comm 324 --- w. suo slide 1. comm 324 --- w. suo slide 2 diversification random selection the...

TRANSCRIPT

Comm 324 --- W. SuoSlide 1Slide 1

Index ModelsIndex Models

Comm 324 --- W. SuoSlide 2Slide 2

Diversification

Random selection The effect of

diversification Markowitz diversification

What information are needed?

How to simplify the approach?

Comm 324 --- W. SuoSlide 3Slide 3

Linear Regression

Review Properties R-square Example

spreadsheet

Comm 324 --- W. SuoSlide 4Slide 4

Advantages: Reduces the number of inputs for diversification Easier for security analysts to specialize

Drawback: the simple dichotomy rules out important risk

sources (such as industry events)

The Single Index Model

Comm 324 --- W. SuoSlide 5Slide 5

ßi = index of a security’s particular return to the factor

F= some macro factor; in this case F is unanticipated movement; F is commonly related to security returns

Single Factor Model

( )i i i ir E r F e

Assumption: a broad market index like the S&P500 is the common factor

Comm 324 --- W. SuoSlide 6Slide 6

Single Index Model

ifMiifi e)rr()rr(

ai = stock’s expected return if market’s excess return is zero

bi(rM-ri) = the component of return due to market movements

ei = the component of return due to unexpected firm-specific events

Comm 324 --- W. SuoSlide 7Slide 7

Let: Ri = (ri - rf)

Rm = (rm - rf)

Risk premiumformat

Ri = αi + ßiRm + ei

Risk Premium Format

Comm 324 --- W. SuoSlide 8Slide 8

Market or systematic risk: risk related to the macro economic factor or market index

Unsystematic or firm specific risk: risk not related to the macro factor or market index

Total risk = Systematic + Unsystematic

Components of Risk

Comm 324 --- W. SuoSlide 9Slide 9

i2 = total variance

i2 m

2 = systematic variance

2(ei) = unsystematic variance

Measuring Components of Risk

2 2 2 2( )ii i M e

Comm 324 --- W. SuoSlide 10Slide 10

Total Risk = Systematic +Unsystematic

Examining Percentage of Variance

2

2M

2i2 squareR

2i

22 )e(

1

)e(22M

2

Comm 324 --- W. SuoSlide 11Slide 11

Security Characteristic Line

Excess Returns (i)SCL

..

..

.... ..

..

.. ..

.. .. ..

.. ..

..

.. ..

......

..

..

..

....

......

....

..

....

....

..

.. ..

..

.. ..

..

.. ...... ..

.. .... ..Excess returnson market index

Ri = i + ßiRm + ei

Comm 324 --- W. SuoSlide 12Slide 12

Index Model

Spreadsheet example

Comm 324 --- W. SuoSlide 13Slide 13

Index Model and Diversification

i i i M iR R e

No. of Securities

St. Deviation

Market Risk

Unique Risk

2(eP)=2(e) / n

P2M

2

Comm 324 --- W. SuoSlide 14Slide 14

Industry Prediction of Beta

BMO Nesbitt Burns and Merrill Lynch examples BMO NB uses returns not risk premiums a has a different interpretation: a + rf (1-b) Merill Lynch’s ‘adjusted b’

Forecasting beta as a function of past beta Forecasting beta as a function of firm size, growth,

leverage etc.

Comm 324 --- W. SuoSlide 15Slide 15

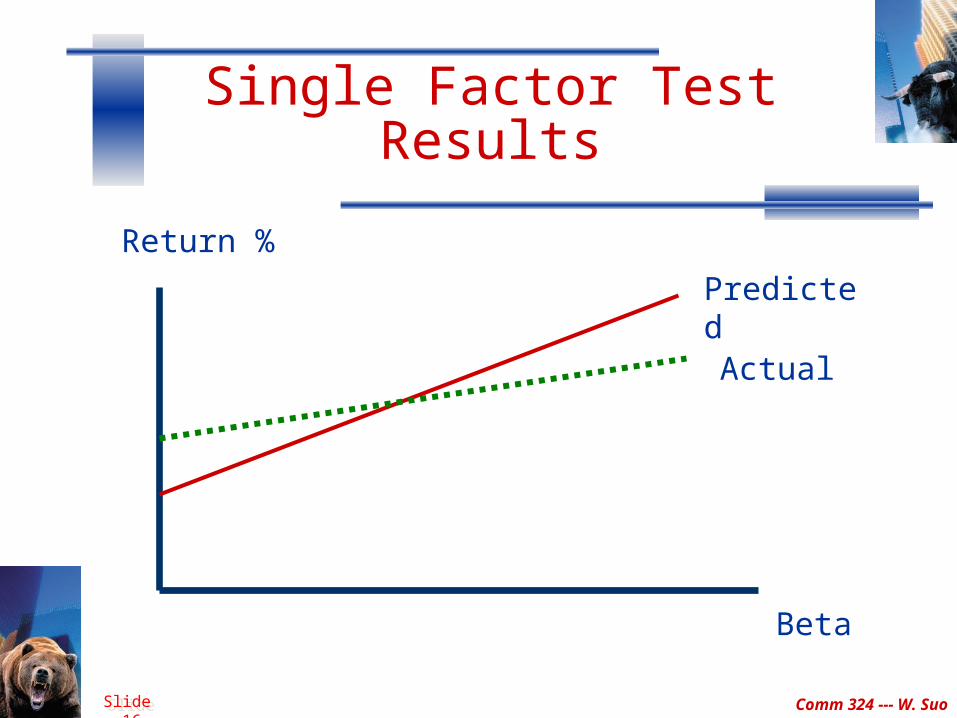

Tests of the Single Factor Model

Tests of the expected return beta relationship First Pass Regression

Estimate beta, average risk premiums and unsystematic risk

Second Pass: Using estimates from the first pass to determine if model is supported by the data

Most tests do not generally support the single factor model

Comm 324 --- W. SuoSlide 16Slide 16

Single Factor Test Results

Return %

Beta

Predicted

Actual

Comm 324 --- W. SuoSlide 17Slide 17

Roll’s Criticism on the Tests

The only testable hypothesis: the mean-variance efficiency of the market portfolio

All other implications are not independently testable

CAPM is not testable unless we use the true market portfolio

The benchmark error

Comm 324 --- W. SuoSlide 18Slide 18

Measurement Error in Beta

Statistical property: If beta is measured with error in the first stage, Second stage results will be biased in the direction

the tests have supported Test results could result from measurement error

Comm 324 --- W. SuoSlide 19Slide 19

Conclusions on the Tests’ Results

Tests proved that CAPM seems qualitatively correct Rates of return are linear and increase with beta Returns are not affected by nonsystematic risk

But they do not entirely validate its quantitative predictions The expected return-beta relationship is not fully consistent with

empirical observation.

Comm 324 --- W. SuoSlide 20Slide 20

Multifactor Models

Use factors in addition to market return Examples include industrial production, expected inflation

etc. Estimate a beta for each factor using multiple regression

Chen, Roll and Ross Returns a function of several macroeconomic and bond

market variables instead of market returns Fama and French

Returns a function of size and book-to-market value as well as market returns

Comm 324 --- W. SuoSlide 21Slide 21

Researchers’ Responses to Fama and French

Utilize better econometric techniques Improve estimates of beta Reconsider the theoretical sources and implications

of the Fama and French-type results Return to the single-index model, accounting for

non-traded assets and cyclical behavior of betas

Comm 324 --- W. SuoSlide 22Slide 22

Jaganathan and Wang Study (1996)

Included factors for cyclical behavior of betas and human capital

When these factors were included the results showed returns were a function of beta

Size is not an important factor when cyclical behavior and human capital are included