contents table of - sedf.gos.pksedf.gos.pk/pdf/gem-ar-2011.pdf · executive summary 1. in 2011, the...

TRANSCRIPT

CONTENTS

01

TABLE

03040506

1012

13162729384041

42

43

56

OF

575860

LIST OF FIGURES

Figure 1: The Entrepreneurship Process and GEM Operational DefinitionsFigure 2: Characteristics of Economic Groups and Key Development FocusFigure 3: The GEM ModelFigure 4: Entrepreneurial Profile of Pakistan compared with other nationsFigure 5: Entrepreneurship Institution Profile of Pakistan with other nationsFigure 6: Sector Structure Total early-stage Entrepreneurial Activity (TEA) and Established Business ActivityFigure 7: TEA rates of GEM 2011 participating countriesFigure 8: Total Early-Stage Entrepreneurial Activity Rates and Per Capita GDP 2011Figure 9: GEM Economies Ranked by Level of Female Participation in Total Early-Stage Entrepreneurship Activity (TEA) by Economic Group, 2011Figure 10A&B: Composite indicators on entrepreneurship institutionsFigure 11: Mean Scores Awarded by National Experts to Entrepreneurial Framework Conditions in Pakistan as compared to factor driven economiesFigure 12: Mean Scores Awarded by National Experts to Entrepreneurial Framework Conditions in Pakistan as compared to efficiency driven economiesFigure 13: Mean Scores Awarded by National Experts to Entrepreneurial Framework Conditions in Pakistan as compared to innovation driven economiesFigure 14 : Entrepreneurial attitudes in Pakistan (%age ALL respondents aged 18 -64 expressing an opinion and agreeing with the statement)Figure: 15 Entrepreneurial attitudes in Pakistan (%age MALE respondents aged 18 -64 expressing an opinion and agreeing with the statement)Figure 16: Entrepreneurial attitudes in Pakistan (%age FEMALE respondents aged 18 -64 expressing an opinion and agreeing with the statement)Figure 17: Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurship in various provinces

of Pakistan (Know someone personally who started a business in the past 2 years.)Figure 18: Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurship in various provinces

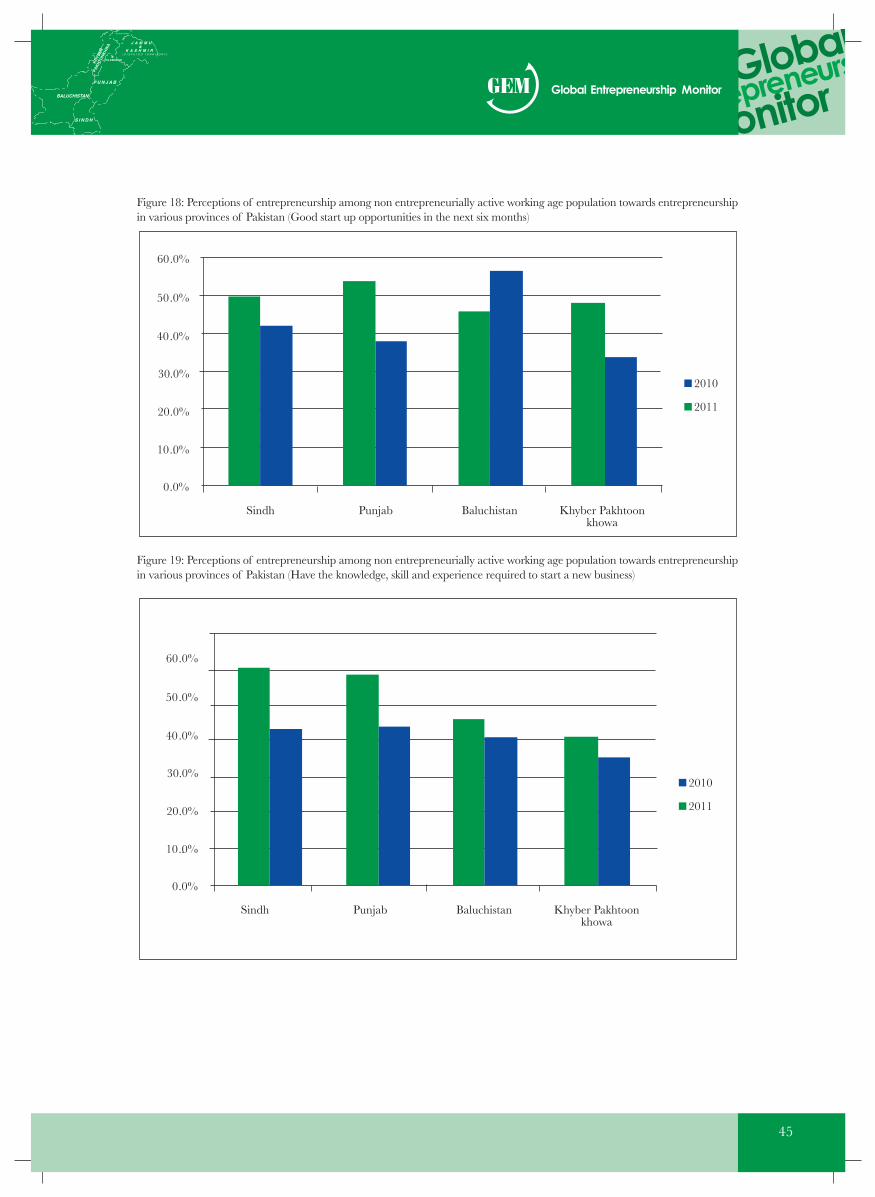

of Pakistan (Good start up opportunities in the next six months)Figure 19: Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurship in various provinces

of Pakistan (Have the knowledge, skill and experience required to start a new business)Figure 20: Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurship in various provinces

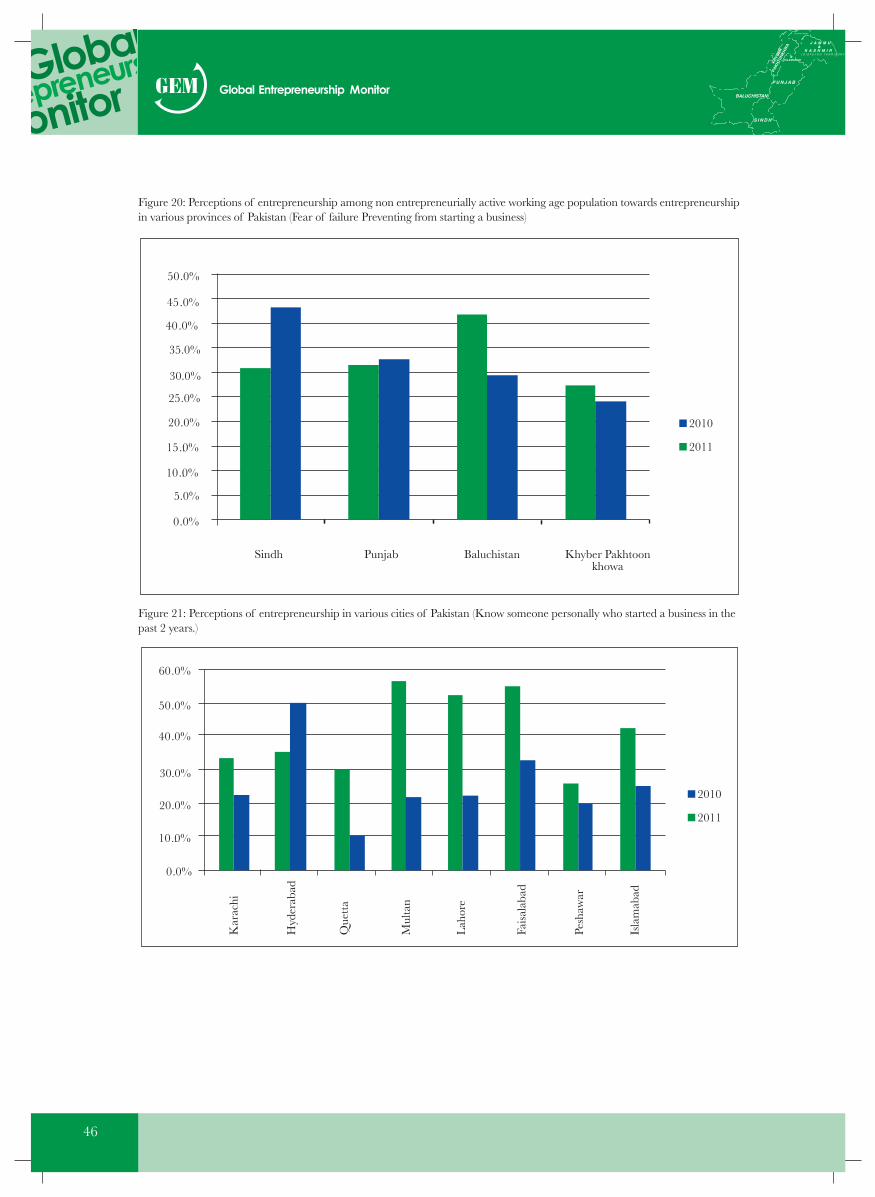

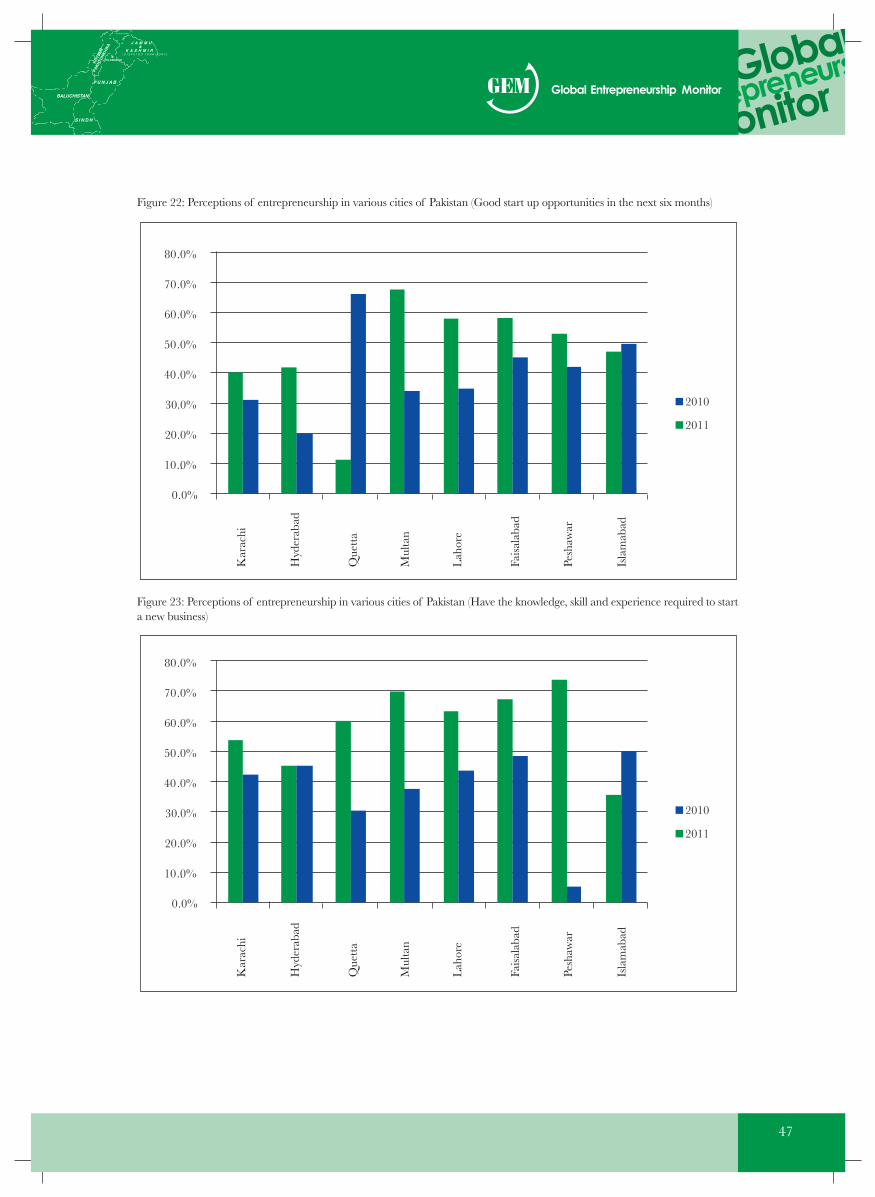

of Pakistan (Fear of failure Preventing from starting a business)Figure 21: Perceptions of entrepreneurship in various cities of Pakistan (Know someone personally who started a business in the past 2 years.)Figure 22: Perceptions of entrepreneurship in various cities of Pakistan (Good start up opportunities in the next six months)Figure 23: Perceptions of entrepreneurship in various cities of Pakistan (Have the knowledge, skill and experience required to start a new business)Figure 24 : Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurship in various provinces

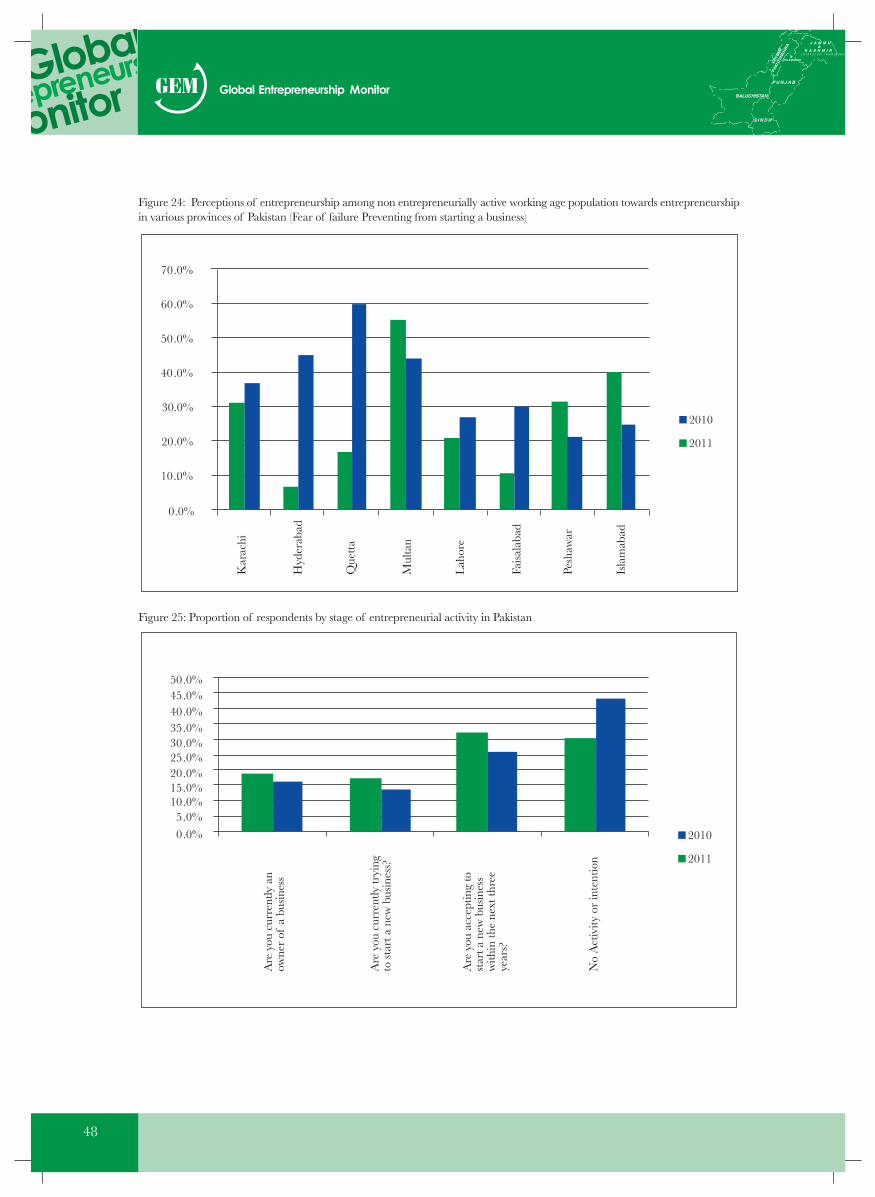

of Pakistan (Fear of failure preventing from starting a business)Figure 25: Proportion of respondents by stage of entrepreneurial activity in PakistanFigure 26: Different measures of entrepreneurial activity in various regions of Pakistan (Expects to start a business in the next 3 years (future))Figure 27: Different measures of entrepreneurial activity in various regions of Pakistan (Nascent Entrepreneurial Activity Rate (Actively involved in start-

up effort, owner, no wages yet))Figure 28: Different measures of entrepreneurial activity in various regions of Pakistan (New Business Owner-Manager Rate (Manages a business that is

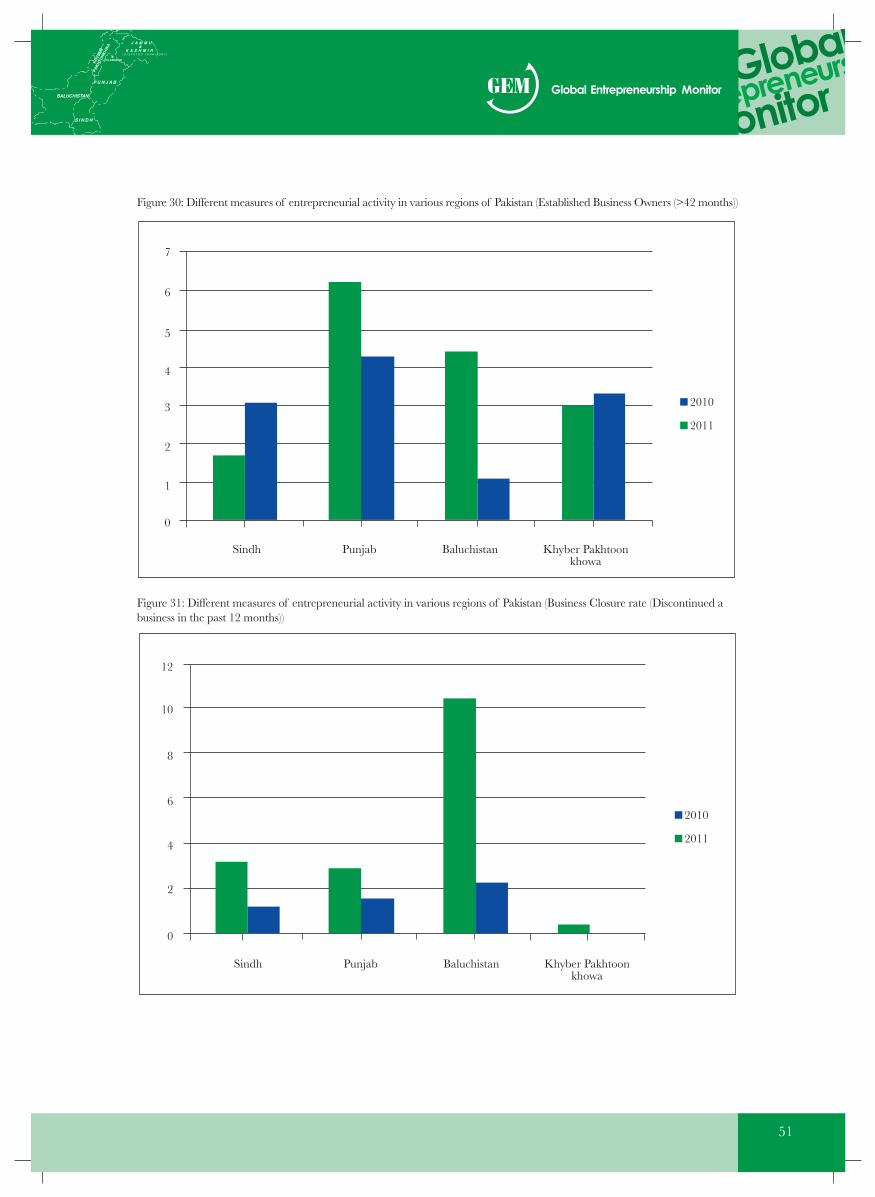

up to 42 months old))Figure 29: Different measures of entrepreneurial activity in various regions of Pakistan (Nascent + New Business Owner Manager Rate)Figure 30: Different measures of entrepreneurial activity in various regions of Pakistan (Established Business Owners (>42 months))Figure 31: Different measures of entrepreneurial activity in various regions of Pakistan (Business Closure rate (Discontinued a business in

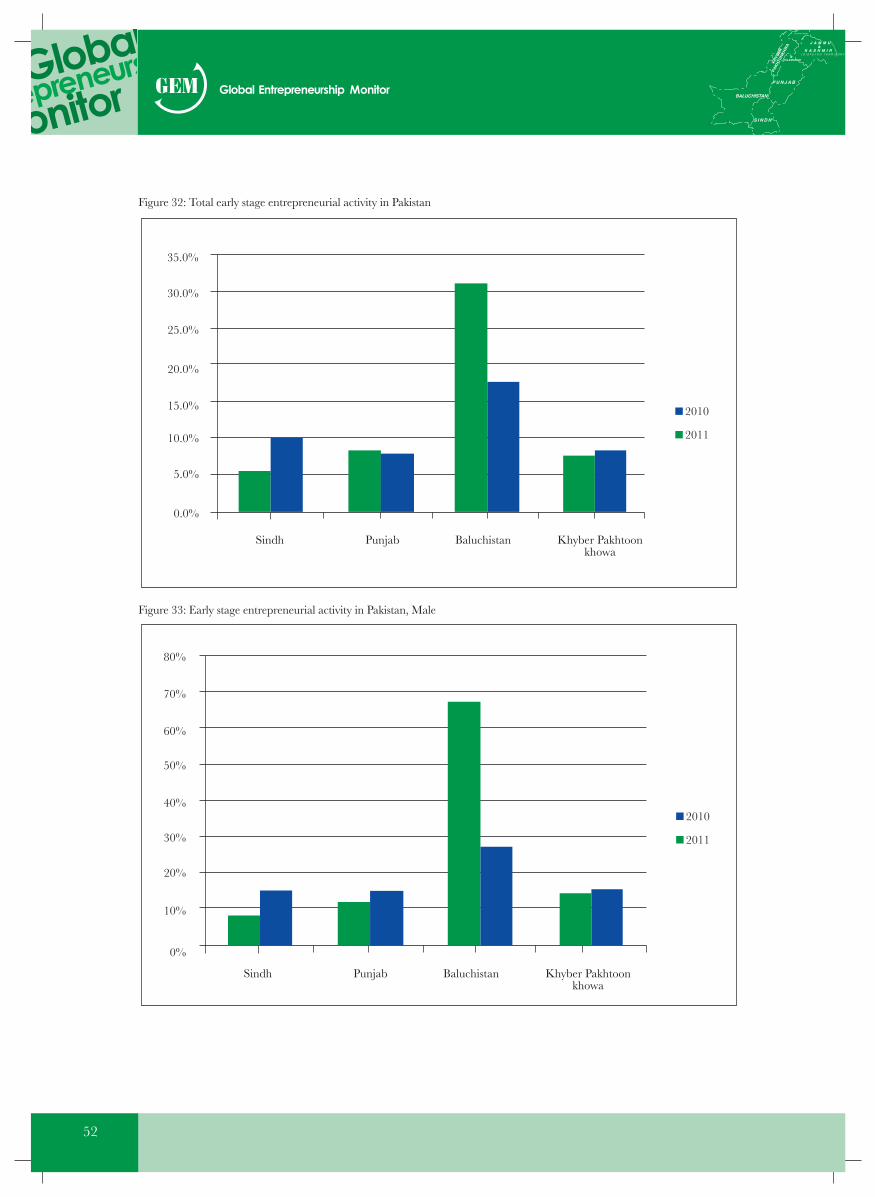

the past 12 months))Figure 32: Total early stage entrepreneurial activity in PakistanFigure 33: Early stage entrepreneurial activity in Pakistan, MaleFigure 34 : Early stage entrepreneurial activity in Pakistan, FemaleFigure 35: Total early stage Entrepreneurial Activity in Pakistan Regions based on opportunity entrepreneurship, MaleFigure 36: Total early stage Entrepreneurial Activity in Pakistan Regions based on opportunity entrepreneurship, FemaleFigure 37: Total early stage Entrepreneurial Activity in Pakistan Regions based on necessity entrepreneurship, MaleFigure 38: Total early stage Entrepreneurial Activity in Pakistan Regions based on necessity entrepreneurship, Female

LIST OF TABLES

Table 1: GEM 2011 Participating Countries Classified by Economy and GeographyTable 2A: Some general characteristics and entrepreneurship indicators of PakistanTable 2B: Comparison of various entrepreneurial characteristics and framework conditions of Pakistan with peer nationsTable 3: Attitudes towards Entrepreneurship in participating GEM Countries in 2011Table 4: Entrepreneurial Attitude in Pakistan: Respondents expressing the opinion and agreeing with the statementTable 5A: Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurship in various

provinces of PakistanTable 5B: Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurship in various

provinces of PakistanTable 6A: Perceptions of entrepreneurship in various cities of PakistanTable 6B: Perceptions of entrepreneurship in various cities of PakistanTable 7: Total early stage Entrepreneurial Activity in GEM participating countries in 2011Table 8: Measurement of entrepreneurial activity in GEM participating countries.Table 9: Proportion of respondents by stage of entrepreneurial activity in PakistanTable 10: Opportunity and Necessity Entrepreneurship in GEM Participating countriesTable 11: Total Early stage entrepreneurial activity by gender in Participating GEM CountriesTable 12: Established business ownership by genderTable 13: Different measures of entrepreneurial activity in various regions of PakistanTable 14: Total Early Stage Entrepreneurial Activity in Pakistani Regions in 2011Table 15A: Male and Female Total early stage Entrepreneurial Activity in Pakistani Regions, 2011Table 15B: Opportunity and Necessity Entrepreneurial Activity in Pakistani Regions, 2011Table 16: Male and Female Total early stage Entrepreneurial Activity in Pakistani Regions, 2011 based on opportunity entrepreneurshipTable 17: Male and Female Total early stage Entrepreneurial Activity in Pakistani Regions, 2011 based on necessity entrepreneurshipTable 18: Measures of entrepreneurial aspiration in GEM participating countries, 2011

02

We are living in a continuously changing and a dynamic world. The demographic, social, economical and technological changesare dramatically impacting the way we live, behave and act. The IT revolution and the internet are playing a pivotal role in thistransformation. We are witnessing the dawn of an entrepreneurial revolution in the entire world as more and more people getaccess to education and the internet.

With a shift towards creating the entrepreneurial economy, and increased calls for public-private partnerships to achieve this goal,the role of the government along with the private sector and the academic institutions is to create an environment and an ecosystem which favours and creates incentives for entrepreneurial activity. The role of the government has to go beyond the traditionaleconomic rational of relying on the existence of market failures and distortions, but rather, intervening so that these market failuresand distortions do not negatively impact on the entrepreneurial society. The academic institutions have to play an important roleof educating the youth of the country and to develop an entrepreneurial mindset.

Pakistan's estimated population in 2011 is over 187 million making it the world's sixth most-populous country, behind Brazil andahead of Bangladesh. During 1950-2011, Pakistan's urban population expanded over sevenfold, while the total population increasedby over fourfold. The structure of the population pyramid has changed a lot in the past decade as the base of the pyramid hasbecome very heavy. 140 million of the population is between the age 0 to 40 and there are about 80 million people in the agebracket of 15 to 40 years.

Although this seems to be a great challenge but it can be converted in to a great opportunity. The Pakistani nation has the Godgifted ability to be entrepreneurial. SMEs constitute nearly 90% of all the enterprises in Pakistan; employ 80% of the non-agricultural labor force; and their share in the annual GDP is 40%, approximately. The industrial belt of Gujranwala, Sialkot isfamous for its entrepreneurial spirit and the contribution to the Pakistani economy. The textile based SMEs are the back bone ofthe economy. I consider entrepreneurship a panacea for a developing country like Pakistan, which has one of the highest populationgrowth rates with the highest number of youth population. It is high time that the government, politicians, the business community,academic institutions and other stake holders join hands in promoting entrepreneurship.

I congratulate the GEM Pakistan Team on the completion of this second GEM research cycle. I am confident that the researchfindings will help our policy makers, researchers and educators in Pakistan to create awareness and enhance learning about theentrepreneurial process with the aim of creating new opportunities for our aspiring entrepreneurs by improving support for newand innovative business ventures.

Dr. Ishrat HusainDean and DirectorIBA, Karachi

FOREWORD

03

On behalf of our GEM Pakistan team, I am pleased to launch the second national Global Entrepreneurship Monitor researchreport based on the 2011 data collection cycle. While, we are celebrating the completion of this second cycle of our researchproject, we are mindful of IBA's strong commitment to entrepreneurship and sponsorship of the GEM Project. For this, I amespecially indebted to Dr. Ishrat Husain, Dean and Director IBA for his leadership and faith in Pakistan's entrepreneurial developmentthat made it possible despite numerous challenges. We are equally grateful to those institutions which provided financial supportover the last two consecutive research cycles: besides IBA, the USAID contributed in the form of paying the project fee and sometravel for which I would like to thank them for the assistance. On behalf of the GEM Pakistan 2011 team, I also wish to thankall those national experts and adult survey respondents who spared their valuable time for interviews and answered our questions(Appendix 3 provides a list of our NES experts).

OASIS Insights played a key role as our APS vendor by collecting data from more than two thousand adult respondents from allover Pakistan - their professionalism and timely completion of the survey is appreciated.

I would like to take this opportunity to recognize my GEM Pakistan 2011 Team colleagues Dr. Shahid Qureshi, and Mr. ZafarSiddiqui of the Center for Entrepreneurial Development at IBA. Dr Qureshi who is the Co-Principal Investigator of this projectsupervised the Adult Population Survey, was responsible for data analysis and co-authored this report with me. Mr. Siddiqui helpedin fund raising and assisted in managing the report launch function. I am thankful to both for this crucial support. Mr. Moid Sultanand Mr. Jehanzeb of IBA's Accounts and Finance Department were always available for help that made our work easier and wethank them for the assistance.

The research associates at CED, Mr. Waleed Wasti and Shaheer Kazmi contributed a lot in the NES and report preparation.

I would also like to thank the members of the IBA led consortium of universities who have contributed financially for the nextGEM 2012 cycle. Special thanks are for Syed Ali Akbar Rizvi, Director Centre for Entrepreneurship, IBA Sukkur, Akhtar AliQureshi, General Manager "Centre for Innovation & Entrepreneurship (CIE)" Centre for Innovation & Entrepreneurship (CIE),NUST Islamabad, Mr. Asif Shah, Director Incubator UET Peshawar and Nadeem Mustafa, Head of GIFT Business School,GIFT University Gujranwala.

Finally, I would like to express my appreciation to Dr. Mike Herrington, Dr. Niels Bosma, Ms. Marcia Cole, Mr. Chris Aylett, Ms.Yana Litovsky, Dr. Alicia Coduras, Dr. Jeff Seaman and Ms. Ingrid Blake, all of the Global GEM Project Management Team fortheir continued encouragement and support of our GEM Pakistan project.

Sincerely,

Sarfraz A. Mian, PhDHead and PI,GEM Pakistan Team

ACKNOWLEDGEMENTS

04

EXECUTIVE SUMMARY1. In 2011, the Global entrepreneurship monitor (GEM) research consortium measured entrepreneurial activity of individuals

in 54 member economies, making it the world's most authoritative comparative study of entrepreneurial activity in the generaladult population. Two thousand adults aged 18-64 participated in the GEM Pakistan Survey in 2011.

2. This national monitoring report compares global entrepreneurship monitor (GEM) measures of various entrepreneurialcharacteristics (attitudes, aspirations, and activities) in Pakistan and other participating countries. It also summarizes theseentrepreneurial characteristics within various regions and cities of Pakistan. It examines the views of entrepreneurs on theimpact of recent global recession on their own businesses. It also reports expert views on the environment for entrepreneurshipin Pakistan and compares these with other GEM nations.

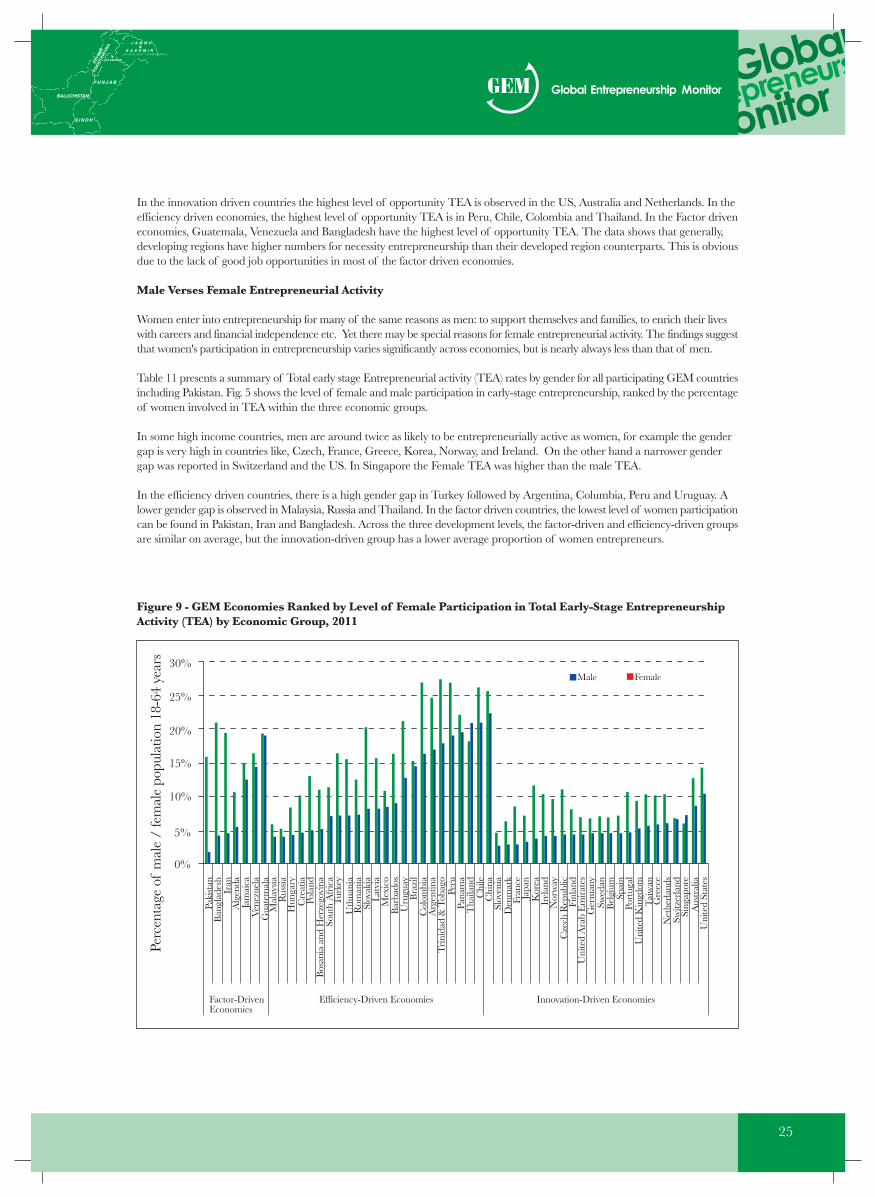

3. The number of people in Pakistan who have a positive attitude towards entrepreneurship is less than the average of its factor- driven peer countries. However it is higher than the average figures of innovation driven economies. Moreover the malepopulation has a more positive attitude towards entrepreneurship in Pakistan as compared to the female population.

4. Within Pakistan, the residents of Sindh and Baluchistan have a higher favorable attitude towards entrepreneurship andperceive more opportunities in the near future. Among the major cities, the residents of Islamabad, Hyderabad and Faisalabadhave a more positive perception of entrepreneurial opportunities in the future and perceive to have the highest level of skillset, knowledge and experience to start an entrepreneurial venture as compared to other major cities of Pakistan.

5. Total early stage Entrepreneurial Activity or TEA rate (the sum of the nascent entrepreneurship rate and the new businessmanager rate) in Pakistan was 9.07 %. This is lower than the average TEA rates for the factor driven economies (1 4.22 %)and efficiency driven economies (13.8 %). However this is greater than the average TEA rate of Innovation driven economies(6.92 %).

6. The TEA is classified into two types i.e. opportunity based TEA and necessity based TEA. About 4% of Pakistanis wereinvolved in opportunity based early stage entrepreneurial activity. This rate is considerably less than the average of factordriven (8.5%) and efficiency driven countries (9.05%).

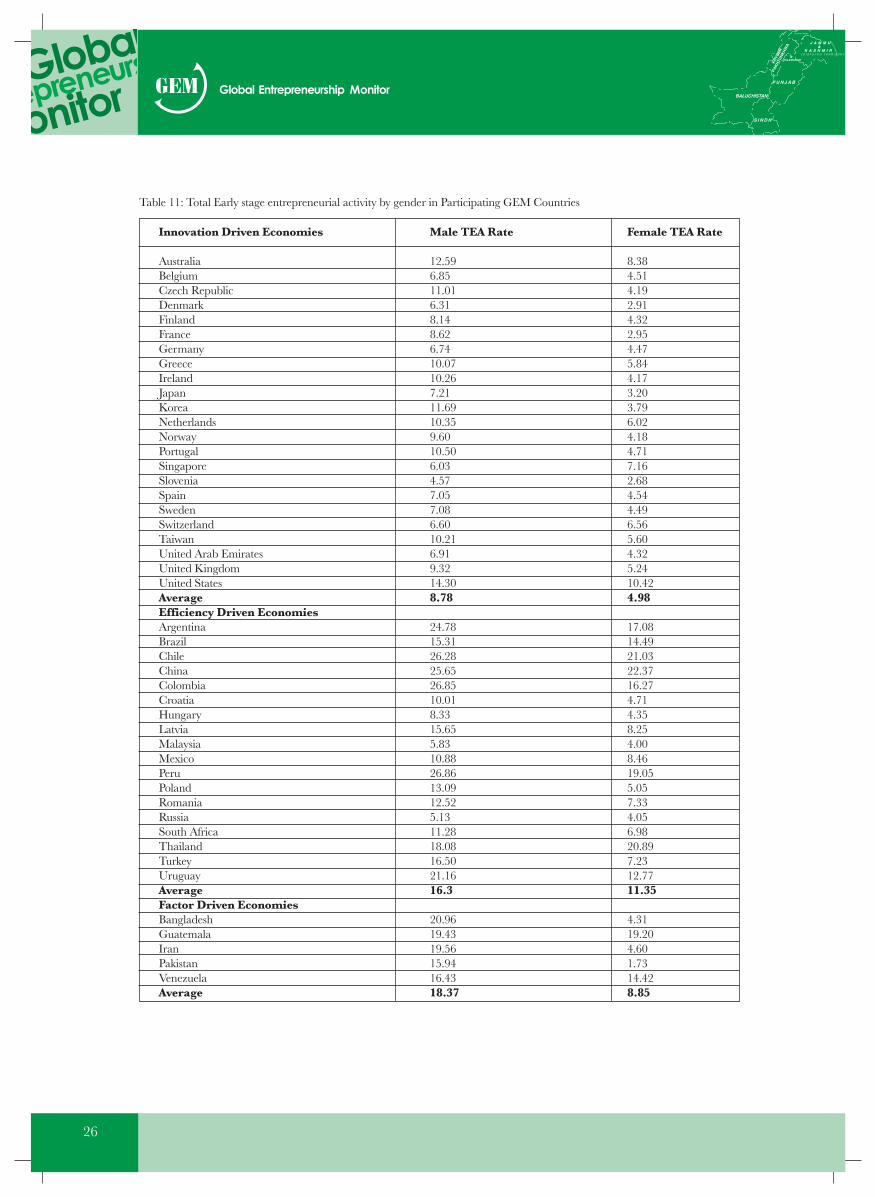

7. The male TEA rate in Pakistan is more than eight times that of the female TEA rate. The gender gap is pretty high ascompared to other factor and efficiency driven countries.

8. The Established Business Ownership (EBO) rate in Pakistan was 4.08 %. This is lower than the average EBO rates forPakistan's peer factor driven economies (6.20 %), as well as efficiency driven (7.5 4 %) and innovation driven (7.22 %)economies

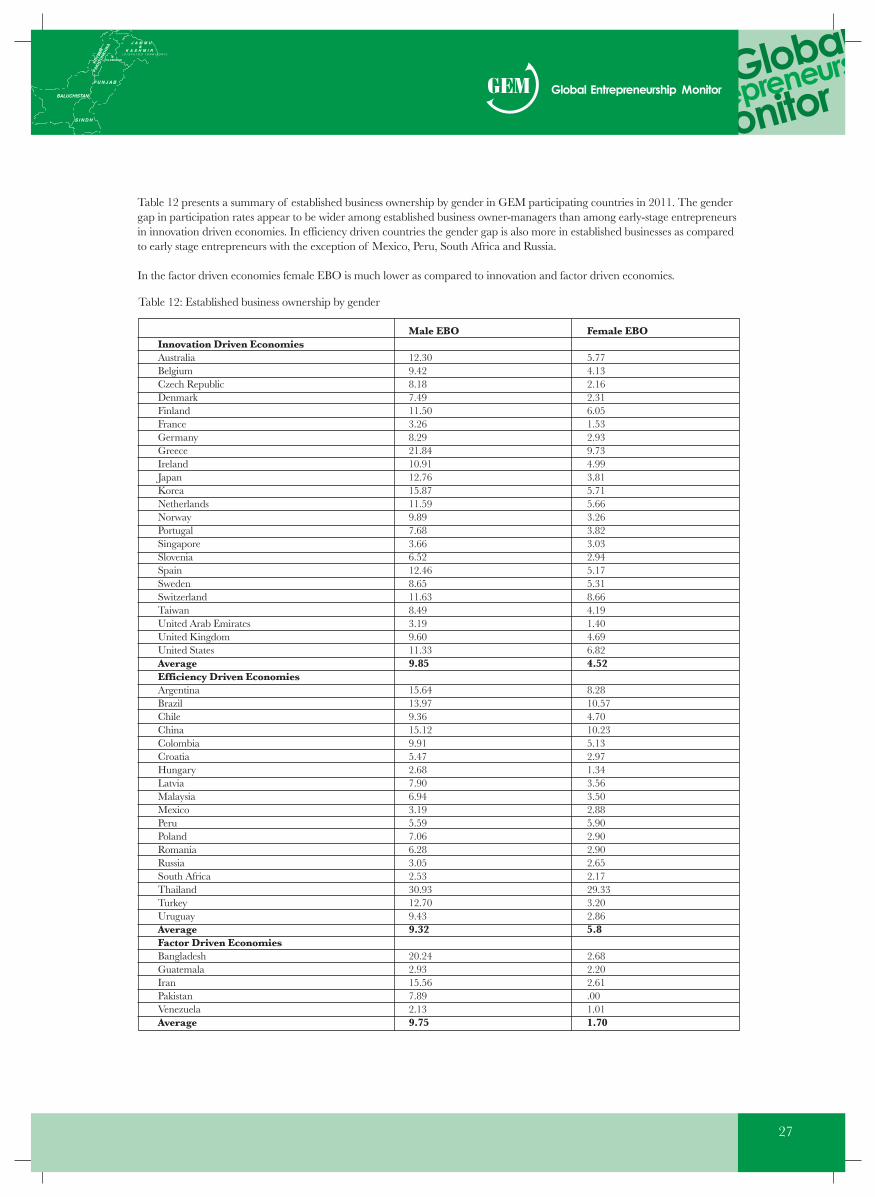

9. The male Established Business Ownership (EBO) rate in Pakistan is almost 8 times that of female EBO rate. This shows thatthe gender gap in EBO is also very high as compared to other factor, efficiency and innovation driven countries.

10. When surveyed, 9.07 % of the adult population in Pakistan was trying to start a business (nascent entrepreneurs) was lowerthan the average of factor-driven economy nations (1 4.2%), compared to 14.5% in Iran, 11.87% in Turkey and 23% inChile.

11. According to the survey, Pakistani population's new business ownership rate (owner managers of a business that was between3 to 42 months old) was 1.7%. This rate is considerably less than the average of factor driven (4.88 %), efficiency driven(6.09%) and innovation driven economies rate (2.7 %)

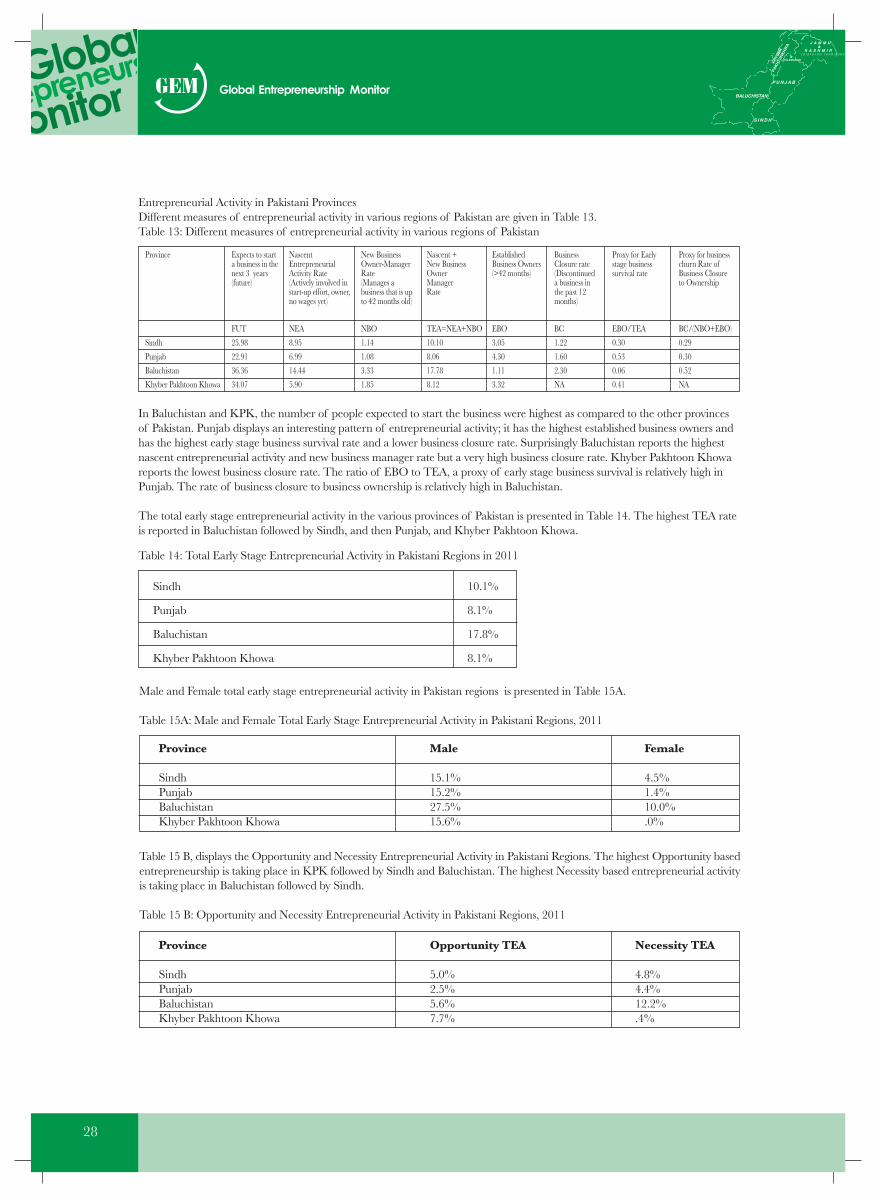

12. Entrepreneurial activity in various Pakistani regions is found to be as follows. Baluchistan has the highest rate of activeinvolvement in startup effort and at the same time has the highest business closure rate. Punjab has the highest rate ofestablished business owners (4.3) and Baluchistan and KPK has the highest rate of expectations to start a business in the nextthree years.

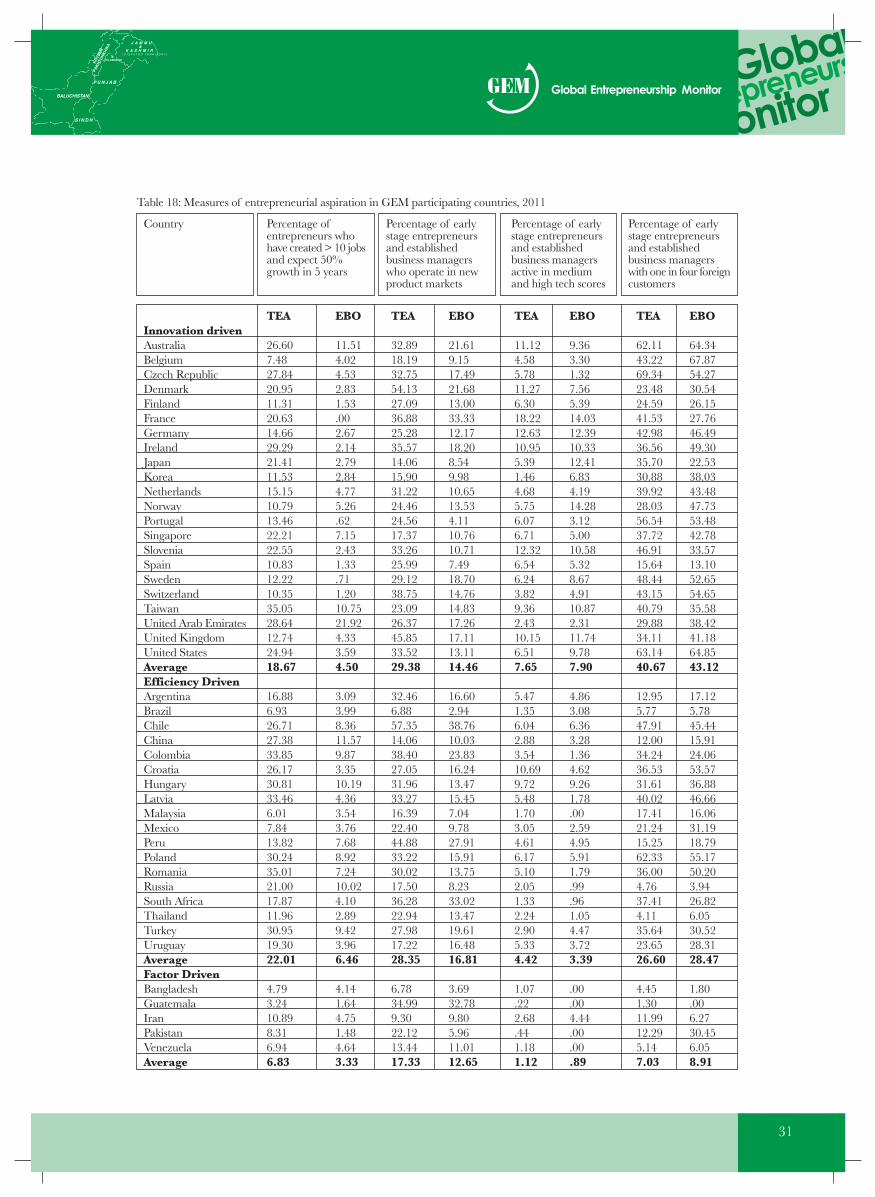

13. In Pakistan early stage entrepreneurs and business managers have low aspirations to grow as compared to most other GEMparticipating countries. The proportion of early stage Pakistani entrepreneurs reporting new product/market combinationsand with at least 25% foreign customers is (12.29) above the average of factor driven countries.

14. In Pakistan 31.19% of the total working age population (including those entrepreneurially active) expressed opinion that fearof failure would prevent them from starting a business. The fear of failure in the Pakistani population is less than the averageof the factor driven economies.

15. Experts on entrepreneurship in Pakistan gave government programs significantly lower ratings than the factor and efficiencydriven countries. Cultural and social norms were also more negative for entrepreneurship in Pakistan than the other factorand efficiency driven countries

05

CHAPTER 1: INTRODUCTIONAND BACKGROUND

06

1.1 Study Introduction

After our first GEM Pakistan 2010 study, a year ago, this report provides the results of Pakistan's second national survey of variousentrepreneurial characteristics studied under the Global Entrepreneurship Monitor (GEM) program. This grass-roots researchprogram is aimed at better comprehending the dynamics of national/local entrepreneurship context by measuring attitudes,activities and aspirations of adult individuals participating in different phases of entrepreneurship. There is an ever increasingevidence of the use of GEM data and its research findings in policy making at all levels of government and academia in orderto promote entrepreneurship in member nations.

The GEM project is implemented through the collaborative efforts of participating national teams and is coordinated by the GlobalGEM consortium. According to the research design, each GEM national team conducts its adult population survey (APS) alongwith a national expert survey (NES) and the data are harmonized allowing national comparisons of the key entrepreneurialdimensions. The last GEM 2011 Global Report summarizing this world-wide data gathering and research activity of 54 nationalteams including Pakistan was released earlier in January 2011 (see www.gemconsortium.org).

Pakistan joined GEM in 2010 under the sponsorship of IBA Karachi and undertook its first GEM study in the summer of 2010.The second study was conducted in the late summer of 2011. Every effort was made to ensure data quality and reliability ofresults, for which necessary weights were calculated (see Appendix 2) to address representativeness of the sample along genderand urban-rural lines. This report focuses on Pakistan specific findings providing necessary analyses and benchmarking with thepeer and other advanced nations. The work is intended to create public awareness, promote research and aid policymakers ofPakistan in identifying and helping to address the underlying issues impeding entrepreneurial growth by formulating enablingpolicies and support programs to enhance entrepreneurship in the nation.

1.2 Overview of the GEM Program and Research Model1

Founded in late 1990s2 , GEM program is administered by the Global Entrepreneurship Research Association (GERA), a not-for-profit body of academic researchers from prominent business schools across the globe. Over the last 12 years of its inceptionthe program has experienced phenomenal growth to include over 80 countries most of whom conduct their national GEM surveysevery year.

GEM focuses on three main objectives:

● To measure differences in entrepreneurial attitudes, activity and aspirations among nations.● To uncover factors determining the nature and level of national entrepreneurial activity.● To identify policy implications for enhancing entrepreneurship in an economy.

GEM is based on the following premises. First, an economy's prosperity is highly dependent on a dynamic entrepreneurship sector.This is true across all stages of development. Yet the nature of this activity can vary in character and impact. Necessity-drivenentrepreneurship, particularly in less developed regions or those experiencing job losses, can help an economy benefit from self-employment initiatives when there are fewer work options available. More developed economies, on the other hand, can leveragetheir wealth and innovation capacity, yet they also offer more employment options to attract those that might otherwise becomeentrepreneurs. In order to maintain their entrepreneurial dynamism they need to instill more opportunity-based motives.

Second, an economy's entrepreneurial capacity requires individuals with the ability and motivation to start businesses, and positivesocietal perceptions about entrepreneurship. Entrepreneurship should include participation from all groups in society, includingwomen, a range of age groups and education levels and disadvantaged populations. Finally, high-growth entrepreneurship is akey contributor to new employment in an economy, and national competitiveness depends on innovative and cross-borderentrepreneurial ventures.

GEM MeasuresAt the time of GEM's founding, traditional analyses of economic growth and competitiveness had, for the most part, neglectedthe role played by new and small firms in national economies, due, in some measure, to the lack of good data on this sector. Thisinformation, when available, tended to be present in only those countries at the most advanced stages of economic development.Existing measures, such as self-employment rates, did not reflect the dynamic scope of entrepreneurship. And while most governments

have long maintained records of formal business registrations, it wasn't until GEM emerged that an accurate picture could bedrawn of the entrepreneurially conscious people, and how many of them are actually involved in businesses in different cornersof the world started.

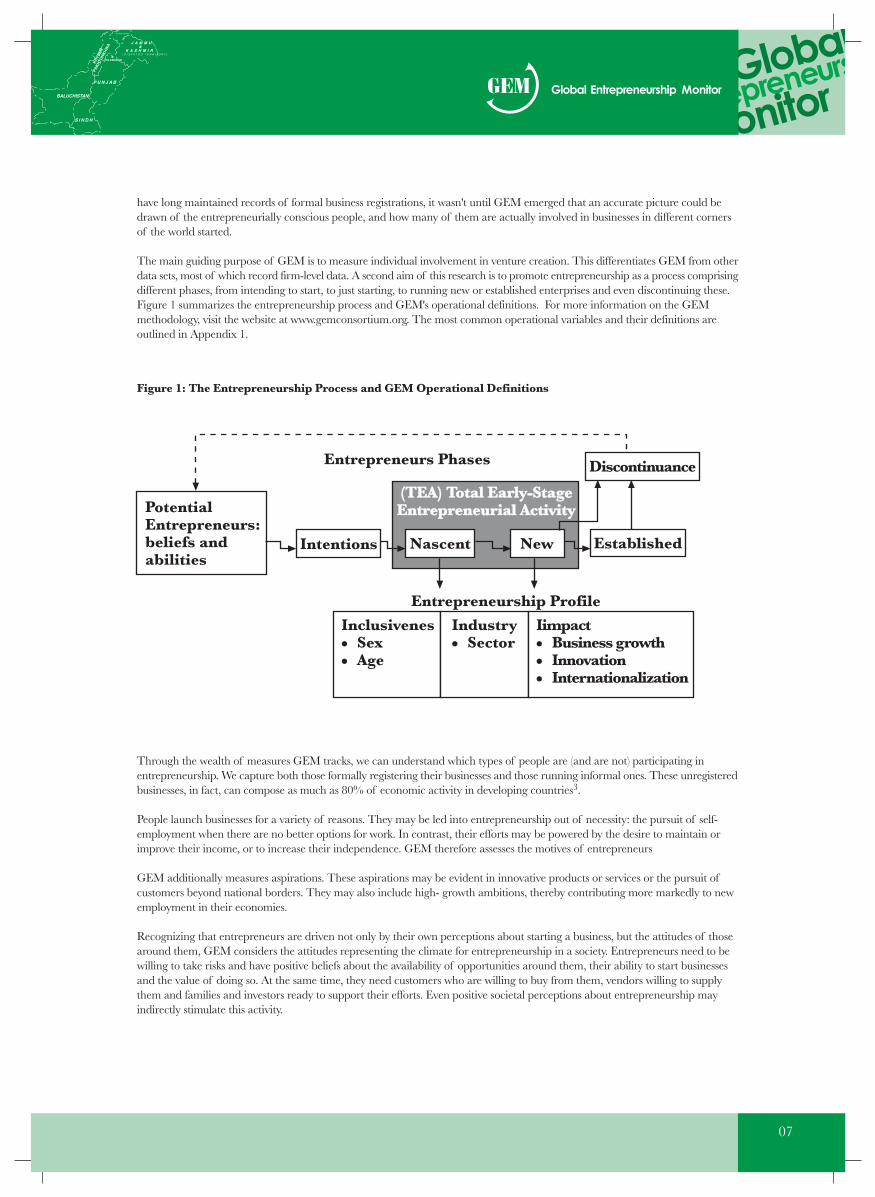

The main guiding purpose of GEM is to measure individual involvement in venture creation. This differentiates GEM from otherdata sets, most of which record firm-level data. A second aim of this research is to promote entrepreneurship as a process comprisingdifferent phases, from intending to start, to just starting, to running new or established enterprises and even discontinuing these.Figure 1 summarizes the entrepreneurship process and GEM's operational definitions. For more information on the GEMmethodology, visit the website at www.gemconsortium.org. The most common operational variables and their definitions areoutlined in Appendix 1.

Through the wealth of measures GEM tracks, we can understand which types of people are (and are not) participating inentrepreneurship. We capture both those formally registering their businesses and those running informal ones. These unregisteredbusinesses, in fact, can compose as much as 80% of economic activity in developing countries3.

People launch businesses for a variety of reasons. They may be led into entrepreneurship out of necessity: the pursuit of self-employment when there are no better options for work. In contrast, their efforts may be powered by the desire to maintain orimprove their income, or to increase their independence. GEM therefore assesses the motives of entrepreneurs

GEM additionally measures aspirations. These aspirations may be evident in innovative products or services or the pursuit ofcustomers beyond national borders. They may also include high- growth ambitions, thereby contributing more markedly to newemployment in their economies.

Recognizing that entrepreneurs are driven not only by their own perceptions about starting a business, but the attitudes of thosearound them, GEM considers the attitudes representing the climate for entrepreneurship in a society. Entrepreneurs need to bewilling to take risks and have positive beliefs about the availability of opportunities around them, their ability to start businessesand the value of doing so. At the same time, they need customers who are willing to buy from them, vendors willing to supplythem and families and investors ready to support their efforts. Even positive societal perceptions about entrepreneurship mayindirectly stimulate this activity.

07

Figure 1: The Entrepreneurship Process and GEM Operational Definitions

PotentialEntrepreneurs:beliefs andabilities

Entrepreneurs Phases Discontinuance

Established

(TEA) Total Early-StageEntrepreneurial Activity

Intentions

Entrepreneurship Profile

Inclusivenes● Sex● Age

Industry● Sector

Iimpact● Business growth● Innovation● Internationalization

Nascent New

Economic Development Level and Entrepreneurship

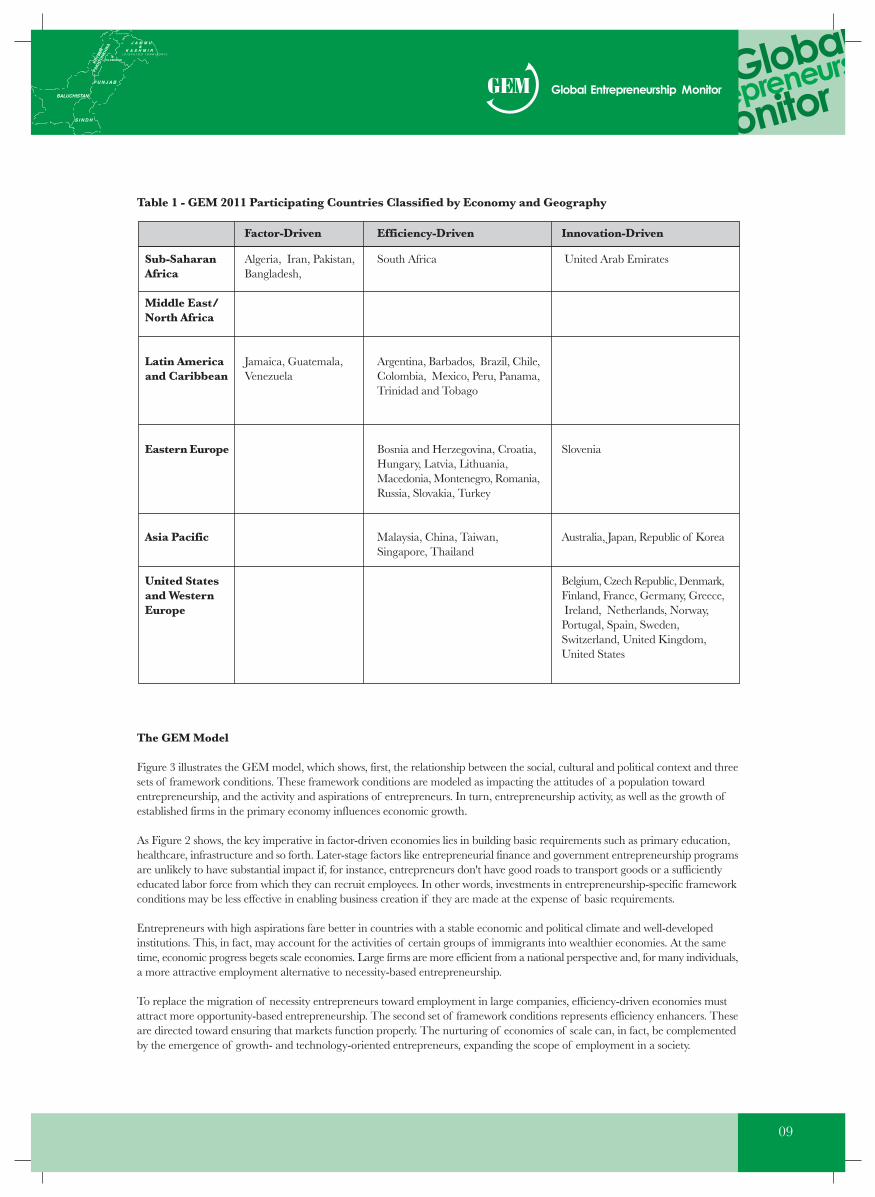

GEM's harmonized dataset enables comparisons of entrepreneurship activity around the globe, and within and across geographicregions. This report additionally examines groups of economies at similar development levels. Following a typology used by theWorld Economic Forum, GEM classifies the 54 GEM participants as “factor-driven,” “efficiency-driven” or “innovation-driven”economies4.

Figure 2 illustrates the characteristics of these economic groups and the key development focus at each level. As an economydevelops, productivity increases and, consequently, so does per capita income. This is often accompanied by the migration of laboracross different economic sectors. For example, labor may move from agricultural and extractive sectors to manufacturing, andthen eventually to services5. In their early stages of development, economies typically have a higher proportion of necessity-drivenactivities. Here, the demand for jobs in high-productivity sectors outpaces supply. As a result, many people must create their ownsource of income.

With further development comes the growth of productive sectors. This increases employment capacity but leads to gradual declinesin the level of necessity-driven entrepreneurship. At the same time, improvements in wealth and infrastructure stimulate opportunity-based businesses, shifting the nature of entrepreneurship activity. These ventures are more likely associated with greater aspirationsfor growth, innovation and internationalization. They rely, however, on the economic and financial institutions created during thedeveloping phases. To the extent these institutions are able to accommodate and support opportunity-seeking entrepreneurshipactivity; innovative entrepreneurial firms may emerge as significant drivers of economic growth and wealth creation6.

GEM additionally considers geographic factors, grouping countries into six geographic regions: sub-Saharan Africa, the MiddleEast and North Africa (MENA), Latin America and the Caribbean, Eastern Europe, Asia/Pacific and the United States andWestern Europe. With both groupings, we can compare economies across similar development levels and geographic locations.The economic and geographic groupings of the 54 participating countries are shown in Table 1.

Factor-DrivenEconomies

Efficiency-DrivenEconomies

Innovation-DrivenEconomies

From subsistenceagriculture to extraction ofnatural resources, creatingregional scale-intensiveagglomerations.

Increased industrializationand economies of scale.Large firms dominate, butsupply chain niches openup for small and mediumenterprises.

R&D, knowledge intensity,and expanding servicessector. Greater potentialfor innovativeentrepreneurial activity.

Basic Requirements Efficiency Enhancers Entrepreneurship & Innovation Conditions

Figure 2 - Characteristics of Economic Groups and Key Development Focus

08

Sub-SaharanAfrica

Middle East/North Africa

Latin Americaand Caribbean

Eastern Europe

Asia Pacific

United Statesand WesternEurope

09

Table 1 - GEM 2011 Participating Countries Classified by Economy and Geography

The GEM Model

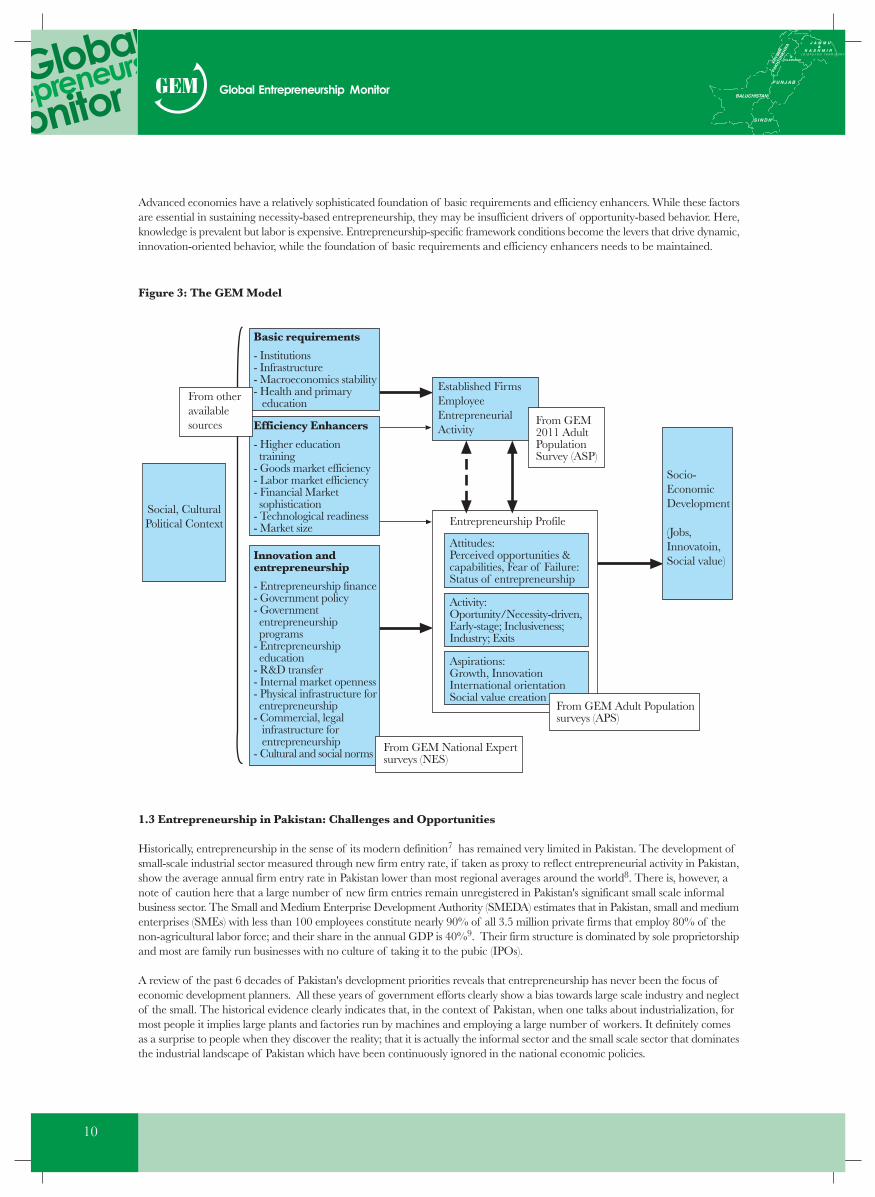

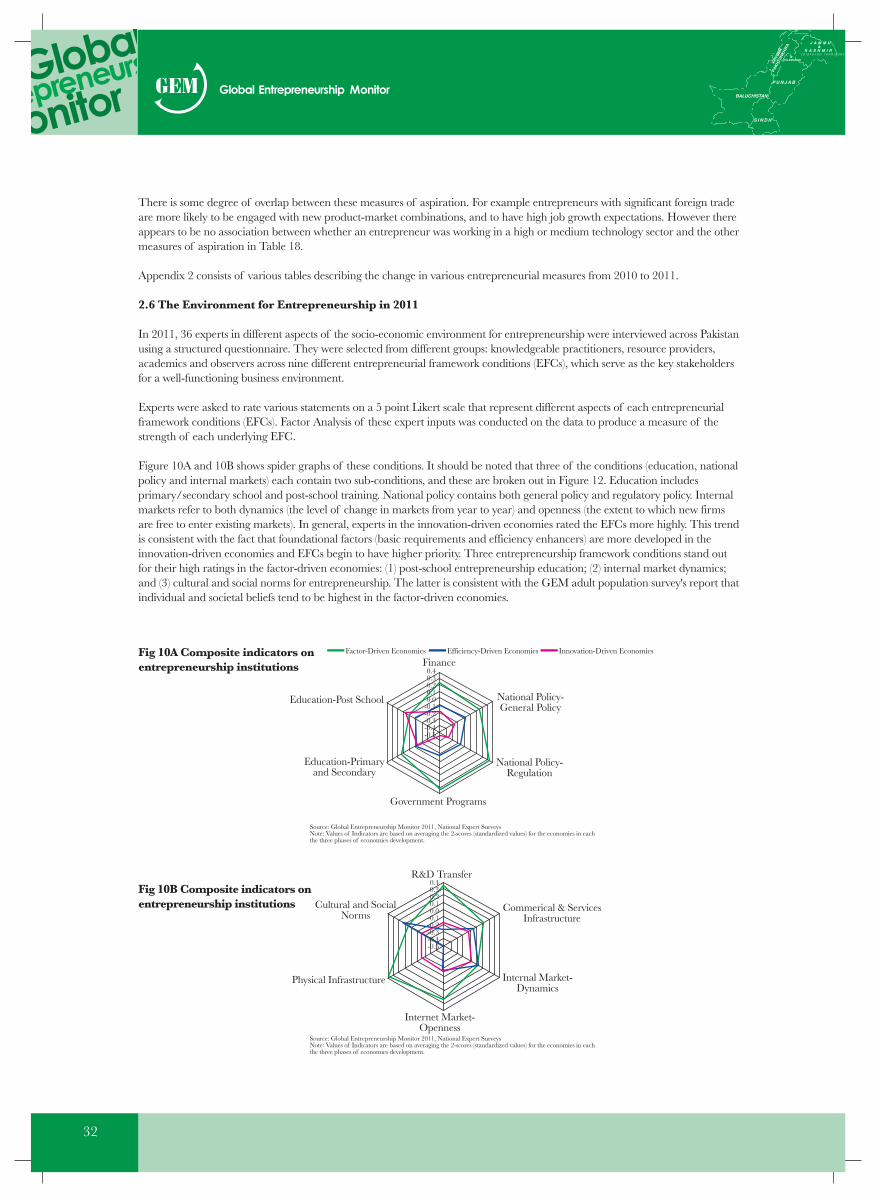

Figure 3 illustrates the GEM model, which shows, first, the relationship between the social, cultural and political context and threesets of framework conditions. These framework conditions are modeled as impacting the attitudes of a population towardentrepreneurship, and the activity and aspirations of entrepreneurs. In turn, entrepreneurship activity, as well as the growth ofestablished firms in the primary economy influences economic growth.

As Figure 2 shows, the key imperative in factor-driven economies lies in building basic requirements such as primary education,healthcare, infrastructure and so forth. Later-stage factors like entrepreneurial finance and government entrepreneurship programsare unlikely to have substantial impact if, for instance, entrepreneurs don't have good roads to transport goods or a sufficientlyeducated labor force from which they can recruit employees. In other words, investments in entrepreneurship-specific frameworkconditions may be less effective in enabling business creation if they are made at the expense of basic requirements.

Entrepreneurs with high aspirations fare better in countries with a stable economic and political climate and well-developedinstitutions. This, in fact, may account for the activities of certain groups of immigrants into wealthier economies. At the sametime, economic progress begets scale economies. Large firms are more efficient from a national perspective and, for many individuals,a more attractive employment alternative to necessity-based entrepreneurship.

To replace the migration of necessity entrepreneurs toward employment in large companies, efficiency-driven economies mustattract more opportunity-based entrepreneurship. The second set of framework conditions represents efficiency enhancers. Theseare directed toward ensuring that markets function properly. The nurturing of economies of scale can, in fact, be complementedby the emergence of growth- and technology-oriented entrepreneurs, expanding the scope of employment in a society.

Algeria, Iran, Pakistan,Bangladesh,

Jamaica, Guatemala,Venezuela

South Africa

Argentina, Barbados, Brazil, Chile,Colombia, Mexico, Peru, Panama,Trinidad and Tobago

Bosnia and Herzegovina, Croatia,Hungary, Latvia, Lithuania,Macedonia, Montenegro, Romania,Russia, Slovakia, Turkey

Malaysia, China, Taiwan,Singapore, Thailand

United Arab Emirates

Slovenia

Australia, Japan, Republic of Korea

Belgium, Czech Republic, Denmark,Finland, France, Germany, Greece, Ireland, Netherlands, Norway,Portugal, Spain, Sweden,Switzerland, United Kingdom,United States

Factor-Driven Efficiency-Driven Innovation-Driven

Advanced economies have a relatively sophisticated foundation of basic requirements and efficiency enhancers. While these factorsare essential in sustaining necessity-based entrepreneurship, they may be insufficient drivers of opportunity-based behavior. Here,knowledge is prevalent but labor is expensive. Entrepreneurship-specific framework conditions become the levers that drive dynamic,innovation-oriented behavior, while the foundation of basic requirements and efficiency enhancers needs to be maintained.

1.3 Entrepreneurship in Pakistan: Challenges and Opportunities

Historically, entrepreneurship in the sense of its modern definition7 has remained very limited in Pakistan. The development ofsmall-scale industrial sector measured through new firm entry rate, if taken as proxy to reflect entrepreneurial activity in Pakistan,show the average annual firm entry rate in Pakistan lower than most regional averages around the world8. There is, however, anote of caution here that a large number of new firm entries remain unregistered in Pakistan's significant small scale informalbusiness sector. The Small and Medium Enterprise Development Authority (SMEDA) estimates that in Pakistan, small and mediumenterprises (SMEs) with less than 100 employees constitute nearly 90% of all 3.5 million private firms that employ 80% of thenon-agricultural labor force; and their share in the annual GDP is 40%9. Their firm structure is dominated by sole proprietorshipand most are family run businesses with no culture of taking it to the pubic (IPOs).

A review of the past 6 decades of Pakistan's development priorities reveals that entrepreneurship has never been the focus ofeconomic development planners. All these years of government efforts clearly show a bias towards large scale industry and neglectof the small. The historical evidence clearly indicates that, in the context of Pakistan, when one talks about industrialization, formost people it implies large plants and factories run by machines and employing a large number of workers. It definitely comesas a surprise to people when they discover the reality; that it is actually the informal sector and the small scale sector that dominatesthe industrial landscape of Pakistan which have been continuously ignored in the national economic policies.

Figure 3: The GEM Model

From otheravailablesources

Social, CulturalPolitical Context

Basic requirements

- Institutions- Infrastructure- Macroeconomics stability- Health and primary education

Efficiency Enhancers

- Higher education training- Goods market efficiency- Labor market efficiency- Financial Market sophistication- Technological readiness- Market size

Innovation andentrepreneurship

- Entrepreneurship finance- Government policy- Government entrepreneurship programs- Entrepreneurship education- R&D transfer- Internal market openness- Physical infrastructure for entrepreneurship- Commercial, legal infrastructure for entrepreneurship- Cultural and social norms

Attitudes:Perceived opportunities &capabilities, Fear of Failure:Status of entrepreneurship

Activity:Oportunity/Necessity-driven,Early-stage; Inclusiveness;Industry; Exits

Aspirations:Growth, InnovationInternational orientationSocial value creation

Entrepreneurship Profile

From GEM Adult Populationsurveys (APS)

Established FirmsEmployeeEntrepreneurialActivity

Socio-EconomicDevelopment

(Jobs,Innovatoin,Social value)

From GEM National Expertsurveys (NES)

10

From GEM2011 AdultPopulationSurvey (ASP)

11

As stated above, generally, the development of small-scale sector reflected the characteristics of entrepreneurship however thissector had largely grown up as an informal sector. The informal small scale sector has dominated employment in the construction,wholesale, retail trading, hotels, transport, communications and storage industries in urban areas. Some of the issues faced by thesmall and medium size firms located in different SME clusters in Pakistan are reported as follows10.

● Small businesses face a complex legal, tax and administrative environment in Pakistan therefore most firms avoided theeconomic obligations associated with the registered status.

● Entrepreneurs generally are not tuned to conducting R&D as they believed that the high cost of production and narrowmargins did not give them the leverage to go for R&D. Major rationale behind the high cost included high utility prices andminimum wage fixed by government. Another reason of lack of focus on R&D was the nature of industry, which was skillbased (imitation) rather than the knowledge based. Nevertheless, research was being undertaken to explore new markets basedon personal visits of entrepreneurs either privately or in some cases in groups sent out by the government organizations topromote trade.

● The small businessman, by and large, expected from the government to provide incentives and subsidies, given the rent-seeking culture that has now been established, businessmen, instead of focusing on their own innovation, expected help fromthe government most of the times.

● Businesses remained largely owner-operated and resistant to developing professionalmanagement, as the business growth was traditionally dependent on policy favors rather than on professional managementand strategy. Moreover, in clusters, there was no expertise for providing practical advice on key areas such as project feasibility,business operations, brand establishment and marketing. Given the lack of market depth, input from research institutions,universities and other forms of specialized knowledge, knowledge spillovers remained narrow and imitative.

● Scarcity of skilled labor was considered a major constraint for the development of entrepreneurship. Like all less resourcefulfirms, the SMEs typically had skill deficiencies and were unable to compete with larger firms' better-qualified manpower.Inter-firm transfer of skilled labor was a usual phenomenon directly influenced by relative wage levels. In this game, the largerfirms had advantage over SMEs. Unfortunately, the technical skills were not adequately rewarded by the employers. Eventhe society never respected people having blue-collared jobs.

● Over and above, lack of trust among the business community was a serious hindrance to growth, impeded cooperation amongentrepreneurs to develop the existing or explore the new markets. The entrepreneurs in their attempts to hide businessinformation used to maintain mailing address and banks in other cities. Another serious complaint was that the labor trainedby one employer, either moved to another employer or opened up his own firm. Businesses remained owner-operated owingto lack of trust on professional employees within the business community as an employee who gained knowledge easilyreplicated with stolen business information.

● Small businessmen had little recourse to bank financing. They believed that the banks lent only to the big borrowers for non-commercial and political reasons. The biggest stumbling block was the State Bank of Pakistan's Prudential Regulations anddocumentation requirements, which most SMEs were unable to meet. Cut-throat competition, willing to go for the solo flight,lack of attitude towards delegation, lack of corporate culture, lack of knowledge/proper homework and lack of relevantbusiness development systems provision in the industry had knocked down the SMEs in Pakistan.

However, in recent years, with the increasing realization of entrepreneurship and innovation as engines of economic growth, therehad been a rise in interest in Pakistan to review the country's economic policies by placing emphasis on entrepreneurial growth11.Given the nation's socio-economic challenges and perceived untapped potential, a more heightened realization has resulted in theadoption of a New Growth Framework by the National Economic Council in May 201112. Barring the forces of status-quo andvested interests of the elite groups which make up the distributional coalition and is content on their rent seeking behavior in theform of subsidies, protectionism and tax evasion, entrepreneurship offers an attractive opportunity driven merit-based option whichis known to serve as equalizer in socio-economic development13. More recently, to operationalize this New Growth Framework,some studies have proposed the use of Expeditionary Economics14 to focus on the nuts-and-bolts implementation of these newentrepreneurially-led economic growth principles in Pakistan's post-conflict settings. It has been noted that while poor infrastructureand weak governance are significant barriers, the nation has the making of a large and dynamic entrepreneurial class with thepotential of facilitating country's rise into the next levels of national economic groups15 .

Despite the challenges, the two key potential areas of opportunity where entrepreneurship can make significant contributions are:First, more than 2/3rd of Pakistan's population is concentrated below the age of 30, which will change the age structure of workingage population over the next few years. Majority of the youth entering the labor force over the next two decades will have littleeducation and skills catering to market demand. Moreover, incessant shocks to the economy such as energy crisis, internationalcommodity price shocks, security issues, and flash floods of 2010/11 have left little resilience in the economy and absorptioncapacity for growing youth labor force. This required a rethinking about the sources of growth in Pakistan's context andentrepreneurship has the greatest potential to fill this gap.

Second, in the area of indigenous technology transfer, various researchers have underscored the need for establishing industry-university linkages. According to some estimates16 in eight years, between 1999 and 2007, Pakistan had increased R&D investmentby 600% which stood at 0.7% of GDP or USD 1.176 billion. At the same time number of researchers in Pakistan has grown from187 per million in 2005 to 310 in 2007. Though Pakistan suffered significant economic challenges in the following years17, thereis still considerable R&D capacity in the nation's universities and institutions, particularly in the science and technology focusedprograms18. This new capacity can be converted into new innovative entrepreneurship opportunities, economic growth and wealthcreation by linking it with better trained young entrepreneurial minds.

The above scenario leads us to believe that the country's underdeveloped small business and entrepreneurial sector which is facingnumerous economic challenges, can benefit from the available manpower resource opportunity if mobilized through anentrepreneurially oriented innovative development approach envisaged in the new entrepreneurially-led economic growth approach19,which is also the ultimate aim envisaged by the GEM project.

12

2.1 Overview of the Research Results

In this cycle Pakistan shows a mix increase and decrease in many entrepreneurship activity indicators. The people of Pakistanperceive more opportunities in the surrounding environment and perceive to have more capabilities than many of its peer countries.The fear of failure is 31% which is a bit higher than the last year but still lower than average of the factor driven countries. TheTEA rate is 9.1, the same as that of last year. Nascent entrepreneurship rate has gone up from 6.6 to 7.5. Necessity driven TEArate has gone up from 3.69 to 4.3 indicating that people are being forced into necessity entrepreneurship. There is a decline innew business manager rate from 2.70 to 1.7 and established business owner rate from 4.72 to 4.1.

Chapter 2: Findings of GEM Pakistan 2011

Some general characteristics and entrepreneurship indicators of Pakistan are presented in Table 2a, Fig 4 and Fig 5

Table 2a: Some general characteristics and entrepreneurship indicators of Pakistan

Fig 4: Entrepreneurial Profile of Pakistan compared with other nations

EntrepreneurialEmployee Acitivity (EEA)

TEA: Solo & Low JobExpection (SLEA)

TEA: Medium-High JobExpection (MHEA)

Percieved Capabilites

Eerly-StageEntrepreneurial Activity

(TEA)

TEA: Necessity-Driven

Percieved Opportunities

Pakistan

Factor-Driven Economies

Group: High non-ambitiousentrepreneurship (SLEA) only

1.51

0.50

-0.5-1

-1.5

13

Note: Medium-High Job Expectation TEA and Solow & Low Job Expectation TEA are based on GEM 2009-2011 APS data,all other indicators based on GEM 2011 APS data. Values of group level indicators are based on averaging the country-level Z-scores (standardized values obtained from the entire GEM 2011 sample).

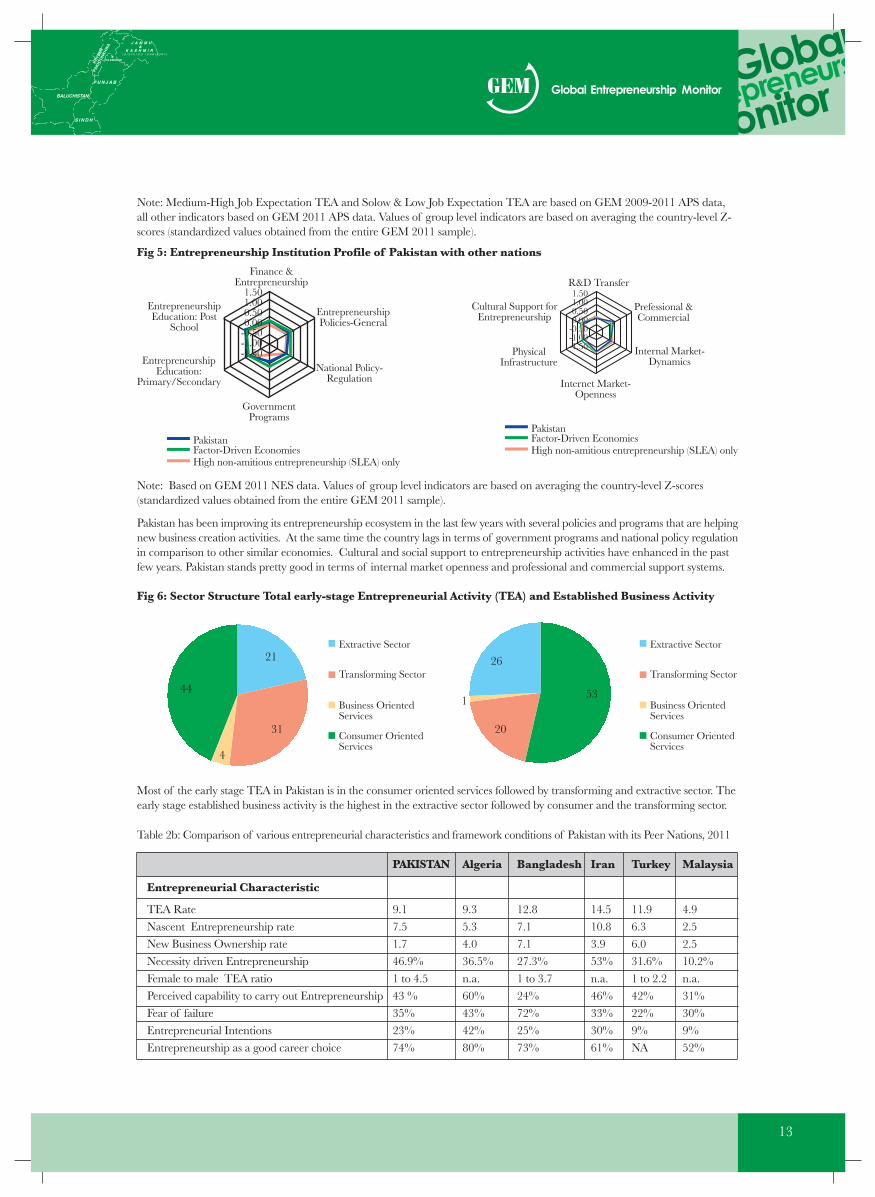

Note: Based on GEM 2011 NES data. Values of group level indicators are based on averaging the country-level Z-scores(standardized values obtained from the entire GEM 2011 sample).

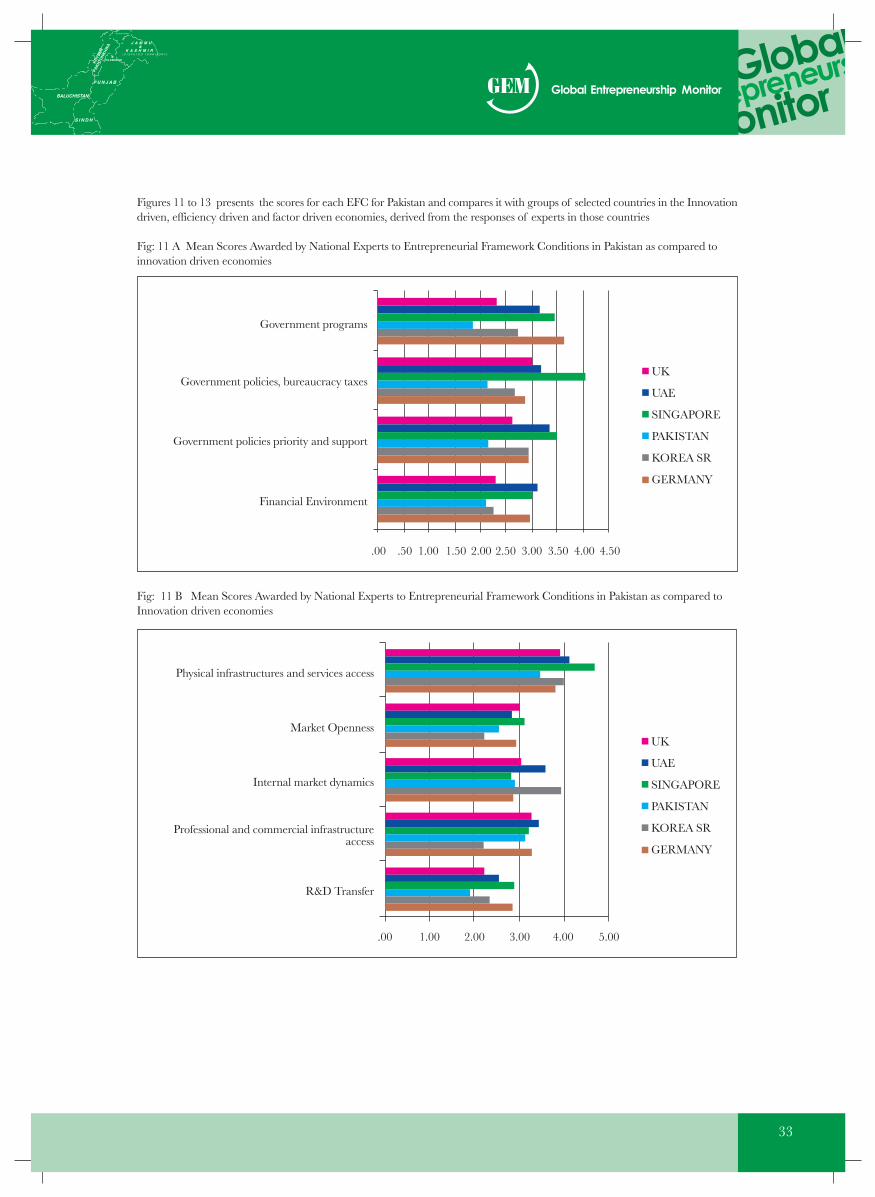

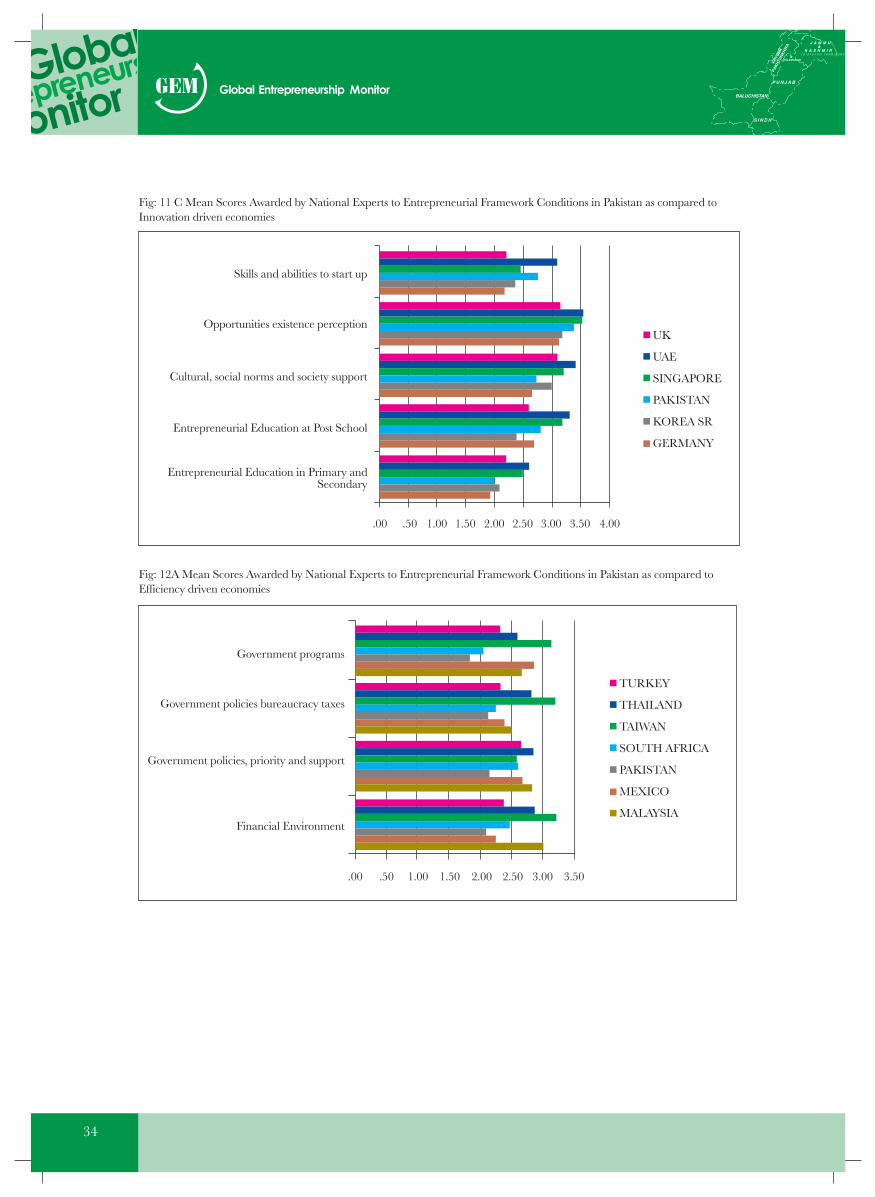

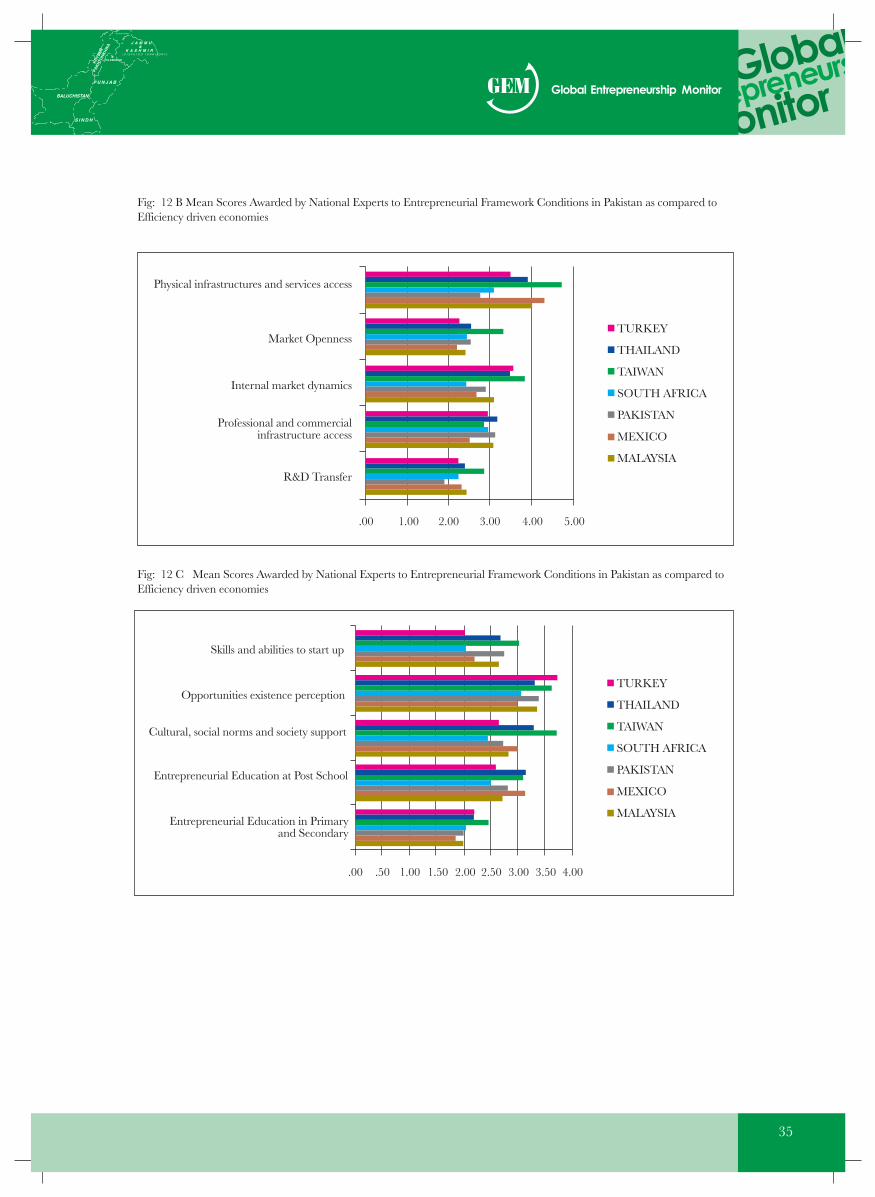

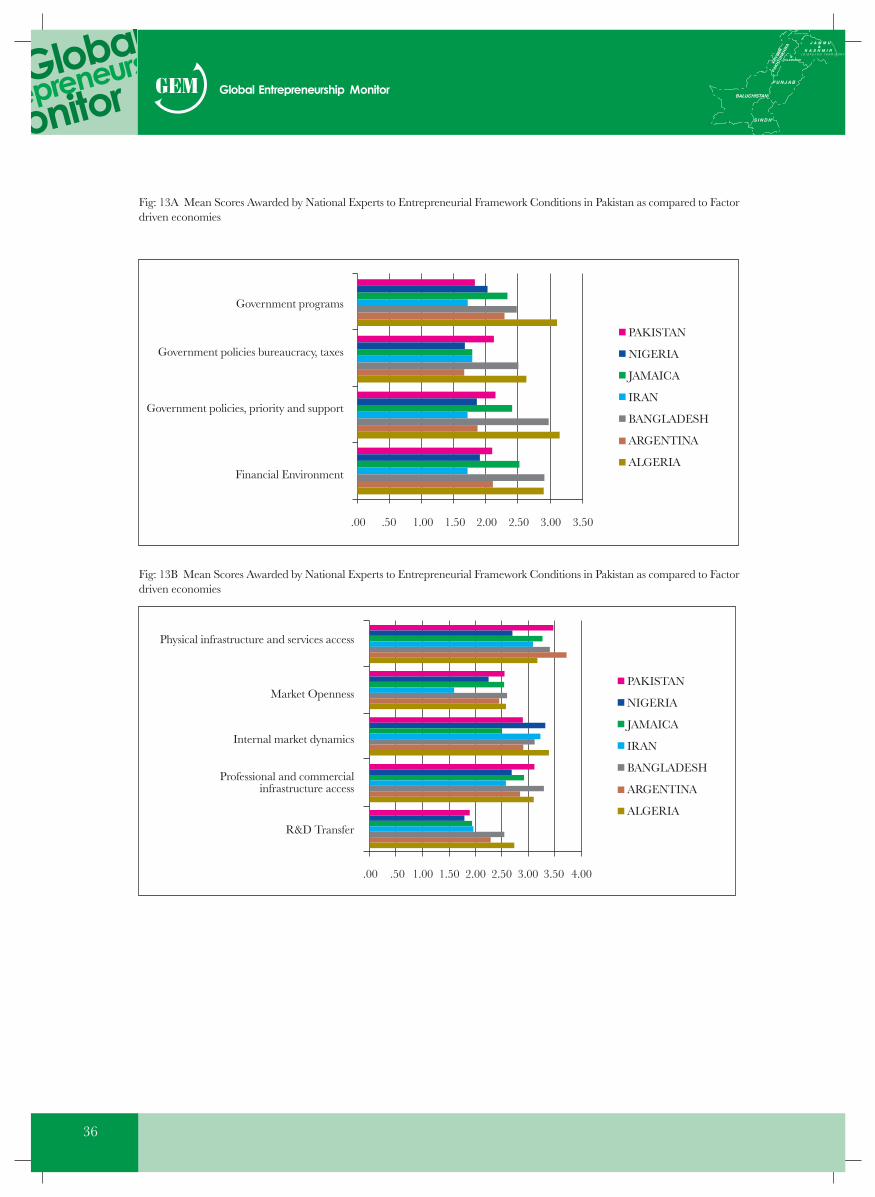

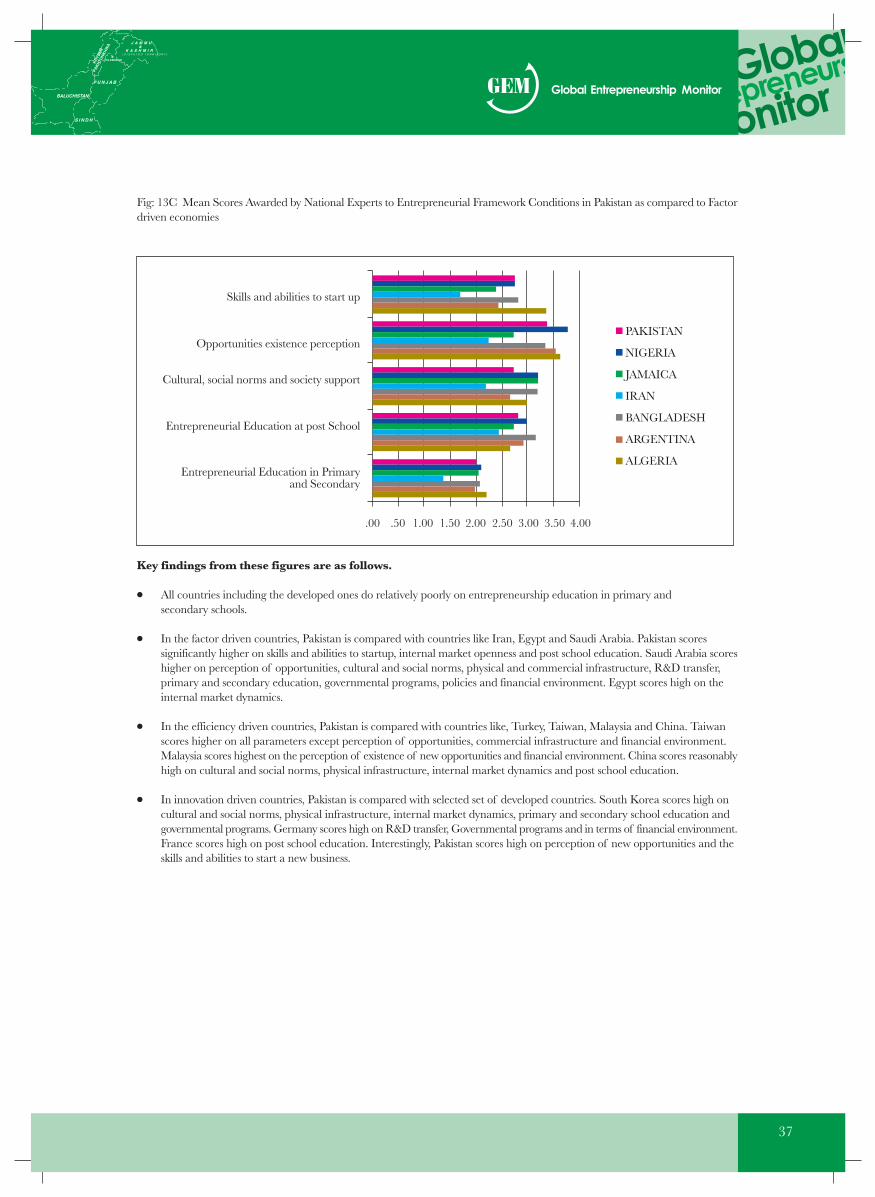

Pakistan has been improving its entrepreneurship ecosystem in the last few years with several policies and programs that are helpingnew business creation activities. At the same time the country lags in terms of government programs and national policy regulationin comparison to other similar economies. Cultural and social support to entrepreneurship activities have enhanced in the pastfew years. Pakistan stands pretty good in terms of internal market openness and professional and commercial support systems.

Fig 6: Sector Structure Total early-stage Entrepreneurial Activity (TEA) and Established Business Activity

Most of the early stage TEA in Pakistan is in the consumer oriented services followed by transforming and extractive sector. Theearly stage established business activity is the highest in the extractive sector followed by consumer and the transforming sector.

Table 2b: Comparison of various entrepreneurial characteristics and framework conditions of Pakistan with its Peer Nations, 2011

9.17.51.746.9%1 to 4.543 %35%23%74%

9.35.34.036.5%n.a.60%43%42%80%

12.87.17.127.3%1 to 3.724%72%25%73%

14.510.83.953%n.a.46%33%30%61%

Iran

11.96.36.031.6%1 to 2.242%22%9%NA

4.92.52.510.2%n.a.31%30%9%52%

Entrepreneurial Characteristic

PAKISTAN Algeria Bangladesh Turkey Malaysia

TEA RateNascent Entrepreneurship rateNew Business Ownership rateNecessity driven EntrepreneurshipFemale to male TEA ratioPerceived capability to carry out EntrepreneurshipFear of failureEntrepreneurial IntentionsEntrepreneurship as a good career choice

44

21

31

4

Extractive Sector

Transforming Sector

Business OrientedServices

Consumer OrientedServices

26

53

20

1

Extractive Sector

Transforming Sector

Business OrientedServices

Consumer OrientedServices

Fig 5: Entrepreneurship Institution Profile of Pakistan with other nations

Finance &Entrepreneurship

PakistanFactor-Driven Economies

EntrepreneurshipEducation: Post

School

EntrepreneurshipEducation:

Primary/Secondary

GovernmentPrograms

National Policy-Regulation

EntrepreneurshipPolicies-General

High non-amitious entrepreneurship (SLEA) only

1.501.000.500.00

-0.50-1.00-1.50

R&D Transfer

PakistanFactor-Driven EconomiesHigh non-amitious entrepreneurship (SLEA) only

1.501.000.500.00

-0.50-1.00-1.50

Cultural Support forEntrepreneurship

PhysicalInfrastructure

Internet Market-Openness

Internal Market-Dynamics

Prefessional &Commercial

14

The predominant motive for pursuing entrepreneurial activity (TEA) in the country is to increase income (38.0 percent) and to amuch lesser degree (2.8 percent) acquire independence. The growth expectations are a modest 3.5 percent.

Of the entrepreneurs (TEA), 75 percent find it more difficult to start a business and 80 percent report more difficult (or about thesame) to grow it, with 56 percent pointing towards less business opportunities, compared to a year ago. Similarly, of the establishedbusinesses 64 percent find it more difficult to start and 83 percent report that it is more difficult (or about the same) to growbusinesses, with 49 percent saying there are less business opportunities, than a year ago.

In terms of entrepreneurial environment manifested in the framework conditions prevailing in Pakistan, the commercial andphysical infrastructure and the internal market dynamics were described as adequate, while the national policy towards entrepreneurshipand related support programs including education were considered weak by the national experts. Overall, new firm start-up aswell as established business growth activity and related opportunities have been severely curtailed during the past several years dueto the on-going 'war on terrorism' in the north western region of Pakistan bordering Afghanistan and the resulting precarioussecurity situation in the rest of the country. The economic situation worsened further due to natural calamities including a majorearth quake and recent widespread floods. In this scenario a precise impact of global financial crisis in light of these nationalcatastrophic events is hard to discern. A comparative review of Pakistan Entrepreneurial Characteristics with its several peernations is table above.

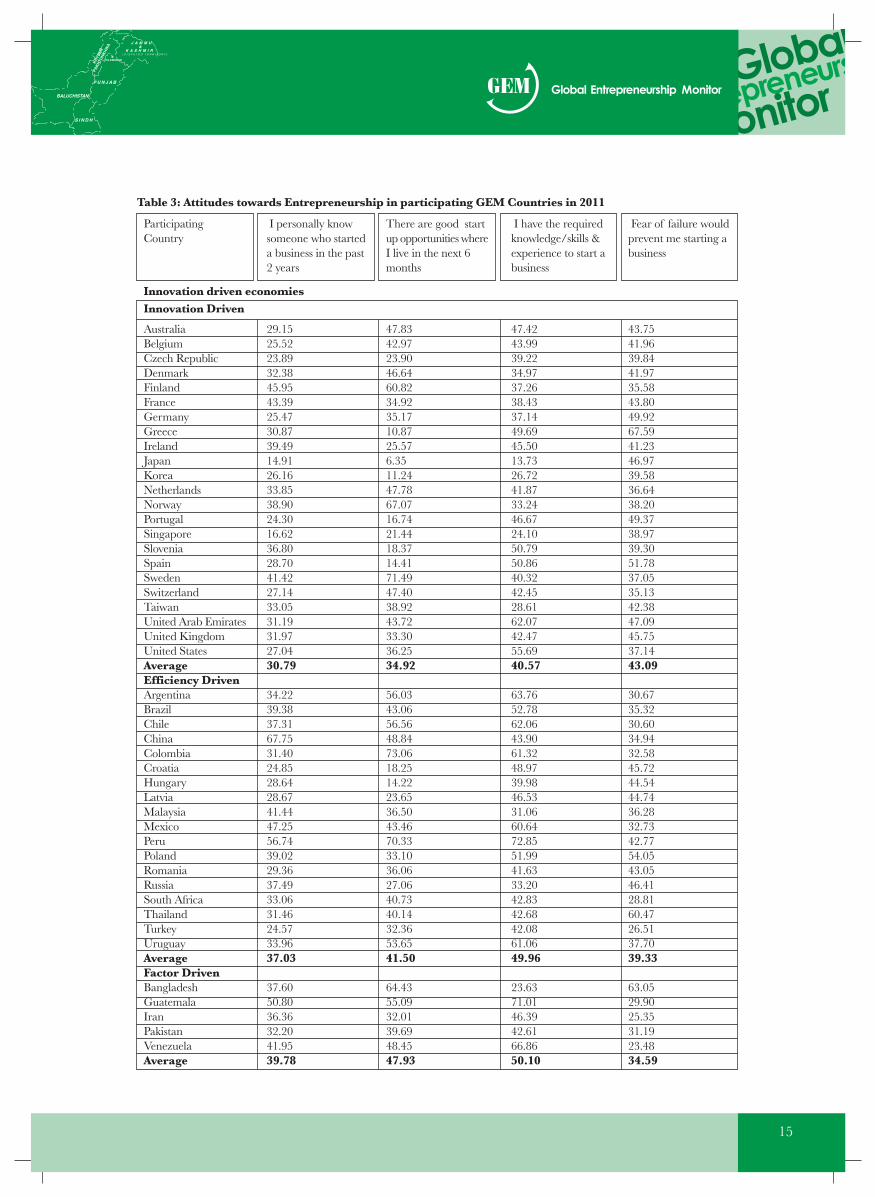

2.1 Entrepreneurial attitudes According to GEM, entrepreneurial attitudes convey the feelings of a population grouptowards entrepreneurship in general. People who recognize the importance of entrepreneurship as it relates to the ability ofindividuals to deploy their competencies in order to exploit opportunities given a favorable or not so favorable environmenttend to formulate certain views about entrepreneurship which are manifested in their attitudes towards this phenomenon. Forthis purpose GEM employs specific questions in the Adult Population Survey (APS) that measure these attitudes through variousindicators.

More importantly, the difference in entrepreneurial activity rates between countries can be explained by differences in attitudesof the population towards entrepreneurship. Table 3 provides the attitudinal estimates for all participating countries in the adultworking age (18-64) population who are not entrepreneurially active . The percentage of the responding adults in eachparticipating country including Pakistan, who expressed an opinion and agreed with the four key indicators, is listed in theTable. The countries are divided into three groups i.e., innovation driven, efficiency driven and factor driven economies withthe following salient findings.

● In the innovation driven countries, the proportion of the non entrepreneurial working age population who are aware of newentrepreneurial startups is the highest in Finland and France. The highest perception of good startup opportunities in thenext six months is in Sweden and Norway. The skill, knowledge and experience perception is highest in the UAE followedby US. The people of Switzerland and Finland have the lowest fear of failure.

● In the efficiency driven countries, the proportion of the non entrepreneurial working age population who are aware of newentrepreneurial startups is the highest in China, who perceive good startup opportunities in the next six months are in Colombiaand Peru and the skill, knowledge and experience perception is the highest in Peru. The South African people have the lowestfear of failure.

● In the factor driven countries, the proportion of the non entrepreneurial working age population who are aware of newentrepreneurial startups and the skill, knowledge and experience perception is the highest in south American countries ofGuatemala and Venezuela. Surprisingly Bangladesh scored highest on the perception of good startup opportunities in thenext six months. The Venezuelan people have the lowest fear of failure.

Overall, respondents from factor-driven economies generally rated their entrepreneurial attitudes more positively followed byefficiency driven economies and innovation-driven economies respectively.

There was a less participation of the factor driven countries in the GEM 2011 cycle. Comparisons within the 5 factor driveneconomies show that Pakistan's adult population attitude measures are less positive than the group averages in the first twoindicators. However Pakistan scores higher than the average in the last two indicators.

Table 3: Attitudes towards Entrepreneurship in participating GEM Countries in 2011

15

Innovation driven economies

AustraliaBelgiumCzech RepublicDenmarkFinlandFranceGermanyGreeceIrelandJapanKoreaNetherlandsNorwayPortugalSingaporeSloveniaSpainSwedenSwitzerlandTaiwanUnited Arab EmiratesUnited KingdomUnited StatesAverageEfficiency DrivenArgentinaBrazilChileChinaColombiaCroatiaHungaryLatviaMalaysiaMexicoPeruPolandRomaniaRussiaSouth AfricaThailandTurkeyUruguayAverageFactor DrivenBangladeshGuatemalaIranPakistanVenezuelaAverage

29.1525.5223.8932.3845.9543.3925.4730.8739.4914.9126.1633.8538.9024.3016.6236.8028.7041.4227.1433.0531.1931.9727.0430.79

34.2239.3837.3167.7531.4024.8528.6428.6741.4447.2556.7439.0229.3637.4933.0631.4624.5733.9637.03

37.6050.8036.3632.2041.9539.78

47.8342.9723.9046.6460.8234.9235.1710.8725.576.3511.2447.7867.0716.7421.4418.3714.4171.4947.4038.9243.7233.3036.2534.92

56.0343.0656.5648.8473.0618.2514.2223.6536.5043.4670.3333.1036.0627.0640.7340.1432.3653.6541.50

64.4355.0932.0139.6948.4547.93

47.4243.9939.2234.9737.2638.4337.1449.6945.5013.7326.7241.8733.2446.6724.1050.7950.8640.3242.4528.6162.0742.4755.6940.57

63.7652.7862.0643.9061.3248.9739.9846.5331.0660.6472.8551.9941.6333.2042.8342.6842.0861.0649.96

23.6371.0146.3942.6166.8650.10

43.7541.9639.8441.9735.5843.8049.9267.5941.2346.9739.5836.6438.2049.3738.9739.3051.7837.0535.1342.3847.0945.7537.1443.09

30.6735.3230.6034.9432.5845.7244.5444.7436.2832.7342.7754.0543.0546.4128.8160.4726.5137.7039.33

63.0529.9025.3531.1923.4834.59

Innovation Driven

ParticipatingCountry

I personally knowsomeone who starteda business in the past2 years

There are good startup opportunities whereI live in the next 6months

I have the requiredknowledge/skills &experience to start abusiness

Fear of failure wouldprevent me starting abusiness

16

Entrepreneurial Attitudes in Pakistan

Table 4 shows estimates of the prevalence of attitudes towards entrepreneurship in Pakistan among the non-entrepreneuriallyactive working age population by gender. Those successful at starting a new business have a high level of status and respect insociety and most people consider starting a new business a good career choice. The Table shows that males tend to have morepositive entrepreneurial attitude than females. The gap is particularly marked between the variables as follows.

● The male respondents are about three times more aware of someone who has started a business in the last two years, a proxymeasure of networking with entrepreneurial individuals

● The male respondents perceive a higher number of startup opportunities and feel better equipped with the knowledge, skilland experience to start a new business.

● The female respondents have less fear of failure to start a business and moreover they are more aware of stories about peoplestarting successful new businesses in the media.

Table 4: Entrepreneurial Attitude in Pakistan: Respondents expressing the opinion and agreeing with thestatement

Statement

I personally knowsomeone personallywho started a businessin the past 2 years.

There will be goodstartup opportunitieswhere I live in the nextsix months.

I have the knowledge,skill and experience tostart a new business.

Fear of failure wouldprevent me fromstarting a business.

Most people in mycountry would preferthat everyone had asimilar standard ofliving

Most people considerstarting a new businessa good career choice.

Those successful atstarting a new businesshave a high level ofstatus and respect insociety.

You will often seestories about peoplestarting successful newbusinesses in themedia.

All

30.9%

39.4%

42.8%

34.6%

68.6%

73.0%

71.9%

48.4%

Male

45.9%

49.4%

55.5%

42.7%

70.0%

76.0%

75.2%

48.3%

Female

16.0%

29.0%

29.8%

25.7%

67.2%

69.7%

68.4%

48.5%

Entrepreneurial attitudes of the non-entrepreneurially active working age population in various provinces of Pakistan are presentedin table 5.

The key findings are as follows.

● The people of Sindh and Baluchistan were more likely to agree with the statement “I personally know someone who hasstarted a business in the last two years” which is a proxy for networking with entrepreneurs.

● Moreover the people of Sindh and Baluchistan had the highest proportion of the non-entrepreneurially active populationreporting that there were good start-up opportunities in their local area in the next six months.

● The people of Sindh and Punjab were the most likely to agree with statement that “I have the knowledge, skill and experiencerequired to start a new business”.

● The people of Khyber Pakhtoon Khowa had the lowest fear of failure to start a business.

Table 5 A: Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurshipin various provinces of Pakistan

17

Sindh

Punjab

Baluchistan

Khyber PakhtoonKhowa

Province

38.9%

27.1%

42.2%

27.4%

I personally knowsomeone who hasstarted a business inthe last two years

42.2%

38.0%

56.6%

33.8%

There will be goodstartup opportunitieswhere I live in the next6 months

44.0%

44.1%

41.6%

35.5%

I have the knowledge,skill and experiencerequired to start a newbusiness

43.6%

32.9%

29.6%

24.4%

Fear of failure wouldprevent me fromstarting a business

Table 5 B: Perceptions of entrepreneurship among non-entrepreneurially active working age population towards entrepreneurshipin various provinces of Pakistan

Sindh

Punjab

Baluchistan

Khyber PakhtoonKhowa

Province

81.1%

62.0%

67.4%

71.4%

I personally knowsomeone who hasstarted a business inthe last two years

68.6%

69.2%

86.4%

92.8%

There will be goodstartup opportunitieswhere I live in the next6 months

71.8%

67.3%

85.1%

86.2%

I have the knowledge,skill and experiencerequired to start a newbusiness

53.0%

46.1%

47.4%

49.4%

Fear of failure wouldprevent me fromstarting a business

18

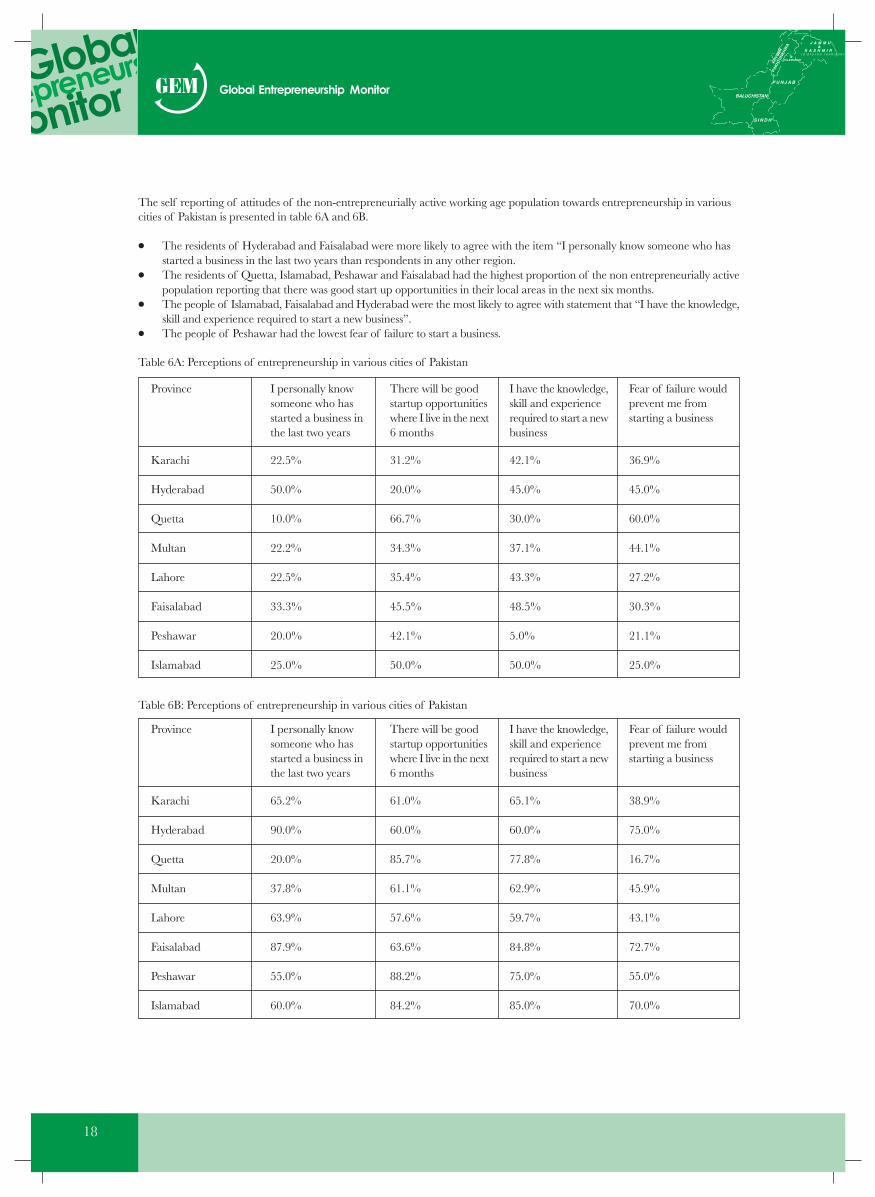

The self reporting of attitudes of the non-entrepreneurially active working age population towards entrepreneurship in variouscities of Pakistan is presented in table 6A and 6B.

● The residents of Hyderabad and Faisalabad were more likely to agree with the item “I personally know someone who hasstarted a business in the last two years than respondents in any other region.

● The residents of Quetta, Islamabad, Peshawar and Faisalabad had the highest proportion of the non entrepreneurially activepopulation reporting that there was good start up opportunities in their local areas in the next six months.

● The people of Islamabad, Faisalabad and Hyderabad were the most likely to agree with statement that “I have the knowledge,skill and experience required to start a new business”.

● The people of Peshawar had the lowest fear of failure to start a business.

Table 6A: Perceptions of entrepreneurship in various cities of Pakistan

Karachi

Hyderabad

Quetta

Multan

Lahore

Faisalabad

Peshawar

Islamabad

Province

22.5%

50.0%

10.0%

22.2%

22.5%

33.3%

20.0%

25.0%

I personally knowsomeone who hasstarted a business inthe last two years

31.2%

20.0%

66.7%

34.3%

35.4%

45.5%

42.1%

50.0%

There will be goodstartup opportunitieswhere I live in the next6 months

42.1%

45.0%

30.0%

37.1%

43.3%

48.5%

5.0%

50.0%

I have the knowledge,skill and experiencerequired to start a newbusiness

36.9%

45.0%

60.0%

44.1%

27.2%

30.3%

21.1%

25.0%

Fear of failure wouldprevent me fromstarting a business

Table 6B: Perceptions of entrepreneurship in various cities of Pakistan

Karachi

Hyderabad

Quetta

Multan

Lahore

Faisalabad

Peshawar

Islamabad

Province

65.2%

90.0%

20.0%

37.8%

63.9%

87.9%

55.0%

60.0%

I personally knowsomeone who hasstarted a business inthe last two years

61.0%

60.0%

85.7%

61.1%

57.6%

63.6%

88.2%

84.2%

There will be goodstartup opportunitieswhere I live in the next6 months

65.1%

60.0%

77.8%

62.9%

59.7%

84.8%

75.0%

85.0%

I have the knowledge,skill and experiencerequired to start a newbusiness

38.9%

75.0%

16.7%

45.9%

43.1%

72.7%

55.0%

70.0%

Fear of failure wouldprevent me fromstarting a business

19

Table 6B reports that the people living in Hyderabad and Faisalabad prefer an egalitarian standard of living for all followed byKarachi and Islamabad. The residents of Peshawar, Islamabad and Quetta gave the highest ratings to starting a new business adesirable career choice. The people of Islamabad, Faisalabad and Quetta have the highest perception that those successful atstarting a new business have a high level of status and respect in society. Moreover Hyderabad, Faisalabad and Islamabad havethe highest number of people reporting that they have seen stories about people starting successful businesses in the media.

2.3 Entrepreneurial Activity

GEM considers entrepreneurship as a step-wise process in which individuals become increasingly engaged in this activity.Total Early-stage Entrepreneurial Activity (TEA) the key regional measure employed by GEM includes nascent entrepreneursinvolved in setting up of businesses and those owning and running new businesses less than 3.5 years (42 months) old. Additionally,GEM assesses the rate and nature of business discontinuance as well as necessity based verses opportunity oriented entrepreneurship.

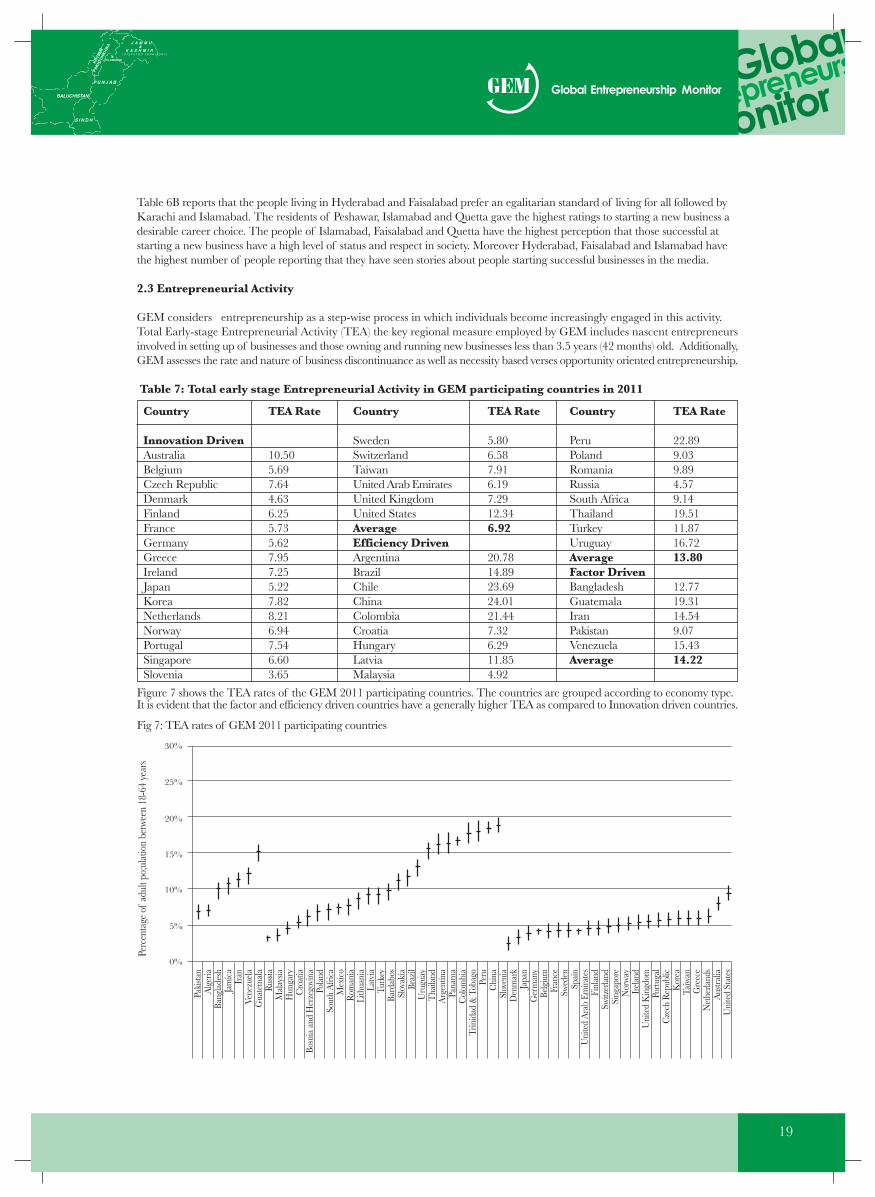

Table 7: Total early stage Entrepreneurial Activity in GEM participating countries in 2011

Country

Innovation DrivenAustraliaBelgiumCzech RepublicDenmarkFinlandFranceGermanyGreeceIrelandJapanKoreaNetherlandsNorwayPortugalSingaporeSlovenia

TEA Rate

10.505.697.644.636.255.735.627.957.255.227.828.216.947.546.603.65

Country

SwedenSwitzerlandTaiwanUnited Arab EmiratesUnited KingdomUnited StatesAverageEfficiency DrivenArgentinaBrazilChileChinaColombiaCroatiaHungaryLatviaMalaysia

TEA Rate

5.806.587.916.197.2912.346.92

20.7814.8923.6924.0121.447.326.2911.854.92

Country

PeruPolandRomaniaRussiaSouth AfricaThailandTurkeyUruguayAverageFactor DrivenBangladeshGuatemalaIranPakistanVenezuelaAverage

TEA Rate

22.899.039.894.579.1419.5111.8716.7213.80

12.7719.3114.549.0715.4314.22

Figure 7 shows the TEA rates of the GEM 2011 participating countries. The countries are grouped according to economy type.It is evident that the factor and efficiency driven countries have a generally higher TEA as compared to Innovation driven countries.

Fig 7: TEA rates of GEM 2011 participating countries

Paki

stan

Alg

eria

Bang

lade

shJa

mic

aIr

anVe

nezu

ela

Gua

tem

ala

Rus

siaM

alay

siaH

unga

ryC

roat

iaBo

snia

and

Her

zego

vina

Pola

ndSo

uth

Afri

caM

exic

oR

oman

iaLi

thua

nia

Latv

iaTu

rkey

Bard

abos

Slov

akia

Braz

ilU

rugu

ayT

haila

ndA

rgen

tina

Pana

ma

Col

ombi

a

Peru

Chi

naSl

oven

ia

Japa

nG

erm

any

Belg

ium

Fran

ceSw

eden

Spai

nU

nite

d A

rab

Emira

tes

Finl

and

Switz

erla

ndSi

ngap

ore

Nor

way

Irel

and

Cze

ch R

epub

licK

orea

Taiw

anG

reec

eN

ethe

rland

sAu

stral

iaU

nite

d St

ates

Trin

idad

& T

obag

o

Den

mar

k

Uni

ted

Kin

gdom

Portu

gal

30%

25%

20%

15%

10%

5%

0%

Perc

enta

ge o

f adu

lt po

;ula

tion

betw

een

18-6

4 ye

ars

20

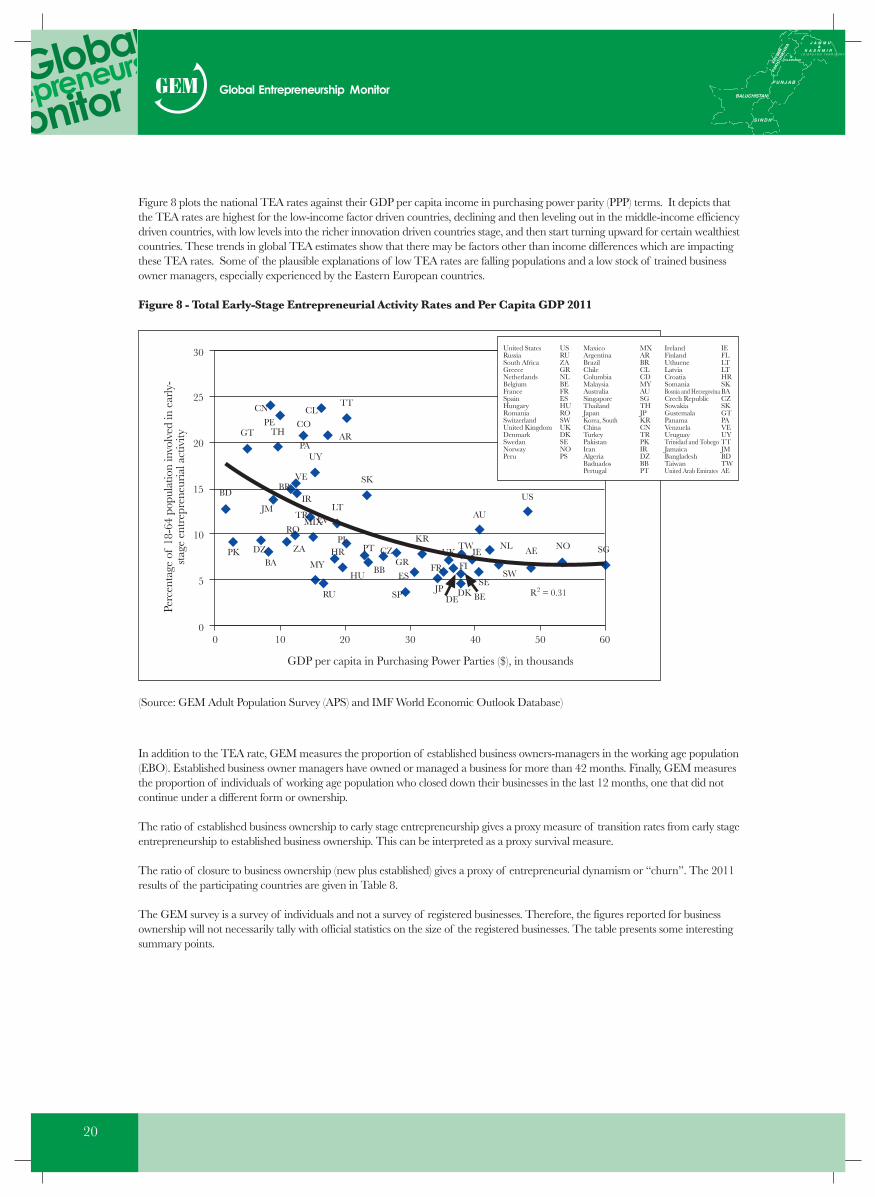

Figure 8 plots the national TEA rates against their GDP per capita income in purchasing power parity (PPP) terms. It depicts thatthe TEA rates are highest for the low-income factor driven countries, declining and then leveling out in the middle-income efficiencydriven countries, with low levels into the richer innovation driven countries stage, and then start turning upward for certain wealthiestcountries. These trends in global TEA estimates show that there may be factors other than income differences which are impactingthese TEA rates. Some of the plausible explanations of low TEA rates are falling populations and a low stock of trained businessowner managers, especially experienced by the Eastern European countries.

Figure 8 - Total Early-Stage Entrepreneurial Activity Rates and Per Capita GDP 2011

(Source: GEM Adult Population Survey (APS) and IMF World Economic Outlook Database)

CN CLTT

PEGT TH

COAR

PAUY

VEBR

IRLT

SKBD

JMMIX

TR LVRO

DZPKBA

ZAPL

HRMY

RU

HU

PT CZ

BBGR

KR

ES

SP

FR

UKTW

AU

US

IE

FI

JPDE

DK BE

SESW

NL AE NO SG

R2 = 0.31

GDP per capita in Purchasing Power Parties ($), in thousands

Perc

enta

ge o

f 18

-64

popu

latio

n in

volv

ed in

ear

ly-

stag

e en

trep

rene

uria

l act

ivity

30

25

20

15

10

5

00 10 20 30 40 50 60

United States USRussia RUSouth Africa ZAGreece GRNetherlands NLBelgium BEFrance FRSpain ESHungary HURomania ROSwitzerland SWUnited Kingdom UKDenmark DKSwedan SENorway NOPeru PS

Maxico MXArgentina ARBrazil BRChile CLColumbia CDMalaysia MYAustralia AUSingapore SGThailand THJapan JPKorea, South KRChina CNTurkey TRPakistan PKIran IRAlgeria DZBaduados BBPertugal PT

Ireland IEFinland FLUthuene LTLatvia LTCroatia HRSomania SKBosnia and Herzegovina BACrech Republic CZSowakia SKGustemala GTPanama PAVenzuela VEUruguay UYTrinidad and Tobego TTJamaica JMBangladesh BDTaiwan TWUnited Arab Emirates AE

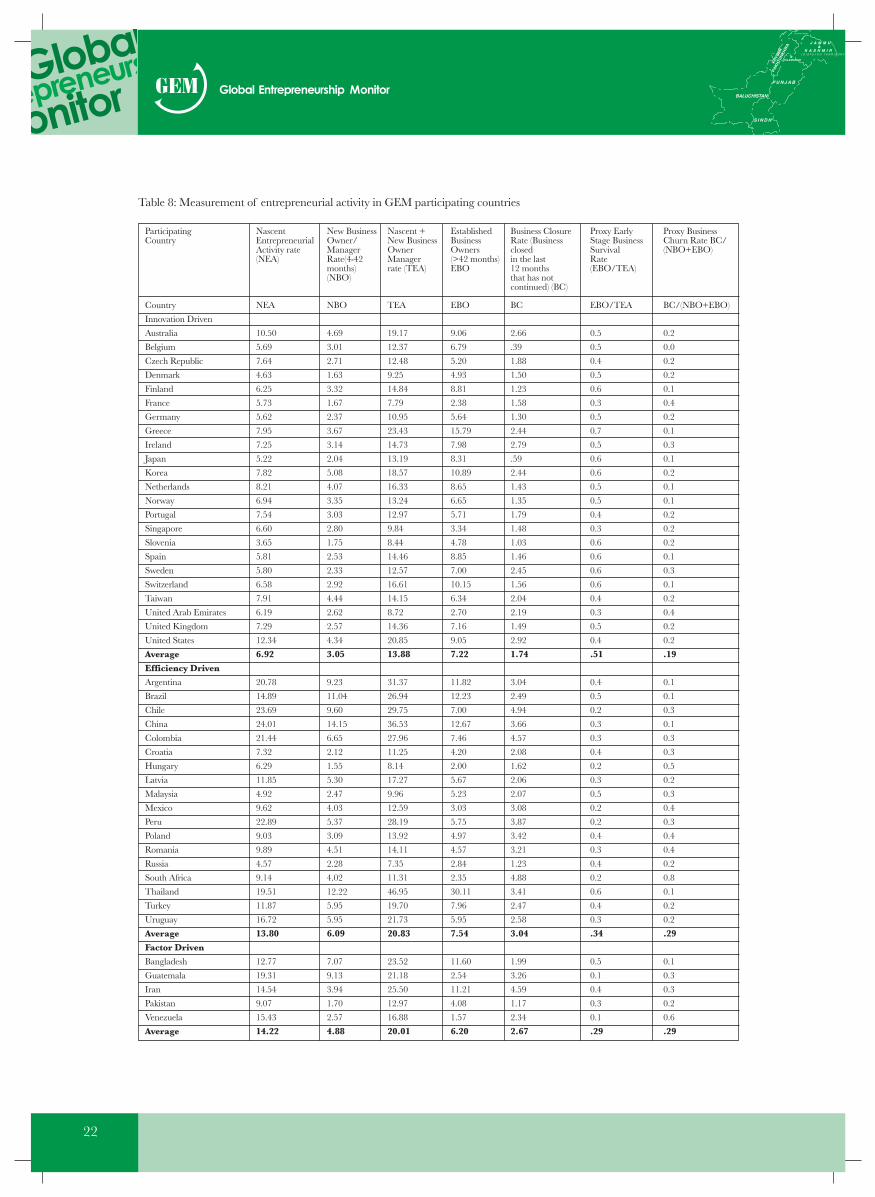

In addition to the TEA rate, GEM measures the proportion of established business owners-managers in the working age population(EBO). Established business owner managers have owned or managed a business for more than 42 months. Finally, GEM measuresthe proportion of individuals of working age population who closed down their businesses in the last 12 months, one that did notcontinue under a different form or ownership.

The ratio of established business ownership to early stage entrepreneurship gives a proxy measure of transition rates from early stageentrepreneurship to established business ownership. This can be interpreted as a proxy survival measure.

The ratio of closure to business ownership (new plus established) gives a proxy of entrepreneurial dynamism or “churn”. The 2011results of the participating countries are given in Table 8.

The GEM survey is a survey of individuals and not a survey of registered businesses. Therefore, the figures reported for businessownership will not necessarily tally with official statistics on the size of the registered businesses. The table presents some interestingsummary points.

21

● Among the innovation driven countries, the nascent entrepreneurial activity (NEA) is the highest in US followed by Australia,Netherland, Taiwan, Greece, Czech and Norway. . Italy, Japan and Portugal have the lowest rate of NEA. The highest totalentrepreneurial activity (TEA) i.e. the sum of nascent entrepreneurship and the new business owner manager rate is reportedto be the highest in Australia followed by Norway, US, Netherland, Ireland and Korea. Slovenia and Denmark reports thelowest level of total entrepreneurial activity. The highest number of established business units (for more than 42 months) isobserved in Greece, Korea and Switzerland. US, Ireland and Australia report the highest number of business closures in thepast 12 months.

● Among the efficiency driven countries, the nascent entrepreneurial activity (NEA) is the highest in the South Americancountries of Peru, Chile, Colombia and Argentina followed by China and Thailand. On the other hand lowest level of NEAis reported in Malaysia and Russia. The highest total entrepreneurial activity (TEA) i.e. the sum of nascent entrepreneurshipand the new business owner manager rate is reported to be the highest in Thailand followed by the South American countriesand in China as well. The highest number of established business units (for more than 42 months) is observed in Thailandand China. Chile, Columbia and South Africa report the highest number of business closures in the past 12 months.

● In the Factor driven countries, the nascent entrepreneurial activity (NEA) is the highest in Guatemala, Venezuela and Iran.The lowest level of NEA is reported in Pakistan. The highest total entrepreneurial activity (TEA) i.e. the sum of nascententrepreneurship and the new business owner manager rate is reported to be the highest in Iran and Bangladesh. The lowestlevel of TEA is observed in Pakistan. The highest number of established business units (for more than 42 months) is observedin Iran and Bangladesh. Guatemala reports the lowest number of established business units.

22

Table 8: Measurement of entrepreneurial activity in GEM participating countries

Country

Innovation Driven

Australia

Belgium

Czech Republic

Denmark

Finland

France

Germany

Greece

Ireland

Japan

Korea

Netherlands

Norway

Portugal

Singapore

Slovenia

Spain

Sweden

Switzerland

Taiwan

United Arab Emirates

United Kingdom

United States

Average

Efficiency Driven

Argentina

Brazil

Chile

China

Colombia

Croatia

Hungary

Latvia

Malaysia

Mexico

Peru

Poland

Romania

Russia

South Africa

Thailand

Turkey

Uruguay

Average

Factor Driven

Bangladesh

Guatemala

Iran

Pakistan

Venezuela

Average

NEA

10.50

5.69

7.64

4.63

6.25

5.73

5.62

7.95

7.25

5.22

7.82

8.21

6.94

7.54

6.60

3.65

5.81

5.80

6.58

7.91

6.19

7.29

12.34

6.92

20.78

14.89

23.69

24.01

21.44

7.32

6.29

11.85

4.92

9.62

22.89

9.03

9.89

4.57

9.14

19.51

11.87

16.72

13.80

12.77

19.31

14.54

9.07

15.43

14.22

NBO

4.69

3.01

2.71

1.63

3.32

1.67

2.37

3.67

3.14

2.04

5.08

4.07

3.35

3.03

2.80

1.75

2.53

2.33

2.92

4.44

2.62

2.57

4.34

3.05

9.23

11.04

9.60

14.15

6.65

2.12

1.55

5.30

2.47

4.03

5.37

3.09

4.51

2.28

4.02

12.22

5.95

5.95

6.09

7.07

9.13

3.94

1.70

2.57

4.88

TEA

19.17

12.37

12.48

9.25

14.84

7.79

10.95

23.43

14.73

13.19

18.57

16.33

13.24

12.97

9.84

8.44

14.46

12.57

16.61

14.15

8.72

14.36

20.85

13.88

31.37

26.94

29.75

36.53

27.96

11.25

8.14

17.27

9.96

12.59

28.19

13.92

14.11

7.35

11.31

46.95

19.70

21.73

20.83

23.52

21.18

25.50

12.97

16.88

20.01

EBO

9.06

6.79

5.20

4.93

8.81

2.38

5.64

15.79

7.98

8.31

10.89

8.65

6.65

5.71

3.34

4.78

8.85

7.00

10.15

6.34

2.70

7.16

9.05

7.22

11.82

12.23

7.00

12.67

7.46

4.20

2.00

5.67

5.23

3.03

5.75

4.97

4.57

2.84

2.35

30.11

7.96

5.95

7.54

11.60

2.54

11.21

4.08

1.57

6.20

ParticipatingCountry

NascentEntrepreneurialActivity rate(NEA)

New BusinessOwner/ManagerRate(4-42months)(NBO)

Nascent +New BusinessOwnerManagerrate (TEA)

EstablishedBusinessOwners(>42 months)EBO

BC

2.66

.39

1.88

1.50

1.23

1.58

1.30

2.44

2.79

.59

2.44

1.43

1.35

1.79

1.48

1.03

1.46

2.45

1.56

2.04

2.19

1.49

2.92

1.74

3.04

2.49

4.94

3.66

4.57

2.08

1.62

2.06

2.07

3.08

3.87

3.42

3.21

1.23

4.88

3.41

2.47

2.58

3.04

1.99

3.26

4.59

1.17

2.34

2.67

Business ClosureRate (Businessclosedin the last12 monthsthat has notcontinued) (BC)

EBO/TEA

0.5

0.5

0.4

0.5

0.6

0.3

0.5

0.7

0.5

0.6

0.6

0.5

0.5

0.4

0.3

0.6

0.6

0.6

0.6

0.4

0.3

0.5

0.4

.51

0.4

0.5

0.2

0.3

0.3

0.4

0.2

0.3

0.5

0.2

0.2

0.4

0.3

0.4

0.2

0.6

0.4

0.3

.34

0.5

0.1

0.4

0.3

0.1

.29

Proxy EarlyStage BusinessSurvivalRate(EBO/TEA)

BC/(NBO+EBO)

0.2

0.0

0.2

0.2

0.1

0.4

0.2

0.1

0.3

0.1

0.2

0.1

0.1

0.2

0.2

0.2

0.1

0.3

0.1

0.2

0.4

0.2

0.2

.19

0.1

0.1

0.3

0.1

0.3

0.3

0.5

0.2

0.3

0.4

0.3

0.4

0.4

0.2

0.8

0.1

0.2

0.2

.29

0.1

0.3

0.3

0.2

0.6

.29

Proxy BusinessChurn Rate BC/(NBO+EBO)

23

Entrepreneurial Activity by Stages in Pakistan

Table 9 illustrates the proportion of respondents by stage of entrepreneurial activity in Pakistan.

In Pakistan 43.4% of working age individuals were not engaged in entrepreneurial activity and had no intention of starting abusiness within the next three years. A further 25.8% expected to start a business in the next three years, but were not activelytrying to start a business or running an existing business. A further 14.1% were nascent entrepreneurs and an additional 16.7%were new business owner/ managers.

Table 9: Proportion of respondents by stage of entrepreneurial activity in Pakistan

Are you, alone or with others, currently the owner of a business you help manage, self-employed, or selling anygoods or services to others?

Are you, alone or with others, currently trying to start a new business, including any self-employment or sellingany goods or services to others?

Are you, alone or with others, expecting to start a new business, including any type of self-employment, withinthe next three years?

No Activity or intention

16.7%

14.1%

25.8%

43.4%

Opportunity and Necessity Based Entrepreneurship Activity

One way of distinguishing between different types of entrepreneurial activity is the extent to which the activity is based on necessity(i.e. there are no better alternatives for work) or opportunity (where entrepreneurs may be exploiting the potential for new marketcreation).

From the GEM 2011 survey both opportunity motivated entrepreneurship rates (Opportunity TEA) and Necessity drivenentrepreneurship rates (Necessity TEA) are presented side by side in Table 10. The Table shows that the levels of necessityentrepreneurship in 2011 are lower than levels of opportunity entrepreneurship in all participating countries except Iran andPakistan.

24

Innovation Driven Economies

AustraliaBelgiumCzech RepublicDenmarkFinlandFranceGermanyGreeceIrelandJapanKoreaNetherlandsNorwayPortugalSingaporeSloveniaSpainSwedenSwitzerlandTaiwanUnited Arab EmiratesUnited KingdomUnited StatesAverageEfficiency Driven EconomiesArgentinaBrazilChileChinaColombiaCroatiaHungaryLatviaMalaysiaMexicoPeruPolandRomaniaRussiaSouth AfricaThailandTurkeyUruguayAverageFactor Driven EconomiesBangladeshGuatemalaIranPakistanVenezuelaAverage

Table 10: Opportunity and Necessity Entrepreneurship in GEM Participating countries

Opportunity TEA

8.784.765.424.254.314.834.155.874.863.854.446.985.995.975.392.964.165.135.526.485.145.809.075.40

13.7910.2316.6413.6415.994.614.058.434.247.5016.544.555.683.175.7914.857.575.579.05

9.2812.765.674.0610.788.51

Necessity TEA

1.58.592.09.331.14.851.042.022.141.303.24.75.301.341.07.441.50.35.751.38.891.252.621.26

6.884.566.499.745.382.591.953.07.501.875.124.304.091.233.183.693.751.853.90

3.496.477.704.264.405.26

25