china market outlook - umtri ihs automotive, lv global segmentation, ... oems moving to emerging...

TRANSCRIPT

© 2016 IHS Markit. All Rights Reserved.© 2016 IHS Markit. All Rights Reserved.

China Market OutlookVolume Growth Engine to the Global Automotive Industry

UMTRI: Ann Arbor, Michigan | 9 November 2016

Mike Jackson, Senior Executive

North America, Vehicle Production Forecasting

+1-248-388-8912

© 2016 IHS

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

World UnitedStates

Japan Eurozone Brazil Russia India China UnitedKingdom

2015 2016 2017 Avg 2018-2023

Global Growth Set to Rise in 2017US Economy Gains as Brazil/Russia Start Recovery

GD

P g

row

th r

ate

%

World average

2016 = 2.4%

World economic growth rates

Source: IHS

© 2016 IHS 3

8890

9194

105

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

50

60

70

80

90

100

110

200

1

200

3

200

5

200

7

200

9

201

1

201

3

201

5

201

7

201

9

202

1

202

3

World Light Vehicle Sales ForecastMarket will reach 100 million by end of the decade; growth peak is approaching

Source: IHS Automotive sales forecasts

Annual LV sales (millions)

3

Annual growth (%)

Average growth 3.2%

Growth rate peaks

in 2019

© 2016 IHS

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

20

12

20

13

20

14

20

15

20

16

20

17

20

18

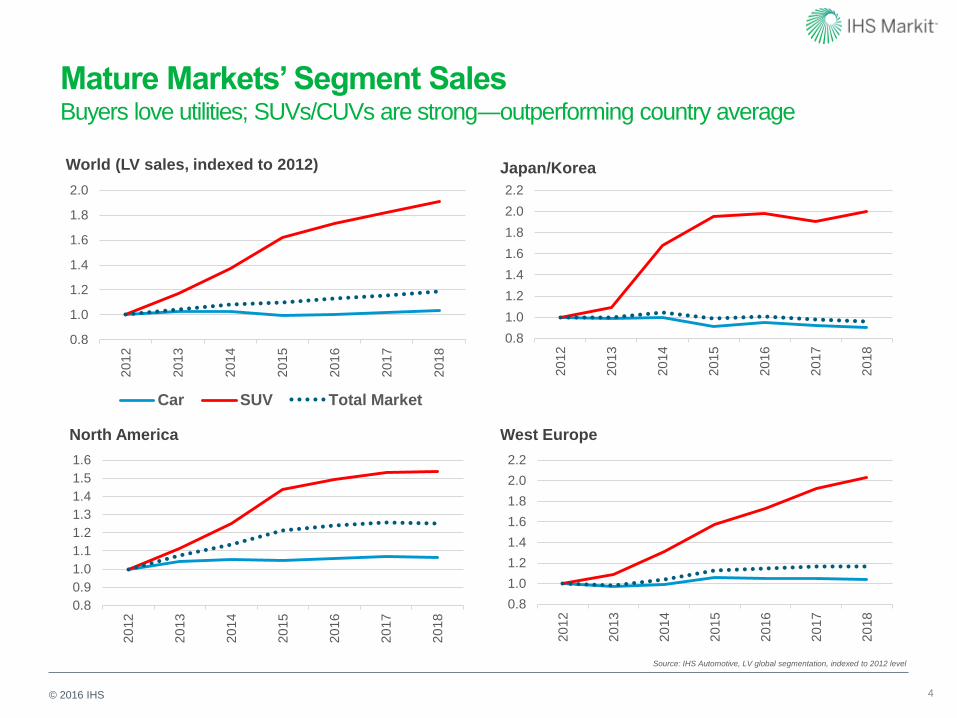

Mature Markets’ Segment SalesBuyers love utilities; SUVs/CUVs are strong―outperforming country average

4

0.8

1.0

1.2

1.4

1.6

1.8

2.0

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Car SUV Total Market

West Europe

Japan/Korea

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

20

12

20

13

20

14

20

15

20

16

20

17

20

18

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

20

12

20

13

20

14

20

15

20

16

20

17

20

18

North America

World (LV sales, indexed to 2012)

Source: IHS Automotive, LV global segmentation, indexed to 2012 level

© 2016 IHS

Developing Markets’ Segment SalesUtilities are strong―even in weaker markets

5

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Brazil (LV sales, indexed to 2012) China

0.4

1.0

1.6

2.2

2.8

3.4

20

12

20

13

20

14

20

15

20

16

20

17

20

18

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

20

12

20

13

20

14

20

15

20

16

20

17

20

18

India Russia

Source: IHS Automotive, LV global segmentation, indexed to 2012 level

0.4

0.6

0.8

1.0

1.2

1.4

1.6

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Car SUV Total Market

© 2016 IHS. ALL RIGHTS RESERVED.

60

91

106

50

60

70

80

90

100

110

2007 2009 2011 2013 2015 2017 2019 2021 2023

Millio

ns 15million

6

Beyond the RecoveryGlobal Production Growth 2016 - 2023

32million

6.6

4.3

2.0

1.2

0.8

0.6

-0.5

-2 0 2 4 6 8 10

Greater China

South Asia

Europe

South America

Middle East/Africa

North America

Japan/Korea

Millions

© 2016 IHS Markit. All Rights Reserved.

0

5

10

15

20

25

30

35

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023

Mill

ions

Sep 2015 FC Sep 2016 FC

Not enough weak data points to call a trend break in the strong relationship of key drivers to automotive sales:- headline GDP- average income- disposable income growth- urban population employment growth Stock market volatility is real, yet less market level.

The auto stimulus program (from October 2015) boosts short term

China Light Vehicle Sales OutlookAutomotive Conference – Shanghai | October 2016

• Termination of tax incentives

• GDP growth rate of 6.2% in 2017

• The government could usher in vehicle demand management because of rising energy security concerns

• Vehicle Purchase Tax cut from 10% to 5% for vehicles (1.6L and below) in October 2015–December 2016

• Improving GDP growth of 6.6% in 2016

• GDP growth to trough out from 2018 with an average growth of 6.4% in 2018–20

• Supported by replacement demand coming from scrappage of vehicles (Euro I and below) in 2014–17

© 2016 IHS Markit. All Rights Reserved.

8

Economy vs. Car Sales: City Tier DevelopmentTier 4–Tier 6 cities market shares increase with Tier 1 share declining

T1

13%

T1.5

13%

T2

13%

T3

24%

T4

10%

T5

15%

T6

12%

T1

6%T1.5

12%

T2

13%

T3

24%

T4

11%

T5

18%

T6

16%T1

12%

T1.5

12%

T2

12%

T3

21%

T4

11%

T5

18%

T6

14%

T1

12%

T1.5

12%

T2

12%

T3

21%

T4

11%

T5

18%

T6

14%

2010

GDP share by city tier 2010–15

2010

2015

2015

PV market share by city tier 2010–15

Automotive Conference – Shanghai | October 2016

© 2016 IHS Markit. All Rights Reserved.

354

915

435463 448

233

282

463

0

100

200

300

400

500

600

700

800

900

1,000

United

States

China Japan Germany France India Brazil Russia

9

Product Nameplates – LV Sales OEMs moving to emerging market quickly to gain customers

Number of nameplates 2006–23

© 2016 IHS MarkitSource: IHS Markit

Automotive Conference – Shanghai | October 2016

© 2016 IHS Markit. All Rights Reserved.

10

Body Type DiversitySUV sales keeps expanding over-proportionally in long term

13%

47%15%

11%

10%36%

34%

13%

9%

4%

SUV Hatchback

Sedan Wagon

MPV Coupe

Convertible Roadster

38%

44%

3%

7%4%

45%

39%

8%3%

SUV Sedan

Hatchback MPV

Coupe Wagon

Convertible Roadster

12%

65%

18%

5%

44%

39%

8%8%

SUV Sedan

Hatchback MPV

Wagon Coupe

Convertible

2010

CHINA North America EUROPE

2010 2010

2025 2025 2025

The Slowdown and the Stimulus in China / October 2016

© 2016 IHS Markit. All Rights Reserved.

11

Production - Long-term DevelopmentSlowing down gradually after 2019, a decline still not expected

Production volume development

© 2016 IHS MarkitSource: IHS Markit

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

30

35

Millio

ns

PV LCV Growth rate y/y

Growth phase Mature phaseAdjustment phase

The Slowdown and the Stimulus in China / October 2016

© 2016 IHS Markit. All Rights Reserved.

4

4.5

5

5.5

6

6.5

7

7.5

8

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Q1

2016

Q2

2016

Q3

2016

Q4

2016

Q1

2017

Q2

2017

Q3

2017

Q4

2017

Q1

2018

Q2

2018

Q3

2018

Q4

2018

Millions

Tax policy ends in 2016 Tax policy ends in 2017

Seasonality abnormality from 2015 to 2017

© 2016 IHS MarkitSource: IHS Markit

12

Scenarios by Stimulation of Tax-cut PolicyExpiration of Tax-Cut Policy as main impact

Growth RatePolicy ends 2016 Policy ends 2017

2014: 8.1% 2014: 8.1%2015: 4.7% 2015: 4.7%2016: 7.5% 2016: 6.5%2017: 1.0% 2017: 3.0%2018: 3.0% 2018: 1.0%

200-300K units shift from Q42016 to 2017

+1%

-3%

The Slowdown and the Stimulus in China / October 2016

© 2016 IHS Markit. All Rights Reserved.

Risk & Reward: Over Capacity

13

Capacity development

Source: IHS Markit © 2016 IHS Markit

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

5

10

15

20

25

30

35

40

Millions

Production Over capacity % Utilization

?4,

000,

000,0 00,0

00CNY

Investment!

The Slowdown and the Stimulus in China / October 2016

14

Greater China Output +6.6M

© 2015 IHS

G315%

US314%

A416%

Other55%

Contributionto Growth %

4.4 5.4

2.83.7

5.46.4

13.2

16.8

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2012 2014 2016 2018 2020 2022

Millio

ns

Other Asian4 US3 German3

© 2016 IHS Markit. All Rights Reserved.

Modular Platforms of JV & China OEMsTotal number of platforms increase, while decrease per OEM by modular platform

The Slowdown and the Stimulus in China / October 2016

JV Brand Local BrandJV & Local Brands

© 2016 IHS Markit. All Rights Reserved.

New OEM entrances and brand expansionNew entrants from other industries drives brand expansion

Existing small OEMs

Mega Tech Companies

New OEMs

Sharing Economy

Brand number

2000 2010 2015 2025

25 62 78 94

The Slowdown and the Stimulus in China / October 2016

© 2016 IHS Markit. All Rights Reserved.

Capacity expansion in ChinaJV brands and COEM - NEV is a main driver for future capacity expansion

17

Volkswagen - Qingdao & TianjinFord – HarbinPSA – ChengduFCA – GuangzhouHyundai – Cangzhou & ChongqingHonda – WuhanRenault – WuhanKarma - HangzhouTesla – ?

BAIC - Huanghua & RuiliGeely – Baoji, Jinzhong Zhangjiakou & GuiyangGAIG - UrumqiChery – ChangshuFDG – HangzhouHanteng – ShangraoJoylong – YangzhouNEXTEV – HefeiShaolin – ZhengzhouCH-Auto - Suzhou

2M

1.3M

Harbin

Tianjin

Qingdao

Zhangjiakou

Suzhou

Changzhou

Hangzhou

Guangzhou

Quanzhou

Ruili

Guiyang

Chengdu

Chongqing Wuhan

Shangrao

Cangzhou

Huanghua

Baoji

Jinzhong

Zhengzhou

Hefei

Yangzhou

Urumqi

The Slowdown and the Stimulus in China / October 2016

© 2016 IHS Markit. All Rights Reserved.

China OEM expansion in Overseas MarketsNew plants and R&D centres, establishment reflect COEMs ambitions

SAIC: SOP2017

SAIC: SOP2017

GWM: SOP2017

SAIC: SOP2017GWM: SOP2018

Rayong, Thailand

Kaliningrad,Russia

Uzlovaya,Russia

Bekasi, Indonesia

Foton: SOP2017

Pune, India Chery: SOP2016

Manila, Philippines

Lifan: SOP2017

Lipetsk, Russia

Jianghuai: SOP2015

Kostanay, Kazakhstan

Haima: SOP2015

Khorasan, Iran Foton: SOP2015

Gateway Thailand

Changhe: SOP2018

Docharkh, Iran

Jianghuai: SOP2016

Camacari, Brazil

FAW: SOP2015

Algeria

Volvo: SOP2018

Ridgeville,USA

London,Britain

Geely

Silicon Valley,USA

BAIC

Goteborg,Sweden

Volvo

Turin,Italy

ChanganJAC

Birmingham,Britain

SAIC

Tokyo,Japan

Great Wall

Detroit,USA

BAIC

Sao Paulo,Brazil

BYD

San Jose,USA

NEXTEV

R&D

Production facility

The Slowdown and the Stimulus in China / October 2016

© 2016 IHS

Global EV Production

0.0

.1

0.6

0.4

1.8

0%

10%

20%

30%

40%

50%

60%

0.0

0.5

1.0

1.5

2.0

2.5

2012 2014 2016 2018 2020 2022

Millio

ns

NA EV ROW EV NA EV Share China EV Share

CAGR = 27.5%

2023: 1.1M

CAGR = 28.3%

2023: .6M

19 Nameplates

146 Nameplates

Proactive Positioning / September 2016

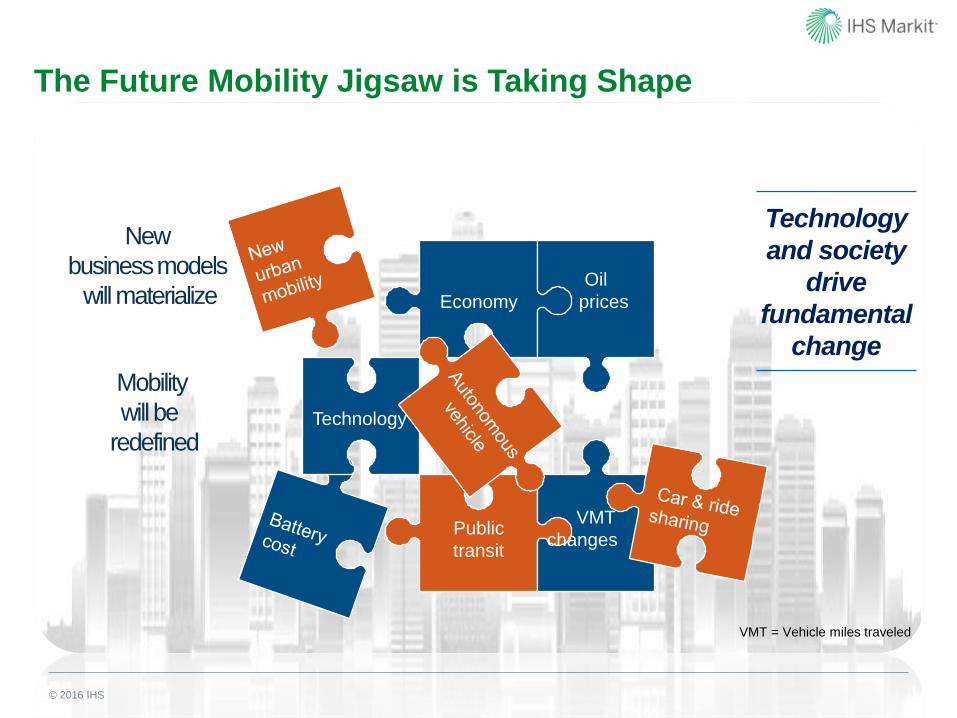

© 2016 IHS

Public

transit

VMT

changes

Economy

Oil

prices

Technology

New

business models

will materialize

Mobility

will be

redefined

Technology

and society

drive

fundamental

change

VMT = Vehicle miles traveled

The Future Mobility Jigsaw is Taking Shape

Automotive Conference – Detroit | 8 September 2016

© 2016 IHS Markit. All Rights Reserved.© 2016 IHS Markit. All Rights Reserved.

Thank You!

Mike Jackson, Senior Executive

North America, Vehicle Production Forecasting

+1-248-388-8912