chapter 7

TRANSCRIPT

Capital Asset Pricing and

Arbitrage Pricing Theory

Chapter 7

The Capital Asset Pricing Model

Equating the CML with the efficient frontier at M and solving for E(Ri) yields:

RFR)-(RRFR)E(R Mi i

For a complete derivation of the CAPM pls see:

http://e.viaminvest.com/A2MonitorSystems/AppA2MonitorSystems/A

ppBtoA2CAP_model/CAP_Model.asp#_ftn1

Assumptions

Individual investors can borrow or lend money at the

risk-free rate of return

Investors are rational mean-variance optimizers

Homogeneous expectations

Single-period investment horizon

Investments are limited to traded financial assets

Information is costless and available to all investors

No taxes, and transaction costs

Security Market Line

)E(R i

)Beta(Cov 2Mim/0.1

mR

SML

0

Negative

Beta

RFR

Plot of Estimated Returns

on SML Graph)E(R i

Beta0.1

mRSML

0 .20 .40 .60 .80 1.20 1.40 1.60 1.80-.40 -.20

.22

.20

.18

.16

.14

.12

Rm

.10

.08

.06

.04

.02

A

B

C

D

E

Inputs to the CAPM

(a) the current risk-free rate

(b) the expected return on the market

index and

(c) the beta of the asset being analyzed

Riskfree Rate & Time Horizon

For an investment to be riskfree, i.e., to have an actual return be equal to the expected return, two conditions have to be met – There has to be no default risk, which generally

implies that the security has to be issued by the government. Note, however, that not all governments can be viewed as default free.

There can be no uncertainty about reinvestment rates, which implies that it is a zero coupon security with the same maturity as the cash flow being analyzed.

http://www.ustreas.gov/offices/domestic-finance/debt-management/interest-rate/yield.shtml

Measurement of the risk premium

The risk premium is the premium that

investors demand for investing in an average

risk investment, relative to the riskfree rate.

As a general proposition, this premium should

be

greater than zero

increase with the risk aversion of the investors in

that market

increase with the riskiness of the “average” risk

investment

Estimating Risk Premiums in

Practice

Survey investors on their desired risk premiums and use the average premium from these surveys.

Assume that the actual premium delivered over long time periods is equal to the expected premium - i.e., use historical data

Estimate the implied premium in today’s asset prices.

The Survey Approach

Surveying all investors in a market place is impractical. However, you can survey a few investors (especially the larger investors) and use these results. In practice, this translates into surveys of money managers’ expectations of expected returns on stocks over the next year.

The limitations of this approach are: there are no constraints on reasonability (the survey could

produce negative risk premiums or risk premiums of 50%)

they are extremely volatile

they tend to be short term; even the longest surveys do not go beyond one year

The Historical Premium Approach

This is the default approach used by most to arrive at the premium to use in the model

In most cases, this approach does the following it defines a time period for the estimation (1926-Present, 1962-

Present....)

it calculates average returns on a stock index during the period it calculates average returns on a riskless security over the period

it calculates the difference between the two and uses it as a premium looking forward

The limitations of this approach are: it assumes that the risk aversion of investors has not changed in a

systematic way across time. (The risk aversion may change from year to year, but it reverts back to historical averages)

it assumes that the riskiness of the “risky” portfolio (stock index) has not changed in a systematic way across time.

Historical Average Premiums for the

United States

Historical period Stocks - T.Bills Stocks - T.Bonds

Arith. Geom Arith Geom

1926-2003 7.92% 5.50% 6.54% 4.82%

1962-2003 6.09% 4.85% 4.70% 3.82%

1992-2003 8.43% 6.68% 4.87% 3.57%

What is the right premium?

What about historical premiums for

other Markets?

Historical data for markets outside the United States tends to be unreliable.

Ibbotson, for instance, estimates the following premiums for major markets from 1970-1990

Country Period Stocks Bonds Risk Premium

Australia 1970-90 9.60% 7.35% 2.25%

Canada 1970-90 10.50% 7.41% 3.09%

France 1970-90 11.90% 7.68% 4.22%

Germany 1970-90 7.40% 6.81% 0.59%

Italy 1970-90 9.40% 9.06% 0.34%

Japan 1970-90 13.70% 6.96% 6.74%

Netherlands 1970-90 11.20% 6.87% 4.33%

Switzerland 1970-90 5.30% 4.10% 1.20%

UK 1970-90 14.70% 8.45% 6.25%

Implied Equity Risk Premiums

If we use a basic discounted cash flow model, we can estimate the implied risk premium from the current level of stock prices.

For instance, if stock prices are determined by the simple Gordon Growth Model:

Value = Expected Dividends next year/ (Required Returns on Stocks - Expected Growth Rate)

Plugging in the current level of the index, the dividends on the index and expected growth rate will yield a “implied” expected return on stocks.

Subtracting out the riskfree rate will yield the implied premium.

The problems with this approach are:

the discounted cash flow model used to value the stock index has to be the right one.

the inputs on dividends and expected growth have to be correct

it implicitly assumes that the market is currently correctly valued

S&P 500 Implied Equity Premium

Current level – 1052

5 yr ave dividend yield 5.48%

Dividend growth rate 4.5%

1052 = 57.65(1.045)

Ke - .045

Ke = 10.23%

Risk premium – 10.23% - 3.5% = 6.73%

http://www.wstreet.com/investing/stocks/18204_is_the_standard_and_poors_500_running_out_of_stream.html

Implied Premiums in the US

Estimating Beta

The standard procedure for estimating betas is

to regress stock returns (Rj) against market

returns (Rm) -

Rj = a + b Rm

where a is the intercept and b is the slope of the

regression.

The slope of the regression corresponds to the

beta of the stock, and measures the relative

volatility of the stock to the market.

Firm Specific and Market Risk

The R squared (R2) of the regression

provides an estimate of the proportion of

the risk (variance) of a firm that can be

attributed to market risk;

The balance (1 - R2) can be attributed to

firm specific risk.

Setting up for the Estimation

Decide on an estimation period Services use periods ranging from 2 to 5 years for the regression

Longer estimation period provides more data, but firms change.

Shorter periods can be affected more easily by significant firm-specific event that occurred during the period

Decide on a return interval - daily, weekly, monthly

Shorter intervals yield more observations, but suffer from more noise.

Noise is created by stocks not trading and biases all betas towards one.

Estimate returns (including dividends) on stock Return = (PriceEnd – PriceBeginning + DividendsPeriod)/ PriceBeginning

Included dividends only in ex-dividend month

Choose a market index, and estimate returns (inclusive of dividends) on the index for each interval for the period.

Choosing the Parameters: Disney

Period used: 5 years

Return Interval = Monthly

Market Index: S&P 500 Index.

For instance, to calculate returns on Disney Price for Disney at end of March = $ 37.87 Price for Disney at end of April = $ 36.42

Dividends during month = $0.05 (It was an ex-dividend month)

Return =($36.42 - $ 37.87 + $ 0.05)/$ 37.87=-3.69%

To estimate returns on the index in the same month Index level (including dividends) at end of March = 404.35

Index level (including dividends) at end of April = 415.53

Return =(415.53 - 404.35)/ 404.35 = 2.76%

Disney’s Historical Beta

The Regression Output

ReturnsDisney = -0.01% + 1.40 ReturnsS & P 500

(0.27)

(R squared=32.41%)

Intercept = -0.01%

Slope = 1.40

Estimating Disney’s Beta

Slope of the Regression of 1.40 is the beta

Regression parameters are always estimated with noise. The noise is captured in the standard error of the beta estimate, which in the case of Disney is 0.27.

Assume that I asked you what Disney’s true beta is, after this regression. What is your best point estimate?

What range would you give me, with 67% confidence?

What range would you give me, with 95% confidence?

Standard Errors for US Stocks

Breaking Down Disney’s Risk

R Squared = 32%

This implies that

32% of the risk at Disney comes from

market sources

68%, therefore, comes from firm-specific

sources

The firm-specific risk is diversifiable and will

not be rewarded

The Relevance of R Squared

You are a diversified investor trying to decide whether you should invest in Disney or Amgen. They both have betas of 1.35, but Disney has an R Squared of 32% while Amgen’s R squared of only 15%. Which one would you invest in:

Amgen, because it has the lower R squared

Disney, because it has the higher R squared

You would be indifferent

The Relevance of R Squared…

I would be indifferent, because they have

the same beta

I am well diversified, and thus can

eliminate all firm-specific risk. If I were

not, I would have picked Disney, since it

has less firm-specific risk.

Estimating Expected Returns

Disney’s Beta = 1.40

Riskfree Rate = 3.50% (Long term

Government Bond rate)

Risk Premium = 7% (Implied)

Expected Return = 3.5% + 1.40 (7%) =

13.3%

Use to a Potential Investor in Disney

As a potential investor in Disney, what does this expected return of 13.30% tell you? This is the return that I can expect to make in the long term on

Disney, if the stock is correctly priced and the CAPM is the right model for risk,

This is the return that I need to make on Disney in the long term to break even on my investment in the stock

Both

Assume now that you are an active investor and that your research suggests that an investment in Disney will yield 25% a year for the next 5 years. Based upon the expected return of 14.70%, you would Buy the stock

Sell the stock

Arbitrage Pricing Theory

•Developed as an alternative to the CAPM

•Reasonably intuitive

•Required limited assumptions

•Allowed for multiple dimensions of

investment risk

Arbitrage Pricing Theory

Based on the Law of One Price

Since two otherwise identical assets cannot sell at different prices, equilibrium prices adjust to eliminate all arbitrage opportunities

Arbitrage opportunity

arises if an investor can construct a zero investment portfolio with no risk, but with a positive profit

Since no investment is required, an investor can create large positions in long and short to secure large levels of profits

In an efficient market, profitable arbitrage opportunities will quickly disappear

APT Model

APT assumes returns generated by a factor model

Factor Characteristics

Each risk factor must have a pervasive influence on

stock returns

Risk factors must have nonzero prices

Risk factors must be unpredictable to the market

The expected return-risk relationship for the APT:

E(Ri) = RF + bi1 (risk premium for factor 1)

+ bi2 (risk premium for factor 2)

+ ... + bin (risk premium for factor n)

APT and CAPM Compared

APT applies to well diversified portfolios, and not

necessarily to individual stocks

With APT, it is possible for some individual stocks to

be mispriced - not lie on the SML

APT is more general in that it gets to an expected

return and beta relationship without the assumption of

the market portfolio

Unlike CAPM, APT does not assume mean-variance

decisions, riskless borrowing or lending, and

existence of a market portfolio

APT can be extended to multifactor models

Arbitrage Pricing Theory (APT)

where:

= the expected return on an asset with zero

systematic risk where

ikkiii bbbRE ...)( 22110

0

1 = the risk premium related to the common jth

factor

bij = the pricing relationship between the risk premium and asset -

that is how responsive asset i is to jth common factor

Using the APT

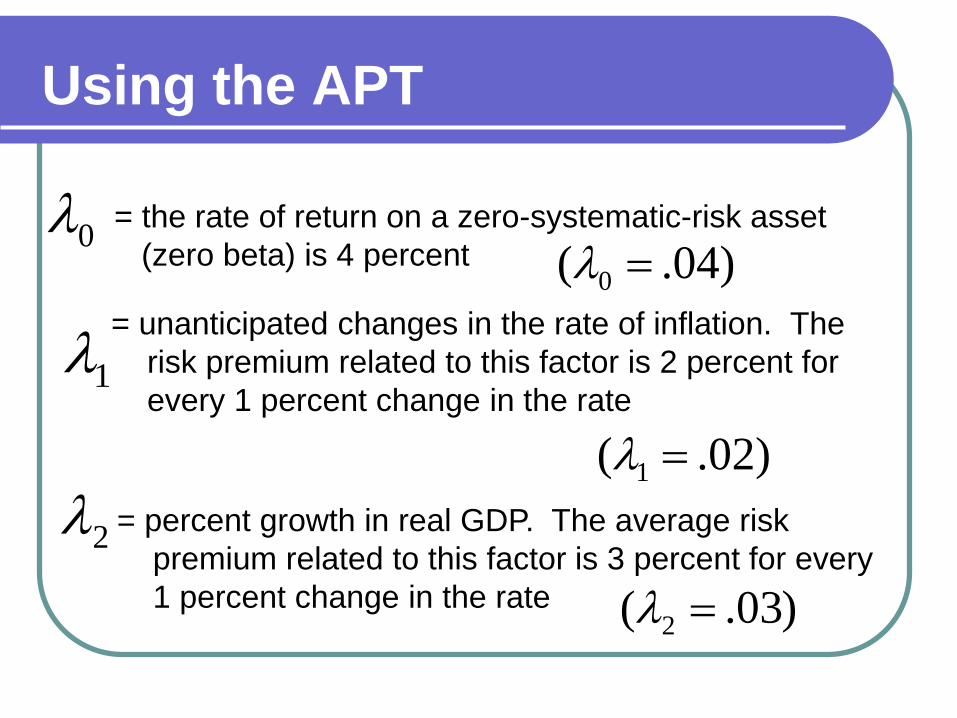

= unanticipated changes in the rate of inflation. The

risk premium related to this factor is 2 percent for

every 1 percent change in the rate1

)02.( 1

= percent growth in real GDP. The average risk

premium related to this factor is 3 percent for every

1 percent change in the rate

= the rate of return on a zero-systematic-risk asset

(zero beta) is 4 percent

2

)03.( 2

)04.( 0 0

Using the APT

= the response of asset X to changes in the inflation

factor is 0.501xb

)50.( 1 xb

= the response of asset Y to changes in the inflation

factor is 2.00 )00.2( 1 yb1yb

= the response of asset X to changes in the GDP

factor is 1.50

= the response of asset Y to changes in the GDP

factor is 1.75

2xb

2yb

)50.1( 2 xb

)75.1( 2 yb

Using the APT

= .04 + (.02)bi1 + (.03)bi2

E(Rx) = .04 + (.02)(0.50) + (.03)(1.50)

= .095 = 9.5%

E(Ry) = .04 + (.02)(2.00) + (.03)(1.75)

= .1325 = 13.25%

22110)( iii bbRE

Security Valuation with the APT:

An Example

Three stocks (A, B, C) and two common

systematic risk factors have the following

relationship( )0 0

21

21

21

)5.0()8.1()(

)3.1()2.0()(

)9.0()8.0()(

C

B

A

RE

RE

RE

%7.9)(

%7.5)(

%7.7)(

C

B

A

RE

RE

RE

%5 and %4 21 if

40.38$%)7.91(35$)(

00.37$%)7.51(35$)(

70.37$%)7.71(35$)(

C

B

A

PE

PE

PE

Currently priced at $35 each and will

not pay dividend

Expected prices a year from now

Your estimates a year from now (you

are sure!) E(PA) = $37.20

E(PB) = $37.80

E(PC) = $38.50

Security Valuation with the APT:

An Example

Riskless arbitrage

Requires no net wealth invested initially

Will bear no systematic or unsystematic risk but

Still earns a profit

Condition must be satisfied as follow:

1.

2

3

0i iw

0 iji ibw

0 ii iRw i.e. actual portfolio return is positive

For all K factors [i.e. no systematic risk] and w is small

for all I [ unsystematic risk is fully diversified]

i.e. no net wealth invested

Wi the percentage investment in security i

Security Valuation with the APT:

An Example

Example: Stock A is overvalued; Stock B and C are two

undervalued securities

Consider the following investment proportions WA=-1.0

WB=+0.5

WC=+0.5

These investment weight imply the creation of a portfolio that is short two shares of Stock A for each share of Stock B and one share of Stock C held long

Security Valuation with the APT:

An Example

Net Initial Investment:

Short 2 shares of A: +70

Purchase 1 share of B: -35

Purchase 1 share of C: -35

Net investment: 0

Net Exposure to Risk Factors:

Factor 1 Factor 2

Weighted exposure from Stock A: (-1.0)(0.8) (-1.0)(0.9)

Weighted exposure from Stock B: (0.5)(-0.2) (0.5)(1.3)

Weighted exposure from Stock C: (0.5)(1.8) (0.5)(0.5)

Net risk exposure 0 0

Net Profit:

Stock A Stock B Stock C

[2(35)-2(37.20)]+[37.80-35]+[38.50-35] =$1.90

Security Valuation with the APT:

An Example

The price of stock A will be bid down while the prices of stock B and C will be bid up until arbitrage trading in the current market is no long profitable.

10.35097.1/40.38$

76.35$057.1/00.37$

54.34$077.1/20.37$

C

B

A

P

P

P

Microeconomic-Based Risk

Factor Models (Fama-French)

The Fama-French Three Factor Model

ittititmtiitit eHMLbSMBbRFRRbaRFRR 321 )()(

SMB (i.e. small minus big) is the return to a portfolio of small

capitalization stocks less the return to a portfolio of large

capitalization stocks

HML (i.e. high minus low) is the return to a portfolio of stocks with

high ratios of book-to-market values less the return to a portfolio of

low book-to-market value stocks

Summary

APT model has fewer assumptions than the

CAPM and does not specifically require the

designation of a market portfolio.

The APT posits that expected security returns

are related in a linear fashion to multiple

common risk factors.

Unfortunately, the theory does not offer

guidance as to how many factors exist or what

their identifies might be

Summary

APT is difficult to put into practice in a theoretically rigorous fashion. Multifactor models of risk and return attempt to bridge the gap between the practice and theory by specifying a set of variables.

Macroeconomic variables have been successfully applied

An equally successful second approach to identifying the risk exposures in a multifactor model has focused on the characteristics of securities themselves. (Microeconomic approach)