company overview - mediobanca · company overview . 4 ferrari at a glance: unique, exclusive,...

TRANSCRIPT

Company Overview

2 2

This document, and in particular the section entitled “2016 Outlook”, contains forward-looking statements. These statements may include terms

such as “may”, “will”, “expect”, “could”, “should”, “intend”, “estimate”, “anticipate”, “believe”, “remain”, “on track”, “design”, “target”, “objective”, “goal”,

“forecast”, “projection”, “outlook”, “prospects”, “plan”, or similar terms. Forward-looking statements are not guarantees of future performance.

Rather, they are based on the Group’s current expectations and projections about future events and, by their nature, are subject to inherent risks

and uncertainties. They relate to events and depend on circumstances that may or may not occur or exist in the future and, as such, undue reliance

should not be placed on them.

Actual results may differ materially from those expressed in such statements as a result of a variety of factors, including: the Group’s ability to

preserve and enhance the value of the Ferrari brand; the success of Ferrari’s Formula 1 racing team and the expenses the Group incurs for Formula

1 activities; the Group’s ability to keep up with advances in high performance car technology and to make appealing designs for its new models; the

Group’s low volume strategy; the ability of Maserati, the Group’s engine customer, to sell its planned volume of cars; changes in client preferences

and automotive trends; changes in the general economic environment and changes in demand for luxury goods, including high performance luxury

cars, which is highly volatile; the impact of increasingly stringent fuel economy, emission and safety standards; the Group’s ability to successfully

carry out its growth strategy and, particularly, the Group’s ability to grow its presence in emerging market countries; competition in the luxury

performance automobile industry; reliance upon a number of key members of executive management and employees; the performance of the

Group’s dealer network on which the Group depend for sales and services; increases in costs, disruptions of supply or shortages of components and

raw materials; disruptions at the Group’s manufacturing facilities in Maranello and Modena; the Group’s ability to provide or arrange for adequate

access to financing for its dealers and clients; the performance of the Group’s licensees for Ferrari-branded products; the Group’s ability to protect

its intellectual property rights and to avoid infringing on the intellectual property rights of others; product recalls, liability claims and product

warranties; exchange rate fluctuations, interest rate changes, credit risk and other market risks; potential conflicts of interest due to director and

officer overlaps with the Group’s largest shareholders and other factors discussed elsewhere in this document.

Any forward-looking statements contained in this document speak only as of the date of this document and the Company does not undertake any

obligation to update or revise publicly forward-looking statements. Further information concerning the Group and its businesses, including factors

that could materially affect the Company’s financial results, is included in the Company’s reports and filings with the U.S. Securities and Exchange

Commission, the AFM and CONSOB

SAFE HARBOUR STATEMENT

2 2

Company Overview

4 4

FERRARI AT A GLANCE: UNIQUE, EXCLUSIVE, SUCCESSFUL, RESILIENT

• The world’s most recognizable luxury performance sports cars

• One of the world's most valuable and powerful brands(1), underpinned by a rich history

• The epitome of exclusivity, sporting performance, technological innovation, Italian style, design and engineering excellence

• The longest running and most successful team in Formula 1 history, with 15 Drivers and 16 Constructors World titles

• Serving a loyal and growing customer base, with 7,664 vehicles shipped in 2015

• Strong free cash flow generation coupled with both a conservative financial policy and solid balance sheet

• Dual listed company: NYSE (RACE US) and MTA (RACE IM).

1 Source: www.brandfinance.com. According to "Brand Finance Global 500", last release in 2016

5 5

FERRARI'S HISTORICAL MILESTONES

First racing car

produced by

Ferrari

Debut of Ferrari

166 Inter –

Ferrari's first

road car

Scuderia Ferrari

begins competing

in Formula 1 in

1950

Jose Froilan

Gonzalez wins the

first race in 1951

GT cars become

relevant part of

Ferrari business

Enzo Ferrari sells to

Fiat Group a 50%

stake in Ferrari

Debut of V8

engine

production

7 Constructors and 6

Drivers’ world titles over

the decade

Launch of F40, the first

supercar by Ferrari

Fiat Group increases its

stake in Ferrari to 90%

Ferrari begins its

branding activities by

launching Ferrari

branded products in

Ferrari stores

Launch of

Enzo Ferrari

supercar

Ferrari World

theme park opens

in Abu Dhabi

Launch of LaFerrari

Ferrari named as

the world’s most

powerful brand by

Brand Finance

NYSE listing

1948 1947

1950/

51

1960s

1969

1970s

1980s

1987

1988

2000s

2002

2010

2013

2015

2002

2016

Spin-off and Milan

listing

6 6

EMEA Americas

Greater China Rest of APAC

39 Markets 11 Markets

3 Markets 9 Markets

94

POS

31

POS

53

POS

20

POS

Dealer performance is regularly monitored and constantly enhanced through ongoing training programs and upgraded when necessary

14% of 2015

Shipments

34% of 2015

Shipments

44% of 2015

Shipments

8% of 2015

Shipments

SALES GLOBAL FOOTPRINT Dealer network of 198 Points of Sale (POS) globally covering 62 markets

7 7

FERRARI’S SHAREHOLDING STRUCTURE

EXOR S.p.A. Free Float

Ferrari N.V.

Ferrari S.p.A.

Mr. Piero Ferrari

~24 % ~66 %

~10 %

100%

Shareholding Structure

• Exor is the largest shareholder of Ferrari through its 23.5%. Exor’s voting power is

approximately 33.4%

• Mr. Piero Ferrari holds 10% of Ferrari common shares and, as a result of the loyalty

voting mechanism, his voting power is approximately 15.4%

• Exor and Mr. Piero Ferrari have entered into a shareholder agreement which

includes, inter alia, a pre-emption right in favor of Exor and right of first offer of Mr.

Piero Ferrari in the event of transfer of common shares

8 8

Competitive Strengths

9 9

COMPETITIVE STRENGTHS

1. Iconic brand with superior, enduring power, benefitting from a loyal customer base

2. Global access to growing wealth creation

3. Exceptional pricing power and value resilience

4. Racing heritage

5. Leading edge engineering capabilities

6. Flexible and efficient development and production process

7. Strong and resilient financial performance and conservative financial profile

8. Superior talent

10 10

1. ICONIC BRAND WITH SUPERIOR, ENDURING POWER,

BENEFITTING FROM A LOYAL CUSTOMER BASE

AAA 1

Brand Finance(1) Top 100

ItalBrand(2)

60% of new Ferrari

cars sold to existing

owners

34% of Ferrari clients

own more than one

Ferrari

1 According to Brand Finance 2 According to ItalBrand Top 100 Italian Brands, Ferrari is the most valuable Italian brand. Latest release in 2012

Unmatched tradition of luxury, world class sporting

performance, Italian design and engineering

innovation

One of the world's most iconic, valuable and

recognizable brands

Loyal and expanding customer base Ability to grow into selected lifestyle categories

11 11

16.3 24 37.4 8.4

17.4

42.1

12.4

17.3

26.6

2006A 2015A 2025E

Americas Asia Pacific EMEA

2. GLOBAL ACCESS TO GROWING WEALTH CREATION Alongside other factors, GDP and High Net Worth Individuals (“HNWIs”) wealth growth contribute to drive

demand in our cars

CAGR '15A-25E

4.4%

9.2%

4.5%

HNWIs wealth by region (US$ trillion)(1)

Ever expanding population of HNWIs

• HNWIs wealth grew by c. 5% over 2006-15

• HNWIs wealth estimated to grow by c. 6%

over the 2015-2025 period reaching

~US$106tn, threefold the 2006 figure

We adopt a flexible car shipping model, covering

emerging pockets of demand globally

1 Source: World Wealth Report 2016 (Capgemini)

37.2

58.7

106.0

12 12

3. EXCEPTIONAL PRICING POWER AND VALUE RESILIENCE Controlled production and distribution model promote unsatisfied demand (waiting lists) and thus scarcity

value, driving premium prices for new cars and resilient aftermarket values

9 OUT OF 10 MOST VALUABLE CARS EVER AUCTIONED ARE FERRARI

# Maker Type Price

(US$m)(1) Auction date

1 250 GTO Berlinetta 1962 38.1 Aug-14

2 335 Sport Scaglietti 1957 35.8 Feb-16

3 W196 Silver Arrow1954 29.6 Jul-13

4 Fangio's Mille Miglia Ferrari

290 28 Dec-15

5 275 GTB/4 S NART Spider

1967 27.7 Aug-13

6 275 GTB/C Speciale 1964 26.4 Aug-14

7 250 GT California Spider

1961 18.5 Feb-15

8 250 LM by Scaglietti1964 17.6 Aug-15

9 250 GT SWB California

Spider 1961 16.8 Aug-15

10 Ferrari 250 GT SWB

Berlinetta Speciale 1962 16.5 Aug-15

• Highly personalized "tailor made" products

• Special limited editions and one-off cars

LaFerrari >€1m

F12 TRS

• Scarcity value strongly supports value resilience

Source: www.gizmag.com, www.rmsothebys.com, www.goodingco.com updated as of February 2016 1. Auction in US$ except for: 250 GT California Spider 1961 (€16.3m), W196 Silver Arrow 1954 (£19.6m), 375-Plus Spider Competizione 1954 (£10.8m) and 355 Sport Scaglietti 1957 (€32m) 2. As of December 31, 2015

+16%(2) average

increase to selling

price from all the

personalization

programs

1%

30%

100%

2-3 per

year

One-off

Special Equipment

Personalization Program

% of clients

F12tdf

13 13

4. RACING HERITAGE Formula 1 racing – with a 2015 global viewership of 420m – is an unparalleled platform to promote our

brand and develop state-of-the-art technology

No need for mainstream product advertising, as Formula 1 participation acts as a core marketing activity

The most successful team in the racing history…

Source: Analysis based on data from IFM Sports Marketing Survey, IEG, SportCal, Sports Business, TV Sports Markets and Eurodata

Formula 1 World Drivers

Championship titles 15 Formula 1 World Constructors

Championship titles 16 Grand Prix won 224

…in one of the leading sport events globally

Local Global

Tie

r 2

Tie

r 1

Regional

2000–04 1964 1961 1958 1956 2007 1979 1975/77 1952–53

Michael Schumacher

F1-2000

John Surtees

158 F1

Phil Hill

156 F1

Mike Hawthorn

326 MI

Juan Fangio

246

Kimi Räikkönen

F2007

Jody Schekter

312 T4

Niki Lauda

312 T

Alberto Ascari

500

14 14

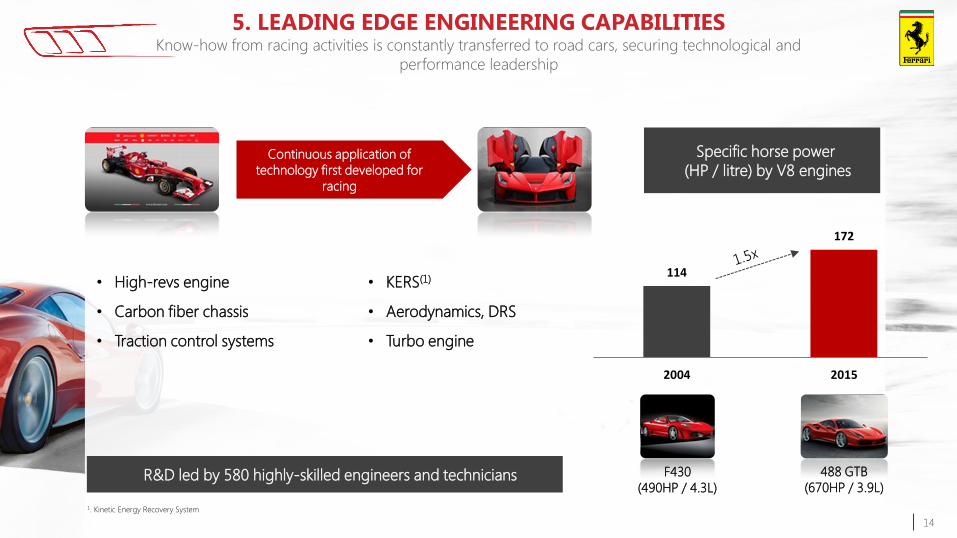

5. LEADING EDGE ENGINEERING CAPABILITIES Know-how from racing activities is constantly transferred to road cars, securing technological and

performance leadership

Specific horse power

(HP / litre) by V8 engines

R&D led by 580 highly-skilled engineers and technicians

114

172

2004 2015

488 GTB

(670HP / 3.9L)

F430

(490HP / 4.3L)

Continuous application of

technology first developed for

racing

• High-revs engine

• Carbon fiber chassis

• Traction control systems

• KERS(1)

• Aerodynamics, DRS

• Turbo engine

1. Kinetic Energy Recovery System

15

6. FLEXIBLE AND EFFICIENT DEVELOPMENT & PRODUCTION PROCESS At least one new model is launched every year, for a life cycle of 4-5 years

40 months development for new models (33 months for modified models)

Design In-house design

development

Product

Development Vehicle dynamics,

powertrain,

control systems,

aerodynamics and

technology

Procurement Strategic and

long-term

partnership

Production Production facilities

(Maranello and Modena)

Ferrari cars are fully designed, engineered and manufactured in Italy,

in recently renovated production facilities

16 16

7. STRONG AND RESILIENT FINANCIAL PERFORMANCE

AND CONSERVATIVE FINANCIAL PROFILE Over the past decade, Ferrari has consistently achieved material growth and margin expansion

Shipment evolution in line with

our controlled growth strategy to

preserve exclusivity

Source: Company filings 1. EBITDA Adjusted for non-recurring items. In 2014, €15m adjustment for former Chairman leaving package, in 2015 €29m due to expenses incurred in connection with our IPO and separation and Employees extra bonus

748

2,854

7.4 Shipments (k)

Net revenues (€m)

Adj. EBITDA(1) (€m)

2005

CAGR

2005-2015

+800bps Margin (%) 18.2% 26.2%

+10.4%

+6.4%

+3.5%

2005

2005

2015

2015

2015

CAGR

2005-2015

CAGR

2005-2015

A resilient business, almost

untouched by the financial crisis

Margin enhancement driven by

operational leverage and cost

control

17 17

8. KEY MANAGEMENT FEATURES: SUPERIOR TALENT

Vice Chairman

P. Ferrari

Chairman and CEO

S. Marchionne*

CFO and

Financial Services

A. Gili*

Internal Audit

M. Lovati

Communication

S. Lai

Legal

C. Daneo

Brand

L. Fuso*

Head of Product

N. Boari*

Chief Human

Resources Officer

M. Antoniazzi*

Chief Manufacturing

Officer

V. Regazzoni*

Chief Commercial

Officer

E. Galliera*

Head of Design

F. Manzoni*

Managing Director of

Gestione Sportiva

M. Arrivabene*

* Members of the Ferrari Group Executive Council

Chief Technology

Officer

M. Leiters*

Business Strategy and Product Portfolio

19 19

REFERENCE MARKET

• Small number of

luxury performance

car manufacturers

• Competition is

driven by the

strength of the

brand and the

appeal of the

products in terms

of performance,

styling and

innovation

Within the luxury goods market, we define our target market for luxury performance cars as two-door cars powered by

engines producing more than 500 horse power (“HP”) and selling at a retail price in excess of €150,000 per unit

Market Our Models Selected Competitors Models

SPORT

GT

488 GTB

488 Spider

F12berlinetta

California T

Lamborghini

Aventador/Huracan

Porsche 911 Turbo,

Turbo S. GT2 and GT3

Aston Martin V12

Vantage/Vanquish

Mercedes S Coupé/Cabrio

63/65 AMG Rolls-Royce Wraith

Audi R8 V10

Mercedes SL 63/65 AMG McLaren 650S

Bentley Cont. GT/GTC, V12 and

V8

GTC4Lusso

20 20

KEY MARKET TRENDS Ferrari sales have proven to be less volatile than competitors, thanks to our low volume strategy, brand

equity and constantly refreshed product range

Luxury goods market affected by

global wealth creation

1. Sources: Bain & Company, 2016 Spring Update for global personal luxury goods market and World Bank data, 1995-2015 for global GDP 2. Ferrari data based on the 22 top countries (excluding Middle East countries) for Ferrari annual registrations and sales (which accounted for approximately 85% of the total Ferrari shipments in 2015).

Data for the Luxury Performance Car Industry based on units registered (in USA, Brazil, Japan, Hong Kong, Taiwan, Australia, United Kingdom, Germany, France, Switzerland, Italy, Spain, Sweden, Netherlands, Belgium and Austria) or sold (in South Korea, Thailand, China, New Zealand, Singapore and Indonesia)

in each period. Source: USA: US Maker Data Club, Brazil-ANFAVEA; Austria-OSZ; Belgium-FEBIAC; France-SIV; Germany-KBA; UK-SMMT; Italy-UNRAE; Netherlands- VWE; Spain- TRAFICO; Sweden-BranschData; Switzerland-ASTRA; China-China Automobile Industry Association-DataClub; Hong Kong-Hong

Kong Motor Trader Association; Taiwan-Ministry of Transportation and Communications; Australia-VFACTS-S; Japan-JAIA; Indonesia-GAIKINDO; New Zealand-VFACTS; Singapore-LTA, MTA (Land Transport Authority, Motor Trader Associations); South Korea-KAIDA; Thailand -Department of Land Transportation

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Jan-05 Dec. 31,

2005

Dec. 31,

2006

Dec. 31,

2007

Dec. 31,

2008

Dec. 31,

2009

Dec. 31,

2010

Dec. 31,

2011

Dec. 31,

2012

Dec. 31,

2013

Dec. 31,

2014

Dec. 31,

2015

FERRARI LUXURY PERFORMANCE CAR INDUSTRY

Ferrari vs. Luxury performance car market(2) (in units)

Personal luxury goods market vs. global GDP evolution(1)

(Relative growth)

(Ferrari’s units) (Luxury performance

car industry)

Personal luxury goods market has

been over-performing global GDP

growth over the past 20 years

Within the luxury performance car

market, Ferrari stands out for its

regularly growing and resilient

business

50

100

150

200

250

300

350

400

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Global Personal-Luxury-Goods Market Global GDP

21 21

UNRIVALLED PRODUCT PORTFOLIO Ferrari cars stand out from competition for their extreme performance, distinctive design and state-of-the-

art technology

THE XX PROGRAM(1) LIMITED EDITION SUPERCARS SPECIAL SERIES MODELS

GT SPORTS

RANGE MODELS

ROAD CARS

1. The XX Program is used to test advanced solutions and innovations by providing a selected group of clients the opportunity to drive cars with superior power and performance

V8

488 Spider

V8

California T

V8

488 GTB

V12

F12berlinetta

V12

FXX K

V12

F60 America

V12

F12tdf

V8

488 GTE

V8

F12 TRS

V12

GTC4Lusso

NON-REGISTERED RACING CARS

NON-REGISTERED CARS

ONE-OFFS “FUORI SERIE” MODELS

V12

LaFerrari

Financial Overview

23 23

Adj. EBITDA (€m) and Adj. EBITDA Margin (%)(1) Net Revenues (€m) and Shipments (k)

1 EBITDA Adjusted for non-recurring items. In 2014, €15m adjustment for former Chairman leaving package, in 2015 €29m due to expenses incurred in connection with our IPO and Separation and Employees extra bonus

3,703 3,309 3,274 3,351

2,208 2,382 2,462 2,640

789 572 675 610 705

737 844 1,063

7,405 7,000 7,255

7,664

2012 2013 2014 2015

EMEA Americas Greater China Rest of APAC

• Consistently highly profitable across the cycle

• Resilient to economic downturns

• Delivering margins above ~26% over the recent years

• Limited exposure to recent emerging markets volatility

Key Highlights Group Shipments

2,225 2,335

2,762 2,854

7.4 7.0

7.3 7.7

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

573 634 693 748

25.8% 27.2%

25.1% 26.2%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

LONG-TERM HISTORICAL PERFORMANCE Resilient to economic downturns and predictable

24 24

Special series and one-offs not included

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

V8

F430

F430 Spider

F430 Scuderia

California

Scuderia Spider 16M

458 Italia

458 Spider

California 30

458 Speciale

California T

458 Speciale A

488 GTB

488 Spider

V12

612 Scaglietti

Superamerica

599 GTB Fiorano

599 GTO

SA APERTA

FF

F12berlinetta

F12tdf

GTC4Lusso

Supercars

LaFerrari

“open-top LaFerrari”

STRONG TRACK-RECORD IN NEW MODELS INTRODUCTION Product Line-Up (at least a new model launched every year)

25 25

FY 2015 HIGHLIGHTS

Shipments

(units)

Total shipments up 6% driven by an 17% increase in V8, which was partially

offset by a 24% decrease in V12

Free Cash

Flow(1) (€M)

Free Cash Flow primarily driven by strong increase in cash from operating activities which included the following one-time cash inflows: the sale of investment properties; the reimbursement of the financing of inventory related to the establishment of the Maserati standalone business in China; and the sale of the financial assets portfolios of FFS S.p.A. and FFS KK; partially offset by the one-time extra bonus payment in December to all Ferrari employees

Net revenues up 3% (-3% at constant FX) led by cars and spare parts (+€136M)

Net revenues

(€M)

Americas: €801M (+40%) due to volumes, LaFerrari and FX

EMEA: €780 (-12%) due to lower shipments to Middle East and FX

Greater China: €239M (-11%) due to lower shipments and mix

Rest of APAC €260M (+23%) due to higher shipments, partially offset by mix

Adjusted EBIT(1)

(€M and

margin %)

Adj. EBIT growth primarily driven by volume and FX, partially offset by mix

EBIT at €444 million up 14% vs. last year, including one-time extraordinary payment in December to all Ferrari employees and IPO/spin-off costs

16.6%

14.6%

Adjusted

EBITDA(1)

(€M and

margin %)

Adjusted EBITDA increased by 8% driven by strong adjusted EBIT, partially offset by lower D&A in line with 458 family phase-out

EBITDA at €719 million (vs. €678 million in FY ‘14), including one-time extra bonus payment in December to all Ferrari employees and IPO/spin-off costs

26.2%

25.1%

Net Industrial

Cash/

(Net Industrial

Debt) (1)

(€M)

Net industrial debt at €797 million due to the capital reorganization in connection with our IPO and spin-off partially offset by the strong Free Cash Flow generation

Dec. 31, 2015

Dec. 31, 2014

1Reconciliation to non-gaap financial measures are provided in the appendix

26 26

161 162 169 185

84 93

145

154 13

16

16

17

2012 2013 2014 2015

R&D AND CAPEX BREAKDOWN

334 359 415 448

258 271

330 356

2012 2013 2014 2015

R&D expensed to the P&L Capex PP&E Capitalised R&D Other intangible assets

Highlights

• Capex have peaked in 2015 due to renewal of our product range and is expected to remain at similar levels in 2016

• The strategic business plan foresees a gradual reduction of capex from 2017 to 2019

• Depreciation and amortisation is expected to increase over the business plan period

R&D and Capex (€m)

Expensed R&D and Capex Gross Capex

Q2 2016 Results

28 28

Note: (1) Reconciliations to non-gaap financial measures are provided in the appendix

(2) Assuming FX consistent with current market conditions

(3) Including an ordinary cash distribution to the holders of common shares

…ON THE WAY TO ANOTHER RECORD YEAR

A RECORD SECOND QUARTER…

Shipments at 2,214 units, increased

by 8% vs. previous year (+155 units) – Solid performance of new models: the 488 GTB,

488 Spider and F12tdf

– LaFerrari finished its limited series run

Financial results – Net revenues grew 5.9% to €811 million

– Adjusted EBIT(1) of €156 million, 310 bps margin

increase

– Adjusted net profit(1) up 35% to €104 million

– Net industrial debt(1) at €763 million, better than

March 2016

New key product launched and

recent events – Recently unveiled open-top LaFerrari, details to be

provided at the Paris International Motor Show

– Recently signed a sponsorship agreement with

Ray-Ban

Confirming 2016 guidance(2) – Shipments: ~8,000 including supercars

– Net revenues: >€3 billion

– Adjusted EBITDA: ≥ €800 million

– Net industrial debt(3): ≤ €730 million

29 29

Q2 2016 HIGHLIGHTS

(797)

(763)

Dec. 31, 2015

Jun. 30, 2016

Shipments

(units)

Total shipments up 8% driven by a 16% increase in V8, which was partially offset by a 22%

decrease in V12:

766

811

Q2'15

Q2'16

194

217

Q2'15

Q2'16

Net revenues up 5.9% (+6.2% at constant currencies), all revenue lines positively contributing, in

particular Cars and spare parts driven by positive volumes partially offset by mix:

173

145

289 Q2'15

Q2'16

2,059

2,214

Q2'15

Q2'16

Industrial free

cash flow(1)

(€M)

Net revenues

(€M)

Adjusted EBITDA(1)

(€M and

margin %)

Net industrial

debt(1)

(€M)

Industrial free cash flow(1) primarily driven by adjusted EBITDA(1), positive change of working

capital and timing effect of advances on the new open-top LaFerrari, partially offset by capex

and the first 2016 tax advance.

Q2 2015 included one-time of €116 million.

Net industrial debt(1) reduced to €763 million primarily due to industrial free cash flow(1)

generation partially offset by €87 million cash distribution to holders of common shares and

€13 million dividends paid to NCI

Adjusted EBITDA(1) grew by 12% primarily driven by higher volume and positive contribution from Sponsorship, commercial and brand as well as other supporting activities. Adjusted EBITDA(1) excludes charges for Takata airbag inflator recalls.

Americas: €209 million (-12.7%) due to lower sales of LaFerrari

EMEA: €217 million (+6.5%) due to higher shipments of 488 family and F12tdf

Greater China: €80 million (+60.6%) due to 488 family volume increase

Rest of APAC: €84 million (-2.1%) due to mix, performance affected by timing, with 488 Spider and F12tdf having just arrived on the market

19.3%

16.2%

Adjusted EBIT(1)

(€M and

margin %) 124

156

Q2'15

Q2'16

Adjusted EBIT(1) margin increased by 310 bps driven by strong adjusted EBITDA(1) and lower D&A mainly due to 458 family and LaFerrari phase-out

26.9%

25.4%

Continuous strong sales of the new 488 GTB and 488 Spider

F12tdf reaching global distribution

F12berlinetta at its 5th year of commercialization continues to perform better than expected

LaFerrari finished its limited series run

FF phasing out in line with plans

GTC4Lusso, distribution will commence in Q3 2016

Note: (1) reconciliations to non-gaap financial measures are provided in the appendix.

Certain totals in the tables included in this document may not add due to rounding.

30 30

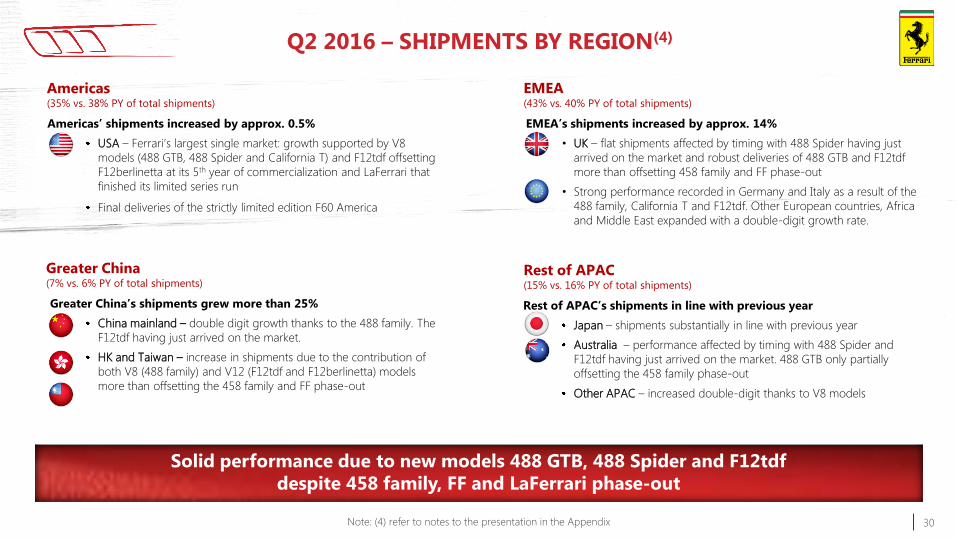

Q2 2016 – SHIPMENTS BY REGION(4)

Americas (35% vs. 38% PY of total shipments)

Americas’ shipments increased by approx. 0.5%

USA – Ferrari’s largest single market: growth supported by V8

models (488 GTB, 488 Spider and California T) and F12tdf offsetting

F12berlinetta at its 5th year of commercialization and LaFerrari that

finished its limited series run

Final deliveries of the strictly limited edition F60 America

Greater China (7% vs. 6% PY of total shipments)

Greater China’s shipments grew more than 25%

China mainland – double digit growth thanks to the 488 family. The

F12tdf having just arrived on the market.

HK and Taiwan – increase in shipments due to the contribution of

both V8 (488 family) and V12 (F12tdf and F12berlinetta) models

more than offsetting the 458 family and FF phase-out

EMEA (43% vs. 40% PY of total shipments)

EMEA’s shipments increased by approx. 14%

• UK – flat shipments affected by timing with 488 Spider having just

arrived on the market and robust deliveries of 488 GTB and F12tdf

more than offsetting 458 family and FF phase-out

• Strong performance recorded in Germany and Italy as a result of the

488 family, California T and F12tdf. Other European countries, Africa

and Middle East expanded with a double-digit growth rate.

Rest of APAC (15% vs. 16% PY of total shipments)

Rest of APAC’s shipments in line with previous year

Japan – shipments substantially in line with previous year

Australia – performance affected by timing with 488 Spider and

F12tdf having just arrived on the market. 488 GTB only partially

offsetting the 458 family phase-out

Other APAC – increased double-digit thanks to V8 models

Solid performance due to new models 488 GTB, 488 Spider and F12tdf

despite 458 family, FF and LaFerrari phase-out

Note: (4) refer to notes to the presentation in the Appendix

31

NET REVENUES BRIDGE Q2 2015-2016

+5.9%

(+6.2% at constant currencies)

579 589

57 71

103117

27

1014 14 7

34

Q2 2015 Cars and spare parts Engines Sponsorship,

commercial and

brand

Other Q2 2016

Cars and spare parts Engines Sponsorship, commercial and brand Other

766

811(€M)

(5) (6)

(7)

(8)

Note: refer to notes to the presentation in the Appendix

• €10 million increase in Cars and spare parts due to higher volumes led by new models 488 GTB, 488 Spider, F12tdf, the

non-registered car FXX K and the limited edition F60 America, along with a higher contribution from personalization partially

offset by LaFerrari that finished its limited series run

• €14 million increase in Engines mainly attributable to higher rental revenues from other Formula 1 Teams, Maserati engines in

line with previous year

• €14 million increase in Sponsorship, commercial and brand mainly due to better championship ranking, higher sponsorship

revenues and positive contribution from brand related activities

32

ADJUSTED EBIT(1) BRIDGE Q2 2015-2016

Note: (1) reconciliations to non-gaap financial measures are provided in the appendix

(€M)

Margin w/o

FX hedges

Adj. EBITDA Adj. EBITDA

194 217

25.4% 26.9%

(25)

124 24

11 0 8 14 156

Adj. EBIT Q2

2015

Vol. Mix Ind. Costs /

R&D

SG&A FX Other Adj. EBIT Q2

2016

Margin

16.2%

20.5%

(41) (23)

Margin

19.3%

21.5%

• Volume increase of approx. 230 cars (excluding LaFerrari) thanks to the newly launched 488 GTB, 488 Spider and F12tdf as well as positive contribution from personalization

• Negative mix impacted by LaFerrari that finished its limited series run and V8 slightly higher compared to the previous year partially offset by the non-registered car FXX K and the limited edition F60 America

• Industrial costs / R&D driven by lower D&A for 458 family and LaFerrari phase-out coupled with positive contribution from industrial cost savings partially offset by F1 costs

• SG&A costs flat with new store openings, new model launches and corporate costs offset by bad debt in Q2 2015

• Positive impact on FX net of hedging mainly due to USD partially offset by GBP

• Other, positive contribution from Sponsorship, commercial, brand as well as other supporting activities

33 33

NET INDUSTRIAL DEBT BRIDGE(1) MAR 31, 2016 – JUN 30, 2016

Note: (1) reconciliations to non-gaap financial measures are provided in the appendix

(€M)

217

7

62(782)

(51)(90) (100)

(26) (763)

March 31, 2016

Net industrial

debt

Adj. EBITDA Net ∆ working

capital

Tax paid Capex Other Cash distribution

and dividends

paid

FX and other June 30, 2016

Net industrial

debt

Industrial FCF €145m

• Industrial free cash flow(1) of €145 million driven by strong adjusted EBITDA(1) of €217 million, positive change of working capital and timing effect of

advances on the new open-top LaFerrari, partially offset by capex of €90 million and the first 2016 tax advance of €51 million

• Net industrial debt(1) of €763 million, better than Q1 primarily due to industrial free cash flow(1) partially offset by €87 million cash distribution to

holders of common shares and €13 million dividends paid to NCI

34 34

DEBT AND LIQUIDITY POSITION

Gross Debt Maturity Profile (€M) Cash and Marketable Securities (€M)

Net Cash/Net Industrial Debt (€M)

Maintaining a Conservative Industrial Leverage

Net Industrial Debt (€M)

Net Industrial Debt in line with EBITDA

Jun. 30, Mar. 31, Adj.

(€M) 2016 2016 FY 2015 (9)FY 2015 FY 2014

Euro 343 356 137 22 10

US Dollar 96 41 21 1 14

Chinese Yuan 73 99 106 106 74

Japanese Yen 29 24 41 41 27

Other Currencies 44 43 17 13 9

Total (€ equivalent) 585 563 322 183 134

At June 30 At March 31 At December 31

(€M) 2016 2016 2015 2014

Gross Debt (2,483) (2,442) (2,260) (510)

Cash & Cash Equivalents 585 563 183 134

Deposits in FCA Cash Management Pools - - 139 942

(Net Debt)/Net Cash (1,898) (1,879) (1,938) 566

Funded Self-Liquidating Financial 1,135 1,097 1,141 1,061

Receivables Portfolio

(Net Industrial Debt)/Net Industrial Cash (763) (782) (797) 1,627

Undrawn Committed Credit Lines 500 500 500 -

Total Available Liquidity 1,085 1,063 822 1,076

Note: (9) After settlement of deposits on FCA Group cash management pools and Financial liabilities with FCA

167

333 333 333 333

500

102 76 47

118

139

4 4 2

2016 2017 2018 2019 2020 2023Term Loan Bond US Securitization Other Financial Liabilities

Cash Maturities

285

574

414 384 335

500

(1,898)

1,135

June 30, 2016

Net Industrial Debt

Funded Self-liquidating

Financial

Receivables Portfolio

June 30, 2016

Net Debt

(763)

35 35

Shipments

Net revenues

Adj. EBITDA

Net industrial debt

˜ 8,000

>€3 billion

≥€800 million

≤€730 million(3)

CONFIRMING 2016 GUIDANCE

Guidance(2)

Note: (2) Assuming FX consistent with current market conditions

(3) Including an ordinary cash distribution to the holders of common shares

36 36

A UNIQUE VALUE PROPOSITION

Controlled Growth

in Developed and

Emerging Markets

Regular New Model

Introductions and

Enhancements

Pursue Excellence

in Formula 1 Racing

Controlled Growth

in Adjacent Luxury

and Lifestyle

Categories

Protect and Enhance the Value and Exclusivity of the Ferrari Brand, While Pursuing Profitable Growth

38 38

INCOME STATEMENT

(€m) At December 31,

2015 2014 2013 2012

Net Revenues 2,854 2,762 2,335 2,225

Cost of sales 1,499 1,506 1,235 1,199

Selling, general and administrative costs 339 300 260 243

Research and development costs 562 541 479 431

Other expenses / (income), net 11 26 (2) 17

EBIT 444 389 364 335

Net financial (expenses) / income (10) 9 3 (1)

Profit before taxes 434 398 366 335

Income tax expense 144 133 120 101

Net profit 290 265 246 233

Net profit attributable to:

Owners of the parent 288 261 241 225

Non-controlling interests 2 4 5 8

Basic and diluted earnings per common share (in €) 1.52 1.38 1.27 1.19

Company filings prepared in accordance with IFRS

39 39

BALANCE SHEET

(€m) At December 31,

(€m) At December 31,

2015 2014 2013 2012 2015 2014 2013 2012

Assets Total (deficit) / equity (19) 2,478 2,316 2,041

Goodwill 787 787 787 787 Debt 2,260 510 317 261

Intangible assets 308 265 242 265 Other financial liabilities 103 104 4 23

Property, plant and equipment 626 585 568 545 Trade payables 507 536 486 480

Other non-current assets 134 159 79 76 Current tax payables 125 110 104 109

Total non-current assets 1,856 1,797 1,677 1,673 Employee benefits 78 77 65 79

Deposits in FCA Group cash

management 139 942 684 457 Provisions 142 135 104 119

Cash and cash equivalents 183 134 114 100 Other liabilities 678 692 498 352

Inventories 295 296 237 216 Total liabilities 3,895 2,163 1,579 1,424

Trade receivables 158 184 206 136 Total (deficit) / equity and liabilities 3,875 4,641 3,895 3,465

Receivables from financing activities 1,174 1,224 863 803

Other current assets 70 64 115 81

Total current assets 2,020 2,845 2,219 1,792

Total assets 3,875 4,641 3,895 3,465

Company filings prepared in accordance with IFRS

40

CASH FLOW STATEMENT

(€m) At December 31,

2015 2014 2013 2012

Profit before taxes 434 398 366 335

Amortization and depreciation 275 289 270 238

Change in Operating Working Capital (33) (52) (88) 14

Change in Receivables from Financing Activities 121 (202) (57) (148)

Paid Taxes (145) (141) (139) (134)

Other Cash Flows from Operating Activities 55 134 101 160

Cash Flow from Operating Activities 707 426 454 463

Net Capex (317) (290) (267) (258)

Cash Flow from Investing Activities (317) (290) (267) (258)

Net Repayment of Bank Borrowings 2,119 79 5 10

Net change in financial liabilities with FCA Group (3,211) 89 51 (293)

Net change in deposits in FCA Group cash management pools 814 (247) (227) 73

Dividends paid to non-controlling interest (54) (15) 0 (7)

Other Cash Flows from Financing Activities (20) (28) 8 23

Cash Flow from Financing Activities (351) (122) (163) (194)

Translation exchange differences 10 6 (9) (4)

Net Change in Cash 48 20 14 6

Cash at Beginning of the Period 134 114 100 94

Cash at End of the Period 183 134 114 100

Company filings prepared in accordance with IFRS

41 41

NOTES TO THE PRESENTATION

1. reconciliations to non-gaap financial measures are

provided in the appendix

2. Assuming FX consistent with current market conditions

3. Including an ordinary cash distribution to the holders of

common shares

4. Shipments geographical breakdown

EMEA includes: Italy, UK, Germany, Switzerland, France,

Middle East (includes the United Arab Emirates, Saudi

Arabia, Bahrain, Lebanon, Qatar, Oman and Kuwait)

and Rest of EMEA (includes Africa and the other

European markets not separately identified);

Americas includes: United States of America, Canada,

Mexico, the Caribbean and Central and South America;

Greater China includes: China, Hong Kong and Taiwan;

Rest of APAC includes: Japan, Australia, Singapore,

Indonesia and South Korea

5. Includes the net revenues generated from shipments of

our cars, including any personalization revenue

generated on these cars and sales of spare parts

6. Includes the net revenues generated from the sale of

engines to Maserati for use in their cars, and the

revenues generated from the rental of engines to other

Formula 1 racing teams

7. Includes the net revenues earned by our Formula 1

racing team through sponsorship agreements and our

share of the Formula 1 World Championship

commercial revenues and net revenues generated

through the Ferrari brand, including merchandising,

licensing and royalty income

8. Primarily includes interest income generated by the

Ferrari Financial Services group and net revenues from

the management of the Mugello racetrack

42 42

GROUP SHIPMENTS

833 953

772 774

127 160

327

327 2,059

2,214

Q2 2015 Q2 2016

1,598 1,903

1,287

1,297

261

316 548

580 3,694

4,096

H1 2015 H1 2016

EMEA Americas Greater China Rest of APAC

3,351 ~3,500

2,640 ~2,700

610 ~700

1,063 ~1,100

7,664 ~8,000

FY 2015 FY 2016E

Note: Graphs not to scale. Shipments including supercar LaFerrari

+8% +11%

43 43

KEY PERFORMANCE METRICS

€M, except as otherwise stated FY ’15 FY ’14 FY ’13 FY ’12

Worldwide Shipments (Units) 7,664 7,255 7,000 7,405

Net Revenues 2,854 2,762 2,335 2,225

EBIT 444 389 364 335

Adjustments 29 15 - -

Adjusted EBIT(1) 473 404 364 335

Net Financial (Expenses)/Income (10) 9 2 (1)

Profit before Taxes 434 398 366 334

Income Tax Expense 144 133 120 101

Effective Tax Rate 33.2% 33.5% 32.8% 30.2%

Net Profit 290 265 246 233

EPS 1.52 1.38 1.27 1.19

EBITDA(1) 719 678 634 573

Adjusted EBITDA(1) 748 693 634 573

Note: (1) Reconciliation of non-gaap financial measures are provided in the appendix

44 44

KEY PERFORMANCE METRICS

Note: (1) Reconciliation to non-gaap financial measures are provided in the appendix.

Certain totals in the tables included in this document may not add due to rounding.

Q2 ‘16 Q2 ‘15 €M, except as otherwise stated H1 ‘16 H1 ‘15

2,214 2,059 Worldwide shipments (units) 4,096 3,694

811 766 Net revenues 1,486 1,387

207 192 EBITDA(1) 385 348

217 194 Adjusted EBITDA(1) 395 354

146 122 EBIT 267 218

156 124 Adjusted EBIT(1) 277 224

5 8 Net financial expenses 14 6

141 114 Profit before taxes 253 212

44 38 Income tax expense 78 71

30.7% 33.5% Effective tax rate 30.8% 33.5%

97 76 Net profit 175 141

104 78 Adjusted net profit(1) 182 145

0.52 0.40 EPS 0.93 0.74

0.55 0.41 Adjusted EPS(1) 0.96 0.76

45 45

NON-GAAP FINANCIAL MEASURES

Non-GAAP financial measures

Operations are monitored through the use of

various Non-GAAP financial measures that

may not be comparable to other similarly

titled measures of other companies

Accordingly, investors and analysts should

exercise appropriate caution in comparing

these supplemental financial measures to

similarly titled financial measures reported by

other companies

We believe that these supplemental financial

measures provide comparable measures of

its financial performance which then facilitate

management’s ability to identify operational

trends, as well as make decisions regarding

future spending, resource allocations and

other operational decisions

Non-GAAP financial measures

EBITDA is defined as net profit before income tax expense, net financial

expenses/(income) and depreciation and amortization. Adjusted EBITDA is defined as

EBITDA as adjusted for income and costs, which are significant in nature, but expected

to occur infrequently

Adjusted Earnings Before Interest and Taxes (“Adjusted EBIT”) represents EBIT as

adjusted for income and costs, which are significant in nature, but expected to occur

infrequently

Adjusted net profit represents net profit as adjusted for income and costs, which are

significant in nature, but expected to occur infrequently

Adjusted earning per share represents earning per share as adjusted for income and

costs, which are significant in nature, but expected to occur infrequently

Net Industrial Debt defined as Net Debt excluding the funded portion of the self-

liquidating financial receivables portfolio, is the primary measure to analyze our financial

leverage and capital structure, and is one of the key indicators used to measure our

financial position

Free Cash Flow and Free Cash Flow from Industrial Activities are two of management’s

primary key performance indicators to measure the Group’s performance. Free Cash

flow is defined as net cash generated from operations less cash flows used in investing

activities. Free Cash Flow from Industrial Activities is defined as Free Cash Flow adjusted

for the change in the self-liquidating financial receivables portfolio.

46 46

RECONCILIATION OF NON-GAAP MEASURES: ADJ. EBIT

€M, except as otherwise state FY ’15 FY ’14 FY ’13 FY ’12

EBIT 444 389 364 335

Expense Related to the Resignation of

the Former Chairman – 15 – –

Income and Expenses Incurred in

Connection with Our IPO and

Separation and Employees Extra Bonus

29 – – –

Adjusted EBIT 473 404 364 335

47 47

RECONCILIATION OF NON-GAAP MEASURES: EBITDA

€M, except as otherwise stated FY ’15 FY ’14 FY ’13 FY ’12

Net Profit 290 265 246 233

Income Tax Expense 144 133 120 101

Net Financial Expenses/(Income) 10 (9) (2) 1

Amortisation and Depreciation 275 289 270 238

EBITDA 719 678 634 573

48 48

RECONCILIATION OF NON-GAAP MEASURES: ADJ. EBITDA

€M, except as otherwise stated FY ’15 FY ’14 FY ’13 FY ’12

EBITDA 719 678 634 573

Expense Related to the Resignation of

the Former Chairman – 15 – –

Income and Expenses Incurred in

Connection with our IPO and

Separation and Employees Extra Bonus

29 – – –

Adjusted EBITDA 748 693 634 573

49 49

RECONCILIATION OF NON-GAAP MEASURES: FREE CASH FLOW

€M, except as otherwise stated FY ’15 FY ’14 FY ’13 FY ’12

Cash Flows from Operating Activities 707 426 454 463

Cash Flows Used in Investing Activities (317) (290) (267) (258)

Free Cash Flow 390 136 187 205

50 50

RECONCILIATION OF NON-GAAP MEASURES:

NET INDUSTRIAL CASH/(DEBT)

€M, except as otherwise stated December 31,

2015

December 31,

2014

December 31,

2013

December 31,

2012

Cash and Cash Equivalents 183 134 114 100

Deposits in FCA Group cash

Management Pools 139 942 684 457

Financial Liabilities with FCA Group (3) (379) (242) (196)

Financial Liabilities with Third-parties (2,257) (131) (76) (65)

Total Net Cash/(Net Debt) (1,938) 566 480 296

Funded Portion of the Self-liquidating

Financial Receivables portfolio 1,141 1,061 782 758

Net Industrial Cash/(Debt) (797) 1,627 1,262 1,054

51 51

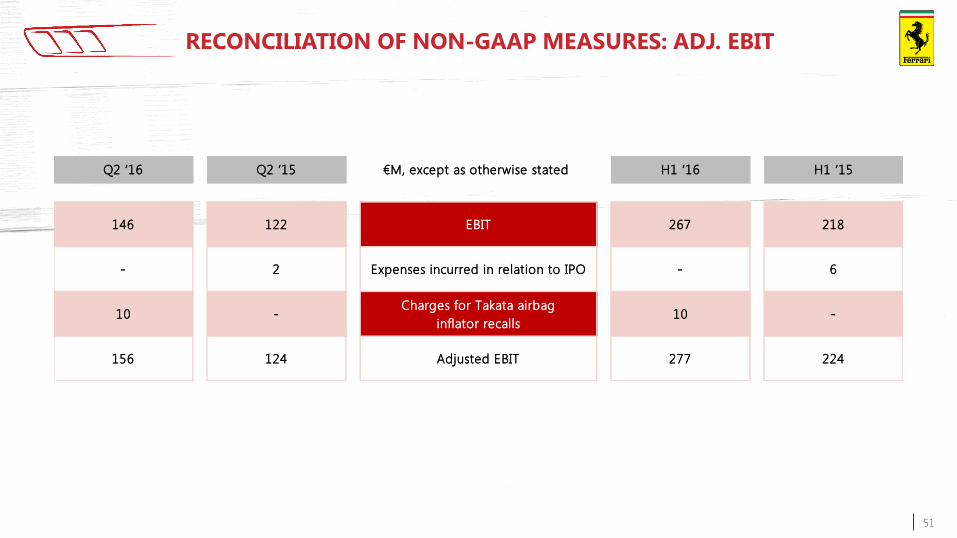

RECONCILIATION OF NON-GAAP MEASURES: ADJ. EBIT

Q2 ‘16 Q2 ‘15 €M, except as otherwise stated H1 ‘16 H1 ‘15

146 122 EBIT 267 218

- 2 Expenses incurred in relation to IPO - 6

10 -Charges for Takata airbag

inflator recalls10 -

156 124 Adjusted EBIT 277 224

52 52

RECONCILIATION OF NON-GAAP MEASURES: EBITDA

Q2 ‘16 Q2 ‘15 €M, except as otherwise stated H1 ‘16 H1 ‘15

97 76 Net profit 175 141

44 38 Income tax expenses 78 71

5 8 Net financial expenses 14 6

61 70 Amortization and depreciation 118 130

207 192 EBITDA 385 348

53 53

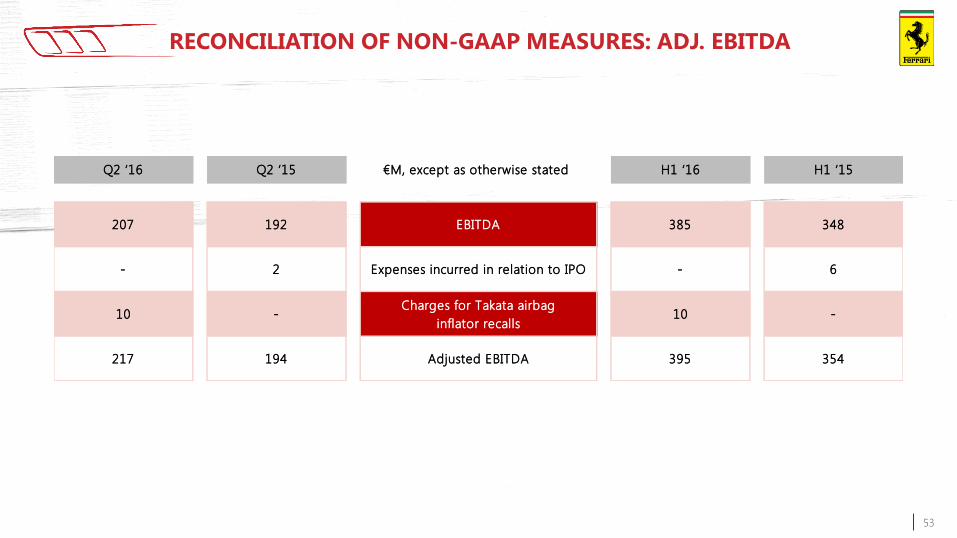

RECONCILIATION OF NON-GAAP MEASURES: ADJ. EBITDA

Q2 ‘16 Q2 ‘15 €M, except as otherwise stated H1 ‘16 H1 ‘15

207 192 EBITDA 385 348

- 2 Expenses incurred in relation to IPO - 6

10 -Charges for Takata airbag

inflator recalls10 -

217 194 Adjusted EBITDA 395 354

54 54

RECONCILIATION OF NON-GAAP MEASURES: ADJ. NET PROFIT

Q2 ‘16 Q2 ‘15 €M, except as otherwise stated H1 ‘16 H1 ‘15

97 76 Net profit 175 141

- 2 Expenses incurred in relation to IPO

(net of tax effect)- 4

7 -Charges for Takata airbag

inflator recalls (net of tax effect)7 -

104 78 Adjusted net profit 182 145

55 55

RECONCILIATION OF NON-GAAP MEASURES: ADJ. EPS

Q2 ‘16 Q2 ‘15 € per common share H1 ‘16 H1 ‘15

0.52 0.40 EPS 0.93 0.74

- 0.01 Expenses incurred in relation to IPO

(net of tax effect)- 0.02

0.04 -Charges for Takata airbag

inflator recalls (net of tax effect)0.04 -

0.55 0.41 Adjusted EPS 0.96 0.76

Certain totals in the tables included in this document may not add due to rounding

56 56

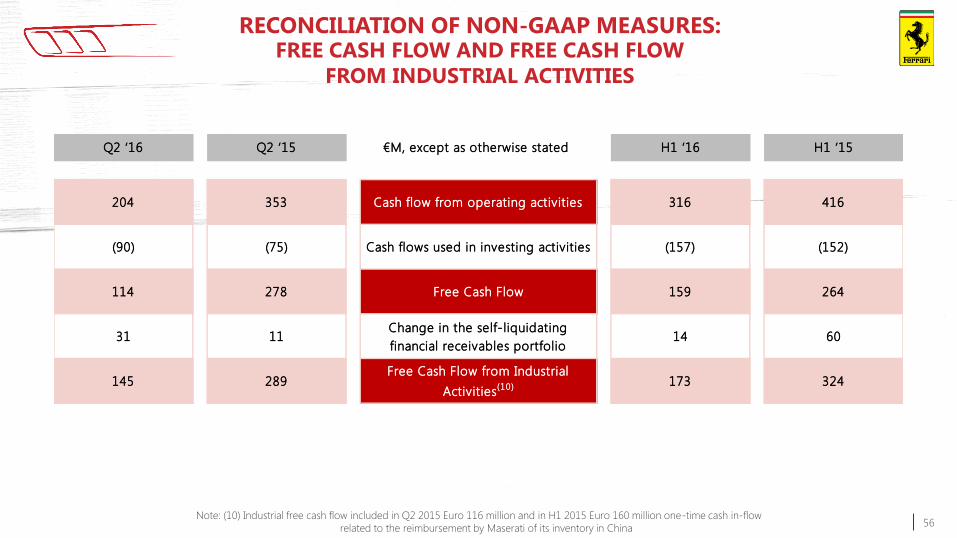

RECONCILIATION OF NON-GAAP MEASURES: FREE CASH FLOW AND FREE CASH FLOW

FROM INDUSTRIAL ACTIVITIES

Q2 ‘16 Q2 ‘15 €M, except as otherwise stated H1 ‘16 H1 ‘15

204 353 Cash flow from operating activities 316 416

(90) (75) Cash flows used in investing activities (157) (152)

114 278 Free Cash Flow 159 264

31 11 Change in the self-liquidating

financial receivables portfolio14 60

145 289 Free Cash Flow from Industrial

Activities(10) 173 324

Note: (10) Industrial free cash flow included in Q2 2015 Euro 116 million and in H1 2015 Euro 160 million one-time cash in-flow

related to the reimbursement by Maserati of its inventory in China

57 57

RECONCILIATION OF NON-GAAP MEASURES:

NET INDUSTRIAL DEBT

€M, except as otherwise stated June 30, 2016 March 31, 2016 December 31, 2015

Net Industrial Debt (763) (782) (797)

Funded portion of the self-liquidating

financial receivables portfolio1,135 1,097 1,141

Net Debt (1,898) (1,879) (1,938)

Financial liabilities with FCA Group - - (3)

Deposits in FCA Group cash management

pools- - 139

Cash and cash equivalents 585 563 183

Gross Debt (2,483) (2,442) (2,257)

A unique combination of

technology,

performance,

versatility

and sport luxury

Mid – front naturally

aspirated V12 engine:

690 hp @ 8,000 rpm

Max speed

in excess

of 335 km/h

Distribution will

commence in

Q3 2016

and it will

substitute the FF

Strictly

confidential

The new limited-edition

special series

already pre-sold

Sporting a 800 hp V12

coupled with a 120 kW

electric motor, unleashing

963 hp in total

The name and technical characteristics of

the new limited-edition special series to

be unveiled at the

Paris International Motor Show