chapter 20instruction2.mtsac.edu/rjagodka/.../chap020_accounting_finance.pdf · variables...

TRANSCRIPT

Chapter 20

Accounting and Finance in the International

Business

Miscommunications

Miscommunications Many forms Video brief Miscommunications

Miscommunications in global accounting Different standards (reporting) Different languages (currencies) Different regulations (taxes)

Country Differences In Accounting Standards

Accounting systems evolve Respond to demand for accounting information

Difficult to harmonize across countries One study found that among 22 countries: 76 ways to assess the cost of goods sold 65 differences in calculating return on assets 20 ways to calculate net profits Different ways to count

Challenge to compare financial performance of firms from different countries

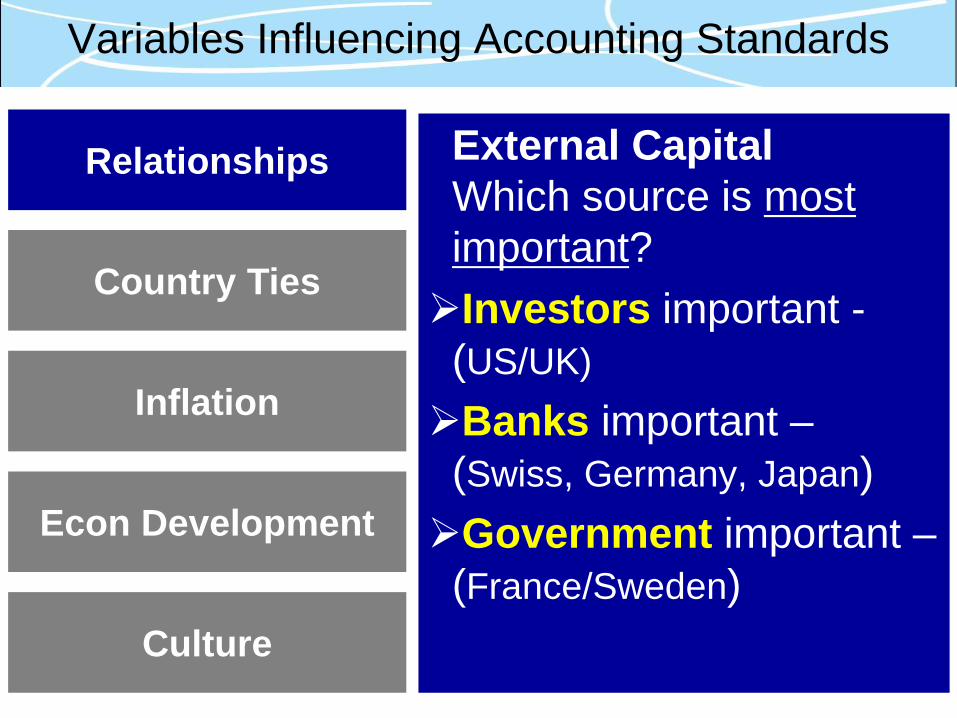

Variables Influencing Accounting Standards

Relationships

Country Ties

Inflation

Econ Development

External Capital Which source is most important? Investors important -

(US/UK) Banks important –

(Swiss, Germany, Japan) Government important –

(France/Sweden) Culture

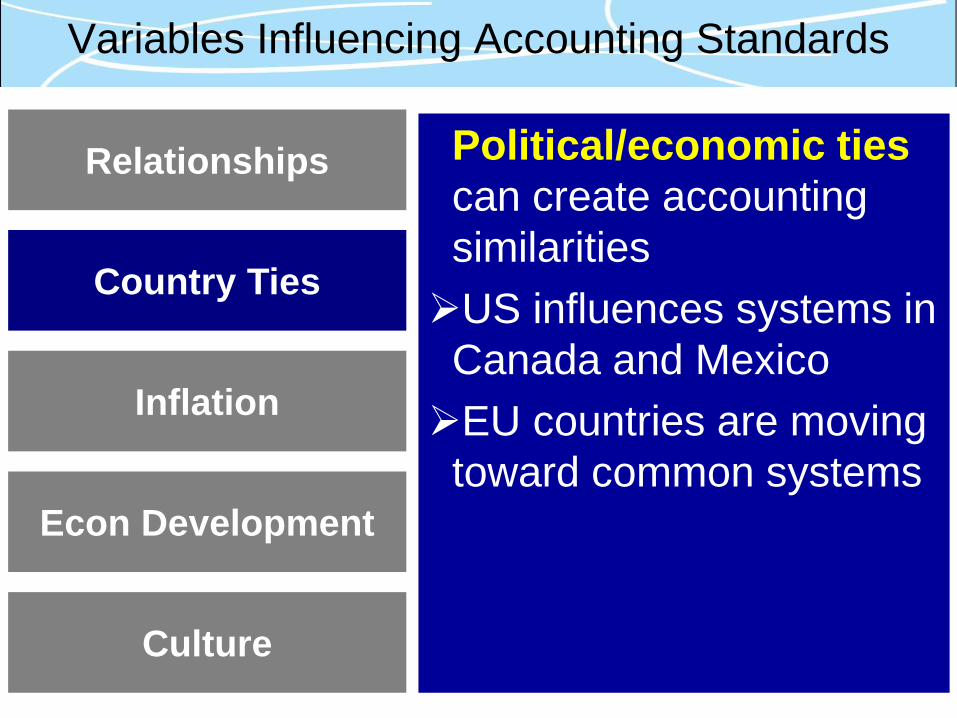

Variables Influencing Accounting Standards

Relationships

Country Ties

Inflation

Econ Development

Political/economic ties can create accounting similarities US influences systems in

Canada and Mexico EU countries are moving

toward common systems

Culture

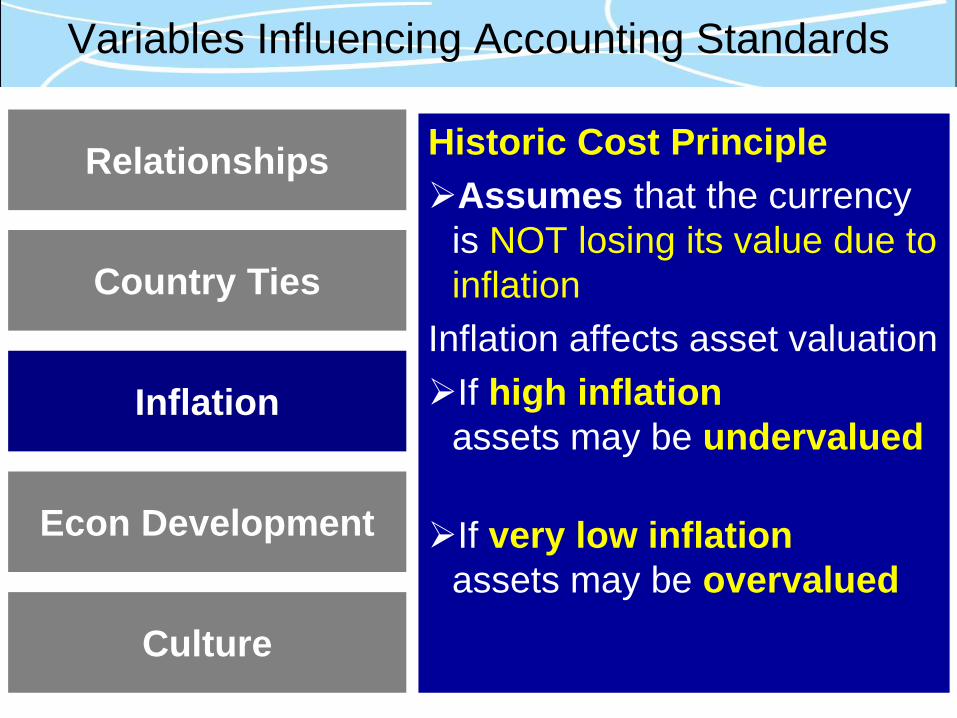

Variables Influencing Accounting Standards

Relationships

Country Ties

Inflation

Econ Development

Historic Cost Principle Assumes that the currency

is NOT losing its value due to inflation

Inflation affects asset valuation If high inflation

assets may be undervalued If very low inflation

assets may be overvalued Culture

Variables Influencing Accounting Standards

Relationships

Country Ties

Inflation

Econ Development

Developed nations More sophisticated

accounting systems Developing nations Inherited accounting

systems from former colonial powers

Culture

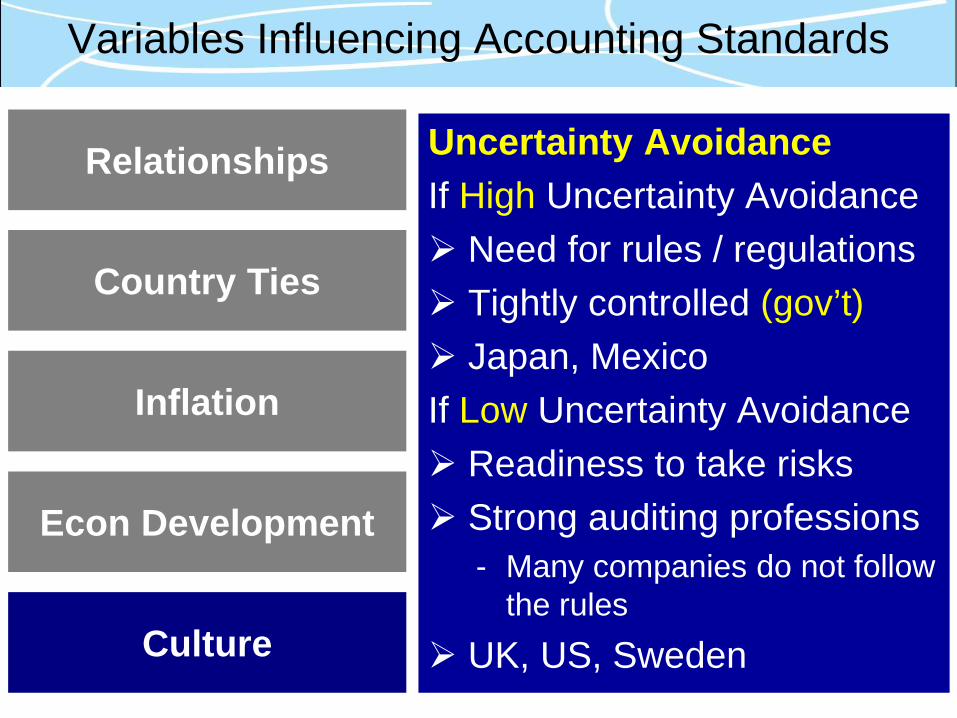

Variables Influencing Accounting Standards

Relationships

Country Ties

Inflation

Econ Development

Uncertainty Avoidance If High Uncertainty Avoidance Need for rules / regulations Tightly controlled (gov’t) Japan, Mexico If Low Uncertainty Avoidance Readiness to take risks Strong auditing professions

- Many companies do not follow the rules

UK, US, Sweden Culture

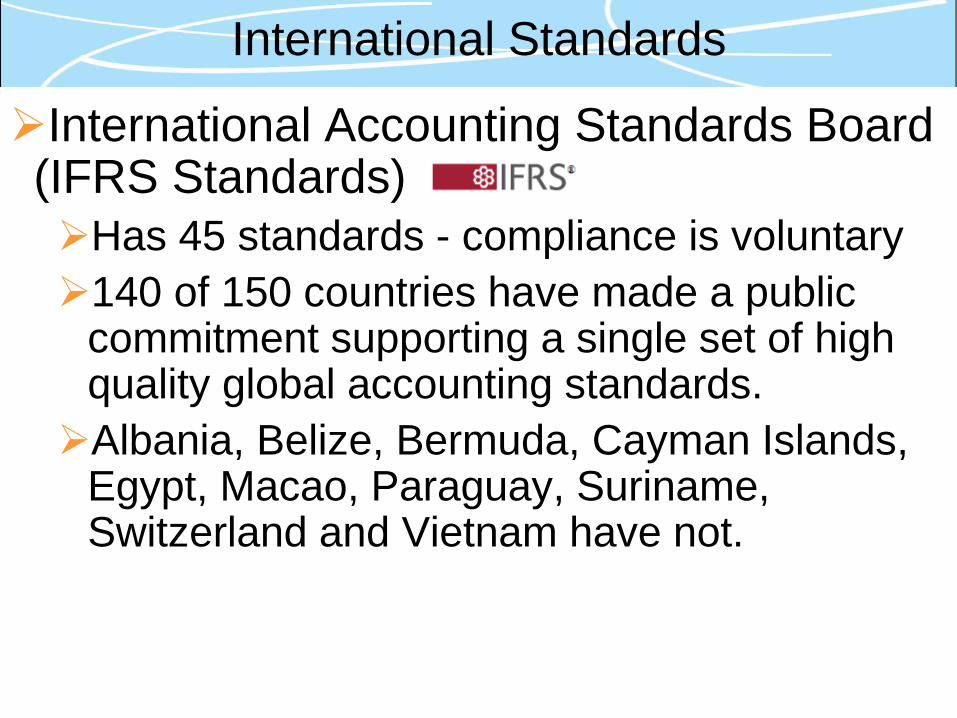

International Standards

International Accounting Standards Board (IFRS Standards) Has 45 standards - compliance is voluntary 140 of 150 countries have made a public

commitment supporting a single set of high quality global accounting standards. Albania, Belize, Bermuda, Cayman Islands,

Egypt, Macao, Paraguay, Suriname, Switzerland and Vietnam have not.

Consolidated Statements

Combine separate financial statements (two or more companies) to yield single set of financial statements (as if the individual companies were really one)

• Used by MNEs

Intra Firm Trade is HUGE Intra firm = Company imports/exports to itself, internationally

Over 50% of U.S. imports were intrafirm (2009)

Much variation: By Country • 74% of U.S. imports from Japan were intrafirm (2000) • 2% of U.S. imports from Bangladesh By Product Category • 70%+ of U.S. imports of autos, medical equipment and

instruments. • 2% of U.S. imports of rubber and plastic footwear

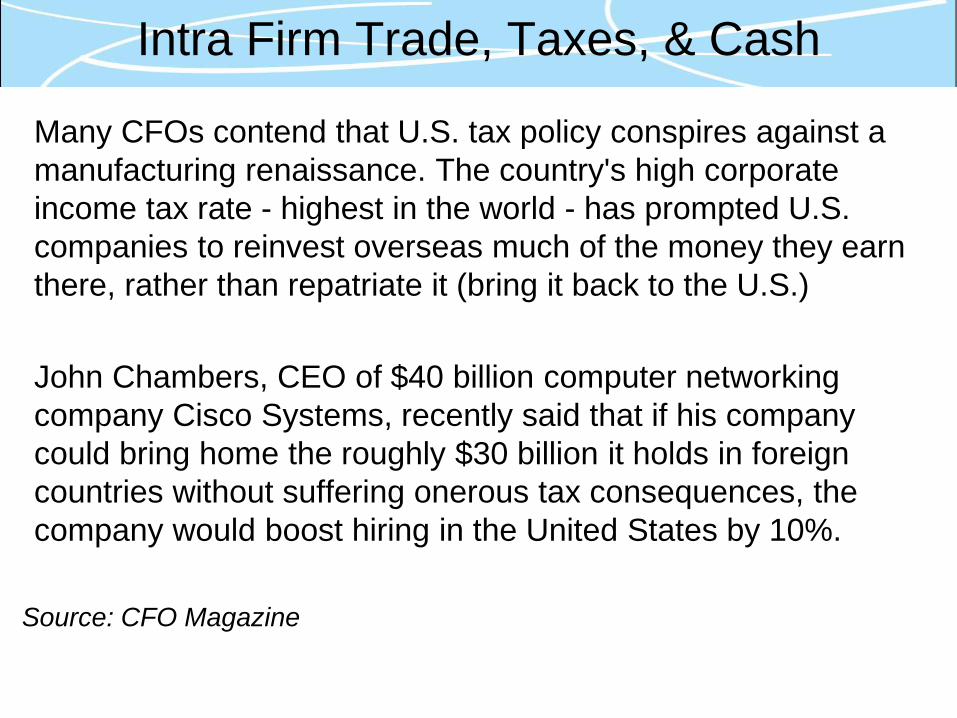

Many CFOs contend that U.S. tax policy conspires against a manufacturing renaissance. The country's high corporate income tax rate - highest in the world - has prompted U.S. companies to reinvest overseas much of the money they earn there, rather than repatriate it (bring it back to the U.S.)

John Chambers, CEO of $40 billion computer networking company Cisco Systems, recently said that if his company could bring home the roughly $30 billion it holds in foreign countries without suffering onerous tax consequences, the company would boost hiring in the United States by 10%.

Source: CFO Magazine

Intra Firm Trade, Taxes, & Cash

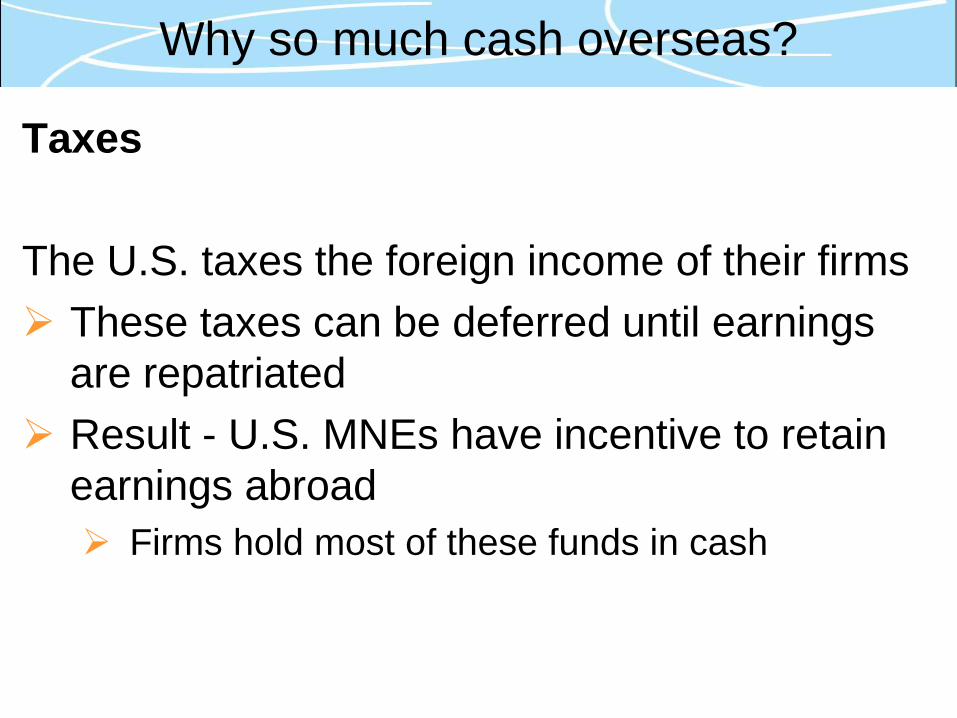

Taxes The U.S. taxes the foreign income of their firms These taxes can be deferred until earnings

are repatriated Result - U.S. MNEs have incentive to retain

earnings abroad Firms hold most of these funds in cash

Why so much cash overseas?

US Firm Cash Holdings Abroad = $1.4 trillion (11/2017)

Intra Firm Trade, Taxes, & Cash

https://www.marketwatch.com - Nov 22, 2017

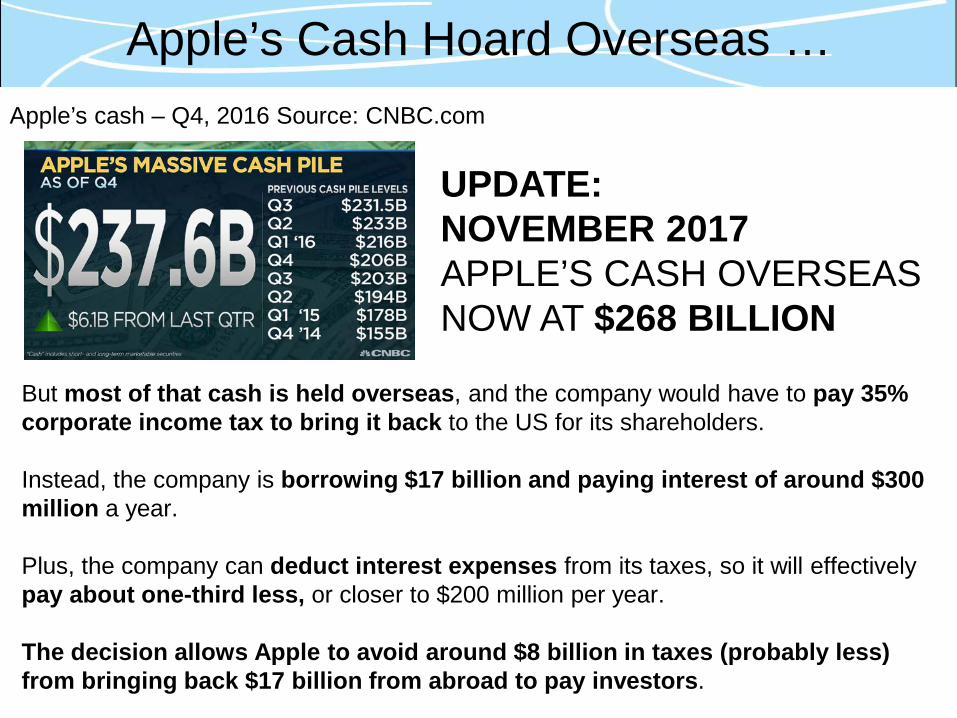

But most of that cash is held overseas, and the company would have to pay 35% corporate income tax to bring it back to the US for its shareholders.

Instead, the company is borrowing $17 billion and paying interest of around $300 million a year.

Plus, the company can deduct interest expenses from its taxes, so it will effectively pay about one-third less, or closer to $200 million per year.

The decision allows Apple to avoid around $8 billion in taxes (probably less) from bringing back $17 billion from abroad to pay investors.

Apple’s Cash Hoard Overseas … Apple’s cash – Q4, 2016 Source: CNBC.com

UPDATE: NOVEMBER 2017 APPLE’S CASH OVERSEAS NOW AT $268 BILLION

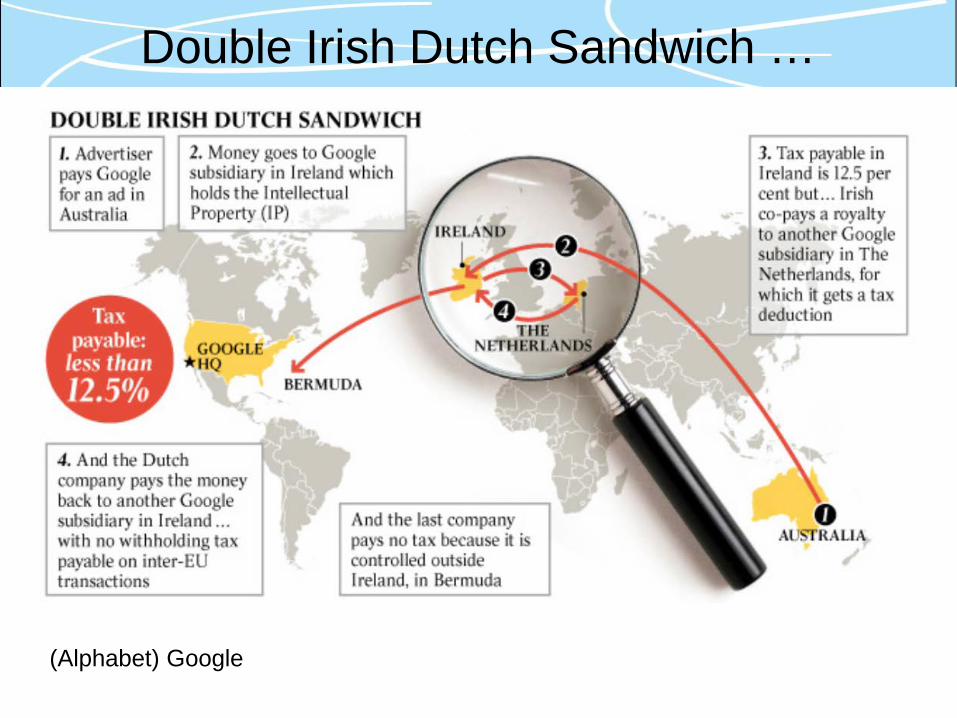

Double Irish Dutch Sandwich …

(Alphabet) Google

Where in the World to Make Your Profit …

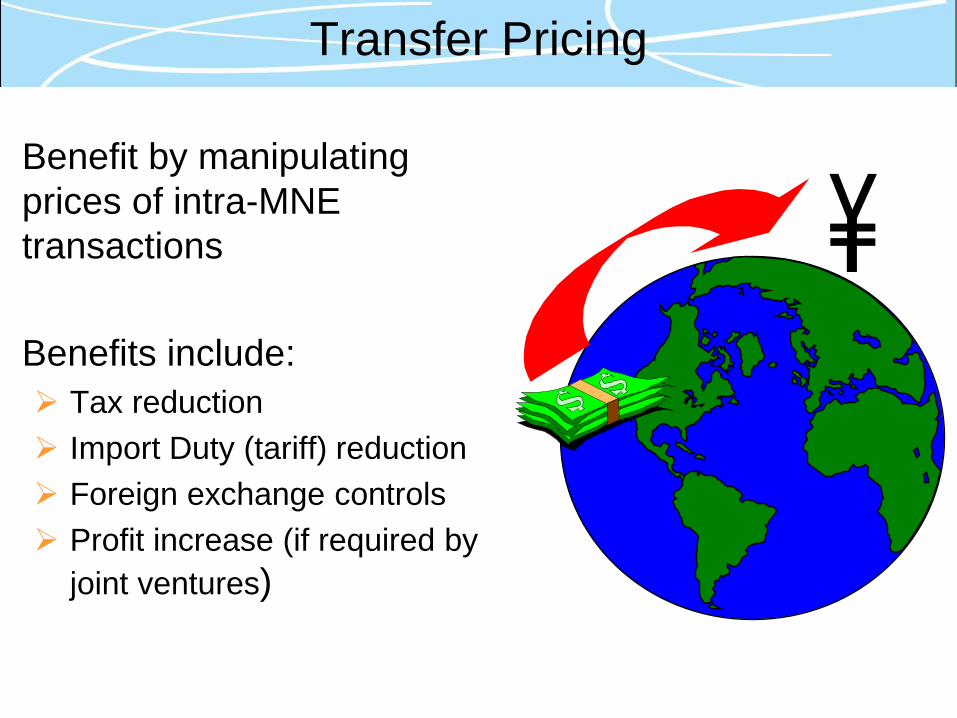

Transfer Pricing

Benefit by manipulating prices of intra-MNE transactions Benefits include: Tax reduction Import Duty (tariff) reduction Foreign exchange controls Profit increase (if required by

joint ventures)

Transfer Pricing & Performance Evaluation

Transfer prices are designed to maximize profitability and currency flows,

But they make an unbiased performance evaluation nearly impossible.

Firms may establish transfer prices because of: differences in national tax rates tough competition in foreign markets anti-dumping legislation

Internal transfer prices may also include the allocation of fixed costs, loans, fees, royalties, and other factors.

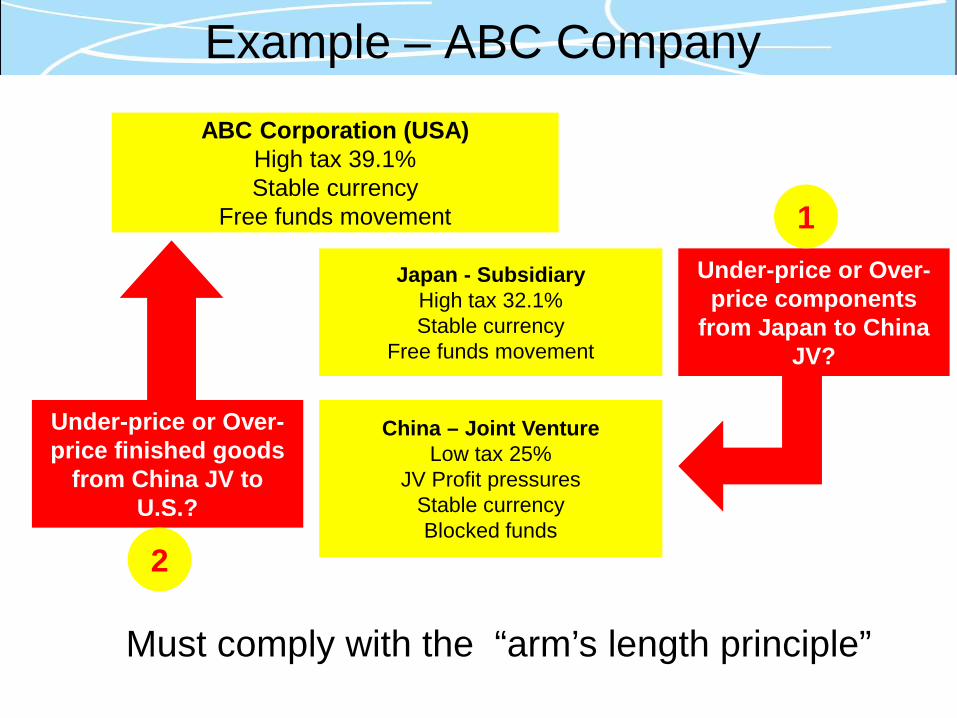

Example – ABC Company

Must comply with the “arm’s length principle”

Japan - Subsidiary High tax 32.1% Stable currency

Free funds movement

China – Joint Venture Low tax 25%

JV Profit pressures Stable currency Blocked funds

ABC Corporation (USA) High tax 39.1% Stable currency

Free funds movement

Under-price or Over-price components

from Japan to China JV?

Under-price or Over-price finished goods

from China JV to U.S.?

1

2

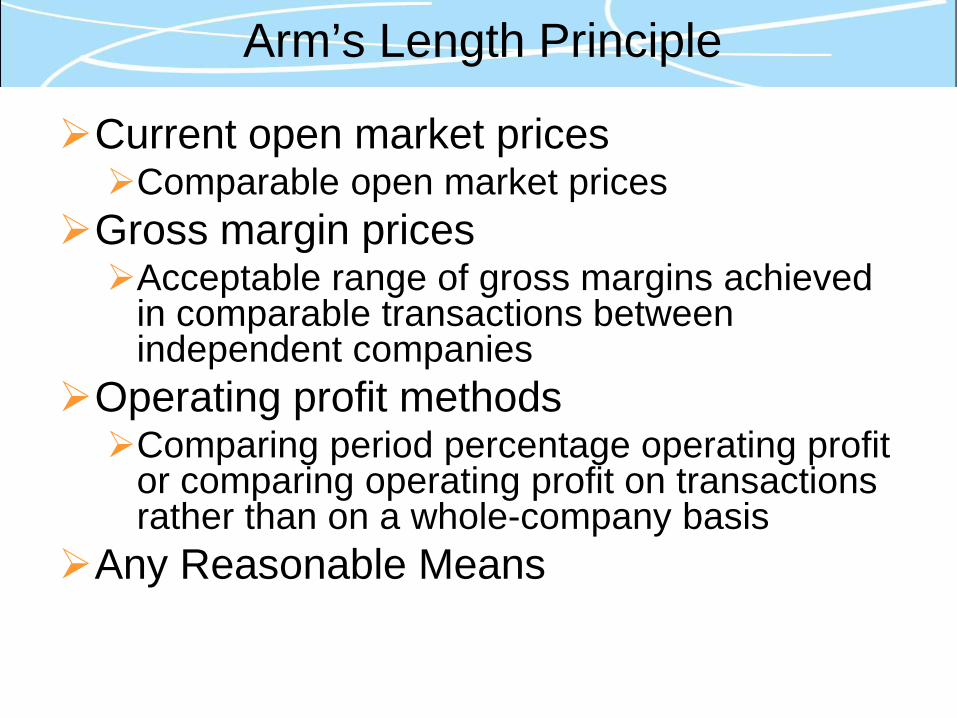

Arm’s Length Principle

Current open market prices Comparable open market prices

Gross margin prices Acceptable range of gross margins achieved

in comparable transactions between independent companies

Operating profit methods Comparing period percentage operating profit

or comparing operating profit on transactions rather than on a whole-company basis

Any Reasonable Means

Scenario – ABC Company

Assuming that we comply with “Arm’s Length” What are the Pros and Cons of this approach?

Japan - Subsidiary High tax 32.1% Stable currency

Free funds movement

China – Joint Venture Low tax 25%

JV Profit pressures Stable currency Blocked funds

ABC Corporation (USA) High tax 39.1% Stable currency

Free funds movement

Underpriced our components from Japan to China JV.

Overpriced our finished goods

from China JV to U.S.

1

2

Transfer Pricing Scenario

If under price exports from Japan subsidiary to China Tax savings (Japan [High tax] to China [Low tax]) Little exchange risk Can repatriate funds quickly (but earn less in Japan)

If over price exports from China JV to USA Pay lower tax (on less profit) in high tax country (USA) Little exchange risk Need to Repatriate funds from China – later can alter transfer price U.S. market may get high prices -> price escalation U.S. duty rates may be based on higher rate

Transfer Pricing Objectives

We need to identify company objectives: Where do we need access to funds? Where do we need to minimize tax liability? Where do we need to maximize profits? Where is price competition the most important?

Financial Management

Investment Decisions

Financing Decisions

Money Management Decisions

Capital Budgeting Estimating the cash flows

associated with the project over time, then discount them to determine (NPV) net present value Adjust for political risk Economic risk - inflation

Financial Management

Investment Decisions

Financing Decisions

Money Management Decisions

Source of Financing Global capital markets Cost of capital usually lowest Government may require local

sources to be used Local debt markets If expect currency depreciation

then use local debt sources Structure (debt vs equity) Norms vary by country Local norms or home country? Minimize cost of capital

Financial Management

Investment Decisions

Financing Decisions

Money Management Decisions

Minimize cash balances Invest cash reserves Short term get lower interest

Gains liquidity Long term get higher interest

Low liquidity

Reduce transaction costs Every time cash is changed

from one currency to another Multilateral netting (next slide)

reduces the number of transactions

Reduces transaction fees

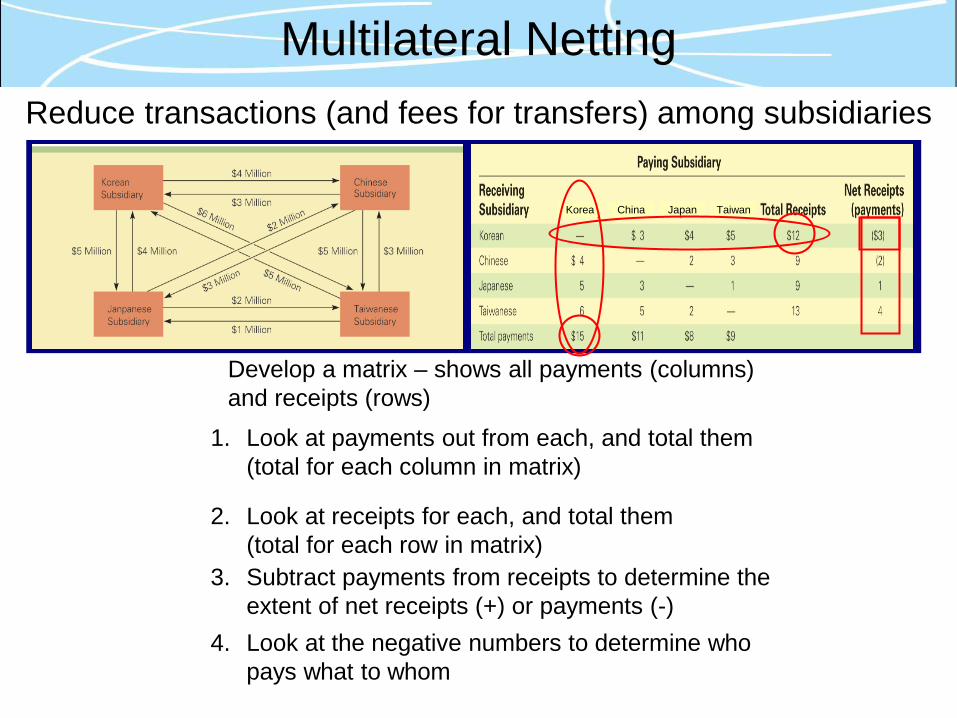

Multilateral Netting Cash Flow with 5 subsidiaries ($ millions) – NEED TO SIMPLIFY

Germany

China

Japan Brazil

UK

$2 $3

$3 $2

$7 $5

$1 $4

$3 $4

$3 $6

Transaction Costs (1%) - Currency exchange - Transfer fees Total Transfers $75 million Total Costs $750,000.00

How to do it?

Korea China Japan Taiwan

Multilateral Netting Reduce transactions (and fees for transfers) among subsidiaries

SIMPLIFY IT ALL

1. Look at payments out from each, and total them(total for each column in matrix)

2. Look at receipts for each, and total them(total for each row in matrix)

3. Subtract payments from receipts to determine theextent of net receipts (+) or payments (-)

Develop a matrix – shows all payments (columns) and receipts (rows)

4. Look at the negative numbers to determine whopays what to whom

Miscommunications - again

Miscommunications Many forms Miscommunications

Miscommunications – especially sensitive when dealing with money, as we have seen