clear out the clutter - gxs inc. · clear out the clutter: modernizing corporate-to-bank...

TRANSCRIPT

+

Clear out the clutter: Modernizing corporate-to-bank communications

+ Clearing out the clutter

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

2

+ Agenda

Introduction

SEPA

PSD II

EBICS

SWIFT CGI and ISO 20022

Clearing out the clutter

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

3

+ The dawn of a new era for C2B communication Are you ready?

Developments in the corporate to bank communication space are changing global commerce.

SEPA and PSD2 will directly effect consumers, corporates, and banks.

Competition

Consumer protection and choice

Transparency

Changes in Europe are significant for non-EU corporates and banks too.

… Although European banks and technology providers mitigate these challenges.

SAAS and cloud computing are enabling new operational and service models.

Communication is changing to match the demands of modern payment methods.

Legacy standards appear to be in their last technology cycle.

Numerous initiatives are looking to help banks and corporates bridge the gap to ISO 20022.

Protocols are undergoing similar changes

Large corporates are being courted aggressively by SWIFT

Many corporates also wish to use communication standards such as EBICS

The variety is overwhelming.

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

4

Technology drivers Business drivers

+ 5

2013 2015 2016 2014 2017

1 November

Ban on cross-border direct debit interchange fees

1 February

Migration end date for credit transfers

Migration end date for direct debits

Mandatory communication of beneficiary’s BIC for domestic transactions (SCT & SDD)

Customer bulk flows & conversion services for free

1 February

Migration end date for niche products (CT & DD products)

Mandatory use of ISO 20022 XML standard for customer bulk transfers and end of transition period for IBAN

1 February / 31 October

Migration deadline for non-Euro countries

SEPA is just a beginning!

1 February

Ban on national direct debit interchange fees

The Single Euro Payments Area (SEPA) is an EU initiative aimed at simplifying bank transfers made in Euros. All CTs and DDs sent within the SEPA area will be treated as domestic transfers.

Migration to SEPA direct debit will be challenging and it will have to occur very rapidly (1 February 2014).

All corporates must use the SEPA standard for Euro-denominated payments and collections throughout Europe.

Major changes to business processes and payment systems will be required to ensure corporates are SEPA compliant.

Some member states are not ready to fulfill requirements.

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

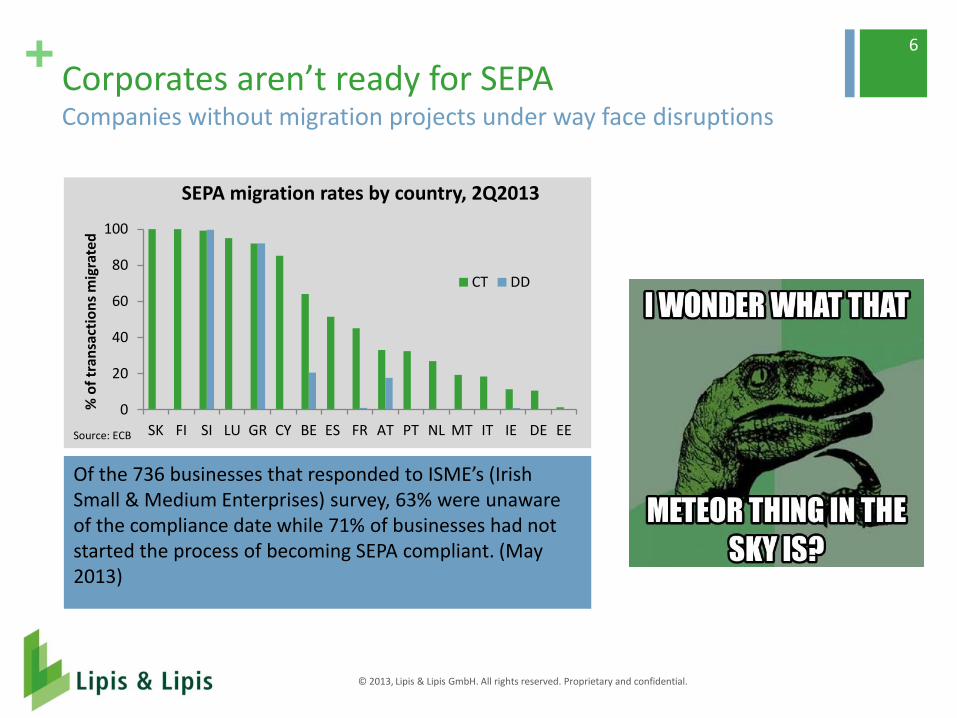

+ Corporates aren’t ready for SEPA Companies without migration projects under way face disruptions

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

Of the 736 businesses that responded to ISME’s (Irish Small & Medium Enterprises) survey, 63% were unaware of the compliance date while 71% of businesses had not started the process of becoming SEPA compliant. (May 2013)

6

0

20

40

60

80

100

SK FI SI LU GR CY BE ES FR AT PT NL MT IT IE DE EE

% o

f tr

ansa

ctio

ns

mig

rate

d

SEPA migration rates by country, 2Q2013

CT DD

Source: ECB

+ Not migrating will disrupt cash flow

27%

19%

3%

16%

6%

16%

0% 10% 20% 30%

≤ 5 days

5-15 days

15-25 days

25-50 days

50-75 days

75 days

46% of companies will have cash flow problems within 2 weeks!

Broadly speaking the technical requirements for corporates will be:

Migrating to an ISO 20022 compatible XML format

BIC / IBAN conversion

Depending on the number of direct debits, some kind of mandate management solution

Business and IT changes to support new workflows

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

7

Imagine that your organization will not be able to migrate to SEPA direct debit by 1 February 2014. How long could your organization abstain from using direct debits without risking liquidity problems?

Source: ibi research: SEPA Umsetzung in Deutschland. n=178 – only organizations which use SEPA direct debit or plan to do so.

+ SEPA DD compliance is complex For non-Euro corporates, a strong IT strategy is essential

Conversion and enrichment of existing data from national / legacy format to XML

Support for transaction files in any national / legacy format.

File transfer to the bank (connectivity)

Automatic display of failed direct debits

Mandate collection and conversion for direct debits

Reporting and reconciliation support

Higher transaction costs

Banks offer legacy format conversion but prices are high

Compliance risk

Technically, banks are not allowed to convert files from national format to SEPA. But most are anyway…

Risk is unknown

Assuming that SEPA workflows are the same as national payment workflows

SEPA DD is quite different

Mandate migration takes up to a year

Some can’t be migrated and may need to be re-authorized.<<<<

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

8

Potential pit-falls Technical support required

+ PSD to PSD II: What’s new?

The European Commissions’ Payment Services Directive is a regulatory initiative that regulates payment services and services providers throughout the EU and European Economic Area (EEA).

The original purpose of the PSD:

Facilitate SEPA development

Regulate payment institutions (including non banks)

Ban interchange fees

Ban surcharges for consumer cards

Increase transparency, consumer protection

Increase competition

The PSD II covers new services (and service providers) enabling access to consumer accounts.

The legislation requires third party payment initiation services to be regulated and supervised as payment institutions.

The expanded scope targets developments in mobile payment applications and B2B transfers (like Dutch iDEAL) to bring them under the legislative umbrella of the PSD.

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

9

Original PSD PSD II

+ PSD 2 covers “one leg out” transactions Money being sent into or out of the EU will now fall under PSD rules

Rules regarding transparency of fees and information provision will now apply to “one-leg-out” transactions and any transaction made in Euros or other EEA currencies.

The original PSD only covered transactions where both PSPs were located in the EU.

New rule will allow consumers to compare services among PSPs and will provide more protection to transactions coming into or out of the EU (for example remittances).

Banks doing business in Europe will have to provide more detailed information to consumers and will face competition on fees and charges due to the added transparency.

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

10

+ PSD II regulates PSPs that use innovative channels Regulating third party processors will bring new service options

TPPs are defined as services that debit one party’s account and credit another party’s, and where the processor does not maintain either account.

TPPs are currently unregulated under the initial PSD

This raises questions about security, liability, and data protection

Under PSD 2, TPPs will have to be licensed and supervised as payment institutions

This will allow TPPs to have direct access to consumer accounts

An effort to keep up with developments in m-payment applications and B2B transfers

Corporates will have more options when it comes to choosing payment institutions

Could open up new channels for corporate payments, as banks have been slow to offer mobile payment solutions for customers

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

11

Effect on payment industry

Effect on corporates

+ EBICS supports multi-national corporates The need for a common protocol is necessary as banks follow corporates into new geographies

The 'Electronic Banking Internet Communication Standard' (EBICS), is a communication framework adopted by the French and German banking sectors.

All major French and German banks support the protocol.

Adoption rates are high, due to low cost, improved functionality, and industry coercion.

Treasurers can also connect via SWIFTNet or web-based portals provided by the bank itself.

For the French and German communities, EBICS provides reliability and SEPA interoperability and is becoming the default C2B standard.

EBICS was designed to function as a secure communication channel to initiate SEPA Direct Debits and SEPA Credit Transfers using the Internet.

EBICS is an open standard which supports standard or customized software to initiate payments.

EBICS is being promoted for adoption on a pan-European scale

Cheaper than SWIFTNet

Interoperable with most data standards.

EBICS may emerge as the single C2B standard for exchanging ISO 20022 messages securely.

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

12

+ SWIFT CGI leads ISO 20022 corporate initiatives

SWIFT’s Common Global Implementation (CGI) allows corporates to use one message structure to interact with banks using ISO 20022 based file formats.

CGI reduces costs and simplifies implementation processes for corporates managing multiple bank relationships

60+ countries use CGI standards

SCORE (Standardized Corporate Environment) is a SWIFT based cash management C2B tool that supports multiple data formats.

Of the total Q1 2013 figures for SCORE, 27% of all payment files use ISO 20022 and the percentage is increasing.

300 corporates using SCORE initiate payments with ISO 20022 and 34 received ISO based reporting messages.

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

13

+ Examples of ISO based C2B initiatives globally

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

The Italian CBI connects corporates of all sizes to their banks. CBI supports ISO

20022 for domestic and cross-border payments. ISO makes up 53% of their CT traffic and pending SEPA DD migration,

only 3% of direct debits.

The Russian initiative CMPG ISO 20022 is in the testing phase to support

corporate financial messaging in cooperation with SWIFT CGI and the Central Bank of Russia.

Over 18 banks will support the service once

implemented.

Denmark’s largest corporates have moved to ISO 20022. Under the umbrella of the Danish

Banking Association, XML message implementation has been harmonized

amongst banks and vendors.

Finland’s SEPA migration required full migration to ISO 20022 for corporate to bank payment initiation and messaging. All legacy formats were replaced. Banks

must be fully migrated for customer reporting in ISO 20022 by Q1 2014.

SUSA (SWIFT users of South Africa) is an initiative that supports ISO based message communication

between a small number of South African corporates and the four major SA banks.

Note: SEPA solely implements the ISO 20022 data format. All 28 EU member countries use IS0 20022 for payment initiation and messaging.

14

+

Solution

Examine payment flows and how best to manage banking relationships

Re-consider connectivity options SWIFT – direct or via bureau Direct to each bank Web-based Third party

Unify communications formats and channels across many relationships EBICS only covers part of Europe,

but can cover all of SEPA Update payment software Consider managed services to reduce

complexity.

Clearing out the clutter for EU treasurers

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

15

Problem

Complexity is bewildering and overwhelming. Legacy formats and protocols are deeply

rooted. Different size corporates will deal with this in

different ways Large go to SWIFT Mediums go to EBICS or other national /

regional solutions Small stay with bank-centric solutions

+

Solution

Simplify the process for clients and hide the complexity.

Consider this a compliance exercise. Support all three basic connectivity

strategies for corporates Non-EU banks should re-evaluate

relationships for sending and receiving payments in the EU Identify payment flows to SEPA

countries Relationships with national

clearing systems and some correspondents

Clearing out the clutter for financial institutions

© 2013, Lipis & Lipis GmbH. All rights reserved. Proprietary and confidential.

16

Problem

European FIs are dealing with most of these issues as matters of compliance.

All EU FIs are SEPA ready., PSD compliant, and offering modern connectivity options.. If you do not modernize, your clients

will look elsewhere. Non-EU banks need to address these issues

as if they were MNCs A few may view Europe strategically,

and may be more like EU banks. The pace of change will not slow. The key

issue is not just how to comply, but in a flexible, future-proof manner.

Slide 17

Modernizing Corporate-to-Bank Communications Case Studies

Slide 18

Multi-National Manufacturing Company SWIFT Service Bureau Case Study

Business Challenge • Implementing new Treasury Management

System

• Seeking flexibility to connect to banks via

SWIFT or directly

• Electronic distribution of payroll, A/P, wire

transfers, international payments

• Intra-day and end-of-day account

statements to understand cash positions

• Approximately 200 accounts at 16

different banks worldwide

Solution • 7 Direct connections to banks via

Managed Services

• Connectivity to 16 banks via SWIFT

Service Bureau

• On-boarding of banks worldwide

• Mapping of data to/from SAP A/P and A/R

applications

• Centralized tracking of all files

Treasury

Management

System

ERP System

Accounts Payable

Accounts Receivable

SWIFT

Service Bureau

Direct Internet

Connection

Managed Services

Slide 19

US Regional Bank SWIFT Service Bureau Case Study

Business Challenge

• Meeting SWIFTNet delivery and SWIFT

format requirements of multi-national

corporate clients for wire payments and

balance reporting

• Bank applications unable to consume

SWIFT formats

• Imminent go-live deadline

Solution

• Managed Services translation

− MT101 – EDI 820

− BAI2 – MT940 / MT942

• Connectivity via SWIFT Service Bureau

• Corporate on-boarding

• Enables additional large corporate

business

Corporate Clients

SWIFT

Service Bureau

MT101

Managed Services

MT940

MT942

820 BAI2

Managed Services

Slide 20

Case Study: Global Transaction Bank Connectivity Options For Your Global Client Base

Business Challenge

• Client was experiencing increased corporate

adoption of EBICS as a preferred

communications protocol for bank connectivity

• Client’s existing French-specific EBICS solution

was not strategic and not scalable to meet pan-

European needs

Solution

• Added EBICS as a communications protocol to

the existing Managed Services host-to-host file

channel already in place for the bank

• Implemented file splitting to route SEPA Direct

Debits to Mandate Management vendor

Business Benefits

• The bank was able to leverage their existing file

channel to meet their customers’ demands

without the need to invest in an additional

communications infrastructure

Corporate Clients

EBICS-as-a- Service

Managed Services

Payment & Direct Debit

Files (BAU)

Reporting & Control Files

(BANSTA, FINSTA,

CONTROL)

H2H

SAP FSN

SEPA DD

Mandate

Management

EUR Direct

Debits (only) Payment &

SDD Files

SEPA

Payments

Engine

Slide 21

For More Information

Patricia Hines, CTP Director, Financial Services

Industry Marketing

GXS

+1 704 969 0763

www.gxs.com

Leo Lipis Managing Director

Lipis & Lipis GmbH

+49 30 8892 2049

www.lipis.net

www.corporatetobank.com