*computation of goodwill - thammasat business school value of identifiable net assets 1,000,000...

TRANSCRIPT

3-1

Problem 2-1 Current Assets 85,000 Plant and Equipment 150,000 Goodwill* 100,000 Liabilities 35,000 Common Stock [(20,000 shares @ $10/share)] 200,000 Other Contributed Capital [(20,000 × ($15 – $10))] 100,000

Acquisition Costs Expense 20,000 Cash 20,000 Other Contributed Capital 6,000 Cash 6,000

To record the direct acquisition costs and stock issue costs * Goodwill = Excess of Consideration of $335,000 (stock valued at $300,000 plus debt assumed of $35,000) over Fair Value of Identifiable Assets of $235,000 (total assets of $225,000 plus PPE fair value adjustment of $10,000) Problem 2-2 Acme Company Balance Sheet October 1, 2011 (000) Part A.

Assets (except goodwill) ($3,900 + $9,000 + $1,300) $14,200 Goodwill (1) 1,160 Total Assets $15,360 Liabilities ($2,030 + $2,200 + $260) $4,490 Common Stock (180 × $20) + $2,000 5,600 Other Contributed Capital (180 × ($50 – $20)) 5,400 Retained Earnings (130) Total Liabilities and Equity $15,360

(1) Cost (180 × $50) $9,000 Fair value of net assets acquired:

Fair value of assets of Baltic and Colt $10,300

Less liabilities assumed 2,460 7,840 Goodwill $1,160 Part B. Baltic 2012: Step1: Fair value of the reporting unit $6,500,000 Carrying value of unit: Carrying value of identifiable net assets 6,340,000 Carrying value of goodwill 200,000*

3-2

Total carrying value 6,540,000 *[(140,000 x $50) – ($9,000,000 – $2,200,000)] The excess of carrying value over fair value means that step 2 is required. Step 2: Fair value of the reporting unit $6,500,000

Fair value of identifiable net assets 6,350,000 Implied value of goodwill 150,000 Recorded value of goodwill 200,000 Impairment loss $ 50,000

(because $150,000 < $200,000) Colt 2012: Step1: Fair value of the reporting unit $1,900,000

Carrying value of unit: Carrying value of identifiable net assets $1,200,000 Carrying value of goodwill 960,000*

Total carrying value 2,160,000 *[(40,000 x $50) – ($1,300,000 – $260,000)] The excess of carrying value over fair value means that step 2 is required. Step 2: Fair value of the reporting unit $1,900,000

Fair value of identifiable net assets 1,000,000 Implied value of goodwill 900,000 Recorded value of goodwill 960,000 Impairment loss $ 60,000

(because $900,000 < $960,000) Total impairment loss is $110,000. Journal entry: Impairment Loss $110,000

Goodwill $110,000 Problem 2-4

Part A January 1, 2011 Accounts Receivable 72,000 Inventory 99,000 Land 162,000 Buildings 450,000 Equipment 288,000 Goodwill* 54,000 Allowance for Uncollectible Accounts 7,000 Accounts Payable 83,000 Note Payable 180,000 Cash 720,000 Liability for Contingent Consideration 135,000

3-3

*Computation of Goodwill Cash paid ($720,000 + $135,000) $855,000 Total fair value of net assets acquired ($1,064,000 - $263,000) 801,000 Goodwill $ 54,000 Part B January 2, 2013

Liability for Contingent Consideration 135,000 Cash 135,000

Part C January 2, 2013

Liability for Contingent Consideration 135,000 Income from Change in Estimate 135,000

Problem 3-1 P COMPANY AND SUBSIDIARY Consolidated Balance Sheet Workpaper November 30, 2011

P S Eliminations Noncontrolling Consolidated Part I Company Company Dr. Cr. Interest Balance Current Assets 880,000 260,000 1,140,000 Investment in S Company 190,000 (1) 190,000 Difference between Implied and Book Value

(1) 71,111 (2) 71,111

Long-term Assets 1,400,000 400,000 (2) 71,111 1,871,111 90,000 40,000 130,000 Other Assets

Total Assets 2,560,000 700,000 3,141,111

Current Liabilities 640,000 270,000 910,000 Long-term Liabilities 850,000 290,000 1,140,000 Common Stock:

P Company 600,000 600,000 S Company 180,000 (1) 180,000

470,000 470,000

Retained Earnings P Company S Company (40,000) (1) 40,000

Noncontrolling Interest (2) 21,111 21,111 21,111 Total Liabilities and Equity 2,560,000 700,000 322,222 322,222 3,141,111

Part II

Current Assets 780,000 280,000 1,060,000 Investment in S Company 190,000 (1) 190,000 Difference between Implied & Book Value

(2) 8,889 (1) 8,889

Long-term Assets 1,200,000 400,000 (2) 8,889 1,591,111 Other Assets 70,000 70,000 140,000

Total Assets 2,240,000 750,000 2,791,111

Current Liabilities 700,000 260,000 960,000 Long-term Liabilities 920,000 270,000 1,190,000

3-4

Common Stock: P Company 600,000 600,000 S Company 180,000 (1) 180,000

Retained Earnings P Company 20,000 20,000 S Company 40,000 (1) 40,000

Noncontrolling Interest (1) 21,111 21,111 21,111 Total Liabilities and Equity 2,240,000 750,000 228,889 228,889 2,791,111

(1) To eliminate investment account and create noncontrolling interest account (2) To allocate the difference between implied value and book value to long-term assets. Computation and Allocation of Difference (Case 2) Parent Non- Entire Share Controlling Value Share Purchase price and implied value 190,000 21,111 211,111* Less: Book value of equity acquired 198,000 22,000 220,000 Difference between implied and book value (8,000) (889) (8,889) Decrease long-term assets to fair value 8,000 889 8,889 Balance - 0 - - 0 - - 0 – * $190,000/.90 Problem 3-9 Part A Computation and Allocation of Difference Schedule Parent Non- Total Share Controlling Value Share Purchase price and implied value $5,800,000 644,444 6,444,444* Less: Book value of equity acquired: Common stock (5,250,000 x .90) 4,725,000 525,000 5,250,000 Other contributed capital 356,400 39,600 396,000 Retained earnings 1,732,500 192,500 1,925,000 Less: Treasury stock (1,080,000) (120,000) (1,200,000) Total book value 5,733,900 637,100 6,371,000 Difference between implied and book value 66,100 7,344 73,444 Plant assets (66,100) (7,344) (73,444) Balance - 0 - - 0 - - 0 - *$5,800,000/.90

4 - 5

Pope Company and Subsidiary Worksheet, January 1, 2009 Eliminations Part B Pope

Company Sun

Company Debit Credit

Noncontrolling Interest

Consolidated Balances

Cash 297,000 165,000 462,000Accounts Receivable 432,000 468,000 900,000Notes Receivable 90,000 (1) 90,000 Inventory 1,980,000 1,447,000 3,427,000Investment in Sun Company 5,800,000 (2) 5,800,000 Difference between Implied and & Book Value (2) 73,444 (3) 73,444 Plant and Equipment (net) 5,730,000 3,740,000 (3) 73,444 9,543,444Land 1,575,000 908,000 2,483,000

Total $15,904,000 $6,728,000 $16,815,444

Accounts Payable 698,000 247,000 945,000Notes Payable 2,250,000 110,000 (1) 90,000 2,270,000Common Stock ($15 par):

Pope Company 4,500,000 4,500,000Sun Company 5,250,000 (2)5,250,000

Other Contributed Capital Pope Company 5,198,000 5,198,000Sun Company 396,000 (2) 396,000

Treasury Stock Held: Sun Company (1,200,000) (2)1,200,000

Retained Earnings Pope Company 3,258,000 3,258,000Sun Company 1,925,000 (2)1,925,000

Noncontrolling Interest (2) 644,444 644,444 644,444Total $15,904,000 $6,728,000 7,807,888 7,807,888 $16,815,444

(1) To eliminate intercompany note receivable and note payable (2) To eliminate Investment in Sun Company and create noncontrolling interest account (3) To allocate the difference between implied and book value to subsidiary plant and equipment. Problem 4-1 Journal Entries - Cost Method

Year Net Income

(Loss) Cumulative Net

Income Cumulative Dividends

Undistributed Income

2009 1,997,800 1,997,800 500,000 1,497,800

2010 476,000 2,473,800 1,000,000 1,473,800

2011 (179,600) 2,294,200 1,500,000 794,200 2012 (323,800) 1,970,400 2,000,000 (29,600)

Part A – Cost Method 2009 Investment in Singer Co. 4,972,000

4 - 6

Cash 4,972,000 Cash (.90)($500,000) 450,000 Dividend Income 450,000 2010 Cash (.90)($500,000) 450,000 Dividend Income 450,000 2011 Cash (.90)($500,000) 450,000 Dividend Income 450,000 2012 Cash (.90)($500,000) 450,000 Dividend Income 423,360 Investment in Singer Co. (.90 × $29,600) 26,640 To account for liquidating dividend

Part B – Partial Equity Method 2009 Investment in Singer Co. 4,972,000 Cash 4,972,000

Cash (.90)($500,000) 450,000 Investment in Singer Co. 450,000

Investment in Singer Co. 1,798,020 Equity in Subsidiary Income 1,798,020 (.90)($1,997,800) 2010 Cash (.90)($500,000) 450,000 Investment in Singer Co. 450,000

Investment in Singer Co. 428,400 Equity in Subsidiary Income 428,400 (.90)($476,000) Problem 4-1 (continued) 2011 Cash (.90)($500,000) 450,000 Investment in Singer Co. 450,000

Equity in Subsidiary Income (.90)($179,600) 161,640 Investment in Singer Co. 161,640 2012 Cash (.90)($500,000) 450,000 Investment in Singer Co. 450,000

Equity in Subsidiary Income (.90)($323,800) 291,420 Investment in Singer Co. 291,420

Part C – Complete Equity Method

Computation and Allocation of Difference between Implied and Book Value Acquired

4 - 7

Parent Non- Entire Share Controlling Value Share Purchase price and implied value 4,972,000 552,444 5,524,444 * Less: Book value of equity acquired: 4,961,160 551,240 5,512,400 Difference between implied and book value 10,840 1,204 12,044 Undervalued depreciable assets (15 year life) (10,840) (1,204) (12,044) Balance - 0 - - 0 - - 0 - * $4,972,000/.90 2009 Investment in Singer Co. 4,972,000 Cash 4,972,000

Cash (.90)($500,000) 450,000 Investment in Singer Co. 450,000

Investment in Singer Co. 1,798,020 Equity Income (.90)($1,997,800) 1,798,020

Equity in Subsidiary Income ($10,840/15 years) 723 Investment in Singer Co. 723 2010 Cash (.90)($500,000) 450,000 Investment in Singer Co. 450,000

Investment in Singer Co. 428,400 Equity Income (.90)($476,000) 428,400

Equity in Subsidiary Income ($10,840/15 years) 723 Investment in Singer Co. 723

4 - 8

2011 Cash (.90)($500,000) 450,000 Investment in Singer Co. 450,000

Equity in Subsidiary Income (.90)($179,600) 161,640 Investment in Singer Co. 161,640

Equity in Subsidiary Income ($10,840/15 years) 723 Investment in Singer Co. 723 2012 Cash (.90)($500,000) 450,000 Investment in Singer Co. 450,000 Equity in Subsidiary Income (.90)($323,800) 291,420 Investment in Singer Co. 291,420 Equity in Subsidiary Income ($10,840/15 years) 723 Investment in Singer Co. 723 Problem 4-2 Part A – Parry Corporation uses the cost method. If the cost method is used, Parry Corporation recognizes dividends received as income.

Part B Parry Corporation and Subsidiary Consolidated Statements Workpaper Workpaper - Cost Method For the Year Ended December 31, 2009

Eliminating Entries

Parry Corp.

Sent Company Dr. Cr.

Consolidated Balances

Income Statement Sales 476,000 154,500 630,500 Dividend Income 3,500 (1) 3,500

Total Revenue 479,500 154,500 630,500 Cost of Goods Sold 285,600 121,000 406,600 Other Expenses 45,500 29,500 75,000

Total Cost and Expense 331,100 150,500 481,600

Net Income to Retained Earnings 148,400 4,000 3,500 148,900 Eliminating Entries

Parry Corp.

Sent Company Dr. Cr.

Consolidated Balances

Retained Earnings Statement Retained Earnings 1/1

Parry Corporation 76,000 76,000 Sent Company 19,500 (2) 19,500

Net Income from above 148,400 4,000 3,500 148,900 Dividend Declared

4 - 9

Parry Corporation (17,500) (17,500)

Sent Company (3,500) (1) 3,500 0 Retained Earnings 12/31 206,900 20,000 23,000 3,500 207,400

Balance Sheet Cash 84,400 29,000 113,400 Accounts Receivable 76,000 56,500 132,500 Inventory 12/31 49,500 36,500 86,000 Investment in Sent Company 140,000 (2) 140,000 Difference between Implied and Book Value (2) 20,500 (3) 20,500 Land 4,000 12,000 (3) 20,500 36,500

Total Assets 353,900 134,000 368,400

Accounts Payable 27,000 14,000 41,000 Common Stock:

Parry Corporation 120,000 120,000

Sent Company 100,000 (2) 100,000 Retained Earnings from above 206,900 20,000 23,000 3,500 207,400

Total Liabilities and Equity 353,900 134,000 164,000 164,000 368,400 (1) To eliminate intercompany dividends (2) To eliminate investment in Sent Company (3) To eliminate difference between implied and book value

4 - 10

Computation and Allocation of Difference between Implied and Book Value Acquired Parent Non- Entire Share Controlling Value Share Purchase price and implied value 140,000 0 140,000 Less: Book value of equity acquired: 119,500 0 119,500 Difference between implied and book value 20,500 0 20,500 Undervalued land (20,500) (0) (20,500) Balance - 0 - - 0 - - 0 - Problem 4-7 Price Company and Subsidiary Consolidated Statements Workpaper Workpaper - Cost Method For the Year Ended December 31, 2013

Eliminating Entries Price Company

Score Company Dr. Cr.

Noncontrolling Interest

Consolidated Balance

Income Statement

Sales 1,420,000 500,000 1,920,000 Dividend and Interest Income 52,500 (3) 45,000 (4) 7,500

Total Revenue 1,472,500 500,000 1,920,000

Cost of Goods Sold 822,000 242,000 1,064,000 Other Expenses 250,500 124,000 (4) 7,500 367,000

Total Cost and Expense 1,072,500 366,000 1,431,000

Net Income 400,000 134,000 489,000 Noncontrolling Interest 13,400 * (13,400)

Net Income to Retained Earnings 400,000 134,000 52,500 7,500 13,400 475,600

Retained Earnings Statement

Retained Earnings 1/1 Price Company 687,000 (1) 108,000 795,000 Score Company 210,000 (5) 210,000

Net Income from above 400,000 134,000 52,500 7,500 13,400 475,600 Dividends Declared

Price Company (70,000 ) (70,000) Score Company (50,000 ) (3) 45,000 (5,000)

Retained Earnings 12/31 1,017,000 294,000 262,500 160,500 8,400 1,200,600

* $134,000 × .10 = $13,400.

4 - 11

Eliminating Entries

Price

Company Score

Company Dr. Cr. Noncontrolling

Interest Consolidated

Balance

Balance Sheet

Cash 109,000 78,000 187,000 Accounts Receivable 166,000 94,000 260,000 Note Receivable 75,000 (2) 75,000 Inventory 12/31 309,000 158,000 467,000 Investment in Score Company 450,000 (1) 108,000 (5) 558,000 Difference b/w Implied & Book Value (5) 50,000 (6) 50,000 Plant and Equipment 940,000 420,000 1,360,000 Land 160,000 70,000 230,000 Goodwill (6) 50,000 50,000

Total 2,209,000 820,000 2,554,000

Accounts Payable 132,000 46,000 178,000 Notes Payable 300,000 120,000 (2) 75,000 345,000 Common Stock:

Price Company 500,000 500,000 Score Company 200,000 (5) 200,000

Other Contributed Capital Price Company 260,000 260,000 Score Company 160,000 (5) 160,000

Retained Earnings from above 1,017,000 294,000 262,500 160,500 8,400 1,200,600 Noncontrolling Interest 1/1 (5) 62,000 ** 62,000

Noncontrolling Interest 12/31 70,400 70,400

2,209,000 820,000 905,500 905,500 2,554,000

** $50,000 + [($210,000 – $90,000) x .10] = $62,000

(1) To establish reciprocity/convert to the equity method ($210,000 - $90,000) × .90 (2) To eliminate intercompany receivables and payables (3) To eliminate intercompany dividends (4) To eliminate intercompany interest expense and income (5) To eliminate investment in Score Company and create noncontrolling interest account (6) To allocate the difference between implied and book value

Computation and Allocation of Difference between Implied and Book Value Acquired

Parent Non- Entire Share Controlling Value Share Purchase price and implied value 450,000 50,000 500,000 *

4 - 12

Less: Book value of equity acquired: 405,000 45,000 450,000 Difference between implied and book value 45,000 5,000 50,000 Goodwill (45,000) (5,000) (50,000) Balance - 0 - - 0 - - 0 - *$450,000/.90 Problem 5-1 Calculations: Computation and Allocation of Difference Schedule Parent Non- Entire Share Controlling Value Share Purchase price and implied value $2,800,000 700,000 3,500,000 * Less: Book value of equity acquired 1,200,000 300,000 1,500,000 Difference between implied and book value 1,600,000 400,000 2,000,000 Equipment (net) ($1,500,000 - $600,000) (720,000) (180,000) (900,000) Balance 880,000 220,000 1,100,000 Goodwill (880,000) (220,000) (1,100,000) Balance -0- -0- -0- *$2,800,000/.80 Depreciation of difference allocated to Palmero ($720,000/10) $72,000 Depreciation of difference allocated to Santos ($180,000/10) $18,000 Part A 2011 (1) Beginning Retained Earnings-Santos Co. 1,000,000 Capital Stock- Santos Co. 500,000 Difference between Implied and Book Value 2,000,000 Investment in Santos Co. 2,800,000 Noncontrolling Interest 700,000 To eliminate investment account and create noncontrolling interest account (2) Depreciation Expense 90,000 Property and Equipment (net) ($900,000 - $90,000) 810,000 Goodwill 1,100,000 Difference between Implied and Book Value 2,000,000 To allocate and depreciate the difference between implied and book value Alternative to entry (2) (2a) Property and Equipment (net) 900,000 Goodwill 1,100,000 Difference between Implied and Book Value 2,000,000 (2b) Depreciation Expense 90,000

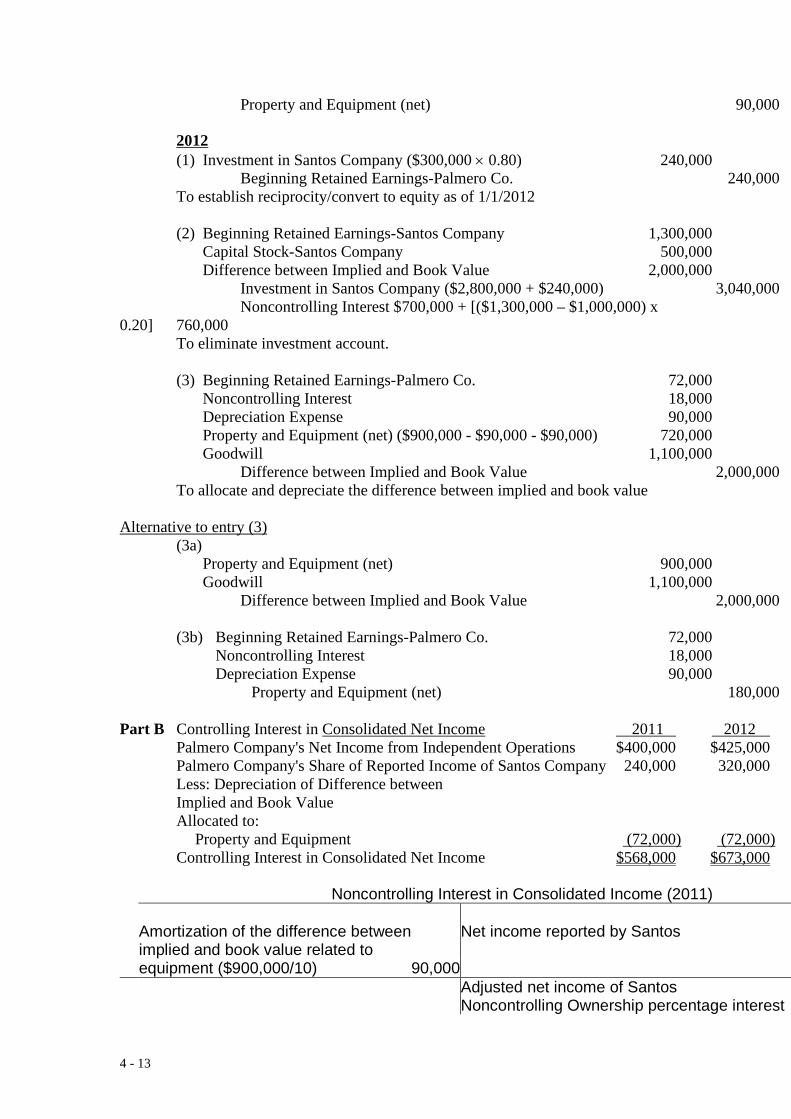

4 - 13

Property and Equipment (net) 90,000 2012 (1) Investment in Santos Company ($300,000 × 0.80) 240,000 Beginning Retained Earnings-Palmero Co. 240,000 To establish reciprocity/convert to equity as of 1/1/2012 (2) Beginning Retained Earnings-Santos Company 1,300,000 Capital Stock-Santos Company 500,000 Difference between Implied and Book Value 2,000,000 Investment in Santos Company ($2,800,000 + $240,000) 3,040,000 Noncontrolling Interest $700,000 + [($1,300,000 – $1,000,000) x 0.20] 760,000 To eliminate investment account. (3) Beginning Retained Earnings-Palmero Co. 72,000 Noncontrolling Interest 18,000 Depreciation Expense 90,000 Property and Equipment (net) ($900,000 - $90,000 - $90,000) 720,000 Goodwill 1,100,000 Difference between Implied and Book Value 2,000,000 To allocate and depreciate the difference between implied and book value Alternative to entry (3) (3a) Property and Equipment (net) 900,000 Goodwill 1,100,000 Difference between Implied and Book Value 2,000,000 (3b) Beginning Retained Earnings-Palmero Co. 72,000 Noncontrolling Interest 18,000 Depreciation Expense 90,000 Property and Equipment (net) 180,000 Part B Controlling Interest in Consolidated Net Income 2011 2012 Palmero Company's Net Income from Independent Operations $400,000 $425,000 Palmero Company's Share of Reported Income of Santos Company 240,000 320,000 Less: Depreciation of Difference between Implied and Book Value Allocated to: Property and Equipment (72,000) (72,000) Controlling Interest in Consolidated Net Income $568,000 $673,000 Noncontrolling Interest in Consolidated Income (2011) Amortization of the difference between Net income reported by Santos implied and book value related to equipment ($900,000/10) 90,000 Adjusted net income of Santos Noncontrolling Ownership percentage interest

4 - 14

Noncontrolling Interest in Consolidated Net Income Controlling Interest in Consolidated Income (2011) Palmero Company's net income from its independent operations Palmero Company's share of the adjusted income of Santos Company (.8 X $210,000) Controlling Interest in Consolidated Net Income Noncontrolling Interest in Consolidated Income (2012) Amortization of the difference between Net income reported by Santos implied and book value related to equipment ($900,000/10) 90,000 Adjusted net income of Santos Noncontrolling Ownership percentage interest Noncontrolling Interest in Consolidated Net Income Controlling Interest in Consolidated Income (2012) Palmero Company's net income from its independent operations Palmero Company's share of the adjusted income of Santos Company (.8 X $310,000) Controlling Interest in Consolidated Net Income Problem 5-2 Computation and Allocation of Difference Schedule Parent Non- Entire Share Controlling Value Share Purchase price and implied value $1,300,000 557,143 1,857,143 *

4 - 15

Less: Book value of equity acquired 1,050,000 450,000 1,500,000 Difference between implied and book value 250,000 107,143 357,143 Unamortized Discount on Bonds Payable (106,143) (45,490) (151,633) Balance 143,857 61,653 205,510 Goodwill (143,857) (61,653) (205,510) Balance -0- -0- -0- *$1,300,000/.70 Present Value on 1/1/2011 of 6% Bonds Payable Discounted at 10%, 5 periods Principal ($1,000,000 × 0.62092) $620,920 Interest ($60,000 × 3.79079) 227,447 Fair value of bonds $848,367 Face value of bonds 1,000,000 Total Discount $151,633 Amortization of amount of difference between implied and book value allocated to unamortized discount on bonds payable (1) (2) (3) (4) (5) Carrying Interest at 10% Interest at 6% Difference Year Value (1/1) of Carrying Value of Par Value [(3)-(4)] 2011 $848,367 $84,837 $60,000 $24,837 2012 $873,204 $87,320 $60,000 $27,320 Part A 2011 (1) Equity in Subsidiary Income (.70)($100,000) 70,000 Investment in Sagon Co. 70,000 To eliminate subsidiary income (2) Beginning Retained Earnings-Sagon Co. 500,000 Capital Stock- Sagon Co. 1,000,000 Difference between Implied and Book Value 357,143 Investment in Sagon Co. 1,300,000 Noncontrolling Interest 557,143 To eliminate investment amount and create noncontrolling interest account (3) Interest Expense 24,837 Unamortized Discount on Bonds Payable ($151,633 - $24,837) 126,796 Goodwill 205,510 Difference between Implied and Book Value 357,143 To allocate and amortize the difference between Implied and book value Alternative to entry (3) (3a) Unamortized Discount on Bonds Payable 151,633 Goodwill 205,510 Difference between Implied and Book Value 357,143

4 - 16

(3b) Interest Expense 24,837 Unamortized Discount on Bonds Payable 24,837 2012 (1) Equity in Subsidiary Income (.70)($120,000) 84,000 Investment in Sagon Co. 84,000 To eliminate subsidiary income

(2) Beginning Retained Earnings-Sagon Company 600,000 Common Stock- Sagon Company 1,000,000 Difference between Implied and Book Value 357,143 Investment in Sagon Company ($1,300,000 + $70,000) 1,370,000 Noncontrolling Interest ($557,143 + ($600,000 – $500,000) x 0.30) 587,143 To eliminate the investment account and create noncontrolling interest account

(3) Beginning Retained Earnings-Paxton Company 17,386 * Noncontrolling Interest 7,451 Interest Expense 27,320 Unamortized Discount on Bonds Payable ($151,633 - $24,837 - $27,320) 99,476 Goodwill 205,510 Difference between Implied and Book Value 357,143 To allocate and amortize the difference between implied and book value

*$24,837 x 70% = $17,386

Alternative to entry (3) (3a) Unamortized Discount on Bonds Payable 151,633 Goodwill 205,510 Difference between Implied and Book Value 357,143

(3b) Beginning Retained Earnings-Paxton Company 17,386 Noncontrolling Interest 7,451 Interest Expense 27,320 Unamortized Discount on Bonds Payable 52,157 (4) Impairment Loss – Goodwill** 25,510 Goodwill 25,510 ** Step 1: Fair value of the reporting unit $1,500,000 Carrying value of unit: Carrying value of identifiable net assets $1,409,000 Carrying value of goodwill 205,510

1,614,510

Excess of carrying value over fair value $ 114,510

The excess of carrying value over fair value means that step 2 is required.

4 - 17

Step 2: Fair value of the reporting unit $1,500,000

Fair value of identifiable net assets 1,320,000 Implied value of goodwill 180,000 Recorded value of goodwill 205,510 Impairment loss $ 25,510

Part B Controlling Interest in Consolidated Net Income 2011 2012 Paxton Company's Net Income from Independent Operations $300,000 $250,000 Paxton Company's Share of Reported Income of Sagon Company 70,000 84,000 Less: Amortization of Difference between Implied and Book Value Allocated to: Bonds Payable (17,386) (19,124)* Controlling Interest in Consolidated Net Income $352,614 $314,876 * $27,320 x 70% = $19,124 Noncontrolling Interest in Consolidated Income (2011) Amortization of the difference between Net income reported by Sagon implied and book value related to bonds payable 24,837 Adjusted net income of Sagon Noncontrolling Ownership percentage interest Noncontrolling Interest in Consolidated Net Income Controlling Interest in Consolidated Income (2011) Paxton Company's net income from its independent operations Paxton Company's share of the adjusted income of Sagon Company (.7 X $75,163) Controlling interest in Consolidated Net Income Noncontrolling Interest in Consolidated Income (2012)

4 - 18

Amortization of the difference between Net income reported by S implied and book value related to bonds payable 27,320 Goodwill Impairment 25,510 Adjusted net income of S Noncontrolling Ownership percentage interest Noncontrolling Interest in Consolidated Net Income Controlling Interest in Consolidated Income (2012) Paxton Company's net income from its independent operations Paxton Company's share of the adjusted income of Sagon Company (.7 X $67,170) Controlling interest in Consolidated Net Income

4 - 19

Problem 5-3 Computation and Allocation of Difference Schedule Parent Non- Entire Share Controlling Value Share Purchase price and implied value $1,970,000 492,500 2,462,500 * Less: Book value of equity acquired 1,440,000 360,000 1,800,000 Difference between implied and book value 530,000 132,500 662,500 Inventory ($725,000 - $600,000) (100,000) (25,000) (125,000) Equipment ($1,075,000 - $900,000) (140,000) (35,000) (175,000) Balance 290,000 72,500 362,500 Goodwill (290,000) (72,500) (362,500) Balance -0- -0- -0- *$1,970,000/.80 2012 Amortization Schedule Inventory (60% in 2012) 60,000 15,000 75,000 Equipment ($175,000/7) 20,000 5,000 25,000 Total 80,000 20,000 100,000

2013 Amortization Schedule Inventory (40% in 2013) 40,000 10,000 50,000 Equipment ($175,000/7) 20,000 5,000 25,000 Total 60,000 15,000 75,000 Part A 2012 Investment in Superstition Company 1,970,000 Cash 1,970,000

Cash (0.8 × $150,000) 120,000 Investment in Superstition Company 120,000 Investment in Superstition Company 600,000 Equity in Subsidiary Income (.80)($750,000) 600,000 Equity in Subsidiary Income 80,000 Investment in Superstition Company 80,000

2013 Cash (0.8 × $225,000) 180,000 Investment in Superstition Company 180,000 Investment in Superstition Company 720,000 Equity in Subsidiary Income (.80)($900,000) 720,000 Equity in Subsidiary Income 60,000 Investment in Superstition Company 60,000

4 - 20

Part B 2012 (1) Equity in Subsidiary Income ((.80)($750,000) - $80,000) 520,000 Dividends Declared (0.80 × $150,000) 120,000 Investment in Superstition Company 400,000 To eliminate intercompany income and dividends

(2) Beginning Retained Earnings - Superstition Company 600,000 Common Stock- Superstition Company 1,200,000 Difference between Implied and Book Value 662,500 Investment in Superstition Company 1,970,000 Noncontrolling Interest 492,500 To eliminate the investment account and create noncontrolling interest account (3) Inventory ($125,000 - $75,000) 50,000 Cost of Goods Sold 75,000 Depreciation Expense 25,000 Equipment (net) ($175,000 - $25,000) 150,000 Goodwill 362,500 Difference between Implied and Book Value 662,500 To allocate and depreciate the difference between implied and book value Alternative to entry (3) (3a) Inventory 50,000 Cost of Good Sold 75,000 Equipment (net) 175,000 Goodwill 362,500 Difference between Implied and Book Value 662,500 (3b) Depreciation Expense 25,000 Equipment (net) 25,000 2013 (1) Equity in Subsidiary Income ((.80)($900,000) - $60,000) 660,000 Dividends Declared (0.80 × $225,000) 180,000 Investment in Superstition Company 480,000 To eliminate intercompany income and dividends (2) Beginning Retained Earnings-Superstition Company 1,200,000 Common Stock - Superstition Company. 1,200,000 Difference between Implied and Book Value 662,500 Investment in Superstition Company ($1,970,000 + $480,000) 2,450,000 Noncontrolling Interest ($492,500 + ($1,200,000 – $600,000) x .20) 612,500 To eliminate investment account and create noncontrolling interest account

(3) Investment in Superstition Company

4 - 21

($60,000 + $20,000) 80,000 Noncontrolling Interest ($15,000 + $5,000) 20,000 Cost of Good Sold 50,000 Depreciation Expense 25,000 Equipment (net) ($175,000 – $25,000 – $25,000) 125,000 Goodwill 362,500 Difference between Implied and Book Value 662,500 To allocate and depreciate the difference between implied and book value Alternative to entry (3) (3a) Investment in Superstition Company 60,000 Noncontrolling Interest 15,000 Cost of Good Sold 50,000 Equipment (net) 175,000 Goodwill 362,500 Difference between Implied and Book Value 662,500 (3b) Investment in Superstition Company 20,000 Noncontrolling Interest 5,000 Depreciation Expense 25,000 Equipment (net) 50,000 Part C Perke Corporation's Net Income from Independent Operations ($1,000,000 - $120,000) $880,000 Perke Corporation's Share of Superstition Company's net income (0.8 × $750,000) 600,000 Less: Assignment, amortization, and depreciation of: Inventory (60,000) Equipment (20,000) Controlling Interest in Consolidated Net Income $1,400,000 Problem 5-7 Computation and Allocation of Difference Schedule Parent Non- Entire Share Controlling Value Share Purchase price and implied value $900,000 300,000 1,200,000 * Less: Book value of equity acquired 506,250 168,750 675,000 Difference between implied and book value 393,750 131,250 525,000 Equipment (net) (135,000) (45,000) (180,000) Balance 258,750 86,250 345,000 Goodwill (258,750) (86,250) (345,000) Balance -0- -0- -0- *$900,000/.75

4 - 22

Amount of Difference Between Implied and Book Value Allocated to Equipment Fair Book Fair Value Minus Value Value Book Value Equipment $990,000 1 $720,000 $270,000 3 Accumulated Depreciation 330,000 2 (240,000) (90,000)4 Net $660,000 $480,000 $180,000 1$660,000/($480/$720) = $990,000 2$990,000 × ($240/$720) = $330,000 3$180,000/($480/$720) = $270,000 4$270,000 × ($240/$720) = $90,000 Annual Depreciation of Difference

Equipment ($180,000/10)) = $18,000 Part A Investment in Sanchez Company 90,000 Dividend Declared-Sanchez Co. ($120,000 × 0.75) 90,000 (1) Equity in Subsidiary Income (($123,000 × 0.75) – $13,500) 78,750 Investment in Sanchez Company 78,750 (2) Beginning Retained Earnings-Sanchez Company 375,000 Common Stock-Sanchez Company 300,000 Difference between Implied and Book Value 525,000 Investment in Sanchez Company 900,000 Noncontrolling Interest 300,000 To eliminate investment and create noncontrolling interest account (3) Depreciation Expense 18,000 Equipment 270,000 Goodwill 345,000 Accumulated Depreciation-Equipment ($90,000 + $18,000) 108,000 Difference between Implied and Book Value 525,000 To allocate and depreciate the difference between implied and book value

Alternative to entry (3) (3a) Equipment 270,000 Goodwill 345,000 Accumulated Depreciation-Equipment 90,000 Difference between Implied and Book Value 525,000 (3b) Depreciation Expense 18,000 Accumulated Depreciation-Equipment 18,000

Part B (1) & (2) Book Value Difference Consolidated Equipment $720,000 $270,000 3 $990,000 1 Accumulated Depreciation (240,000) (90,000) (330,000) Carrying Value 1/1/2011 $480,000 $180,000 $660,000

4 - 23

× 8/10 × 8/10 Carrying Value 1/1/2013 384,000 528,000 Proceeds from Sale (450,000) (450,000) (Gain) Loss on Sale $(66,000) $78,000 (3) Investment in Sanchez Company 36,000 Gain on Disposal of Equipment - Sanchez 66,000 Loss on Disposal of Equipment 78,000 Difference between Implied and Book Value 180,000 (4) In all subsequent years, the $180,000 difference between implied and book value

that was allocated to the equipment that was disposed of will be debited to the Investment in Sanchez Company in the consolidated statements workpaper for the cumulative amount of additional depreciation expense ($18,000 + $18,000 = $36,000) and for the amount of adjustment to the reported gain or loss on the disposal of equipment ($66,000 + $78,000 = $144,000) recognized in the consolidated financial statements in prior years.

Note: The $66,000 reduction of the gain plus the $78,000 loss equals $144,000

which is equal to the unamortized difference associated with the equipment on the date it was sold to outsiders ($180,000 - $18,000 - $18,000 = $144,000)