china eastern airlines 2012 interim results announcement · china eastern airlines ... depreciation...

TRANSCRIPT

1

China Eastern Airlines

2012 Interim Results

Announcement

(IFRS)

2012.09.03

2

This presentation contains forward-looking forecast and statements that reflect

the presenting company’s current opinions on future events and its future

financial performance. These opinions were based on certain assumptions,

which were determined by various risk factors and subject to change. This

presentation does not give the assurance that the events predicted will actually

occur, the forecast will materialize, or the assumptions made were correct. The

actual results may deviate materially from the forecast.

This presentation is prepared under IFRS. Except for otherwise stated, 1H2012,

2011 and 2010 financial and operating figures include Shanghai Airlines

Company Limited, while 2009 and prior years do not. 2012 financial figures are

VAT-based, while 2011 and prior years are based on business tax.

Disclaimer

3

1H12 Market Analysis

1H12 Operating Results

2H12 Operating Plan

4

1H2012 Internal / External Environment

Challenges Opportunities

Macro economy

Industry development

Slower global economic recovery,

weakness in mature markets such

as US and EU, and slower GDP

growth in China

Global oil prices remain high

The pace of RMB appreciation

slowed down, with the exchange rate

turning downward in 1H2012

Per capita income of domestic

residents continued to rise, with the

wealth effect further released

Monetary policies further liberalized

with interest cut

The cargo market remains weak. In

1H2012, the airline industry delivered a

total cargo and mail traffic of 2.525

million tons, down 5.0% on a YoY basis

The impact from high-speed rails has

been normalized

In 1H2012, the domestic airlines

industry witnessed a total traffic of

151 million person times, up by 8.7%

on a YoY basis

Outbound tourists totaled 38.5

million, up by 19% on a YoY basis,

and demand on international routes

remains robust

The global economic environment turned out to be more complicated in 2012, bringing

both opportunities and challenges to the industry. The passenger market continues to

grow steadily, yet the cargo market remains relatively weak.

5

1H2012 Market Features

Slower passenger demand growth

Less business travelers, yet more tourists and casual travelers

The demand dynamics are changing rapidly, demonstrating stronger

seasonal characteristics

The yield of domestic routes has been improved

The operating capability of international routes has been enhanced,

with the passenger load factor substantially improved

Regional routes:Hong Kong routes shrank while Taiwan routes

increased

The cargo market remains weak

1

2

6

Optimize the capacity allocation based on

changing market dynamics 1

2 Tap into our business potentials with

innovative product offerings

3 Expand customer resource by strengthening the

construction of transportation hubs

Key Operating Strategies in 1H2012

7

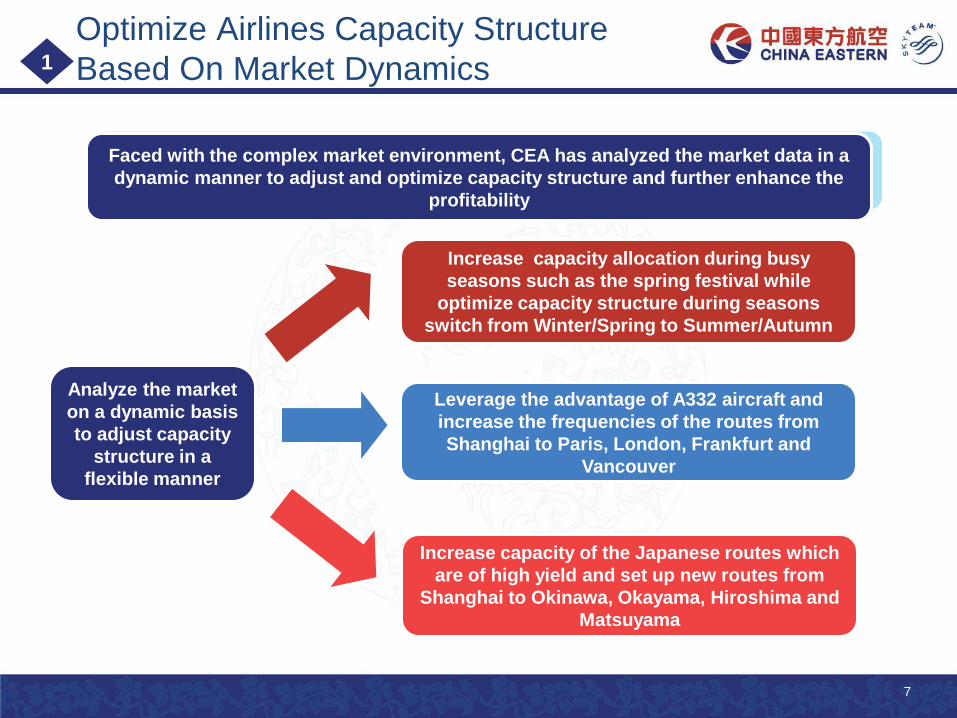

Optimize Airlines Capacity Structure

Based On Market Dynamics

Faced with the complex market environment, CEA has analyzed the market data in a

dynamic manner to adjust and optimize capacity structure and further enhance the

profitability

1

Analyze the market

on a dynamic basis

to adjust capacity

structure in a

flexible manner

Increase capacity allocation during busy

seasons such as the spring festival while

optimize capacity structure during seasons

switch from Winter/Spring to Summer/Autumn

Leverage the advantage of A332 aircraft and

increase the frequencies of the routes from

Shanghai to Paris, London, Frankfurt and

Vancouver

Increase capacity of the Japanese routes which

are of high yield and set up new routes from

Shanghai to Okinawa, Okayama, Hiroshima and

Matsuyama

8

Innovate On Products to Tap

Operation Potential 2

Promote new products

according to the

seasonal and regional

market features Cooperate with

railway bureau to

enhance market

control in the Yangtze

River Delta

Accelerate launches of

core products

1

Innovate on products to

increase profitability

2

3

9

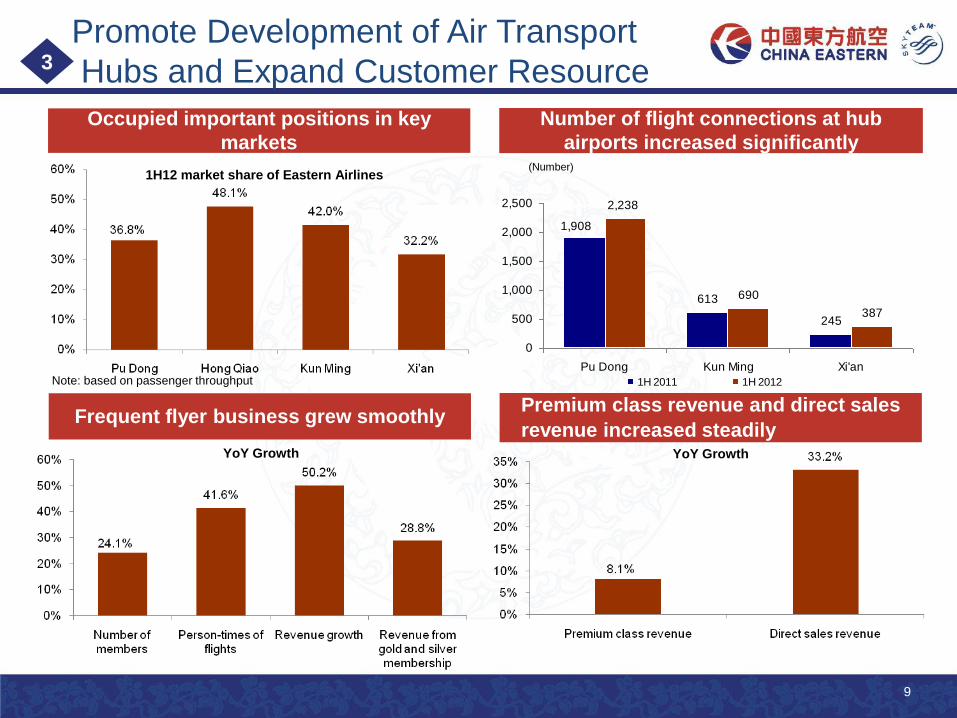

613

245

690

387

1,908

2,238

0

500

1,000

1,500

2,000

2,500

Pu Dong Kun Ming Xi'an

1H 2011 1H 2012

Premium class revenue and direct sales

revenue increased steadily

Promote Development of Air Transport

Hubs and Expand Customer Resource

Occupied important positions in key

markets

Note: based on passenger throughput

1H12 market share of Eastern Airlines

Number of flight connections at hub

airports increased significantly (Number)

Frequent flyer business grew smoothly

YoY Growth

3

YoY Growth

10

1H2012 Cargo Business

Facilitate

M&A among

subsidiaries

Transform

into a

logistics

service

provider

Shanghai Eastern

Logistics Co., Ltd.

Improve the

value chain of

logistics

Connect air

transport with

land transport

Provide

holistic

logistics

solution

Accumulate

customer

resources

11

1H12 Market Analysis

1H12 Operating Results

2H12 Operating Plan

12

1H2011 1H2012 YoY Change

Available tonne-kilometers (ATK) (million)

8,801 9,537 8.36%

Available seat-kilometers (ASK) (million)

62,299 65,191 4.64%

Available freight tonne-kilometers (AFTK) (million) 3,194 3,670 14.89%

Revenue tonne-kilometers (RTK) (million) 6,251 6,861 9.75%

Revenue passenger-kilometers (RPK) (million)

48,564 51,546 6.14%

Revenue freight tonne-kilometers (RFTK) (million)

1,921 2,267 18.00%

Passenger number (1,000) 33,246 34,614 4.12%

Cargo freight volume (million kilogram) 666 682 2.37%

Number of aircrafts 362 395 9.12%

Passenger load factor (%) 77.95 79.07 1.12pts

Freight load factor (%) 60.14 61.77 1.63pts

Daily utilization (hours) 9.8 9.7 -1.02%

Selected Operating Data

13

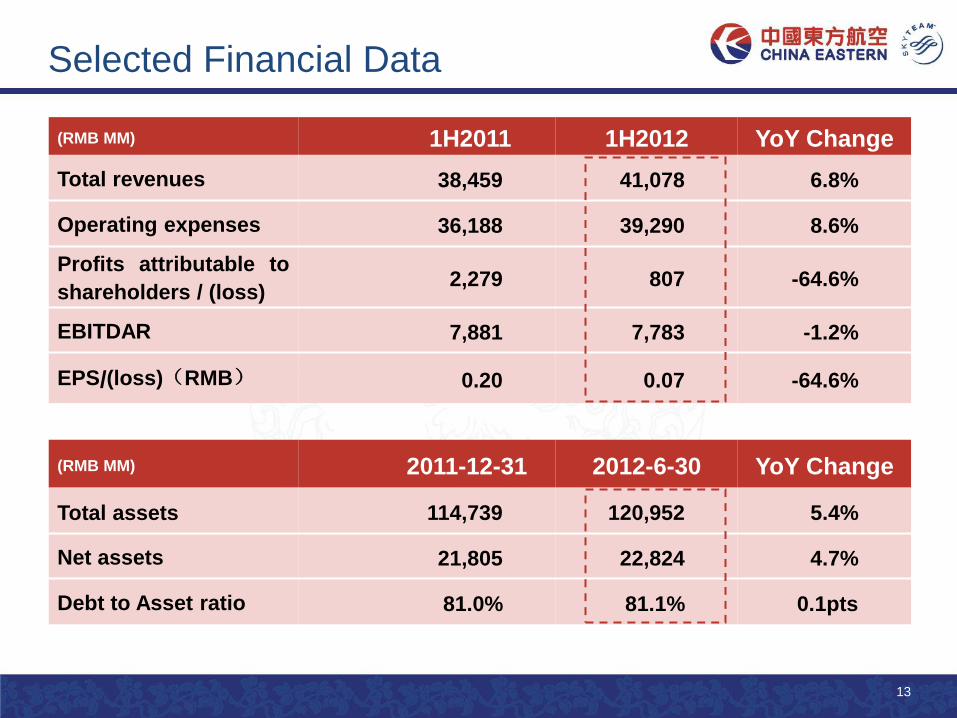

(RMB MM) 1H2011 1H2012 YoY Change

Total revenues 38,459 41,078 6.8%

Operating expenses

36,188 39,290 8.6%

Profits attributable to

shareholders / (loss) 2,279 807 -64.6%

EBITDAR 7,881 7,783 -1.2%

EPS/(loss)(RMB)

0.20 0.07 -64.6%

(RMB MM) 2011-12-31 2012-6-30 YoY Change

Total assets 114,739 120,952 5.4%

Net assets 21,805 22,824 4.7%

Debt to Asset ratio 81.0% 81.1% 0.1pts

Selected Financial Data

14

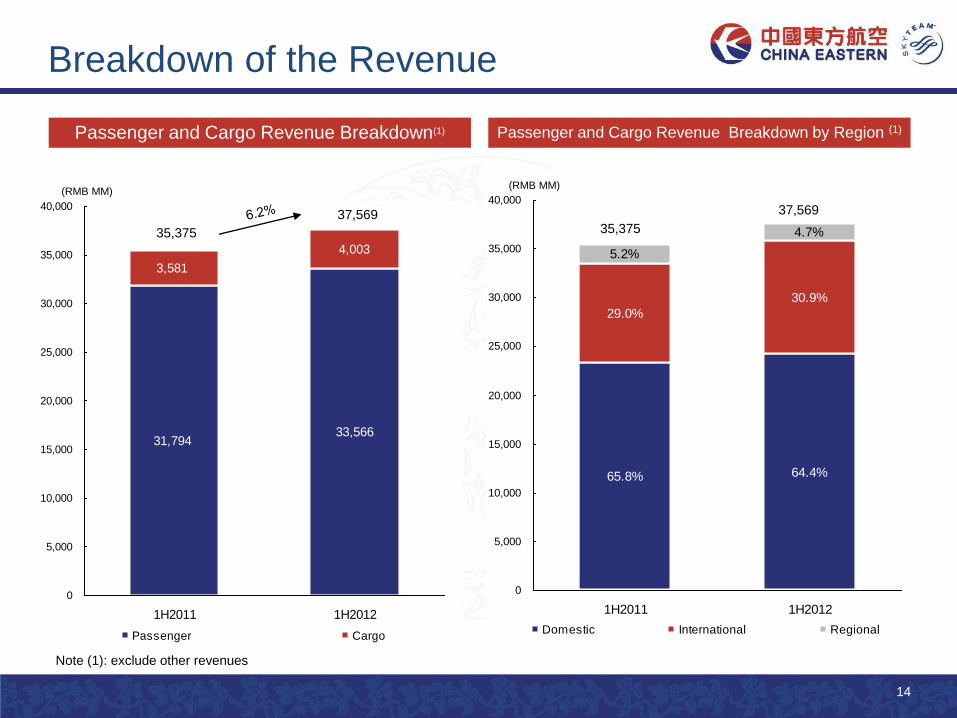

31,79433,566

3,581

4,003

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1H2011 1H2012

Passenger Cargo

Passenger and Cargo Revenue Breakdown(1) Passenger and Cargo Revenue Breakdown by Region (1)

Breakdown of the Revenue

Note (1): exclude other revenues

(RMB MM)

65.8% 64.4%

29.0%

30.9%

5.2%

4.7%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1H2011 1H2012

Domestic International Regional

(RMB MM)

35,375

37,569 35,375

37,569

15

35.375

37,569

2,009

588

889(1,292)

33,000

34,000

35,000

36,000

37,000

38,000

39,000

40,000

1H2011 passenger and cargo revenue

Capacity Load factor Price VAT impact 1H2012 passenger and cargo revenue

35.375

37,569

2,624

929

(66)

(1,292)

33,000

34,000

35,000

36,000

37,000

38,000

39,000

40,000

1H2011 passenger

and cargo revenue

Domestic factor Int'l factor Regional factor VAT impact 1H2012 passenger

and cargo revenue

Factors Contribution by Region (1)

Driving Factors Contribution (1)

Revenue Change

Note (1): exclude other revenues

(RMB MM)

(RMB MM)

16

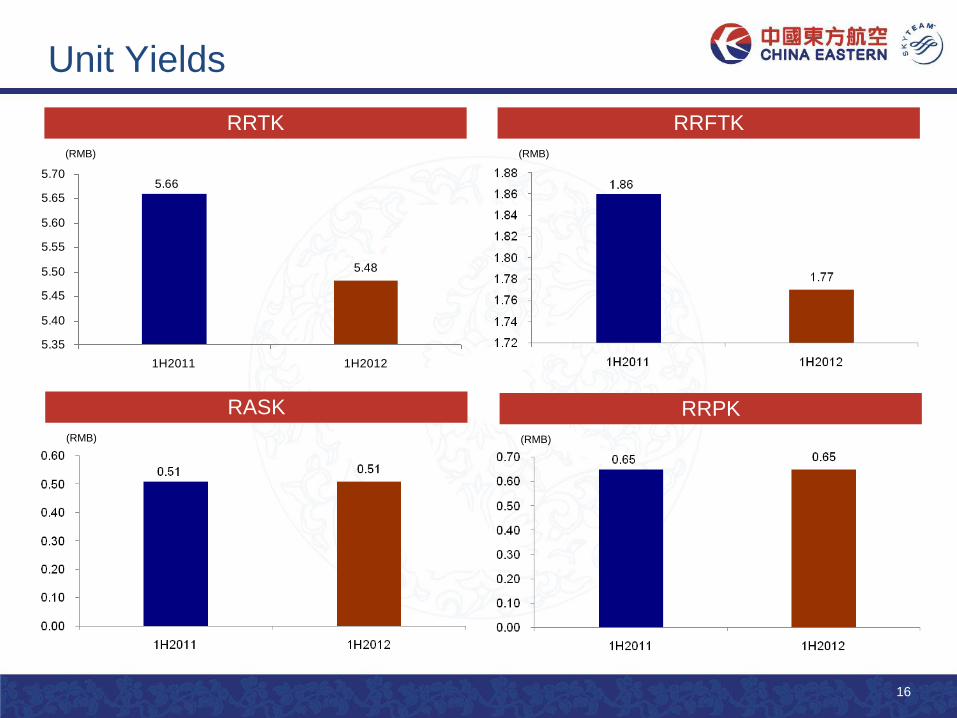

Unit Yields

RRPK

(RMB)

RRFTK

(RMB)

RRTK

(RMB)

5.48

5.66

5.35

5.40

5.45

5.50

5.55

5.60

5.65

5.70

1H2011 1H2012

RASK

(RMB)

17

Aircraft fuel

37%

Compensation

11%Landing fee

11%

Depreciation and

amortization

9%

Administration

8%

Aircraft

operational lease

5%

Maintenance

6%

Selling expense

4%

Others

9%

37.3%37.0%

62.7%

63.0%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1H2011 1H2012

Aircraft fuel cost Other costs VAT impact

Cost Scale (1) Cost Structure (2)

Cost Scale and Structure Analysis

36,188

39,290

(RMB MM)

Note(2): the VAT impact is not excluded from the cost structure Note(1): the contribution of aircraft fuel cost and other costs in total

and the total cost growth do not consider the VAT impact

18

Profit Change Analysis

(RMB MM)

19

1H12 Market Analysis

1H12 Operating Results

2H12 Operating Plan

20

Fleet Plan and Capacity Structure

2H12 Self Owned and

financial lease Operating lease

Aircraft New Delivery 17 8

Aircraft Disposal — 4

Capex (RMB 100 MM) 126 —

2H12 Domestic International Regional

ASK breakdown 72% 25% 3%

Added ASK breakdown 69% 31% —

21

Key Markets in 2H12

Europe

America

Africa

Oceania

Japan