coca - center of creative arts3h0wk28l0121u1mlr3h2fw6j-wpengine.netdna-ssl.com/wp... · 2019. 4....

TRANSCRIPT

Report To Governance

for the year ended August 31, 2018

COCA - Center of Creative Arts

COCA - Center of Creative Arts

32For Board Of Directors, Finance Committee And Management Use Only

Page

Auditor Communications 1 - 7

Status Of Prior Year Recommendations 8

Financial Analysis 9 - 16

Data Analytics 17 - 18

Emerging Financial Reporting Issues 19 - 26

Impact Of The Tax Cuts And Jobs Act 27 - 28

Independent Auditors’ Report On Additional Information 29

Management Representation Letter Exhibit 1

Table Of Contents

COCA – Center of Creative Arts

1For Board Of Directors, Finance Committee And Management Use Only

Auditor Communications

Board of Directors and Finance CommitteeCOCA - Center of Creative ArtsSt. Louis, Missouri

We have audited the financial statements of COCA - Center of Creative Arts (COCA) for the year ended August 31,2018. Our audit was performed in accordance with auditing standards generally accepted in the United States ofAmerica. Those standards require that we plan and perform the audit to obtain reasonable assurance about whetherthe financial statements are free from material misstatement and presented in accordance with accounting principlesgenerally accepted in the United States of America. Our audit included examining, on a test basis, evidence supportingthe amounts and disclosures in the financial statements. We also assessed the accounting principles used by COCA andthe significant estimates made by COCA’s management, as well as evaluated the overall financial statementpresentation.

Audit standards require the auditor to ensure that those charged with corporate governance receive additionalinformation regarding the scope and results of the audit that may assist the governing body in overseeing the financialreporting and disclosure process for which management is responsible. The following section describes matters which arerequired to be reported to you.

This information is intended solely for the Board of Directors, Finance Committee and management of COCA, and is notintended to be, and should not be used by anyone other than those specified parties.

March 18, 2019

COCA – Center of Creative Arts

2For Board Of Directors, Finance Committee And Management Use Only

Auditor Communications (Continued)

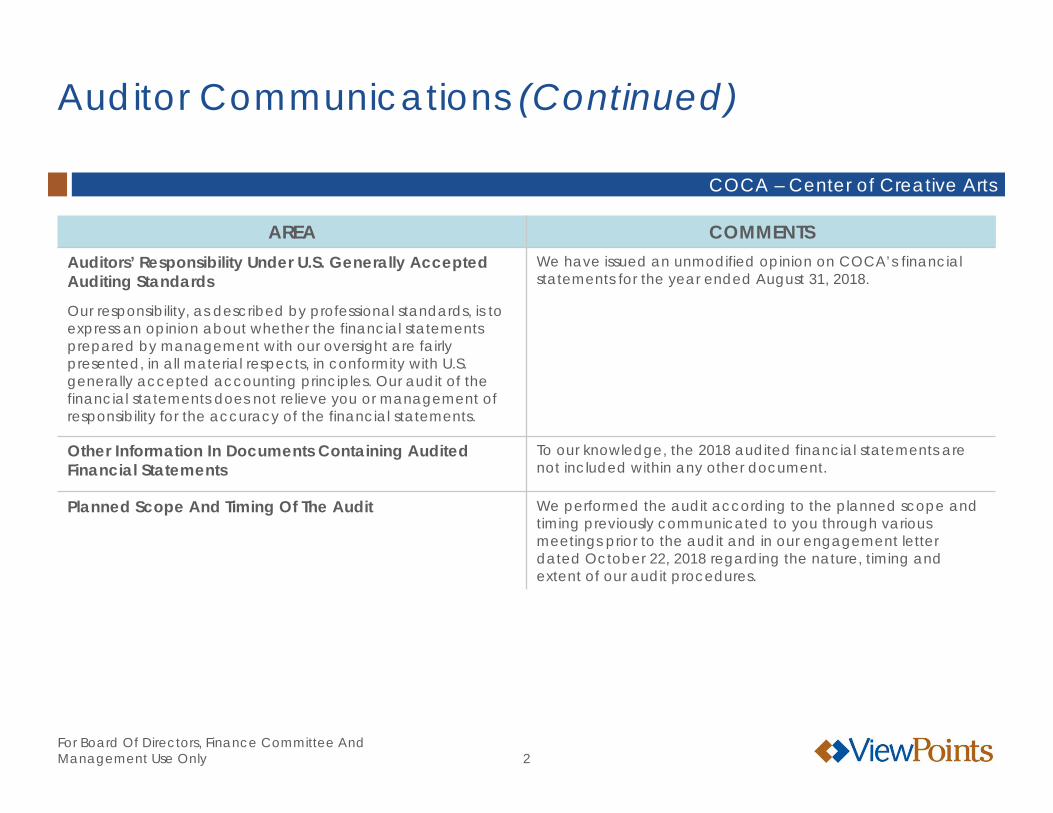

AREA COMMENTSAuditors’ Responsibility Under U.S. Generally Accepted Auditing Standards

Our responsibility, as described by professional standards, is to express an opinion about whether the financial statements prepared by management with our oversight are fairly presented, in all material respects, in conformity with U.S. generally accepted accounting principles. Our audit of the financial statements does not relieve you or management of responsibility for the accuracy of the financial statements.

We have issued an unmodified opinion on COCA’s financial statements for the year ended August 31, 2018.

Other Information In Documents Containing Audited Financial Statements

To our knowledge, the 2018 audited financial statements are not included within any other document.

Planned Scope And Timing Of The Audit We performed the audit according to the planned scope and timing previously communicated to you through various meetings prior to the audit and in our engagement letter dated October 22, 2018 regarding the nature, timing and extent of our audit procedures.

COCA – Center of Creative Arts

3For Board Of Directors, Finance Committee And Management Use Only

Auditor Communications (Continued)

AREA COMMENTSQualitative Aspects Of Accounting Practices

Management is responsible for the selection and use of appropriate accounting policies. In accordance with the terms of our engagement letter, we will advise management about appropriateness of accounting policies and their application.

Significant accounting policies are described in Note 1.

No new accounting policies were adopted in the current year and there were no changes in the application of existing accounting policies.

We noted no transactions entered into during the year for which there was a lack of authoritative guidance or consensus.

No significant transactions have been recognized in a different period than when the transactions occurred.

Management Judgments And Accounting EstimatesThe preparation of the financial statements requires the use of accounting estimates. Certain estimates are particularly sensitive due to their significance to the financial statements and the possibility that future events may differ significantly from management’s expectations.

Significant accounting estimates affecting the financial statements include:

Allowances for doubtful promises to give and accounts receivable are based on past collection history and a review of outstanding balances. Management estimates that an allowance of $365,000 is appropriate for promises to give. Management estimates that no allowance is necessary for accounts receivable.

Valuation of long-term promises to give is based on a 3% discount factor.

Functional expense allocations are based on periodic time and expense studies.

COCA – Center of Creative Arts

4For Board Of Directors, Finance Committee And Management Use Only

Auditor Communications (Continued)

AREA COMMENTSManagement Judgments And Accounting Estimates (Continued)

Depreciable lives used to calculate depreciation are based on the assets’ useful lives.

Impairment of excess construction costs is based on management’s estimate of the recoverability of these costs upon their eventual disposition.

We evaluated the key factors and assumptions used to develop the above estimates and determined they are reasonable in relation to the financial statements taken as a whole.

Financial Statement DisclosuresThe disclosures to the financial statements are neutral, consistent and clear. Certain financial statement disclosures are particularly sensitive because of their significance to the financial statements’ users.

The most sensitive disclosures affecting the financial statements are:

Uninsured cash in Note 1 discloses risks to COCA

Promises to give in Note 3 require management judgment to determine appropriate valuation

Capital commitments in Note 6 and lease commitments in Note 12 disclose future obligations of COCA

Subsequent event disclosure in Note 13 discloses a significant New Markets Tax Credit transaction completed by COCA

Difficulties Encountered In Performing The Audit We encountered no difficulties in dealing with management in performing and completing our audit.

COCA – Center of Creative Arts

5For Board Of Directors, Finance Committee And Management Use Only

Auditor Communications (Continued)

AREA COMMENTSCorrected And Uncorrected Misstatements

Professional standards require us to accumulate all factual, judgmental and projected misstatements identified during the audit, other than those that are trivial, communicate them to the appropriate level of management, and request their correction.

The following audit adjustments were recorded by management:

No uncorrected misstatements were noted.

Increase(Decrease) InNet Assets At

August 31, 2018To reverse write off of a promise to give subsequently

determined to not be from a donor-advised fund 500,000$ To adjust discount and allowance on long-term

promises to give (355,000) To record in-kind rent contribution of $63,500 — To recognize current year expense related to a multi-year

in-kind promise to give (24,623) To record donated security pledge payments of

approximately $404,000 and contribution of $645received but not liquidated as of year end 645

To adjust depreciation expense (30,240) To record impairment of excess construction costs (557,402) To accrue approximately $287,000 of construction in

progress costs at year end — To capitalize debt issuance costs 67,148

(399,472)$

COCA – Center of Creative Arts

6For Board Of Directors, Finance Committee And Management Use Only

Auditor Communications (Continued)

AREA COMMENTSDisagreements With ManagementProfessional standards define a disagreement with management as a financial accounting, reporting, or auditing matter, whether or not resolved to our satisfaction, that could be significant to the financial statements or the auditors’ report.

We are pleased to report that no disagreements arose during the course of our audit.

Management Representations Management representation letter received dated March 18, 2019, a copy of which is attached.

Management Consultations With Other Independent AccountantsIn some cases, management may decide to consult with other accountants about auditing and accounting matters, similar to obtaining a “second opinion” on certain situations. If a consultation involves application of an accounting principle to an organization’s financial statements or a determination of the type of auditors’ opinion that may be expressed on those statements, our professional standards require the consulting accountant to check with us to determine that the consultant has all the relevant facts.

To our knowledge, there were no such consultations with other accountants.

COCA – Center of Creative Arts

7For Board Of Directors, Finance Committee And Management Use Only

Auditor Communications (Continued)

AREA COMMENTSOther Audit Findings Or Issues We generally discuss a variety of matters, including the

application of accounting principles and auditing standards, with management each year prior to retention as the COCA’s auditors. However, these discussions occurred in the normal course of our professional relationship and our responses were not a condition to our retention.

COCA – Center of Creative Arts

8For Board Of Directors, Finance Committee And Management Use Only

Status Of Prior Year Recommendations

PRIOR YEAR RECOMMENDATIONS STATUS Given the unique elements of charitable giving

vehicles, additional consideration from the accounting department should be given to any donor commitments or gifts from donor-advised funds, and/or community foundations, especially from a donor acknowledgement perspective.

The development department is identifying within the development software any gifts or pledges from donor-advised funds or community foundations and communicating to the accounting department to ensure proper recognition.

Periodic review of the Executive Director’s credit card transactions and expense reports should be performed by a member of the Board or Finance Committee.

Management will evaluate implementation in the upcoming year.

COCA – Center of Creative Arts

9For Board Of Directors, Finance Committee And Management Use Only

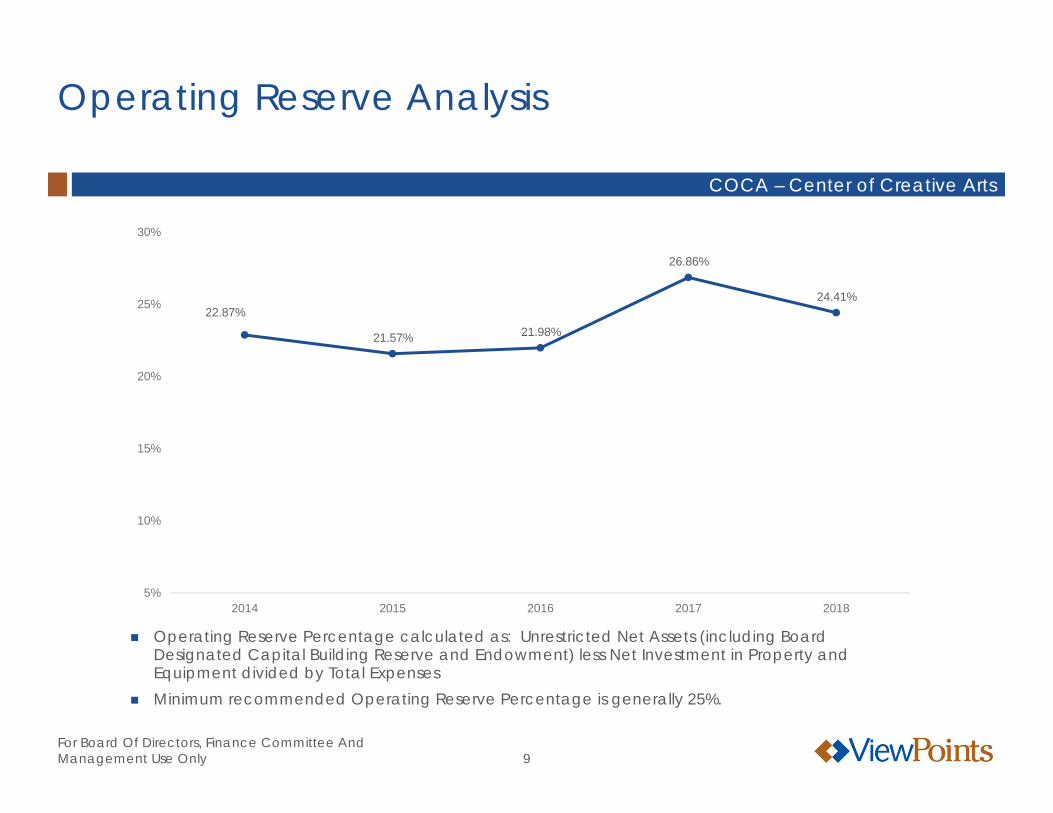

Operating Reserve Percentage calculated as: Unrestricted Net Assets (including Board Designated Capital Building Reserve and Endowment) less Net Investment in Property and Equipment divided by Total Expenses

Minimum recommended Operating Reserve Percentage is generally 25%.

Operating Reserve Analysis

22.87%

21.57% 21.98%

26.86%

24.41%

5%

10%

15%

20%

25%

30%

2014 2015 2016 2017 2018

COCA – Center of Creative Arts

10For Board Of Directors, Finance Committee And Management Use Only

Composition Of Support, Revenue And Gains

$2,244,368

$6,052,441

$664,256$217,429

$2,208,953

$7,980,963

$596,616 $387,301

$2,395,806

$13,616,218

$593,550 $410,857

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

Program Revenues Contributions Fundraising Events Investments and Other

2016 2017 2018

COCA – Center of Creative Arts

11For Board Of Directors, Finance Committee And Management Use Only

Percentage Of Program

Expenses Fund

ed By Program

RevenueProgram Revenues As A Percentage Of Program Expenses

$2,158,560 $2,147,134 $2,244,368 $2,208,953 $2,395,806

$3,589,358 $3,550,230 $3,759,032 $3,807,527

$4,200,211

60.1% 60.5% 59.7%58.0% 57.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

$-

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

2014 2015 2016 2017 2018

Program Revenue Program Expenses % Covered

COCA – Center of Creative Arts

12For Board Of Directors, Finance Committee And Management Use Only

Revenues And Expenses By Program

$964,435$677,318

$182,670 $245,209 $139,321

$1,523,809

$723,331$515,306

$754,366

$290,715

63.3%

93.6%

35.4% 32.5%47.9%

$0

$600,000

$1,200,000

$1,800,000

$2,400,000

Education Camps COCAedu Productions and Exhibits COCAbiz

2017

Program Revenues Program Expenses % Expenses Covered By Revenues

$993,963$755,218

$190,330 $266,024 $190,271

$1,658,500

$775,232$557,299

$875,981

$333,199

59.9%

97.4%

34.2% 30.4%

57.1%

—

600,000

1,200,000

1,800,000

2,400,000

Education Camps COCAedu Productions and Exhibits COCAbiz

2018

Program Revenues Program Expenses % Expenses Covered By Revenues

COCA – Center of Creative Arts

13For Board Of Directors, Finance Committee And Management Use Only

Functional Expense Allocations

$3,807,52764.8%

$1,213,59420.7%

$854,14014.5%

2017 = $5,875,261

Program Expenses Fundraising Expenses Management And General

$4,200,21165.2%

$1,336,51520.7%

$910,25414.1%

2018 = $6,446,980

COCA – Center of Creative Arts

14For Board Of Directors, Finance Committee And Management Use Only

Create Our Future Campaign expenses were $666,946 and $498,592 in 2018 and 2017, respectively.

Functional Expense Allocations (Excluding Create Our Future Campaign Expenses)

$3,807,52770.8%

$715,00213.3%

$854,14015.9%

2017 = $5,376,669

Program Expenses Fundraising Expenses Management And General

$4,200,21172.7%

$669,56911.6%

$910,25415.7%

2018 = $5,780,034

COCA - Center of Creative Arts

15For Board Of Directors, Finance Committee And Management Use Only

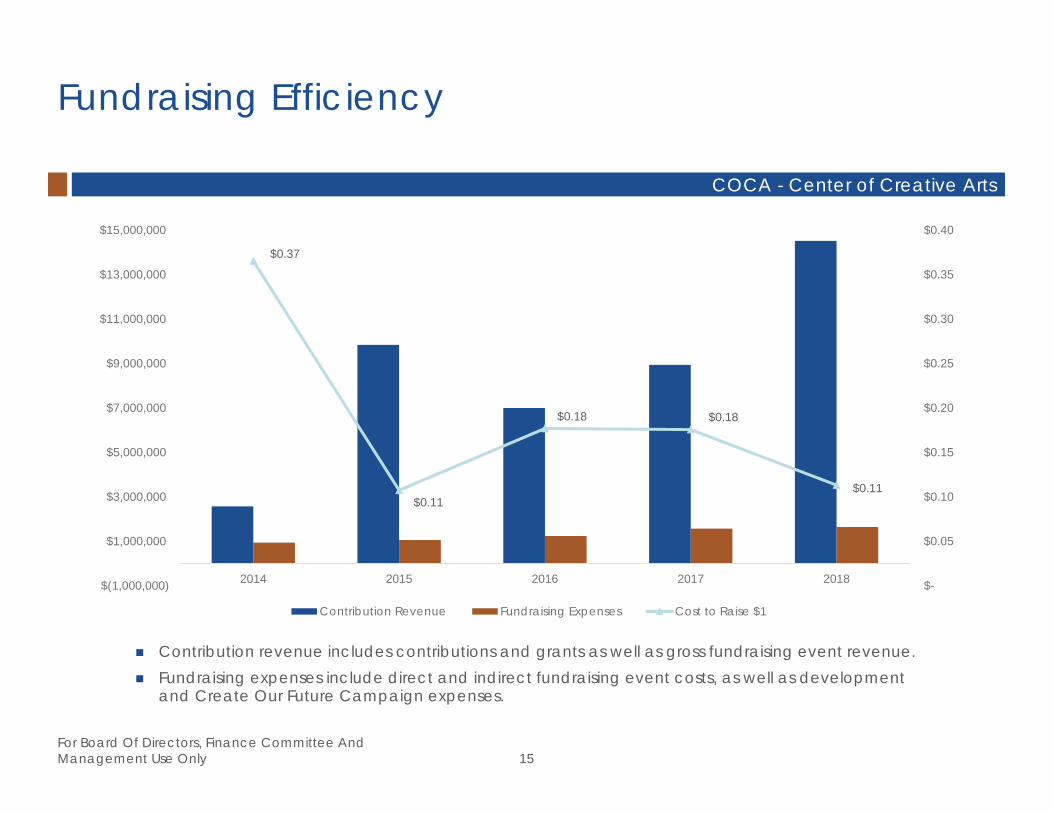

Contribution revenue includes contributions and grants as well as gross fundraising event revenue. Fundraising expenses include direct and indirect fundraising event costs, as well as development

and Create Our Future Campaign expenses.

Fundraising Efficiency

$0.37

$0.11

$0.18 $0.18

$0.11

$-

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$(1,000,000)

$1,000,000

$3,000,000

$5,000,000

$7,000,000

$9,000,000

$11,000,000

$13,000,000

$15,000,000

2014 2015 2016 2017 2018

Contribution Revenue Fundraising Expenses Cost to Raise $1

COCA - Center of Creative Arts

16For Board Of Directors, Finance Committee And Management Use Only

AMOUNT DESCRIPTION

$29,260,285 Create Our Future Campaign Contributions included in the Financial Statements(FY’15 - $8,000,000 + FY’16 - $4,188,000 + FY’17 - $5,986,531 + FY’18 - $11,085,754)

95,916 Endowment Contributions included in the Financial Statements(FY’16 - $4,545 + FY’17 - $55,566 + FY’18 - $35,805)

500,000 Neighborhood Assistance Program Contributions

1,140,679 Additional Contributions Received from September 1 through December 31, 2018

9,110,000 Planned Gifts

1,830,000 Unrecorded Commitments from Donor-Advised Funds and Community Foundations

461,250 Verbal Commitments with Pending Paperwork

$42,398,130 Total Create Our Future Campaign Gifts

Create Our Future Campaign Reconciliation As Of December 31, 2018

COCA - Center of Creative Arts

17For Board Of Directors, Finance Committee And Management Use Only

Data Analysis: Summary Of Procedures

RubinBrown performed the following analysis during the audit:

Benford’s Law Analysis on disbursements from September 1, 2017 through August 31, 2018 to see if the pattern ofdisbursements is as expected.

Analyzed top vendors based on total payments made to those vendors during the fiscal year through August 31, 2018(see results on page 18)

Identified potential duplicate amounts to a single vendor

Identified gaps in the check sequence

Performed journal entry testing utilizing the complete general ledger detail

COCA - Center of Creative Arts

18For Board Of Directors, Finance Committee And Management Use Only

Top 10 Vendors

VENDOR2018

AMOUNT2017

AMOUNT PURPOSE

S.M. Wilson $2,647,090 Construction Services (Renovations)

Christner $1,424,254 $640,383 Architectural Services

C. Rallo $273,866 $82,138 Construction Services (Elevator and Courtyard)

Christian Fine Cabinetry $150,182 Cabinetry (Kitchen Remodel)

Acropolis $149,521 $121,413 Technology Services

Butler's Pantry $134,486 Catering for Fundraising Events

Anthem $123,514 $130,835 Health Insurance

Ameren $116,800 $105,648 Utilities

Ritz-Carlton $102,214 COCACabana Event Site

Clean-Tech $87,552 $87,552 Janitorial Services

AALCO $63,740 Demolition

Bussmann $54,346 Marketing Services for Create Our Future Campaign

Thompson Coburn $52,673 Legal Services

Cincinnati Insurance $44,460 Insurance

Emerging Financial Reporting Issues

COCA - Center of Creative Arts

20For Board Of Directors, Finance Committee And Management Use Only

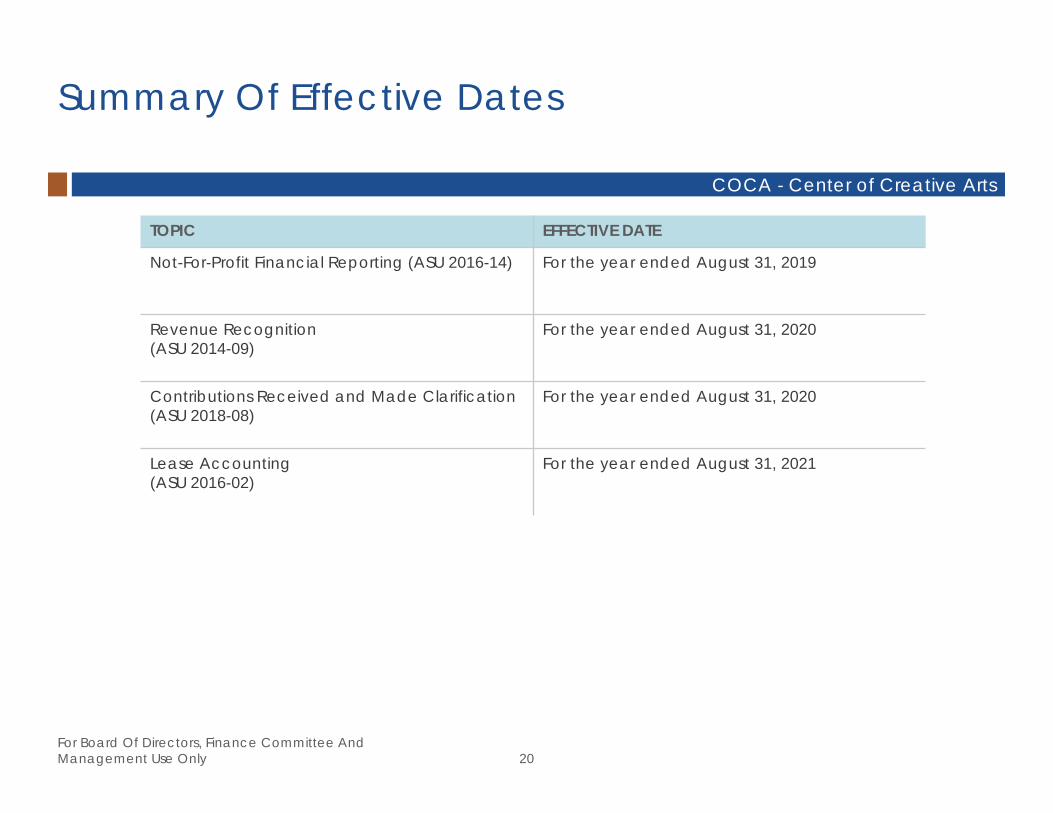

Summary Of Effective Dates

TOPIC EFFECTIVE DATE

Not-For-Profit Financial Reporting (ASU 2016-14) For the year ended August 31, 2019

Revenue Recognition(ASU 2014-09)

For the year ended August 31, 2020

Contributions Received and Made Clarification (ASU 2018-08)

For the year ended August 31, 2020

Lease Accounting(ASU 2016-02)

For the year ended August 31, 2021

COCA - Center of Creative Arts

21For Board Of Directors, Finance Committee And Management Use Only

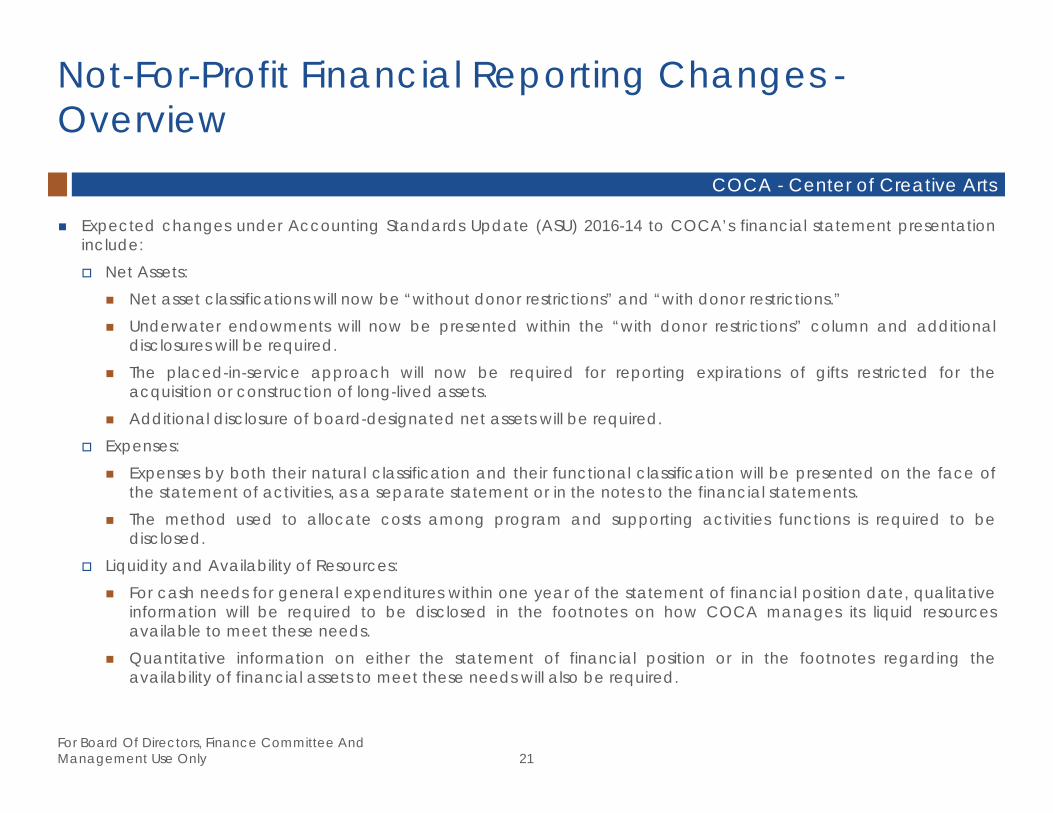

Not-For-Profit Financial Reporting Changes -Overview

Expected changes under Accounting Standards Update (ASU) 2016-14 to COCA’s financial statement presentationinclude: Net Assets:

Net asset classifications will now be “without donor restrictions” and “with donor restrictions.” Underwater endowments will now be presented within the “with donor restrictions” column and additional

disclosures will be required. The placed-in-service approach will now be required for reporting expirations of gifts restricted for the

acquisition or construction of long-lived assets. Additional disclosure of board-designated net assets will be required.

Expenses: Expenses by both their natural classification and their functional classification will be presented on the face of

the statement of activities, as a separate statement or in the notes to the financial statements. The method used to allocate costs among program and supporting activities functions is required to be

disclosed. Liquidity and Availability of Resources:

For cash needs for general expenditures within one year of the statement of financial position date, qualitativeinformation will be required to be disclosed in the footnotes on how COCA manages its liquid resourcesavailable to meet these needs.

Quantitative information on either the statement of financial position or in the footnotes regarding theavailability of financial assets to meet these needs will also be required.

COCA - Center of Creative Arts

22For Board Of Directors, Finance Committee And Management Use Only

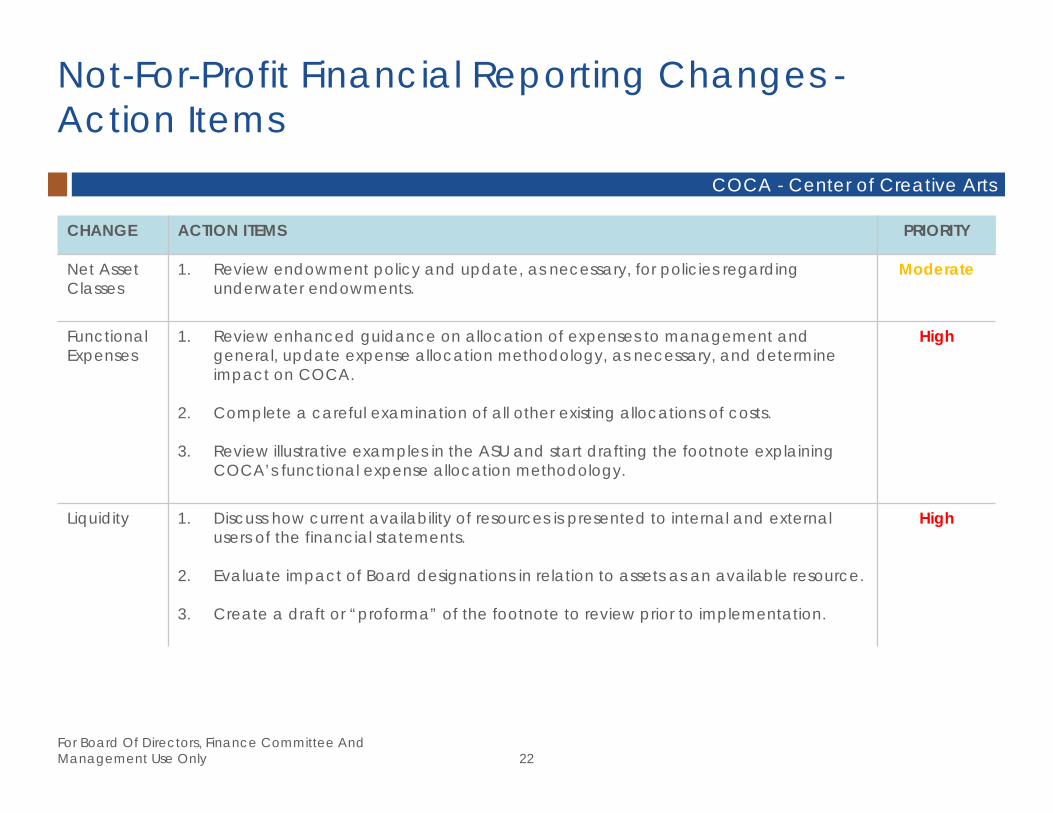

Not-For-Profit Financial Reporting Changes -Action Items

CHANGE ACTION ITEMS PRIORITY

Net Asset Classes

1. Review endowment policy and update, as necessary, for policies regarding underwater endowments.

Moderate

Functional Expenses

1. Review enhanced guidance on allocation of expenses to management and general, update expense allocation methodology, as necessary, and determine impact on COCA.

2. Complete a careful examination of all other existing allocations of costs.

3. Review illustrative examples in the ASU and start drafting the footnote explaining COCA’s functional expense allocation methodology.

High

Liquidity 1. Discuss how current availability of resources is presented to internal and external users of the financial statements.

2. Evaluate impact of Board designations in relation to assets as an available resource.

3. Create a draft or “proforma” of the footnote to review prior to implementation.

High

COCA - Center of Creative Arts

23For Board Of Directors, Finance Committee And Management Use Only

Revenue Recognition - Overview

Contributions are specifically excluded from this ASU but this will apply to COCA’s transactions with customers such as: Education, camps, COCAedu, productions and exhibits, and COCAbiz revenue Certain fundraising event revenue

Revenue recognition for transactions would be reviewed to: Identify the contract(s) with the customer Identify the performance obligation Determine the transaction price Allocate the transaction price Recognize revenue when (or as) a performance obligation is satisfied

AICPA Revenue Recognition Task Forces, which included the AICPA, NACUBO, preparers and auditors, reviewedissues with the Financial Reporting Executive Committee (FinREC) and developed implementation guidance in theAICPA Guide Revenue Recognition. This guidance includes the following type of transactions which may be useful toCOCA: Bifurcation of transactions between contributions and exchange transactions (for fundraising event revenue) Tuition and housing revenue as well as subscriptions and membership dues (for program revenue)

COCA - Center of Creative Arts

24For Board Of Directors, Finance Committee And Management Use Only

Revenue Recognition - Action Items

CATEGORY ACTION ITEMS PRIORITY

General Assign and train an internal champion for this effort. High

Education, Camps, COCAedu, Productions and Exhibits, and COCAbiz Revenue as well as Certain Fundraising Event Revenue

Create an inventory of all revenue streams, with a focus on the following: Duration of the contract Timing of payments and services provided

High

COCA - Center of Creative Arts

25For Board Of Directors, Finance Committee And Management Use Only

Contributions Received And Made Clarification -Overview

Provides guidance on: Characterizing grants and similar contracts with government agencies and others as reciprocal transactions

(exchange transactions) or nonreciprocal transactions (contributions) Additional considerations added to evaluate whether the resource provider is receiving commensurate value Expectation is this will result in more government agency funding being accounted for as conditional

contributions Determining whether a contribution is conditional or unconditional

The definition of conditional has been revised such that a contribution is conditional if: A barrier must be overcome AND There is a right of return of assets transferred or a right of release of promisor’s obligation to transfer assets

Effective Dates For resource recipients, this is effective for calendar year end 2019 and fiscal year end 2020 For resource providers, this is effective for calendar year end 2020 and fiscal year end 2021 Early adoption is permitted

COCA - Center of Creative Arts

26For Board Of Directors, Finance Committee And Management Use Only

Right-of-use assetLease liability

Amortization expense

Interest expense

Cash paid for principal and

interest payments

Right-of-use assetLease liability

Single lease expense on a

straight-line basis

Cash paid for lease payments

Financing (Type A)

Statement of Financial Position

Operating (Type B)

Statement of Cash FlowsStatement of Activities

All leases greater than 12 months shall be classified as: Type A (Financing) - if the term of the lease is for a major part of the remaining economic life of the underlying

asset (such as leases for equipment, vehicles, etc.) Type B (Operating) - lease of property (such as land, all/part of a building, etc.)

Effective for public companies (including not-for-profit organizations with publicly traded or conduit debt) for annual and interim periods beginning after December 15, 2018 and for all other entities for annual periods beginning after December 15, 2019; however, early adoption is permitted

Lease Accounting - Overview

COCA - Center of Creative Arts

27For Board Of Directors, Finance Committee And Management Use Only

Impact Of The Tax Cuts And Jobs Act

Direct Impact Unrelated Business Income (UBI)

Separate determination of UBI for each trade and business – losses from one trade or business cannot offsetincome from another trade or business

Now includes the cost of certain fringe benefits that are not included in the taxable income of employees such astransportation, parking, and athletic facilities

Change in corporate income tax rates Change in federal income tax withholding tables Additional taxable benefits to employees:

Moving expenses paid by COCA Employee achievement awards

21% excise tax (paid by COCA) for compensation to certain individuals of more than $1,000,000 per employee, peryear, or separation payments in excess of 3 times average salary for the 5 years prior to separation (can apply topayments less than $1 million)

COCA - Center of Creative Arts

28For Board Of Directors, Finance Committee And Management Use Only

Impact Of The Tax Cuts And Jobs Act (Continued)

Indirect Impact Effect of the increased standard deduction on charitable giving

Potential organizational responses: Educate donors on charitable giving options such as:

Charitable donation “bundling” (donors contributing every 2 – 3 years, instead of each year) Use of donor advised funds Use of direct contributions from IRAs for donors over the age of 70 ½

Emphasis on mission-based giving Elimination and limitation, respectively, of entertainment and meals business deductions could lead to requests to

bifurcate the fair value of meals versus entertainment for special events – if attendees determine the meal portion ofan event is a “business” expense and not entertainment, 50% of the fair value could be deductible as a businessexpense

COCA - Center of Creative Arts

29For Board Of Directors, Finance Committee And Management Use Only

Independent Auditors’ Report On Additional Information

Board of DirectorsCOCA - Center of Creative ArtsSt. Louis, Missouri

Our report on our audit of the financial statements of COCA - Center of Creative Arts (COCA) as of August 31, 2018appears in the financial statements of the COCA. That audit was conducted for the purpose of forming an opinion onthe financial statements taken as a whole. The additional information presented on pages 8 through 28 is presented forpurposes of additional analysis and is not a required part of the financial statements. Such information has not beensubjected to the auditing procedures applied in the audit of the financial statements and, accordingly, we express noopinion on it.

March 18, 2019

Exhibit 1Management Representation Letter