concentration in the italian banking industry: future

TRANSCRIPT

Corso di Laurea magistrale (ordinamento ex D.M. 270/2004) in Amministrazione, Finanza e Controllo

Tesi di Laurea

Concentration in the Italian banking industry: future prospects. Relatore Prof.ssa Francesca Checchinato Laureando Jacopo Maria Parise Matricola 816090 Anno Accademico 2012 / 2013

i

C O N C E N T R A T I O N I N T H E I T A L I A N B A N K I N G

I N D U S T R Y : F U T U R E P R O S P E C T S

WRITTEN BY

Jacopo Maria Parise

RELATOR

Prof. Alain Chevalier

Paris, May 2013

ii

iii

A B S T R A C T

English Version :

During the last 3 decades, the aggregation process among different financial intermediaries has

represented the most clear evolving feature of all the major financial markets. Even the credit

market of the European countries, initially fragmented and characterized - especially in some

countries - by structures and conditions often underdeveloped has been interested by deep

changes, heading towards a progressive integration, although incomplete. Under the lens of the

concentration process undertaken since the beginning of the 80’s of the previous century, this

paper aims to analyse and deepen the concentration process in the Italian banking industry, in

order to produce an univocal judgment over its state of health after the financial crisis and its

strategic perspectives for the future. The following analysis is directed to underline modality

and effects of these changes, with particular attention to their relevance in terms of competition

and efficiency in the national credit market; integration in the European market and, through it,

in the global one.

Keywords: Concentration in Banking, European Union, M&As in banking, Italy.

JEL Classification: G34, L22, N20.

Version Française:

Au cours des trente dernières années, le processus d'agrégation de différents intermédiaires

financiers représente le point d'évolution majeur dans les marchés financiers. Bien

qu'initialement fragmenté et caractérise par une structuration ancienne, le marché du crédit

européen également a subit un profond changement amenant à une intégration progressive,

bien que partiellement incomplète. En considérant le processus de concentration mis en œuvre à

partir des années quatre-vingt, le but de notre recherche sera d' analyser la concentration du

secteur bancaire en Italie afin de mieux en comprendre l'état actuel après la crise financière de

2007 et d'élaborer ses prospectives stratégiques futures. Ainsi, nous soulignerons les modalités

et les effets d'une telle mutation, en se penchant plus particulièrement sur le concept de

concurrence et efficience du marché national du crédit, ainsi que sur le concept d'intégration au

niveau du marché européen et, plus généralement, au niveau global.

Mots-clés: Concentration dans le secteur bancaire, Union Européenne, M&As bancaires, Italie.

Classification JEL: G34, L22, N20.

iv

Versione Italiana:

Durante gli ultimi trent'anni, il processo di aggregazione tra intermediari finanziari di diversa

natura ha rappresentato il tratto evolutivo più evidente in tutti i maggiori mercati finanziari.

Anche il mercato creditizio europeo, inizialmente frammentato e caratterizzato - specialmente

per alcuni Stati - da strutture e condizioni arretrate, è stato interessato da un profondo

cambiamento, portando ad una progressiva integrazione, sebbene incompleta. Sotto la lente del

processo di concentrazione intrapreso dagli inizi degli anni Ottanta del secolo scorso, la presente

ricerca intende analizzare e approfondire la concentrazione del settore bancario in Italia, in

modo da giungere ad un giudizio univoco sul suo stato di salute dopo la Crisi Finanziaria del

2007 e le sue prospettive strategiche future. La seguente analisi sarà rivolta a sottolineare

modalità ed effetti di questi cambiamenti, in particolare in relazione ai concetti di concorrenza e

efficienza del mercato creditizio nazionale; dell'integrazione nel Mercato Europeo e, attraverso

questo, in quello globale.

Parole chiave: Concentrazione bancaria, Unione Europea, M&As tra banche, Italia.

Classificazione JEL: G34, L22, N20.

v

I N D E X

I N T R O D U C T I O N

A. Content of the research and analysis objective . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

B. Methodology of the research . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

C. Literature Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

C H A P T E R I - B A N K I N G C O N C E N T R A T I O N P R O C E S S

1.1 Environment evolution and competitive pressures: evidences from U.S.. . . . . . . . . . .13

1.2 Main determinants of banking concentration.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

1.3 Effects on the structure of credit systems. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

1.4 Effects on the stock performance of the banks involved. . . . . . . . . . . . . . . . . . . . . . . . . . . .29

1.5 Concluding remarks. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

C H A P T E R II - T H E E U R O P E A N B A N K I N G I N D U S T R Y

2.1 Concentration of the banking sector in Europe: general evolution . . . . . . . . . . . . . . . . .35

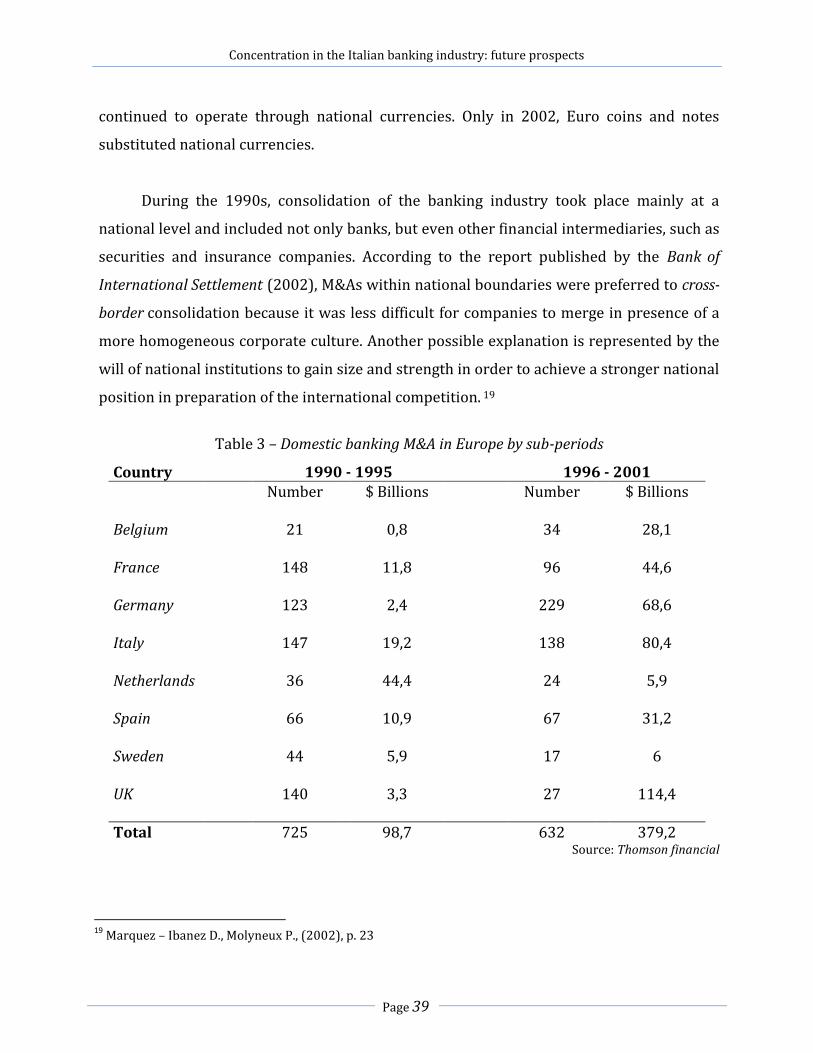

2.2 Cross – border M&As in Europe before the financial crisis . . . . . . . . . . . . . . . . . . . . . . . . .45

2.3 The 2007 financial crisis and consequences in Europe. . . . . . . . . . . . . . . . . . . . . . . . . . . . .52

2.4 Concentration among companies and European regulation. . . . . . . . . . . . . . . . . . . . . . . .61

2.5 Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

vi

C H A P T E R III - T H E I T A L I A N B A N K I N G I N D U S T R Y

3.1 Evolutionary profiles of the concentration process in Italy. . . . . . . . . . . . . . . . . . . . . . . . .69

3.2 Characteristics of concentration in Italy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .81

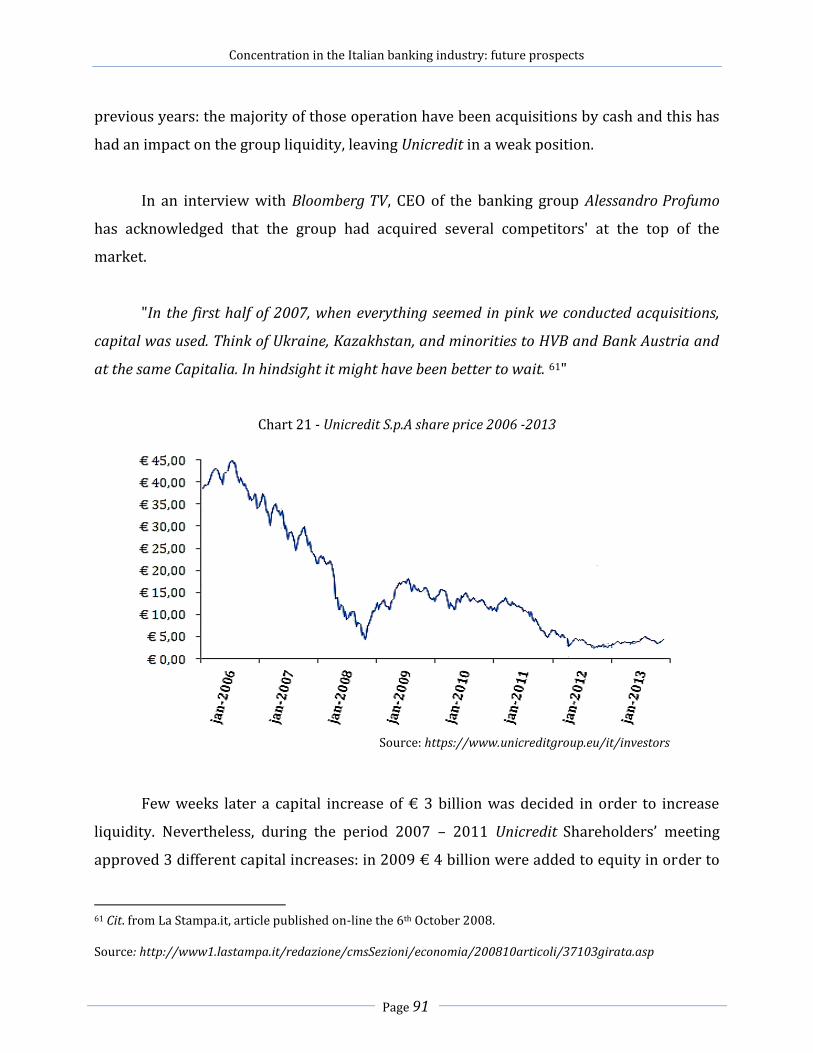

3.3 Focus: Unicredit Group. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .88

3.4 The 2007 financial crisis and the sovereign debt crisis. . . . . . . . . . . . . . . . . . . . . . . . . . . . .92

3.5 Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .100

C H A P T E R IV - C O N C L U D I N G R E M A R K S

4.1 Final considerations and main implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .105

4.2 Suggestions for future research. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .113

R E F E R E N C E S

D. Books . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .i

E. Report and Researches. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ii

F. Websites. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viii

T A B L E O F P I C T U R E S

G. Charts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ix

H. Tables. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .x

vii

viii

To my family, that with passion and sacrifice allowed me to reach this milestone.

ix

Concentration in the Italian banking industry: future prospects

Page 1

I N T R O D U C T I O N

A. Content of the research and analysis objective

“I believe that banking institutions are more dangerous to our liberties than standing

armies” – Thomas Jefferson, 1809.1

By this famous sentence, the third President of United States intended to underline

the milestone role that banks – and more in general credit market – have had for the

development of any country. Connecting people with deficits and surpluses of capitals,

allowing the first to finance their activities and second to save their money, has been

considered the basis of modern economies. Nevertheless, the crucial importance taken on

by these intermediaries often has crashed into opportunistic behaviours that have led to

tremendous consequences, bringing policy makers to change regulations in order to

prevent such situations and increase financial stability.

History of the economic capitalistic systems has been often characterized by a

continuous tension between regulation and free market, within a process that have led

policy makers in front of a trade – off between financial stability and economic growth.

“Disorder breeds socialism. […] The controls of socialism do well when times are bad,

but they inhibit progress when times are good. Order therefore breeds capitalism2”.

In periods where the ideology of regulation prevailed, the grater relevance given to

stability justified a pervading intervention of the State in the economy while, at the

opposite, when economic growth became a priority, free market paved the way to financial

1 “Debate Over the Recharter of the Bank Bill”, (1809)

2 Peter Temin, (1989) p. 133

Concentration in the Italian banking industry: future prospects

Page 2

innovation, deregulation and globalization. Even if the real challenge is represented by a

stable equilibrium in the trade-off, in the course of time we have assisted to a regular

turnover between these opposed positions.

“It [trade-off] emerged in a so clear way to draw economic and political cycles starting

the day after an epochal crisis and finishing with the burst of further3”.

Even if different cycles exist, one pattern has remained constant in the last 40 years:

the concentration process undertaken among intermediaries operating in different fields of

financial markets. Again, banks have played a fundamental role, having been not only

vanguards but even the key-players in the markets.

Despite the concept of bank was developed in Europe at least 600 years ago, market

structure of the European banking industries has been for long time highly fragmented and

closed within national boundaries, with the existence of different sub-markets where few

players used their oligopolistic power in order to maximize profits. A turning point has

been represented by the growing integration that has taken place after the II World War,

when European countries started to experience – initially within their boundaries and then

among them – the aggregation of many industrial companies and financial institutions

thanks to the progressive creation of a single market, an unified currency and common

rules.

The aim of this research paper is to study and better deepen the concentration

process in the banking industry both in a theoretical way, by analysing the main literature

produced, and in an applied way, by looking at concrete experiences. In particular, the focus

of the research will be represented by the analysis of changes occurred in the Italian

banking sector thanks to the presence of features that will help readers to better

understand the impact of concentration process over an entire economy.

3D’Apice V., (2013), p. 2

Concentration in the Italian banking industry: future prospects

Page 3

The objective of the analysis is, thus, to demonstrate that creation of the European

single market – and the increased level of competition reached – have determined a shove

to concentrate in order to face the grown need of stability and efficiency, to increase

market share and to reach the appropriate size for competing in a renovate and

international environment.

Concentration in the Italian banking industry: future prospects

Page 4

B. Literature Review

Much has been written to explore the theory and the cases of concentration in

industrial and financial sectors, often presenting controversial results. This paper takes into

consideration different author’s perspectives with the aim of finding, to the extent possible,

common points of view above the topic.

In the last decades researchers have decided to deepen the perspectives through

which analyze banks, allowing economists and practitioners to have a broader view about

the concentration process in the banking industry, its determinants and implications not

only for credit market, but more in general for the entire economy. As of the early 1990s,

empirical researches on the effects of banking concentration and competition were mainly

interested in understanding whether the traditional structure-conduct-performance (SCP)

model could be applied to the banking industry. Researches were aimed to investigate if

bank concentration or normative impediments to competition could create a “dangerous”

environment for banks, with implications in terms of performance and stability of the

entire system. These studies were characterized by testing the assumptions through the

application of simple measures of concentration – such as the Herfindahl-Hirschman Index

(HHI) or non-firm concentration ratio (CRn) – by focusing on the examination of the United

States market thanks to the definition of Metropolitan Statistical Areas (MSAs) and by

considering all sizes and types of banks equal. Typical empirical studies of bank

concentration and competition of this period fund that U.S. banks in more concentrated

local markets charged higher interest rate on SME loans and pay lower interest rates on

retail deposits (Berger and Hannan, 1989; Hannan 1991) and that their deposit rates were

slow to respond to changes in open – market interest rates (Hannan and Berger, 1991;

Neumark and Sharpe, 1992).

With the progress of time, literature went beyond the SCP hypothesis and tested a

number of different models of competition with alternative measures of competitiveness,

including indicators of market structure that took into consideration the possibility that

Concentration in the Italian banking industry: future prospects

Page 5

different sizes and types of commercial banks could affect competitive conditions

differently. Analyses, thus, have expanded to include indicators of efficiency, service quality,

risk of the banks and consequences for the economy as a whole.

Since the early 1990s, progresses have been made on a high number of fronts.

Researchers have recognized the problems with SCP model and tried other methods. For

example, some studies tested the relation between X – efficiency or scale efficiency and

concentration and market share in local U.S. banking markets, achieving evidences that

support the effect of both market power and efficiency on profitability (Berger, 1995; Frame

and Kamerschen, 1997). Other studies broadened analysis of concentration in banking

industry including also indicators for entry restrictions, regulation and other legal

impediments to bank competition. These researches have shown that financial regulation,

creditor and shareholder rights, banking and openness trade and entry have an important

effects on competition among banks and between banks and financial markets, with

significant consequences for economic growth (La Porta et al., 1997, 1998).

More recent studies stopped to consider credit market as a uniform environment

composed by an unique typology of players, theorizing that different sizes of banks may

affect competitive conditions differently. Small banks are often considered to be

“community banks” with different competitive advantages than large banks. Relative to

large banks, small banks in developed nations tend to serve smaller, more local customers

and to provide more retail-oriented rather than wholesale-oriented financial services (De

Young, Hunter and Udell; 2004). Following researches, having considered previous findings

as a point of departure, investigated whether banks of different size could deliver their

services using different technologies. Banking groups may have a comparative advantages

in lending technologies such as credit scoring that are based on “hard” quantitative data.

Small banks, on the contrary, could have comparative advantage in technologies based on

“soft” information, that is those information more difficult to quantify and transmit through

the communication channels typical of large banking organization (Stein, 2002; Berger and

Udell, 2002). In accord with these arguments, banking groups have been found to lend

Concentration in the Italian banking industry: future prospects

Page 6

proportionately less of their assets to SMEs (Kashyap, Berger and Scalise; 1995), to lend to

larger, older and more financially secure SMEs (Haynes, Ou and Berney; 1999), to have

shorter and less exclusive relationships (Berger et al.; 2002) and to lend more on an

impersonal basis and at longer distances (Berger et al. 2002). These new papers generally

have an international orientation that includes developing nations, a significant change

from the vast majority of the studies in the precedent literature.

A further step in the analysis of the credit markets, financial markets and, more in

general, the banking environment, became established when other studies started

distinguishing between concentration and broader measure of competition, such as entry

restrictions and legal impediments to bank activities. Investigators have, thus, expanded

their research field to include analysis on the effect that competition and consolidation in

the banking industry produce on economic growth, credit availability to SMEs and

performance of non – financial industries. The empirical researches brought to mixed

findings. Some studies, in fact, have found unfavorable effects from high concentration and

other restrictions to competition, including less new firms concentration, expansion and

employment, less economic growth and slower exit of mature companies (Black and

Strahan, 2002; Cetorelli and Strahan, 2002; Cetorelli, 2003). Other studies, instead, have

found favorable effects of bank concentration, such as greater access to credit by new firms

and other SMEs and higher growth rates (Cetorelli and Gambera, 2001; Bonaccorsi di Patti

and Gobbi, 2001; Zarutskie, 2003). In particular, some authors (Boyd and Runkle, 1993;

Mishkin, 1999) have claimed that concentration is a destabilizing element (concentration-

fragility view) due to the likelihood that these larger intermediaries could take more risks

due to the implicit “too big to fail” policies. Some studies have deepened the effect of a bank

concentration on the stability of a national financial market, claiming that concentration

leads to stability (concentration-stability view) because few large banks should be more

profitable, easier to monitor and more diversified, allowing them to better resist in front of

a shock (Allen and Gale, 2000).

Concentration in the Italian banking industry: future prospects

Page 7

A certain number of papers have examined the different competitive effects of

foreign – owned and state – owned banks. Some researchers have suggested that foreign –

owned banks could compete in different ways from domestic institutions. Foreign – owned

banks are, in fact, part of large banking groups and so they might have many competitive

advantages and disadvantages over domestic operators in serving multinational customers,

access to capital, use of technology and so on. However these institutions may also have

disadvantages depending on distance, the existence of different economic environments

and so on. Evidences on efficiency and profitability, however, have permitted to claim that

advantages of foreign – owned banks outweigh the disadvantages in developed nations

(Classens, Demirgüç-Kunt and Huizinga; 2001). Building on this work, other studies (Levine,

2003) found that regulatory restrictions on the entry of foreign banks, rather than foreign –

owned banks, are robustly linked with higher banks’ interest margin. Other researches,

instead, have investigated the possibility that state – owned banks could compete

differently from private banks due to the difference in objectives: compared to the private

banks’ profit and value maximization, in fact, state objective are usually represented by the

development of specific geographical areas or industries, the assistance to new

entrepreneurs, the expansion of the economic activities and so on. Many researches have

shown that large concentration of state – owned banks determines a weaker competition

and, in in the time, less favorable economic consequences (Caprio, Levine and Barth, 2001,

2004; Berger, Hasan and Klapper, 2004).

Lately, the academic production has shifted its attention to other developed

countries or developing countries and on the international comparison between these

countries. Most of the non – United States studies, however, consider the entire nation as a

single market, while several nations have had a different history and, thus, should have a

different credit market. For example, studies on the European Union credit market often

consider it as a single market due to the regulatory changes promoted by European policy

makers in order to create a single market. These studies (Goddard, Molyneus and Wilson,

2001; Dermine, 2003) typically have found that differences in profitability and

performance among banks placed in different nations still remain due to the different credit

Concentration in the Italian banking industry: future prospects

Page 8

market structures and the complexity in harmonizing them in a single market driven by

common rules.

Far from the possibility to include all the researches and relations analyzed in the

last twenty five years, the aim of this part of the research has been to briefly summarize the

most important contributes developed by academics and practitioners to understand how

changes in the size and market power of banks can influence the economy of a country.

According to the previous views, when the concentration of banks is not followed by a

process of deregulation, the economic environment is weakened due to the increased

market power belonging to the banks. If, on the contrary, the consolidation is accompanied

by a regulation that increases the competition between these intermediaries, through the

removal of barriers to entry or other restrictions, the process of concentration can lead not

only to greater system stability financial but also to improve the supply of credit both for

people and for companies.

Concentration in the Italian banking industry: future prospects

Page 9

C. Methodology of the research

Methodology applied to the following paper is:

Analytical: through the analysis of articles and previous researches it investigates

how and why banks have started to integrate by taking over other intermediaries operating

in the same market, (horizontal integration) or through acquisitions of companies operating

in a different position of the value chain (vertical integration).

Quali – quantitative: the subject under investigation is too wide to be simply

summarized through a numerical approach and too technical to be supported only by

observatory evidences. So the descriptive part will be integrated by numerical evidences

with the aim of providing more detailed data and supporting findings and implications.

Numerical evidences derive from secondary data, obtained mainly from periodical reports

of international economic institutions (ECB, IMF, Bank of Italy) and from mandatory

disclosures that banks and other intermediaries are obliged to produce according to law.

Deductive: even if it seems reductive to define the outputs of this paper as simply

depending on a deductive approach, several economic theories can be applied in order to

justify the concentration process, as in industrial sectors as in the financial industry. Case

studies provided in the paper have the aim of confirming or denying the economic theories

that, in the end, will be applied to the Italian banking industry in order to inductively

predict future prospects. A contribution to the deductive analysis will be provided by

specialized press reviews, in order to show examples and to link theoretical knowledge

with information and episodes coming from the reality of financial markets.

The extensive use of M&As in the banking industry has spread in Europe in

conjunction with the emergence of a more competitive banking market and has found

fundament in casual factors that have established a common denominator in the evolution

of the banking industry at an international level. It refers to the interaction of the so-called

Concentration in the Italian banking industry: future prospects

Page 10

exogenous environmental factors, as the deregulation process, technological innovation,

markets globalisation and the introduction of a single currency (Euro), that between the

end of 1980s and the beginning of 1990s have weakened the entry barriers in the main

European markets, preparing the ground for the entrance of international players in

domestic markets. The progressive intensification of the competitive pressures and the

resulting danger of market share erosion have imposed, thus, to banks an intense

restructuring process with the aim of restoring efficiency and profitability.

In consideration of these premises, this research has the goal of deepening the

evolution of the concentration process since now registered in the Italian banking industry,

both in the domestic market and in the European one. The purpose is firstly to isolate

casual factors that have led to improve the level of competition in the market and the

determiners that have pushed banks to use these strategies of external growth and,

secondly, the most significant macro-economic effects produced by consolidation.

In this respect, it was decided to structure the present work in four chapters.

First chapter provides the main theoretical background by analysing the rationale of

concentration. Thanks to the vast amount of time series available for the United States

banking system and relevant amount of studies focused on it; American credit market will

be used in order to better explain how different determinants - ascribable mainly to the

deregulation process undertaken in the last 30 years of the previous century, the diffusion

of technological innovation and the gradual globalization of markets - have changed the

external environment and have brought banks to concentrate. Chapter ends with an

explanation of the main effects related with the concentration process, distinguishing

between the effect on the credit market and the effects on the performance of the

operators involved.

Second chapter, after having analysed factors considered responsible of the change

in the competitive environment through the constitution of the European single market

Concentration in the Italian banking industry: future prospects

Page 11

(1993) and the European Monetary Union (1999), focuses on the different effects produced

by banking concentration. In particular, analysis intends to deepen the macro-economic

perspective with the aim of investigating how structure of European credit markets has

changed. Financial crisis of 2007 is taken into consideration separately mainly for two

different reasons: from an institutional point of view, crisis has led international policy

makers to change direction, moving from the deregulation process to a new regulatory

framework – with strong implications over financial markets and banks in particular –

while from banks’ internal point of view crisis has laid the foundations for a strategic

rearrangement of financial businesses. Chapter ends through the analysis of the European

regulation on control of concentration among companies – Regulation CEE N° 139/2004 –

issued with the aim of homologating national norms due to the risk of applying within the

European single market different rules.

Third chapter focuses its attention on the M&A phenomenon in the Italian banking

industry, started only at the beginning of 1990s, in order to underline its distinctive

features. In particular, after having underlined the reasons for the delay in the

consolidation process - justifications related to the presence of a market that for several

decades has been characterized by a lack of competition and efficiency, being divided in

different regional sub-markets few connected among them – fundamental characteristics of

the M&A process are described both under a quantitative point of view (number of M&As

realized, temporal distribution, main modalities used from the Italian banks) and

qualitative (territorial distribution and size of the banks involved in this process).

Fourth and last chapter has the goal to provide, summarized, the main results

reported in previous chapters and to underline possible future strategies of European and

Italian intermediaries in order to face the growing interconnection of the national markets

and the increased level of competition due to the change in the environment.

Concentration in the Italian banking industry: future prospects

Page 12

Concentration in the Italian banking industry: future prospects

Page 13

C H A P T E R I

B A N K I N G C O N C E N T R A T I O N P R O C E S S

1.1 Environmental evolution and competitive pressures: evidences from U.S

In the last 30 years, credit industry has been affected by a strong consolidation

process among banks, started in 1980s in United States and continued later in several other

developed countries. Fast expansion in M&As can be ascribed to the change in the

exogenous environmental factors that, from mid-1960s to the beginning of 1990s, have

interested the majority of the financial markets of the developed countries, deeply

transforming their structures and competitive dynamics: it refers to 1) the evolution in the

macro-economic environment, 2) the deregulation process undertaken in the financial

markets and 3) the technological evolution. These drivers, even if with different modalities

and intensities, have contributed to lower the entry barriers and, consequently, to increase

competitive pushes in the banking industries. In order to face this renovate environment,

banks started to pursue new strategies to bring back profitability to acceptable values. To

do that, banks adopted growth-based strategies, mainly ascribable to two different

categories: internal growth and external growth. Dynamics of internal growth consists in the

use of structures and resources already present inside the company in order to push the

growth while external growth is represented by the increase in company’s size thank to the

acquisition of one or more companies already operative. M&A operations – Merger and

Acquisition operations –became the more used means both from United States and

European banks, being considered the fastest way to acquire a larger dimension4.

In particular, according to the contingency theory, that claims the absence of the one

best way as theorized by Taylor and the existence of several different courses of action

depending from internal and external factors that influence any business activity, banks

4 Quarante U. (1990), p 37

Concentration in the Italian banking industry: future prospects

Page 14

have changed their business models in order to adapt themselves to a new and more

complex environment. First part of this chapter provides an analysis of the main

environmental changes taking into consideration United States financial market. Reason

underlying this choice are represented by the presence of a vast amount of time series

related to the American credit market that allow to have a numerical evidence around the

process of banking concentration.

Regarding the evolution of the macro-economic environment, a crucial role has been

played by inflation. The rise in inflation in the 1970s was strongly related with the

increases in oil prices engineered by OPEC. On 19 October 1973, the decision undertaken

by OPEC Gulf Members of a 5% monthly production cut until the total evacuation of Israeli

forces from all Arab territories occupied during the June 1967 war had taken place,

brought the oil price to rise from 3.65 $/barrel up to 11.65 $/barrel. The second oil price

rise came in 1979 with the Iranian revolution. During that period, price of Saudi Arabian

crude oil arrived at 28.00 $/barrel: inflation and unemployment rose in most countries5.

Chart 1 –Inflation in United States 1970 – 2012

Source: Federal Deposit Insurance Corporation - OECD

5 Kahn, (1985), p. 27

-

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

90,00

100,00

0,00%

5,00%

10,00%

15,00%

20,00%U.S Inflation Crude Oil Spot Price

Concentration in the Italian banking industry: future prospects

Page 15

Higher inflation brought to increase interest rate. In that period banks were

constrained by several regulations, such as the Regulation Q6, that didn’t permit to adapt

the rates of interests in function of the specific level of inflation. Many investors became

more sensitive in front of the yield differentials on different assets and the result was a

disintermediation process, through which clients took their money out of banks and started

purchasing higher yielding assets, weakening banks.

The impact of regulation, which is considered the second factor heavy influencing

the competitive environment of any industry, banking system included, has a deep impact

on market structure and, thus, on strategies and organizations of players within that

market. Since 1970s, regulation has been used in order to limit competition, due to the

implicit assumption of policy makers that limiting competition among credit institutions

was the only way to limit risk taking and thus, to guarantee stability of the financial system.

There have been several motivations to impose regulatory restrictions to banks’ activities.

According with Edey and Hviding (1995), direct control was used to allocate financing to

specific industries according with the economic development plan of Governments, to

restrict market access and competition in order to guarantee more stability, to protect

savers and to use banks as instruments of macroeconomic management.

“The shortest way to characterize the transformation of the banking industry is to say

that the emphasis has gone from regulation to competition. Indeed, in the first period,

regulation rate, entry restriction and charter limitation of banks (including the separation of

commercial and investment banking) have been used by regulators to limit competition. Other

regulatory facilities, like the lender of last resort and the deposit insurance, have been widely

implemented in order to prevent runs and instability in the banking system”7.

In particular, until the early 1970s financial markets were characterized by several

restrictions, including interest rate controls, quantitative investment restrictions on

7 Cit. Vives (1999), p. 2

Concentration in the Italian banking industry: future prospects

Page 16

financial institutions; line – of – business restrictions and regulations on ownership

linkages among financial institutions and restrictions on the entry of foreign financial

institutions.

Table 1 – Banking Industry regulation and deregulation in United States 1863 – 1999

Concentration in the Italian banking industry: future prospects

Page 17

From mid – 1970s, a significant process of regulatory reform has been undertaken in

many developed countries. This process, based on a shift towards more market – oriented

forms of regulation, cannot be seen as an independent pattern due to the presence of inter-

related factors, such as the diminishing effectiveness of traditional controls due to financial

innovation and rapid technological development; the development of various types of

regulatory avoidance – just as example, the rise in out of balance sheet methods of financing

– and the increased competition between financial institutions under different regulatory

environments8.

Regulatory reforms have brought several different benefits by giving to financial

firms more freedom to adopt the most efficient practices and by allowing them to develop

new products and services able to compete against non – bank financial companies that had

beforehand benefitted from the disintermediation process caused by the rise of inflation.

Second, deregulation and the increased level of competition obliged banks to take under

control efficiency by forcing the exit of inefficient firms and by encouraging the

consolidation of the financial system.

The third factor that has influenced the competitive environment of banks has been

the technological evolution. The development of Information Technology in order to collect,

store, process and distribute data has influenced (and still influences) banking activities for

two reasons: first, IT has modified the way in which customers can have access to banks’

services and products, mainly through automated channels, grouped under the name of

remote banking. The application of this technological progress to the banking activity has

permitted to overcome temporal and spatial boundaries, allowing banks to sell services and

products independently from the opening times of their branches (temporal boundaries)

and in geographical areas not touched before (spatial boundaries).

On the other hand, IT has contributed to the reduction of the costs associated with

the management of information by replacing paper–based and labor–intensive methods

with automated processes. The possibility of achieving cost reductions especially in the

8 Biggar, Heimler, (2005), p. 5

Concentration in the Italian banking industry: future prospects

Page 18

retail businesses, due to the reduction of labor force, the existence of scale and scope

economies, the rationalization of production and distribution structures, the

standardization of banking processes, the shorter response times and the improved

utilization of customer information have led banks to adopt these technologies.

According to the ECB (1999), however, technology cannot be considered the major

driving force for M&As among banks. Despite investments in IT are quite expansive, a

critical size in order to be able to amortize those costs and to remain competitive is not the

only solution banks have. Strategic alliances among banks currently exist, based on the

reciprocal incentives these operators may find in sharing IT development costs and in

providing interoperable systems, like common platforms for the use of ATMs, compatible

payment instruments and compatible technical standards. For the most part of the

literature that has analyzed the impact of technological development over financial and

non – financial industries, the focus of the research has been the cost side, claiming that

technological investments represent a possibility to lower costs and, thus, increase

efficiency. Under this perspective, banks should chose to invest in IT simply to have a

competitive advantage in front of direct competitors.

However, technological evolution has affected the competitive environment of

banks by increasing competition and allowing customers to better serve their interests

without passing through the banks. Edwards and Mishkin (1995), claimed that advance in

information and data processing technology have enabled non-bank competitors to

originate loans, transform these into marketable securities and sell them to obtain more

funding. Computer technology has destroyed the competitive advantage of banks by

lowering transaction costs and enabling non-bank financial institutions to evaluate credit

risk efficiently through the use of statistical method.

“When credit risk can be evaluated using statistical techniques, as in the case of

consumer and mortgage lending, banks have no longer an advantage in making loans. In

addition, these improvements have made easier for households corporations and financial

Concentration in the Italian banking industry: future prospects

Page 19

institutions to evaluate quality of securities, allowing business firms to borrow directly from

the public by issuing securities9”.

The advance in Information Technology, thus, before becoming an opportunity for

banks, has represented a threat caused by the increased number of competitors that have

weakened their supply of credit products and consequently profitability in their core

business.

To survive and maintain adequate profit levels, banks had to face different

alternatives, such as through the increase of lending activities towards riskier clients, by

providing other services not connected with interest rates and by pursuing new off –

balance sheet and derivatives activities. Both these possibilities have been strongly

criticized due to the excessive risk that banks may take.

Chart 2 – Rise in non-interest income for commercial banks in U.S 1970 - 2011

Source: Federal Deposit Insurance Corporation

Edward and Mishkin (1995) underlined that standard measure of commercial bank

profitability, such as ROE or ROA, don’t provide a clear picture of the state-of-health of this

industry. The reasons are mainly ascribable to the increase of non-traditional businesses of

banks.

9 Cit. Mishkin, (1995), p. 32

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

35,00%

40,00%

Concentration in the Italian banking industry: future prospects

Page 20

Chart 3 – Historical ROE and ROA for United States banks 1970 - 2012

Source: Federal Deposit Insurance Corporation

Nevertheless, in any industry the decline in profitability usually results in an exit

from that industry (often caused by defaults and bankruptcies) and in a transformation of

market share. This occurred in the United States during the 1980s through bank failures

and the beginning of a consolidation process of banking system.

Chart 4 – Bank failures in United States 1970 – 2012

Source: Federal Deposit Insurance Corporation

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

12,00%

14,00%

16,00%

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%ROE ROAROA ROE

0

100

200

300

400

500

600

Concentration in the Italian banking industry: future prospects

Page 21

Chart 5 –Credit Institute in United States 1970 - 2012

Source: Federal Deposit Insurance Corporation

In conclusion, the consolidation of the banking industry has started as an answer to

the changes in the environment that have led banks to lose part of their market share, all to

the good of non-banks intermediaries, and consequently part of their profitability. In order

to block the wave of defaults that have determined United States banking industry during

the 1980s and part of the 1990s, policy makers intervened through a deregulation process

that increased the opportunity for banks to grow and to restore a suitable level of

profitability. The reduction of constrains brought banks to extend their traditional

activities outside from their original boundaries, which can explain the M&A phenomenon

among banks operating in the same business or to differentiate into different business,

driven by goals of profitability or growth rate.

1.2 Main determinants of banking concentration.

Once understood as influences from outside are crucial in modifying business

performances, any player can have more than one justification in order to merge or

takeover other intermediaries. In particular, literature has classified several economic or

extra-economic reasons to explain why banks should conclude an M&A. Referring to the

multiple determinants that may drive a bank to aggregate itself with other banks, it proves

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

Concentration in the Italian banking industry: future prospects

Page 22

to be difficult to arrive at a classification univocal, well defined and able to include all the

possible motivations that can lead a banking company to carry out these operations of

external growth. Motivations around these processes vary in fact from situation to

situation. Nevertheless, it is possible to group all justifications into two different

categories: business economics and extra-business economics motivations.

All those situations that lead a bank to takeover or merge with other institutions

with the aim of increasing shareholder value or the economic performance are called

Business economics motivations. These are:

1. An increase in efficiency: the improvement of the operative efficiency among the

banks interested by mergers can be achieved in different ways. It can happen through the

recourse to economies of scale, depending on the possibility of lowering the average cost of

production thanks to the new size reached, or economies of scope, that allow to produce

goods or services jointly at a lower price compared with separated productions. Academic

studies, as reported by Berger and Humphrey (1994), have determined that scale effects

account for 5 per cent of the costs in smaller banks, while in large banks constant average

costs or diseconomies of scale prevail, due to the increase in coordination & control costs.

Regarding economies of scope, Berger and Humphrey showed that jointly production can

bring to a cost reduction of 5 per cent. The same authors, however, underlined that

managerial ability in defining the more appropriate combination of inputs in order to

minimize costs and maximize revenues is considered much more important than

scale/scope economies: they refer to the so-called X-efficiency as theorized by Leibenstein

(1966).

“Scale and scope economies in banking are not found to be important, except for the

smallest banks. X-efficiency, or managerial ability to control costs, is of much greater

magnitude - at least 20% of banking costs”10.

10

Berger A. N., Humprhrey D. B. (1994), p 1

Concentration in the Italian banking industry: future prospects

Page 23

2. Risk diversification: the creation of a stronger banking subject allows to better

diversify risks not only through a new and more complete portfolio of financial products

and services but even for the possibility of trading them in more sectors and geographical

areas. Hughes, Moon et. al (1999) showed that probability of default tended to decrease in

connection with consolidation strategies enhancing geographical diversification.

Nevertheless, consolidation can expose banks, such as other institutions, to managerial

moral hazard, being bank conglomerates too big to fail (Berger, 1998; De Nicolò, 2000;

Gorton and Winton, 2002).

3. An increase in the market power: studies conducted on the consolidation of the

banking industry in U.S in 1990s that have examined dynamic effects of bank M&As on

prices have found that mergers, and thus consolidation, have increased quality of banking

services thanks to superior branching networks, access to ATMs, etc. but even higher fees to

pay (Board of Governors of the Federal Reserve System, 2003). An Italian study of bank

M&As over the same topic has shown that in the short period banking services prices were

unfavorable to consumers while in the long term they became favorable. Panetta and

Focarelli (2004), authors of the research, considered as a possible justification of this

behavior the dominating effect of market power in the first period while, secondly,

efficiency allowed to lower prices. Berger and Hannan (1989) found that in more

concentrated local markets, banks charge higher rates on SME (Small and Medium

Enterprise) loans and pay lower rates on retail deposits. Neumark and Sharpe (1992)

obtained same results.

4. Investment opportunities (growth rate): growth rate can have an effect over the

concentration decision for two different reasons. Kocagil et al. (2002) empirically showed

that some banks with high growth rate experienced problems due to managerial and/or

structural inability to deal with high level of growth. Bidder banks, thus, may be interested

in purchasing these banks in order to better exploit their potential. On the other hand,

Moore (1996) found that banks could be interested in M&As even when the growth rate is

quite slow thanks to the possibility of increasing market value of the target.

Concentration in the Italian banking industry: future prospects

Page 24

On the contrary, extra-business economics motivations are ascribable to interests and

purposes of the management. In particular:

5. Private and opportunistic reasons of managers: according to this view, agency costs

can have an impact over the consolidation strategy of a bank due to the managerial interest

of enhancing salaries and prestige, diversifying personal risks or protecting their working

positions through the construction of empires, at the expense of shareholders (Bliss and

Rosen, 2001; Hughes et al., 2003).

6. Protective/defensive purposes: size of a bank can be considered as a deterrent

against M&As for different reasons. Large banks are more difficult to be acquired due to the

higher liquidity necessary to conclude the deal. Focarelli (2002), found in the Italian

banking sector a negative and statistically significant correlation between size and

probability to be acquired, while Wheelock and Wilson (2000) reported that smaller banks

are more probable to be acquired than large ones. Other possible explications are

represented by the possibility for large banks to fight against hostile acquisitions thank to

the bigger amount of resources available and by the difficulty for bidder banks to integrate

big intermediaries in their organizations.

Before concluding, it is important to underline that M&As cannot be considered all

equal. According with Sapienza (2002), it is possible to distinguish between in – market

mergers and out – market mergers. The firsts are characterized by combining banks that

belong to the same local market while the latters are represented by operations undertaken

in order to penetrate a new market. Evidences have shown that effects on market structure

are different. In the first case (in – market mergers) banks can decrease the number of

competitors and acquire more market power and adopt a cooperative behaviour. The result

is a less competitive environment where players can reduce their output and rise prices. On

the other hand, these kinds of mergers may offer more opportunity for cost savings due to

the possibility to remove the least efficient operations when they overlap. On the other

hand, out – market mergers are considered able to rise competition among market players

Concentration in the Italian banking industry: future prospects

Page 25

due to the interest of the bid company in penetrating the new market through the already

existing structure of the bank incorporated.

1.3 Effects on the structure of credit systems.

Focusing attention on one of the most widespread implication of the concentration

process just described, it leaps out the creation of a limited number of big financial groups

that tend to take on the role of key – actors in the events of the market, affecting

significantly the processes of transformation of the same.

Even if large – size bank has always existed (in relation with the specific historic

period), the impression is that this phenomenon has assumed innovative features in the

recent times in relation to:

- to the positions of domain taken by these subjects in many domestic markets, in

specific business areas and, in some cases, even in widely globalized activities;

- to the ever increasing internationalization of their activities and the dissemination of

distributive networks in a large number of countries in the world, not least the large

emerging markets;

- to the central position taken in the financial markets and in the wide range of

services and activities that these intermediaries provide in the markets.

These players take on a crucial importance in order to analyse and to understand the

processes of transformation of the credit structures and markets; and to direct the function

of government oversight, function become very sensitive in the context of globalization11.

In particular, according to the Group of Ten research (2001) conducted on the

Member Countries (Belgium, Canada, France, Italy, Japan, Netherlands , Sweden, United

11

Bottiglia R, (2009) p. 176

Concentration in the Italian banking industry: future prospects

Page 26

Kingdom and United States), it is possible to consider the effect of concentration on 4

different aspects of the credit system: 1) financial risks; 2) monetary policy; 3) competition

and credit, 4) interbank payment systems.

Financial risk

Potential effects of the concentration process of the credit market on the risk

exposition of banks are various and the final outcome cannot be generalized. In any case, it

seems possible to underline some features common in the different countries taken into

consideration.

The reason for which consolidation seems better able to limit the business risk is

linked with the diversification, especially geographic, of activities. Even in this case,

however, risk reduction is not a sure result since profitable returns depend on the

composition of the bank’s portfolio. After consolidating, some institutions have modified

the composition of their portfolios towards riskier activities increasing in this way the

operational risk. Other issues could depend on the increased complexity of the managerial

structure. Systemic financial risk – that is the risk determined by interdependencies in a

system or market, where the failure of a single entity or cluster of entities can cause

a cascading failure – can be transmitted more likely through larger – value activities of

bigger intermediaries: consolidation may have increased the likelihood that situations of

business disruption can cause strong repercussion on the whole system.

Empirical evidences suggest that the interdependences among the major players of

the banking industry in the last two decades are strongly increased in United States, Japan

and Europe. Causes can be ascribed mainly to globalisation of the markets and to the

existence of few national – giants with a strong influence on the national credit market.

Among the areas when the interdependences have grown more there are interbank loans,

relation on the OTC markets and payment and settlement systems.

Concentration in the Italian banking industry: future prospects

Page 27

Monetary policy

According to the Group of Ten (2001), consolidation process can have an impact on

the implementation on monetary policies due to the its impact on the interbank market or

the one used by Central Bank to modify the money supply. Consolidation may reduce the

level of competition on these markets, increasing the cost of liquidity for some banks and

hindering the process of arbitrage between the prevailing interest rates in the various

markets. Consolidation process may even alter the monetary transmission mechanism that

regulates Central Banks monetary decisions and operations towards the rest of the

economy. It can happen through the Monetary Channel – that is the transfer of changes in

interest rates controlled by the Central Bank to the other interest rates including rates on

deposits and bank lending – through an increase in the spread between active and passive

rates. The increase in the degree of concentration may also affect the delay with which

monetary policies are transmitted in two different ways:

- by reducing the delay, if these bigger players are able to process information more

rapidly thank to the improvement of the IT system;

- by increasing the delay, if banks are able to exploit the inertia of consumers in

response to changes in interests rates.

Concentration process may also affect the transmission mechanism through effects

on other 2 channels of monetary policy. These are primarily the Bank Lending Channel,

operating through monetary policy actions on the supply of bank loans, or through the

Channel of Financial Statements of companies, by modifying the value of collateral and the

availability of credit to lend.

Competition and credit

Effects of concentration on competition depend on specific condition of the demand

and supply of credit in the markets and in this juncture a relevant factor is represented by

Concentration in the Italian banking industry: future prospects

Page 28

the presence of barriers to entry. For retail banking products, empirical evidences on the

Group of Ten countries show that market are geographical segmented, with the prevalence

of few leading players with higher market power. Local markets usually coincide with

restricted areas of a country, such as Provinces, Regions, Metropolitan Cities or Cantons,

according with evidences that suggest families and SMEs benefit mainly from banking

services offered by companies located at a short distance.

Phenomenon just described may have negative repercussion on consumers, in

particular in the markets of SMEs loans, retail deposits and payment services. In particular,

SMEs make an important contribution to the economies of the countries surveyed: in agree

with the research conducted by The Group of Ten, in 1996, 66% of the total employment in

Europe depended on these companies while in United States the amount of employed was

around 50%. The reduction in the number of small banks, due to the consolidation, may

adversely affect credit availability for smaller customers. Bank resulting from the

consolidation process, in fact, could restructuring its portfolio through a credit expansion to

customers of larger size thanks to the greater amount of information available, capable of

reducing the information asymmetry between the parties and therefore the credit risk.

Insofar the credit relationships between small banks and SMEs are characterized by higher

information asymmetry, small companies must face an increasing difficulty in finding

financing. This problem is more serious in Europe because of the specific characteristics of

the credit market that, unlike the United States, has not been subjected to a

disintermediation process during the 1970s and 1980s.

Referring to wholesale banking products, investment banking services, currencies

market and derivatives, even if these markets usually have a national or international

dimension, consolidation process and the creation of bigger player may affect negatively

them due to the exercise of the grown market power.

Interbank payment systems

Bank consolidation has repercussion on the efficiency of the processes of payment

settlement and transfer of securities, on the level of competition between banks and market

Concentration in the Italian banking industry: future prospects

Page 29

infrastructures, on financial and operational risks. It has also implications to the approach

taken by Central Banks in the oversight of the interbank payment systems. Consolidation,

in fact, has led to concentrate payment and settlement flows in a smaller number of

counterparts within the credit, and more in general financial, markets.

The emergence of multinational institutions and specialized providers of services

involved in a number of systems for payments settlement and securities transactions, as

well as the growing interdependence in terms of liquidity between different systems,

contribute to further accentuating the role that payment and settlement systems may have

in the transmission of the effects of a financial contagion. For this reason, in the last 10

years Central Banks have made considerable efforts to reduce the systemic risks arising

from liquidity problems, in particular through the adoption of systems for real – time gross

settlement and urging the introduction of effective measures to control the risk in the net

settlement systems: European Union experienced, in 2007, a shift from the interbank

payment system TARGET to the newest one TARGET 2 (Trans-European Automated Real-

Time Gross Settlement Express Transfer System).

1.4 Effects on the stock performance of the banks involved.

The analysis of the effects of stock market performance of the banks involved in an

M&A has the aim of investigating whether these operations are able or not to create value

for the bidder banks and their shareholders. Technique typically used in these situations is

called “Event Studies” and represents an empirical analysis that allow to measure the impact

of an event, such as the merger announces, on the value of a specific company. Through this

technique, share price is divided in two different components: one is called Normal Return

and reflects “the expected return without conditioning on the event taking place” while the

second part of the share value is given by the Abnormal Return, that is “the actual ex-post

Concentration in the Italian banking industry: future prospects

Page 30

return of the security over the event minus the Normal Return of the firm over the same

period”12. For firm i and event date τ, the Abnormal Return (AR), is:

ARiτ = Riτ – E(Riτ|Xτ)

where Riτ is Actual Return, that is the share price at the observation date; E(Riτ|Xτ) is

the Normal Return. Xτ is the conditioning information for the normal return model. There

are two choices for modeling the Normal Return: the Constant Mean Return, which considers

Xτ is a constant and assumes that the mean return of a given security is constant through

time; and the Market Model, where Xτ is the market return, under the hypothesis of a stable

linear relation between the market return and the security return.

Abnormal Returns can be positive or negative. When positive, it means that market is

willing to bet on a value creation while, in the opposite, when Abnormal Return is negative,

it means that expected return from the event announced is consider to impact negatively on

the global performances of a company.

Unfortunately, literature does not permit to reach univocal conclusions about the

effect that M&As produce on economic performances of a company and, thus, on the share

price. Hannan and Wolken (1989), have shown that there is no clear evidence of a

production of new value, but only a redistribution of wealth among shareholders of the

acquired bank and sold. In particular, focusing on a total of 112 United States banks (43

buyers and 69 acquired) during the period from 1982 to 1987, researchers have shown

that, even if in presence of negative Abnormal Returns for bidder banks and positive for the

target ones during a period of +/- 15 days, outcomes have determined a null impact on the

creation of wealth for the shareholders involved in the deal.

The study conducted by Hawawini and Swary (1990) has come to slightly different

results, according to which the loss of value suffered by the bidder bank is more than offset

12

MacKinlay (1997), p 15

Concentration in the Italian banking industry: future prospects

Page 31

by the positive Abnormal Returns registered by the acquired bank. According to this view,

M&A operations seem to create value, on the whole, for shareholders interested.

Among the most recent studies, it should be mentioned Ferretti (2000), who has

deepened the M&As’ stock performance referring only to bidder banks. The results have

permitted to claim that United States market reactions were not univocal, being observed

both positive and negative reactions. Nevertheless, according to the study, in the more

recent time negative reactions have prevailed over the positive, clear evidence that

investors consider mergers as a transfer of wealth from bidder bank to the target one.

Referring to the European market, studies investigating stock performances before

and after an M&A are quite lesser due to the primacy of United States in the process of

aggregation and because of the methodological difficulties in analysing the highly

fragmented European banking market. However, among the main studies conducted, Cybo,

Ottone and Murgia (2000) claimed that, after having analysed 54 European M&As, in the

majority of the situations reactions have been strongly positive, considering those

operations as a future value creation. Authors have, thus, underlined that in domestic

operations, that is operations between counterparts of the same country, banks have

benefitted from the aggregation process. This study, however, does not reach the same

answer when it considers the cross – border aggregations.

Beitel and Schiereck (2001) obtained the same result through a study based on a

sample of 98 cross – border M&As conducted by European banks over EU and extra-EU

intermediaries coming from different fields of the financial markets during the period 1985

– 2000: by analysing the reflection of banks mergers on shareholders, they concluded that

cross – border mergers destroy value.

Concentration in the Italian banking industry: future prospects

Page 32

1.5 Concluding remarks

The aim of this first chapter is to provide the reader with the key-tools to understand

the process of concentration in the financial markets. Supported by evidences coming from

the U.S. market, it has been possible to verify how the concentration process among

banking intermediaries has been caused by changes in the external environmental. Rise of

inflation, mainly caused by the Vietnam War in the 1960s and the 2 oil shocks in the 1970s,

technological innovation, that permitted to non-banking intermediaries to enter in the

loan market by becoming able to evaluate credit risk, globalisation, which decreased the

entry barriers through a growing interconnection of national economies; and deregulation,

often required in front of overwhelming changes in a business ecosystem, have caused a

strong decline in banks’ core-business profitability, obliging them to find a way to restore

adequate level of profits.

Companies usually have 2 different possibilities to support the expansion of

activities: through the recourse to own resources (internal growth), or through the

acquisition of other companies (external growth). When a company merges or acquires

(M&A) another player, it means that it is financing its growth in an external way.

There are several factors that can explain the recourse of companies to M&As

operations. These can be grouped into 2 different categories: business economics

motivations, mainly ascribable to an increase in efficiency, risk diversification, an increase in

market power, investment opportunities; and extra-business economics motivations, that

refers to private and opportunistic reasons of managers or to protective/defensive purposes.

Changes in size and number of intermediaries in the credit markets can have severe

repercussions on the market itself under 4 different perspectives:

1) Financial risk: on one hand, geographical diversification allows banks to limit the impact

of systemic risk but not the operational risk, strongly related with the portfolio

Concentration in the Italian banking industry: future prospects

Page 33

composition. On the other hand, systemic risk can be transmitted with more intensity

through a single larger entity, increasing the likelihood of cascading failure.

2) Monetary policy: consolidation can have an impact on the way in which monetary policies

are implemented by Central Banks due to its impact on interbank market. Consolidation

may increase in fact the cost of liquidity and hinder the process of arbitrage between the

prevailing interest rates in the various markets.

3) Competition and credit: consolidation may have a negative impact on credit lending, in

particular for householders and SMEs. The reasons is manly ascribable to the intention of

large banking group to reduce the information asymmetry between the parts. Referring to

the wholesale market, concentration may affect negatively the environment due to the

increased market power.

4) Interbank payment system: consolidation reduces the number of payments in the

interbank system but increases the amount of each transfer. Concentration of payment

flows can increase the probability of contagion among intermediaries.

Consolidation process has been analysed even under the lens of the stock market

performance of the banks involved in the M&A operation. Through an Event Study, the

impact of the merge or acquisition is studied in order to quantify the Abnormal Return

over the share price Normal Return. A positive Abnormal Return means that investors

considers merge able to create value; a negative Abnormal Return, on the opposite, means

that value destruction is expected.

Concentration in the Italian banking industry: future prospects

Page 34

Concentration in the Italian banking industry: future prospects

Page 35

C H A P T E R II

T H E E U R O P E A N B A N K I N G I N D U S T R Y

2.1 Concentration of the banking sector in Europe: general evolution

During the 1990s, financial systems of the major European countries have been

subjected to deep changes that, with particular reference to the credit industry, have

determined a substantial growth of competition, until then remained at very low levels. In

front of these competitive pressures, banking intermediaries have reacted with a broad

recourse to external growth with the aim of implementing their supply, increasing

efficiency and obtaining the operative dimension essential to compete in an renovate

environment.

It is possible to describe the evolution of European banking industry under the lens

of the chronological evolution of the European integration. After the II World War,

European countries realized that the only way to prevent other destructive conflicts was to

begin a process of economic, social and politic integration. The first effort in this direction

was represented by the establishment of the Coal and Steel Community (Treaty of Paris,

1951) followed by the will of future integration in other economic areas. A turning point in

the European integration has been represented by the signature, in 1957, of the Treaty of

Rome that led to the foundation of the European Economic Community (EEC) aimed to

allow freedom of providing goods, services, labour and capital across Member States

within the Community. Although several progresses were achieved in some areas,

including the creation of common customs, the abolition of quotas and the free movement

of workers, full integration remained incomplete.

Concentration in the Italian banking industry: future prospects

Page 36

In June 1973, European Council issued the Directive on “The abolition of restrictions

of banks and other financial institutions13” with the aim of insuring an equal regulatory and

supervisory treatment of all financial firms operating in the same country. Even though the

underlying principles of the directive were widely shared by the Member States of the EEC,

the objectives were quite far to be reached due to the resistance of the individual State to

accept the opening of the domestic market to the advantage of foreign companies, banks

included. Focusing in particular to the banking industry, international competition of cross

– border services was severely restricted by 2 different factors: by the national regulations

on capital flows, that had a strong impact on the costs of operating internationally; and by

the absence of any coordination in banking supervision.

Table 2 – European banking regulation in 1980

Belgium Germany Denmark Spain France Italy Netherlands Portugal

Control of interest rates

x x x x x x

x

Capital controls

x

x x x x

x

Branch restrictions

x x

x

Foreign bank entry restriction

x

x

x

Credit ceilings

x x x x

x

Mandatory investment requirements

x x

x x

Restrictions on insurance

x x x x

x x

Sources: Emerson (1988), Bröke (1989), European Commission (1997)

13

Directive 73/183, EEC.

Concentration in the Italian banking industry: future prospects

Page 37

The need of harmonization pushed Member States to adopt, in 1977, the First

Banking Directive14, “The coordination of laws, regulations, and administrative provisions

relating to the taking up and pursuit of credit institutions”, through which the principle of

home country control was established. This principle stated that responsibility for the

supervision of credit institutions should have passed, gradually, from the host country to

the home country of the parent bank15.

Nevertheless, according to Dermine (2002), different factors contributed to leave

European market fragmented, ranging from the mismatch between the supervision,

committed to the Supervisory Authority of the host country that often imposed constraints

on the activities of the foreign institution; to the need of considering foreign branches as

new institutions and, thus, to provide them enough capital; up to the restrictions on capital

flows. The inability to agree on a common set of rules brought to the definition of a new

approach toward European banking integration that culminated, in 1989, through the issue

of the Second Banking Directive16.

The main innovation was to allow foreign banks to establish branches and to

provide a set of services in a host country without waiting for further authorizations, being

considered enough to prove that a bank was authorized to provide such services in the

home State17. The removal of regulatory constraints that obstructed banking companies to

carry out cross - border activities, therefore, has meant that banks could compete in open

markets, both inside the national borders and outside from them. The recognition of the

Second Banking Directive, thus, has expanded the geographical boundaries of the

competitive arena in which banks operate, contributing to change widely the environment. 14