consumer trends - bord iascaigh mharaand,events/jonathan,banks.pdf · consumer trends jonathan...

TRANSCRIPT

4 7 7 7

5

11 12 13

26

2

1 1 2 6

1 0 1

0 Inflation

Unemployment

Are we happy?

5.7

7.8 8.0 8.9

10.5 11.8 13.4

25.8 Misery Index

Sources: Haver Analytics/The Economist March 2014/CSO Ireland

11.9

Consumer Confidence Index

124

115

114

111

110

110

109

105

105

102

101

100

Indonesia

India

Philippines

China

UAE

Brazil

Thailand

Hong Kong

Denmark

Peru

Saudia Arabia

New ZealandSource: Nielsen Global Online Survey Q4 2013

77

Wealth and life expectancy...

IndiaIndonesia

China

Brazil

MexicoMalaysia

Korea

JapanR

2 = 0.91

0

5

10

15

20

25

30

35

69 71 73 75 77 79 81 83

Life expectancy

GD

P $

k p

er

cap

ita (

PP

P)

R² = 0.63

45

50

55

60

65

70

75

80

85

0 10000 20000 30000 40000 50000 60000

Source: CIA 2014

Life e

xpecta

ncy a

t bir

th

Per capita GDP (PPP)

The growth of modern retailing and economic development are highly correlated

GD

P P

er

Capita,

US $

Modern Format Retailing

India Indonesia

Malaysia

Thailand Philippines

Korea

Argentina

Taiwan

Singapore

U.K.

Germany

France

Brazil

33% 66% 100%

China

Evolution of formats in Europe

14% 15% 16% 17% 18% 19% 20% 22% 23% 24% 26% 27% 28% 29% 30% 31% 32% 32% 33% 34% 34% 35% 35% 35% 35% 36% 36% 36% 36% 12% 12%

13% 13% 15% 16%

17% 18%

19% 19% 20% 20%

21% 21% 21% 21% 22% 22% 22% 22% 23% 23% 22% 22% 23% 23% 23% 24% 24%

25% 26%

26% 27%

26% 25% 25%

25% 24%

25% 25%

26% 26% 26% 26%

27% 27% 27% 27% 27% 26% 27% 27% 28% 28% 28% 27% 28% 28%

22% 22%

21% 21%

21% 21% 20%

19% 19%

18% 17%

16% 16% 15% 15% 14% 14% 13% 12% 12% 12% 12% 11% 11% 10% 10% 10% 10% 9%

26% 25% 23% 22% 20% 19% 18% 16% 15% 14% 12% 10% 9% 8% 8% 7% 6% 6% 5% 5% 5% 4% 4% 4% 4% 3% 3% 3% 3%

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Trad Supret SSM LSM HMSource: Nielsen

Convenient to get to

Good value for money

Everything I need in the one shop

Display of products

Always wellstocked

High quality brandsWide range of well known brands

High quality prepared meal

Attractive andinteresting

promotions

Easy to quickly find

Low Price

Clean and hygienic Ease of parking

High quality fresh food

Efficient checkout countersPrivate

Labels

Loyalty Programs

Long opening hours

Wide range of freshmeat & fish

Page 7

Subliminal

Say it, mean it

Low

discriminators

High

DER

IV

ED

IM

PO

RTA

NC

E

High STATED IMPORTANCE

Low

Say it, don’t

mean it

23 attributes that differentiate

Source: Nielsen ShopperTrends GB

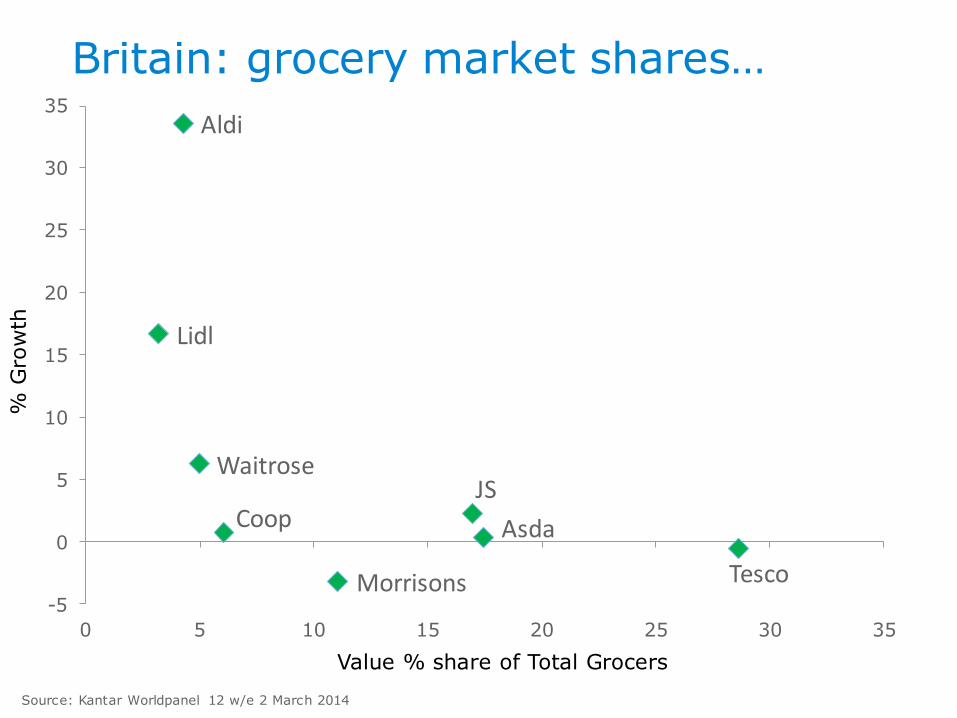

Discounters

Britain: grocery market shares…

Source: Kantar Worldpanel 12 w/e 2 March 2014

-5

0

5

10

15

20

25

30

0 5 10 15 20 25 30

% G

row

th

Value % share of Total Grocers

Tesco

Asda

JS

Morrisons

Aldi

Lidl

Waitrose

Coop

-5

0

5

10

15

20

25

30

35

0 5 10 15 20 25 30 35

Consumer confusion

• “Salad options are less fattening”

• “Organic (Bio) is better for me”

• “GM is bad for me”

• “Banning ads to kids will reduce obesity”

• “I’m too busy to eat/exercise properly”

• “Vegetarian options are healthier”

• “I need to eat more fruit and veg, but:

–an apple contains 4 tsp of sugar

–a third of all produce contains pesticide residue

–the fruit looks unappetising”

• “If it’s cheap it must be rubbish”

• “Moving food half-way round the world is wrong”

• “Fair trade can only be a good thing”

Consumer confusion

Source: The Daily Telegraph UK 16/9/12

Source: The Grocer 22 February, 2014

On average, how often do you eat fish (including seafood)?

3.3

3

2.9

2.8

2.8

2.7

2.6

2.6

2.3

2.3

2.1

1.9

1.9

1.7

1.7

1.7

1.7

Philippines

Malaysia

Singapore

Portugal

Thailand

Hong Kong

Indonesia

Japan

Spain

Taiwan

Vietnam

China

Norway

Denmark

South Korea

Russia

UAE

1.4

1.3

1.3

1.3

1.3

1.3

1.3

1.2

1.2

1.2

1.2

1.1

1.1

1.1

1

0.9

0.8

Latvia

Belgium

Brazil

Chile

NZ

Switzerland

Venezuela

Canada

Turkey

US

Colombia

Netherlands

Czech

Pakistan

Argentina

India

Hungary

Source: Nielsen Global Online Survey 2008

Occasions per week

Global average 1.6

1.6

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.5

1.4

1.4

1.4

1.4

1.4

1.4

1.4

Israel

France

Ireland

Italy

Poland

Sweden

UK

Estonia

Lithuania

Egypt

Australia

Austria

Finland

Germany

Greece

Mexico

S Africa

100

110

120

130

140

150

160

170

180

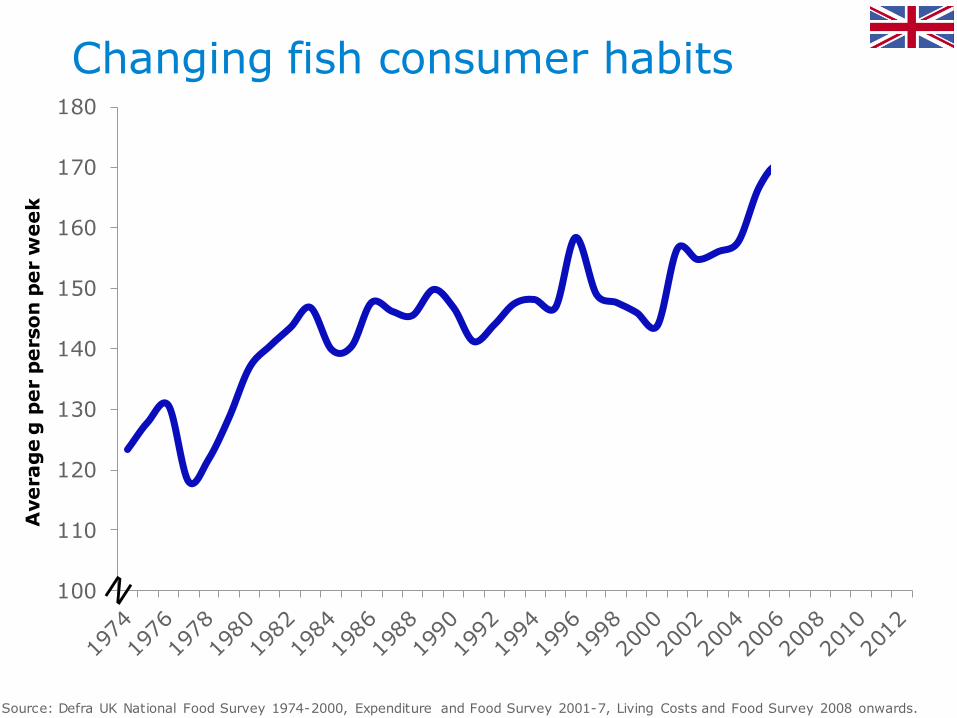

Changing fish consumer habits

Source: Defra UK National Food Survey 1974-2000, Expenditure and Food Survey 2001-7, Living Costs and Food Survey 2008 onwards.

Total fish

Avera

ge g

per

pers

on

per

week

Long term consumption changes

9

11

13

15

0

400

800

12001

974

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

Avera

ge g

per

pers

on

per

week

Fis

h %

sh

are

of p

rote

in

Meat

Fish

Source: Defra UK National Food Survey 1974-2000, Expenditure and Food Survey 2001-7, Living Costs and Food Survey 2008 onwards.

1,768 1,824 1,872 1,960 2,032

609 598 567 598 645 821 815 842 840 849

2,040 2,098 2,259 2,395 2,536

1,598 1,622 1,686

1,734 1,814

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2009 2010 2011 2012 2013

£m

reta

il s

ale

s v

alu

e

Source: Kantar Worldpanel

Beef

Fish

Poultry

Pork

Lamb

Robust competition from other proteins

Changing fish consumer habits

0

10

20

30

40

50

60

Ave

rage

g/p

ers

on

/we

ek

Ready meals

Take away fish

Salmon

White fish

Source: Defra UK National Food Survey 1974-2000, Expenditure and Food Survey 2001-7, Living Costs and Food Survey 2008

onwards

0

10

20

30

40

50

601974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Ready meals

White fish

Salmon

Shellfish

Takeaway fish

Avera

ge g

per

pers

on

per

week

Spend looks better than tonnage

705 721 749 760 766

187 192 181 181 192

705 709 755 793 856

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2009 2010 2011 2012 2013

Wet/Smoked Fish

Shellfish

Frozen Fish£m

reta

il s

ale

s v

alu

e

Source: Kantar Worldpanel

Private Label evolution: brand architecture

Basic

Regular

Premium Better for you

Better for the planet

Health & Wellness

Value for

money

Responsible consumption

80% of CEO’s believe their brand provides a superior customer experience

8% of their customers agree

Source: Bain & Company

How much do you agree with the following statements?

31%

32%

31%

40%

39%

37%

I would prefer to do business withcompanies that implemented

programs to give back to society

I would prefer to work for a companythat implemented programs to give

back to society

I would prefer to invest in companiesthat implemented programs to give

back to society

Source: Nielsen Global Online Survey October 2009:

Base: those who think it important that companies implement programs that contribute to improving society

Agree

strongly Agree

Closing thought: Profits, people, planet...

“It is not your duty to finish the work, but neither are you free to neglect it.”

Source: Rabbi Tarfon, Pirke Avot, The Talmud