chapters ssgc

TRANSCRIPT

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Chapter # 01

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Introduction to

SSGC

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

INTRODUCTION TO SSGC

INTRODUCTION:

Sui Southern Gas Company (SSGC) is Pakistan's leading integrated gas Company.

The company is engaged in the business of transmission and distribution of natural

gas besides construction of high pressure transmission and low pressure distribution

systems.

SSGCL transmission system extends from Sui in Baluchistan to Karachi in Sindh

comprising over 3,200 KM of high pressure pipeline ranging from 12 - 24" in

diameter. The distribution activities covering over 1200 towns in the Sindh and

Baluchistan are organized through its regional offices. An average of about 378,468

million cubic feet (MMCF) gas was sold in 2008-09 to over 2.040 million (industrial

3,448, commercial 22,192and domestic 2,014,827 consumers) in these regions

through a distribution network of over 31,877 Km. The company also owns and

operates the only gas meter manufacturing plant in the country, having an annual

production capacity of over 550,150 meters.1

The Company has an authorized capital of Rs. 10 billion of which Rs 6.7117 billion is

issued and fully paid up. The Government owns the majority of the shares which is

presently over 70%.2

The Company is managed by an autonomous Board of Directors for policy

guidelines and overall control. Presently, SSGC's Board comprises of 14 members.

The Managing Director/Chief Executive is nominee of GOP and has been delegated

with such powers by the Board of Directors as are necessary to effective conduct the

business of the company.

1

2

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

SSGC at a Glance:

The Company in its present shape was formed on March 30, 1989 following a series

of mergers of three pioneering companies, namely Sui Gas Transmission Company

Limited, Karachi Gas Company Limited and Indus Gas Company Limited.

Sui Gas Transmission Company Limited was formed in 1954 with the primary

responsibility of gas purification at the Sui field in Balochistan and its transmission to

the consumption centres at Karachi. Two distribution companies were established in

1955 and were responsible for the distribution of gas to consumers in Karachi and in

other towns along the route of the transmission pipeline between Sui and Karachi. In

1985, these two distribution companies were merged to form Southern Gas

Company Limited and later, in 1989, Southern Gas Company Limited and Sui Gas

Transmission Company Limited were merged to form the Sui Southern Gas

Company Limited.

Today, half a century of professionalism and progress has made the SSGC one of

the largest integrated natural gas transmission and distribution companies in

Pakistan, serving the entire Southern region of the country, comprising the provinces

of Sindh and Balochistan.3

Core Business

The main activity of the company is transmission and distribution of gas in Sindh and

Baluchistan

3

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

SSGC’s VISION

To be a model utility, providing quality service by maintaining a high level of ethical

and professional standards and through the optimum use of resources.

SSGC’s MISSION

To meet the energy requirements of customers through reliable, environment-friendly

and sustainable supply of natural gas, while conducting company business

professionally, efficiently, ethically and with responsibility to all our stakeholders,

community and the nation.

CORE VALUES

Integrity:

Keep Company's Interest above self. Acts in ethical manner. Promote

ethical business environment. Take effective actions if observers

unethical behavior or situation. Seen & known to be honest. Lives

within means. Intellectually hones.

Excellence:

Makes positive contribution towards the achievement of SSGC's

Vision. Strives for Continuous improvement. Respond effectively to

customer needs. Takes timely and Quality decisions.

Teamwork:

Builds strong relationships within across functions. Works well with

all type of Peoples and corporate with others. Solicits and share

ideas/best practice with others. Supports the achievements of

Company/team goals. Contributes to team effectiveness using people's different

skills and styles. Arrives at constructive solutions while maintaining Positive working

relationships. Demonstrates sensitivity.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Transparency:Promotes open environment. Displays openness and consistency in

applying policies & Procedures. Respects dissent and resolves

conflicts fairly.

Creativity:

Comes up with new ideas. Encourages innovation. Promotes

modified approaches. Convert Ideas into actions.

Responsibility to Stakeholders:

Stays abreast of change in operating environment that impacts our

business (i.e. markets, competitors, Technology, customers,

suppliers, employees, regulatory, political and public). Create

solutions to make Customer needs. Develops colleagues and team members to

improve their skills and performance. Ensure Optimum utilization of resources.

Balances short term and long term priorities to maximize on results. Ensures

compliance of law.4

COMPANY’S OBJECTIVE

The Company aims to supply natural gas wherever there is sufficient load to justify

the cost of infrastructure. In many places the gas network is being expanded to meet

economic and social requirements through active funding support from the Federal

and Provincial governments. In 2003, the Company launched a comprehensive five-

year gas network development and expansion

Plan to connect hundreds of small towns and villages in remote areas of

Sindh and Balochistan, which currently are deprived of piped natural gas.

Every year, the Company adds nearly 75,000 new customers (industrial,

commercial & domestic) to its customer base and lays hundreds of kilometres.

Transmission pipelines and distribution network and installs other facilities such

as metering/ billing stations in its system using its staff of technically qualified and

skilled personnel.

4 Annual report of SSGC

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

FUTURE OUTLOOK

The Company is pursuing an ambitious five year development and expansion plan

estimated at Rs 42.9 billion. Key objectives of the strategic plan for the next five

years (2005-06 to 2009-10) are the following:

Expansion of transmission network by 608 Kms from 2,942 km in 2005 to

3,550 km by 2010, enhancing capacity from 1,300 MMCFD in 2005 to 1,700

MMCFD by 2010.

Expansion of distribution network and supply mains by 5,236 km from 25,764

km in 2005 to 31,000 km by 2010 connecting 600 new towns and villages in

Sindh and Balochistan

Enhancement of gas supply to power plants, industrial and commercial

sectors including supply of gas to previously deprived areas in the domestic

sector.

Increase of the customer base from nearly 1.8 million to 2.2 million by adding

447,000 new customers to the Company’s system.

Consistent appreciation in shareholder’s value by increasing the company’s

asset base and significant improvement in productivity and efficiency.

Focus on improved, friendly and efficient customer services under the vision

of “Service with a smile”;

Establishment of 16 fully automated (additional 8 in progress) on line

customer facilitation centres;

Multiple bill payment options and channels (ATM, Call Centres, ORIX POS,

Internet, Drop Boxes, NADRA-Kiosk);

Latest technology digital prepaid meters with improvement of call centres to

include an online customer information system.

Revamp the current business processes, to improve company efficiency and

implement ERP, CIS, GIS and the best business policies for ISO 9000

certification;

Increase surveillance and introduce an automated emergency response

system (ERS) and SCADA for the security of company assets including the

transmission and distribution networks;

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Improve the quality of human resource through career planning, training of

employees and development of management;

Implement environment management system, occupational health and safety

system as required under Certification ISO 14001 and OHSAS 18001

standards;

Set up Enterprise Information System (EIS) in all areas of business using

state of the art technology to make SSGC the “Most IT Enabled Company;”

Human resource development and empowerment of employees through

career planning and continuous management/vocational training.

Community support services and corporate communication initiatives to meet

the national and social responsibilities, as a good corporate citizen.5

5 www.ssgc.com.pk/outlook

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

RESEARCH METHODOLOGY

Methodology is a major component of any research report which enables to

choose the right techniques and tools for the collection of data and analysis of

data in order to get the accurate results. It is vital element for research and

provides in-depth details of chosen strategies and tools for gathering and

analysing data.

The aim of this topic is to emphasize and validate the methods and line of actions used in

conducting this report. The topic includes the explanation of various stages of data

collection methods used in obtaining primary and secondary data.

Data Collection Methods:

Data collection is the central part of any research, which requires an effective planning.

There are two generic classification of data on which research project design depends,

one is primary, and the next one is secondary, so I have chosen the strategy to gather data

from the previous work done (secondary data) and gathered (Primary) data myself, which

is beneficial for this project, and was not available.

Primary Data Collection

Primary data is that kind of data which is required to research purpose, but not collected

before, so that first-hand data which collected by self called primary data.

Primary data can be collected by one, or combination of more than one method, such as

observation, experimentation, interviews and questionnaires. Whereas choosing of

method to collect the primary data depend on the nature of research report. I chooses the

method of primary data collection for this report, are the combination of in-depth

interviews and questionnaire.

Data Collection Method

Primary Data Secondary Data

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Secondary Data Collection

Secondary method of data collection includes the piece of work which is being already

used for some other purpose or work. In secondary data collection we have the facility to

use data which may be available on desk. Major sources of secondary data collection used

in this research report, collected through the internal sources of SSGC, which was in the

form of printed material, that includes reports of sale, price lists, consumption and market

share, segment wise data, operation and finance documents, and others which required

time to time, another sources for data collection was external sources, like public

information and governmental statistics figures, news, electronic media, and technology,

like search engines electronics journals, books, and websites.

Limitation of the Study

Following limitations hamper research report work:

Time constraints

Limited resources

Limited access of data, and instrument in SSGC House.

Confidential information (ambiguity of answers)

Language barriers

Inaccuracy in response

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Chapter # 02

Organization Structure

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

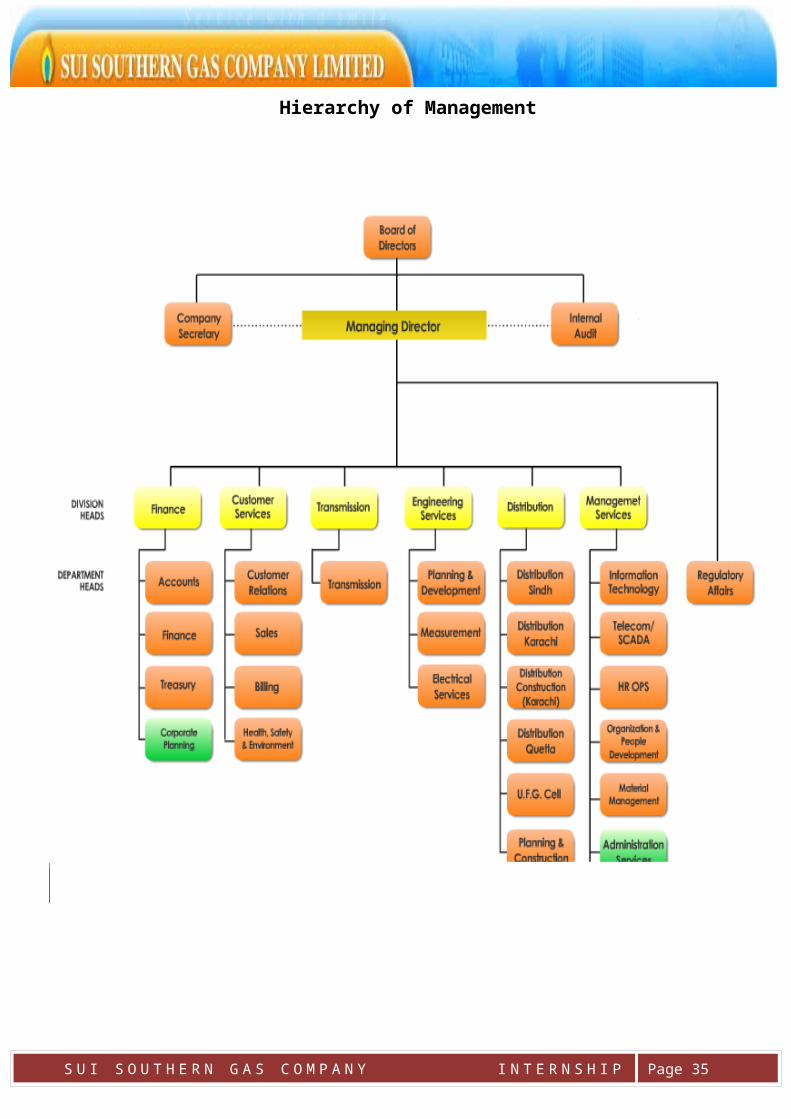

ORGANIZATIONAL STRUCTURE

The Company is organized into six functional divisions -Transmission, Distribution,

Commercial, Engineering Services, Management Services, and Finance. Each

division is headed by a Senior General Manager (SGM) assisted by a team of

professional staff, with the exception of Finance, which is headed by the Chief

Financial Officer (CFO). Policy matters relating to the natural gas sector are handled

by the GOP. OGRA is responsible for regulation, pricing, revenue determination and

compliance to service standards. The Board of Directors has the overall

responsibility for the management and control over the Company. The management

enjoys operational autonomy. The major portion of the work force consists of

technically qualified and skilled personnel.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Hierarchy of Management

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Chapter # 03

OVERVIEW OF THE FINANCE DEPARTMENT

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

OVERVIEW OF THE FINANCE DEPARTMENT

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

MAJOR ACCOUNTING POLICIES

Property, Plant &Equipments:

Assets are not revalued and historical cost is taken into account. Property, plant

and equipment except freehold land, leasehold land and capital work in progress

are stated at cost less accumulated depreciation. Freehold land, leasehold land

and capital work in progress are stated at cost

FINANCE

Finance

Payroll

Insurance

Payments

Gas Purchase

Transmission Project

Treasury

Cash & Bank

Loans

Investments

Gas Sales

Taxation

Revenue Control

Accounts

Cost & Revenue Budget

Fixed Assets

MIS

Distribution System

Financial Feasibilities

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Depreciation on compressor, transmission lines and other operating assets is

calculated under the straight line method over their estimated remaining useful

lives. It is charged from the dates these projects are available for intended use

upto the date these are disposed off.

Stock-in-trade:

The stock in trade comprises of Gas in pipelines and Meter manufacturing

division.

Stock of Gas in transmission pipelines is valued at lower of cost determined

under the weighted average basis and net realizable value whereas the materials

for meter manufacturing division is valued at lower of moving average cost and

net realizable value.

Net realizable value is the estimated selling price in the ordinary course of

business less the estimated costs of completion and the estimated costs

necessary to make the sale.

Stores, Spares and Loose Tools:

These are valued at cost determined under the moving average basis less

impairment losses, if any. Goods in transit are valued at cost incurred up to

the balance sheet date

Trade Debts:

Trade debts are carried at cost less provision for doubtful debts, if any. Balances

considered bad and irrecoverable are written off when identified.

Trade and Other Payables:

Liabilities for trade and other payables are carried at cost which is the fair value

of the consideration to be paid in the future for goods and services received.

Deferred Credit:

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Amount received from customers and the government as contributions and

grants for providing the service connections, extention of gas mains, laying of

transmission lines, etc are deferred and are recognized in the profit and loss

account over the useful life of the related assets.

Revenue Recognition:

Revenue from Gas sales is recognized on the basis of gas supplied to customers

at rates periodically announced by the Oil and Gas Regulatory Authority (OGRA).

The meter rental is recognized monthly at specified rates for various categories of

customers on an accrual basis whereas the sale of meters and gas condensate is

recognized on dispatch to the customers.

Deferred credit income is amortised to the profit and loss account over the useful

life of the related assets. Dividend income on equity investments is recorded on

accrual basis.

However the company is required to earn a minimum annual return before

taxation of 17% per annum o the net average operating fixed assets (net of

deferred credit) for the year. Income earned in excess or short of the above

guaranteed return is payable to or recoverable from the Government of Pakistan

and is adjusted from or to the gas development surcharge payable to or

receivable from GoP.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Long Term Deposit:

Long Term deposits consist of security deposits from Gas customers and gas

contractors.

Gas customers’ deposits represent Gas supply deposits based on an estimate

of three months consumption of gas sales to industrial and commercial

customers while deposits from domestic customers are based on the rates

fixed by the

Government of Pakistan. These deposits are repayable and adjustable on the

disconnection of gas supply.

Security deposits from contractors are free of mark-up and refundable on the

cancellation of contract.6

6 Accounting documents of SSGC

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

AREAS OF WORKING

I sought opportunity to join SSGC to upgrade my skills in multi-dimensional approach

to the section of the Finance Department. Whatever I attained there is elaborated as

under:

General Ledger

Fixed Asset and Capital Budget

Gas Purchase

Bid Bond

Inventory Accounting

Cost and Revenue Budget

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Chapter # 04

General Ledger

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

GENERAL LEDGER SECTION

Function:

Processing of all journal voucher (JV) from different section and location in

finance department.

Resolution of queries raised by the ERP system during JV processing.

Posting of all financial modules to general ledger.

Processing of reports from oracle on monthly, quarterly, yearly basis for top

management.

Processing of reports from oracle on monthly, quarterly, yearly basis for oil

and gas regulatory authority (OGRA).

Purpose:

To maintain proper and accurate, books of accounts.

To facilitate and co-ordinate the annual audit.

To comply with the policies and the procedure notified by OGRA from time to

time.

To comply with the policies and the procedure notified by Security and

Exchange Commission of Pakistan (SECP).

To report the results to board of directors and share holders of the company.7

General Ledger- Reports:

With the help of Oracle Financial Application general ledger reports can be viewed.

General Ledger Reports facilitate tracing back each transaction to the original

source. These reports list beginning and ending account balances and all journal

entry lines affecting each account balance. The report provides detailed information

on each journal entry line including source, category and date. Through this option

the journal details can be reviewed and checked for errors.

7 Introduction by Muhammad Saleemmemon (Manager – GL)

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

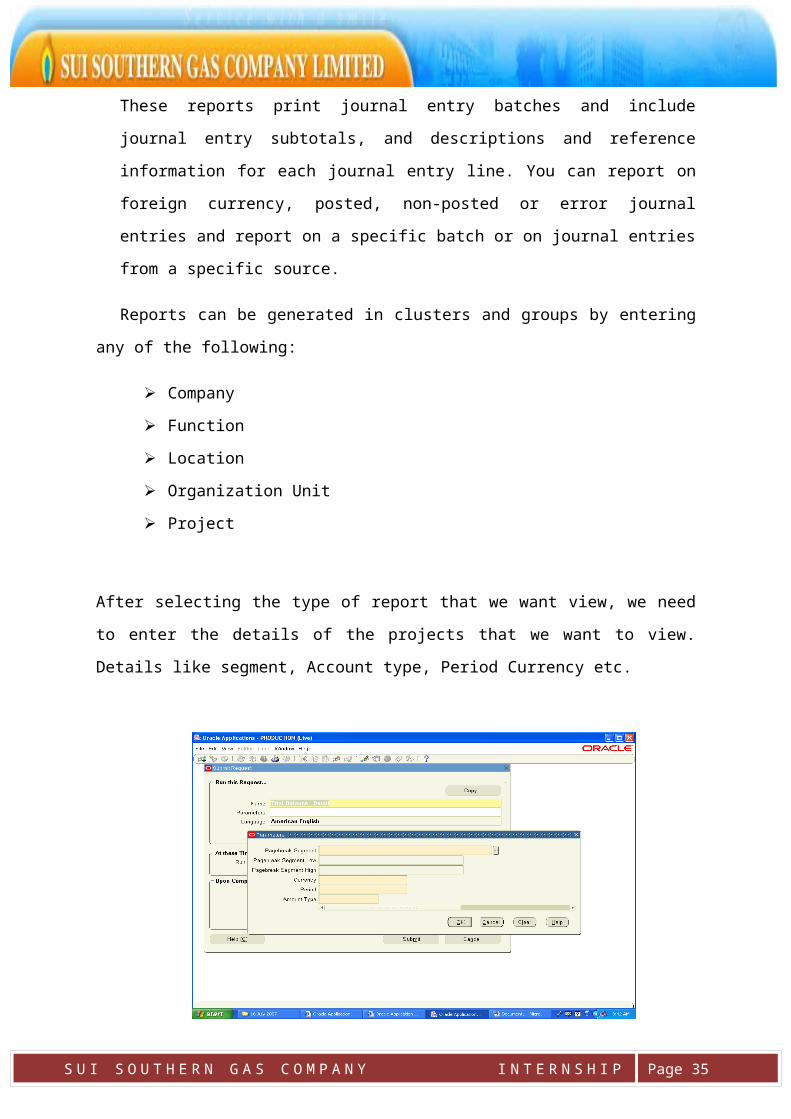

For generating general ledger reports we first need submit a request. We can either

submit a single request or a request set.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

After selecting the type of request, we need to enter the type of report that we

want to view. In order to run the request, first we need to type in the name of the

report that we want to generate. Oracle GL provides us with a number of options. For

example we can view a detail Trial Balance detail report or an account analysis

Reports etc.

Accounts Analysis Reports:

These reports list the accumulated balances of a range of Accounting Flex fields

and all journal entries that affect that range. Detailed information is provided for

each journal entry line which includes the source, batch name, and description.

Trial Balance Reports:

Use trial balance reports to review account balances and activity in summary or

detail.

Journal Report:

These reports print journal entry batches and include journal entry subtotals, and

descriptions and reference information for each journal entry line. You can report

on foreign currency, posted, non-posted or error journal entries and report on a

specific batch or on journal entries from a specific source.

Reports can be generated in clusters and groups by entering any of the following:

Company

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Function

Location

Organization Unit

Project

After selecting the type of report that we want view, we need to enter the details of

the projects that we want to view. Details like segment, Account type, Period

Currency etc.

As soon as the request is submitted, Oracle application starts processing the given

request and as a result of that it provides the user with various options which

includes viewing the output or details of the requests. It also provides the option of

diagnostics and holding and canceling of a request.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

The Screen shot below shows the format of the generated reports.

By selecting the view detail button, the user can easily view the details of the project

which includes the date, submission date, completion date, status etc8

8 From Oracle system of SSGC

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Chapter # 05

Fixed Asset

&

Capital Budget

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

FIXED ASSETS & CAPITAL BUDGET PROCESS

FUNCTION

To maintain and control the fixed asset of the company

Working of Fixed Asset:

Budget Proposal

The budget section of finance department prepares capital expenditure budgets

annually for all the department of SSGCL. Whenever a budget is to be prepared for

any department, the budget section notifies the department to prepare list of assets

required by them & forward it to the budget section. On receiving the requirements,

the budget team examines it & discusses all particulars with the related head of

department & staff giving special consideration to the justification of fixed asset

requirement & funds available with the company.

At this stage, the budget team may reduce the requirements of fixed assets of the

department, which may be considered to be necessary as that may be defined to

latter period.

The budget [in the form of budget proposal] is now sent to GM & SGM for its

approval/changes which may be made by them & finally to the M.D for its approval

the case of transmission project which exceeds Rs.100 million approval is then

sought from the government by filing PC-1 form & after its approval , same

procedure is followed for others.

When the budgets for all the departments have been finalized and approved by MD,

then agenda is prepared by budget section, which is reviewed by finance committee,

the board of directors’ grants approval to the agenda and now the budgets are

authorized to be followed.

Each department is now intimated through inter departmental note (along with a

copy of their budget) that the budget has been approved.9

9 Introduction by GulabBaloch (Deputy Chief Manager SSGC)

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Fixed Asset purchasing process:

In order to purchase an asset, fixed asset requisition (FAR) is required to be filed

by concerned department, which should be approved by the head of that

department. FAR contains details of assets required by the department.

The FAR is now forwarded to Procurement department, where Deputy Manager

checks whether the FAR falls within the budget. The procurement department invites

quotations through tender (if not available in store) and on the basis of commercial

and technical evaluation and lowest bidders, a supplier is selected (all such

procedures documented in Evaluation Report) and then Purchase order (PO) is

prepared and sent to supplier.

All assets are received by the KT stores department, where quality inspection is

conducted (however not documented) and then a Material Receiving Statement

(MRS) is generated and a copy of which is forwarded to the finance department.

Following entry is generated:

Inventory receiving account xxx

AP accrual account xxx

On delivery of asset to the concern department, following entry is generated:

Asset clearing account xxx

Inventory receiving account xxx

When invoice received by finance department, Account payable department enter

invoice in AP module which match invoice with material receiving statement and

following entries are generated:

AP accrual account xxx

Liability account xxx

Asset cost account xxx

Asset clearing account xxx

Depreciation expense xxx

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Accumulated depreciation xxx

At payment of invoice, following entry is generated:

Liability account xxx

Bank xxx

Fixed Assets Purchase Process:

Requisition verified by the

inventory section and

approved by CM, DGM and

GM/MD

Requisition sent to the

procurement department for

order placement

Supply of assets by the

supplier at Receipt

&Despatch section at Karachi

Terminal

Asset delivered to the user /

requisitioning department

Details incorporated in the relevant

records at month end

Fixed Asset Requisition

sent to the inventory

section duly authorised by

the departmental head

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Depreciation and Adjustment Process

Once an asset has been capitalized, working for its depreciation starts. Full year

depreciation is charged for the first year regardless of its purchase data. The

company uses the straight line method of depreciating except for meter plant, where

reducing balance method is used. Depreciation rates differ for different assets. It

even differs for same assets in different cities.

In the certain situation we call for making adjustments e.g. transfer of an asset from

one unit to another, different between assets in books and its physical existence etc.

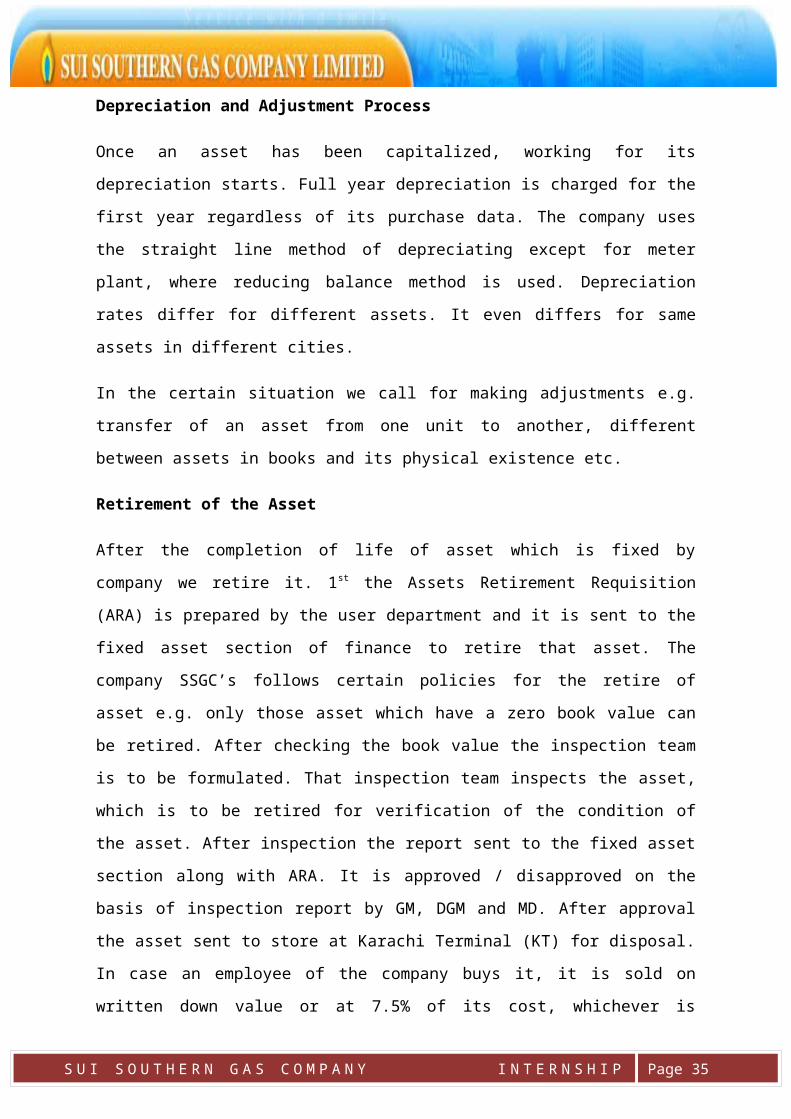

Retirement of the Asset

After the completion of life of asset which is fixed by company we retire it. 1 st the

Assets Retirement Requisition (ARA) is prepared by the user department and it is

sent to the fixed asset section of finance to retire that asset. The company SSGC’s

follows certain policies for the retire of asset e.g. only those asset which have a zero

book value can be retired. After checking the book value the inspection team is to be

formulated. That inspection team inspects the asset, which is to be retired for

verification of the condition of the asset. After inspection the report sent to the fixed

asset section along with ARA. It is approved / disapproved on the basis of inspection

report by GM, DGM and MD. After approval the asset sent to store at Karachi

Terminal (KT) for disposal. In case an employee of the company buys it, it is sold on

written down value or at 7.5% of its cost, whichever is higher. And some old assets,

which are fully scraped and not present physically, are deleted from the books

through approval of the management.10

10 From the documents of Fixed Assets Section

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Fixed AssetsRetirement Process:

Asset Retirement Advice

prepared by the user

department and sent to

the inventory section

Inspection of the asset to

be retired is conducted for

verification of the

condition of that asset

Section Inspection

report sent to the

inventory along with

ARA

Retirement advice is

approved / disapproved

on the basis of inspection

report by GM, DGM and

MD

Asset sent to store at KT

for disposal

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Chapter # 06

INVENTORY ACCOUNTING

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

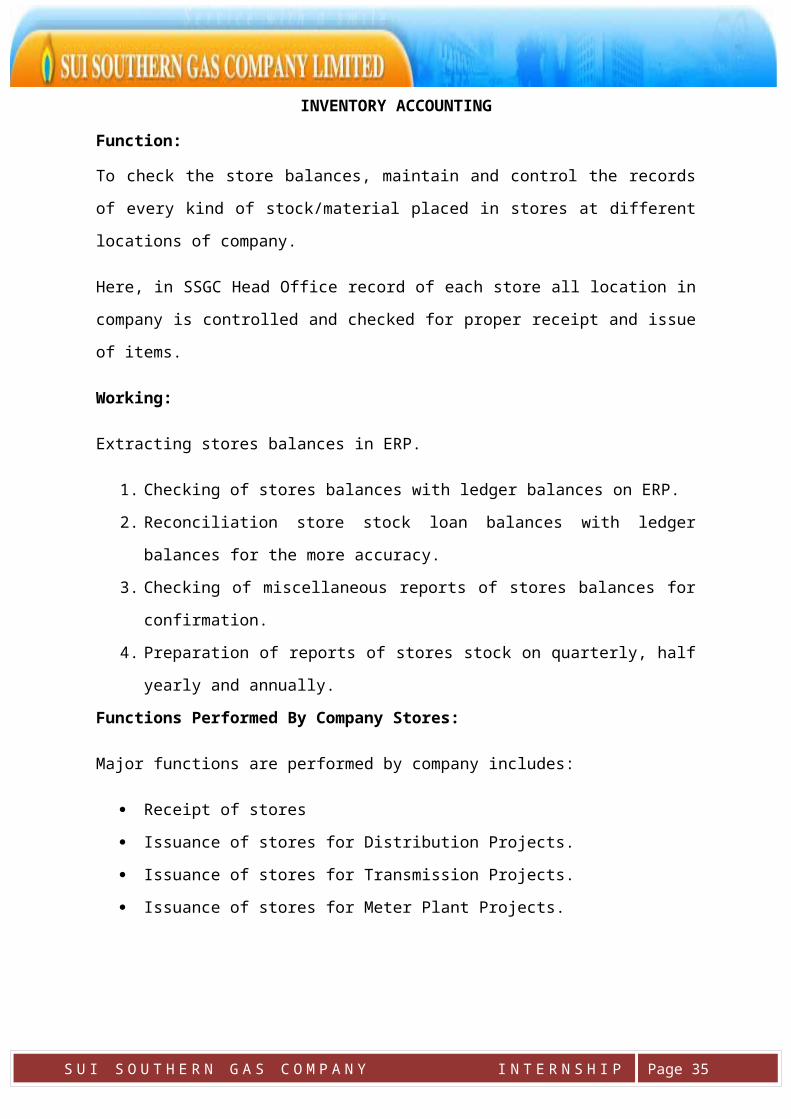

INVENTORY ACCOUNTING

Function:

To check the store balances, maintain and control the records of every kind of

stock/material placed in stores at different locations of company.

Here, in SSGC Head Office record of each store all location in company is controlled

and checked for proper receipt and issue of items.

Working:

Extracting stores balances in ERP.

1. Checking of stores balances with ledger balances on ERP.

2. Reconciliation store stock loan balances with ledger balances for the more

accuracy.

3. Checking of miscellaneous reports of stores balances for confirmation.

4. Preparation of reports of stores stock on quarterly, half yearly and annually.

Functions Performed By Company Stores:

Major functions are performed by company includes:

Receipt of stores

Issuance of stores for Distribution Projects.

Issuance of stores for Transmission Projects.

Issuance of stores for Meter Plant Projects.

In order to fulfill these functions , company has several stores ate different locations.

And here we go in the detail of these stores by using tables.11

11 Introduction by Muhammad SaleemDurani (Manager)

COMPANY

DISTRIBUTION TRANSMISSION METER PLANT

DISTRIBU-TION STORE

KARACHI

MAIN STORE SITE

GULSHAN STORE

ST.STORE SITE

DISTRICT SITE

SINDH

HYDERABAD SUKKUR

NAWABSHAH LARKANA

ST. HYDERABAD ST. SUKKUR

QUETTA

QNGDP

ST. QUETTA

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

MAJOR FUNCTIONS OF COMPANY

DISTRIBUTION STORES

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

TRANSMISSION STORES

TRANSMISSIONOPERATION STORE-KT HQ-III HYDERABAD

HQ-II NAWABASHAH HQ-I, SUKKUR

IRBPC-HQ-DADU IRBPC-HQ –SHIKARPUR

QPL(O&M)-SIBI QPL(O&M)-QUETTA

CD-KHADEJI GRIEP PROJECT KHADEJI

PIRKOH-SUI ST. KHADEJI

DISTRICT KHI KHADEJI DISTRICT KHI TERMINAL

METER PLANT

METER PLANT ST. METER PLANT

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

METER PLANT STORES

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Store Dealings:Store accounting is based on meaning average basis. Each item has been allotted

index number according to the description and specification of material. Store index

is based on seven digits having fields of 00/00/000. 1st 2 digits denote main section

to whom material is to be sent e.g. HO, Trans, MMP, etc. 2nd 2 digits denote sub

section e.g. Finance in HO etc. 3rd 3 digits denote serial no of item like as Printing

Paper, Pen, Pipes etc. Stores system is based on the following store documents:

1. Material Receiving Statement

Foreign Receiving Statement.

Local Receiving Statement

2. Material Requisition

3. Inter Store Stock Transfer

4. Material Return Voucher

5. Adjustment Memo

Store accounting is based on above store documents for generation of cost of

material received of issued.

Purpose of Store Document:

1. Material Receiving Statement

When the material is received in the store department by the supplier or the

company the store department sends two receipts 1st for supplier or respected

department and 2nd for store section for maintaining the record and controls it.

That receipt is known as Material Receiving Statement. If the material is supplied

from abroad in that case the Foreign Receiving Statement is issued and in the

case of local supplier the Local Receiving Statement is issued. When the receipt

is received by the store section from the store department the store section check

R/S number, date of issue, delivery challan / invoice no: Supplier name and

address, index number, description, units, and quantity (ordered, received, and

balance) through ERP that the received material is present at store department or

not. After confirmation the receipt is put into records.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

2. Material Requisition

When the store department issue the material to the user department according

to user demand the receipt is send to the store section for informing that we issue

that material to that user department in case of availability and approval of high

level management. That receipt known as Material Requisition. After receiving

that receipt the store department check the indenting department and particular

of job, store location code where from the material is issued, requisition serial

NO:, date of issued material, company code, function, account, organization unit

and project code, order number, quantity required, store index number, and

quantity issued through ERP that the requisite material is issued from store

department or not. After confirmation the receipt is put into records.

3. Inter Store Stock Transfer

Sometimes material is required for one store due to out of stock and that material

is in access for another store department then needed department sent the

requisite for material and then material will transfer from accessible point to out of

stock point and receipt is to be sent to the store section for maintaining and

controlling the account with the name of Inter Stores Stock Transfer. The store

section check that from which store department to which store department

material is transferred along with the respected location code. And store section

also check the issuing store code NO:, serial NO:, date of transferring,

description of material transferred, store index number, unit code and quantity

transferred through ERP that the transferred material is in actual transferred from

one store department to another store department. After confirmation the receipt

is put into records.

4. Material Return Voucher

When the material is issued against the requisition sometimes material is not in

use or unserviceable and the user department return that unserviceable material

to the store department. When it is received by the store department they send

the voucher to the store section with the name of Material Return Voucher for the

purpose of maintaining. When it is received by the store section they check that

from which location material is return, department name, date of return,

organization code, serial number, description, job number, M.R NO. & date

against which drawn, index NO., and quantity returned through ERP that the

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

returned material is correctly record or not by the store department. After

confirmation the receipt is put into records.

5. Adjustment Memo

Sometimes during the entry we are doing mistake like wrong entry of index

number, invoice number, quantity, amount, job number, or others to correct these

mistake companies make a journal voucher (JV) and correct the mistake. After

correcting the mistake the store department sends a receipt to the store section

with the name of Stores Adjustment Memo for updating changes. When the

receipt is received by the store section they check date of changing, store index

no:, job number, quantity and remarks for what purpose that adjustment memo

made.12

12 Documents of Store Department

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Chapter # 07

COST & REVENUE BUDGET SECTION

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

COST & REVENUE BUDGET SECTION

Function:

The major function of cost and budget section is cost controlling and maintaining of

revenue expenses and also accumulation of revenue cost which is incurred during

the period, and planning for allocating the budget to the individual department. And

another function of this section is to calculate the cost of operating and

administration section.

Purpose:

To minimize the extra cost

To operate the organization effectively and efficiently

Closely watch t the individual department

To run the organization smoothly

To control the cost of operating and administration.13

Budget Planning Process:

Cost &Budget is one of the hub section of finance department. This section is

indispensable because planning & cost both are the backbone of every successful

organization and this section is first and foremost responsible for the budget

planning. Budget planning begins before the distribution of budget for the new fiscal

year. The SSGC provide the authority to every department to make their budget like

wise, it means department wise and it is controlled and maintained by the cost and

budget section in finance department. The 1st step of budget scheduling is

“Proposal”. This section send proposal to every department of company in order to

know the requisite budget by the departments. Every department suggest their

required budget for the new fiscal year along with the details where they want to

spend budget and send the proposal back to cost & budget section. The section

checks their budget proposal and compare with previous budget. In case of big

difference between the current and previous budget the budget will not approved

before the justification of respected department.

13 Introduction by the Manager of C&RBS)

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Then this section brings together these proposals according to organizations wise

and sends these proposals to the board for the approval. The board makes

necessary changes and approves the compiled budget and report will send to every

department. And approved proposals are loaded in ERP system (Oracle Financial).

The budget is to be made according to year wise but it is issued quarter wise. After

that we are uploading the budget.

The process of uploading budget is shown below:

Uploading Budgets:

Usually budget is uploaded using Application Desktop Integrator (ADI). ADI allows

the user to create and modify budget in an Excel spreadsheet which can then be

uploaded to Oracle General Ledger.

For maintaining security, the people of the respective department are provided with

their own user ids and password. Access is allowed only to limited individuals

For uploading the budget we first need to select the journal type i.e. budgeted journal

and the numbers of Journal

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Before any data can be uploaded, the sheet needs to be made unprotected first by

selecting the “Unprotect Sheet” option from the tools menu.

While viewing the budget worksheet that we want to upload, we have to choose

Upload to Interface from the Ledger icon in the ADI toolbar. After that decide whether

to upload All Rows or Flagged Rows (those marked with Y).

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Start the budget upload process by selecting one of the following options

Start if no errors in upload

Start regardless of errors

Choose the ok icon to initiate the process When the process completes the system

will notify of the completion status.

After the uploading of budgets, these are checked to make sure that budgets are

correctly allocated in their accounts. After having complete satisfaction the cost &

budget section release or allocate the budgets in the accounts of every department.

Release of budgets completes the process of budget allocation. In the new fiscal

year the departments perform their activities and incur expenses. The expenses are

debited in the accounts causing the budget accounts credit.14

14 Oracle system of SSGC

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Additional Budget & Re-appropriation:

This Re-appropriation form will use due to shortfall in budget or the departments

spend their budget before the specified period or that project is not mentioned in

their budget for whom they are sending the requisition. In order to solve this problem

which are occurred due to shortfall in budget, 1st the required department sends the

appeal for Additional Budget or Re-appropriation to CFO for approval of required

material. After the approval from CFO they sent that request to cost and budget

section for further procedure.

The cost and budget section checks that from which department the required

department to take budget and also checks that is that department budget is

available or not and also check the required department is really needed for that

material or not.

After checking and confirmed these things the cost and budget section transfer the

budget from the required department is needed through ERP.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

Chapter # 08

CONCLUSIONS&

SUGGESTIONS

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

CONCLUSIONS

1. There is not an availability of specific conference room to the internees.

2. The extra curricular activities except the project of the internees are not being

carried out.

3. There is no program of training and development for the contract based

employees to enhance their skills.

4. Top executive of the company are less willing to share their valuable

experiences with the juniors.

5. The company provides an opportunity of internship to the short number of

students.

6. There is no proper method for the recruitment and selection of the internees.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

SUGGESTIONS

1. It is worthy to respect SSGC management that provides a platform to the

students for internship, but I suggested to SSGC management that they also

provide a facility of conferencing room where internees carry on discourse

and discussion regard in projects.

2. SSGC management ought to arrange a debate contest and other extra

curricular activities among the internees on suitable day, that might be

enhance the inter personal and mental skills.

3. Contracted-based employees to be provided a facility of training and

development that might enrich and enhance skills of employees.

4. All executives must extend hand of moral and material support to diversify the

knowledge to staff members.

5. I request to SSGC management for increasing number of seats for internees,

that is noble cause to humanity and nation.

6. I further recommended that SSGC management to chalk out strategy for

proper recruitment and selection of internees that ultimately is benefit of

company itself.

S U I S O U T H E R N G A S C O M P A N Y I N T E R N S H I P R E P O R T 2 0 1 4 Page 35

REFERENCES

1. K.K.Dewit “ Modern Economics Theory And Practice “ 2005 published from University of Delhi.

2. M.SaeedNasir “ Money and Banking “ 2008

3. Prof. Dr. Anwar Ali Shah G. Syed “ Banking for Intermediate “ 1991 published by Kifayat Academy Karachi.

4. Christopher Viny “ Financial Management “ 2005 4th edition.

5. M.A. RaufBaig “ intermediate Accounting “ 2007

6. H. Kent Baker “ Financial Management “ 2000

7. C. Vann Horne “ Financial management “ 2006 8th edition.

8. Sher Mohammad Chudhary“ Statistics “ 2009 3rd edition.

9. Oxford Advanced Learners Dictionary 2007.

10.Annual report of SSGC 2008-09

11.Financial report of the year 2008-09

12.www.ssgc.com.pk/introduction

13.Annual report of SSGC

14.www.ssgc.com.pk/outlook

15.Accounting documents of SSGC

16. Introduction by Muhammad SaleemMemon (Manager – GL)

17.From Oracle system of SSGC

18. Introduction by GulabBaloch (Deputy Chief Manager SSGC)

19.From the documents of Fixed Assets Section

20. Introduction by Faiq and ShujjaShaikh (Managers of Gas Purchase)

21.Guider book of Gas Purchase Section

22. Introduction by Muhammad IqbalBatavia (Manager B.B.S)

23. Introduction by Muhammad SaleemDurani (Manager)