closing the loop in 2019 - euler hermes · 1995-1996 (president bill clinton): december 5, 1995, to...

TRANSCRIPT

© Copyright Allianz

Economic Research Department

Global Economic Outlook

Q4 2018

CLOSING THE LOOP IN 2019

© Copyright Allianz

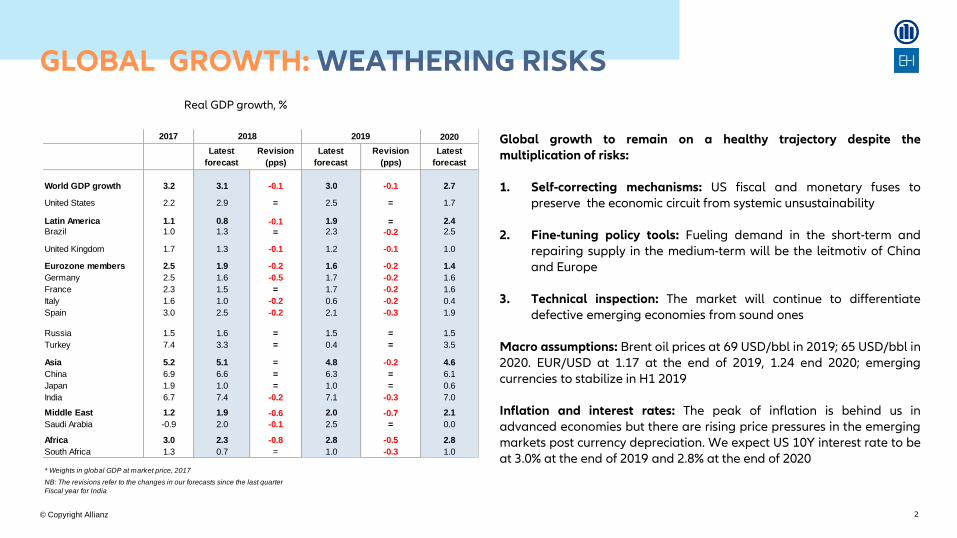

GLOBAL GROWTH: WEATHERING RISKS

Global growth to remain on a healthy trajectory despite the multiplication of risks:

1. Self-correcting mechanisms: US fiscal and monetary fuses to

preserve the economic circuit from systemic unsustainability

2. Fine-tuning policy tools: Fueling demand in the short-term and repairing supply in the medium-term will be the leitmotiv of China and Europe

3. Technical inspection: The market will continue to differentiate defective emerging economies from sound ones

Macro assumptions: Brent oil prices at 69 USD/bbl in 2019; 65 USD/bbl in 2020. EUR/USD at 1.17 at the end of 2019, 1.24 end 2020; emerging currencies to stabilize in H1 2019 Inflation and interest rates: The peak of inflation is behind us in advanced economies but there are rising price pressures in the emerging markets post currency depreciation. We expect US 10Y interest rate to be at 3.0% at the end of 2019 and 2.8% at the end of 2020

Real GDP growth, %

2

2020

Latest

forecast

Revision

(pps)

Latest

forecast

Revision

(pps)

Latest

forecast

World GDP growth 3.2 3.1 -0.1 3.0 -0.1 2.7

United States 2.2 2.9 = 2.5 = 1.7

Latin America 1.1 0.8 -0.1 1.9 = 2.4

Brazil 1.0 1.3 = 2.3 -0.2 2.5

United Kingdom 1.7 1.3 -0.1 1.2 -0.1 1.0

Eurozone members 2.5 1.9 -0.2 1.6 -0.2 1.4

Germany 2.5 1.6 -0.5 1.7 -0.2 1.6

France 2.3 1.5 = 1.7 -0.2 1.6

Italy 1.6 1.0 -0.2 0.6 -0.2 0.4

Spain 3.0 2.5 -0.2 2.1 -0.3 1.9

Russia 1.5 1.6 = 1.5 = 1.5

Turkey 7.4 3.3 = 0.4 = 3.5

Asia 5.2 5.1 = 4.8 -0.2 4.6

China 6.9 6.6 = 6.3 = 6.1

Japan 1.9 1.0 = 1.0 = 0.6

India 6.7 7.4 -0.2 7.1 -0.3 7.0

Middle East 1.2 1.9 -0.6 2.0 -0.7 2.1

Saudi Arabia -0.9 2.0 -0.1 2.5 = 0.0

Africa 3.0 2.3 -0.8 2.8 -0.5 2.8

South Africa 1.3 0.7 = 1.0 -0.3 1.0

* Weights in global GDP at market price, 2017

NB: The revisions refer to the changes in our forecasts since the last quarter

Fiscal year for India

2017 2018 2019

© Copyright Allianz 17-Dec-18 File name | department | author

3

Low impact, medium probability

•No-deal Brexit

Moderate impact, medium probability

•Escalating US-China trade tensions

•US corporate debt crisis

•Monetary policy mistake (boom/bust)

•Full-fledged EM crisis

•Populist win EU elections

High impact, low probability

•Global trade war

•Italexit/EZ debt crisis 2.0

•Capital markets freeze in China

•US systemic debt crisis

Pro

ba

bil

ity

Imp

act

The political and economic risk landscape remains crowded with potential recession triggers. Uncertainty is unlikely to escalate further, but expect it to linger. Visible impact could still increase as the negative effect kicks in with a lag

Hig

h

Lo

w

Hig

h

Lo

w

GLOBAL RISKS: MULTIPLE PERTURBATIONS IN 2019-20

The multiplication of uncertainty sources has contributed, beside the normalization of monetary policies in developed markets, to a significant tightening of world credit conditions, pointing toward a deceleration of growth

-80

-60

-40

-20

0

20

40

60

80

07 08 09 10 11 12 13 14 15 16 17 18

EM United Kingdom

China Japan

United States Euro Area

FCI

Tightening

Easing

World monetary and financial conditions (level)

3

Sources: IHS Global Insight. Allianz Research

© Copyright Allianz

Sources: IHS Global Insight. Allianz Research

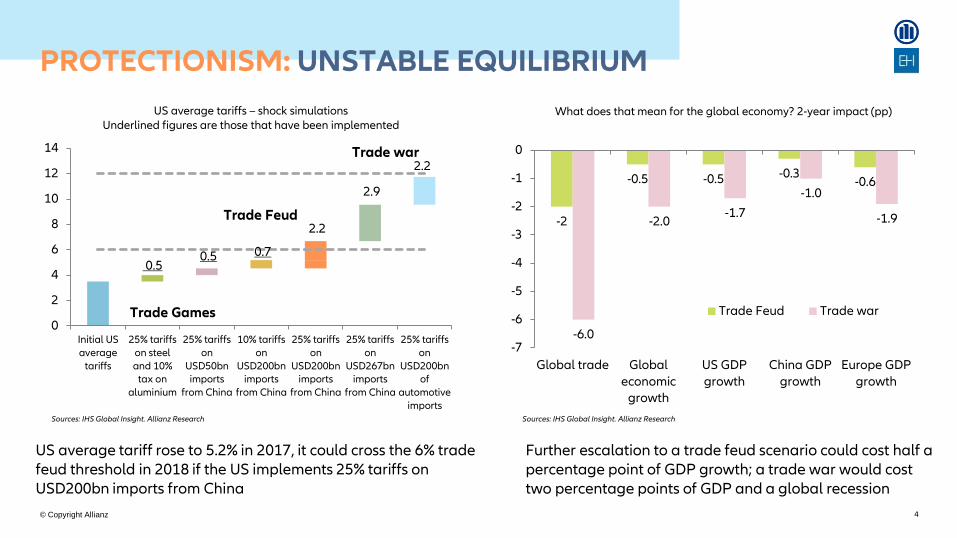

US average tariffs – shock simulations Underlined figures are those that have been implemented

US average tariff rose to 5.2% in 2017, it could cross the 6% trade feud threshold in 2018 if the US implements 25% tariffs on USD200bn imports from China

0.5 0.5 0.7

2.2

2.9

2.2

0

2

4

6

8

10

12

14

Initial USaverage

tariffs

25% tariffson steeland 10%

tax onaluminium

25% tariffson

USD50bnimports

from China

10% tariffson

USD200bnimports

from China

25% tariffson

USD200bnimports

from China

25% tariffson

USD267bnimports

from China

25% tariffson

USD200bnof

automotiveimports

Trade Feud

Trade Games

Trade war

-2

-0.5 -0.5 -0.3 -0.6

-6.0

-2.0 -1.7

-1.0

-1.9

-7

-6

-5

-4

-3

-2

-1

0

Global trade Global

economicgrowth

US GDP

growth

China GDP

growth

Europe GDP

growth

Trade Feud Trade war

What does that mean for the global economy? 2-year impact (pp)

Further escalation to a trade feud scenario could cost half a percentage point of GDP growth; a trade war would cost two percentage points of GDP and a global recession

Sources: IHS Global Insight. Allianz Research

PROTECTIONISM: UNSTABLE EQUILIBRIUM

4

© Copyright Allianz

Global trade in goods and services

Sources: IHS, Datastream, Allianz Research Source: Euler Hermes

Additional import needs by country in 2019 (Goods & Services, in USD bn)

3.6% 3.8%2.8% 2.1%

4.8% 3.8% 3.6%2.8%

2.1%

-10.2%

-1.6%

9.4%

7.2%6.3%

-15%

-10%

-5%

0%

5%

10%

15%

13 14 15 16 17 18f 19f

Volume Price Value

FDI inward stock vs. trade in goods and Services (growth average over 2014-2017)

Source: Euler Hermes

Global trade growth to slow in line with global demand

The US, the Eurozone and increasingly also China will act as a key driver for trade growth in the short-run

China

Indonesia

Philippines

Malaysia

Vietnam

Bangladesh

Poland

Romania

Russia

Brazil Colombia

Mexico

Morocco

Cambodia

India

Pakistan

Nigeria

Thailand

Côte d'Ivoire

Chile

United States

Argentina

Canada

France

Germany

Japan

Turkey

United Kingdom

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-5% 0% 5% 10% 15% 20%

Tra

de o

f g

oo

ds a

nd

se

rvic

es

FDI inward stock

Trade diversion has already started and could disrupt supply chains. Asian pivot stands to benefit the most

GLOBAL TRADE: LOOKING FOR A NEW EQUILIBRIUM

5

© Copyright Allianz 6

GLOBAL INSOLVENCIES: ON THE UPSIDE Insolvency Heat Map 2019

EH Global and Regional Insolvency Indices (yearly changes in %)

Sources: National statistics, Euler Hermes, Allianz Research Sources: IHS Global Insight. Allianz Research

We expect our Global Insolvency Index to keep on increasing in 2019 (+6% after +10% in 2018). We expect 2 out of 3 countries to post an increase in insolvencies, and 1 out of 2 countries to register in 2019 more insolvencies than over the 2003-2007 period

© Copyright Allianz

01

FISCAL AND MONETARY FUSES

TO PRESERVE THE US FROM

DEBT UNSUSTAINABILITY

© Copyright Allianz

US labor markets and household consumption

Sources: IHS Global Insight. Allianz Research Sources: IHS Global Insight. Allianz Research Sources: IHS Global Insight. Allianz Research

US economic circuit signals end of the cycle US investment and exports (%, y/y)

The fed funds rate looks set to rise above the US nation’s saving rate from Q4 2019 onwards. In these territories, the probability of a recession becomes non negligible

0.0

0.2

0.4

0.6

0.8

1.0

-5

0

5

10

15

80 83 86 89 92 95 98 01 04 07 10 13 16 19

US GDP (%, y/y, LHS) US nation saving rate (%, LHS)

Fed Funds Target rate (%, LHS) Recessions (0 or 1, RHS)

-30

-20

-10

0

10

20

30

-30

-20

-10

0

10

20

30

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

Total investment YoY Fixed non residential investment YoY

IT investment YoY Residential investment YoY

Exports

Investment is showing signs of weakening amid higher interest rates, less supportive external conditions and deteriorating corporate credit quality

3

4

5

6

7

8

9

10-4

-2

0

2

4

6

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Consumption (%, y/y, LHS)

Unemployment rate (%, inverse order, RHS)

Solid employment growth provides a strong boost to household confidence and stronger consumption

US ECONOMY: GROWTH ENGINE IS ROARING BUT…

8

© Copyright Allianz

The share of high yield bonds has been flat since 2015 at around one third (below the 2009 peak of 45%). But the share of the lowest invest grade level (BBB) has reached a record high of 35% in Q2 2018

Sources: IHS Global Insight. Allianz Research Sources: IHS Global Insight. Allianz Research

Debt of US economic sectors (as % of GDP) US non financial debt (% of GDP) US net issuance of risky business debt (leveraged loans and high yield or unrated bonds, USD bn)

Sources: Fed, Allianz Research

0

50

100

150

200

250

300

350

400

70 72 75 78 81 84 87 89 92 95 98 01 04 06 09 12 15 18

Financial sector Household US Treasury Non financial business

Looking at total US debt aggregated across all sectors, the deleveraging mode is still on, suggesting that the systemic risk is not implicated for now

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

70 73 76 79 82 85 88 91 94 97 00 03 06 09 12 15 18

Business Debt US Treasury Debt

Household Debt Financial

median

Deviations from the long-term growth trend of debt is traditionally a good indicator for the nature of an upcoming crisis. Today, public debt and corporate debt are at risk

-40

-30

-20

-10

0

10

20

30

40

50

60

70

20

06

20

07

20

08

20

09

20

11

20

11

20

12

20

13

20

14

20

15

20

16

20

18

US DEBT: LOCALIZING THE MALFUNCTIONS

9

© Copyright Allianz

Sources: IHS Global Insight. Allianz Research

US CPI (%, y/y) History of US government shutdowns

Sources: Wikipedia , Allianz Research

Circuit breaker #1: The Fed will hike interest rates twice in 2019 as inflation remains stuck above 2%

Circuit breaker #2: A government shutdown is possible in Q4 2019. It will trigger a significant tightening of monetary and financial conditions

2013 (President Barack Obama): Oct. 1 to Oct. 17 - 16 days 1995-1996 (President Bill Clinton): December 5, 1995, to January 6, 1996, - 21 days 1995 (President Bill Clinton): Nov. 13 to 19 - 5 days 1990 (President George H.W. Bush): October 5 to 9 - 3 days 1987 (President Ronald Reagan): December 18 to December 20 - 1 day 1986 (President Ronald Reagan): October 16 to October 18 - 1 day 1984 (President Ronald Reagan): October 3 to October 5 - 1 day 1984 (President Ronald Reagan): September 30 to October 3 - 2 days 1983 (President Ronald Reagan): November 10 to November 14 - 3 days 1982 (President Ronald Reagan): December 17 to December 21 - 3 days 1982 (President Ronald Reagan): September 30 to October 2 - 1 day 1981 (President Ronald Reagan): November 20 to November 23 - 2 days 1979 (President Jimmy Carter): September 30 to October 12 - 11 days 1978 (President Jimmy Carter): September 30 to October 18 18 days 1977 (President Jimmy Carter): November 30 to December 9 - 8 days 1977 (President Jimmy Carter): October 31 to November 9 - 8 days 1977 (President Jimmy Carter): September 30 to October 13 - 12 days 1976 (President Gerald Ford): September 30 to October 11 - 10 days

-200

0

200

400

600

800

1000

-200

0

200

400

600

800

1000

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Net issuance

Gross issuance

Bond refinancing needs

Nonfinancial companies’ debt issuance in the US

Record high refinancing needs will make tightening credit conditions painful for US non-financial companies

Sources: IHS , Allianz Research

US POLICY: FUSES AGAINST FURTHER DEBT INFLATING

10

© Copyright Allianz

Sources: Fed. Allianz Research

Corporate bond mutual fund and loan mutual fund assets (USD bn)

A rush to redeem shares of mutual funds could exacerbate losses of relatively illiquid types of assets. Negative wealth effects will hurt consumption prospects

0

500

1000

1500

2000

2500

02 04 05 07 09 10 12 14 15 17

Bank loan mutual funds

High-yield corporate bond mutual funds

Investment-grade corporate bond mutual funds

GDP growth

A technical recession is possible as early as 1H20. US growth slowdown will start in 2019 amid diluting impact of the fiscal stimulus and tightening credit conditions

Sources: Fed. Allianz Research

US SCENARIO: A MORE ABRUPT ADJUSTMENT IN 2020

11

© Copyright Allianz

02

EUROZONE AND CHINA: FUELING

DEMAND IN THE SHORT-TERM

AND REPAIRING SUPPLY OVER

THE MEDIUM-TERM

© Copyright Allianz

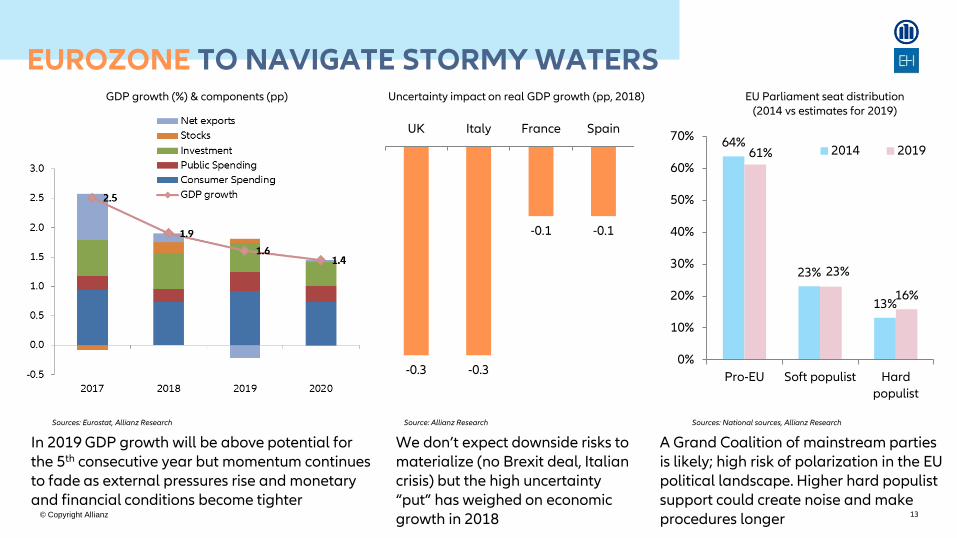

A Grand Coalition of mainstream parties is likely; high risk of polarization in the EU political landscape. Higher hard populist support could create noise and make procedures longer

EUROZONE TO NAVIGATE STORMY WATERS GDP growth (%) & components (pp)

Sources: Eurostat, Allianz Research

-0.3 -0.3

-0.1 -0.1

UK Italy France Spain

Uncertainty impact on real GDP growth (pp, 2018)

Source: Allianz Research

In 2019 GDP growth will be above potential for the 5th consecutive year but momentum continues to fade as external pressures rise and monetary and financial conditions become tighter

64%

23%

13%

61%

23%

16%

0%

10%

20%

30%

40%

50%

60%

70%

Pro-EU Soft populist Hard

populist

2014 2019

EU Parliament seat distribution (2014 vs estimates for 2019)

Sources: National sources, Allianz Research

We don’t expect downside risks to materialize (no Brexit deal, Italian crisis) but the high uncertainty “put” has weighed on economic growth in 2018 13

© Copyright Allianz 14

EUROZONE CORPORATES: STILL RESILIENT…

France: Business creations

France: Creative destruction in the making. Corporate creations increased by +11% in 2018 and should continue to the upward trend. At the same time, business insolvencies rose by +2.2% from the May trough to October

Sources: IHS Global Insight, Allianz Research

40000

45000

50000

55000

60000

65000

07 08 09 10 11 12 13 14 15 16 17 18

54275insolvencies at end-

October 2018

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

08 09 10 11 12 13 14 15 16 17 18

France: Business insolvencies

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

10 11 12 13 14 15 16 17 18

Unit Labor Cost

Investment in equipment

Investment in construction

Spain: Unit labor costs (ULC) and investment growth (%, y/y)

Spain: Resilience partly explained by corporate dynamism. Historically high profit shares (>43% of GVA) and subdued ULC growth allows companies to invest. Reforms such as giving priority to company-level wage agreements (2012) controlled the wage increases despite employment gains

Sources: IHS, Allianz Research

© Copyright Allianz

Cost of funds and balance sheet constraints

Q2 2018 Q3 2018

Eurozone -3 3

Germany 0 0

Spain -10 0

France 0 0

Italy -10 10

Netherlands 0 0

Note: The net percentages for the questions relating to contributing factors are defined as the difference between the percentage of banks reporting that the given factor contributed to a tightening and the percentage reporting that it contributed to an easing

Belgium

Ireland

Greece

Netherlands

Germany

France

Portugal

Italy Spain

UK

Finland

0%

10%

20%

30%

40%

50%

60%

70%

80%

0% 30% 60% 90% 120% 150% 180% 210%

No

n-f

ina

nci

al c

orp

oa

tio

ns'

ma

rgin

s, %

of

valu

e a

dd

ed

Non-financial corporates' debt, % of GDP

-100

0

100

200

300

400

500

0

50

100

150

200

250

300

350

400

450

00 02 04 06 08 10 12 14 16 18

IG corporate spread (lhs)

OAT-Bund spread (rhs)

BTP-Bund spread (rhs)

Corporate debt vs profitability ECB Bank Lending Survey Corporate vs sovereign spreads (bp)

Sources: BIS, Eurostat, Allianz Research

Sources: ECB, Allianz Research Sources: Bloomberg, Allianz Research

The Eurozone investment cycle has been boosted by credit growth. Tighter financial conditions will make banks more risk adverse while market conditions could remain volatile as the ECB starts to normalize monetary policy

EUROZONE CORPORATES: …BUT FEWER BUFFERS

15

© Copyright Allianz

In times of past-the-peak economic growth and waning liquidity, we expect fiscal policy to step up its game to address lingering political discontent – at least in Eurozone countries where fiscal room for maneuver allows for it

Reinvestment policy

16

Fiscal balance (% of GDP) Spreads between 10-yr govt bonds over German Bunds

ECB QE stock and flows (EURbn)

Sources: IHS Global Insight. Allianz Research Sources: IHS Global Insight. Allianz Research Sources: IHS Global Insight. Allianz Research

The ultra-expansive monetary policy has served as a buffer in times of elevated political uncertainty, drowning out market concerns while supporting risk appetite

As the ECB takes a first step towards normalizing its policy by ending monthly QE net purchases come Jan 2019, market discipline will start to return. But the re-investment of maturing principal until at least early 2021 will act as a safety-net

-6

-5

-4

-3

-2

-1

0

1

2

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

Italy

Germany

France

Spain

Eurozone

EUROZONE: POLICY-MIX TO TAME UNCERTAINTY

© Copyright Allianz

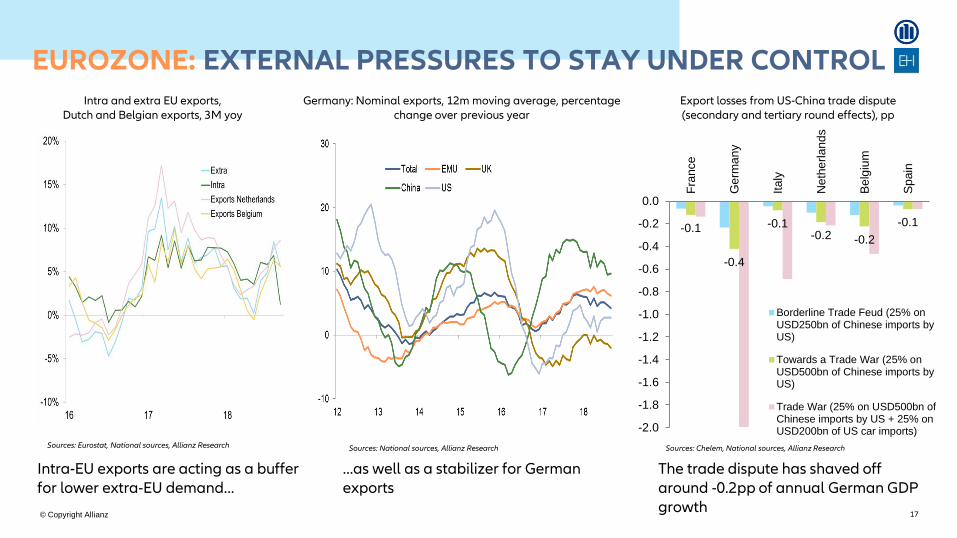

The trade dispute has shaved off around -0.2pp of annual German GDP growth

17

Intra and extra EU exports, Dutch and Belgian exports, 3M yoy

Germany: Nominal exports, 12m moving average, percentage change over previous year

…as well as a stabilizer for German exports

-0.1

-0.4

-0.1-0.2 -0.2

-0.1

-2.0

-1.8

-1.6

-1.4

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

Fra

nce

Germ

an

y

Italy

Neth

erl

and

s

Be

lgiu

m

Sp

ain

Borderline Trade Feud (25% onUSD250bn of Chinese imports byUS)

Towards a Trade War (25% onUSD500bn of Chinese imports byUS)

Trade War (25% on USD500bn ofChinese imports by US + 25% onUSD200bn of US car imports)

Intra-EU exports are acting as a buffer for lower extra-EU demand…

Export losses from US-China trade dispute (secondary and tertiary round effects), pp

Sources: Eurostat, National sources, Allianz Research Sources: National sources, Allianz Research Sources: Chelem, National sources, Allianz Research

EUROZONE: EXTERNAL PRESSURES TO STAY UNDER CONTROL

© Copyright Allianz

Households Saving (% Disposable income)

Sources: IMF, Allianz Research

Household debt vs. credit to households

10%

15%

20%

25%

30%

30%

35%

40%

45%

50%

55%

60%

14 15 16 17 18

Households debt (% GDP, left)

Credit to households (y/y, right)

8.9 8.4

9.0 8.7 8.5

2.62.0

1.62.0

2.5

6.3 6.5

7.5

6.76.0

0

1

2

3

4

5

6

7

8

9

10

15 16 17 18f 19f

Nominal per capita disposable incomeInflationReal Disposable income

38.5

38.0

37.1

35.5 35.5 35.1

34.6

32

33

34

35

36

37

38

39

13 14 15 16 17 18f 19f

Income growth

Driver #1: Strong credit growth Driver #2: Positive income growth Driver #3: Declining savings rate

Sources: IMF, Allianz Research Sources: IMF, Allianz Research

CHINA: BETTING (BOLDLY) ON HOUSEHOLDS

18

© Copyright Allianz

-40

-20

0

20

40

60

80

100

120

14 15 16 17 18

Bank domestic claims On Government

On private sector On Other NBFI

19

Banks’ domestic claims by agents Financial sector indicators

N.B: loan to deposit and NPL ratios figures stop end Q3 2018, shadow banking flows take into account trust, entrusted loans and undiscounted bank acceptances over October 2017-Septmber 2018, Non-financial corporations debt is based on BIS figures which end Q1 2018. Sources: WIND, IHS, BIS, Allianz Research

2017 Last

Loan to deposit ratio 70.6 73.6

Bank NPL ratio 1.7 1.9

Urban banks 1.5 1.7

Rural banks 3.2 4.2

SOE 1.5 1.5

Shadow Banking Flow s (% GDP) 4.3 -1.9

Non-Financial corporations debt (%

GDP)

160.3 164.1

Credit to private sector increase gradually (+12.6% y/y in October from a low 11% in June)

Overall credit growth is stable. By segments, the private sector is the one benefitting from current monetary easing

Prudence is justified by the fact that the financial system is still under stress and room for maneuver is increasingly limited

Sources: IHS, Allianz Research

CHINA: PRIORITIZING BETTER CAPITAL ALLOCATION

© Copyright Allianz 17-Dec-18 20

Bold figures indicate where we are end Q4. 10% on USD200bn imports and 25% on USD50bn imports from China have been enacted. RMB depreciated by -10% since March Sources: IHS, Allianz Research

10% tariff on USD imports from China

Cost 25% tariff on USD imports from China

Cost RMB

depreciation Cost

Absorption

50 5 50 12.5 -2% -10

100 10 100 25.0 -4% -20

150 15 150 37.5 -6% -30

200 20 200 50.0 -8% -40

250 25 250 62.5 -10% -50

300 30 300 75.0 -12% -60

350 35 350 87.5 -14% -70

400 40 400 100.0 -16% -80

450 45 450 112.5 -18% -90

500 50 500 125.0 -20% -100

How much RMB depreciation is required to make up for the US tariff shock?

A static approach (USD bn)

Nominal investment (YTD, y/y)

0

5

10

15

20

25

30

35

40

14 15 16 17 18

Total

State Holding Enterprises

Private investment

Infrastructure spending

• Infrastructure spending up +3.7% YTD YY in Jan-Oct (after +3.3%)

• SOE investment up +1.8% (after +1.2%)

A 10% RMB depreciation would help absorb a cost increase of USD 50 bn. More should be expected if the US raises tariffs further

Fiscal stimulus is bearing fruit: Infrastructure and SOE investment are starting to pick up

Sources: IHS, Allianz Research

CHINA: FINE-TUNING SHOCK ABSORBERS

© Copyright Allianz

CHINA: OPENING UP WISELY

Tariff cut: China’s tariff cuts help support import growth and absorb higher inputs cost due to oil prices and RMB depreciation

Partnerships: Accelerating partnerships helps diversify trade opportunities. The Belt and Road Initiative is the core strategy for now. Watch out for partnership in Asia (RCEP) and Europe

-25

-20

-15

-10

-5

0

5

10

15

20

25

-10

-5

0

5

10

14 15 16 17 18

Producer prices (y/y, left)

USD denominated imports (3mma y/y,right)

USD denominated imports and producer prices

16%

18%

20%

22%

24%

26%

28%

30%

32%

34%

36%

05 06 07 08 09 10 11 12 13 14 15 16 17 18

United States

OBOR countries

Share of US and BRI exports in total USD denominated exports

Reforms: Business-friendly reforms will be important to attract much-needed investment. Investor protection and insolvency resolution remain key problems

0 20 40 60 80 100

Starting a business

Getting electricity

Trading across borders

Registering property

Enforcing contract

Total score

Paying taxes

Construction permits

Getting credit

Protec. minority investors

Resolving insolvency

2019

2018

Ease of doing business - score and subcomponents (100 = best)

Sources: IHS, Allianz Research Sources: IHS, Allianz Research Sources: WB, Allianz Research

Best sub-components

To improve

21

© Copyright Allianz

03

EMERGING ECONOMIES :

TECHNICAL INSPECTION BY THE

MARKET TO CONTINUE

© Copyright Allianz

In a scenario where US growth decelerates progressively, US monetary policy tightening would ease with Emerging Markets standing to benefit

Foreign reserve adequacy: FX reserves in % of liquidity potential needs

Sources: IHS Global Insight, Allianz Research

Growth differentials between Advanced Economies and Emerging Markets vs. exchange rates

Sources: IHS Global Insight, Allianz Research

Capital flows to Emerging Markets (excl. China and Russia), USD bn

Capital flows to Emerging Markets to prove fickle, but attractiveness to remain and reignite capital inflows in periods of lower risk-aversion

Sources: IHS Global Insight, Allianz Research

-40

-20

0

20

40

60

80

100

12 13 14 15 16 17 18

Long-term average

0%

50%

100%

150%

200%

250%

In case of adverse shocks, several Emerging Markets may face liquidity crises, adversely impacting the entire EM asset class

80

85

90

95

100

105

110

115

120

125

130

0

1

2

3

4

5

6

7

03 05 07 09 11 13 15 17 19 21

Growth differential (left)

Exchange rate (right)

Appreciation

%

EMERGING MARKETS: RESILIENCE AMID VOLATILITY

23

© Copyright Allianz

7.16.6

6.36.0

5.3

4.6

3.6

7.06.4

6.15.7

5.0

4.1

3.2

0

1

2

3

4

5

6

7

8

India Vietnam China Philippines Indonesia Malaysia Thailand

18 19 20

Emerging Economies: High tides for high flyers • Emerging Markets in the region will continue to grow above

global growth on average benefitting from (i) resilient growth in China, (ii) trade diversion as corporates look for cheap alternative hubs of production (Vietnam, India, Indonesia and Philippines, e.g.) and (iii) supportive fiscal policy (Thailand). Yet tightening of monetary conditions and weaker global demand will lead to a growth deceleration

• Main risks stem from continued pressures on the currency of markets with twin deficits (India, Indonesia and Philippines), overheating risks (Vietnam and Philippines) and the outcome of elections in India, Indonesia and Thailand

Advanced Economies: Adjusting to slower global demand • Economic growth is set to slow to in line with slower global trade

especially for trade related economies (South Korea, Singapore, Hong Kong and Taiwan)

• Policymakers will use fiscal leeway's to support economic growth next year. Apart from Japan, public finances are generally sound in all markets

• High households debt (e.g. in Australia, South Korea, New Zealand), tighter global financing conditions and trade uncertainties (with a large potential impact on Singapore, Taiwan and Hong Kong) are the big ticket items that corporates and the private sector should keep in mind for 2019

GDP growth (%) GDP growth (%)

ASIA-PACIFIC: KEEPING THE SYSTEM RUNNING

2.5 2.5 2.4 2.4

2.0

1.0

2.01.9

1.71.6

1.4

0.6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Australia Korea (South) Singapore Hong Kong Taiwan Japan

18 19 20

24

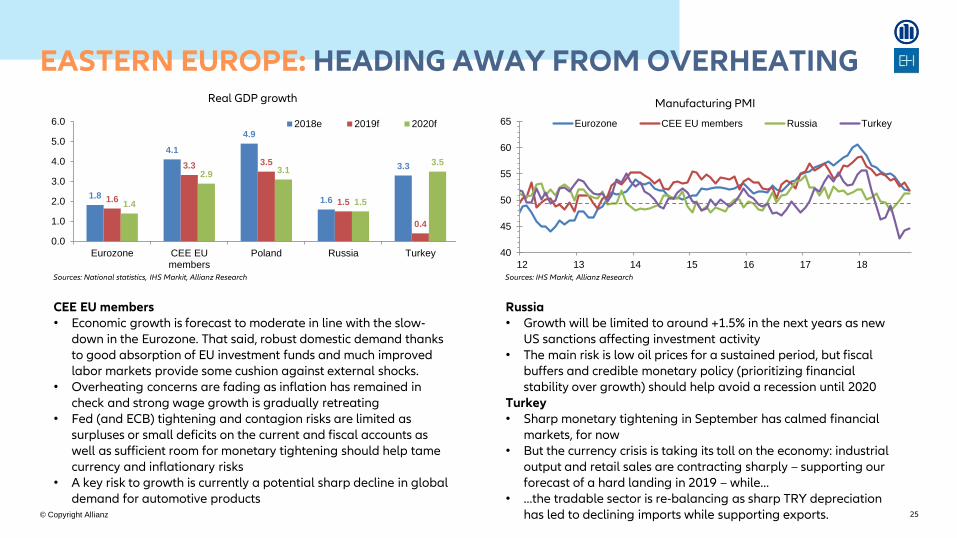

© Copyright Allianz 25

CEE EU members • Economic growth is forecast to moderate in line with the slow-

down in the Eurozone. That said, robust domestic demand thanks to good absorption of EU investment funds and much improved labor markets provide some cushion against external shocks.

• Overheating concerns are fading as inflation has remained in check and strong wage growth is gradually retreating

• Fed (and ECB) tightening and contagion risks are limited as surpluses or small deficits on the current and fiscal accounts as well as sufficient room for monetary tightening should help tame currency and inflationary risks

• A key risk to growth is currently a potential sharp decline in global demand for automotive products

Sources: National statistics, IHS Markit, Allianz Research

Russia • Growth will be limited to around +1.5% in the next years as new

US sanctions affecting investment activity • The main risk is low oil prices for a sustained period, but fiscal

buffers and credible monetary policy (prioritizing financial stability over growth) should help avoid a recession until 2020

Turkey • Sharp monetary tightening in September has calmed financial

markets, for now • But the currency crisis is taking its toll on the economy: industrial

output and retail sales are contracting sharply – supporting our forecast of a hard landing in 2019 – while…

• …the tradable sector is re-balancing as sharp TRY depreciation has led to declining imports while supporting exports.

40

45

50

55

60

65

12 13 14 15 16 17 18

Eurozone CEE EU members Russia Turkey

Manufacturing PMI

Sources: IHS Markit, Allianz Research

1.8

4.1

4.9

1.6

3.3

1.6

3.3 3.5

1.5

0.4

1.4

2.9 3.1

1.5

3.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Eurozone CEE EUmembers

Poland Russia Turkey

2018e 2019f 2020f

EASTERN EUROPE: HEADING AWAY FROM OVERHEATING Real GDP growth

© Copyright Allianz

LATAM : POLICY RISK & END OF MONETARY EASING

26

Latin America’s activity decelerated (+1.5%, excluding Venezuela) in 2018 as Argentina sank into recession. Going forward we expect a gradual acceleration to +2% in 2019, +2.4% in 2020. Recovery still slow, and late cycle dynamics will exacerbate divergence. Two stories:

1. Financial conditions will be less favorable for corporates as monetary policy gradually shifts to tightening mode

2. B.A.M’s future contingent on policy risk: Brazil, instability of policy platform + pension reform outlook challenging; Mexico: policy choices contradicting pro-business stance; Argentina: severe austerity could fuel social discontent, mind elections in October 2019

Country risk and economic growth Latin America vulnerability scorecard: not all in the same boat

Policy rates in inflation-targeting economies

Sources: IHS, IMF, Euler Hermes, Allianz Research

Sources: IHS, IMF, Euler Hermes, Allianz Research

Sources: IHS, Euler Hermes, Allianz Research

2%

4%

6%

8%

10%

12%

14%

11 12 13 14 15 16 17 18 19

Brazil

Chile

Colombia

Mexico

Peru

Forecast

2018 2020

20182019 2020

20182019 2020

2018 2020

20182019 2020

20182019 2020

20182019 2020

20182019 2020

20182019 2020

A1

B3

D4

Brazil

Venezuela

Argentina

Chile

BB1 Peru

BB2 Mexico

BB2Uruguay

-3.0%

2.0%

2.6% 2.6%

2.3%1.3%

3.8%3.0%

3.1% 3.0%

2.5%3.0%

2.3%1.7%

-18%-5%

C4

2018 2019

Low risk

Medium risk

Sensitive risk

High risk

2020

2.0%

2.5%

-2.0%

2.0 %

-2%

2018 2019 2020

2018 2019 2020

2018 2019 20202018 2019 2020

2018 2019 2020

2018 2019 2020

2018 2019 2020

Data as of Q4 2018

2018 2019 2020

EcuadorC3

1.1%0.7%

1.3%

ColombiaBB1

2.7%

3.5%

2.5%

2019 forecasts Argentina Brazil Mexico Colombia Chile

External

vulnerabilites and

debt rollover risk

Current account

balance-1.49% -0.8% -1.9% -2.7% -0.7%

External debt (% GDP) 27% 14% 36% 31% 45%

% of foreign-

denominated debt

(2017)

51% 18% 25% 27% 40%

Reserve adequacy (Aug

18)Adequate High Adequate Adequate Low

Cycle

management

Real interest rate (Aug

18, policy rate - CPI

inflation)

11.3% 2.0% 3.1% 1.0% -0.2%

Real GDP growth -2.0% 2.3% 2.0% 3.0% 3.0%

Fiscal riskFiscal deficit -2.6% -6.7% -2.5% -2.1% -0.9%

Public debt 80% 88% 54% 48% 25%

Policy uncertainty

risk

Probability of policy

mistakesModerate High High Low Low

© Copyright Allianz 27

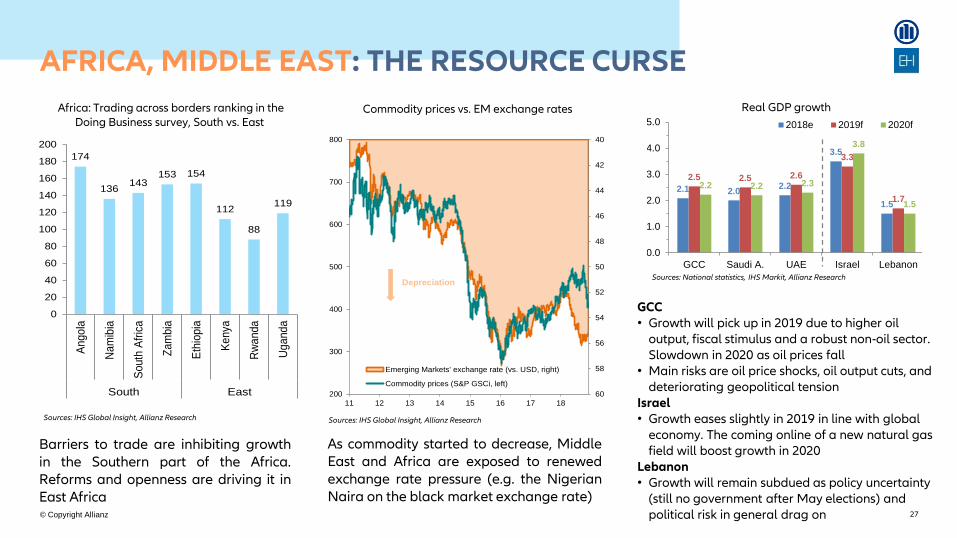

Real GDP growth

Sources: National statistics, IHS Markit, Allianz Research

GCC • Growth will pick up in 2019 due to higher oil

output, fiscal stimulus and a robust non-oil sector. Slowdown in 2020 as oil prices fall

• Main risks are oil price shocks, oil output cuts, and deteriorating geopolitical tension

Israel • Growth eases slightly in 2019 in line with global

economy. The coming online of a new natural gas field will boost growth in 2020

Lebanon • Growth will remain subdued as policy uncertainty

(still no government after May elections) and political risk in general drag on

2.1 2.02.2

3.5

1.5

2.5 2.5 2.6

3.3

1.7

2.2 2.2 2.3

3.8

1.5

0.0

1.0

2.0

3.0

4.0

5.0

GCC Saudi A. UAE Israel Lebanon

2018e 2019f 2020f

As commodity started to decrease, Middle East and Africa are exposed to renewed exchange rate pressure (e.g. the Nigerian Naira on the black market exchange rate)

Sources: IHS Global Insight, Allianz Research

Africa: Trading across borders ranking in the Doing Business survey, South vs. East

Barriers to trade are inhibiting growth in the Southern part of the Africa. Reforms and openness are driving it in East Africa

Sources: IHS Global Insight, Allianz Research

174

136143

153 154

112

88

119

0

20

40

60

80

100

120

140

160

180

200

Ango

la

Na

mib

ia

South

Afr

ica

Zam

bia

Eth

iopia

Kenya

Rw

anda

Ug

and

a

South East

40

42

44

46

48

50

52

54

56

58

60200

300

400

500

600

700

800

11 12 13 14 15 16 17 18

Emerging Markets' exchange rate (vs. USD, right)

Commodity prices (S&P GSCi, left)

Depreciation

AFRICA, MIDDLE EAST: THE RESOURCE CURSE

Commodity prices vs. EM exchange rates

© Copyright Allianz

THANK YOU!

Ph

oto

by

raw

pix

el.c

om

on

Un

spla

sh

Economic research Department

Q4 2018