ch&cie risk regulation and strategy occasional papers number 1 - vfinale - 15122014

TRANSCRIPT

1

© CHAPPUIS HALDER & CIE

Risk, Regulation & Strategy Occasional Papers, N°1.

December 2014

Post-crisis financial reforms and their impact on banking business models and strategies

By Alexandre Kateb

Assisted by Claire Guinot (Paris Office)

Global Research & Analytics1

1This work was supported by the Global Research & Analytics Dept. of Chappuis Halder & Cie. E-mail : [email protected] or [email protected]

© Global research & Analytics Dept.| 2014 | All rights reserved

2

Table of content

Overview and executive summary .......................................................................................... 3

1. Introduction ....................................................................................................................... 4

1.1. Market failures, twisted incentives and negative externalities as the core triggers of the financial crisis ................................................................................................................. 4

1.1.1. The twisted incentives behind the originate-to-distribute banking model .......... 5

1.1.2. Too-big-to-fail institutions, systemic issues and the consequences of moral hazard .................................................................................................................. 6

2. An overview of the global regulatory reform agenda and its results ........................... 8

2.1. The micro-prudential reforms: from Basel II to Basel III .............................................. 8

2.2. Systemic risk, G-SIBs and macro-prudential regulations ............................................ 10

2.3. The move toward more transparency: standardization and centralized clearing of OTC derivatives ..................................................................................................................... 12

3. From spirit to letter: the implementation of financial reforms in the US and EU .... 13

3.1. Separation laws in the United States, the UK and the rest of Europe .......................... 13

3.2. The new supervisory and resolution frameworks in the US, UK and Eurozone .......... 15

3.3. Regulatory equivalence or dual burden? ...................................................................... 17

4. Impact of the reforms on banking strategies and business models ............................ 19

4.1. Funding and liquidity risk management becomes a strategic issue .............................. 19

4.2. A shifting landscape for Capital Markets and Investment Banking ............................. 20

4.2.1. Increased segmentation between Global CIBs, high-end multi-specialists and local corporate banks ........................................................................................ 21

4.2.2. A commoditization and standardization of most cash and derivatives products alongside tailor-made and customized products and services .......................... 22

4.2.3. The de-globalization (or “reverse globalization”) and re-regionalization of the banking industry ............................................................................................... 23

4.3. Toward a renaissance of the “originate-to-distribute” model ....................................... 24

4.3.1. The rebirth of mass-market securitization and its prospects ............................ 24

4.3.2. The direct sell-off of loan portfolios to specialized asset management companies ......................................................................................................... 26

Bibliography ........................................................................................................................... 28

Appendixes ............................................................................................................................. 30

© Global research & Analytics Dept.| 2014 | All rights reserved

3

Post-crisis financial reforms and their impact on banking business models and strategies Overview and executive summary

After a short introduction on the origins and causes of the global financial crisis, we describe in the first part of this paper, the philosophy and the main features of the global financial reform agenda set up by the G20 in the aftermath of the crisis. We discuss micro-prudential reforms (i.e. the Basel III new capital, liquidity and leverage regulations) before elaborating on measures targeting systemic risk and reviewing some macro-prudential proposals. We end this part with a discussion on the new requirements for market infrastructures, and the push for transparency in the trading and post-trading of OTC derivatives.

In the second part of the paper, we analyze the reforms undertaken in the United States and in the European Union (especially in the UK and in the Eurozone). Altogether these two regions of the world still concentrate 80% of the total outstanding global financial assets. In addition, they host the majority of the global systemically important financial institutions (G-SIFIs), and they are home to the two most important financial centers in the world, New York and London. In the United States, the reforms undertaken under the Dodd-Frank Act banner aimed at reinforcing micro-prudential regulations to prevent new bank failures, while drafting at the same time a robust resolution framework for winding down failed large financial institutions – including non-banks. In the European Union, in addition to the implementation of new micro-prudential requirements, the Eurozone sovereign crisis triggered a complete overhaul of the prevailing fragmented financial supervisory framework. The resulting Banking Union, although still incomplete, represents an unprecedented transfer of power from the individual Member-state level to the European level, putting the European Central Bank at the center of the new supervisory regime.

In the third part of the paper, we discuss the potential implications of these new regulatory developments on the business models and strategies of banking institutions, especially in the European Union, following three main lines:

-‐ The transformation of bank internal governance and the rise of integrated Funding and Liquidity Risk Management (FLRM) frameworks which are translated into new operating models and service offerings

-‐ The restructuring and segmentation of banking institutions – especially in the CIB space – as a result of the tradeoff between scale economies and loss-absorption capabilities

-‐ The rebirth of securitization and the sell-off of some banking assets to non-bank financial companies (“shadow banks”) for balance sheet optimization reasons

© Global research & Analytics Dept.| 2014 | All rights reserved

4

1. Introduction

1.1. Market failures, twisted incentives and negative externalities as the core triggers of the financial crisis

The classical view on regulation treats it as a set of incentive contracts within a principal-agent relationship, where the regulator is the principal, and the agent is the regulated firm2. Hence, regulation involves creating incentive-compatible contracts, so that any market failures are corrected, and that regulated firms have an incentive to behave in a way that is consistent with systemic stability and investor protection. Against this theoretical background, it has been often argued that the global financial crisis of 2007-2008, is first and foremost a crisis of the prevailing self-regulation and laissez-faire doctrine, especially in the United States and in the United Kingdom.

Indeed, the general sentiment among policymakers, in the decade running up to the crisis, was that light-touch regulation and large-scale transfer of risk to the markets the through securitization and structuring of banking assets alleviated risk concentration in the banking system, and that it exerted a positive effect on economic growth and job creation through its support to the housing sector3. The repeal of the Glass-Steagall Act of 1933 by the Clinton Administration in 1999 was a direct consequence of this anti-regulation or self-regulation bias4. For its part, the Basel II agreement which allowed financial institutions to use their internal risk models to measure their risks and assess their compliance with the required solvency ratio, was yet another example of this self-regulation bias. And the abundant liquidity flushed out by the Federal Reserve – the so-called “Greenspan put” –, following the crash of the Internet bubble and the mild recession of 2001, blurred further the line between sound business practices and hazardous undertakings.

2 Llewellyn [1999] 3 The same rationale was put forward by the World Bank and IMF to justify financial liberalization in the developing world in the 1980s and early 1990s. It was subsequently watered down following the major emerging markets crises of the 1990s in Mexico, East Asia, Russia, Brazil, Turkey, etc. Cf. Kose et alli [2006]. 4 The repeal of the Glass-Steagall Act following an intense lobbying by Wall Street was achieved through the Gramm-Leach-Bliley Act in 1999.

© Global research & Analytics Dept.| 2014 | All rights reserved

5

1.1.1. The twisted incentives behind the originate-to-distribute banking model

It is well acknowledged that the 2007-2008 financial crisis was triggered by the collapse of the mortgage bubble that ballooned on the back of the “Greenspan put” and the Bush-era fiscal incentives for homebuyers. This mortgage bubble was fueled and amplified by the financial innovations of the time. Indeed, US banks gradually moved from an “Originate and hold” model to an “Originate and distribute” model, in which mortgages that were initially originated by community banks – including the growing volumes of subprime mortgages that were not guaranteed by federal agencies - were pooled and sold to investment banks. The later structured these contracts and sold them in turn to other financial institutions in the form of CDOs5.

The rationale behind that model was that it enabled banks to offload risk from their balance sheets. It contributed to a further expansion of mortgage lending while supposedly preserving financial stability, by diluting risk among a plethora of financial investors. In addition, through the tranching process this model offered to different investors a tailored exposure to the mortgage market with an adjusted risk-return couple that was consistent with their risk tolerance, quest for yield and fiduciary obligations. Some institutional asset managers for example could only invest in AAA-rated securities.

However, as Markus Brunnermeier pointed out6, investment banks actually increased their exposure to liquidity and liability mismatch risk as they granted unlimited liquidity backstops to their off balance-sheet securitization vehicles. At the same time they relied more and more on short term funding. Any reduction in funding liquidity could thus lead to significant stress for those institutions and for the financial system as a whole, through the complex interactions between market liquidity and funding liquidity. Through this nexus, a relatively minor shock to the value of the collateral could cause market and funding liquidity to dry up, and precipitate a full-blown financial meltdown.

5 Collateralized Debt Obligations 6 Brunnermeier [2009].

© Global research & Analytics Dept.| 2014 | All rights reserved

6

1.1.2. Too-big-to-fail institutions, systemic issues and the consequences of moral hazard

In addition, to information asymmetry between investors and borrowers, to ill-conceived incentives for structurers and rating agencies, and to herd behavior in the structured products market, the financial sector was also ripe with another set of market failures, called negative externalities. Indeed, as a result of their hyper-leveraged nature, the profits of financial institutions are captured by their shareholders, while the cost of their failure is ultimately borne by tax payers as it usually exceeds by far the value of their equity and long term debt. This is particularly true for large and complex financial institutions (LCFIs) which could benefit from implicit safety-net arrangements, because they are perceived “too big to fail” (TBTF). However, this implicit bailout guarantee only reinforces the moral hazard problem posed by excessive risk taking that is not backed by adequate risk absorption capabilities.

This was evident in the United States, not only with the major banks, but also with other financial institutions such as the so-called GSEs7, Fannie Mae and Freddie Mac, that have played an instrumental role in the refinancing of the US mortgage market for decades. These privately owned institutions could borrow at lower costs than other private financial firms, because investors believed the government would not let them fail. Although GSEs were subject to capital requirements, they held little capital compared with deposit-taking institutions. In addition, they were not diversified and they experienced consequent losses at the onset of the financial crisis8. Their situation deteriorated so badly that in September 2008, the US Federal government had to take them into conservatorship in order to avoid a systemic collapse.

The same could be said of AIG9 - the largest insurance company of the world at that time - that had to be rescued by the US Federal Government in that same month of September 2008. As it developed its credit insurance business, AIG came to hold more than half a trillion dollars of CDS10 contracts. These contracts were hidden in tiny footnotes and not included in its table of derivatives11. According to public hearings before the US Congress, the rationale behind the AIG bailout was to avoid a chain reaction that would have been caused by a desperate unwinding of all those derivatives contracts. As for the GSEs, it was the fear of unleashing systemic risk that led to government intervention.

It is interesting to contrast the AIG bailout with the refusal of the US Federal authorities to rescue Lehman Brothers12. The events that followed this decision illustrate the dilemmas associated with TBTF institutions. In this case, regulators and government officials had to balance between bailing-out Lehman Brothers to preserve financial stability, and letting it fail

7 Government Sponsored Enterprises 8 CRS (2014) 9 American Insurance Group 10 Credit Default Swaps 11 Robert Lenzner, Why Wasn’t AIG hedged?, Forbes online, 28/09/2008. 12 The Federal government and the Federal Reserve considered different options including facilitaing the sale of Lehman Brothers to BofA but it refused to provide the asset guarantees required by the buyer.

© Global research & Analytics Dept.| 2014 | All rights reserved

7

in order to discourage moral hazard and excessive risk taking by similar institutions13. Ironically, the global credit crunch that followed the Lehman bankruptcy and its consequences for the US and global economy was indeed a confirmation of Lehman’s TBTF status. This was also a wake-up call for financial regulators and policymakers. It brought about the TBTF issue to the foreground of the global financial reform agenda, and it convinced policymakers to devise appropriate procedures and rules that would enable orderly resolutions of large and complex financial institutions.

13 Final Report of the Financial crisis Inquiry Commission, Chapter 18, September 2008: the bankruptcy of Lehman, FCIC, January 2011.

© Global research & Analytics Dept.| 2014 | All rights reserved

8

2. An overview of the global regulatory reform agenda and its results

The global financial industry and its main players have been subjected to an intense scrutiny following the financial crisis. The political leaders of the twenty most important economies in the world gathered in Pittsburgh in the immediate aftermath of the Lehman failure to discuss the most urgent measures to address the crisis. Six months later, they reached an agreement at the G20 summit in London in April 2009 on a broad and ambitious regulatory reform agenda for the financial sector. A new international body, the Financial Stability Board, was established to give the initial impetus to reforms, and to monitor their implementation across the board. Half a decade later, it is interesting to assess the results that have been achieved so far on the micro-prudential, macro-prudential and institutional levels.

2.1. The micro-prudential reforms: from Basel II to Basel III

As the financial crisis unfolded, an unprecedented number of banks and non-bank financial institutions failed and most of the survivors were in dire need of recapitalization. A consensus emerged among the G20 policymakers that these institutions wrecked havoc, not only because they underestimated the credit and liquidity risks associated with their usual business practices, but also because they neglected the counterparty risk associated with huge off-balance sheet exposure to OTC14 derivatives. This prompted a severe tightening of capital requirements, both in quantity and in quality, in order to cover these unforeseen risks, and to provide a capital cushion that could be used in times of market stress. Hence, the new minimum Common Equity Tier 1 (CET) of 4,5% of risk-weighted assets (RWAs) was implemented, alongside a conservation capital buffer of 2,5%, a countercyclical capital of 0% - 2,5% to mitigate the impact of the economic cycle, and an additional capital buffer of 1% - 2,5% for systemically important banks (SIBs). Given all these components, regulators would expect the capital ratio for a bank to remain somewhere between 9,5% - 12% of RWAs depending on the position in the economic cycle. In practice, however, a capital ratio of 12% - 14% seems to be the new standard for large internationally active banks.

In addition, although the Basel Committee continued to endorse an internal ratings based (IRB) approach for assessing RWAs and calculating capital requirements, it started to ask for more transparency regarding the methodologies used by the different banks. Indeed, the Regulatory Consistency Assessment Program (RCAP) conducted by the BIS in 2012-2013, showed considerable variation in the risk weighting of assets and provisioning methods among different market participants. Following the CCAR 15 undertaken by the Federal Reserve, the AQR (Asset Quality Review) conducted by the European Central Bank in 2014 tackled this issue. It imposed a more prescriptive methodology for calculating RWAs, identifying non-performing loans (NPLs) and provisioning them. We believe this could be followed by another large-scale exercise – an MQR (Model Quality Review) so to say - that would review more in detail the theoretical principles and assumptions supporting the models used for calculating Basel IRB parameters.

14 Over-the-counter. 15 Comprehensive Capital Analysis and Review

© Global research & Analytics Dept.| 2014 | All rights reserved

9

The Basel Committee was also tasked with defining a new liquidity ratio (LCR 16 ), a transformation or funding ratio (NSFR17), and an overall leverage (SLR) ratio that would be gradually phased-‐in over the next five years18.

So far, the work has focused on the calibration and implementation of the LCR introduced in January 2015 with a gradual phase-‐in through to January 2019. The LCR shall ensure that banks hold sufficient amounts of HQLA19 that can be used without any restraints (i.e. unencumbered assets), so that they can survive a significant stress scenario lasting for 30 days. The LCR has been revised following some initial calibration problems that were voiced out by the banking industry. The pool of eligible liquid assets has been extended to include equities, high rated corporate bonds and some types of ABS (Asset Backed Securities). The work on the leverage ratio is also underway with an expected introduction in 2015-‐2016, and as for the NCFR, which has yet to be fully recalibrated, following a number of initial comments and critics from the industry, the final rules are expected in 2016.

16 Liquidity Coverage Ratio 17 Net Stable Funding Ratio 18 BCBS (2011) for the new capital rules, and BCBS (2013) for the new liquidity rules. 19 High Quality Liquid Assets

© Global research & Analytics Dept.| 2014 | All rights reserved

10

2.2. Systemic risk, G-SIFIs and macro-prudential regulations

The G20 recognized the role played by a few Systemically Important Financial Institutions (SIFI) in the build-up of financial risks and in the diffusion of the financial crisis on the global stage. As from the G20 Seoul declaration, such institutions: “should have higher loss absorbency capacity to reflect the greater risk that the failure of these firms poses to the global financial system; more intensive supervisory oversight; robust core financial market infrastructure to reduce contagion risk from individual failures; and other supplementary prudential and other requirements as determined by the national authorities, which may include, in some circumstances, liquidity surcharges, tighter large exposure restrictions, levies and structural measures”.

As a result, the Financial Stability Board published in 2011 a list of 29 G-SIBs20. Some commentators argued that publishing a list of systematically important institutions would be interpreted as an endorsement of their TBTF status. This is all the more true that the financial crisis did not stop the secular trend toward the concentration of banking assets in a few gigantic bank holding companies. Indeed, in the United States, the five largest bank holding companies held 50% of total US banking assets in 2010 compared to 30% ten years before that21.

20 Global Systemically Important Banks 21 Saint-Louis FED website and Hoenig (2014)

© Global research & Analytics Dept.| 2014 | All rights reserved

11

However, the size criterion is not sufficient, nor is it necessary to assess the systemic importance of a financial institution. Indeed, an institution could play a major role in one segment of the market, making it systemically important for that market (e.g. CDS market), while remaining small overall compared to other large diversified financial institutions22. This has been acknowledged by the Basel Committee which now considers cross-jurisdictional activity (20%), interconnectedness (20%), complexity (20%) and substitutability (20%) alongside size (20%) as determinants of the systemic importance of a bank23.

The G20 policymakers and regulators are now implementing the additional Basel III capital buffer required for G-SIBs, ranging from 1% to 2,5% of RWAs. They have also enacted ring-fencing mechanisms to protect deposits-holders, and to limit uncollateralized exposure to OTC derivatives24. However, the policymakers fell short from breaking them into more manageable and more transparent entities as this would have meant a complete overhaul of the large financial conglomerate model – or the so-called “universal bank” model. So far, the most important step taken by policymakers to deal with TBTF institutions is the establishment of an orderly resolution process for these institutions on both sides of the Atlantic. This includes bail-in rules to ensure that a bank’s shareholders and subordinated (junior) creditors bear the bulk of the cost in case of failure, before any taxpayers money is injected.

Beyond the case of individual institutions, the IMF also voiced concern about the general approach taken by the G20 regulators to the reform of the financial sector to be “based on an outmoded and by now largely repudiated conceptual framework of regulations which (..) often misses key risks”25. As a matter of fact, according to the IMF, “systemic risk in modern financial systems arises endogenously and cannot be captured by individual institutions’ balance sheets, or specific market or asset-price based measures alone, especially when these metrics are static or backward looking”. This points out to the intrinsic limitations of micro-prudential regulations, as they often fail to capture and to address system-wide risk dynamics.

In response to these critics, the international regulatory focus shifted toward macro-prudential regulations and the construction of early warning indicators (EWIs) of financial crises26. Empirical studies show for example that the evolution of the credit-to-gdp ratio has a good power for predicting future banking crises. This ratio reflects the build-up of financial leverage in the economy over a certain period of time. Hence, putting an upper limit to this ratio is equivalent to capping the financial sector’s growth relatively to the non-financial sector. This could be achieved through a tightening of monetary conditions, and, if needed, by applying unconventional measures such as restrictions on foreign capital inflows. It is difficult however, in this context, to distinguish macro-prudential policies from traditional macroeconomic stabilization policies.

22 Labonte (2014) 23 BCBS (2013b) 24 Cf. Vickers rule, Volcker Commission and Liikanen report outlined in the sections below 25 IMF [2014] 26 Drehmann (2014)

© Global research & Analytics Dept.| 2014 | All rights reserved

12

2.3. The move toward more transparency: standardization and centralized clearing of OTC derivatives

The role of OTC derivatives is well documented in the initiation and propagation of the global financial crisis. Many exposures to these instruments were not collateralized, which led to chain reactions of losses when counterparties defaulted as in the case of Lehman Brothers. In addition, the opacity of OTC trades weighed down on the financial situation of the institutions that were most exposed to them as third parties refused to provide credit to them, further exacerbating the systemic consequences of a few individual defaults. As a result, the regulation of these transactions became one of the top priorities in the global post-crisis regulatory agenda. The resulting G20 regulatory framework comprised three complementary recommendations: centralized clearing of OTC derivatives through central counterparties (CCPs), collateralization of all OTC trades, and additional capital requirement for banks to account for their exposure to CCPs (alongside credit valuation adjustments on the value of non-cleared derivatives).

According to the BIS, only 40% of the $480 trillion notional amount of outstanding OTC derivatives were centrally cleared in 2012. Multilateral netting reduces counterparty exposures to 15% of market values on average. Following the implementation of the new BSBC-IOSCO regulations, all OTC trades would be collateralized and the share of centrally cleared trades would jumps to 60% - 70% of total trades. This will clearly lower the counterparty risk exposure at the individual level. But a recent OECD study27 outlined the risks associated with such a centralization of transactions. Indeed, according to the authors of this study, the move to CCPs and the calculation of capital charges (including for Credit Valuation Adjustment on derivatives) based on netted pools would actually increase the risk of concentration, as the largest derivatives dealers – the G16 group - will tend to trade among themselves in order to minimize the netted exposures.

Critics also contend that these new regulatory requirements will substantially raise transaction costs for banks by imposing additional capital charges on them to account for CCP exposure. They also point to the increased demand (and potential shortage) of high-quality collateral that will be used for clearing transactions, at a time when banks already need to mobilize hundreds of billions of high quality unencumbered and liquid assets in order to comply with the Basel III liquidity ratio (LCR). Finally, they say the new requirements will strengthen the pro-cyclical link between market liquidity and banking liquidity. Indeed, the haircuts applied on the collateral used in margin calls are generally based on market volatility indices, which makes banks engaged in derivatives transactions particularly vulnerable to sudden market volatility swings.

Despite these critics and legitimate remarks, most analysts expected the move toward centralized clearing of OTC derivatives to have a positive impact on the mitigation of systemic risk both at the micro and macro levels. All in all, this will bring more transparency

27 Blundell-Wignall et alli. (2014)

© Global research & Analytics Dept.| 2014 | All rights reserved

13

on the distribution and concentration of risks within the system making it easier for regulators and supervisors to respond in a timely manner to new emerging risks.

3. From spirit to letter: the implementation of financial reforms in the US and EU

It is fair to recognize that the reform momentum set in motion by the G20 summit in London five years ago was tremendous, as were the expectations of a radical overhaul of financial markets and financial institutions all around the world. However, the progress in the implementation of the reform agenda is uneven. The different national - or supranational, in the case of the EU – authorities have often proceeded on a standalone and uncoordinated basis. This is due to differences in institutional and political settings, as well as to cultural differences that sometimes lead to diverging solutions.

In the long run, if no harmonization is achieved between the national standards, it could open the door to regulatory arbitrage and constitute a threat to global financial stability. This is all the more true that the global financial industry is getting more and more integrated while there is no global financial supervision authority that is recognized as such. In this regard, two sets of regulations are particularly worth exploring given their potential for regulatory arbitrage:

-‐ The “going concern” regulations which have a direct impact on banking operating models and strategies. This includes Basel III and bank separation laws.

-‐ The financial supervision frameworks and “gone concern” resolution rules dealing with bank failures.

3.1. Separation laws in the United States, the UK and the rest of Europe

In the immediate aftermath of the crisis, the G20 leaders reached a broad consensus on the necessity to enhance the protection of deposits holders, by building firewalls between the traditional retail and commercial banking activities, and the more volatile investment banking and trading activities. The rationale behind that was to prevent banks from funding risky activities with retail deposits that are protected by a government guarantee, as was the case in the United States before the repeal of the Glass-Steagall Act in the late 1990s. However, the apparent consensus on this issue masked heterogeneous views between different national regulators on the extent and scope of this separation.

-‐ The Volcker rule28 in the United States prohibited banking subsidiaries with insured deposits to engage in proprietary trading with exceptions related to investment in government and municipal bonds. It also prohibited banks from acting as principal investors in hedge funds and private equity funds. In addition, the “swap push-out

28 Originally a distinct reform proposal, the Volcker rule was subsequently added to the Dodd-Frank Act.

© Global research & Analytics Dept.| 2014 | All rights reserved

14

rule” initially required all swap transactions undertaken by a bank to be transferred into a distinct separately capitalized subsidiary29.

-‐ The report of the Independent Banking Commission - also called the Vickers Commission - in the UK came out with a comprehensive proposal to ring-fence operationally the deposit-taking retail activities from the trading and investment banking activities undertaken within the same banking group. The British legislators endorsed an even stronger version of this proposal by “electrifying the ring-fence” – i.e. giving the power to the regulators to dismantle a banking group if the ring-fence was not respected.

-‐ Other EU states would have to apply a forthcoming European regulation that is still in the making, and that would be based on the report of the Liikanen Group which adopted a middle ground between the Volcker rule and the Vickers proposal. However, France, Germany and Belgium have already implemented their own national banking separation laws, and they are not prepared to adopt more coercive reforms. This may constitute a source of conflict and tensions down the road as the French and German regulations appear too lax and toothless in comparison with the EU-sponsored regulation proposal. For that reason, some analysts and commentators are talking of a “balkanization” of the European regulatory landscape.

29 This swap push-out rule was eventually substantially watered-down following a successful lobbying campaign led by the major US banks.

© Global research & Analytics Dept.| 2014 | All rights reserved

15

3.2. The new supervisory and resolution frameworks in the US, UK and Eurozone

In the United States, the Dodd-Frank Act is the foundation of the new post-crisis supervisory and regulatory framework. It created a new agency, the Consumer Financial Protection Bureau (CFPB) which monitors consumer lending (including mortgage origination and servicing rules). Lawmakers also set up an early warning system through the Federal Stability Oversight Council which is tasked with detecting firms and business practices that could threaten financial stability, and subjecting them to tougher regulation under the Federal Reserve. In addition, the public authorities now have a functioning process for carrying through orderly resolutions of failing financial institutions.

Despite these advances, the US financial system remains fragmented as regulatory and supervisory power are shared between state regulators and federal regulators, and among the later between different federal agencies. Indeed, there are three different federal supervisors for banks (Federal Reserve, OCC30, FDIC31) depending on their size, complexity and status32. As was mentioned before, Too big to fail (TBTF) institutions have not been dismantled. They have become even bigger by absorbing the failing financial institutions and taking over their business franchises and customers. There were no serious attempts to change the banking culture, and the organizational patterns beyond the limited provisions of the Volcker rule. For these reasons, the real threat for the established large US financial conglomerates is not coming from regulators, but from disruptive technological innovations championed by digital giants such as Google, Facebook and Paypal and from the start-ups operating in the fintech33 space.

In contrast, it is not exaggerated to say that an institutional big bang happened in the European Union after the 2010-2012 euro sovereign crisis. Before the sovereign crisis, the initial post-crisis reform proposals intended to reinforce the existing financial regulations, and the supervision frameworks at the national EU-member level. In addition, this led to the creation of three consultative technical bodies: EBA (European Banking Authority), ESMA (European Securities and Markets Authority) and EIOPA (European Insurance and Occupational Pensions Authority). But following the euro crisis, a whole new financial architecture was set in place under the auspices of the Banking Union, which became operational in October 2014.

The Banking Union relies on a complex multiple-staged supervision framework for the Euro area involving European-level regulatory bodies - with the ECB at the core of the system -, and national regulators. Depending on their size and complexity, banks are now either supervised directly by the ECB (for the 130 largest banks with holdings representing 85% of Eurozone total banking assets) or by national regulators (for all the others banks). In addition,

30 Office of the Comptroller of the Currency 31 Federal Deposit Insurance Corporation 32 The Dodd-Frank merged the Office of the Thrift Supervision (OTS) with the OCC and other Federal regulators. Before its dissolution, the OTC chartered, supervised, and regulated all federally chartered and state-chartered US savings banks and savings and loans associations. 33 A contraction of the words finance and technology

© Global research & Analytics Dept.| 2014 | All rights reserved

16

the ECB retains the right to engage in direct supervision of any financial institution in the Eurozone, be it large or small. The Banking Union was needed to overcome the nascent financial fragmentation between the core and the periphery of the Eurozone. By ensuring that all the banking institutions will get the same level of attention and will face the same regulatory rules and supervisory practices, the Banking Union represents a very important milestone toward a completely integrated economic and financial space in the Eurozone.

However, the full deployment of the mechanisms supporting the Banking Union will take some time. The single supervision mechanism (SSM) is now up and running, but the single resolution mechanism (SRM) and the related single resolution fund (SRF) will not be fully operational before 2018. During the transition period, the resolution of a failing bank will have to be carried over principally by the member states with the proceeds of their own resolution funds. As for the single deposit guarantee scheme (DGS), which is the third pillar of the Banking Union, no progress on its implementation is expected before some years. Indeed, the German government which is instrumental to achieve any additional institutional development at the EU-level, wants to make sure that the legacy costs from the financial crisis have been settled down, before committing any new financial resources to the Banking Union.

© Global research & Analytics Dept.| 2014 | All rights reserved

17

© Global research & Analytics Dept.| 2014 | All rights reserved

18

3.3. Regulatory equivalence or dual burden?

Given the differences in terms of regulations and supervisory cultures across both sides of the Atlantic and beyond, it is easy to understand that without coordination, the situation is not optimal. There is room for regulatory arbitrage and regulatory capture by global financial institutions that can relocate some of their activities in the less regulated business environments. This also entails high compliance costs (human resources, IT systems) for those financial institutions that genuinely want to play by the rules.

One way to solve this problem in a cooperative manner would be to enact regulatory equivalence rules. This means allowing local subsidiaries of foreign institutions to comply with their home regulations instead of having to comply with a whole set of equivalent host regulations. This has been partially achieved for the clearing and settlement of OTC derivatives. As a result there is no discrimination between European and American players on this increasingly globally integrated market. The on-going negotiations around the Transatlantic Free Trade agreement (TAFTA) also refer to the principle of regulatory equivalence for a wide range of subjects. However, the inclusion of financial services as part of the transatlantic free trade agreement has been rebuked by the American authorities which fear that it could twist the regulatory burden and compliance costs in favour of European banks.

So far, there is no progress on this issue. A form of “regulatory nationalism” continues to prevail. The FBO (Foreign Banking Organizations) regulation – also called the Tarullo rule – published in March 2014 by the Federal Reserve, requires foreign banks with a sizeable presence in the US (i.e. banks with at least USD 50 billions of assets in the United States) to comply with the same regulations as the largest US banks34. As a result, foreign banks will need to change their legal status by July 2016. They will also have to inject new capital, hold more liquid assets and ring-fence their lending activities in the US from the other activities of their parent institutions.

34 Deloitte (2014).

© Global research & Analytics Dept.| 2014 | All rights reserved

19

4. Impact of the reforms on banking strategies and business models

4.1. Funding and liquidity risk management becomes a strategic issue

The global financial crisis that erupted in 2007-2008 blurred the traditional distinction between bank illiquidity and insolvency drawn forth by William Bagehot more than a century ago35. The Lehman failure in the United States and the Dexia failure in Europe are good examples of how a liquidity crisis can turn into an insolvency crisis which - if left unchecked - could have a disastrous effect on a whole set of other financial institutions and on mainstream economic agents that would face a credit crunch at the worst time.

The new Basel III liquidity and funding ratios, the LCR and the NSFR, are intended to prevent the apparition of such devastating liquidity crises. But there is more to a bank’s business and risk management than mere compliance with a set of new regulatory rules. In fact, it requires a complete change of strategic and operational paradigm. The old frontiers between ALM, financial control and risk management are indeed becoming increasingly irrelevant. Decisions regarding asset and liability management (ALM) can no longer be treated apart from treasury management choices, or from capital budgeting and allocation decisions. In place of the old functional silo approach, integrated FLCRM (Funding, Liquidity and Credit Risk Management) processes are appearing to optimize the way in which banks manage their balance sheets. In this vain, the performance of business strategies would be measured by using risk-adjusted performance metrics that take into account liquidity and counterparty risks.

In addition, collateral management is becoming a strategic issue as collateralized funding increasingly becomes the preferred refinancing option available for banks36. For example, high rated non-cash collateral is required in refinancing operations conducted on the interbank market, or in REPO-style open market refinancing operations conducted with the Central Bank. It is also increasingly used instead of cash to satisfy initial and variation margin calls in centrally – or even bilaterally – cleared transactions. According to the BIS, the combined impact of the new Basel III liquidity regulations and of the new EMIR / Dodd-Frank clearing requirements could generate an additional global demand of collateral in the tune of USD 4 trillion37. Even if the concerns about a shortage of high quality collateral seem unjustified on a global basis, the situation may still vary markedly across different financial jurisdictions, and among different players within the same jurisdiction. This will undoubtedly generate new incentives for banks of various sizes and specialization to better manage their existing collateral pools, and to create new collateral pools through the securitization and pooling of their loans portfolios.

35 Bagehot (1873) 36 In fact as secured funding develops, unsecured funding can become more risky for investors as banks do not fully disclose the degree of asset encumbrance on their balance sheets. 37 BIS(2013)

© Global research & Analytics Dept.| 2014 | All rights reserved

20

As an illustration of this trend, there is now an expanding market for securities lending and collateral transformation services. In a typical collateral re-hypothecation scheme, securities administrators and custodians or large institutional investors lend high quality collateral to their clients in exchange for lower quality collateral plus a fee.

4.2. A shifting landscape for Capital Markets and Investment Banking

The universal bank model gradually became the dominant banking model over the last three decades, as a result of the financial deregulation and liberalization waves that swept through the OECD countries from the 1970s to the 1990s. The philosophy behind this model is based on using cheap and relatively stable resources collected by the retail banking subsidiary to refinance and cross-subsidize volatile investment banking and capital markets activities. It was assumed that the underlying idiosyncratic risks in terms of liquidity and maturity transformation associated to a specific operation would be diversified away and diluted as the size of the balance sheet grows. However, the financial crisis undermined some fundamental assumptions behind this paradigm, such as the idea that idiosyncratic risk can always be diversified away. Even though the post-crisis financial regulations do not frontally attack the universal bank model, they try to harness it by imposing the following constraints:

-‐ The new Basel III constraints on capital (CET and additional capital buffers), liquidity (LCR), stable funding (NCFR) and overall leverage (SLR).

-‐ The “separation laws” that prohibit and/or ring-fence - either legally or operationally, or both – a range of capital markets activities away from the deposit-taking entities

-‐ The host supervision of foreign banks and the creation of subsidiaries which have to respect capital and liquidity ratios and compete for local funding

© Global research & Analytics Dept.| 2014 | All rights reserved

21

As a result of these constraints, many banking institutions have already started to divest and to move out from a range of non-core business lines such as project finance or structured products. Only large scale economies and superior business franchises can justify the preservation of these activities from an economic point of view. In addition, large balance sheets with robust funding are needed to support capital markets activities, especially in the FICC arena. The extent to which this model reshuffle and restructuring of operating models will go is not clear, but some on-going trends can be outlined.

4.2.1. Increased segmentation between Global CIBs38, high-end multi-specialists and local corporate banks

One insufficiently analyzed consequence of the financial crisis is the tendency toward the concentration of capital markets activities within a few large global financial conglomerates with broad expertise and substantial market clout (G-CIBs). These Tier 1 financial institutions – that can be either standalone CIBs or subsidiaries of global universal banks – are increasingly playing the role of services providers to smaller financial institutions lacking the balance sheet strength and human resources of the former category. The regulatory reforms reinforce this trend toward the concentration of CIB activities and the emergence of a “core-periphery” – or “wholesale service producers versus local distributors” – model.

Indeed, the CIB subsidiaries of global universal banks with a strong and diversified balance sheet (Bank of America, Citigroup, UBS, Deutsche Bank, BNPP, …) still benefit from a substantial advantage in flow activities such as securities lending (prime brokerage) and market making in rates, currencies and commodities markets (FICC). The ring-facing laws (Volcker, Vickers, Liikanen) will make it more difficult for them to move liquidity and capital from the retail deposit-taking arms to their CIB subsidiaries, but these institutions will find innovative ways to circumvent the most restrictive rules. For example by creating new structures that will host mutualized capabilities and services between the retail and investment banking subsidiaries.

On the other side, pure player G-CIBs (J.P. Morgan, Goldman Sachs, Morgan Stanley, ..) which are focused on CIB activities and have strong global franchises and reputations will continue to attract the best and brightest talents. These pure player G-CIBs, which are mostly American, will continue to incur higher overall funding costs than their universal bank competitors, as they rely more on wholesale liquidity. But they now have access to central bank refinancing facilities, following their recent incorporation as bank holding companies. This lowers the likelihood of destructive liquidity crises on the magnitude of those that led to the bankruptcy of Lehman Brothers, and to the absorption of “pure players” Bear Stearns and Merril Lynch by large universal banks.

In addition to the G-CIBs, there is also one particular breed of high-end specialists or multi-specialists that is worth mentioning. This Tier 1 category includes Black Rock, Lone Star and

38 Corporate and Investment Banking

© Global research & Analytics Dept.| 2014 | All rights reserved

22

other alternative investment management firms (hedge funds and private equity firms) that are increasingly using their technical expertise and high talent pool to provide customized solutions to a range of institutional and private clients (large banks and asset management companies, pension funds, family offices, governments and central banks, etc.). Lacking the balance sheet strength of the former players, they act like the pilot fish that congregates around sharks forming mutually advantageous relations.

Against this background of Tier 1 global CIB institutions and their ecosystem of service providers (brokers, clearinghouses, custodians, consulting companies, technology firms), Tier 2 and Tier 3 CIBs which can be split into local generalists and local specialists could still manage to compete. But they will need to leverage more astutely their close relationship with their local clients by delivering tailor-made services, and using whenever needed white label financial solutions supplied by G-CIBs and high-end specialists. In essence, the local corporate banks will likely act like as a local “distribution platform” for commoditized financial products, and as partners to Tier 1 institutions in complex financial engineering transactions requiring advanced product customization. They will also have to work more on the acquisition of new clients and on the maximization of revenue from existing clients, using advanced quantitative customer analytics - the so called “Big data”.

4.2.2. A commoditization and standardization of most derivatives alongside residual tailor-made products

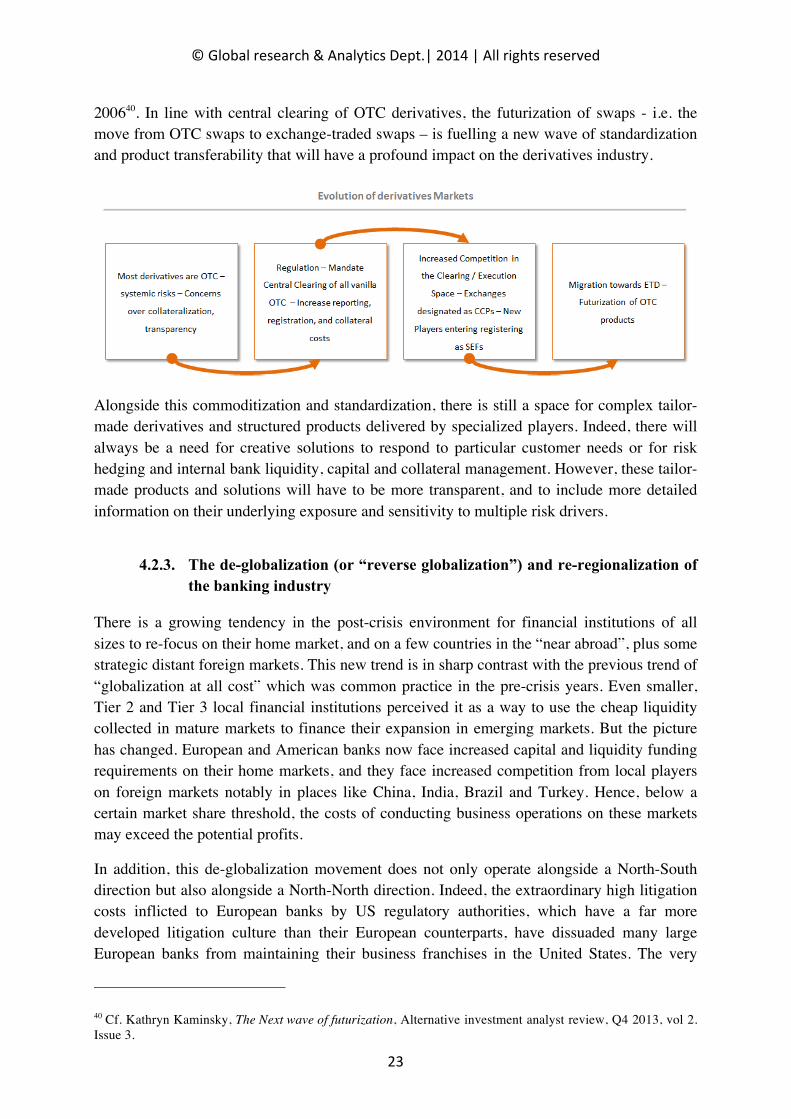

Simplicity, transparency, efficiency and cost-effectiveness are the cardinal values of banking products and services in the post-crisis environment. Neither clients nor regulators are tolerating any more the opaque highly priced products that financial engineering gurus used to manufacture and sell to credulous clients. The commoditization and standardization of many capital markets products has gone hand in hand with this increased demand for simplicity and efficiency. It is also the result of massive technological investments that enabled the automation of many business processes – e.g. with the apparition of fully automated electronic trade execution, clearing and settlement platforms - and that is now allowing the digitalization of those same processes and businesses. This led to a continuous fall in profit margins on “vanilla” flow activities such as cash management and equities and bonds brokerage and clearing39. It has also led to a “futurization” of the derivatives products space, which is accelerating with the progressive implementation of the post-crisis regulatory reforms (EMIR, Dodd-Frank).

Basically, this means that as more and more OTC derivatives contracts will have to be registered and cleared through CCPs, the difference between OTC products and exchange-traded derivatives is being blurred and more and more OTC products are converted to exchange-traded products. For example, futures and forwards which are mostly exchange-traded have climbed in 2012 to 19% of the total notional value in derivatives up from 11% in

39 For example, the clearing fees for cash products (equities, bonds) at leading CCPs such as LCH Clearnet or Eurex are only a fraction of what they used to be a decade ago.

© Global research & Analytics Dept.| 2014 | All rights reserved

23

200640. In line with central clearing of OTC derivatives, the futurization of swaps - i.e. the move from OTC swaps to exchange-traded swaps – is fuelling a new wave of standardization and product transferability that will have a profound impact on the derivatives industry.

Alongside this commoditization and standardization, there is still a space for complex tailor-made derivatives and structured products delivered by specialized players. Indeed, there will always be a need for creative solutions to respond to particular customer needs or for risk hedging and internal bank liquidity, capital and collateral management. However, these tailor-made products and solutions will have to be more transparent, and to include more detailed information on their underlying exposure and sensitivity to multiple risk drivers.

4.2.3. The de-globalization (or “reverse globalization”) and re-regionalization of the banking industry

There is a growing tendency in the post-crisis environment for financial institutions of all sizes to re-focus on their home market, and on a few countries in the “near abroad”, plus some strategic distant foreign markets. This new trend is in sharp contrast with the previous trend of “globalization at all cost” which was common practice in the pre-crisis years. Even smaller, Tier 2 and Tier 3 local financial institutions perceived it as a way to use the cheap liquidity collected in mature markets to finance their expansion in emerging markets. But the picture has changed. European and American banks now face increased capital and liquidity funding requirements on their home markets, and they face increased competition from local players on foreign markets notably in places like China, India, Brazil and Turkey. Hence, below a certain market share threshold, the costs of conducting business operations on these markets may exceed the potential profits.

In addition, this de-globalization movement does not only operate alongside a North-South direction but also alongside a North-North direction. Indeed, the extraordinary high litigation costs inflicted to European banks by US regulatory authorities, which have a far more developed litigation culture than their European counterparts, have dissuaded many large European banks from maintaining their business franchises in the United States. The very

40 Cf. Kathryn Kaminsky, The Next wave of futurization, Alternative investment analyst review, Q4 2013, vol 2. Issue 3.

© Global research & Analytics Dept.| 2014 | All rights reserved

24

high fines against BNPP, Credit Suisse, UBS, Deutsche Bank and other less important players do not compel these entities to develop their business activities in the United States or with US dollar funding, unless they want to keep their operations there for reputational or other strategic reasons.

4.3. Toward a renaissance of the “originate-to-distribute” model

Balance sheet and capital-constrained retail banks funded through customer deposits are concerned in the first place by the new regulatory and supervisory landscape. There are not many solutions to deal with the new Basel III capital adequacy rules and leverage ratio: banks have either to increase their capital – which can be very costly at times - or they have to shed risk and/or compress their balance sheets and reduce off-balance commitments to their customers (credit lines, guaranties, etc.). Basically, although there are many ways to mitigate credit and market risk associated with banking assets while retaining those assets on the balance sheet, there are only two ways to offload assets before their maturity: it could be done either through securitization vehicles that repackage and sell them to investors, or through direct sale of these loans to asset management companies (e.g. to distressed debt funds or infrastructure and project finance funds).

4.3.1. The rebirth of mass-market securitization and its prospects

Mass-market securitization - be it vanilla or synthetic - is a good solution for offloading credit risk associated with large retail loan portfolios. It is used on a very large scale by retail loan originators in the United States. Indeed, the mortgage risk is borne in the United States not by banks but by institutional investors (pension funds, etc.) that buy residential mortgage backed securities (RMBS) issued by the federal mortgage refinancing agencies Fanny Mae and Freddy Mac. Even at the height of the subprime crisis, these Agencies continued to play the dominant role in the refinancing of mortgage origination in the United States. After the financial crisis, almost all ABS issued in the United States consisted of agency-backed RMBS.

© Global research & Analytics Dept.| 2014 | All rights reserved

25

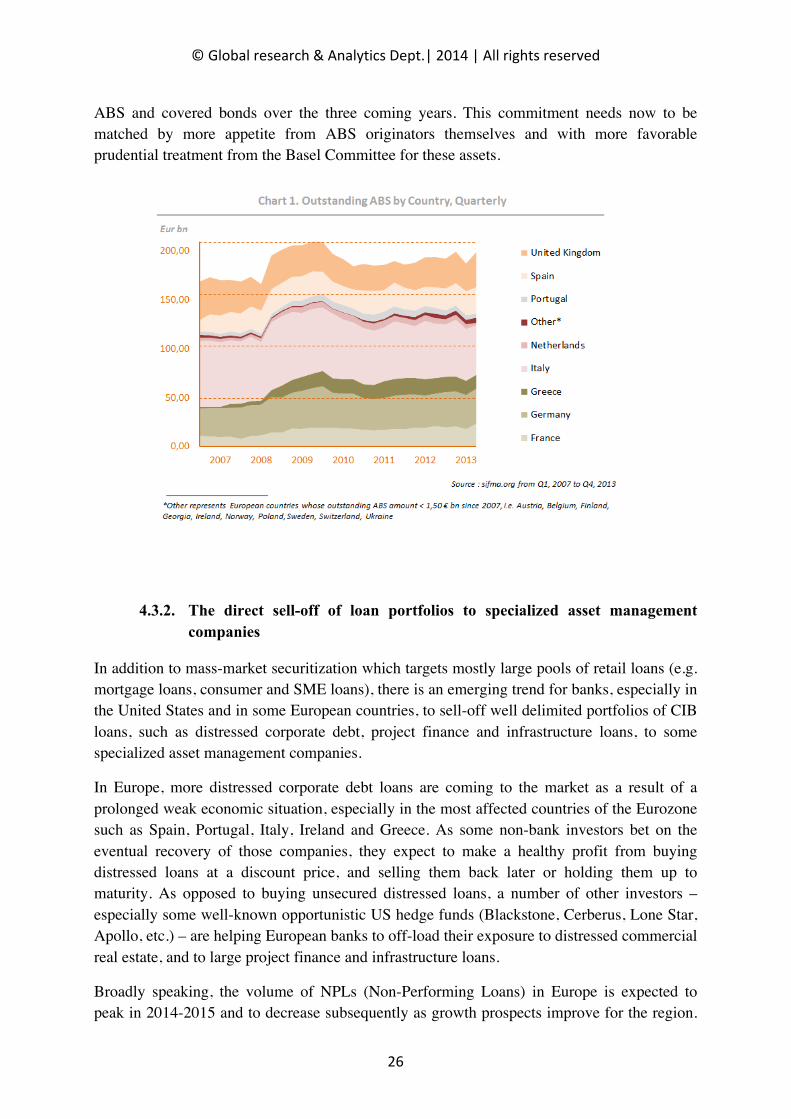

In Europe, the situation is quite different with securitization playing a more modest role in the financing of non-financial corporations and households. Beyond this general appreciation, the situation remains very different from one country to another and from one market segment to another one. In the UK, the Netherlands and Spain, the securitization and issuance of RMBS grew at a steady rhythm in the years leading to the crisis. Following a slump in 2009-2010, securitization of high quality low default mortgage portfolios could be taking up again, especially in the UK, provided there is an appetite for that from investors and a facilitated prudential treatment by regulators41.

It is also worth mentioning that the outstanding volume of ABS in Europe is comparable with the volume of the covered bonds market. Covered bonds, which are mostly used in Sweden, Denmark, Germany, France, Spain and the UK, provide a robust alternative for offloading credit risk while retaining the underlying assets on the balance sheet (contrary to securitization in which these assets are removed and sold to investors). In Europe, most of the ABS issued after the 2007-2008 have been retained by the banks themselves and used as a collateral in order to obtain cheap funding from the ECB. The proportion of retained ABS out of the outstanding securitization volume in Europe climbed from 0% to 60% over the 2007-2013 period. Until very recently, covered bonds enjoyed a more favorable treatment by the ECB than ABS as a collateral accepted in its liquidity provision operations. This is starting to change as the monetary policy focus is becoming more favorable to the development of the ABS market42.

However, given the steady decline of ABS issuance in Europe starting from 2008, which is essentially due to a diminution of RMBS issuance in the UK and in Spain, it is too early to speak of a renaissance of securitization in Europe. In the short term, the revival of the “originate-to-distribute” model relies on regulatory incentives and policy-backed initiatives. In the Eurozone, where there is an urgent need to reactivate credit growth and to avoid falling into a deflationary trap, this is envisioned as a promising option. The president of the ECB, Mario Draghi, announced in September 2014 a new program to buy hundreds of billions of

41 According to an analysis by S&P’s quoted by the ECB, the cumulative default rate on European structured finance assets from the beginning of the financial downturn, July 2007, until Q3 2013 has been only 1.5%. 42 The ECB reduced its haircuts on ABS, in July 2013, from 16% to 10% in the permanent framework.

© Global research & Analytics Dept.| 2014 | All rights reserved

26

ABS and covered bonds over the three coming years. This commitment needs now to be matched by more appetite from ABS originators themselves and with more favorable prudential treatment from the Basel Committee for these assets.

4.3.2. The direct sell-off of loan portfolios to specialized asset management companies

In addition to mass-market securitization which targets mostly large pools of retail loans (e.g. mortgage loans, consumer and SME loans), there is an emerging trend for banks, especially in the United States and in some European countries, to sell-off well delimited portfolios of CIB loans, such as distressed corporate debt, project finance and infrastructure loans, to some specialized asset management companies.

In Europe, more distressed corporate debt loans are coming to the market as a result of a prolonged weak economic situation, especially in the most affected countries of the Eurozone such as Spain, Portugal, Italy, Ireland and Greece. As some non-bank investors bet on the eventual recovery of those companies, they expect to make a healthy profit from buying distressed loans at a discount price, and selling them back later or holding them up to maturity. As opposed to buying unsecured distressed loans, a number of other investors – especially some well-known opportunistic US hedge funds (Blackstone, Cerberus, Lone Star, Apollo, etc.) – are helping European banks to off-load their exposure to distressed commercial real estate, and to large project finance and infrastructure loans.

Broadly speaking, the volume of NPLs (Non-Performing Loans) in Europe is expected to peak in 2014-2015 and to decrease subsequently as growth prospects improve for the region.

© Global research & Analytics Dept.| 2014 | All rights reserved

27

But the delayed economic recovery compared with the US, the accumulation of legacy assets, and the focus on balance sheet deleveraging, have created a vast market for such assets. According to Cushman & Wakefield, in the distressed European property loans segment alone, total transactions are expected to reach €60 billion in 2014, twice as high as the €30 billion recorded in 2013.

A substantial share of these deals has taken place in Ireland through the Irish government “bad bank”, NAMA (National Asset Management Agency) that has mandate to acquire and liquidate NPLs from Irish banks. The Spanish national bad bank, SAREB (Sociedad de Gestión de Activos Inmobiliarios Procedentes de la Reestructuración Bancaria) which manages a loans portfolio of €90 billion is also expected to ramp up its assets sales in the coming years. Italy also offers a lot of opportunities for investors as bank deleveraging there has only started and as the consolidation of the banking sector around a few dominant players has still a way to go.

© Global research & Analytics Dept.| 2014 | All rights reserved

28

Bibliography

ACPR, Le marché de la titrisation en Europe: caractéristiques et perspectives, Analyses et syntheses, n°31, juin 2014.

Bagehot William, Lombard Street: A Description of the Money Market. King, London, 1873.

BCBS (Basel Committee on Banking Supervision), Basel III: A global regulatory framework for more resilient banks and banking systems – revised version, BIS, June 2011.

BCBS (Basel Committee on Banking Supervision), Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring tools, BIS, January 2013.

BCBS (Basel Committee on Banking Supervision), Global systematically important banks: updated assessment methodology and the higher loss absorbency requirement, July 2013.

BIS, Macroeconomic impact assessment of OTC derivatives regulatory reform, Report of the Macroeconomic Assessment group on derivatives, August 2013.

Blundell-Wignall Adrian, Paul Atkinson, Caroline Roulet, Bank business models and the Basel system: complexity and interconnectedness, OECD Journal: Financial Market Trends 2014, Volume 2013/2, OECD, Paris, 2014.

Brunnermeier Markus K., Deciphering the liquidity and credit crunch 2007-2008, Journal of Economic Perspectives, Vol. 23, No. 1 – Winter 2009 – p. 77-100.

Carr Alexandria et alli., Does Volcker + Vickers = Liikanen ? EU proposal for a regulation on structural measures improving the resilience of EU credit institutions, Mayer Brown, Legal update, February 2014.

CGFS, Asset encumbrance, financial reform and the demand for collateral assets, Report of the working group headed by Aerdt Houben, CGFS Papers No. 49, May 2013.

Classens Stijn and Laura Kodres, The Regulatory responses to the financial crisis: some unconfortable questions, prepared by, IMF Working Paper WP/14/46, March 2014

Davis Kevin, Regulatory reform post the global financial crisis: An overview, Report prepared for the Melbourne APEC Finance Center, 2010.

Deloitte, Final look: a practical guide to the Federal Reserve’s enhanced prudential standards for foreign banks, June 2014.

Drehmann Mathias and Mickael Juselius, Evaluating early warning indicators of banking crises: Satisfying policy requirements, BIS Working Papers, No421, August 2013.

Dullien Sebastian, How to complete Europe’s banking union, ECFR Policy Brief, June 2014.

Gambacorta Leonardo and Adrian van Rixtel, Structural bank regulation initiatives: approaches and implications, BIS Working papers, No 142, April 2013.

© Global research & Analytics Dept.| 2014 | All rights reserved

29

Hoenig Thomas M., Speech presented to the National Association for Business Economics 30th Annual Economic Policy Conference; Arlington, Virginia, February 2014.

Kose Ayhan, Eswar Prasad, Kenneth Rogoff, and Shang-Jin Wei, Financial Globalization: a reappraisal, IMF Working Papers 06/189, August 2006.

Labonte Marc, Systemically important or “too big to fail” financial institutions, CRS Report, August 2014.

Llewellyn David, The Economic rationale of financial regulation, FSA Occasional Papers in Financial regulation, No. 1, April 1999.

McKinsey & Cie, Between deluge and drought. The divided future of European bank-funding markets. McKinsey Working Papers on Risk, N° 41, March 2013.

© Global research & Analytics Dept.| 2014 | All rights reserved

30

Appendixes

Appendix 1. Progress in the Implementation of G20/FSB Recommendations (as of end 2013)

United States of America

N° G20 Recommendations Responsible institutions Reference Status ImplementedI Refining the regulatory perimeter

1Review the boundaries of the regulatory framework including strengthening of oversight of shadow banking

SEC / FSOC Final Rule and Interpretative Guidance 100% April 2012

II Hedge funds2 Registration, appropriate disclosures and oversight of hedge funds SEC Registration of hedge funds managers in force 100% April 20133 Establishment of international information sharing framework IOSCO Model supervisory cooperation arrangements 100% May 2010

4 Enhancing counterparty risk management SEC-‐ Exchange Act Release No. 68071-‐ Exchange Act Rule 15c3-‐4-‐ Appendix E & F to Rule 15c3-‐1

100% June 2011

III Securitisation

5 Improving the risk management of securitisation Federal Reserve-‐Disclosure for ABS Required by Section 943 of the Dodd-‐Frank Act-‐ Issuer Review of Assets and Offerings of ABS

100% January 2011

6 Strengthening of regulatory and capital framework for monolines NY Department of Insurance na

7 Strengthening of supervisory requirements or best practices for investment in structured products NAIC 0%

8 Enhanced disclosure of securitised products Federal Reserve-‐Disclosure for ABS Required by Section 943 of the Dodd-‐Frank Act-‐ Issuer Review of Assets and Offerings of ABS

100% January 2011

IV Enhancing supervision

9 Consistent, consolidated supervision and regulation of SIFIs Federal ReserveCreation of the FSOC (Dodd Frank Act) :-‐ Final Rule and Guidance

100% May 2012

10 Establishing supervisory colleges and conducting risk assessments Crisis Management Group na 100% October 201211 Supervisory exchange of information and coordination Crisis Management Group na 100% July 201012 Strengthening resources and effective supervision National supervisors National laws and policy frameworks (inc. DFA) 100% November 2011

V Building and implementing macroprudential frameworks and tools

13 Establishing regulatory framework for macro-‐prudential oversight Federal Reserve

-‐ Final Rule for Board of Governors of the Federal Reserve System (Board) and Federal Deposit Insurance Corporartion-‐ Final Rule for Federal Deposit Insurance Corporation

100%November 2011 / January 2012

14 Enhancing system-‐wide monitoring and the use of marco prudential instruments CFTC-‐CFTC Notice of Proposed Rulemaking on Margin Requirements for Uncleared Swaps for Swap Dealers and Major Swap participants

70%

15 Improved cooperation between supervisors and central banks SEC / FSOC Dodd Frank Act : Creation of the FSOC 100% July 2010

VI Improving oversight of Credit Rating Agencies

16 Enhancing regulation and supervisions to Credit Rate Agencies SEC Credit Rating Agency Reform Act 50% June 2007

17 Reducing the reliance on ratings na

VII Enhancing and aligning accounting standards

18 Consistent application of high-‐quality accounting standards US Banking agenciesRegular regulatory reporting guidance consistent with US GAAP

90% na

19 Appropriate application of Fair Value Accounting IASB / FASB-‐Accounting Standards updates N° 2011-‐04, Fair Value measurement-‐ IFRS 13, Fair Value measurement

80% May 2011

VIII Enhancing risk management

20Enhancing guidance to strengthen bank's risk management practices, including liquidity and foreign currency funding risks

Federal Reserve Dodd Frank Act : Requirements for stress testing 100% March 2010

21 Efforts to deal with impaired assets and raise additional capitalIASB / FASBUS Regulators

-‐ Amendments on standards on financial instrument impairment-‐ Additional guidance for the 19 SCAP firms

80%-‐ May 2011

-‐ September 2009

22 Enhanced risk disclosures by financial institutions FASB Final Accounting Standard 80% January 2010

IX Strengthening deposit insurance23 Strengthening of national deposit insurance arrangements na na 70% February 2013

X Safeguarding the integrity and efficency of financial markets

24 Enhancing market integrity and efficiency SEC

-‐ Rule 13h-‐1 -‐ Rule 15c3-‐5-‐ Rule 613-‐ Proposed Regulation Systems Compliance and Integrity

80% January 2010

25 Enhanced market transparency in commodity markets CFTC

-‐Final Rule and Interim Final Rule on Position Limits for Futures and Swaps-‐ Final Rule on Large Trader Reporting for Physical Commodity Swaps-‐ The Commodity Exchange Act-‐ Final Rule on Swap Data Recordkeeping and Reporting Requirements-‐ Final Rule on Real Time Public Reporting of swap transaction data-‐ Compliance Date and Time Delay phase Ins for Real Time Reporting-‐ Final Rule Making on Procedures to establish appropriate minimum block sizes for large notional off facility swaps and block trades

100% July 2011

26 Creation of a Legal Entity Identified CFTCNotice of Final Rule Making on Swap Data Recordkeeping

100% December 2012

XI Enhancing financial consumer protection

27 Enhancing financial consumer protection CFPBCreation of Consumer Financial Protection Bureau regulations

100% July 2011

© Global research & Analytics Dept.| 2014 | All rights reserved

31

European Commission

N° G20 Recommendations Responsible institutions Reference Status ImplementedI Refining the regulatory perimeter

1Review the boundaries of the regulatory framework including strengthening of oversight of shadow banking

The European Commission

-‐ Alternative Investment Funds Directive-‐ Capital Requirements Directives and Regulations-‐ EMIR-‐ CRA I, II, III

30%

II Hedge funds

2 Registration, appropriate disclosures and oversight of hedge funds Member StatesAIMFD : Rules for the registration or autorisation of AIFMs, the on-‐going operation of the AIFM's business and rules on transparency and supervision

90%

Directive : July 2012Regulation : April 2013

3 Establishment of international information sharing framework Member StatesAIMFD : Rules for the registration or autorisation of AIFMs, the on-‐going operation of the AIFM's business and rules on transparency and supervision

100%

Directive : July 2012Regulation : April 2013

4 Enhancing counterparty risk managementEU national supervision authorities

CRR / CRD IV 90% June / July 2013

III Securitisation

5 Improving the risk management of securitisationEU national supervision authoritiesMember States

-‐ CRD II / III-‐ Solvency II Directive (Art. 135 (2))-‐ AIFMD : Legal framework of AIFM

80%-‐ End of 2010-‐ July 2013

-‐ exp. Jan 2014

6 Strengthening of regulatory and capital framework for monolinesEU national supervisions authorities

Solvency II 80%

7 Strengthening of supervisory requirements or best practices for investment in structured productsEU national supervision authorities

-‐ Provisions on CRD III-‐ Solvency II

80%-‐ 2011

-‐ Exp. Jan 2014

8 Enhanced disclosure of securitised productsEU national supervision authorities

-‐ CRA III-‐ Solvency II

90%-‐June 2013

-‐ exp. Jan 2014

IV Enhancing supervision

9 Consistent, consolidated supervision and regulation of SIFIsEU national supervision authorities

-‐ CRR / CRD IV-‐ Solvency II

80%-‐ June /July 2013-‐ Exp. Jan 2014

10 Establishing supervisory colleges and conducting risk assessmentsEU national supervision authorities

-‐ CRD IV -‐ Solvency II

80%-‐ June /July 2013-‐ Exp. Jan 2014

11 Supervisory exchange of information and coordinationEU national supervision authorities

-‐ Solvency II-‐ SSM

80%

12 Strengthening resources and effective supervisionEU national supervision authorities

-‐ European System of Financial Supervision-‐ SSM

80%-‐ January 2011-‐ Exp. Autumn

2013

V Building and implementing macroprudential frameworks and tools

13 Establishing regulatory framework for macro-‐prudential oversight ESRB-‐Recommendations of the ESRB : ESRB / 2011/3, OJ 2012 / C41/01-‐ ESRB / 2013 / 1; OJ 2013/C 170/01

80% 2012

14 Enhancing system-‐wide monitoring and the use of marco prudential instruments ESRB-‐Recommendations of the ESRB : ESRB / 2011/3, OJ 2012 / C41/01-‐ ESRB / 2013 / 1; OJ 2013/C 170/01

80% 2012

15 Improved cooperation between supervisors and central banksEU national supervision authorities

-‐ CRR / CRD IV-‐ BRRD-‐ SRM proposal

70%

VI Improving oversight of Credit Rating Agencies

16 Enhancing regulation and supervisions to Credit Rate Agencies ESMA-‐ Regulation 1060/2009 -‐ Regulation 513 / 2011-‐ CRA III

80%-‐ January 2010-‐ July 2011-‐ June 2013

17 Reducing the reliance on ratings na

VII Enhancing and aligning accounting standards18 Consistent application of high-‐quality accounting standards ESMA IFRS guidelines 100% na

19 Appropriate application of Fair Value Accounting ESMA-‐IFRS 13-‐ Regulatory Technical Standards on 'Prudential Valuation'

90% January 2013

VIII Enhancing risk management

20Enhancing guidance to strengthen bank's risk management practices, including liquidity and foreign currency funding risks

EU national supervision authorities

CRD IV / CRR 100% June 2013

21 Efforts to deal with impaired assets and raise additional capital EBA Recommendation on capital preservation 60% 2012

22 Enhanced risk disclosures by financial institutions ESMA IFRS 13 and amendments on IFRS 7 100% January 2013

IX Strengthening deposit insurance

23 Strengthening of national deposit insurance arrangements The European Commission Deposit Guarantee Schemes 70%Expected :

Summer 2013

X Safeguarding the integrity and efficency of financial markets

24 Enhancing market integrity and efficiency The European Commission-‐ MIFID II-‐ Review of the Market Abuse Directive

60% na

25 Enhanced market transparency in commodity markets The European Commission-‐ MIFID II-‐ Review of the Market Abuse Directive

60% na

26 Creation of a Legal Entity Identified na-‐Members of LOI ROC : European Commission, ECB, ESMA, alongside numerous authorities from Member States

100% March 2013

XI Enhancing financial consumer protection

27 Enhancing financial consumer protection The European Commission

-‐ MIFID II-‐ Packaged Retailed Investment Product (PRIPs)-‐ Revision of the Insurance Mediation Directive (IMD)-‐ The Mortgage Credit Directive-‐ Bank account package

60% na

© Global research & Analytics Dept.| 2014 | All rights reserved

32

United Kingdom

N° G20 Recommendations Responsible institutions Reference Status ImplementedI Refining the regulatory perimeter

1Review the boundaries of the regulatory framework including strengthening of oversight of shadow banking

UK AuthoritiesFinancial Policy Committee can make recommendation to Treasury

100% 2013

II Hedge funds

2 Registration, appropriate disclosures and oversight of hedge fundsFCAUK Authorities

-‐ Supervision by the FCA -‐ AIMFD : Rules for the registration or autorisation of AIFMs, the on-‐going operation of the AIFM's business and rules on transparency and supervision

na

3 Establishment of international information sharing framework FCA na 100% na

4 Enhancing counterparty risk management FSA na na

III Securitisation

5 Improving the risk management of securitisationEU national supervision authorities

CRD II 100% December 2010

6 Strengthening of regulatory and capital framework for monolinesEU national supervision authorities

Solvency II 80%

7 Strengthening of supervisory requirements or best practices for investment in structured productsEU national supervision authorities

-‐ CRD II-‐ Supervision by the FCA

100% December 2010

8 Enhanced disclosure of securitised productsEU national supervision authorities

CRD II through BIPRU 9.15 100% December 2010

IV Enhancing supervision

9 Consistent, consolidated supervision and regulation of SIFIsPrudential Regulation Authorities

Supervision by PRA 80% pre crisis

10 Establishing supervisory colleges and conducting risk assessmentsPrudential Regulation Authorities

Supervision by PRA 80% mid 2009

11 Supervisory exchange of information and coordinationEuropean Supervision Authorities

Extensive set of MoUs 80% 2010

12 Strengthening resources and effective supervision-‐ Prudential Regulation Authorities-‐ FCA