate Average annual sales growth over past 3 yearsDelaware incorporation It equals 1 if the firm is incorporated in Delaware, and 0 otherwiseROA Net income over book value of total assets

23

Appendix B Implied Cost of Capital Models

We follow Hail and Leuz (2006) by employing the average of four different ICOCs as a proxy for each firm’s yearly costof capital. For consistency and for comparison of results with those of Hail and Leuz, we closely adopt the two authors’specifications and assumptions of the four models, as described below, when estimating the ex ante cost of capital as impliedby each model.

1. Gebhardt, Lee, and Swaminathan’s (2001) residual income valuation model is given by

Pt = bvt +

T∑τ=1

( ˆepst+τ − rGLS · bvt+τ−1)

(1 + rGLS)τ+

( ˆepst+T+1 − rGLS · bvt+T )

rGLS(1 + rGLS)T, (1)

where Pt is the market price of a firm’s stock at time t, ˆepst+τ is the expected future earnings per share for period(t+ τ − 1, t+ τ), and bvt+τ−1 is the book value per share at time t+ τ − 1. The model obtains the initial three yearsof expected future residual income from actual book values per share and forecasted earnings per share up to threeyears ahead. Assuming clean surplus, future book values are imputed from current book values, forecasted earnings,and dividends; the same assumption is also adopted by Claus and Thomas (2001) below. For each year, dividendsare set equal to the average of the past three years of payout ratios. Dividends are defined in the same way for thefollowing three models. Beyond the initial three years, the stream of residual incomes is derived by linearly decreasingthe forecasted accounting return on equity over the next nine years to the firm’s specific sector’s median return onequity determined over the past three years. Following Hail and Leuz (2006), we classify firms into industrial, service,and financial sectors. If a specific sector’s median is negative, then we replace it by the country-year median. Residualincome is assumed to remain constant beyond 12 years.

2. Claus and Thomas’s (2001) residual income valuation model is given by

Pt = bvt +T∑τ=1

( ˆepst+τ − rCT · bvt+τ−1)

(1 + rCT )τ+

( ˆepst+T − rCT · bvt+T−1)(1 + g)

(rCT − g)(1 + rCT )T. (2)

The model obtains the stream of expected future residual income from actual book values per share and forecastedearnings per share up to five years ahead. Beyond year five, nominal residual income is assumed to grow at the rateg equal to the expected inflation (as proxied by the annualized median of a country’s one-year ahead realized monthlyinflation rates).

3. Easton’s (2004) MPEG model is given by

Pt =( ˆepst+2 + rMPEG · d̂t+1 − ˆepst+1)

r2MPEG

. (3)

The model derives a measure of abnormal earnings growth by using one-year and two-year ahead earnings per shareforecasts as well as expected dividends per share in period t + 1. It assumes perpetual growth in abnormal earningsafter the initial period.

4. Ohlson and Juettner-Nauroth’s (2005) abnormal earnings growth valuation model is specified as follows.

Pt =ˆepst+1

rOJ·

(gst + rOJ · d̂t+1

ˆepst+1− glt)

(rOJ − glt). (4)

The model uses one-year-ahead forecasted earnings and dividends per share as well as forecasts of short-term and long-term abnormal earnings growths. The short-term growth rate gst is equal to the average of the forecasted percentagechange in the first two years of earnings and the five-year growth forecast provided by financial analysts on I/B/E/S.The long-term earnings growth rate glt is set equal to the annualized country-specific median of one-year-ahead realizedmonthly inflation rates.

24

Tab

le1

Dis

trib

uti

on

of

Corp

ora

teG

overn

ance

This

table

show

sth

euniv

ari

ate

dis

trib

uti

on

of

corp

ora

tegov

ernance

for

dual-

class

firm

sand

single

-cla

ssfirm

s.P

anel

Apro

vid

esth

edis

trib

uti

on

of

the

poole

dsa

mple

.P

anel

Bpro

vid

esth

edis

trib

uti

on

of

the

matc

hed

sam

ple

.T

he

table

pre

sents

mea

ns

and

med

ians

of

gov

ernance

indic

esand

att

ribute

s.P−

valu

esoft−

test

sfo

rth

em

eans

of

diff

eren

ces

andp−

valu

esof

Wilco

xon

rank-s

um

test

for

the

med

ians

of

diff

eren

ces

are

show

nin

the

pare

nth

eses

ben

eath

the

diff

eren

ces.

TSI

isth

ep

erce

nta

ge

of

non-m

issi

ng

takeo

ver

att

ribute

sth

at

afirm

sati

sfies

.B

SI

isth

ep

erce

nta

ge

of

sati

sfied

board

-rel

ate

datt

ribute

sto

non-m

issi

ng

board

-rel

ate

datt

ribute

s.T

Iis

the

per

centa

ge

of

all

the

non-m

issi

ng

corp

ora

tegov

ernance

att

ribute

s(i

ncl

udin

gta

keo

ver

att

ribute

sand

board

-rel

ate

datt

ribute

s)th

at

the

firm

sati

sfies

.***,

**

and

*den

ote

stati

stic

al

signifi

cance

at

the

level

of

1%

,5%

and

10%

,re

spec

tivel

y.

PanelA

Distribution

ofPooled

Sample

Du

al

class

Sin

gle

class

Sep

ara

tion

Du

al-

Sin

gle

Sep

ara

tion

-Sin

gle

Mea

nM

edia

nM

ean

Med

ian

Mea

nM

edia

nM

ean

Med

ian

Mea

nM

edia

nT

SI

0.7

90.8

00.5

90.6

00.8

71.0

00.2

0***

0.2

0***

0.2

8***

0.4

0***

(0.0

0)

(0.0

0)

(0.0

0)

(0.0

0)

BS

I0.6

10.6

00.7

00.7

10.6

10.6

0-0

.09***

-0.1

1***

-0.0

9***

-0.1

1***

(0.0

0)

(0.0

0)

(0.0

0)

(0.0

0)

TI

0.7

20.7

30.6

40.6

40.7

60.7

50.0

8***

0.0

9***

0.1

2***

0.1

1***

(0.0

0)

(0.0

0)

(0.0

0)

(0.0

0)

Call

spec

ial

mee

tin

g0.6

91.0

00.5

71.0

00.7

81.0

00.1

20.0

00.2

10.0

0

Act

by

wri

tten

con

sent

0.7

11.0

00.5

91.0

00.7

71.0

00.1

30.0

00.1

90.0

0

No

pois

on

pill

0.7

61.0

00.3

90.0

00.8

61.0

00.3

71.0

00.4

71.0

0

No

stagger

edb

oard

0.5

91.0

00.3

80.0

00.6

81.0

00.2

11.0

00.3

01.0

0

Cu

mu

lati

ve

voti

ng

rights

0.8

41.0

00.8

31.0

00.8

41.0

00.0

10.0

00.0

20.0

0

All

att

end

more

than

75%

of

board

mee

tin

gs

0.5

81.0

00.5

31.0

00.5

71.0

00.0

60.0

00.0

50.0

0

CE

Ose

rves

2or

few

erou

tsid

eb

oard

s0.6

01.0

00.5

01.0

00.5

91.0

00.0

90.0

00.0

90.0

0

Ou

tsid

ed

irec

tor>

50%

0.3

30.0

00.4

70.0

00.3

20.0

0-0

.14

0.0

0-0

.15

0.0

0

5<

Board

size<

16

0.6

91.0

00.5

81.0

00.6

61.0

00.1

10.0

00.0

80.0

0

Nom

inati

ng

com

pose

dso

lely

of

ou

tsid

er0.1

00.0

00.2

30.0

00.1

20.0

0-0

.13

0.0

0-0

.12

0.0

0

Ch

air

man

an

dC

EO

are

sep

ara

ted

0.1

90.0

00.1

40.0

00.1

70.0

00.0

50.0

00.0

30.0

0

Com

pen

sati

on

com

pose

dso

lely

of

ou

tsid

er0.3

30.0

00.3

90.0

00.3

00.0

0-0

.06

0.0

0-0

.08

0.0

0

Nu

mb

erof

ob

serv

ati

on

s1,4

52

1,4

52

19,8

02

19,8

02

534

534

25

PanelB

Distribution

ofM

atched

Sample D

ual

class

Sin

gle

class

Diff

eren

ceM

ean

Med

ian

Mea

nM

edia

nM

ean

Med

ian

TS

I0.8

10.8

00.6

30.6

00.1

8***

0.2

0***

(0.0

0)

(0.0

0)

BS

I0.6

10.6

00.7

10.7

1-0

.10***

-0.1

1***

(0.0

0)

(0.0

0)

TI

0.7

40.7

40.6

70.6

70.0

7***

0.0

7***

(0.0

0)

(0.0

0)

Call

spec

ial

mee

tin

g0.8

01.0

00.6

61.0

00.1

30.0

0

Act

by

wri

tten

con

sent

0.8

01.0

00.6

61.0

00.1

50.0

0

No

pois

on

pill

0.8

51.0

00.5

00.0

00.3

61.0

0

No

stagger

edb

oard

0.6

71.0

00.4

40.0

00.2

21.0

0

Cu

mu

lati

ve

voti

ng

rights

0.9

41.0

00.9

11.0

00.0

40.0

0

All

att

end

more

than

75%

of

board

mee

tin

g0.5

81.0

00.4

80.0

00.1

01.0

0

CE

Ose

rves

2or

few

erou

tsid

eb

oard

s0.5

91.0

00.5

00.0

00.0

91.0

0

Ou

tsid

ed

irec

tor>

50%

0.3

00.0

00.4

10.0

0-0

.11

0.0

0

5<

board

size<

16

0.6

91.0

00.5

31.0

00.1

60.0

0

Nom

inati

ng

com

pose

dso

lely

of

ou

tsid

er0.1

00.0

00.2

30.0

0-0

.13

0.0

0

Ch

air

man

an

dC

EO

are

sep

ara

ted

0.1

70.0

00.1

50.0

00.0

20.0

0

Com

pen

sati

on

com

pose

dso

lely

of

ou

tsid

er0.3

20.0

00.3

80.0

0-0

.06

0.0

0

Nu

mb

erof

ob

serv

ati

on

s1,0

70

1,0

70

1,0

70

1,0

17

26

Table 2 Probit Regressions on Individual Governance Attributes

This table shows the results of probit regressions on individual corporate governance attributes. The dependent

variable is a dummy variable indicating if a company is a dual-class firm. The dummy variable takes the value of 1 if

it is a dual-class firm, and 0 otherwise. The independent variables are governance attribute dummy variables, which

indicate whether a firm meets the threshold level for certain corporate governance standards. Variable definitions

are given in the Appendix. P−values are shown in the parentheses. We drop firms in utilities or financial industries

and control for year and Fama-French industry fixed effects in all the regressions. ***, ** and * denote statistical

significance at the level of 1%, 5% and 10%, respectively.

27

1 2Takeover attributesCall special meeting 0.213*** 0.296***

(0.000) (0.009)Act by written consent 0.285*** 0.478***

(0.000) (0.000)No poison pill 0.691*** 0.588***

(0.000) (0.000)No staggered board 0.308*** 0.312***

(0.000) (0.001)Cumulative voting rights 0.197** 0.506***

(0.031) (0.000)Board-related attributesAll attend more than 75% of board meetings -0.139** 0.028

(0.025) (0.812)CEO serves 2 or fewer outside boards 0.065 -0.227

(0.587) (0.335)Outside director>50% -0.426*** -0.403***

(0.000) (0.000)5<Board size<16 0.448*** 0.182

(0.000) 0.386Nominating composed solely of outsider -0.315*** -0.214*

(0.000) (0.059)Chairman and CEO are separated -0.062 -0.105

(0.276) (0.278)Compensation composed solely of outsider -0.010 -0.178**

(0.866) (0.050)Control variablesIPOname 0.252*** 0.025

(0.000) 0.808Media 0.686*** 3.329***

(0.000) (0.000)StateLaw -0.004 -0.004

0.819 0.885SalesRank 0.009*** 0.020***

(0.000) (0.000)ProfitRank 0.002** 0.005**

(0.020) (0.028)%Firms -0.074*** -0.055

(0.005) (0.262)%Sales 0.023 0.026

(0.148) (0.351)Sales/RegionSales -0.021*** -0.073***

(0.000) (0.000)Insider ownership 0.618***

(0.004)R&D/Sales -0.005*

(0.083)Ad expenditures dummy 0.339***

(0.001)M/B -0.001

(0.715)Capex/Assets 2.952***

(0.002)Log Asset 0.041

(0.400)Market cap -0.045**

(0.023)Leverage 0.037

(0.885)Age 0.029***

(0.000)External financing -0.002

0.287Assetintangible 1.603***

(0.000)Sales growth rate 0.105

(0.261)

Industry Yes YesYear Yes Yes

Intercept -6.578*** -12.076***(0.000) (0.000)

Number of Obs. 10,337 4,651

28

Table 3 Probit Regressions on Corporate Governance Indices

This table reports the results of probit estimations on corporate governance indices TSI, BSI and TI, where thedependent is a dummy variable indicating if a company is a dual class firm. TSI is the percentage of non-missingtakeover attributes that a firm satisfies. BSI is the percentage of satisfied board-related attributes to non-missingboard-related attributes. TI is the percentage of all the non-missing corporate governance attributes (includingtakeover attributes and board-related attributes) that the firm satisfies. P−values are shown in the parentheses. Wedrop firms in utilities or financial industries and control for year and Fama-French industry fixed effects in all theregressions. ***, ** and * denote statistical significance at the level of 1%, 5% and 10%, respectively.

1 2 3 4Governance indicesTSI 2.146*** 2.170***

(0.000) (0.000)BSI -0.925*** -1.051***

(0.000) (0.000)TI 1.793***

(0.000)Control variablesIPOname 0.011 0.076 0.011 0.062

(0.911) (0.425) (0.913) (0.488)Media 3.331*** 2.450*** 3.269*** 2.911***

(0.000) (0.003) (0.000) (0.000)StateLaw -0.009 -0.001 -0.015 -0.003

(0.755) (0.957) (0.613) (0.915)SalesRank 0.017*** 0.013*** 0.018*** 0.014***

(0.000) (0.000) (0.000) (0.000)ProfitRank 0.007*** 0.006*** 0.006*** 0.007***

(0.005) (0.003) (0.006) (0.003)%Firms -0.055 -0.022 -0.063 -0.024

(0.239) (0.594) (0.181) (0.570)%Sales 0.031 0.010 0.033 0.016

(0.235) (0.706) (0.206) (0.528)Sales/RegionSales -0.063 -0.056 -0.067 -0.051

(0.000) (0.000) (0.000) (0.000)Insider ownership 1.288*** 1.694*** 1.052*** 1.918***

(0.000) (0.000) (0.000) (0.000)R&D/Sales -0.004 -0.004 -0.006* -0.003

(0.123) (0.124) (0.059) (0.354)Ad expenditures dummy 0.339*** 0.281*** 0.312*** 0.348***

(0.000) (0.001) (0.001) (0.000)M/B -0.001 -0.001 -0.001 -0.001

(0.543) (0.756) (0.614) (0.630)Capex/Assets 3.053*** 2.698*** 2.987*** 2.940***

(0.003) (0.008) (0.002) (0.008)Log Asset 0.101** 0.053 0.084* 0.096**

(0.033) (0.254) (0.075) (0.048)Market cap -0.060*** -0.057*** -0.055*** -0.066***

(0.001) (0.002) (0.002) (0.001)Leverage -0.119 -0.199 -0.095 -0.186

(0.639) (0.417) (0.706) (0.462)Age 0.029*** 0.024*** 0.029*** 0.026***

(0.000) (0.000) (0.000) (0.000)External financing -0.003 -0.007* -0.004* -0.005

(0.205) (0.062) (0.069) (0.344)Assetintangible 1.507*** 1.239*** 1.529*** 1.324***

(0.000) (0.000) (0.000) (0.000)Sales growth rate 0.084 0.124 0.078 0.112

(0.289) (0.113) (0.360) (0.152)

Industry Yes Yes Yes YesYear Yes Yes Yes Yes

Intercept -12.382*** -8.708*** -11.539*** -11.465***(0.000) (0.000) (0.000) (0.000)

Number of firm-year obs. 4,651 4,651 4,651 4,651

29

Table 4 Distribution of Firm Values in Different Portfolios

This table shows the distribution of industry-adjusted Tobins, industry-adjusted ln Q, and inverse industry-adjustedQ across different portfolios. The portfolios are created based on TSI and voting rights, TSI and cash flow rights,BSI and voting rights, and BSI and cash flow rights, respectively. The table provide both means and medians. Thep−values of t−test for means and p−values of Wilcoxon rank-sum test for medians are shown in parentheses beneaththe means and medians. ***, ** and * denote statistical significance at the level of 1%, 5% and 10%, respectively.

Panel A Portfolios Created on TSI and Voting Rights

TSI Voting rights Industry-adjusted Q Industry-adjusted LnQ −[1/Q− 1/(industryQ)]mean median N mean median N mean median N

1 1 0.112 0.000 169 0.004 0.000 169 -0.027 0.000 169(0.181) (0.898) (0.920) (0.633) (0.192) (0.344)

1 2 0.199** -0.004 168 0.049 -0.004 168 0.001 -0.003 168(0.020) (0.387) (0.180) (0.563) (0.943) (0.881)

1 3 0.384*** 0.049*** 165 0.104*** 0.039** 165 0.017 0.029 165(0.000) (0.004) (0.007) (0.016) (0.420) (0.133)

2 1 0.256** 0.020 108 0.058 0.017 108 -0.009 0.012 108(0.027) (0.270) (0.226) (0.486) (0.752) (0.869)

2 2 0.128 -0.033 107 -0.016 -0.028 107 -0.053** -0.024 107(0.236) (0.402) (0.704) (0.234) (0.039) (0.106)

2 3 0.394*** 0.068*** 105 0.142*** 0.0477** 105 0.049** 0.0370* 105(0.000) (0.008) (0.001) (0.015) (0.037) (0.058)

3 1 0.365*** 0.112*** 166 0.132*** 0.062*** 166 0.0422** 0.043*** 166(0.000) (0.000) (0.000) (0.000) (0.018) (0.009)

3 2 0.227*** -0.021* 174 0.060 -0.018 174 -0.006 -0.013 174(0.005) (0.055) (0.109) (0.231) (0.802) (0.914)

3 3 0.273*** 0.030** 178 0.079*** 0.022** 178 0.015 0.017 178(0.000) (0.012) (0.010) (0.050) (0.382) (0.266)

Panel B Portfolio Created on TSI and Cash Flow Rights

TSI Cash flow rights Industry-adjusted Q Industry-adjusted LnQ −[1/Q− 1/(industryQ)]mean median N mean median N mean median N

1 1 0.128* 0.000 171 0.018 0.000 171 -0.023 0.000 171(0.060) (0.655) (0.581) (0.949) (0.237) (0.416)

1 2 0.171* -0.001 171 0.021 -0.001 171 -0.017 -0.001 171(0.082) (0.869) (0.601) (0.963) (0.453) (0.632)

1 3 0.387*** 0.035*** 165 0.113*** 0.031** 165 0.029 0.027* 165(0.000) (0.004) (0.002) (0.011) (0.123) (0.082)

2 1 0.058 -0.084 115 -0.024 -0.049 115 -0.054** -0.038* 115(0.473) (0.606) (0.556) (0.324) (0.036) (0.073)

2 2 0.506*** 0.111** 98 0.142** 0.0711** 98 0.032 0.049* 98(0.001) (0.016) (0.011) (0.030) (0.274) (0.073)

2 3 0.249*** 0.000 108 0.077** 0.000 108 0.014 0.000 108(0.003) (0.224) (0.040) (0.339) (0.542) (0.699)

3 1 0.257*** 0.000*** 162 0.080*** 0.000** 162 0.013 0.000 162(0.000) (0.003) (0.005) (0.027) (0.441) (0.355)

3 2 0.418*** 0.029*** 176 0.120*** 0.021** 176 0.025 0.016 176(0.000) (0.002) (0.003) (0.015) (0.262) (0.175)

3 3 0.285*** 0.066*** 182 0.094*** 0.043** 182 0.020 0.027 182(0.000) (0.002) (0.003) (0.020) (0.281) (0.249)

30

Panel C Portfolios Created on BSI and Voting Rights

BSI Voting rights Industry-adjusted Q Industry-adjusted LnQ −[1/Q− 1/(industryQ)]mean median N mean median N mean median N

1 1 -0.009 -0.056* 186 -0.039 -0.041** 186 -0.046*** -0.030*** 186(0.864) (0.085) (0.161) (0.039) (0.009) (0.007)

1 2 0.195*** -0.039 192 0.039 -0.038 192 -0.020 -0.027 192(0.002) (0.171) (0.172) (0.732) (0.271) (0.311)

1 3 0.304*** 0.0211** 191 0.080*** 0.018* 191 0.009 0.016 191(0.000) (0.018) (0.008) (0.085) (0.579) (0.556)

2 1 0.260*** 0.019** 153 0.089** 0.010* 153 0.027 0.006 153(0.002) (0.017) (0.010) (0.056) (0.164) (0.227)

2 2 0.187** 0.000 149 0.044 0.000 149 -0.011 0.000 149(0.032) (0.220) (0.303) (0.376) (0.674) (0.941)

2 3 0.329*** 0.039** 151 0.103*** 0.029** 151 0.033 0.019* 151(0.001) (0.011) (0.005) (0.018) (0.105) (0.061)