commercial forum presentation: economic outlook in uncertain times

TRANSCRIPT

Economic Outlook in Uncertain Times

Lawrence Yun, Ph.D.Chief Economist

NATIONAL ASSOCIATION OF REALTORS®

Presentation at NAR Annual Meeting New Orleans, LA

November 5, 2010

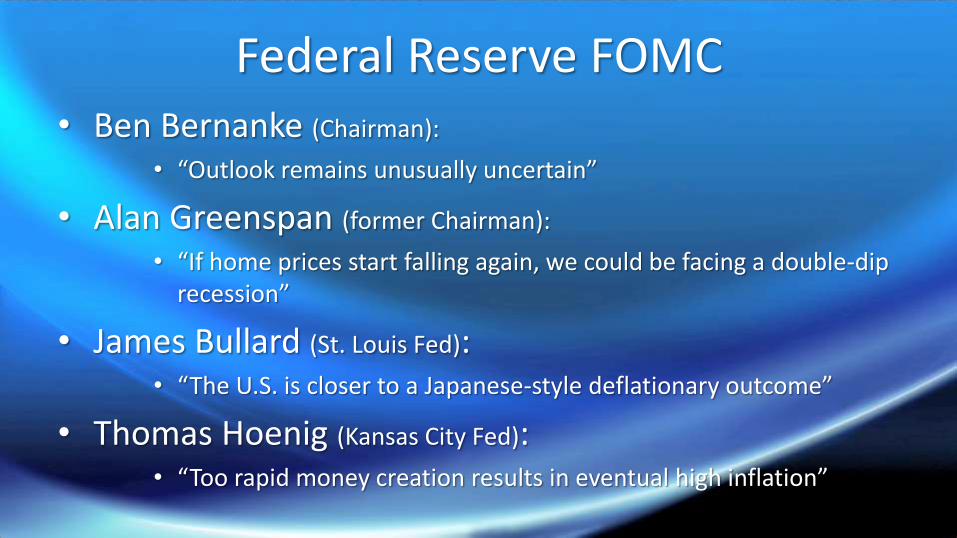

Federal Reserve FOMC • Ben Bernanke (Chairman):

• “Outlook remains unusually uncertain”

• Alan Greenspan (former Chairman):

• “If home prices start falling again, we could be facing a double-dip recession”

• James Bullard (St. Louis Fed): • “The U.S. is closer to a Japanese-style deflationary outcome”

• Thomas Hoenig (Kansas City Fed): • “Too rapid money creation results in eventual high inflation”

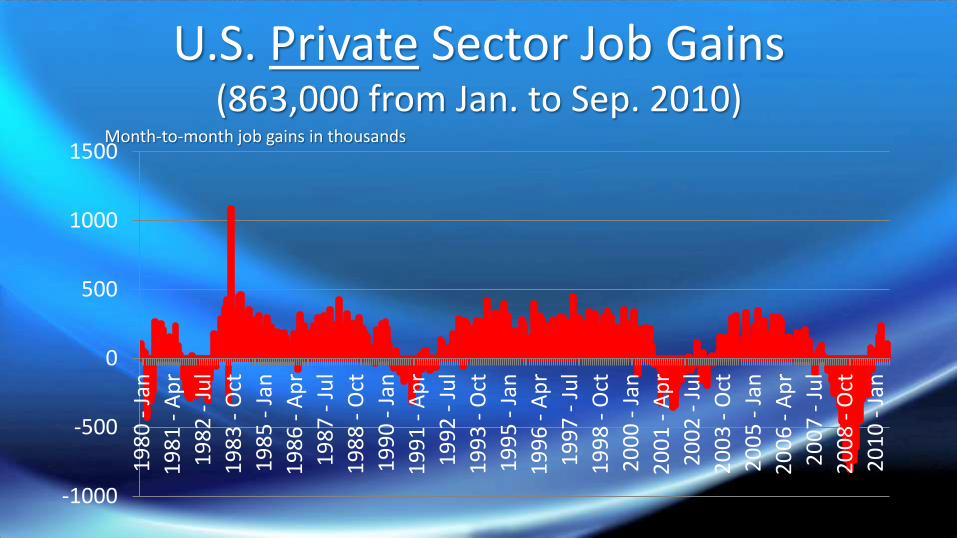

U.S. Private Sector Job Gains(863,000 from Jan. to Sep. 2010)

-1000

-500

0

500

1000

15001

98

0 -

Jan

19

81

- A

pr

19

82

- J

ul

19

83

- O

ct

19

85

- J

an

19

86

- A

pr

19

87

- J

ul

19

88

- O

ct

19

90

- J

an

19

91

- A

pr

19

92

- J

ul

19

93

- O

ct

19

95

- J

an

19

96

- A

pr

19

97

- J

ul

19

98

- O

ct

20

00

- J

an

20

01

- A

pr

20

02

- J

ul

20

03

- O

ct

20

05

- J

an

20

06

- A

pr

20

07

- J

ul

20

08

- O

ct

20

10

- J

an

Month-to-month job gains in thousands

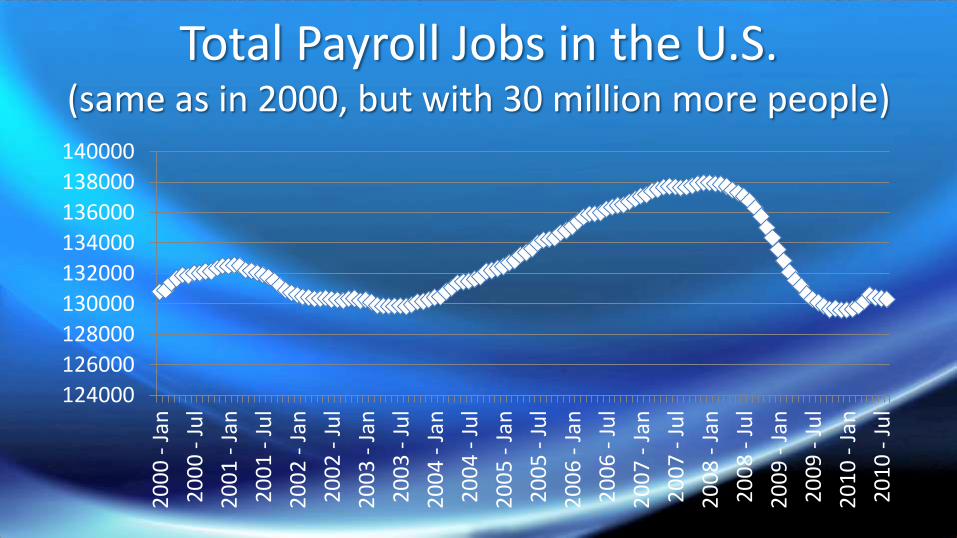

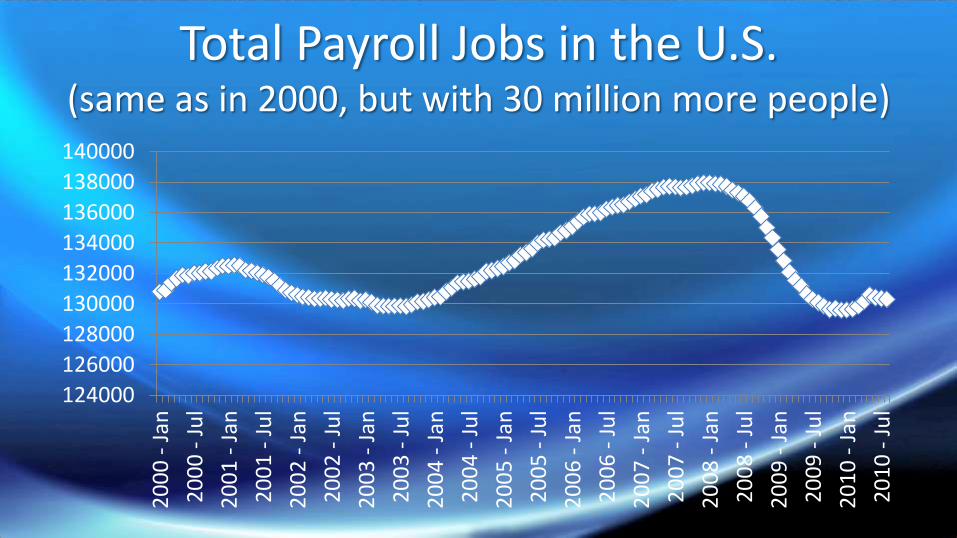

Total Payroll Jobs in the U.S. (same as in 2000, but with 30 million more people)

124000

126000

128000

130000

132000

134000

136000

138000

1400002

00

0 -

Jan

20

00

- J

ul

20

01

- J

an

20

01

- J

ul

20

02

- J

an

20

02

- J

ul

20

03

- J

an

20

03

- J

ul

20

04

- J

an

20

04

- J

ul

20

05

- J

an

20

05

- J

ul

20

06

- J

an

20

06

- J

ul

20

07

- J

an

20

07

- J

ul

20

08

- J

an

20

08

- J

ul

20

09

- J

an

20

09

- J

ul

20

10

- J

an

20

10

- J

ul

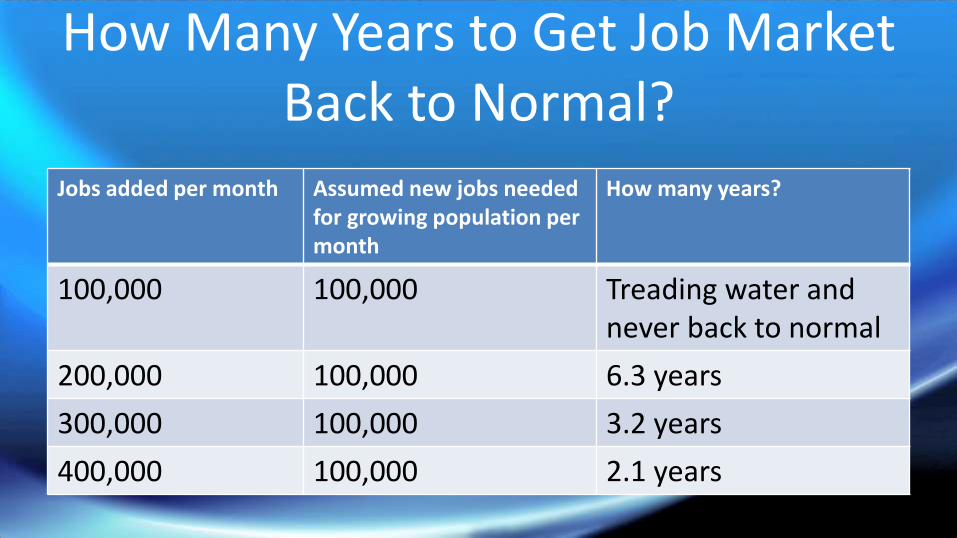

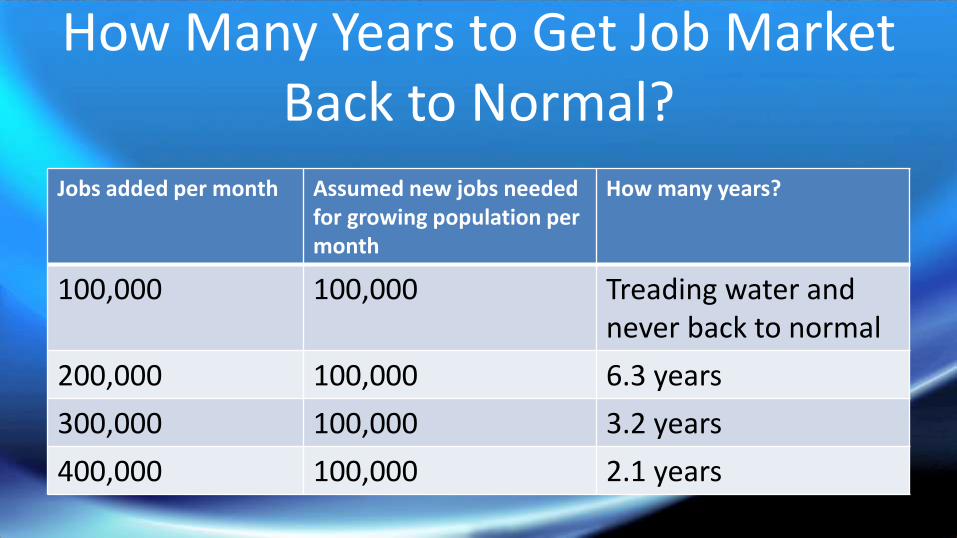

How Many Years to Get Job Market Back to Normal?

Jobs added per month Assumed new jobs needed for growing population per month

How many years?

100,000 100,000 Treading water and never back to normal

200,000 100,000 6.3 years

300,000 100,000 3.2 years

400,000 100,000 2.1 years

GDP Growing, but Deceleratingannualized % growth rate

Consumer Expenditure (Inflation adjusted in GDP accounting)

7000

7500

8000

8500

9000

9500 $ billion

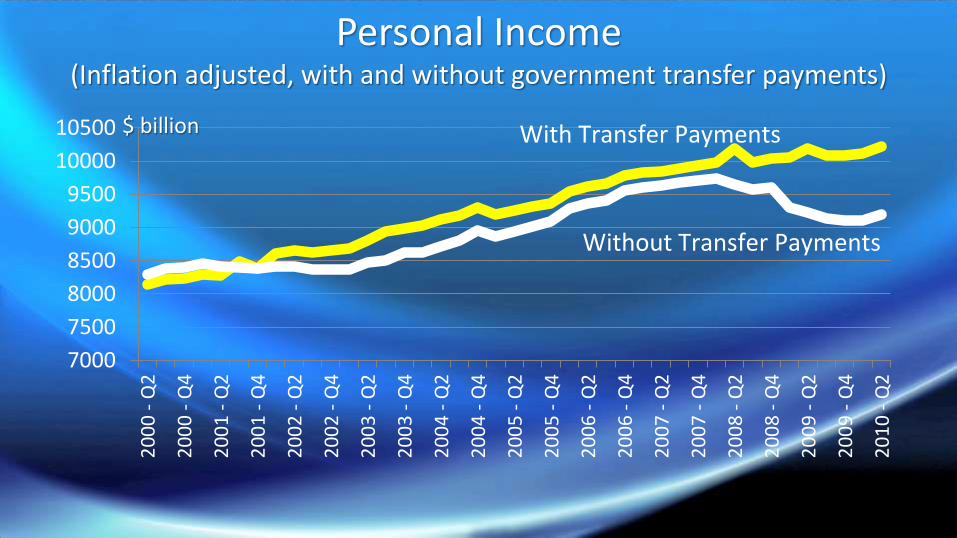

Personal Income(Inflation adjusted, with and without government transfer payments)

7000

7500

8000

8500

9000

9500

10000

105002

00

0 -

Q2

20

00

- Q

4

20

01

- Q

2

20

01

- Q

4

20

02

- Q

2

20

02

- Q

4

20

03

- Q

2

20

03

- Q

4

20

04

- Q

2

20

04

- Q

4

20

05

- Q

2

20

05

- Q

4

20

06

- Q

2

20

06

- Q

4

20

07

- Q

2

20

07

- Q

4

20

08

- Q

2

20

08

- Q

4

20

09

- Q

2

20

09

- Q

4

20

10

- Q

2

With Transfer Payments

Without Transfer Payments

$ billion

Savings Rate

0

2

4

6

8

10

12

141

98

0 -

Jan

19

81

- M

ar

19

82

- M

ay

19

83

- J

ul

19

84

- S

ep

19

85

- N

ov

19

87

- J

an

19

88

- M

ar

19

89

- M

ay

19

90

- J

ul

19

91

- S

ep

19

92

- N

ov

19

94

- J

an

19

95

- M

ar

19

96

- M

ay

19

97

- J

ul

19

98

- S

ep

19

99

- N

ov

20

01

- J

an

20

02

- M

ar

20

03

- M

ay

20

04

- J

ul

20

05

- S

ep

20

06

- N

ov

20

08

- J

an

20

09

- M

ar

20

10

- M

ay

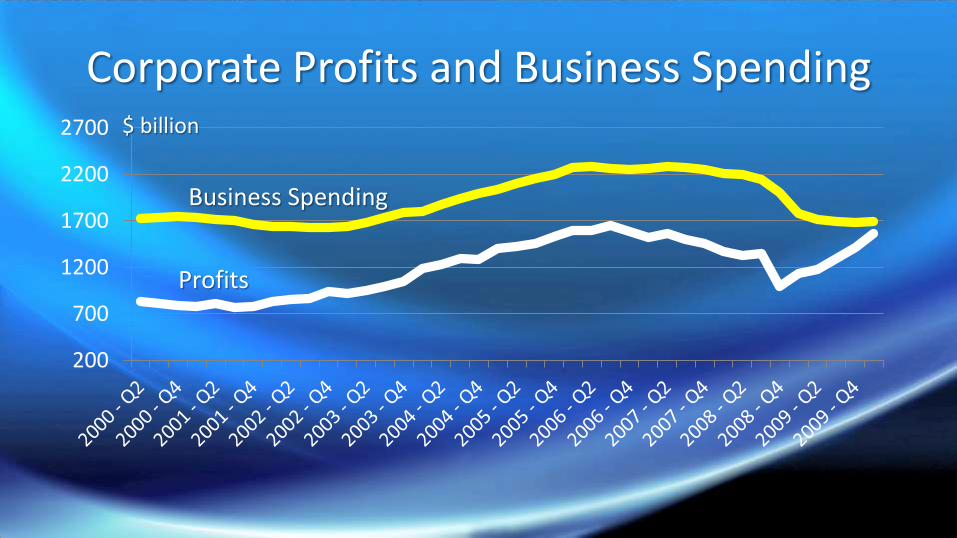

Corporate Profits and Business Spending

200

700

1200

1700

2200

2700

Business Spending

Profits

$ billion

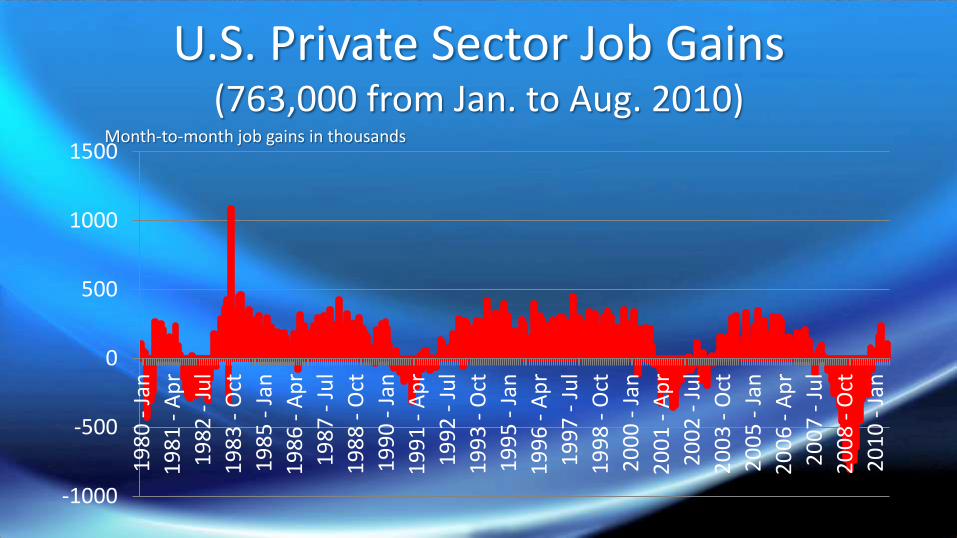

U.S. Private Sector Job Gains(763,000 from Jan. to Aug. 2010)

-1000

-500

0

500

1000

15001

98

0 -

Jan

19

81

- A

pr

19

82

- J

ul

19

83

- O

ct

19

85

- J

an

19

86

- A

pr

19

87

- J

ul

19

88

- O

ct

19

90

- J

an

19

91

- A

pr

19

92

- J

ul

19

93

- O

ct

19

95

- J

an

19

96

- A

pr

19

97

- J

ul

19

98

- O

ct

20

00

- J

an

20

01

- A

pr

20

02

- J

ul

20

03

- O

ct

20

05

- J

an

20

06

- A

pr

20

07

- J

ul

20

08

- O

ct

20

10

- J

an

Month-to-month job gains in thousands

Total Payroll Jobs in the U.S. (same as in 2000, but with 30 million more people)

124000

126000

128000

130000

132000

134000

136000

138000

1400002

00

0 -

Jan

20

00

- J

ul

20

01

- J

an

20

01

- J

ul

20

02

- J

an

20

02

- J

ul

20

03

- J

an

20

03

- J

ul

20

04

- J

an

20

04

- J

ul

20

05

- J

an

20

05

- J

ul

20

06

- J

an

20

06

- J

ul

20

07

- J

an

20

07

- J

ul

20

08

- J

an

20

08

- J

ul

20

09

- J

an

20

09

- J

ul

20

10

- J

an

20

10

- J

ul

How Many Years to Get Job Market Back to Normal?

Jobs added per month Assumed new jobs needed for growing population per month

How many years?

100,000 100,000 Treading water and never back to normal

200,000 100,000 6.3 years

300,000 100,000 3.2 years

400,000 100,000 2.1 years

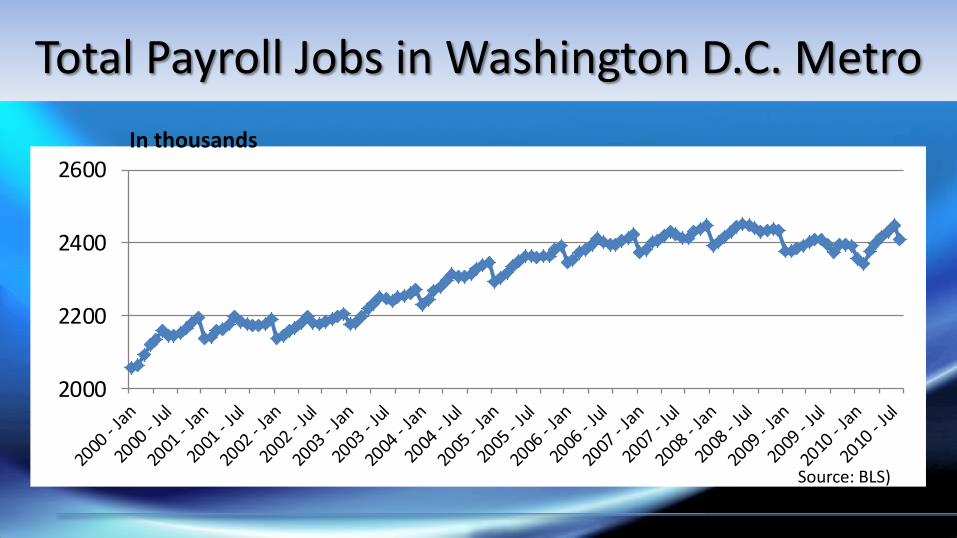

Local Job Market DifferencesMetro Job Changes from 12-months ago

Boston +36,600

Dallas – Ft. Worth +28,700

Washington +20,500

Detroit -31,700

San Francisco -42,000

Chicago -71,600

3500

4000

4500

5000

Source: BLS

In thousands

Total Payroll Jobs in Michigan

2000

2200

2400

2600

Source: BLS)

In thousands

Total Payroll Jobs in Washington D.C. Metro

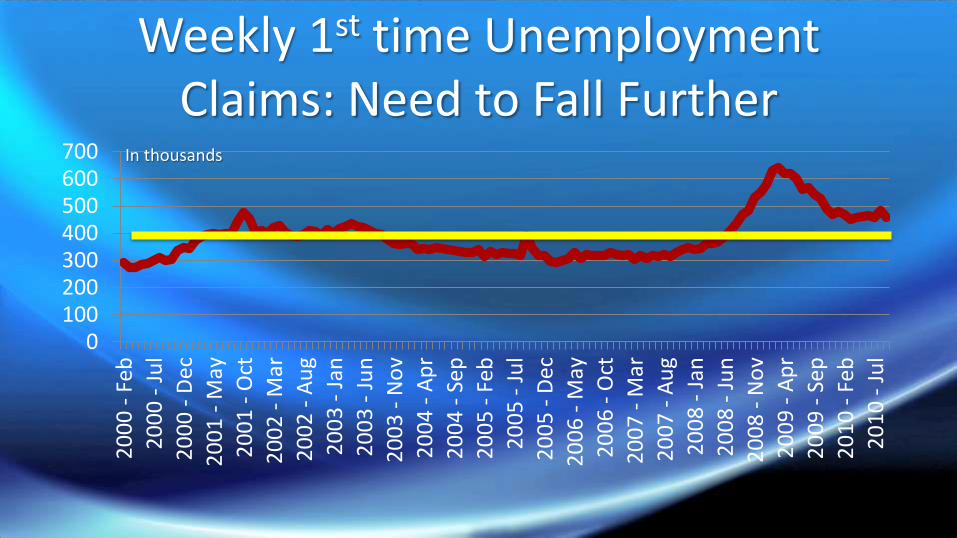

Weekly 1st time Unemployment Claims: Need to Fall Further

0100200300400500600700

20

00

- F

eb

20

00

- J

ul

20

00

- D

ec

20

01

- M

ay

20

01

- O

ct

20

02

- M

ar

20

02

- A

ug

20

03

- J

an

20

03

- J

un

20

03

- N

ov

20

04

- A

pr

20

04

- S

ep

20

05

- F

eb

20

05

- J

ul

20

05

- D

ec

20

06

- M

ay

20

06

- O

ct

20

07

- M

ar

20

07

- A

ug

20

08

- J

an

20

08

- J

un

20

08

- N

ov

20

09

- A

pr

20

09

- S

ep

20

10

- F

eb

20

10

- J

ul

In thousands

$-

$50

$100

$150

$200

$250

$300

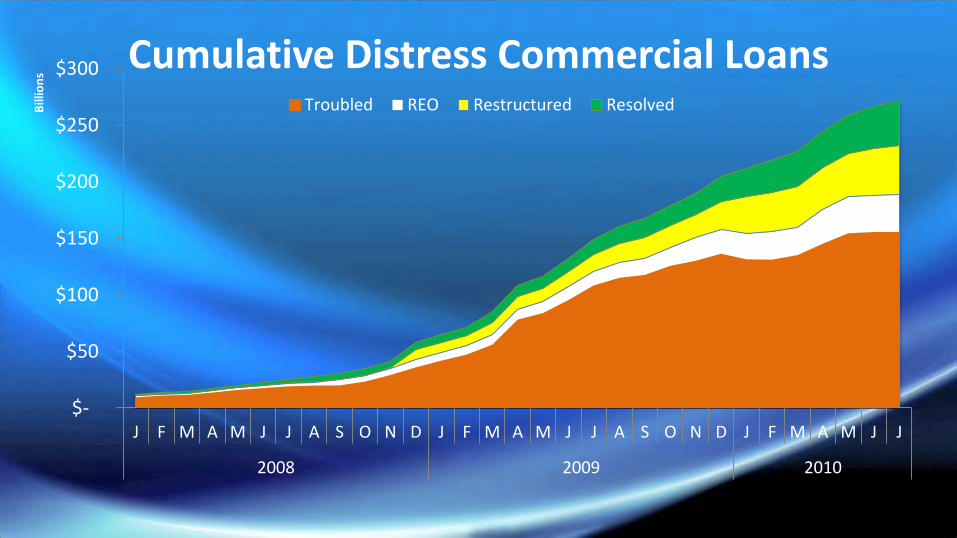

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J

2008 2009 2010

Bill

ion

s

Cumulative Distress Commercial LoansTroubled REO Restructured Resolved

Source: Real Capital Analytics

Real Estate Price

1.0

1.2

1.4

1.6

1.8

2.0

20

01

- J

an

20

01

- J

un

20

01

- N

ov

20

02

- A

pr

20

02

- S

ep

20

03

- F

eb

20

03

- J

ul

20

03

- D

ec

20

04

- M

ay

20

04

- O

ct

20

05

- M

ar

20

05

- A

ug

20

06

- J

an

20

06

- J

un

20

06

- N

ov

20

07

- A

pr

20

07

- S

ep

20

08

- F

eb

20

08

- J

ul

20

08

- D

ec

20

09

- M

ay

20

09

- O

ct

20

10

- M

ar

Residential: Case-Shiller

Commercial: MIT

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

J06

M M J S N J07

M M J S N J08

M M J S N J09

M M J S N J10

M M J S

Commercial Mortgage Backed Security IssuanceMonthly CMBS Issuance ($ Mil)

Source: Commercial Mortgage Alert

0

50

100

150

200

250

300

350

400

20

02

.Q1

20

02

.Q2

20

02

.Q3

20

02

.Q4

20

03

.Q1

20

03

.Q2

20

03

.Q3

20

03

.Q4

20

04

.Q1

20

04

.Q2

20

04

.Q3

20

04

.Q4

20

05

.Q1

20

05

.Q2

20

05

.Q3

20

05

.Q4

20

06

.Q1

20

06

.Q2

20

06

.Q3

20

06

.Q4

20

07

.Q1

20

07

.Q2

20

07

.Q3

20

07

.Q4

20

08

.Q1

20

08

.Q2

20

08

.Q3

20

08

.Q4

20

09

.Q1

20

09

.Q2

20

09

.Q3

20

09

.Q4

20

10

.Q1

20

10

.Q2

Origination Volume Index (2001 Qtr Avg=100)

Source: Mortgage Bankers Association

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

J06

F M A M J J A S O N D J07

F M A M J J A S O N D J08

F M A M J J A S O N D J09

F M A M J J A S O N D J10

F M A M J J A S

Public EquityMonthly US REIT Equity Issuance ($ Mil)

Source: NAREIT

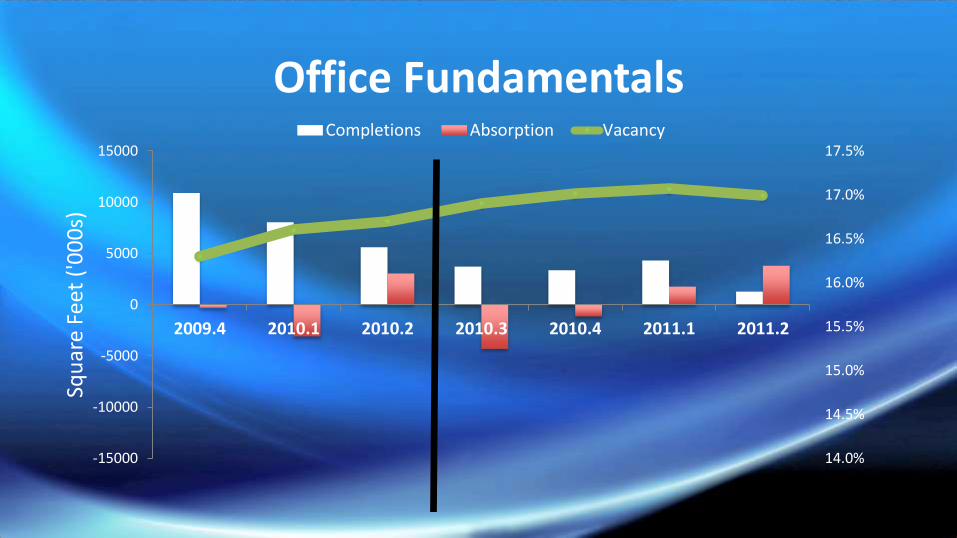

14.0%

14.5%

15.0%

15.5%

16.0%

16.5%

17.0%

17.5%

-15000

-10000

-5000

0

5000

10000

15000

2009.4 2010.1 2010.2 2010.3 2010.4 2011.1 2011.2

Squ

are

Feet

('0

00

s)Office Fundamentals

Completions Absorption Vacancy

Source: NAR / CBRE-EA

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Office Vacancies: 2010.Q3

Source: NAR / CBRE-EA

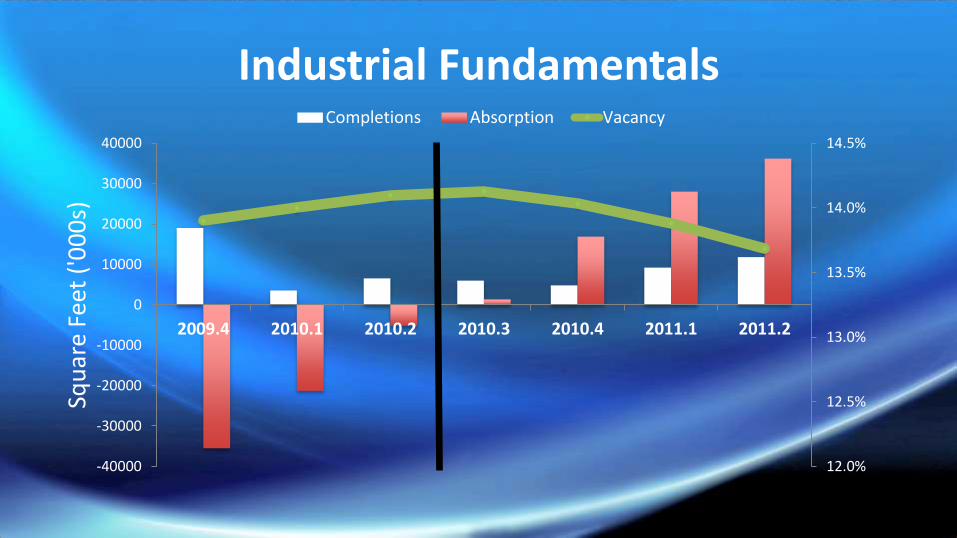

12.0%

12.5%

13.0%

13.5%

14.0%

14.5%

-40000

-30000

-20000

-10000

0

10000

20000

30000

40000

2009.4 2010.1 2010.2 2010.3 2010.4 2011.1 2011.2

Squ

are

Feet

('0

00

s)Industrial Fundamentals

Completions Absorption Vacancy

Source: NAR / CBRE-EA

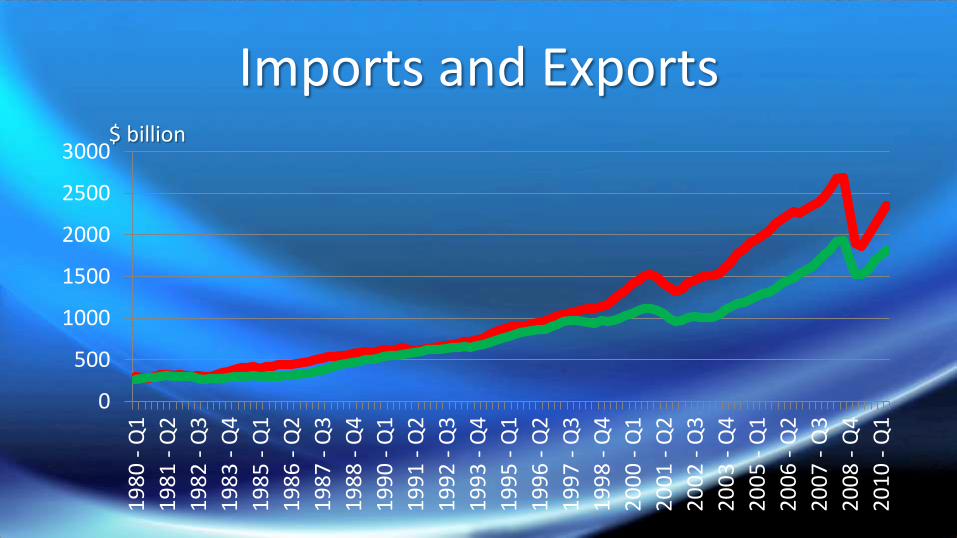

Imports and Exports

0

500

1000

1500

2000

2500

30001

98

0 -

Q1

19

81

- Q

2

19

82

- Q

3

19

83

- Q

4

19

85

- Q

1

19

86

- Q

2

19

87

- Q

3

19

88

- Q

4

19

90

- Q

1

19

91

- Q

2

19

92

- Q

3

19

93

- Q

4

19

95

- Q

1

19

96

- Q

2

19

97

- Q

3

19

98

- Q

4

20

00

- Q

1

20

01

- Q

2

20

02

- Q

3

20

03

- Q

4

20

05

- Q

1

20

06

- Q

2

20

07

- Q

3

20

08

- Q

4

20

10

- Q

1

$ billion

U.S. Dollar Strength

0

20

40

60

80

100

120

1401

98

0 -

Feb

19

81

- F

eb1

98

2 -

Feb

19

83

- F

eb1

98

4 -

Feb

19

85

- F

eb1

98

6 -

Feb

19

87

- F

eb1

98

8 -

Feb

19

89

- F

eb1

99

0 -

Feb

19

91

- F

eb1

99

2 -

Feb

19

93

- F

eb1

99

4 -

Feb

19

95

- F

eb1

99

6 -

Feb

19

97

- F

eb1

99

8 -

Feb

19

99

- F

eb2

00

0 -

Feb

20

01

- F

eb2

00

2 -

Feb

20

03

- F

eb2

00

4 -

Feb

20

05

- F

eb2

00

6 -

Feb

20

07

- F

eb2

00

8 -

Feb

20

09

- F

eb2

01

0 -

Feb

Federal Reserve Board’s Trade Weighted Exchange Value of $

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

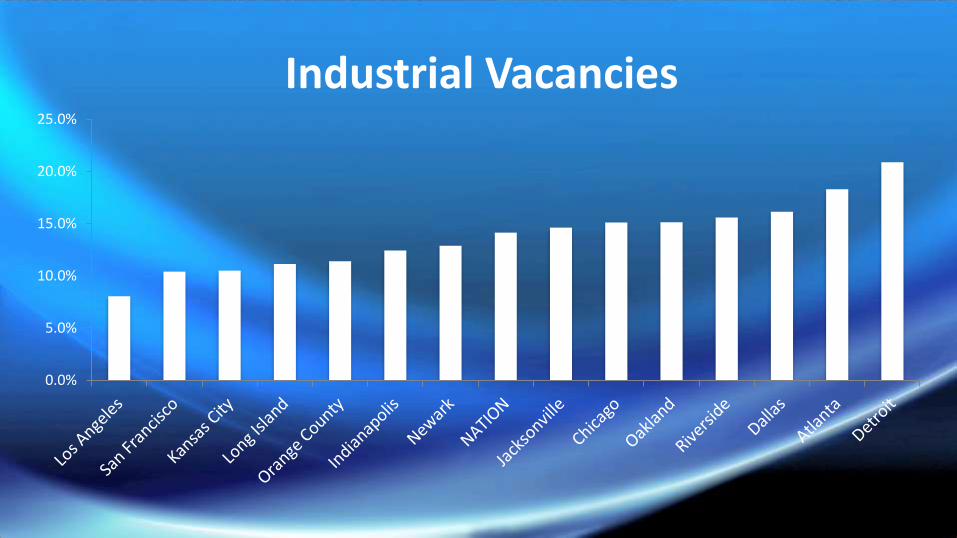

Industrial Vacancies

Source: NAR / CBRE-EA

11.0%

11.5%

12.0%

12.5%

13.0%

13.5%

-3000

-2000

-1000

0

1000

2000

3000

4000

2009.4 2010.1 2010.2 2010.3 2010.4 2011.1 2011.2

Per

cen

tage

(%

)

Squ

are

Feet

(0

00

's)

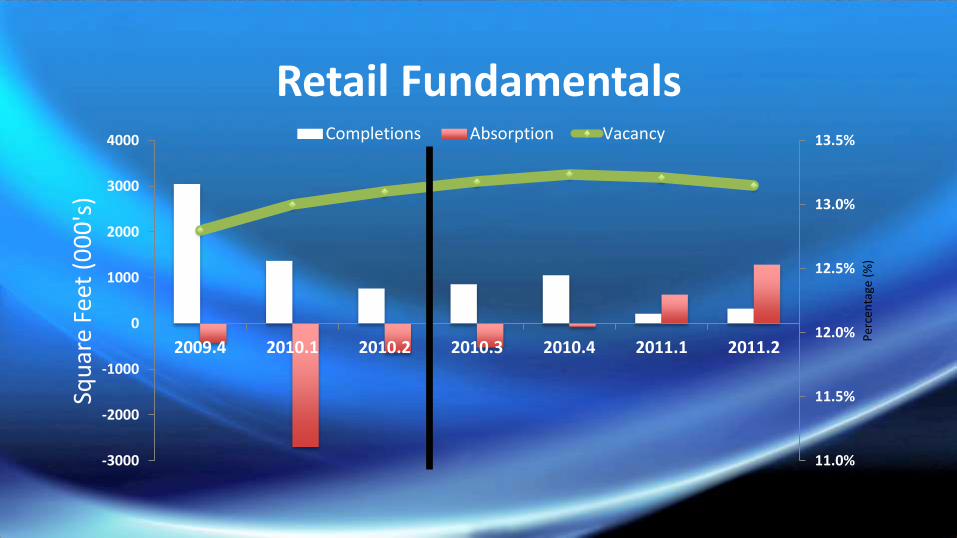

Retail FundamentalsCompletions Absorption Vacancy

Source: NAR / CBRE-EA

Retail Sales(Raw nominal dollar figures)

250000

270000

290000

310000

330000

350000

370000

3900002

00

0 -

Jan

20

00

- J

ul

20

01

- J

an

20

01

- J

ul

20

02

- J

an

20

02

- J

ul

20

03

- J

an

20

03

- J

ul

20

04

- J

an

20

04

- J

ul

20

05

- J

an

20

05

- J

ul

20

06

- J

an

20

06

- J

ul

20

07

- J

an

20

07

- J

ul

20

08

- J

an

20

08

- J

ul

20

09

- J

an

20

09

- J

ul

20

10

- J

an

20

10

- J

ul

$ million

Retail Sales (adjusted for inflation)

0.85

0.90

0.95

1.00

1.05

1.10

1.152

00

0 -

Jan

20

00

- J

un

20

00

- N

ov

20

01

- A

pr

20

01

- S

ep2

00

2 -

Feb

20

02

- J

ul

20

02

- D

ec2

00

3 -

May

20

03

- O

ct2

00

4 -

Mar

20

04

- A

ug

20

05

- J

an2

00

5 -

Ju

n2

00

5 -

No

v2

00

6 -

Ap

r2

00

6 -

Sep

20

07

- F

eb2

00

7 -

Ju

l2

00

7 -

Dec

20

08

- M

ay2

00

8 -

Oct

20

09

- M

ar2

00

9 -

Au

g2

01

0 -

Jan

20

10

- J

un

5% higher

From 2000

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Retail Vacancies

Source: NAR / CBRE-EA

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

-100000

-50000

0

50000

100000

150000

200000

2009.4 2010.1 2010.2 2010.3 2010.4 2011.1 2011.2

Per

cen

t (%

)

# o

f U

nit

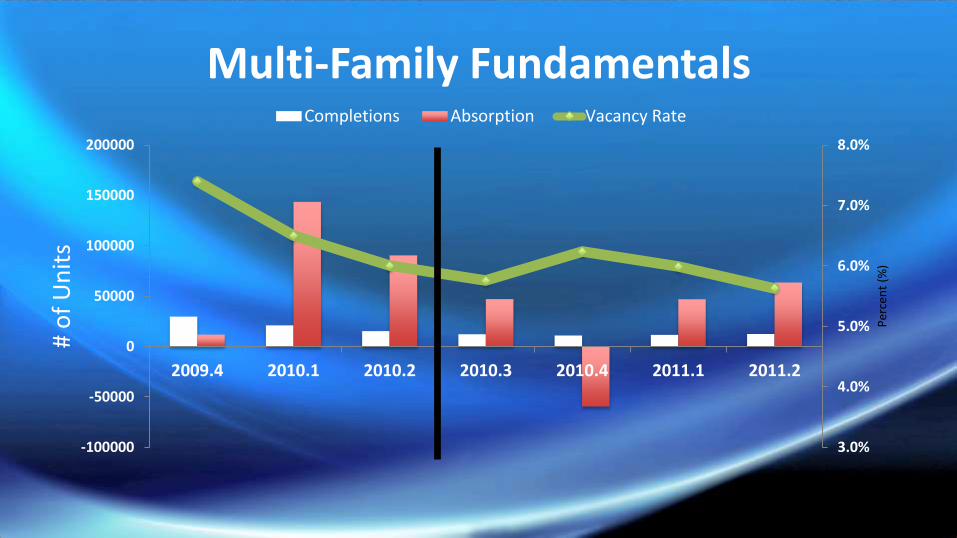

sMulti-Family Fundamentals

Completions Absorption Vacancy Rate

Source: NAR / CBRE-EA

Homeownership Rate

6061626364656667686970

19

80

- Q

1

19

81

- Q

2

19

82

- Q

3

19

83

- Q

4

19

85

- Q

1

19

86

- Q

2

19

87

- Q

3

19

88

- Q

4

19

90

- Q

1

19

91

- Q

2

19

92

- Q

3

19

93

- Q

4

19

95

- Q

1

19

96

- Q

2

19

97

- Q

3

19

98

- Q

4

20

00

- Q

1

20

01

- Q

2

20

02

- Q

3

20

03

- Q

4

20

05

- Q

1

20

06

- Q

2

20

07

- Q

3

20

08

- Q

4

20

10

- Q

1

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

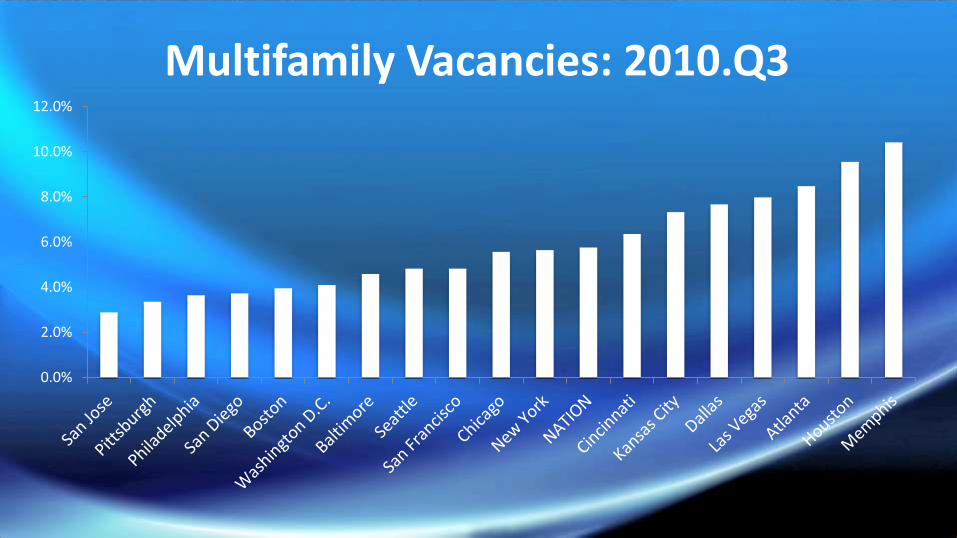

Multifamily Vacancies: 2010.Q3

Source: NAR / CBRE-EA

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

2009.1 2009.2 2009.3 2009.4 2010.1 2010.2 2010.3 2010.4 2011.1 2011.2

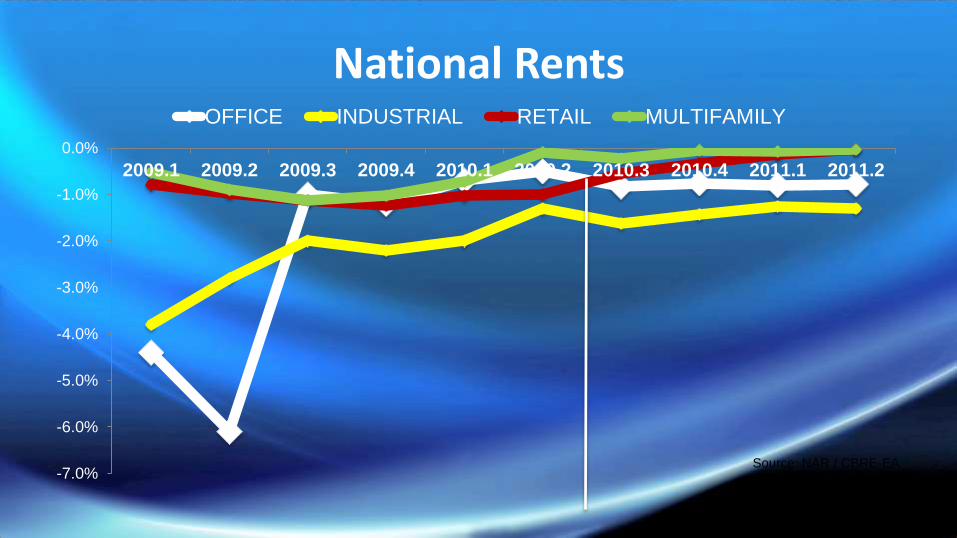

National RentsOFFICE INDUSTRIAL RETAIL MULTIFAMILY

Source: NAR / CBRE-EA

57%43%

Did you complete a commercial sales transaction?

Yes

No

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Current ChallengesOther

Pricing Gapbetween Buyersand SellersNationalEconomy

Local Economy

Financing

Distress

Source: NAR

REALTORS® Commercial Activity: 2010.Q2

0

20

40

60

80

100

120

140

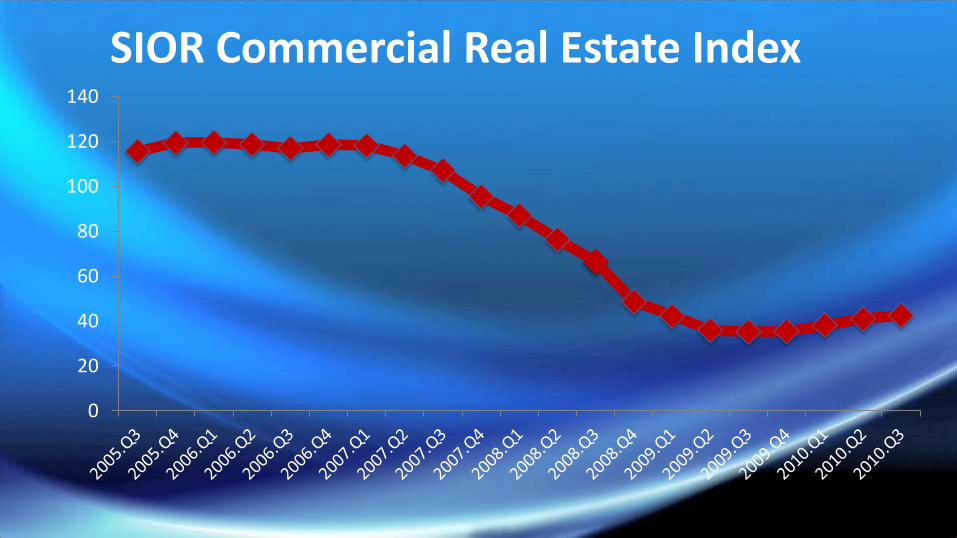

SIOR Commercial Real Estate Index

Source: SIOR, NAR

$0

$20

$40

$60

$80

$100

$120

$140

Bill

ion

s

U.S. Sales Volume: Properties valued over $2.5 million

Apartment Industrial Office Retail

Source: Real Capital Analytics

2010.Q3: UP 115% Y-o-Y

1%

2%

8%

13%

22%

54%

Over $10 M

Between $5 M and $10 M

$2 M and $5 M

Between $1 M and $2 M

Between $500K and $1 M

Under $500K

Dollar amount of last transaction

Source: NAR

REALTORS® Commercial Activity: 2010.Q2

REALTORS® Commercial Activity – 2010.Q2

Sales Volume Compared with Previous Year Down 16%

Sales Prices Compared with Previous Year Down 18%

Expected Inventory Availability for the Next 12 Months Up 13%

Rental Volume Compared with Previous Quarter Down 6%

Rental Rates Compared with Previous Quarter Down 10%

Level of Rent Concessions Compared with Previous Quarter Up 9%

Direction of Business Opportunities Compared with Previous

Quarter

Down 4%

5%

6%

7%

8%

9%

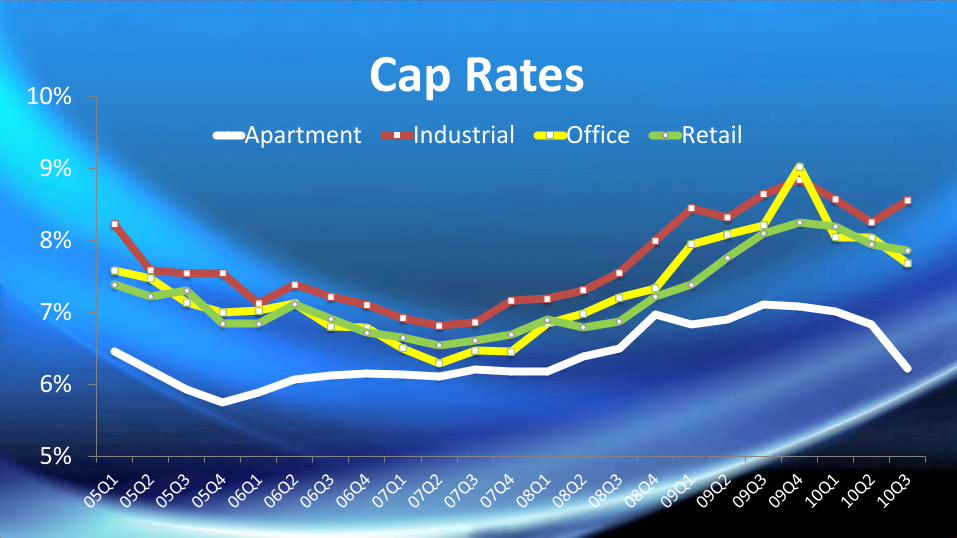

10% Cap RatesApartment Industrial Office Retail

Source: Real Capital Analytics

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

J'01

A J O J'02

A J O J'03

A J O J'04

A J O J'05

A J O J'06

A J O J'07

A J O J'08

A J O J'09

A J O J'10

A J

All Core Properties10-Year Treasury Avg Cap rate

Source: Real Capital Analytics

483489

10-Year Treasury impacted by Inflationary Expectations

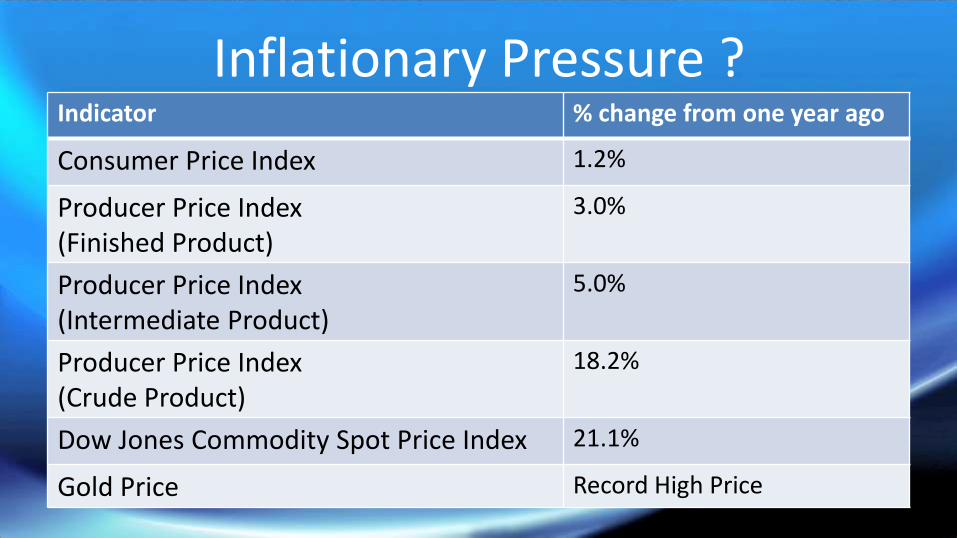

Inflationary Pressure ?Indicator % change from one year ago

Consumer Price Index 1.2%

Producer Price Index (Finished Product)

3.0%

Producer Price Index (Intermediate Product)

5.0%

Producer Price Index (Crude Product)

18.2%

Dow Jones Commodity Spot Price Index 21.1%

Gold Price Record High Price

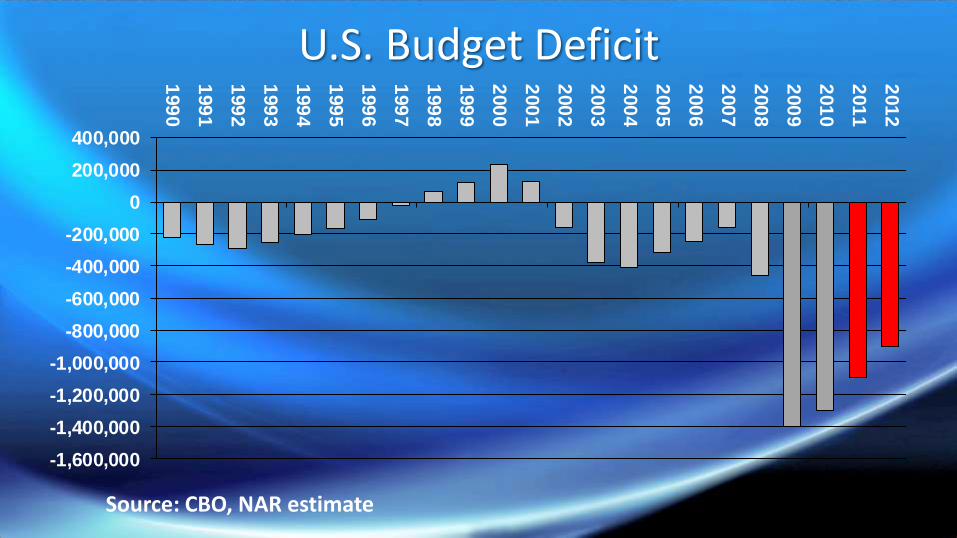

U.S. Budget Deficit

-1,600,000

-1,400,000

-1,200,000

-1,000,000

-800,000

-600,000

-400,000

-200,000

0

200,000

400,000

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

Source: CBO, NAR estimate

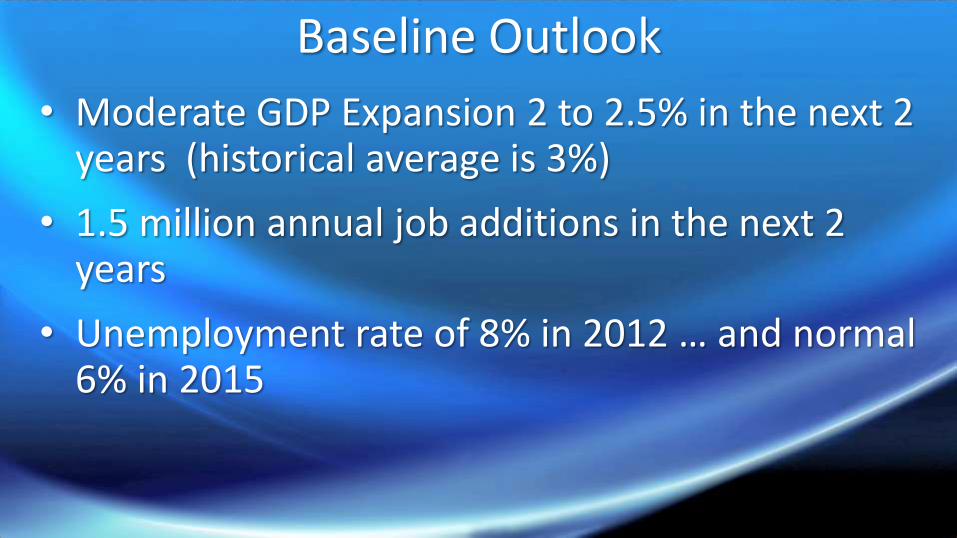

Baseline Outlook

• Moderate GDP Expansion 2 to 2.5% in the next 2 years (historical average is 3%)

• 1.5 million annual job additions in the next 2 years

• Unemployment rate of 8% in 2012 … and normal 6% in 2015

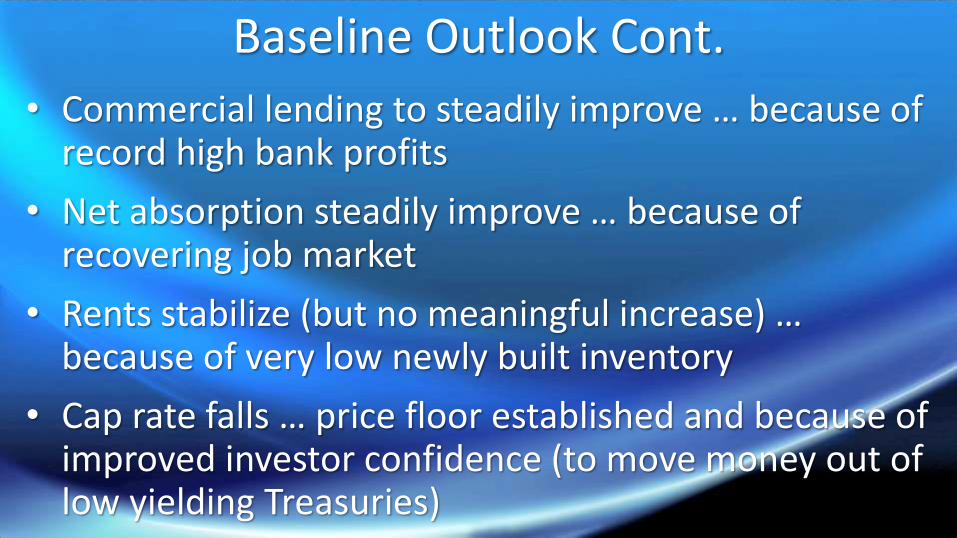

Baseline Outlook Cont.

• Commercial lending to steadily improve … because of record high bank profits

• Net absorption steadily improve … because of recovering job market

• Rents stabilize (but no meaningful increase) … because of very low newly built inventory

• Cap rate falls … price floor established and because of improved investor confidence (to move money out of low yielding Treasuries)

Alternative Outlooks• High inflation … people desire tangible investment like real estate, but

interest rate will be higher

• Deflation … investors hold back for better price … holds back economy

• Budget deficit tipping point … higher interest rate and sharp cut back in standard of living

• Sharp 4% to 5% GDP growth … business spending returns in line with profits … faster job creation … faster commercial market recovery