climate-related financial disclosure report - china airlines

TRANSCRIPT

Climate-Related Financial Disclosure Report

China Airlines

Climate-Related Financial Disclosure

Report

January 2021

Climate-Related Financial Disclosure Report

I

Contents

Abstract...................................................................................................................................................................... 4

Chapter 1. Preface ............................................................................................................................................ 5

Chapter 2. Governance ..................................................................................................................................... 8

I. Supervisory mechanisms of the Board of Directors and the role, responsibility, and duties of the

management ....................................................................................................................................................... 8

Chapter 3. Strategy .......................................................................................................................................... 9

I. Results of the identification of short, medium, and long-term climate-related risks and opportunities ........... 9

II. Potential climate risks and opportunities for business, strategy, and financial planning, and response

strategies ........................................................................................................................................................... 13

(I) Plotting short, medium, and long-term risks and impact on operations under the 2°C and 4°C scenarios. 13

(II) Risks to be addressed and strategic adjustments in response to possible resulting material impact ......... 17

Chapter 4. Risk management ......................................................................................................................... 18

I. Identification and evaluation framework for climate change risks and opportunities ..................................... 18

(I) Climate Risk and Opportunity Assessment Procedures ............................................................................... 18

(II) Establishment of the climate risk management methodology .................................................................... 19

II. Climate risk and opportunity materiality identification .................................................................................... 19

III. Integration of climate-related risk identification, assessment and management procedures into internal

procedures of the Company .............................................................................................................................. 20

Chapter 5. Indicators and Targets ................................................................................................................... 21

I. Climate-related risk indicators .......................................................................................................................... 21

II. Greenhouse gas emissions and related risks ..................................................................................................... 21

III. Climate change targets and mitigation and adaptation strategy ...................................................................... 22

Chapter 6. Conclusion .................................................................................................................................... 26

Climate-Related Financial Disclosure Report

II

TABLES

Table 4-1. Standards for assessing climate impact risks and opportunities ............................................................... 20

Table 5-1. Climate risk indicators ............................................................................................................................. 21

Table 5-2. Greenhouse gas emissions ....................................................................................................................... 22

Table 5-3. Climate risk management strategy and operations .................................................................................. 23

Climate-Related Financial Disclosure Report

III

Figures

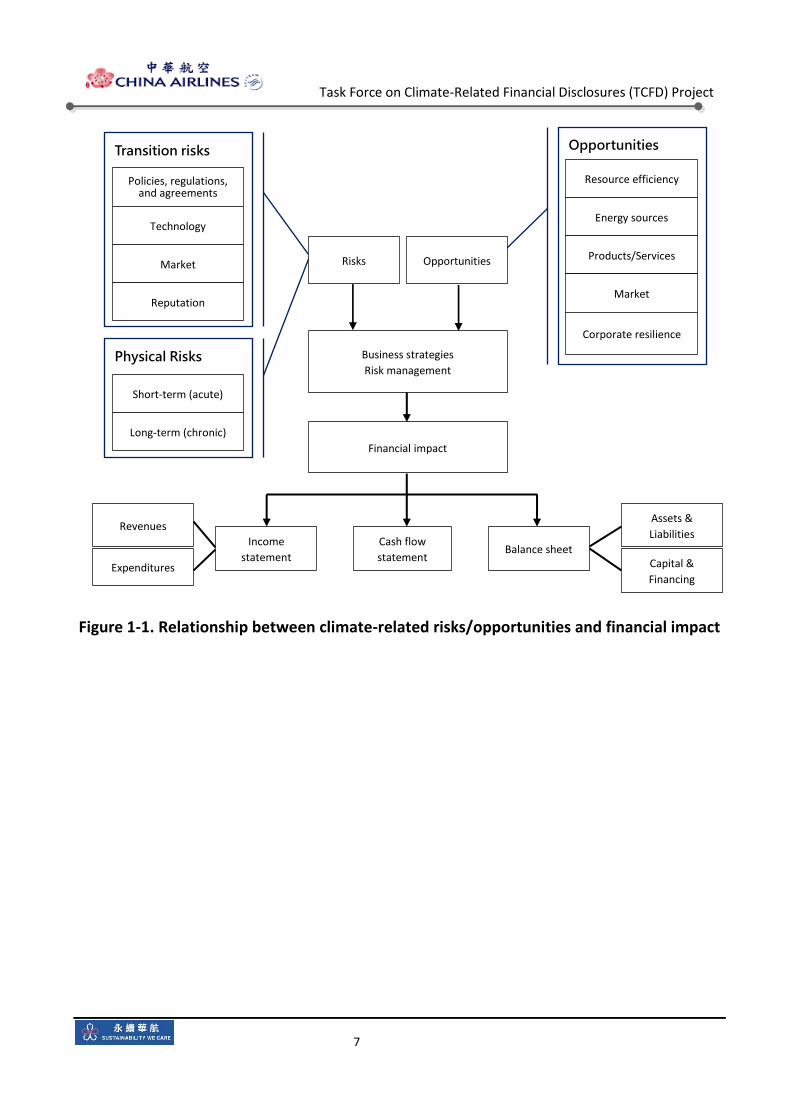

Figure 1-1. Relationship between climate-related risks/opportunities and financial impact ...................................... 7

Figure 2-1. TCFD management duties and organizational structure ............................................................................ 8

Figure 3-1. Climate scenarios .................................................................................................................................... 10

Figure 3-2. Climate risk/opportunity type and definitions ........................................................................................ 11

Figure 3-3. Impact of 2°C on operations ................................................................................................................... 12

Figure 3-4. Impact of 4°C on operations ................................................................................................................... 12

Figure 3-5-1. Short-term risks and risk distribution under the 2°C scenario .............................................................. 13

Figure 3-5-2. Medium-term risks and risk distribution under the 2°C scenario ......................................................... 14

Figure 3-5-3. Long-term risks and risk distribution under the 2°C scenario ............................................................... 14

Figure 3-6-1. Short-term risks and risk distribution under the 4°C scenario .............................................................. 15

Figure 3-6-2. Medium-term risks and risk distribution under the 4°C scenario ......................................................... 15

Figure 3-6-3. Long-term risks and risk distribution under the 4°C scenario ............................................................... 16

Figure 4-1. Climate risk/opportunity assessment procedures ................................................................................... 18

Figure 4-2. Climate risk financial quantitative management methods ...................................................................... 19

Figure 5-1. Four main strategies for climate change risks ......................................................................................... 23

Task Force on Climate-Related Financial Disclosures (TCFD) Project

4

Abstract

As companies now face increasingly complex challenges in the external environment, climate

change has become one of the most urgent issues in the world today. China Airlines (CAL)

understands the intricate relations between the operations of the aviation industry and climate

issues, and therefore signed and adopted the guidelines of the Task Force on Climate-Related

Financial Disclosures (TCFD) in 2018. We incorporated the guidelines into the operations of the

Company’s internal risk management mechanisms and established a TCFD Task Force composed of

different units to implement related operations.

CAL referenced the international carbon reduction pathways, scientific research (IPCC AR5), and

climate change and extreme weather incidents in recent years to identify and classify issues related

to CAL. We then gradually completed the analyses based on the operating procedures of units to

ensure the comprehensiveness of the evaluation contents. We use a matrix assessment for the

operational risk and classify the severity of risks based on their impact on operations. We also

consider both financial and non-financial impacts. We consider short, medium, and long-term impact

for time boundaries. We have identified 7 short-term risks and 10 medium to long-term risks. The

main medium to long-term high-risk issue is sustainable aviation fuel.

In addition, we have also identified three issues with direct and long-term impact on the aviation

industry for which we need to pay particular attention to, and they include the increase in operating

costs due to the intensification of extreme weather events, the shortage of water resources which

may affect daily operations and passenger services, and the cost of carbon trading or carbon

taxes/fees arising from international carbon control mechanisms. These costs will become additional

operating costs with direct impact on the operating performance and test the capabilities of

companies for cash flow management.

Contact Information for the Report:

Environment Department, Corporate Safety Office

E-mail: [email protected]

Address: No.1, Hangzhan S. Rd., Dayuan Dist., Taoyuan City

China Airlines Concern for Climate Change website:

https://calec.china-airlines.com/csr/en/environment/manage-climate.html

Task Force on Climate-Related Financial Disclosures (TCFD) Project

5

Chapter 1. Preface

In April 2015, the G20 Financial Stability Board established the Task Force on Climate-related

Financial Disclosure (TCFD) to help the public and private sectors establish mechanisms for

information disclosure and provide investors, lenders, and insurance underwriters with the

necessary information to adequately assess the capacity of companies to respond to climate-

related risks and opportunities. TCFD provided clear, comparable, and consistent

recommendations and guidelines for information disclosure in June 2017. More than 1,600

organizations/companies and 70 countries have expressed support, and TCFD recommendations

have been incorporated by international mainstream sustainability evaluations into their surveys.

China Airlines (CAL) has signed on as a supporter of the Task Force on Climate-related Financial

Disclosures (TCFD) in September 2018 and became the first company in Taiwan’s transportation

industry to become a supporter.

The aviation industry emits large quantities of greenhouse gases and faces a staggering

amount of pressure and duties for reducing carbon emissions. They include the three-phase

carbon reduction goals and four-pillar strategy (technology improvement, operational efficiency,

infrastructural efficiency, and effective economic measures) proposed by the International Air

Transport Association (IATA), Carbon Neutral Growth from 2020 (CNG2020) proposed by the

International Civil Aviation Organization (ICAO), the Green Deal of the European Union, and

carbon pricing and carbon taxes/fees implemented by governments.

On the other hand, international stakeholders now pay closer attention to the disclosure of

non-financial information on corporate ESG (environmental, social and corporate governance)

performance. In addition to the existing sustainability standards and assessments, the

Sustainability Accounting Standards Board (SASB) has recently strengthened the industry-specific

"Sustainability Accounting Standards (SASB Standards)". In August 2020, Taiwan's Financial

Supervisory Commission (FSC) announced the "Corporate Governance 3.0 - Sustainable

Development Roadmap" and "Green Finance Action Plan 2.0". The FSC explicitly stated that it will

incorporate the guidelines published by the Task Force on Climate-Related Financial Disclosures

(TCFD) and the Sustainability Accounting Standards Board (SASB) to strengthen information

Task Force on Climate-Related Financial Disclosures (TCFD) Project

6

disclosure in corporate sustainability reports.

CAL formulated short, medium, and long-term carbon reduction targets based on the

aforementioned carbon reduction targets and strategies for the aviation industry, international

development trends, legislation development trends, the expectations of stakeholders, the

Company’s finance and operation planning, and technical feasibility. We also incorporated the

management structure in the TCFD guidelines and the indicators regarding greenhouse gas

emissions of the aviation industry in the "SASB Standards" to analyze the potential transition and

physical risks and opportunities. We implement the following key operations to gradually

strengthen CAL’s management of climate-related risks and opportunities and competitiveness.

I. We follow the TCFD guidelines and framework to identify climate risks and opportunities,

analyze the impact on finance and capital utilization, and develop decision-making

strategies and high-level governance mechanisms to strengthen our ability to address and

manage climate risks and opportunities.

II. We created methods to quantify risks and opportunities in monetary terms and learn about

the impact of climate change on current and future operations and cash flow. (Figure 1-1)

III. We enhance the efficiency of internal and external communication in governance, strategy,

risk management, and indicators and targets in response to the disclosure requirements in

TCFD and SASB Standards.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

7

Figure 1-1. Relationship between climate-related risks/opportunities and financial impact

Transition risks

Policies, regulations, and agreements

Technology

Market

Reputation

Opportunities

Resource efficiency

Energy sources

Products/Services

Market

Corporate resilience

Physical Risks

Short-term (acute)

Long-term (chronic)

Risks Opportunities

Business strategies

Risk management

Financial impact

Income

statement

Cash flow

statement Balance sheet

Revenues

Expenditures

Assets &

Liabilities

Capital &

Financing

Task Force on Climate-Related Financial Disclosures (TCFD) Project

8

Chapter 2. Governance

I. Supervisory mechanisms of the Board of Directors and the role, responsibility,

and duties of the management

CAL has included the issue of climate risks as a key issue for corporate sustainability and

environmental governance. It is monitored by the Corporate Sustainability and Corporate

Environmental Committee through control mechanisms and the performance is reported to the

Board of Directors on a regular basis.

This Climate Governance Report was presented to the Board of Directors in the fourth

quarter of 2020. The contents mainly included background climate information, risk and

opportunity identification results, quantitative conclusions drawn from financial information,

risks to be resolved, issues to be monitored by the Company, short/medium/long-term

strategies and performance, and difficult issues to be addressed. The action plans and budgets

were revised and formulated based on the opinions of the Directors/Committee Members after

the meeting.

The TCFD management duties and organizational structure are shown in Figure 2-1.

Figure 2-1. TCFD management duties and organizational structure

The Management - Risk Management

Corporate Sustainability Committee

Corporate Environmental Committee

The Board of Directors - Risk Supervision

Board of Directors To review the formulation of various risks and opportunities management strategies and performances.

The Working Level - Risk Control

Strategy units, finance units, flight control units, business units, administrative units, maintenance units, and service units

Sup

ervision

M

anagem

ent

Rep

ort

Rep

ort

To oversee all accountable division, which identify and evaluate potential risk faced by CAL

Task Force on Climate-Related Financial Disclosures (TCFD) Project

9

Chapter 3. Strategy

I. Results of the identification of short, medium, and long-term climate-related

risks and opportunities

CAL set 2050 as the milestone year for verification based on reduction targets of IATA and

certain countries. Therefore, we analyzed the risks and opportunities arising from different

climate scenarios and related issues until the year 2050. However, the current assessments of

international transportation associations and investment institutions based on the feasibility and

effectiveness of the implementation of corporate strategies, and the impact of the COVID-19

epidemic showed that the aviation industry could only recover to operations before the epidemic

after the end of 2023. Therefore, the time and geographical boundaries for the assessment were

set as follows:

(I) Short, medium, and long-term settings:

1. Short term: 2021-2023

2. Medium term: 2024-2025

3. Long term: 2026-2030

(II) Geographical boundaries:

The geographical boundaries cover all global stations of CAL. We implemented a

"general" analysis based on the potential scenarios associated with the stations and will

incorporate the regional environmental, political, and economic conditions of the stations for

analyses.

(III) Scientific reports:

In terms of climate scenarios, we adopted the more moderate greenhouse gas emission

scenario (RCP2.6; limiting temperature increase to below 2°C) and the more extreme

greenhouse gas emission scenario (RCP8.5; global temperature increases by 4°C) in the Fifth

Assessment Report (AR5) of the IPCC, as well as the carbon reduction paths of ICAO Carbon

Offsetting and Reduction Scheme for International Aviation (CORSIA) and IATA. Climate

scenario sets as shown in Figure 3-1.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

10

(IV) Climate scenario:

The Company analyzes and identifies risks and opportunities that may affect operating

costs or revenues under 2°C and 4°C scenarios, and classifies the risks into transition risks

and physical risks based on TCFD guidelines. The definitions of each category are shown in

Figure 3-2.

Figure 3-1. Climate scenarios

Task Force on Climate-Related Financial Disclosures (TCFD) Project

11

Figure 3-2. Climate risk/opportunity type and definitions

Climate scenario Risk type Definitions Associated risks and

opportunities

International carbon reduction paths: ‧ ICAO and IATA carbon

reduction targets and strategies

‧ ICAO CORSIA and EU ETS regulations

‧ ICAO proposed 2% SAF target

‧ EU Green Deal carbon reduction targets

Regulations in Taiwan: ‧ Taiwan’s

energy/greenhouse gas regulations and regulatory requirements

Science-based report: ‧ IPCC AR5

RCP 2.6 RCP 4.5 RCP 6.0 RCP 8.5

Market competition:

‧ Competitors’ carbon

reduction targets and

strategies

‧ Sustainable

consumption trends

ESG investments

Transition risks

Physical Risks

Low-carbon economy transformational and transition risks

Impact of climate change on the climate system and environment, such as floods and intense typhoons.

Opportunities created by climate change such as the low-carbon economy, carbon rights, and business reputation.

Opportunities

Policy and Legal

regulations

Technology

Market

Reputation

Immediate (acute)

Long-term (chronic)

Resource efficiency

Access to energy

Resilience

Market

Products/services

Task Force on Climate-Related Financial Disclosures (TCFD) Project

12

Risks and opportunities under 2°Cand 4°C scenarios are shown in Figure 3-3 and 3-4.

Figure 3-3. Impact of 2°C on operations

Figure 3-4. Impact of 4°C on operations

Task Force on Climate-Related Financial Disclosures (TCFD) Project

13

II. Potential climate risks and opportunities for business, strategy, and financial

planning, and response strategies

(I) Plotting short, medium, and long-term risks and impact on operations under the 2°C and 4°C scenarios.

The Company has included climate risk identification and management as an important issue

for corporate sustainability and environmental management. The related risks and

operational impacts after the identification, assessment, response and review process of the

internal risk management mechanisms are as follows:

1. Plotting risks under the 2°C scenario (Note: Green bubbles correspond to

transformational risks; orange bubbles correspond to physical risks)

Figure 3-5-1. Short-term risks and risk distribution under the 2°C scenario

Task Force on Climate-Related Financial Disclosures (TCFD) Project

14

Figure 3-5-2. Medium-term risks and risk distribution under the 2°C scenario

Figure 3-5-3. Long-term risks and risk distribution under the 2°C scenario

Task Force on Climate-Related Financial Disclosures (TCFD) Project

15

2. Plotting risks under 4°C scenarios

Figure 3-6-1. Short-term risks and risk distribution under the 4°C scenario

Figure 3-6-2. Medium-term risks and risk distribution under the 4°C scenario

Task Force on Climate-Related Financial Disclosures (TCFD) Project

16

Figure 3-6-3. Long-term risks and risk distribution under the 4°C scenario

3. Impact on operations

All climate risks have small short-term impact on operations and there is no

need to increase capital expenditures. The impact on medium-term operations

increases within a limited scope mainly due to ICAO CORSIA mechanisms. If we

calculate the impact based on an operating growth of 1.5% per year and a full

adoption of 2% sustainable fuel, the increased cost of sustainable fuel has a higher

impact on operations. The long-term impact is the same as the medium-term

impact. If we calculate the impact based on a growth rate of 3% per year and a full

adoption of 2% sustainable fuel, the increased cost of sustainable fuel will still have

the highest impact on operations. However, the adoption of sustainable fuel is

dependent on the scale of market supply, and it is less likely for the Company to

fully adopt sustainable fuel within a short period. Therefore, the results of the

evaluation are only provided for internal reference by CAL, and are not results of

financial forecasts. In addition, there may be mandatory long-term requirements

for the use of renewable energy due to regulations. If we choose to invest in

renewable energy facilities, capital expenditures will be required.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

17

(II) Risks to be addressed and strategic adjustments in response to possible resulting material impact

1. We implement adjustments and mitigation each year to reduce the carbon trading

costs added as a result of ICAO CORSIA mechanisms. Please refer to "V. Description of

Mitigation and Adjustment Strategies for Targets and Indicators" for related

information.

2. In response to renewable energy use and energy transformation, we will continue to

improve the energy management system and various energy conservation measures

to reduce the electricity contract capacity and reduce the increased operating costs

from the use of renewable energy.

3. In response to the impact of climate change and rising sea levels on company

operations, units incorporate factors for related issues in the Company’s flight plans,

business performance management, and other operations and formulate future

response strategies and business operation adjustments and plans when necessary.

4. As sustainable aviation fuel is not readily available in Taiwan, we need the

government’s support with integrated policies and assistance for industries. We

therefore need to continue to lobby industries, the government, and the academia to

help create a development strategy for sustainable aviation fuel in Taiwan.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

18

Chapter 4. Risk management

I. Identification and evaluation framework for climate change risks and

opportunities

(I) Climate Risk and Opportunity Assessment Procedures

The Company designs climate risk assessment procedures based on the impact of

climate change on the Company’s overall operations. We also referenced to the "TCFD

recommendations report" and the "Guidelines for the Analysis of Climate-Related Risk and

Opportunities V2.01". We first identified the key units and equipment in the internal

operations of CAL such as the energy necessary for providing transportation services, the

electricity demand of aircrafts, air-conditioning systems, and other electricity consumption,

and assessed the potential impact and degree of impact. The climate risk/opportunity

assessment procedures are shown in Figure 4-1.

Figure 4-1. Climate risk/opportunity assessment procedures

1 Practical guide for Scenario Analysis in line with the TCFD recommendations 2nd edition (March 2020), Climate

Change Policy Division, Ministry of the Environment, Government of Japan.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

19

(II) Establishment of the climate risk management methodology

CAL collected information on the international carbon reduction methods, IPCC Fifth

Assessment Report (AR5), and phenomena caused by climate change in recent years in its

risk/opportunity assessment procedures to categorize and identify potential issues related

to CAL to implement the environmental impact assessment. The climate-related financial

quantitative management methodology is shown in Figure 4-2.

B/S: Balance sheet

P/L: Income statement

Figure 4-2. Climate risk financial quantitative management methods

II. Climate risk and opportunity materiality identification

CAL considers the impact and possibilities of material climate risks and opportunities on

operations. We prioritize the financial impact for the assessing the impact on operations.

Where financial information cannot be quantified, we will use non-financial information to

Input Process Output

Financial information

B/S, P/L Operating revenues

and expenses

Non-financial information

CO2 emissions

Percentage of sustainable fuel

External issues

Information published by different countries

Other reports

B/SP/L

Impact factors and parameters

(2℃)

Impact factors and parameters

(4℃)

Financial impact on B/SP/L

(2℃)

Financial impact on B/SP/L

(4℃)

Fuel consumption Fuel efficiency

IATA, ICAO, IPCC, and IEA reports

Task Force on Climate-Related Financial Disclosures (TCFD) Project

20

consider the impact.

The risks and opportunities to be addressed are shown in Table 4-1.

Table 4-1. Criteria/matrix for assessing climate impact risks and opportunities

Risk Level Strategy Action

High Immediate improvements Establish control and management

measures and review the effectiveness.

Medium Improvements based on

actual conditions

Establish control and management

measures and review the effectiveness

for the following conditions:

‧ Regulatory requirements

‧ Commitments

‧ Decisions of high-level

management

Follow development trends and the

impact for other items and establish

control and management measures

based on requirements.

Low

Continue to follow

development trends and

the impact

III. Integration of climate-related risk identification, assessment and management

procedures into internal procedures of the Company

CAL has established a TCFD Task Force, which has been included in the scope of

Corporate Environmental Risk Management Mechanisms. We also use the following

principles to periodically collect information on domestic and foreign climate and carbon

reduction policies, identify related risks and opportunities, implement regular reviews, and

propose improvement measures.

(I) Incorporate climate factors into the existing enterprise risk management mechanism

to strengthen climate risk / opportunity detection, response, and control capabilities

in all units.

(II) Incorporate climate change consideration to continuously improve and implement

various management procedures.

(III) Combine the CAL value chain environmental risk management to strengthen the

detection of climate risks and opportunities as well as management, and enhance the

capability of continued operations in response to extreme weather.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

21

Chapter 5. Indicators and Targets

I. Climate-related risk indicators

CAL has adopted GRI 302-3 and 305-4 indicators to assess and track climate-related risks.

We focus on aviation fuel use and fuel efficiency, and will gradually adopt disclosure indicators

of Sustainability Accounting Standards in the future to enhance performance tracking. The

related indicators for 2018 and 2019 are shown in the table below (5-1). The specific

performance has been disclosed in the annual CSR Report and the green performance webpage

on the official CSR website.

Table 5-1. Climate risk indicators Item 2018 2019 2019 Compared to

2018

Fuel use (ton) 2,284,957 2,230,971 -53,986

CO2 emissions (CO2e) 7,229,839 7,059,083 -170,756

Transport volume (1000

RTK)

9,544,260 9,072,762 -471,498

Fuel efficiency (fuel / 1000

RTK)

0.2394 0.2459 0.0065

Carbon emission intensity

(ton CO2 / 1000 RTK)

0.7575 0.7781 0.0206

II. Greenhouse gas emissions and related risks

CAL introduced a complete ISO 14064-1 greenhouse gas management mechanism, and

established a Carbon Management Task Force under the framework of the Corporate

Environmental Committee to comprehensively manage the carbon risk issues of corporate

operations and manage compliance with international carbon control schemes based on the

structure of carbon management. CAL’s 2018 and 2019 greenhouse gas emissions are shown

in the table below (5-2). Refer to the green performance webpage on the official CSR website

for detailed energy efficiency information.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

22

Table 5-2. Greenhouse gas emissions (Unit: tons CO2e)

GHG Scope 2018 2019 Related risks

Scope 1

Flight

operations 7,229.903 7,059,083

Risks of international carbon reduction pressure

and increased carbon offsetting costs

Ground

operations 3,511 4,981

Risks of reduction agreements with green airport

partners

Scope 2 19,949 18,169 Risks of mandatory renewable energy usage

Scope 3 1,644,656 1,607,690 Risks of brand customer requirements and

supplier management

III. Climate change targets and mitigation and adaptation strategy

In terms of short-term carbon reduction targets, CAL referenced and adopted ICAO and

IATA strategic recommendations, practices of benchmark international airlines, and experience

accumulated in reduction operations. We work with the Civil Aeronautics Administration and

published the first voluntary greenhouse gas reduction statement in the aviation industry

with the aim of promoting autonomous management for flight operations before the activation

of the global carbon management mechanisms planned by ICAO. To attain carbon reduction

targets of the aviation industry, CAL continued to enhance fuel efficiency improvement plans

and formulated the four major strategies including " establish a TCFD information system",

"improve fuel efficiency", "participate in the international carbon management mechanisms",

and "strengthen the emergency response system" (Figure 5-1) and other specific

implementation measures. The four major climate risk management strategies and operations

are shown in Table 5-3.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

23

Figure 5-1. Four main strategies for climate change risks

Table 5-3. Climate risk management strategy and operations

Response Item Target and Specific Actions

Governance

Strengthen climate

governance Continue to submit climate governance reports to the Board of Directors

Enhance management

supervision and cross-

departmental

operations

1. Implement corporate governance and green finance and introduce TCFD

and SASB standards and requirements.

2. Implement rolling management to improve the short, medium, and long-

term ESG performance

Strategy

Enhance TCFD

capabilities

1. Increase the comprehensiveness and depth of quantified Climate related

financial information.

2. Establish a cross-unit information operation platform.

Climate response

strategies and

management

1. Incorporate climate risks and opportunities into the Company’s overall

strategies and plans and implement related response actions.

2. Incorporate discussions of the impact of climate change in the Company’s

flight plans, business performance management, and other operations

and formulate response strategies and business operation adjustments

when necessary.

Participate in important

engagements

1. Participate in the international and Taiwan's important climate policy

engagement platforms, keep abreast of policy development trend, and

get hold of the right to speak.

2. Lobby the industry, government, and academia to create a development

strategy for domestic sustainable aviation fuel.

Use fleet renewal, aircraft weight reduction, flight optimization, and O&M improvement to reduce

carbon emissions

Participate in ICAO CORSIA carbon offsetting mechanisms to achieve the goal

of carbon neutral growth

Establish a climate financial information framework and data collection system to strengthen climate risk assessment and

accuracy

Improve the emergency response system and enhance response and resilience

against extreme weather incidents

Four main

strategies

for climate

change risks

Improving fuel efficiency

Participation in international carbon

management mechanisms

Emergency response

system

TCFD information

system

Task Force on Climate-Related Financial Disclosures (TCFD) Project

24

Response Item Target and Specific Actions

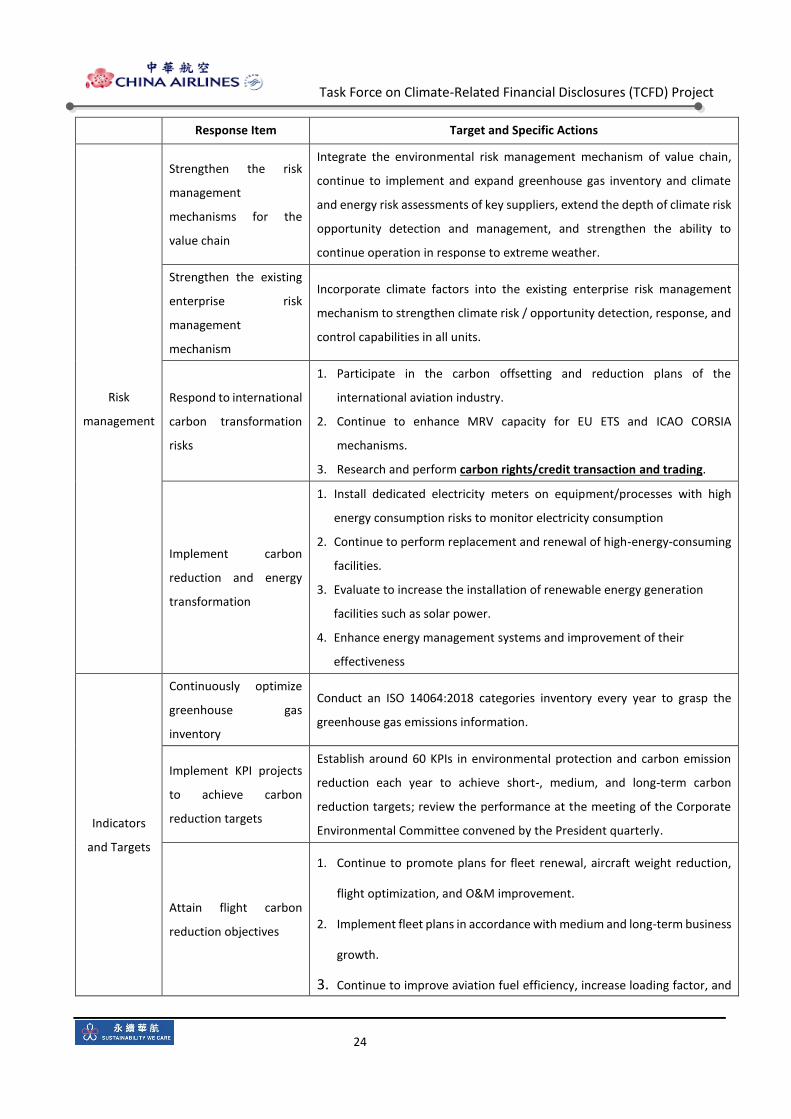

Risk

management

Strengthen the risk

management

mechanisms for the

value chain

Integrate the environmental risk management mechanism of value chain,

continue to implement and expand greenhouse gas inventory and climate

and energy risk assessments of key suppliers, extend the depth of climate risk

opportunity detection and management, and strengthen the ability to

continue operation in response to extreme weather.

Strengthen the existing

enterprise risk

management

mechanism

Incorporate climate factors into the existing enterprise risk management

mechanism to strengthen climate risk / opportunity detection, response, and

control capabilities in all units.

Respond to international

carbon transformation

risks

1. Participate in the carbon offsetting and reduction plans of the

international aviation industry.

2. Continue to enhance MRV capacity for EU ETS and ICAO CORSIA

mechanisms.

3. Research and perform carbon rights/credit transaction and trading.

Implement carbon

reduction and energy

transformation

1. Install dedicated electricity meters on equipment/processes with high

energy consumption risks to monitor electricity consumption

2. Continue to perform replacement and renewal of high-energy-consuming

facilities.

3. Evaluate to increase the installation of renewable energy generation

facilities such as solar power.

4. Enhance energy management systems and improvement of their

effectiveness

Indicators

and Targets

Continuously optimize

greenhouse gas

inventory

Conduct an ISO 14064:2018 categories inventory every year to grasp the

greenhouse gas emissions information.

Implement KPI projects

to achieve carbon

reduction targets

Establish around 60 KPIs in environmental protection and carbon emission

reduction each year to achieve short-, medium, and long-term carbon

reduction targets; review the performance at the meeting of the Corporate

Environmental Committee convened by the President quarterly.

Attain flight carbon

reduction objectives

1. Continue to promote plans for fleet renewal, aircraft weight reduction,

flight optimization, and O&M improvement.

2. Implement fleet plans in accordance with medium and long-term business

growth.

3. Continue to improve aviation fuel efficiency, increase loading factor, and

Task Force on Climate-Related Financial Disclosures (TCFD) Project

25

Response Item Target and Specific Actions

focus on the development of new technologies and new low-carbon

aircrafts for purchase at an appropriate time.

Increase fuel efficiency

1. Continue to promote aviation fuel-saving operations to increase 1.5% fuel

efficiency each year.

2. Optimizing route planning and develop the most suitable passenger /

cargo fleet in response to the epidemic and international development

trends.

Task Force on Climate-Related Financial Disclosures (TCFD) Project

26

Chapter 6. Conclusion

I. Although CAL has committed itself greenhouse gas emission mitigation and adaption, the rising

pressure of climate risks and opportunities have continued to increase. The introduction of

guidelines of the Task Force on Climate-Related Financial Disclosures (TCFD) helps CAL enhance

the identification and management of climate risks and opportunities, and increase business

resilience and low-carbon competitiveness.

II. Based on the short, medium, and long-term impact assessment of climate issues on CAL, we

have identified 7 short-term risks and 10 medium to long-term risks. The main medium to long-

term high-risk issue is sustainable aviation fuel. As sustainable aviation fuel is not readily

available in Taiwan, we need the government’s support with integrated policies and assistance

for industries. We therefore need to continue to lobby industries, the government, and the

academia to help create a development strategy for sustainable aviation fuel in Taiwan.

III. To continue the effective management of the identified climate risks and opportunities, CAL

proposed the core strategies of "creating a TCFD information system", "improving fuel

efficiency", "participating in international carbon management mechanisms", and

"strengthening the emergency response system". We have also promoted 13 major operation

strategies based on the four major TCFD structures for climate governance, strategy, risk

management, and indicators and targets, and implemented rolling management and reported

results to the Board of Directors each year to improve the CAL climate governance and

management.

IV. We will continue to expand and include climate change risks and opportunities to enhance the

value chain and supply chain management mechanisms.