completing the regional and wealth management platform

DESCRIPTION

First Half 2001 Results Briefing. July 23, 2001. Completing the regional and wealth management platform. Completing the regional and wealth management platform. Top line earnings impacted by weaker economic conditions and adverse competitive environment - PowerPoint PPT PresentationTRANSCRIPT

Completing the regional and

wealth management platform

July 23, 2001

First Half 2001 Results Briefing

2

Top line earnings impacted by weaker economic conditions and adverse competitive environment

Focus on other non-interest income bolsters results

Expenses peaked amidst repositioning activities

Improved asset quality and strong capital position

Completing the regional and wealth management platform

Completing the regional and wealth management platform

3

Top line earnings impacted by weaker economic conditions and adverse competitive environment

Focus on other non-interest income bolsters results

Expenses peaked amidst repositioning activities

Improved asset quality and strong capital position

Completing the regional and wealth management platform

Completing the regional and wealth management platform

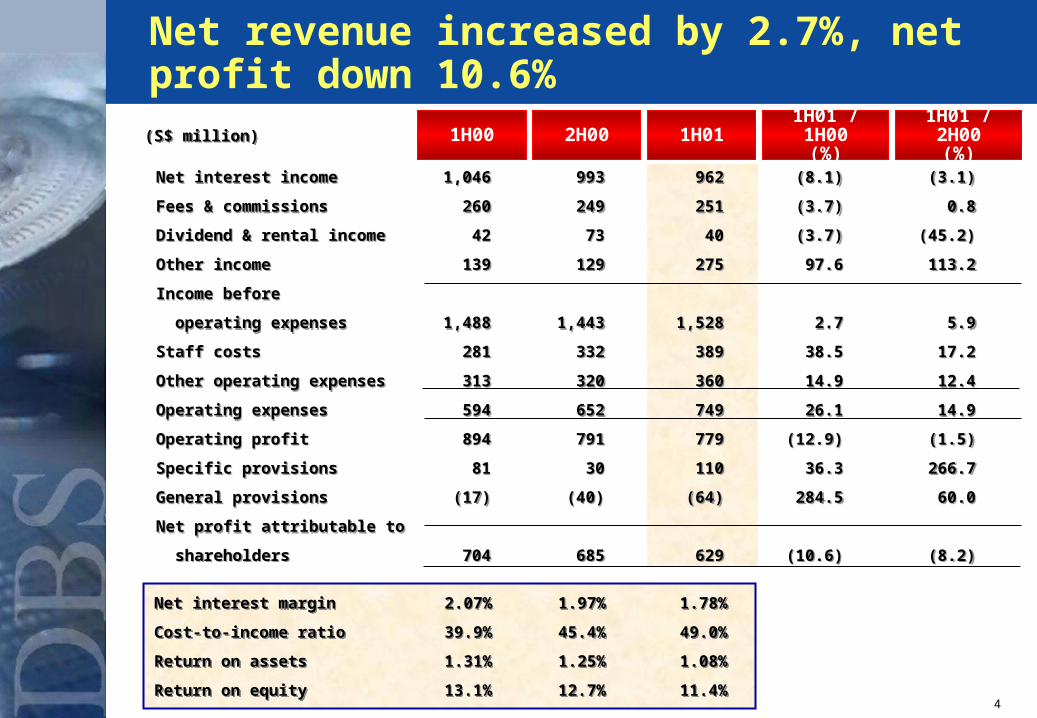

4

Net interest margin 2.07% 1.97% 1.78%

Cost-to-income ratio 39.9% 45.4% 49.0%

Return on assets 1.31% 1.25% 1.08%

Return on equity 13.1% 12.7% 11.4%

Net interest margin 2.07% 1.97% 1.78%

Cost-to-income ratio 39.9% 45.4% 49.0%

Return on assets 1.31% 1.25% 1.08%

Return on equity 13.1% 12.7% 11.4%

Net interest income 1,046 993 962 (8.1) (3.1)

Fees & commissions 260 249 251 (3.7) 0.8

Dividend & rental income 42 73 40 (3.7) (45.2)

Other income 139 129 275 97.6 113.2

Income before

operating expenses 1,488 1,443 1,528 2.7 5.9

Staff costs 281 332 389 38.5 17.2

Other operating expenses 313 320 360 14.9 12.4

Operating expenses 594 652 749 26.1 14.9

Operating profit 894 791 779 (12.9) (1.5)

Specific provisions 81 30 110 36.3 266.7

General provisions (17) (40) (64) 284.5 60.0

Net profit attributable to

shareholders 704 685 629 (10.6) (8.2)

Net interest income 1,046 993 962 (8.1) (3.1)

Fees & commissions 260 249 251 (3.7) 0.8

Dividend & rental income 42 73 40 (3.7) (45.2)

Other income 139 129 275 97.6 113.2

Income before

operating expenses 1,488 1,443 1,528 2.7 5.9

Staff costs 281 332 389 38.5 17.2

Other operating expenses 313 320 360 14.9 12.4

Operating expenses 594 652 749 26.1 14.9

Operating profit 894 791 779 (12.9) (1.5)

Specific provisions 81 30 110 36.3 266.7

General provisions (17) (40) (64) 284.5 60.0

Net profit attributable to

shareholders 704 685 629 (10.6) (8.2)

(S$ million)(S$ million) 1H00 2H00 1H01 1H01 / 1H00(%)

1H01 / 2H00(%)

Net revenue increased by 2.7%, net profit down 10.6%

5

400

800

1200

1.5

2

2.5

(S$ million)

Modest decline in net interest income despite sharp fall in net interest margins

Net interest income

Net interest margin(gross basis)

2.00%2.04%

9891,046 1,046

2.07%

1.97%

993

1H99 2H99 1H00 2H00 1H01

962

1.78%

6

Excess liquidity dampens margins, but strengthens ability to fund lending growth

23.720.2

17.8

8.1

(7.2)

3.2

(10)

(5)

0

5

10

15

20

25

30

63.464.466.173.3

115.9

97.5

0

20

40

60

80

100

120

140

19961996 19971997 19981998 19991999 20002000 1H011H01

(%)(%)

Net Interbank Placement / AssetNet Interbank Placement / Asset

19961996 19971997 19981998 19991999 20002000 1H011H01

(%)(%)

Loan / DepositLoan / Deposit

7

(S$ million) Change in Gross Loans

56,083

54,16656,21958,43861,40459,195

45,404

16,420

0

30000

60000

90000

-3000

0

3000

6000

9000

12000

15000

18000

-10

-5

0

5

10

15

20

25

30

35

10.7%

30.4%

4,373

13,791

3.7%2,209

-4.8%(2,966)

-3.8%(2,219)

-3.7%(2,053) 3.5%

1,917

Jun 98Jun 98 Dec 98Dec 98 Jun 99Jun 99 Dec 99Dec 99 Jun 00 Jun 00 Dec 00Dec 00 Jun 01Jun 01

Dao HengDao Heng

Jun 98Jun 98 Dec 98Dec 98 Jun 99Jun 99 Dec 99Dec 99 Jun 00 Jun 00 Dec 00Dec 00 Jun 01Jun 01

Outstanding Gross Loans

72,503

Loan growth has turned around

8

Top line earnings impacted by weaker economic conditions and adverse competitive environment

Focus on other non-interest income bolsters results

Expenses peaked amidst repositioning activities

Improved asset quality and strong capital position

Completing the regional and wealth management platform

Completing the regional and wealth management platform

9

Strong fee income despite stockbroking liberalisation and weak markets

(S$ million)(S$ million)

Investment banking 42 56 39 (7.1) (30.2)

Stockbroking 47 31 24 (48.9) (22.6)

Trade-related 38 37 40 5.3 7.8

Fund management 37 25 35 (5.4) 40.0

Deposit-related 23 37 43 87.0 15.3

Loan-related 24 27 28 16.7 4.5

Others 49 36 42 (14.3) 16.3

Total fee income 260 249 251 (3.7) 0.8

Fee to income ratio (%) 17.5 17.3 16.4

1998 – 2000Fee Income CAGR: 36.2%

1H00 2H00 1H01 1H01 / 1H00(%)

1H01 / 2H00(%)

10

Other income : FX & securities trading doubled

(S$ million)

Foreign exchange 52 67 112 115.4 67.2

Gains on securities & derivatives trading 55 - 102 85.5 -

Gains on investment securities 8 33 16 100.0 -

Gains on fixed assets 4 5 26 550.0 420.0

Other income 20 24 19 (5.0) (20.8)

Total 139 129 275 97.6 113.2

1H00 2H00 1H01 1H01 / 1H00(%)

1H01 / 2H00(%)

11

Emphasis on non-interest income yields strong returns

Dec 98Dec 98 Dec 99Dec 99 Dec 00Dec 00 Jun 00Jun 00

(%)(%) Non-interest income to Operating Income *Non-interest income to Operating Income *

* Excluding gains on disposal of non-core assets* Excluding gains on disposal of non-core assets

37.1

29.730.428.7

23.8

Jun 01Jun 01

12

(S$ million) Sales Volume

0

100

200

300

400

500

600

700

800

900

314

558

322

2H99 1H00 2H00

Investment products include Horizon, Ei8ht, Up and other DBSAM programs

Investment products

Record growth in wealth management products

1H01

611

Insurance

15

222

180573573 544544

791791

13

(S$ b)

S$ Current accounts 5.6 5.8 6.00.5

S$ Autosave deposits 5.5 5.4 5.70.2

S$ Savings deposits 30.5 31.0 31.10.6

S$ Fixed deposits 14.3 13.2 12.3(2.0)

ACU Fixed deposits 9.4 11.1 12.02.6

DBS Kwong On 5.1 5.7 6.31.2

DBS Thai Danu 3.3 2.9 3.1(0.2)

Others* 6.7 5.6 13.77.0

Sub-total 80.4 80.7 90.39.9

Dao Heng - - 24.624.6

Total 80.4 80.7 114.934.5

Market share of S$ deposits 31.8% 32.3% 32.8%

Dec2000

Jun 2000

Jun2001

YoY Difference

90.3

80.780.424.6

0

50

100

150

Jun 00 Dec 00 Jun 01

Customer Deposits

Deposit base provides platform for cross selling wealth management products

**

* Include a once off short-term deposit of $5.0b * Include a once off short-term deposit of $5.0b

114.9

14

Top line earnings impacted by weaker economic conditions and adverse competitive environment

Focus on other non-interest income bolsters results

Expenses peaked amidst repositioning activities

Improved asset quality and strong capital position

Completing the regional and wealth management platform

Completing the regional and wealth management platform

15

(S$ million)(S$ million)

Staff costs 281 332 389 38.5 17.2

Occupancy expenses 73 75 77 5.5 2.7

Technology-related expenses 63 69 87 38.1 26.1

Professional & consultancy fees 38 35 33 (13.2) (5.7)

Others 139 141 163 17.3 15.6

Total 594 652 749 26.1 14.9

1H00 2H00 1H01 1H01 / 1H00(%)

1H01 / 2H00(%)

Operating costs increased 26% due to timing and non-recurring items

16

594

749+10+13+24+108

(S$ million)

1H2000 1H2001

Co

mp

uterisatio

n

Oth

ersStaff co

sts

Ad

vertising

(+26.1%)

Cost-to-Income Ratio: 39.90% 49.01%

Cost-to-AssetRatio(a): 1.10% 1.30%

Focused investment in people, technology and products

(a) Annualized without Dao Heng Bank

17

Phone Banking

Technology Procurement

Most significant investments completed between January 1, 2000 and June 30, 2001 Consultants now limited to implementation of specific, technical projects

Use of consultants winding down

DBS Securities’ Projects Customer Relationship Mgt Treasury & Mkts System E-Commerce/Payments Risk Mgt System Datawarehouse Call Centre Automation

1998 1999 2000 20011H99 9M00 1H01

Branch ReconfigurationCustomer Service

POSBank, DTDB & DKOBIntegration

Strategy Development Retail Strategy Improving Profitability (DTDB NPL,

Recapitalisation of DTDB, Sale of DBSL shares, acquisition of BPI)

Institutional Banking Group ReorganisationRe-engineering Processing & Services

Process Improvement Procurement

E-banking initiative

Cost & Profitability Mgt SystemMeasurement

18

Cost management

measures initiated to

contain increase to 2000 growth

rate

Improve processes for greater efficiency Improve processes for greater efficiency

Reduce focus on non-performing businesses Reduce focus on non-performing businesses

Defer low revenue yielding projects Defer low revenue yielding projects

Performance enhancement program to optimise efficiency

19

Low cost/income ratio by international standards

6.7

58.4 57.4 56.3 55.353.5

51.0

42.5

Stanchart NAB CBA HSBC Westpac ANZ DBS

(a) Based on Dec 2000 cost/income ratios

1H20011H2001

Cost/Income for International Peers (a)Cost/Income for International Peers (a)(%)(%)

49.249.2

20

Top line earnings impacted by weaker economic conditions and adverse competitive environment

Focus on other non-interest income bolsters results

Expenses peaked amidst repositioning activities

Improved asset quality and strong capital position

Completing the regional and wealth management platform

Completing the regional and wealth management platform

21

2,705 2,8242,425 2,452

1,735 1,610

642772

1,239

1,408 1,365 1,144

624

1,735

2,874

3,018 3,2073,000

1,2381,143

1,249649

770

10701152871

267

151

97366

667

815

Dec 97 Jun 98 Dec 98 Jun 99 Dec 99 Jun 00 Dec 00 Jun 01

7.6%

12.7%

8.5%

13.0%13.1%

11.8%

2.7%

Dao Heng Bank

DBS Thai Danu Bank

5 Regional CountriesOthers

Singapore

NBk NPL/NBk Loans (%)

(S$ million)

1,112

3,907

7,085

8,121 8,1497,666

4,4114,834

6.2%

Asset quality continues to improve

22

73% of NPLs are graded “Substandard”

3,554

1,369

844

292

450

353

244

193

943

170

8

111

7

125

14

435

5

60

232

63

193

0 1,000 2,000 3,000 4,000 5,000

DTDB

Dao Heng

DKOB

Others

5RC

S'pore 1,610

624

323

4,834

85%

72%

73%

1,143

815

82% Total

9% 18%

17%

(S$’M )

1%

318

Substandard

Doubtful

Loss

23

948

1,463801

946

1,115

1,294

1,191

1,174

1,049

1,180

179

1,237

3,095

2,032

2,8042,558

Dec 97 Jun 98 Dec 98 Jun 99 Dec 99 Jun 00 Dec 00 Jun 01

146.5%

164.6%

119.6% 102.7%110.6% 118.4% 114.8%

129.9%

54.7%51.8%51.9%52.6%47.4%44.4%48.5%

88.1%

59.9%55.3% 63.0% 60.8% 61.4%

General Provisions (GP)

Specific Provisions (SP)

SP+GP/NPLs (SEC) (%)

SP+GP/Unsec NPLs (%)

SP+GP/NPLS (%)

980

1,894

3,147

3,852

4,2863,978

2,286

(S$ million)

Cumulative provisions covered 146.5% of unsecured NPLs and 54.7% of total NPLs

2,643

24

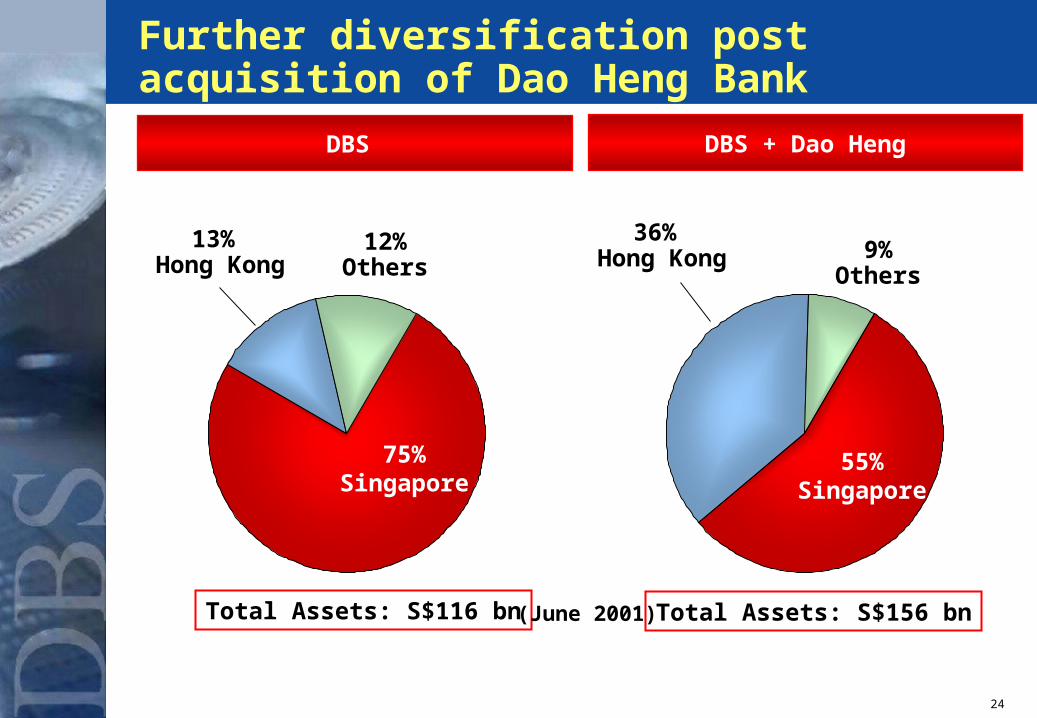

Further diversification post acquisition of Dao Heng Bank

55%Singapore

9%Others

36% Hong Kong

Total Assets: S$156 bn

DBS + Dao Heng

75%Singapore

12%Others

13% Hong Kong

Total Assets: S$116 bn

DBS

(June 2001)

25

Efficient capital management

(a) Includes goodwill, minority interest and capital required against asset base.

DBS Group Holdings Consolidated Capital Adequacy

(a) (b)

(%)(%)

Dec2000 Dec

2000 HybridTier 1

HybridTier 1

PreferenceShares

PreferenceShares

Tier 2Sub-debt

Tier 2Sub-debt

1H01Net

Income

1H01Net

Income

Adjustmentsfor

Dao Heng/Others

Adjustmentsfor

Dao Heng/Others

Jun2001Jun2001

5.5%

17.5%

12.0%Tier 114.4%

18.9%

0.7%1.7%1.2%

1.5%Tier II4.5%

0

5

10

15

20

25

30

35

6.5%6.5%

26

10.09.2

8.47.7 7.5 7.3 7.2 7.0

6.0

0

4

8

12

DBS will maintain a healthy buffer above the regulatory Tier I requirement of 8%

DBS capital position post Dao Heng

* Source : Annual reports of respective banks* Source : Annual reports of respective banks

DBS

(%)(%)

HSBC

CitiGroup

StanChartBNP

ANZ

WestpacFortis

Dresdner

27

Top line earnings impacted by weaker economic conditions and adverse competitive environment

Focus on other non-interest income bolsters results

Expenses peaked amidst repositioning activities

Improved asset quality and strong capital position

Completing the regional and wealth management platform

Completing the regional and wealth management platform

28

Putting the strategy together – positioning for the future

Optimal Organisation

Business units reorganised

Built seasoned management team

Enhanced training

Redesigned incentive systems

Wholesale Banking: Capital Markets, Advisory, Treasury, FX and Trade Financing

Wholesale Banking: Capital Markets, Advisory, Treasury, FX and Trade Financing

Management

ManagementWealthWealth

Brokerage Services

Brokerage Services BancassuranceBancassurance

Consumer Banking

Consumer Banking

DBS / OUB

Vickers Ballas Frank Russell TD Waterhouse

CGNU

Dao Heng Kwong OnThai Danu

BPI

Aligned internal practices to global standards

Strengthened risk management and credit approval policies

Prudent management of off-balance sheet exposures and liquidity, forex, interest rate and investment risks

Leading IT Capabilities

On-line, real-time systems

Data warehouse application with data mining capabilities (CRM)

E-commerce infrastructure

E-payment gateway

Comprehensive, complementary channel mix

Reconfigured branches

Integrated on-line services

Usage of sophisticated capital instruments

Maximise non-dilutive capital

Sale of non-core assets

Scale / Scope Regionalisation /

diversification Growth / market

share Pricing flexibility

Policies, Processes and SystemsPolicies, Processes and Systems

Balanced Channel MixBalanced Channel Mix

Efficient Capital StructureEfficient Capital Structure

Infrastructure building and reorganisation substantially completed

Focused areas

29

InfrastrucInfrastructureture

Infrastructure

Geography

ProductsSignificant

infrastructure

investment to create

world class back office

and STP initiatives

Vickers Ballas

TD Waterhouse

Frank Russell

CGNU

Dao Heng / Kwong On

OUB

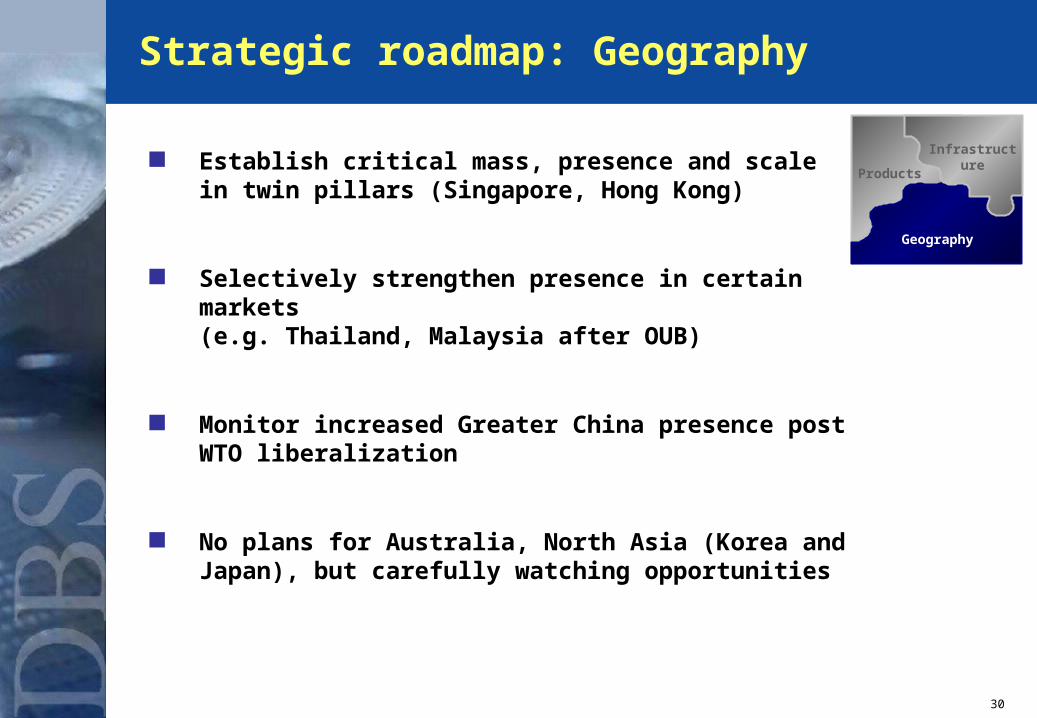

Strategic roadmap

30

Establish critical mass, presence and scale in twin pillars (Singapore, Hong Kong)

Selectively strengthen presence in certain markets(e.g. Thailand, Malaysia after OUB)

Monitor increased Greater China presence post WTO liberalization

No plans for Australia, North Asia (Korea and Japan), but carefully watching opportunities

InfrInfrastrastructuctureure

Infrastructure

Geography

Products

Strategic roadmap: Geography

31

As of first close on July 20, DBS’ effective ownership in Dao Heng Bank is 71%

98% of Dao Heng shareholders have tendered their shares

Dao Heng Bank governance and management in place

Harmonization objectives and implementation plan defined

Harmonization infrastructure up and running

Key milestones defined with good progress to date

Dao Heng Bank became a DBS subsidiary on June 29, 2001

Dao Heng harmonization ahead of schedule

(a) Assumes 100% of outstanding options exercised(a) Assumes 100% of outstanding options exercised

32

Leverage infrastructure across business units

Create Regional Processing Centres for appropriate processes

Centralize remaining branch back-office processes

Pursue selected out-sourcing, in-sourcing and co-sourcing

Focus on quality (ISO certification of process factories, 6 sigma initiative)

Continue trend of significant unit cost reductions and increase of straight-through processing rates

InfrInfrastrastructuctureure

Infrastructure

Geography

Products

Strategic roadmap: Infrastructure

33

Retail brokerage – Vickers Ballas, TD Waterhouse

Wealth management – leverage distribution for best-in-breed products, capitalize on MPF / CPF deregulation and excess liquidity

Bancassurance – provide insurance related savings products. Life and general insurance partnership with CGNU

Unsecured consumer lending

Credit cards

SME lending

Treasury / FX

Trade finance

Corporate finance

Leveraged finance

Asset Asset AccumulationAccumulation

Enterprise Enterprise and and

Consumer Consumer LendingLending

InfrInfrastrastructuctureure

Infrastructure

Geography

Products

Corporate & Corporate & Investment Investment

BankingBanking

Strategic roadmap: Products

34

Bancassurance alliance accelerates wealth management business

Sale of 100% of ICS to CGNU 10-year exclusive bancassurance

strategic alliance for life and general insurance

Total proceeds to DBS of S$446 million of which: S$395 million as payment for

ICS and the bancassurance alliance

S$51 million special dividend from ICS

DBS to receive additional payments of up to S$20 million on meeting performance targets

DBS will record a net initial gain of S$139 million

Transaction Highlights

Accelerates revenue growth in DBS’ wealth management business

Expands DBS’ sales channels with the establishment of a specialist sales force dedicated to insurance, wealth management products

Provides DBS with a dedicated bancassurance product provider without equity investment

DBS retains ownership of customers, concentrates on distribution, leaving product manufacturing to CGNU

Allows DBS to rationalize ownership in ICS and continue policy of monetizing assets

Allows DBS to strengthen capital position by $139 million

Strategic Rationale

DBS has concluded a bancassurance alliance with CGNU

35

Only bank whose non-core asset disposals largely completed

Singapore Petroleum Company

DBS Land

DBS Tampines Centre

POSBank Centre

DBS Securities Building

Insurance Corporation of Singapore (ICS)

What we have done

4 listed companies (Keppel Capital, NatSteel, Intraco, CWT)

What needs to be done

Insignificant

Focusing on core banking and financial businesses

Divested non-core assets ahead of MAS guidelines

36

Significant Events Affecting Results and Outlook

Jan 29 Assets and liabilities of DBS Finance transferred to DBS Bank

Feb 13 Announced proposed acquisition of approximately 60% of Vickers Ballas

Mar 25 Issued US$725 million 7.657% Non-cumulative Guaranteed Preference Shares

(NGPS) and S$100 million 5.35% NGPS

Announced intention to make a voluntary conditional offer for Dao Heng.Acquired an effective 56.9% of Dao Heng Bank on June 29

Apr 11 Consolidated with negligible P&L impact

Goodwill of S$4.9 billion to be amortised over 20 years from July 2001

May 10 Issued US$850 million 7.125% Upper Tier II Subordinated Notes due in 2011

May 25 Issued S$1.1 billion 6% Tier I Non-cumulative Preference Shares

Jun 20 Entered into a joint-venture with TD Waterhouse to form a regional online

financial services company

Jun 22 Announced intention to make a voluntary conditional offer for OUB

37

Top line earnings impacted by weaker economic conditions and adverse competitive environment

Focus on other non-interest income bolsters results

Expenses peaked amidst repositioning activities

Improved asset quality and strong capital position

Completing the regional and wealth management platform

Completing the regional and wealth management platform

Completing the regional and

wealth management platform

July 23, 2001

First Half 2001 Results Briefing