chapter 1: introduction - govt of bihar · 26 chapter 1: introduction 1.1 background and context...

TRANSCRIPT

26

Chapter 1: Introduction

1.1 Background and Context

Bihar is one of the largest maize growing state and the crop was grown primarily as a

subsistence crop to meet food needs for a long time till recently. But now like in non-

traditional areas (Karnataka and Andhra Pradesh), it is also grown for commercial

purposes (i.e., mainly to meet the raw material requirements of the animal feed sector).

It is third largest maize producing state contributing around 10 percent to national

production. Around 0.65 million hectare is presently under maize cultivation, which is

about 7 per cent of Gross Cropped Area (GCA) in the state and over 13 lakh farmers

are engaged in maize cultivation. During 2005-06, the state produced about 1.4 million

MT, which is about 5 per cent of the total crop production.

Maize can be utilized in many different forms by converting it into a variety of

products, through grinding, alkali processing, boiling, cooking and fermenting, such as

corn starch, corn flakes and cereals, ethanol etc. It also has many industrial

applications, which can make it a profitable crop in the state. Maize processing and

utilization pattern shows that in India, around 60 per cent of the total produce is for

animal feed, 28 per cent for human consumption and 12 per cent is used by the industry

(starch, brewery etc). In Bihar only 8-10% of maize (5% directly by the processors and

another 3-5% is being used by road side snack joints etc.) is processed within the state

despite the fact that the state has huge and rising marketable surplus.

While the area under cultivation, maize production & yield have increased during 1977

to 2007, there are only 8-10 maize processing units in Bihar. They are mainly into

milling of flour and production poultry feed. In absence of adequate processing facility,

the huge marketable surplus of Bihar, especially in rabi season depends completely on

other states for its consumption. Any obstruction in this trading chain in future may

lead into spoilage of that surplus, affecting the entire value chain.

27

Also due to inadequate processing facilities in the state, result more than 80% of

Bihar maize goes outside the state and gets processed there depriving it of value

addition and higher income for the people in the state. The processed maize in the form

of poultry feed and seeds then comes back to the state.

There is potential for processing of both high & low value added products in

maize sector in the state itself. There are factors contributing to increase in the demand

of processed maize. Some of them are (1) growing demand for eggs and chicken

leading to increased demand for poultry feed in the state; (2) the state has 8 lakh hectare

land under water which is suitable for fish farming; (3) increased demand for ethanol as

a fuel additive; (4) growing urbanization leading to increased demand for processed

food like corn flakes etc; (5) dairy sector is on growth path and this sector can provide a

good market for cattle feed products. Thus there is growing demand for processed

maize in the state and there is also adequate supply of good quality maize in the state.

Yet the processing industry in Bihar is almost non-existent as there are only 10

processing units in the state engaged mainly in manufacturing of traditional food

products (flour, besan, suji etc) and poultry feed. It is therefore important to study the

reasons and factors restricting the growth of processing industry in the state.

It is in this context the study was commissioned by World Bank to study the maize

sector in Bihar with the following objectives

1.2 Objectives

The broad objective of the study is to assess the investment climate for processing of

maize (corn) into value added products in Bihar.

1. To assess and analyse the status of maize cultivation with respect to inputs,

harvesting and post harvesting practices and infrastructure (including storage,

warehousing etc)

2. To map major mandis and analyse price movements

3. To study the trade channels (marketing network) and value chain in maize

cultivation

28

4. Study the status of maize processing in the state

5. To find potential of maize processing industry in the state,

6. To out line the regulatory/Policy guidelines of the government,

7. To identify the constraints with farmers, traders and processors.

8. Suggest measures for improving investment climate for maize processing in the

state.

1.3. Approach, Database and Methodology

The assignment involved collection and scanning of secondary data available about the

maize sector with a focus on status of maize processing industry in the state. It was felt

that benchmarking the sector in Bihar with other states would enable us identify the

constraints and draw best practice cases. Therefore information has also been collected

from Andhra Pradesh and Karnataka.

Primary data collection

Data was collected from both primary and secondary sources. The Primary data was

collected through a diagnostic survey of the farmers/growers, traders and maize

processors in the state in order to study existing cultivation and post harvesting

practices, storage systems, maize arrivals and price movements, marketing channels,

value chains etc and identifying the factors constraining the growth of the sector at

different levels of production and marketing.

A structured questionnaire was developed for data collection and collate the critical

information. The quantitative data was mainly collected by interviewing over 60

growers, 20 traders and all 10 processors operating in the state. The data on physical

infrastructure in mandis, monthly prices and corresponding arrivals, name and share of

the markets (local as well as outside state), etc has been collected directly from mandis.

All major mandis trading in maize i.e Gulabagh, Katihar, Mansi etc have been covered

by the survey for studying the trade channels and value chain mapping in maize

cultivation.

29

The diagnostic survey itself was carried out in two phases: qualitative and quantitative

surveys. The survey was carried out in the identified 4 districts of Bihar, namely

Begusarai, Khagaria, Purnea and Bhagalpur. Secondary data was used as the basis for

short-listing the target group for obtaining trade feedback and critical inputs from

various stakeholders including government agencies. The short listing was done on the

basis of following parametres:

Current area, production, productivity of all districts for maize production

Marketable surplus of maize in these districts

Linkages of production hubs to different consumption sources.

The ultimate objective of the survey was to come out with credible inputs and database

for the formulation of recommendations to improve the competitiveness of the sector.

Secondary Data Collection

The secondary database sources included published books, Reports of multi-lateral

bodies like World Bank, articles published in national and international journals,

magazines, newspapers, Reports of the various Government departments, consultancy

firms, research projects etc. It was used to study the status of maize production in world

with a focus on India and Bihar. This included data related to production, productivity

and area of the crop in India and Bihar, existence, role and relevance of concerned

institutions, policy framework etc. The data have been sourced from various sources

including government agencies including Department of Agriculture (DoA), and

Rajendra Agricultural University (RAU), Department of Industry, CGIAR (Maize

Regional Research Centre and Seed Production), Begusarai and Confederation of

Indian Industry (CII), Patna.

In addition to the above structured interviews, 4 Focussed Group Discussions (FGDs)

were held among farmers, commission agents, traders, processors, industry

associations, and research institutions to get the first hand information on the sector

with a primary focus on maize trading and processing.

30

The data and information have also been collected through interactions and in-depth

interviews with various stakeholders including Government departments like

Department of Agriculture (DoA), Industrial Development Commissioner (IDC),

Department of Fisheries, Research Institutions, bankers, trade and industry associations

etc.

Study Tools

As stated, separate structured questionnaires were developed for farmers/growers,

traders and processors in accordance with the objectives of the study. They were

pre-tested and later administered in the field. Similarly, guides for FGDs and in-

depth interviews were developed and finalized to get optimum results.

Field Operations and Data Management

In all, 4 field investigators and 2 supervisors were deployed for conducting the field

study. All of them have had prior experience in conducting such surveys. These

field officials administered the quantitative questionnaire among the target group.

The gaps and inconsistencies found in the filled - in questionnaires were rectified in

the field itself.

The information collected through field survey was tabulated and analysed. The issues

that emerged during FGDs and discussion with various stakeholders, including state

government officials, have also been captured in the Report.

31

Chapter 2 : Maize Production – Global and National Scenario

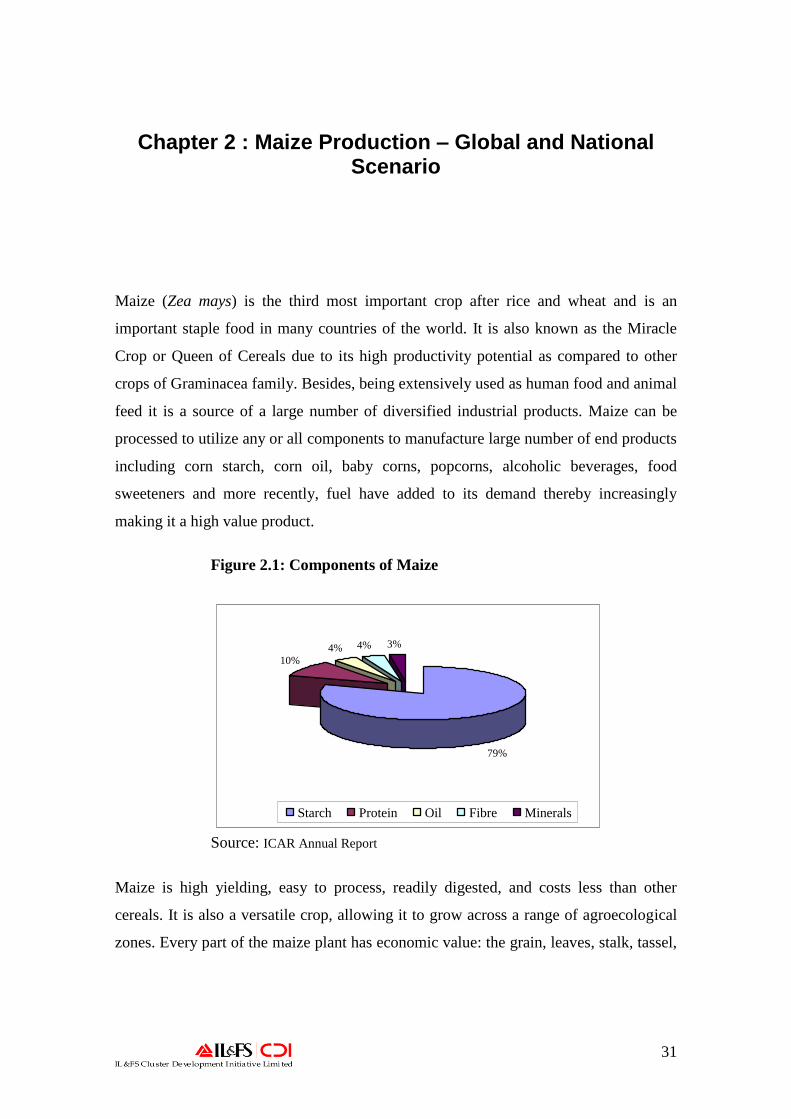

Maize (Zea mays) is the third most important crop after rice and wheat and is an

important staple food in many countries of the world. It is also known as the Miracle

Crop or Queen of Cereals due to its high productivity potential as compared to other

crops of Graminacea family. Besides, being extensively used as human food and animal

feed it is a source of a large number of diversified industrial products. Maize can be

processed to utilize any or all components to manufacture large number of end products

including corn starch, corn oil, baby corns, popcorns, alcoholic beverages, food

sweeteners and more recently, fuel have added to its demand thereby increasingly

making it a high value product.

Figure 2.1: Components of Maize

79%

10%

4% 4% 3%

Starch Protein Oil Fibre Minerals

Source: ICAR Annual Report

Maize is high yielding, easy to process, readily digested, and costs less than other

cereals. It is also a versatile crop, allowing it to grow across a range of agroecological

zones. Every part of the maize plant has economic value: the grain, leaves, stalk, tassel,

32

and cob can all be used to produce a large variety of food and nonfood products etc.

Generally following three types of corn is grown

Grain or field corn,

Sweet corn used mainly as food

Popcorn.

Maize in India is an important cereal. Its area and production have steadily increased

during the past two decades. Maize has varied usages from food preparation to poultry

feed. In India, it is mainly used in poultry feed manufacturing.

2.1. Trend in Global Production, Consumption and Trade in Maize

2.1.1. Status of Maize Production in the World

The area under cultivation and as well as the production of maize have been increasing

continuously over last decades. Though the acreage has increased consistently,

production pattern has been erratic owing to the variations in the yield. There are many

factors that have contributed towards changes in yield like weather during crop growth,

pest and disease attack, technological advances and development of new hybrids and

varieties etc.

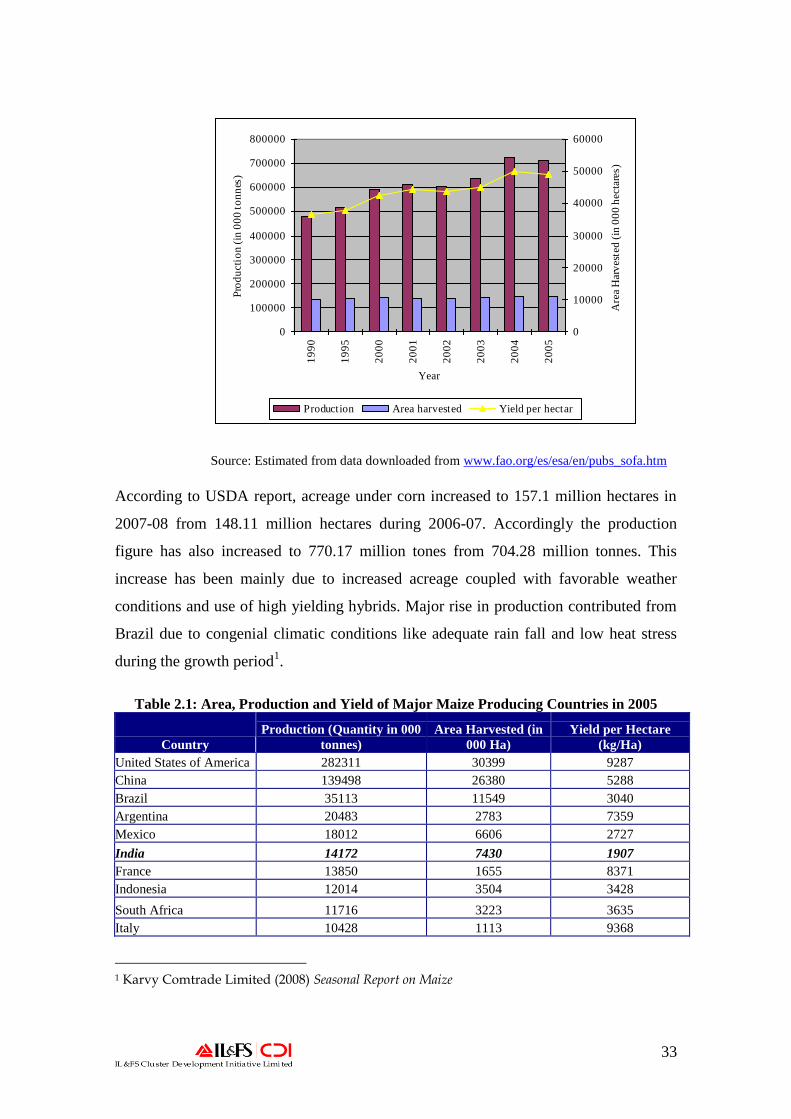

Figure 2.2: World Area, Production and Yield (In Kgs/Ha) of Maize (2005)

33

0

100000

200000

300000

400000

500000

600000

700000

800000

19

90

19

95

20

00

20

01

20

02

20

03

20

04

20

05

Year

Pro

du

ctio

n (

in 0

00

to

nn

es)

0

10000

20000

30000

40000

50000

60000

Are

a H

arv

este

d (

in 0

00

hec

tare

s)

Production Area harvested Yield per hectar

Source: Estimated from data downloaded from www.fao.org/es/esa/en/pubs_sofa.htm

According to USDA report, acreage under corn increased to 157.1 million hectares in

2007-08 from 148.11 million hectares during 2006-07. Accordingly the production

figure has also increased to 770.17 million tones from 704.28 million tonnes. This

increase has been mainly due to increased acreage coupled with favorable weather

conditions and use of high yielding hybrids. Major rise in production contributed from

Brazil due to congenial climatic conditions like adequate rain fall and low heat stress

during the growth period1.

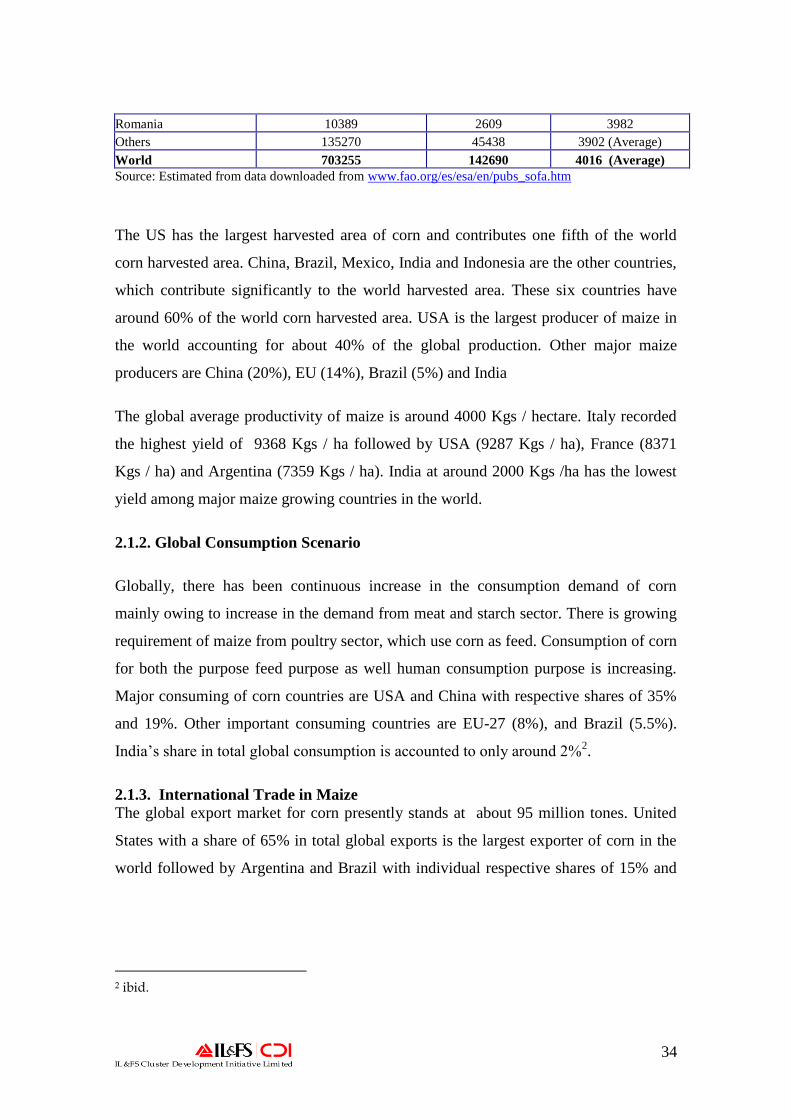

Table 2.1: Area, Production and Yield of Major Maize Producing Countries in 2005

Country

Production (Quantity in 000

tonnes)

Area Harvested (in

000 Ha)

Yield per Hectare

(kg/Ha)

United States of America 282311 30399 9287

China 139498 26380 5288

Brazil 35113 11549 3040

Argentina 20483 2783 7359

Mexico 18012 6606 2727

India 14172 7430 1907

France 13850 1655 8371

Indonesia 12014 3504 3428

South Africa 11716 3223 3635

Italy 10428 1113 9368

1 Karvy Comtrade Limited (2008) Seasonal Report on Maize

34

Romania 10389 2609 3982

Others 135270 45438 3902 (Average)

World 703255 142690 4016 (Average)

Source: Estimated from data downloaded from www.fao.org/es/esa/en/pubs_sofa.htm

The US has the largest harvested area of corn and contributes one fifth of the world

corn harvested area. China, Brazil, Mexico, India and Indonesia are the other countries,

which contribute significantly to the world harvested area. These six countries have

around 60% of the world corn harvested area. USA is the largest producer of maize in

the world accounting for about 40% of the global production. Other major maize

producers are China (20%), EU (14%), Brazil (5%) and India

The global average productivity of maize is around 4000 Kgs / hectare. Italy recorded

the highest yield of 9368 Kgs / ha followed by USA (9287 Kgs / ha), France (8371

Kgs / ha) and Argentina (7359 Kgs / ha). India at around 2000 Kgs /ha has the lowest

yield among major maize growing countries in the world.

2.1.2. Global Consumption Scenario

Globally, there has been continuous increase in the consumption demand of corn

mainly owing to increase in the demand from meat and starch sector. There is growing

requirement of maize from poultry sector, which use corn as feed. Consumption of corn

for both the purpose feed purpose as well human consumption purpose is increasing.

Major consuming of corn countries are USA and China with respective shares of 35%

and 19%. Other important consuming countries are EU-27 (8%), and Brazil (5.5%).

India‘s share in total global consumption is accounted to only around 2%2.

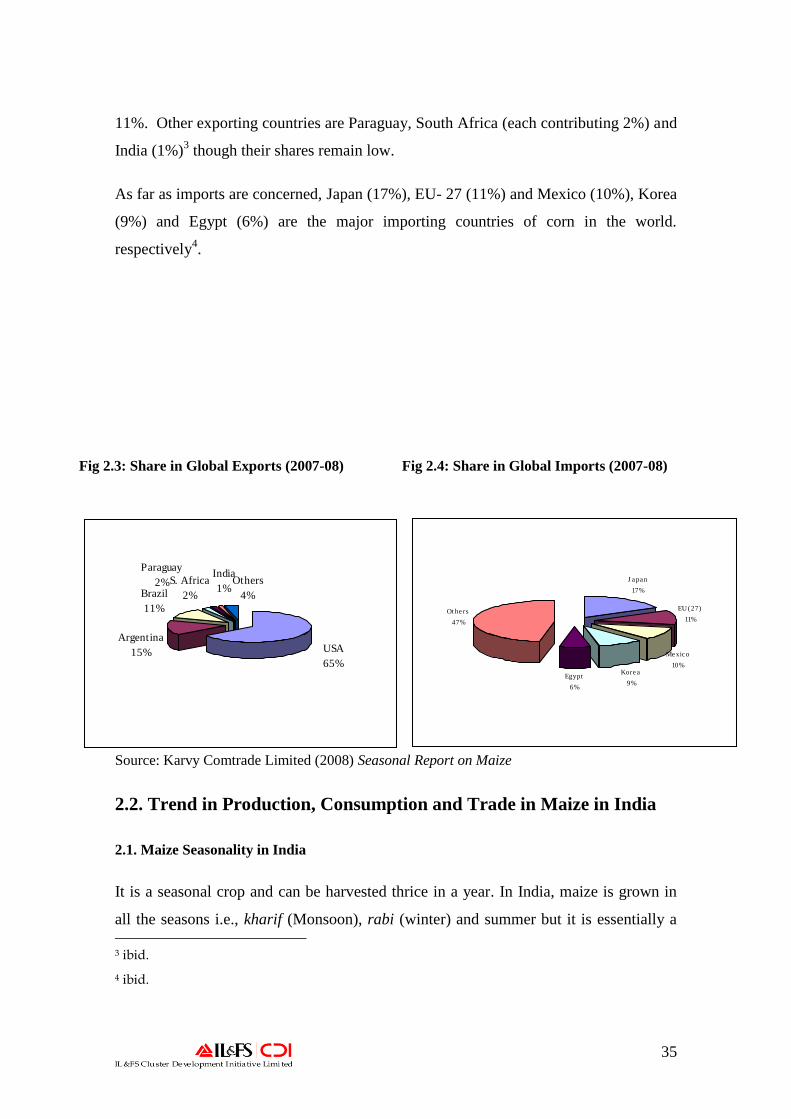

2.1.3. International Trade in Maize

The global export market for corn presently stands at about 95 million tones. United

States with a share of 65% in total global exports is the largest exporter of corn in the

world followed by Argentina and Brazil with individual respective shares of 15% and

2 ibid.

35

11%. Other exporting countries are Paraguay, South Africa (each contributing 2%) and

India (1%)3 though their shares remain low.

As far as imports are concerned, Japan (17%), EU- 27 (11%) and Mexico (10%), Korea

(9%) and Egypt (6%) are the major importing countries of corn in the world.

respectively4.

Fig 2.3: Share in Global Exports (2007-08) Fig 2.4: Share in Global Imports (2007-08)

Source: Karvy Comtrade Limited (2008) Seasonal Report on Maize

2.2. Trend in Production, Consumption and Trade in Maize in India

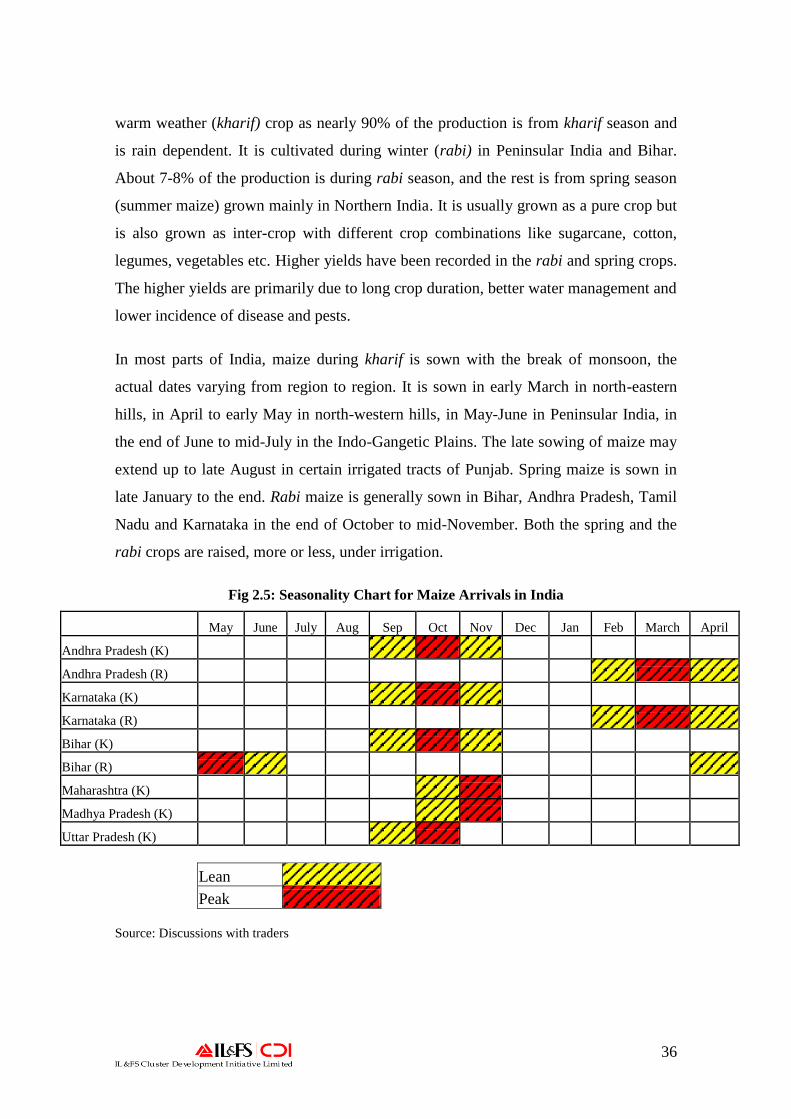

2.1. Maize Seasonality in India

It is a seasonal crop and can be harvested thrice in a year. In India, maize is grown in

all the seasons i.e., kharif (Monsoon), rabi (winter) and summer but it is essentially a

3 ibid.

4 ibid.

S. Africa

2%

Argentina

15% USA

65%

Brazil

11%

Paraguay

2% Others

4%

India

1%J a pa n

17%

EU (27)

11%

Me xic o

10%Kore a

9%Egypt

6%

Ot he rs

47%

36

warm weather (kharif) crop as nearly 90% of the production is from kharif season and

is rain dependent. It is cultivated during winter (rabi) in Peninsular India and Bihar.

About 7-8% of the production is during rabi season, and the rest is from spring season

(summer maize) grown mainly in Northern India. It is usually grown as a pure crop but

is also grown as inter-crop with different crop combinations like sugarcane, cotton,

legumes, vegetables etc. Higher yields have been recorded in the rabi and spring crops.

The higher yields are primarily due to long crop duration, better water management and

lower incidence of disease and pests.

In most parts of India, maize during kharif is sown with the break of monsoon, the

actual dates varying from region to region. It is sown in early March in north-eastern

hills, in April to early May in north-western hills, in May-June in Peninsular India, in

the end of June to mid-July in the Indo-Gangetic Plains. The late sowing of maize may

extend up to late August in certain irrigated tracts of Punjab. Spring maize is sown in

late January to the end. Rabi maize is generally sown in Bihar, Andhra Pradesh, Tamil

Nadu and Karnataka in the end of October to mid-November. Both the spring and the

rabi crops are raised, more or less, under irrigation.

Fig 2.5: Seasonality Chart for Maize Arrivals in India

May June July Aug Sep Oct Nov Dec Jan Feb March April

Andhra Pradesh (K)

Andhra Pradesh (R)

Karnataka (K)

Karnataka (R)

Bihar (K)

Bihar (R)

Maharashtra (K)

Madhya Pradesh (K)

Uttar Pradesh (K)

Lean

Peak Source: Discussions with traders

37

Maize can grow from sea level to 3000 metre altitudes under diverse conditions. Maize

does however, require considerable moisture and warmth from germination to

flowering. The ideal temperature for germination is 21° C and for growth 32°C. 50-75

cms of well-distributed rainfall is conducive to growth. It can be successfully grown

where the night temperature does not go below 15.6oC (60

oF). It cannot withstand frost

at any stage of its growth. In India, its cultivation extends from the hot arid plains of

Rajasthan and Gujarat to the wet hill of Assam and Bengal (receiving over 400 cm of

rainfall)5.

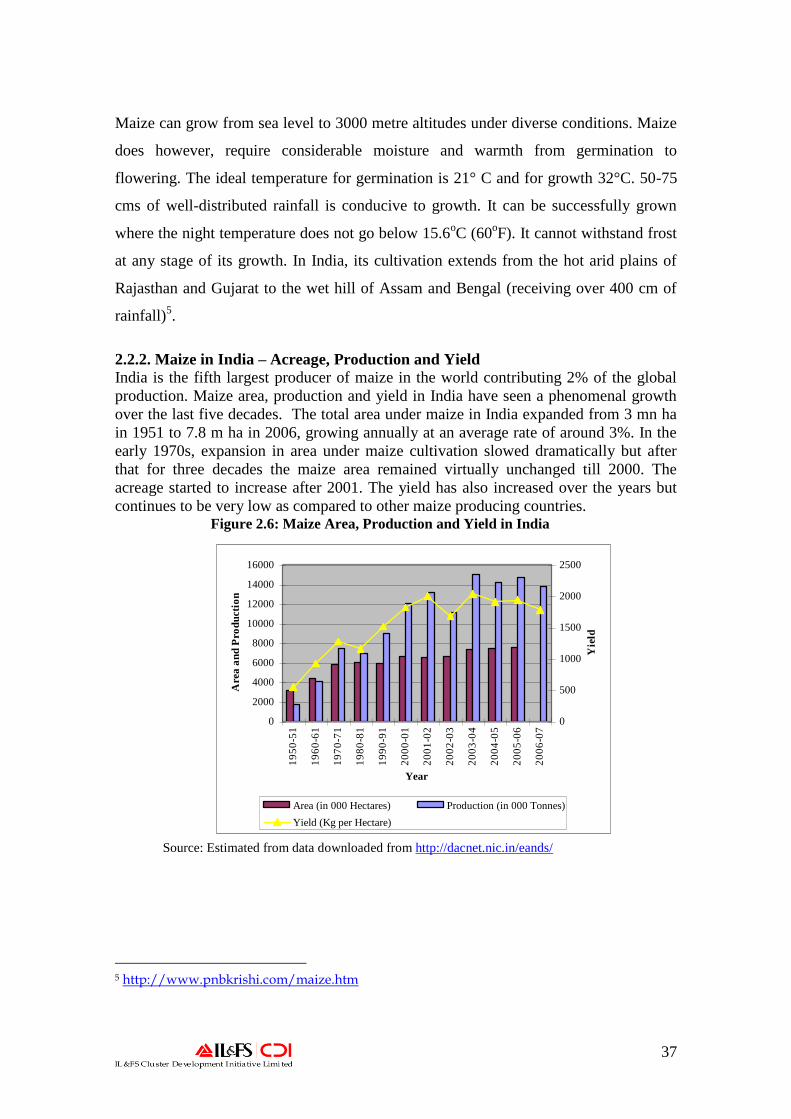

2.2.2. Maize in India – Acreage, Production and Yield

India is the fifth largest producer of maize in the world contributing 2% of the global

production. Maize area, production and yield in India have seen a phenomenal growth

over the last five decades. The total area under maize in India expanded from 3 mn ha

in 1951 to 7.8 m ha in 2006, growing annually at an average rate of around 3%. In the

early 1970s, expansion in area under maize cultivation slowed dramatically but after

that for three decades the maize area remained virtually unchanged till 2000. The

acreage started to increase after 2001. The yield has also increased over the years but

continues to be very low as compared to other maize producing countries. Figure 2.6: Maize Area, Production and Yield in India

0

2000

4000

6000

8000

10000

12000

14000

16000

19

50

-51

19

60

-61

19

70

-71

19

80

-81

19

90

-91

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

Year

Are

a a

nd

Pro

du

ctio

n

0

500

1000

1500

2000

2500

Yie

ld

Area (in 000 Hectares) Production (in 000 Tonnes)

Yield (Kg per Hectare)

Source: Estimated from data downloaded from http://dacnet.nic.in/eands/

5 http://www.pnbkrishi.com/maize.htm

38

Rising yields, coupled with a steady expansion in area, led to growth in maize

production of 5.9% and 5.2% per annum in the 1950s and 1960s, respectively. After

slowing down in the 1970s as the area under cultivation stabilized, growth in maize

production, fueled by continuing improvements in yield, averaged about 2.6% per

annum in the 1980s and 3.2% per annum during 1990s. A significant shift occurred in

the 1990s when irrigated winter (rabi) maize cultivation expanded rapidly, particularly

in the states of Bihar, Andhra Pradesh and Karnataka. Total maize production exceeded

10 million tons in 1997-98. Production of corn in India has shown an increasing trend

consistently except the year 2002 when production showed a little decline due to

drought conditions in some of the states in India.

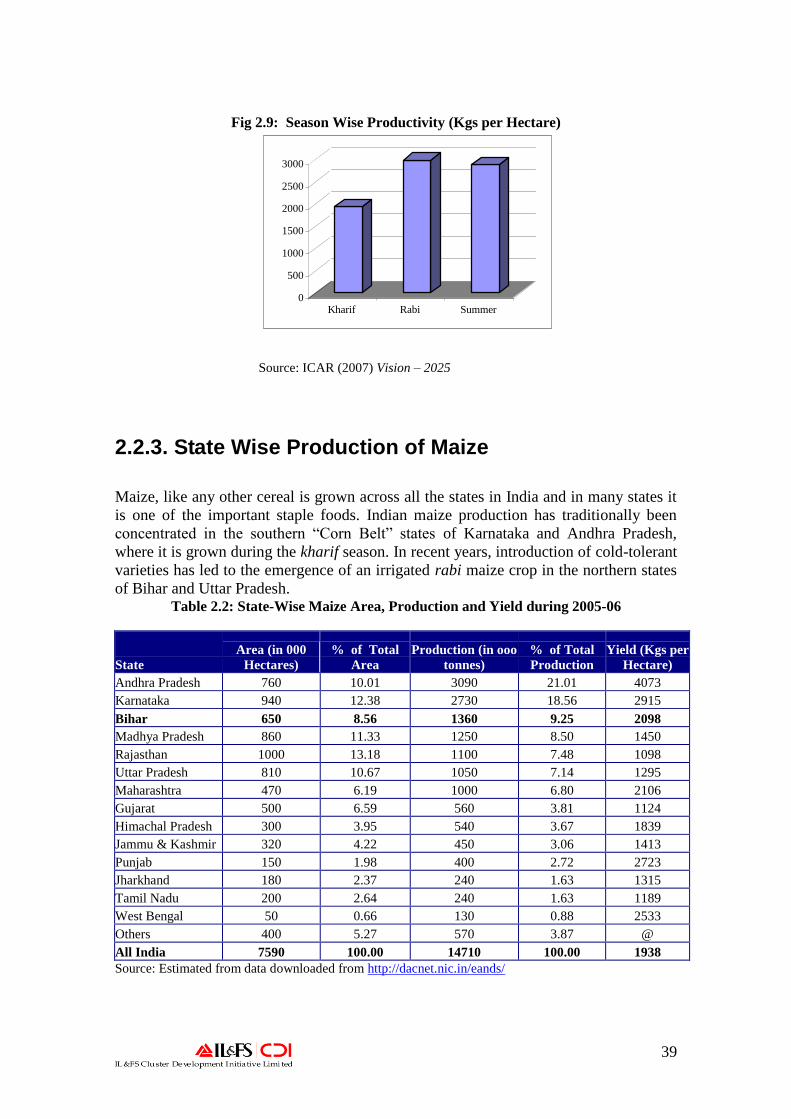

Though kharif maize dominates the acreage and thus the production, productivity is

highest for Rabi maize. The average yield of kharif maize is about 2 tonnes/hectare

while that of rabi maize is more than 3 tonnes /hectare. The average yield for spring

season is also around 3 tonnes per hectare. The higher yield during rabi and spring are

primarily due to (a) relatively mild climatic conditions rabi and spring seasons during

which the duration of the crop is longer resulting in sustained harvesting of solar energy

leading to higher recovery of grain and biomass; (b) larger coverage of hybrid seeds

having higher productivity. The states with favourable ecosystem specially Bihar (rabi)

are witnessing expansion of winter maize area. Almost 90% of the total hybrid seed

production of the country is confined to Andhra Pradesh and Karnataka in rabi season

due to seasonal and productivity advantages6.

Fig 2.7: Season Wise Area Under Cultivation Fig 2.8: Season Wise Production

R a b i

(8%)

S u m m e r

(2%)

( Kh a r i f )

90%

R a b i

(11%)

S u m m e r

(3%)

Kh a r i f

(86%)

6 ICAR (2007) Vision - 2025

39

Fig 2.9: Season Wise Productivity (Kgs per Hectare)

0

500

1000

1500

2000

2500

3000

Kharif Rabi Summer

Source: ICAR (2007) Vision – 2025

2.2.3. State Wise Production of Maize

Maize, like any other cereal is grown across all the states in India and in many states it

is one of the important staple foods. Indian maize production has traditionally been

concentrated in the southern ―Corn Belt‖ states of Karnataka and Andhra Pradesh,

where it is grown during the kharif season. In recent years, introduction of cold-tolerant

varieties has led to the emergence of an irrigated rabi maize crop in the northern states

of Bihar and Uttar Pradesh. Table 2.2: State-Wise Maize Area, Production and Yield during 2005-06

State

Area (in 000

Hectares)

% of Total

Area

Production (in ooo

tonnes)

% of Total

Production

Yield (Kgs per

Hectare)

Andhra Pradesh 760 10.01 3090 21.01 4073

Karnataka 940 12.38 2730 18.56 2915

Bihar 650 8.56 1360 9.25 2098

Madhya Pradesh 860 11.33 1250 8.50 1450

Rajasthan 1000 13.18 1100 7.48 1098

Uttar Pradesh 810 10.67 1050 7.14 1295

Maharashtra 470 6.19 1000 6.80 2106

Gujarat 500 6.59 560 3.81 1124

Himachal Pradesh 300 3.95 540 3.67 1839

Jammu & Kashmir 320 4.22 450 3.06 1413

Punjab 150 1.98 400 2.72 2723

Jharkhand 180 2.37 240 1.63 1315

Tamil Nadu 200 2.64 240 1.63 1189

West Bengal 50 0.66 130 0.88 2533

Others 400 5.27 570 3.87 @

All India 7590 100.00 14710 100.00 1938

Source: Estimated from data downloaded from http://dacnet.nic.in/eands/

40

Among the major producing states, Andhra Pradesh tops the list with the contribution

of over 20% to the total Indian maize production. Other producers are Karnataka

(18.6%), Bihar (9.2%), Madhya Pradesh (8.5%), Rajasthan (7.5%), Uttar Pradesh (7%),

and Maharashtra (6.8%).

The maize growing states can be divided into two groups

1. High Productivity States: Karnataka, Andhra Pradesh, Bihar (Rabi) Maharashtra,

Punjab and West Bengal account for about 30 percent

of the national maize acreage and their productivity

levels range from 2 – 4 tonnes per hectare.

2. Low Productivity States : Rajasthan, Madhya Pradesh, Gujarat, Uttar Pradesh,

Bihar (Kharif) which together cover about 50 percent of

the area have yields ranging 1 – 2 tonnes / hectare (i.e.

< 2 tonnes/hectare) which is lower than the national

average

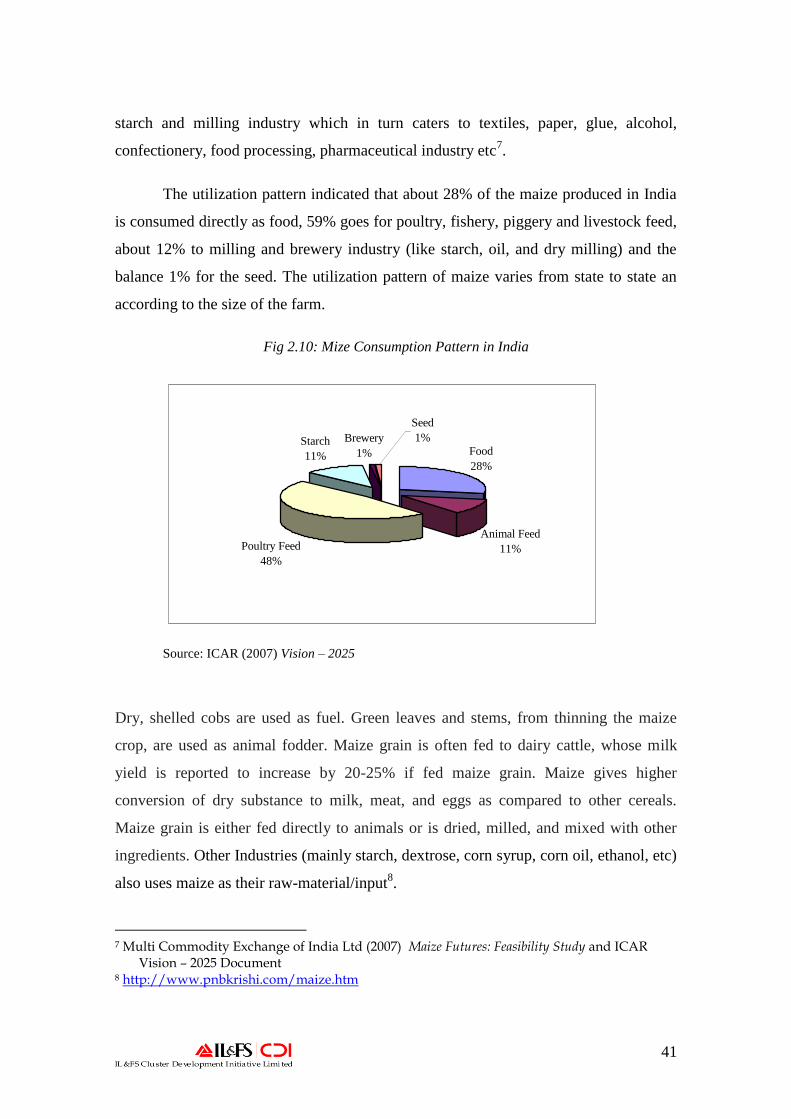

2.2.4. Utilisation / Consumption Pattern of Maize in India

Diversified uses of maize have prompted higher production in India. Presently,

maize is mainly used for preparation of poultry feed and extraction of starch in the

country. In India both white and yellow both types of maize are grown. While white

maize in grown mostly for human food purpose, yellow maize is consumed primarily in

the manufacturing of poultry and animal feed. The maize consumption pattern in given

in the following graph.

Direct human consumption of maize has declined over time, while feed and

industrial uses have increased. A recent study by NCAP has shown that the per capita

human maize consumption which stands at around 3 kg per annum (average rural –

3.89 kg per annum; and urban average – 0.61 kg per annum) is declining at 2% per

annum due to greater availability of maize and rice at subsidized rates through Public

Distribution System (PDS). Rising household incomes have also shifted consumption

from maize to other cereals like rice and wheat. This has also led to an increased

consumption of meat, particularly of poultry, which has in turn increased the demand

for maize as feed. Increased industrial demand for maize comes primarily from the

41

starch and milling industry which in turn caters to textiles, paper, glue, alcohol,

confectionery, food processing, pharmaceutical industry etc7.

The utilization pattern indicated that about 28% of the maize produced in India

is consumed directly as food, 59% goes for poultry, fishery, piggery and livestock feed,

about 12% to milling and brewery industry (like starch, oil, and dry milling) and the

balance 1% for the seed. The utilization pattern of maize varies from state to state an

according to the size of the farm.

Fig 2.10: Mize Consumption Pattern in India

Food

28%

Animal Feed

11%Poultry Feed

48%

Starch

11%

Brewery

1%

Seed

1%

Source: ICAR (2007) Vision – 2025

Dry, shelled cobs are used as fuel. Green leaves and stems, from thinning the maize

crop, are used as animal fodder. Maize grain is often fed to dairy cattle, whose milk

yield is reported to increase by 20-25% if fed maize grain. Maize gives higher

conversion of dry substance to milk, meat, and eggs as compared to other cereals.

Maize grain is either fed directly to animals or is dried, milled, and mixed with other

ingredients. Other Industries (mainly starch, dextrose, corn syrup, corn oil, ethanol, etc)

also uses maize as their raw-material/input8.

7 Multi Commodity Exchange of India Ltd (2007) Maize Futures: Feasibility Study and ICAR

Vision – 2025 Document 8 http://www.pnbkrishi.com/maize.htm

42

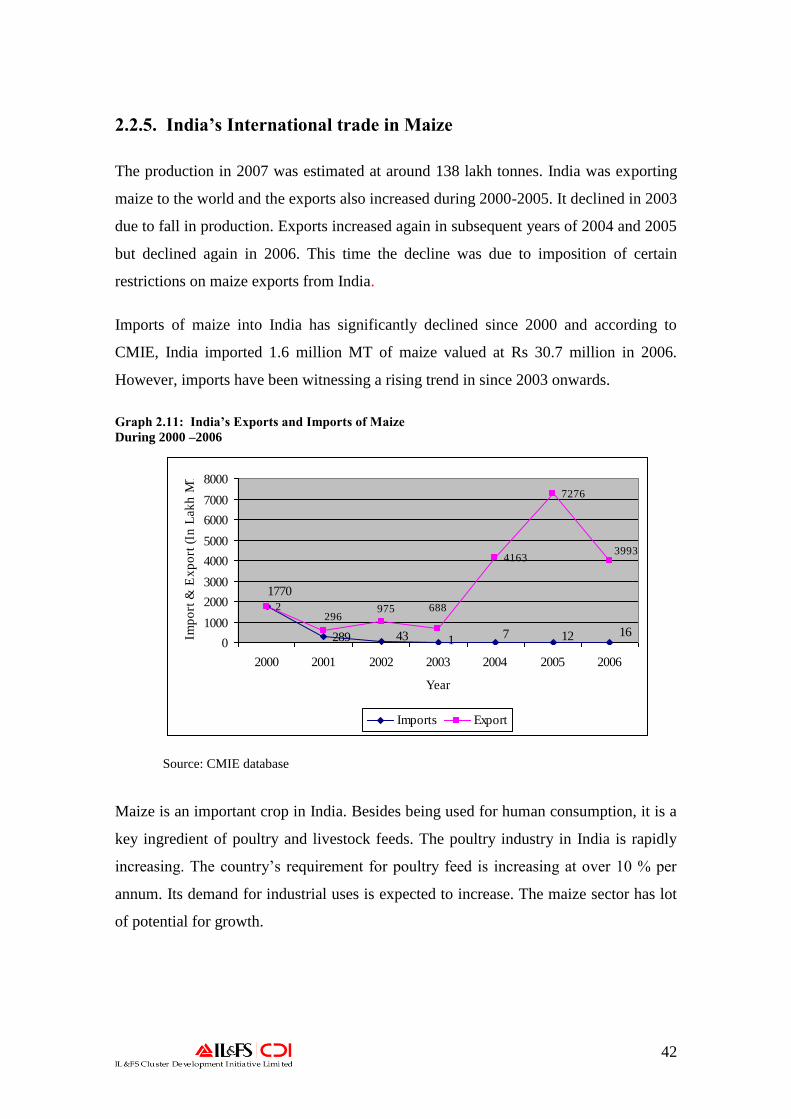

2.2.5. India’s International trade in Maize

The production in 2007 was estimated at around 138 lakh tonnes. India was exporting

maize to the world and the exports also increased during 2000-2005. It declined in 2003

due to fall in production. Exports increased again in subsequent years of 2004 and 2005

but declined again in 2006. This time the decline was due to imposition of certain

restrictions on maize exports from India.

Imports of maize into India has significantly declined since 2000 and according to

CMIE, India imported 1.6 million MT of maize valued at Rs 30.7 million in 2006.

However, imports have been witnessing a rising trend in since 2003 onwards.

Graph 2.11: India’s Exports and Imports of Maize

During 2000 –2006

289

2

4163

7276

1770

11612743

3993

688975296

0

1000

2000

3000

4000

5000

6000

7000

8000

2000 2001 2002 2003 2004 2005 2006

Year

Imp

ort

& E

xp

ort

(In

Lak

h M

T)

Imports Export

Source: CMIE database

Maize is an important crop in India. Besides being used for human consumption, it is a

key ingredient of poultry and livestock feeds. The poultry industry in India is rapidly

increasing. The country‘s requirement for poultry feed is increasing at over 10 % per

annum. Its demand for industrial uses is expected to increase. The maize sector has lot

of potential for growth.

43

Chapter 3: Policy and Institutional Framework for

Maize Sector in Bihar

This chapter will map the institutional framework and the policies/programmes relating

to maize sector in Bihar. The presence and role of major institutions and associations

that are associated directly or indirectly with maize have been discussed.

3.1. Institutions in Maize Sector in Bihar

Following institutions are working in Bihar on maize sector.

1. Bihar Veterinary College, Patna - This College helps the farmers & the

industries, related to poultry & dairy sector. It also does technology transfer

(Lab to Land program) through its respective Krishi Vigyan Kendra‘s (KVKs).

Poultry in Bihar is not a great success story due to socio-economic constrains,

but dairy is a success.

2. College of Agricultural Engineering, Samastipur, Rajendra Agricultural

University, Pusa, Samastipur - This institute is primarily responsible for the

irrigation aspects of maize in Bihar. Good work is being done on spring maize.

The exponential increment in the quality & quantity of spring maize yields in

the last half a decade is the proof of it.

3. College of Fisheries, Dholi & College of Fisheries, Tirhut , College of

Agriculture (TCA) campus, Muzaffarpur – Pusa Road, Doli, Muzaffarpur

– Though traditionally a fish eating state, these two colleges has not been

exploited by the fishermen & government to make fisheries an industry. This is

evident from the fact quoted by Deputy Director Fisheries, Department of

Fisheries, GoB, who had an interview with World Bank & IL&FS-CDI that

presently 25% of the water bodies are being utilized with a ―capture fishing

process‖ not the ―culture fishing process‖. The state imports 20% of its

requirement from West Bengal & Andhra Pradesh. At present, the total fish

requirement in Bihar is 2 lakh tons per year with an average yield of 3-5 t per ha

per year. There are no fish feed unit in Bihar. According to a recent research

44

carried out in the Institute, fish feed should contain about 45% of maize for

better fish production per year. Presently the fishermen are using cow-dung &

organic manures to grow phytons for the fish while they use mustard cake with

rice bran cake, mixed in molasses to directly feed the fish. This feed is works

out to be cheaper than maize as in the fish producing districts of Bihar, maize is

not adequately produced/available. These flood prone fish producing districts

mostly grow paddy in kharif followed by mustard in Rabi. GoB is planning to

double its fish volume by 2013, by bringing in additional 20000 ha under fish

culture to make it a total of 50000 ha of area under fish culture. The output will

also be increased from 3 tons to 5 tons fish per ha per year. To make this happen

by 2013, about 2.58 lakh tons of fish feed is required which would have over

one lakh tons of maize in it.

These two colleges are now consulting Central Institute of Fresh Water

Aquaculture (CIFWA), Bhubneshwar to make fish feed units in Bihar. A

proposal is with GoB submitted by the department that 25% subsidy with a cap

of Rs.12 lakh will be given to fisheries graduate for setting up a new fish feed

unit. To make these feed units viable Rs.20000/- per acre of pond will be given

to energize it. This one acre can hold 1 lakh fingerlings which can be sold @5

paise per fingerlings. Feeding the fish from these feed units can produce 1kg of

Katla (local freshwater fish variety), @ Rs.50 per kg, in a year from the

fingerlings. The proposal looks to be viable but requires initiatives from

fishermen & fisheries graduate.

4. Rajendra Agricultural University, Faculty Of Agriculture, P O Pusa,

Samastipur - Established on 3rd

December 1974, it has a mandate for overall

development of the maize sector. This institute has done good work in the initial

stages till 1979 for white corn. Presently it has a full-fledged maize research

team with the Maize Coordinator as head. It produces small quantity of seed for

Bihar Beej Nigam, but the volumes are decreasing as the seed sector is

dominated by the private players. The university is helping GoB in drafting the

―Bihar Road Map for Agriculture‖ with the following highlights on maize:

45

DoA will soon bring out a MAIZE MISSION for Bihar. The highlights of it will

be as follows

1) Growing maize in flood prone areas.

2) Setting up 12 godowns in all the maize growing districts

3) Setting up of rural godowns in 216 blocks of each 250 MT.

4) Target production by 2012 to be 3 million MT per annum from 1 million

hectare with yield of 3t/ha

Seed production will be private companies' domain

Immediate investment in farm mechanization and rural warehousing.

Warehousing will cost Rs.2.5 million for 1000 MT.

With the joint effort of this university and Directorate of Maize Research (DMR),

Begusarai some good Quality Protein Maize (QPM) has been released. GoB is

promoting QPM as mid-day meal in all government schools. To make this happen,

the university is helping the processors like Katyani Makka Udayog, to set up a unit

in Khagaria. The World Bank & IL&FS-CDI, has visited this processing unit at

Chautham in Khagaria district. This unit is temporarily closed due to financial

issues. One of the best cases of technology transfer by the university can be

observed as given below:

46

Source: www.rwc.cgiar.org/RSCRTCC/2005/Sessions

5. Sanjay Gandhi Institute of Dairy Science and Tech., Pusa, Samastipur &

Sanjay Gandhi Institute of Dairy Technology, Patna, Rajendra

Agricultural University, P O Dhelwan, Lohiyanagar, Patna – These two

institutes have done a commendable job creating an oldest (25 years old) single

most success story of Bihar, i.e., Bihar State. Cooperative Milk Producers‘

Federations Limited (COMPFED). As per interview conducted by World Bank

and IL&FS-CDI with the General Manager, Operations, COMPFED, will be

doubling its capacity to 200t/day of cattle feed in the next four years with 16%

growth per annum. COMPFED procures 60-70% of its maize requirement from

Bihar. COMPFED prepares the following animal feeds with different maize

compositions:

47

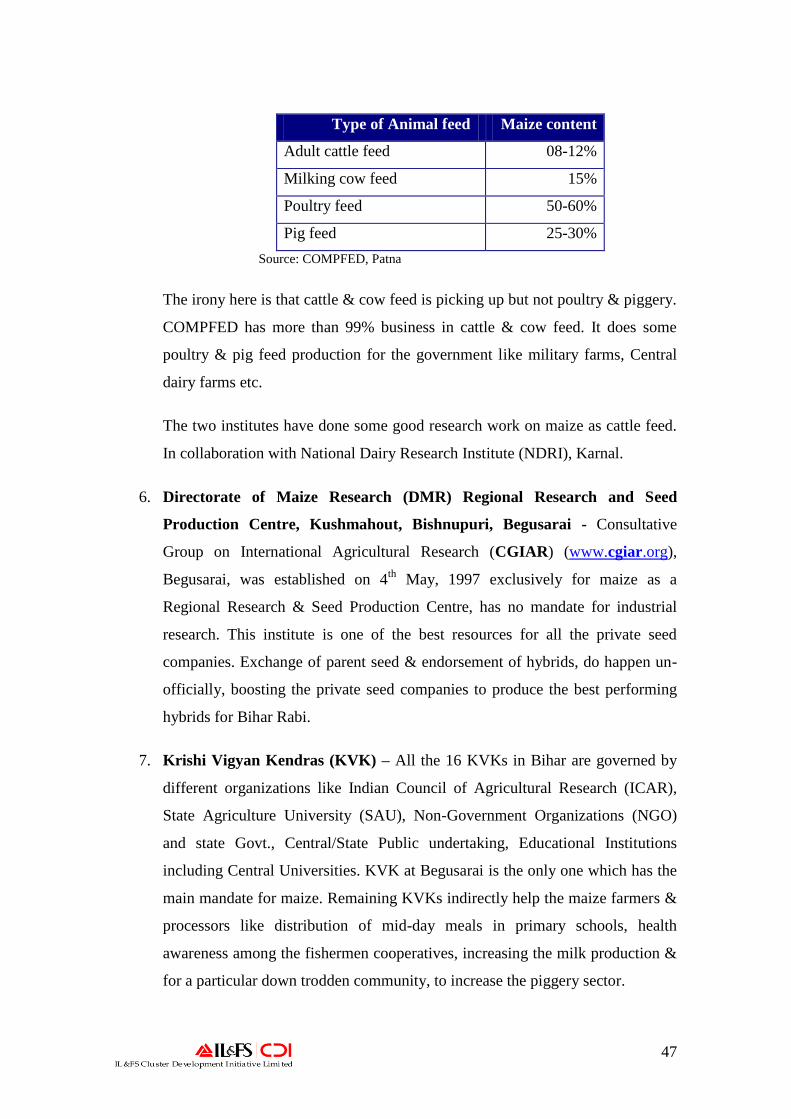

Type of Animal feed Maize content

Adult cattle feed 08-12%

Milking cow feed 15%

Poultry feed 50-60%

Pig feed 25-30%

Source: COMPFED, Patna

The irony here is that cattle & cow feed is picking up but not poultry & piggery.

COMPFED has more than 99% business in cattle & cow feed. It does some

poultry & pig feed production for the government like military farms, Central

dairy farms etc.

The two institutes have done some good research work on maize as cattle feed.

In collaboration with National Dairy Research Institute (NDRI), Karnal.

6. Directorate of Maize Research (DMR) Regional Research and Seed

Production Centre, Kushmahout, Bishnupuri, Begusarai - Consultative

Group on International Agricultural Research (CGIAR) (www.cgiar.org),

Begusarai, was established on 4th

May, 1997 exclusively for maize as a

Regional Research & Seed Production Centre, has no mandate for industrial

research. This institute is one of the best resources for all the private seed

companies. Exchange of parent seed & endorsement of hybrids, do happen un-

officially, boosting the private seed companies to produce the best performing

hybrids for Bihar Rabi.

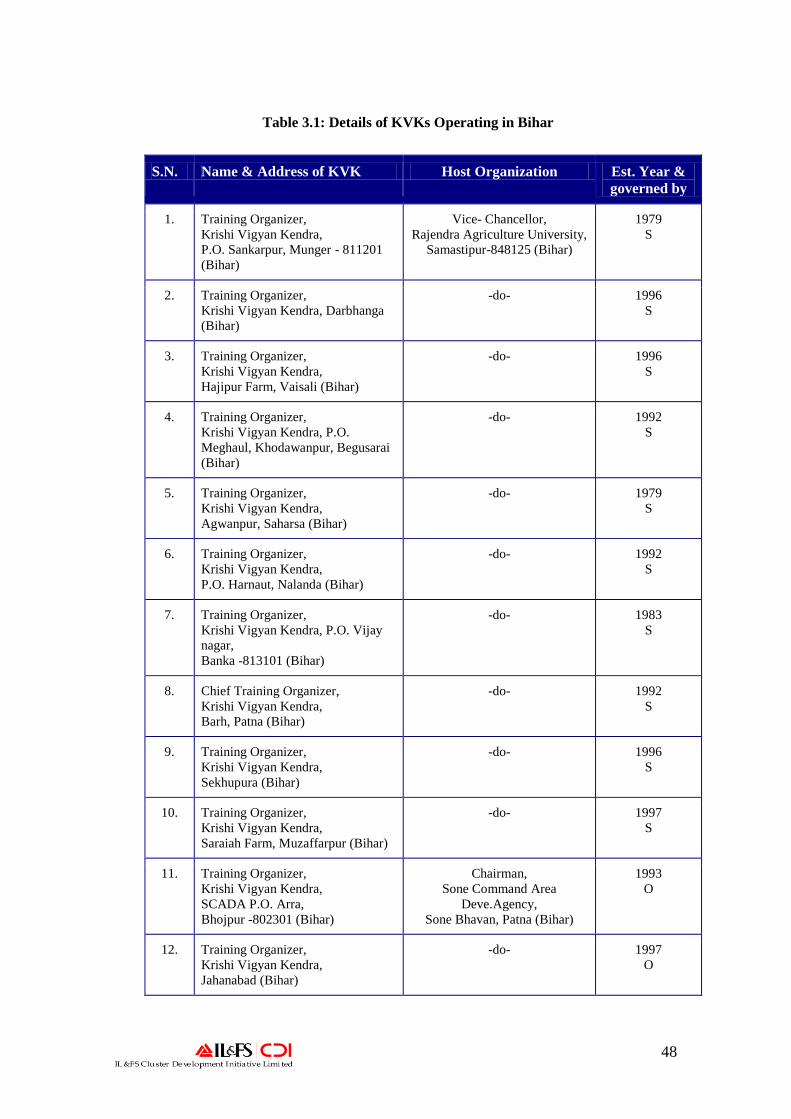

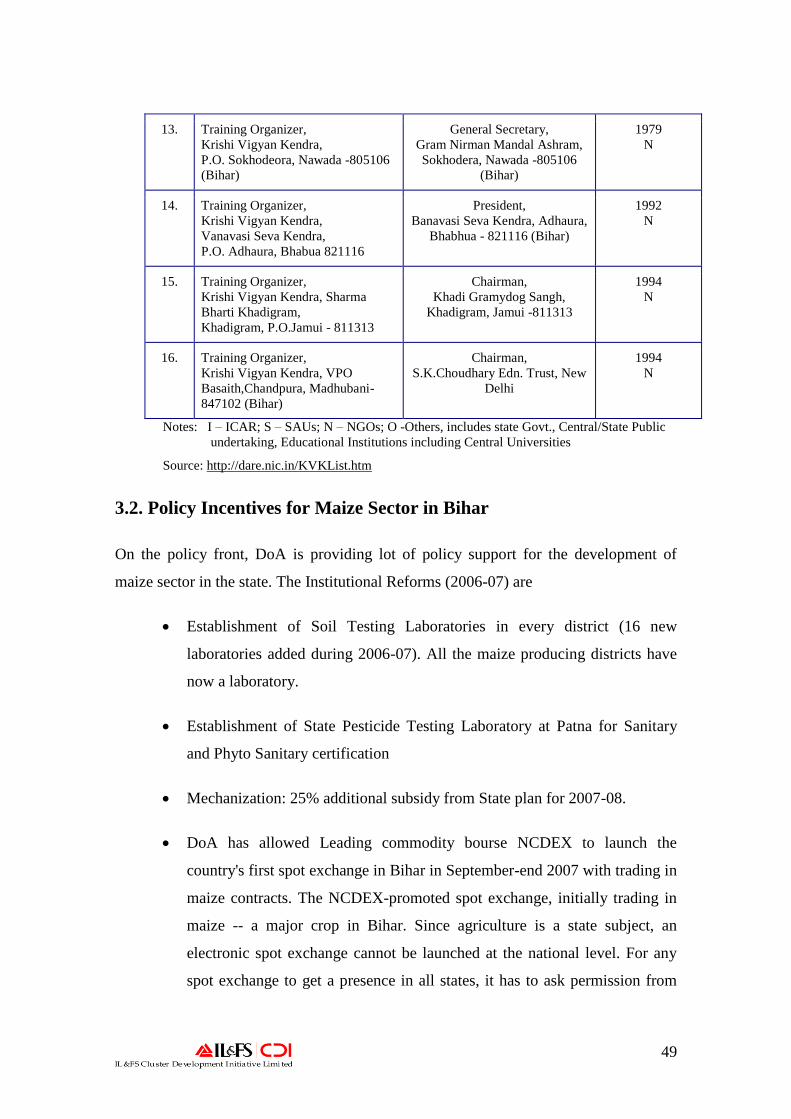

7. Krishi Vigyan Kendras (KVK) – All the 16 KVKs in Bihar are governed by

different organizations like Indian Council of Agricultural Research (ICAR),

State Agriculture University (SAU), Non-Government Organizations (NGO)

and state Govt., Central/State Public undertaking, Educational Institutions

including Central Universities. KVK at Begusarai is the only one which has the

main mandate for maize. Remaining KVKs indirectly help the maize farmers &

processors like distribution of mid-day meals in primary schools, health

awareness among the fishermen cooperatives, increasing the milk production &

for a particular down trodden community, to increase the piggery sector.

48

Table 3.1: Details of KVKs Operating in Bihar

S.N. Name & Address of KVK Host Organization Est. Year &

governed by

1. Training Organizer,

Krishi Vigyan Kendra,

P.O. Sankarpur, Munger - 811201

(Bihar)

Vice- Chancellor,

Rajendra Agriculture University,

Samastipur-848125 (Bihar)

1979

S

2. Training Organizer,

Krishi Vigyan Kendra, Darbhanga

(Bihar)

-do- 1996

S

3. Training Organizer,

Krishi Vigyan Kendra,

Hajipur Farm, Vaisali (Bihar)

-do- 1996

S

4. Training Organizer,

Krishi Vigyan Kendra, P.O.

Meghaul, Khodawanpur, Begusarai

(Bihar)

-do- 1992

S

5. Training Organizer,

Krishi Vigyan Kendra,

Agwanpur, Saharsa (Bihar)

-do- 1979

S

6. Training Organizer,

Krishi Vigyan Kendra,

P.O. Harnaut, Nalanda (Bihar)

-do- 1992

S

7. Training Organizer,

Krishi Vigyan Kendra, P.O. Vijay

nagar,

Banka -813101 (Bihar)

-do- 1983

S

8. Chief Training Organizer,

Krishi Vigyan Kendra,

Barh, Patna (Bihar)

-do- 1992

S

9. Training Organizer,

Krishi Vigyan Kendra,

Sekhupura (Bihar)

-do- 1996

S

10. Training Organizer,

Krishi Vigyan Kendra,

Saraiah Farm, Muzaffarpur (Bihar)

-do- 1997

S

11. Training Organizer,

Krishi Vigyan Kendra,

SCADA P.O. Arra,

Bhojpur -802301 (Bihar)

Chairman,

Sone Command Area

Deve.Agency,

Sone Bhavan, Patna (Bihar)

1993

O

12. Training Organizer,

Krishi Vigyan Kendra,

Jahanabad (Bihar)

-do- 1997

O

49

13. Training Organizer,

Krishi Vigyan Kendra,

P.O. Sokhodeora, Nawada -805106

(Bihar)

General Secretary,

Gram Nirman Mandal Ashram,

Sokhodera, Nawada -805106

(Bihar)

1979

N

14. Training Organizer,

Krishi Vigyan Kendra,

Vanavasi Seva Kendra,

P.O. Adhaura, Bhabua 821116

President,

Banavasi Seva Kendra, Adhaura,

Bhabhua - 821116 (Bihar)

1992

N

15. Training Organizer,

Krishi Vigyan Kendra, Sharma

Bharti Khadigram,

Khadigram, P.O.Jamui - 811313

Chairman,

Khadi Gramydog Sangh,

Khadigram, Jamui -811313

1994

N

16. Training Organizer,

Krishi Vigyan Kendra, VPO

Basaith,Chandpura, Madhubani-

847102 (Bihar)

Chairman,

S.K.Choudhary Edn. Trust, New

Delhi

1994

N

Notes: I – ICAR; S – SAUs; N – NGOs; O -Others, includes state Govt., Central/State Public

undertaking, Educational Institutions including Central Universities

Source: http://dare.nic.in/KVKList.htm

3.2. Policy Incentives for Maize Sector in Bihar

On the policy front, DoA is providing lot of policy support for the development of

maize sector in the state. The Institutional Reforms (2006-07) are

Establishment of Soil Testing Laboratories in every district (16 new

laboratories added during 2006-07). All the maize producing districts have

now a laboratory.

Establishment of State Pesticide Testing Laboratory at Patna for Sanitary

and Phyto Sanitary certification

Mechanization: 25% additional subsidy from State plan for 2007-08.

DoA has allowed Leading commodity bourse NCDEX to launch the

country's first spot exchange in Bihar in September-end 2007 with trading in

maize contracts. The NCDEX-promoted spot exchange, initially trading in

maize -- a major crop in Bihar. Since agriculture is a state subject, an

electronic spot exchange cannot be launched at the national level. For any

spot exchange to get a presence in all states, it has to ask permission from

50

each state separately. The sellers would be from Bihar but buyers could be

from anywhere in the country. Traders functioning in futures market can

also buy from the spot market. (Source: Fifth Column in KOILAKH NEWS

on August 27, 2007 3:39:00 PM & DoA)

On seed, DoA is still following the National Seeds Policy, 2002 9. The

present government under the initiative for development of agriculture in

state of Bihar has formulated a ‘Bihar Seed Plan’, mainly comprising of –

1. Revival of ‗Bihar State Seed Corporation‘

2. Revival of State Seed Farms

3. Establishment of Seed Testing Laboratory at district, subdivision, and

block levels subsequently.

4. To promote the use of hybrid maize seeds during kharif up to 50 percent.

5. Development of very short duration seed banks in flood prone areas.

Bihar Government has started working on ‘Bihar Seed Plan’, but substantial progress

is yet to be made in this direction.

In addition to above, DoA is also planning for

Implementation of Vaidyanathan Committee Report on Cooperative Credit.

Krishak Salahkar (Agri-consultants) as para extension service providers to

farmers in all Panchayats

Department of Industries has not yet taken any concrete steps exclusively for

development of maize processing sector in Bihar. The policy remains the same which is

in general for all the industries.

9 Source: www. indian seed act 2002_files

51

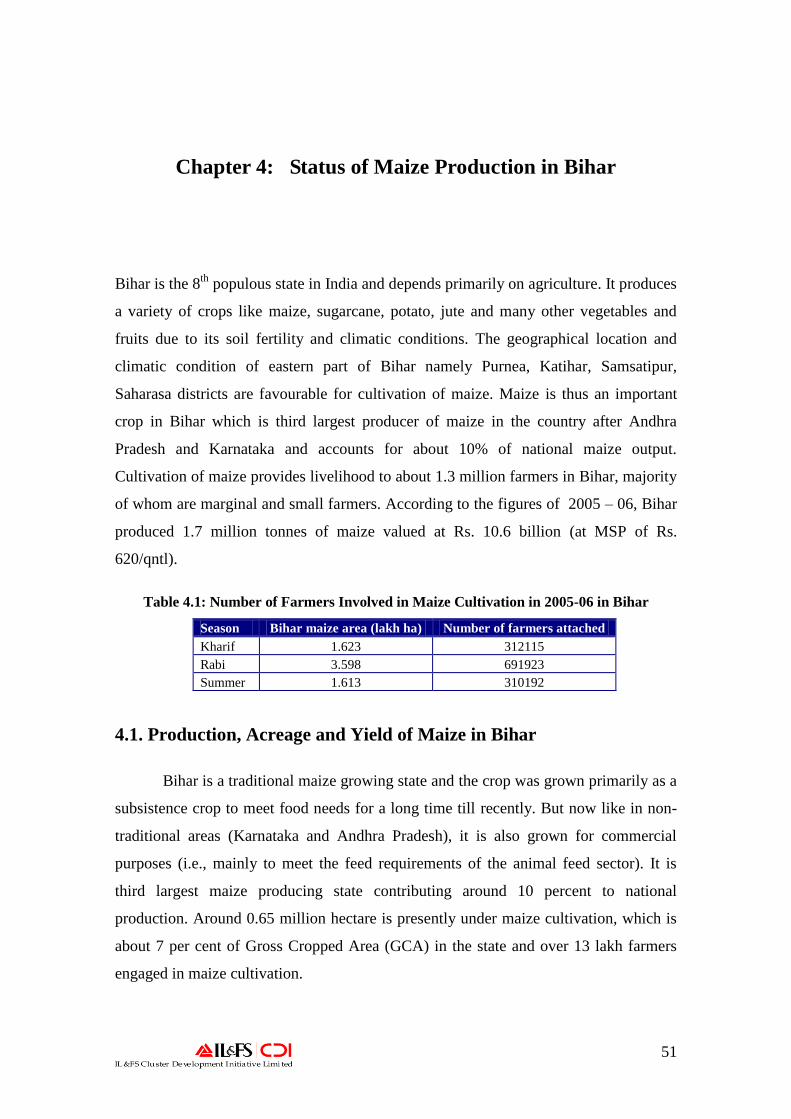

Chapter 4: Status of Maize Production in Bihar

Bihar is the 8th

populous state in India and depends primarily on agriculture. It produces

a variety of crops like maize, sugarcane, potato, jute and many other vegetables and

fruits due to its soil fertility and climatic conditions. The geographical location and

climatic condition of eastern part of Bihar namely Purnea, Katihar, Samsatipur,

Saharasa districts are favourable for cultivation of maize. Maize is thus an important

crop in Bihar which is third largest producer of maize in the country after Andhra

Pradesh and Karnataka and accounts for about 10% of national maize output.

Cultivation of maize provides livelihood to about 1.3 million farmers in Bihar, majority

of whom are marginal and small farmers. According to the figures of 2005 – 06, Bihar

produced 1.7 million tonnes of maize valued at Rs. 10.6 billion (at MSP of Rs.

620/qntl).

Table 4.1: Number of Farmers Involved in Maize Cultivation in 2005-06 in Bihar

Season Bihar maize area (lakh ha) Number of farmers attached

Kharif 1.623 312115

Rabi 3.598 691923

Summer 1.613 310192

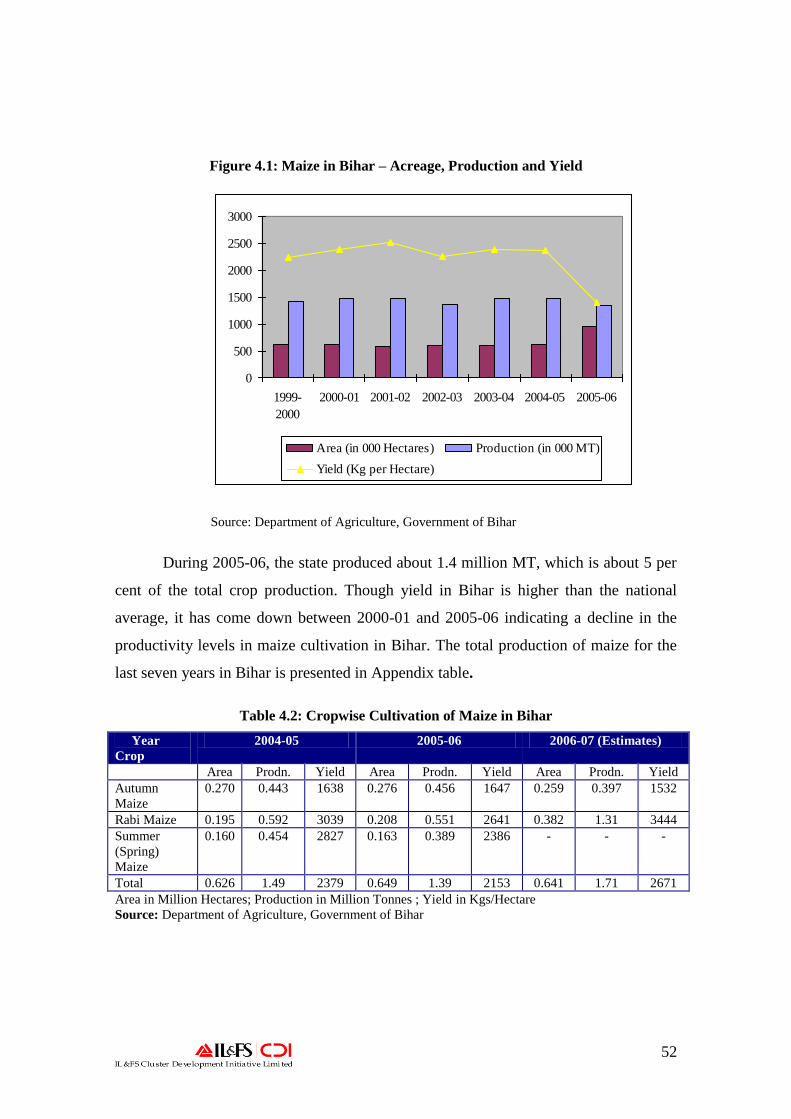

4.1. Production, Acreage and Yield of Maize in Bihar

Bihar is a traditional maize growing state and the crop was grown primarily as a

subsistence crop to meet food needs for a long time till recently. But now like in non-

traditional areas (Karnataka and Andhra Pradesh), it is also grown for commercial

purposes (i.e., mainly to meet the feed requirements of the animal feed sector). It is

third largest maize producing state contributing around 10 percent to national

production. Around 0.65 million hectare is presently under maize cultivation, which is

about 7 per cent of Gross Cropped Area (GCA) in the state and over 13 lakh farmers

engaged in maize cultivation.

52

Figure 4.1: Maize in Bihar – Acreage, Production and Yield

0

500

1000

1500

2000

2500

3000

1999-

2000

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

Area (in 000 Hectares) Production (in 000 MT)

Yield (Kg per Hectare)

Source: Department of Agriculture, Government of Bihar

During 2005-06, the state produced about 1.4 million MT, which is about 5 per

cent of the total crop production. Though yield in Bihar is higher than the national

average, it has come down between 2000-01 and 2005-06 indicating a decline in the

productivity levels in maize cultivation in Bihar. The total production of maize for the

last seven years in Bihar is presented in Appendix table.

Table 4.2: Cropwise Cultivation of Maize in Bihar

Year

Crop

2004-05 2005-06 2006-07 (Estimates)

Area Prodn. Yield Area Prodn. Yield Area Prodn. Yield

Autumn

Maize

0.270 0.443 1638 0.276 0.456 1647 0.259 0.397 1532

Rabi Maize 0.195 0.592 3039 0.208 0.551 2641 0.382 1.31 3444

Summer

(Spring)

Maize

0.160 0.454 2827 0.163 0.389 2386 - - -

Total 0.626 1.49 2379 0.649 1.39 2153 0.641 1.71 2671

Area in Million Hectares; Production in Million Tonnes ; Yield in Kgs/Hectare

Source: Department of Agriculture, Government of Bihar

53

Fig 4.2: Agricultural Map of Bihar

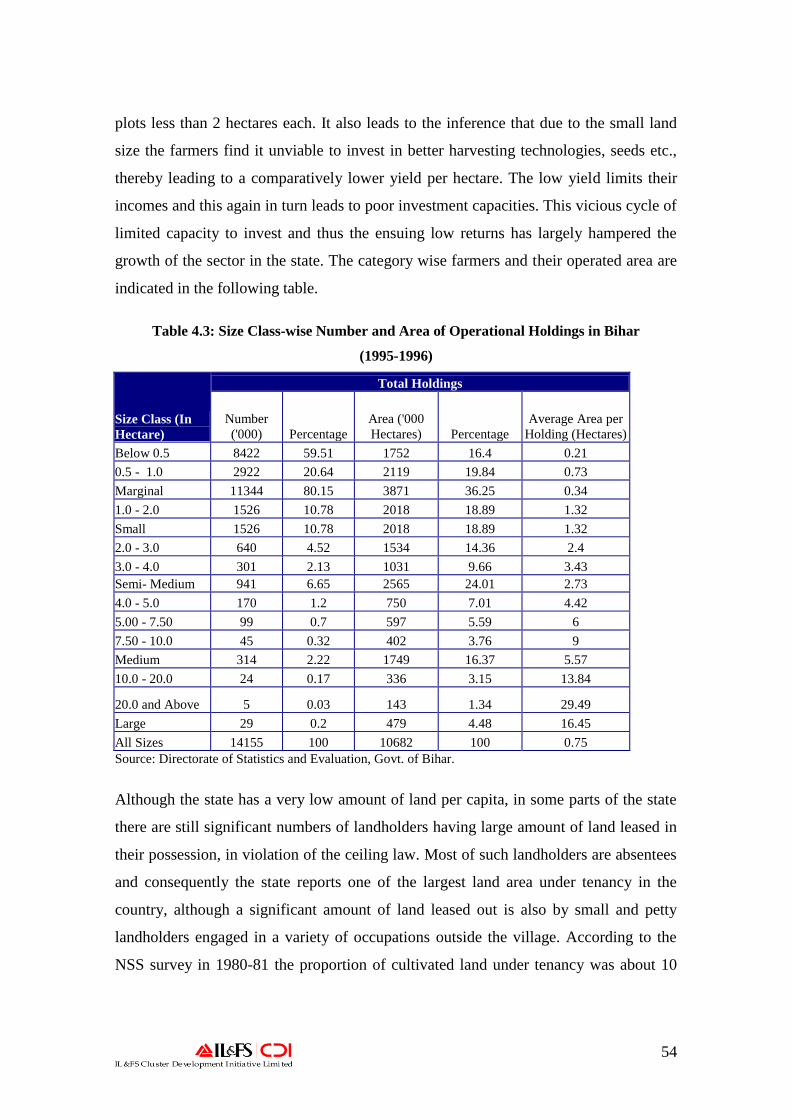

4.2. Status of Maize Cultivation in Bihar

4.2.1. Size of Farm Land Holdings

Maize is mainly grown by small and marginal farmers in Bihar. The

fragmentation of land holdings is much more pronounced in Bihar than other states as

the average per capita operational holding in the state was 0.75 hectares in 1995-96

much below the national average and nearly one quarter of the size of Punjab. About

one-third of the operational holdings are marginal (less than one hectare) in which the

average size is merely 0.34 hectare. This explains the largely unorganised nature of

maize cultivation in the state where about 91% of the cropped area is dissected into

54

plots less than 2 hectares each. It also leads to the inference that due to the small land

size the farmers find it unviable to invest in better harvesting technologies, seeds etc.,

thereby leading to a comparatively lower yield per hectare. The low yield limits their

incomes and this again in turn leads to poor investment capacities. This vicious cycle of

limited capacity to invest and thus the ensuing low returns has largely hampered the

growth of the sector in the state. The category wise farmers and their operated area are

indicated in the following table.

Table 4.3: Size Class-wise Number and Area of Operational Holdings in Bihar

(1995-1996)

Size Class (In

Hectare)

Total Holdings

Number

('000) Percentage

Area ('000

Hectares) Percentage

Average Area per

Holding (Hectares)

Below 0.5 8422 59.51 1752 16.4 0.21

0.5 - 1.0 2922 20.64 2119 19.84 0.73

Marginal 11344 80.15 3871 36.25 0.34

1.0 - 2.0 1526 10.78 2018 18.89 1.32

Small 1526 10.78 2018 18.89 1.32

2.0 - 3.0 640 4.52 1534 14.36 2.4

3.0 - 4.0 301 2.13 1031 9.66 3.43

Semi- Medium 941 6.65 2565 24.01 2.73

4.0 - 5.0 170 1.2 750 7.01 4.42

5.00 - 7.50 99 0.7 597 5.59 6

7.50 - 10.0 45 0.32 402 3.76 9

Medium 314 2.22 1749 16.37 5.57

10.0 - 20.0 24 0.17 336 3.15 13.84

20.0 and Above 5 0.03 143 1.34 29.49

Large 29 0.2 479 4.48 16.45

All Sizes 14155 100 10682 100 0.75

Source: Directorate of Statistics and Evaluation, Govt. of Bihar.

Although the state has a very low amount of land per capita, in some parts of the state

there are still significant numbers of landholders having large amount of land leased in

their possession, in violation of the ceiling law. Most of such landholders are absentees

and consequently the state reports one of the largest land area under tenancy in the

country, although a significant amount of land leased out is also by small and petty

landholders engaged in a variety of occupations outside the village. According to the

NSS survey in 1980-81 the proportion of cultivated land under tenancy was about 10

55

percent. Thus farmers have limited interest and capacity to invest in farm land fertility

etc.

Maize is grown throughout the year in Bihar all three seasonal crops of maize are

cultivated; however, main crop is Rabi maize. Winter (Rabi) maize is the USP of the

state that dominates total maize production in the state with a 40 percent share.

Monsoon (Kharif) maize and Summer maize each contributes about 23 percent to the

total maize area.

Maize is grown in almost all the districts of Bihar. The leading district is Khagaria,

which accounts for about 12 per cent of maize production in the state. Other important

maize producing districts include Begusarai, Madhepura, Saharsa, Purnea, Katihar,

Muzaffarpur, Vaishali, and Samstipur. As maize is grown in most of the districts of the

state, there is not much movement of the grains within the state. Entire stretch form

Begusarai to Khagaria on the north side of national highway, having highly fertile land

of Gangetic plains provides very favourable soil for maize cultivation. The acreage,

production and yield of major maize (Rabi, Kharif and Summer) growing districts in

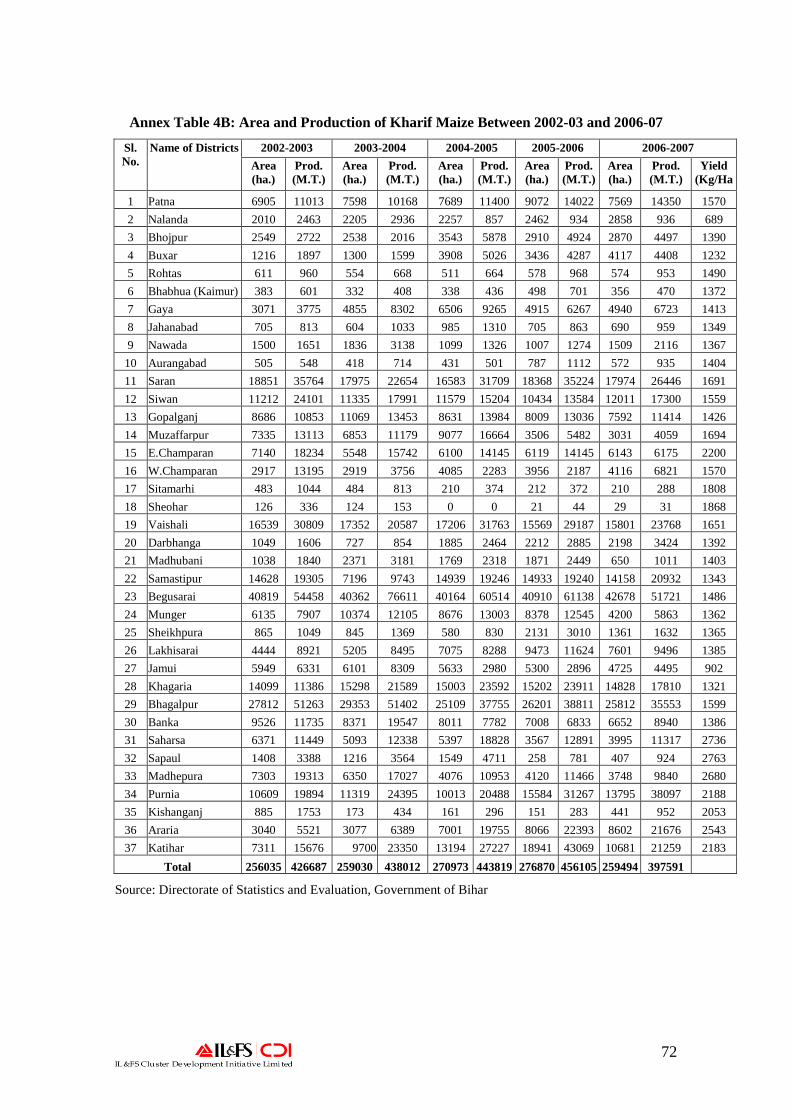

Bihar during 2006-07 is indicated in the following table

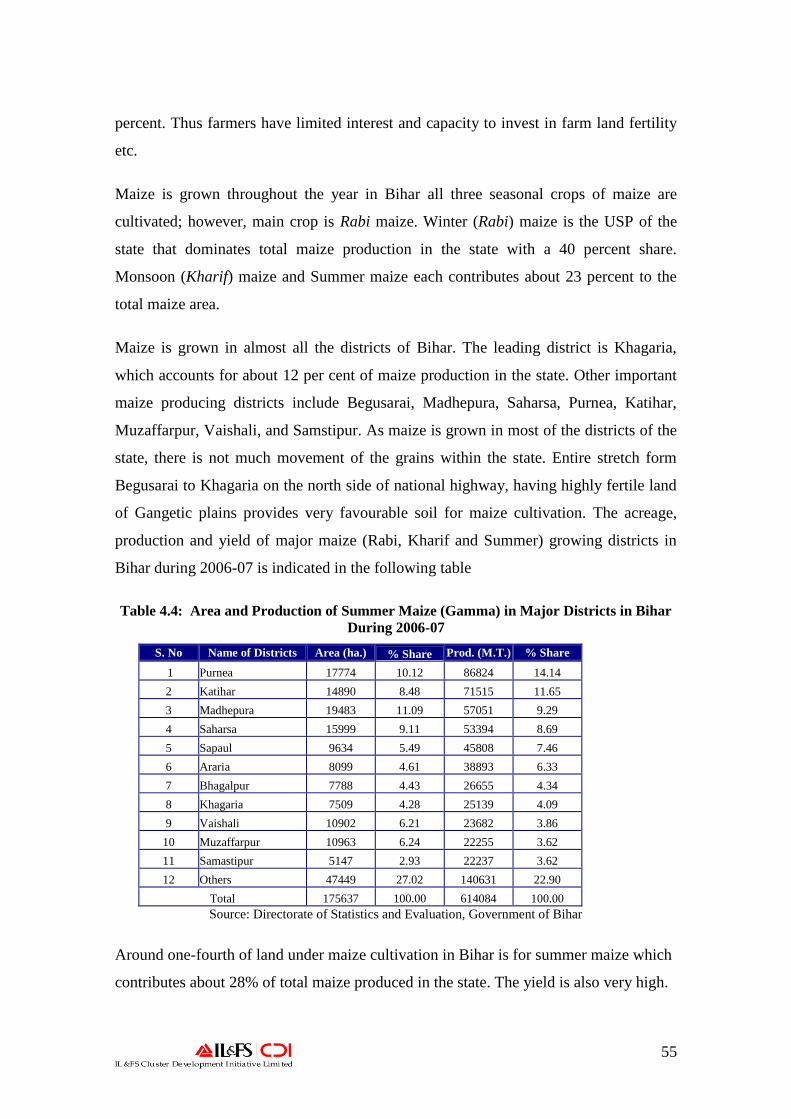

Table 4.4: Area and Production of Summer Maize (Gamma) in Major Districts in Bihar

During 2006-07

S. No Name of Districts Area (ha.) % Share Prod. (M.T.) % Share

1 Purnea 17774 10.12 86824 14.14

2 Katihar 14890 8.48 71515 11.65

3 Madhepura 19483 11.09 57051 9.29

4 Saharsa 15999 9.11 53394 8.69

5 Sapaul 9634 5.49 45808 7.46

6 Araria 8099 4.61 38893 6.33

7 Bhagalpur 7788 4.43 26655 4.34

8 Khagaria 7509 4.28 25139 4.09

9 Vaishali 10902 6.21 23682 3.86

10 Muzaffarpur 10963 6.24 22255 3.62

11 Samastipur 5147 2.93 22237 3.62

12 Others 47449 27.02 140631 22.90

Total 175637 100.00 614084 100.00

Source: Directorate of Statistics and Evaluation, Government of Bihar

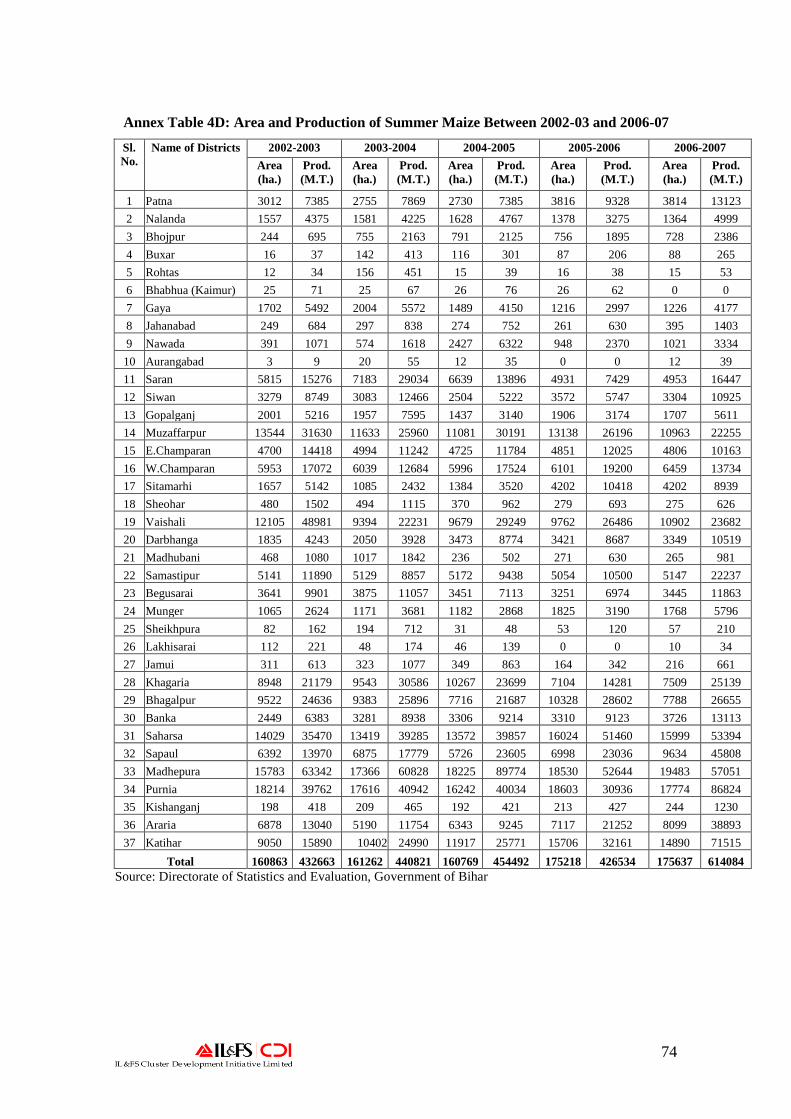

Around one-fourth of land under maize cultivation in Bihar is for summer maize which

contributes about 28% of total maize produced in the state. The yield is also very high.

56

It is mainly grown in the districts pf Purnea, Katihar, Madhepura, Saharsa, and Supaul.

These together account for 45% of acreage and 50% of production of summer maize in

the state.

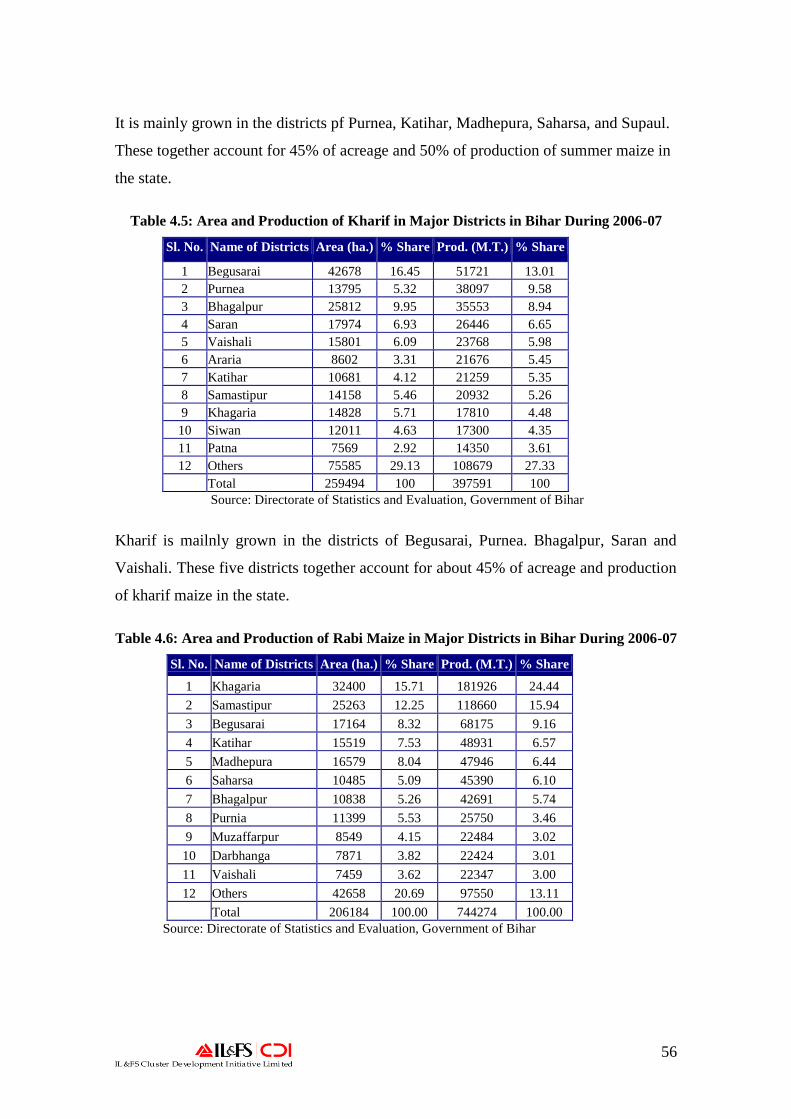

Table 4.5: Area and Production of Kharif in Major Districts in Bihar During 2006-07

Sl. No. Name of Districts Area (ha.) % Share Prod. (M.T.) % Share

1 Begusarai 42678 16.45 51721 13.01

2 Purnea 13795 5.32 38097 9.58

3 Bhagalpur 25812 9.95 35553 8.94

4 Saran 17974 6.93 26446 6.65

5 Vaishali 15801 6.09 23768 5.98

6 Araria 8602 3.31 21676 5.45

7 Katihar 10681 4.12 21259 5.35

8 Samastipur 14158 5.46 20932 5.26

9 Khagaria 14828 5.71 17810 4.48

10 Siwan 12011 4.63 17300 4.35

11 Patna 7569 2.92 14350 3.61

12 Others 75585 29.13 108679 27.33

Total 259494 100 397591 100

Source: Directorate of Statistics and Evaluation, Government of Bihar

Kharif is mailnly grown in the districts of Begusarai, Purnea. Bhagalpur, Saran and

Vaishali. These five districts together account for about 45% of acreage and production

of kharif maize in the state.

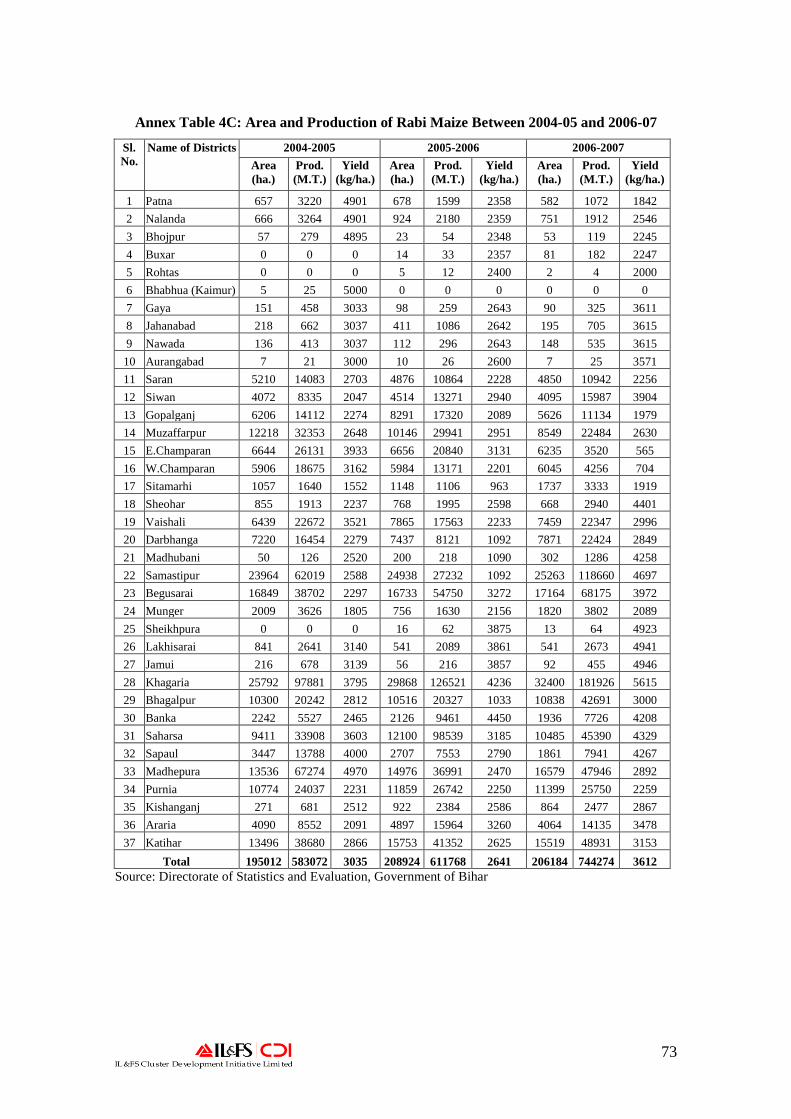

Table 4.6: Area and Production of Rabi Maize in Major Districts in Bihar During 2006-07

Sl. No. Name of Districts Area (ha.) % Share Prod. (M.T.) % Share

1 Khagaria 32400 15.71 181926 24.44

2 Samastipur 25263 12.25 118660 15.94

3 Begusarai 17164 8.32 68175 9.16

4 Katihar 15519 7.53 48931 6.57

5 Madhepura 16579 8.04 47946 6.44

6 Saharsa 10485 5.09 45390 6.10

7 Bhagalpur 10838 5.26 42691 5.74

8 Purnia 11399 5.53 25750 3.46

9 Muzaffarpur 8549 4.15 22484 3.02

10 Darbhanga 7871 3.82 22424 3.01

11 Vaishali 7459 3.62 22347 3.00

12 Others 42658 20.69 97550 13.11

Total 206184 100.00 744274 100.00

Source: Directorate of Statistics and Evaluation, Government of Bihar

57

As far as Rabi maize is concerned Khagaria alone accounts for about one-fourth

of total production in the state. Samastipur, Begusarai and Katihar are other important

districts for maize production. These 4 districts together contribute 44% to acreage and

56% of total rabi maize produced in the state.

4.2.2. Cropping Pattern

There are two distinct maize cropping patterns in Bihar. In the flood prone areas

of Khagaria, Saharsa (Kosi) and parts of Samastipur maize is being cultivated during

rabi. In these districts sowing starts in October (after flood water recedes) and continues

up to early January. The majority of the sowing is done during December. Maize

harvest starts towards the end of February and continues till the end of June. Majority

of the crop is harvested during the months of May and June. In these parts of Bihar

maize is the major and in some cases the only crop.

In Begusarai and Samastipur, maize is cultivated during both seasons Rabi and

Khariff. The sowing, during the khariff season, starts during the month of June and

continues up to July. The harvesting starts around the month of September and last up

to October. The sowing and harvesting during rabi follow the similar pattern as

observed in other places. The seasonality chart is given below:

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Khariff

Rabi

Since most of the maize cultivation is concentrated in the districts of Khagaria, Saharsa,

Katihar and Purnea where it is grown only in Rabi, it can be concluded that the

proportion of Rabi maize (including both winter and spring) in the total maize

production of Bihar can be up to 80%. This was also corroborated during discussions

with farmer groups.

58

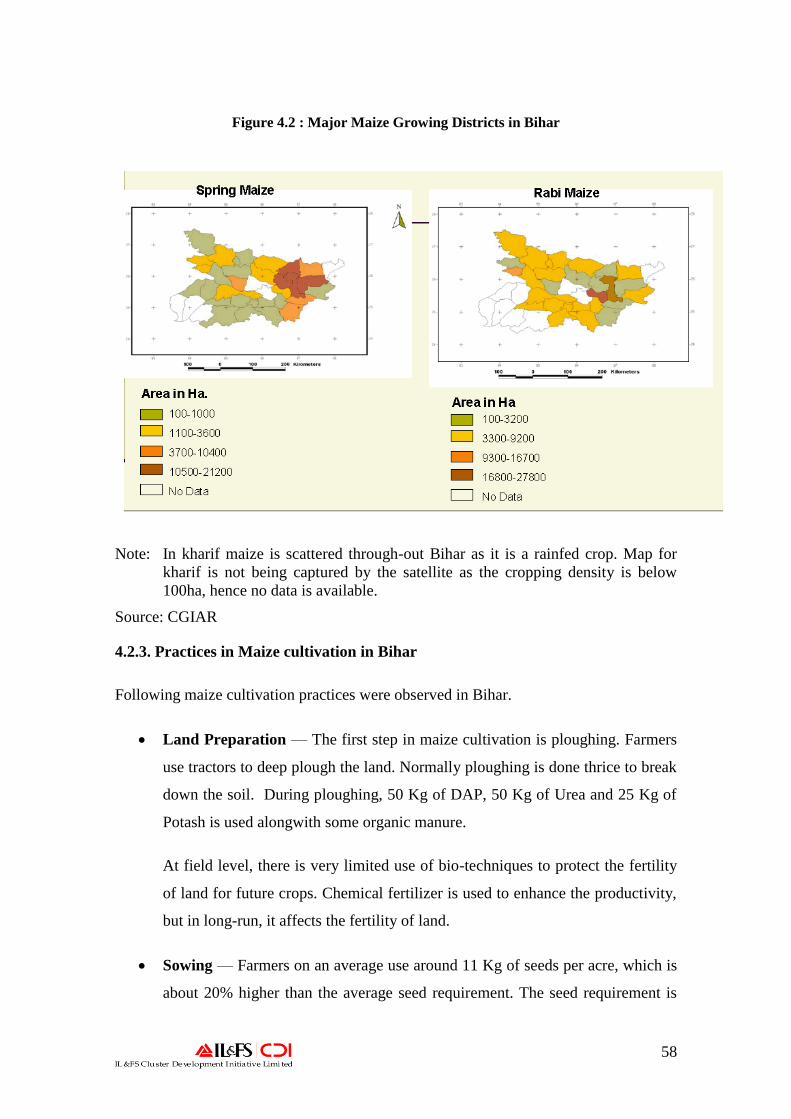

Figure 4.2 : Major Maize Growing Districts in Bihar

Note: In kharif maize is scattered through-out Bihar as it is a rainfed crop. Map for

kharif is not being captured by the satellite as the cropping density is below

100ha, hence no data is available.

Source: CGIAR

4.2.3. Practices in Maize cultivation in Bihar

Following maize cultivation practices were observed in Bihar.

Land Preparation — The first step in maize cultivation is ploughing. Farmers

use tractors to deep plough the land. Normally ploughing is done thrice to break

down the soil. During ploughing, 50 Kg of DAP, 50 Kg of Urea and 25 Kg of

Potash is used alongwith some organic manure.

At field level, there is very limited use of bio-techniques to protect the fertility

of land for future crops. Chemical fertilizer is used to enhance the productivity,

but in long-run, it affects the fertility of land.

Sowing — Farmers on an average use around 11 Kg of seeds per acre, which is

about 20% higher than the average seed requirement. The seed requirement is

59

higher because of lower germination rate and high incidence of plant mortality.

Line sowing was observed in most of the places.

Weeding — Normally weeding is done only once by the farmers when the

plant is 3-4 weeks old. Approximately 10 labours are used per acre to carry out

the process of weeding.

Irrigation — Normally the crop is irrigated 3 times but the number of

irrigations can vary between 2-6 times depending upon the climate. Normally

flood irrigation is applied to the crop. Use of sprinklers and/or drift irrigation

was not observed in the study area.

Diesel motors attached to bore-wells are used to irrigate the crop. The cost of

one time irrigation per acre is between Rs.400-Rs500.

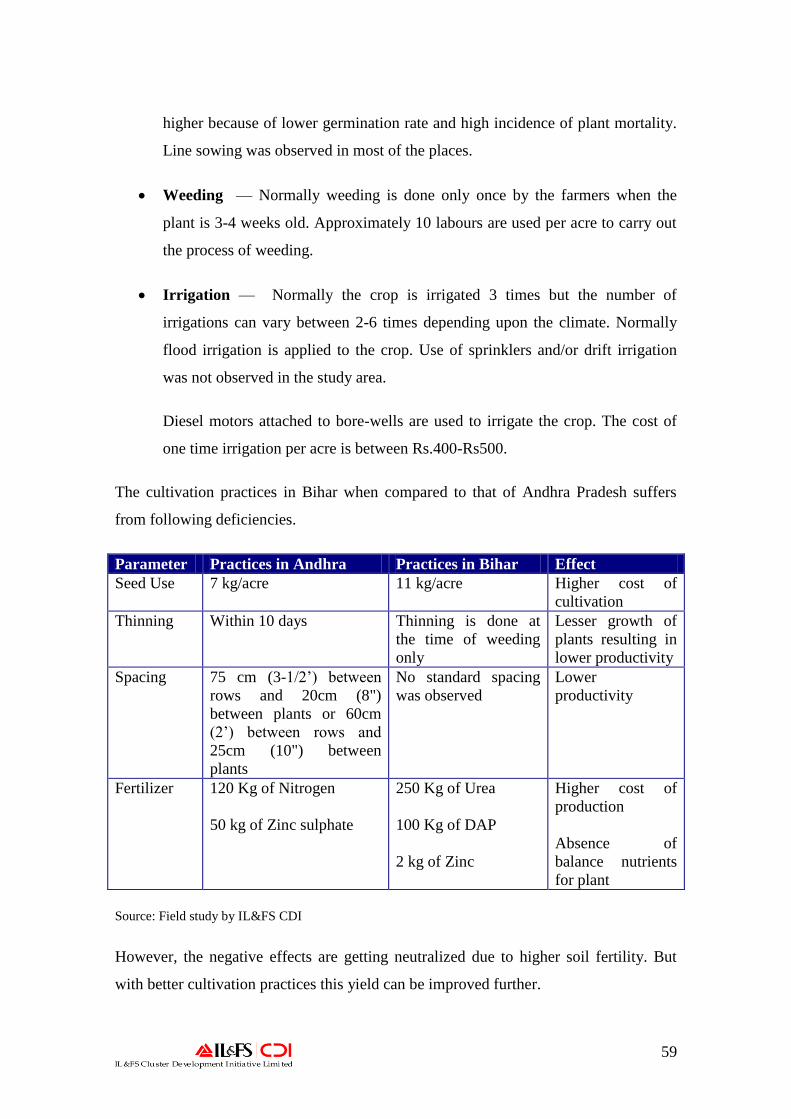

The cultivation practices in Bihar when compared to that of Andhra Pradesh suffers

from following deficiencies.

Parameter Practices in Andhra Practices in Bihar Effect

Seed Use 7 kg/acre 11 kg/acre Higher cost of

cultivation

Thinning Within 10 days Thinning is done at

the time of weeding

only

Lesser growth of

plants resulting in

lower productivity

Spacing 75 cm (3-1/2‘) between

rows and 20cm (8")

between plants or 60cm

(2‘) between rows and

25cm (10") between

plants

No standard spacing

was observed

Lower

productivity

Fertilizer 120 Kg of Nitrogen

50 kg of Zinc sulphate

250 Kg of Urea

100 Kg of DAP

2 kg of Zinc

Higher cost of

production

Absence of

balance nutrients

for plant

Source: Field study by IL&FS CDI

However, the negative effects are getting neutralized due to higher soil fertility. But

with better cultivation practices this yield can be improved further.

60

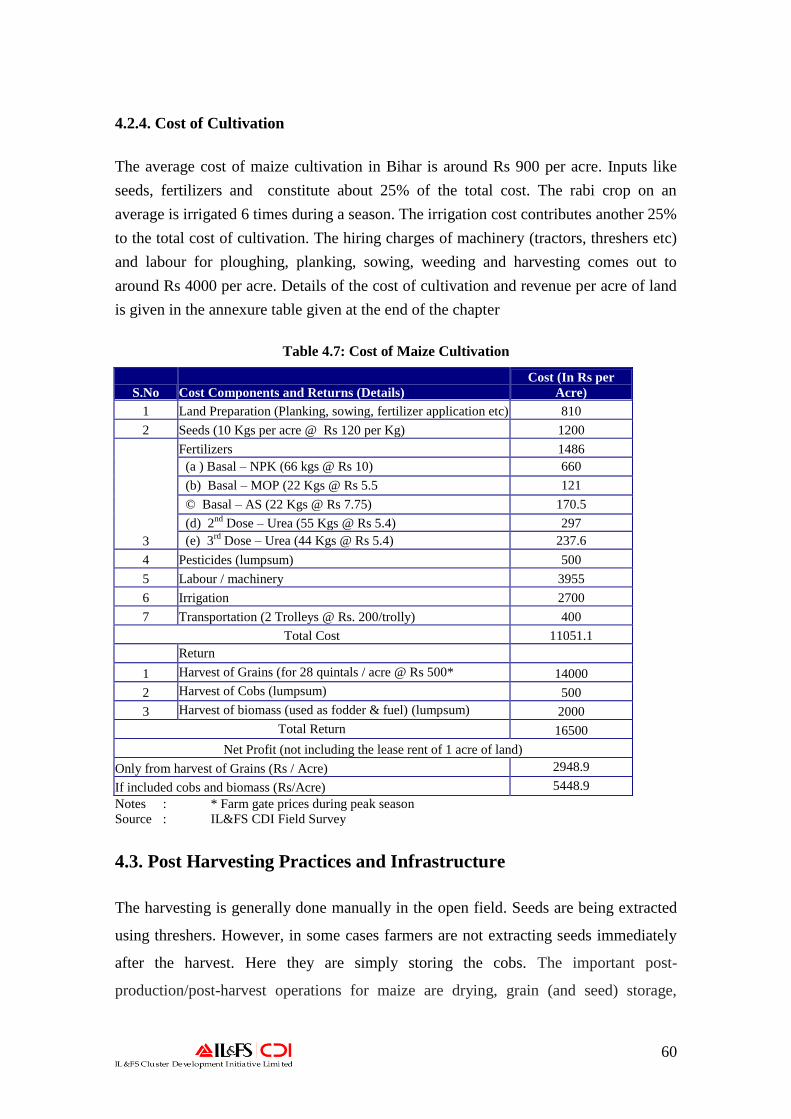

4.2.4. Cost of Cultivation

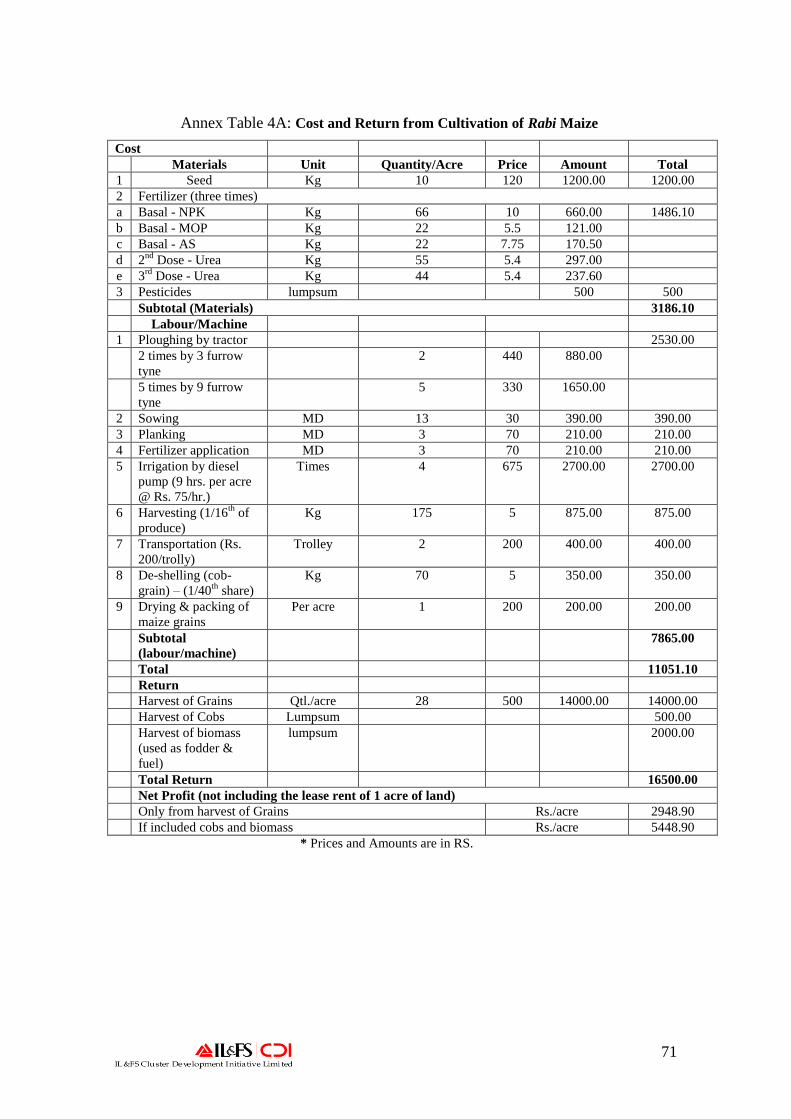

The average cost of maize cultivation in Bihar is around Rs 900 per acre. Inputs like

seeds, fertilizers and constitute about 25% of the total cost. The rabi crop on an

average is irrigated 6 times during a season. The irrigation cost contributes another 25%

to the total cost of cultivation. The hiring charges of machinery (tractors, threshers etc)

and labour for ploughing, planking, sowing, weeding and harvesting comes out to

around Rs 4000 per acre. Details of the cost of cultivation and revenue per acre of land

is given in the annexure table given at the end of the chapter

Table 4.7: Cost of Maize Cultivation

S.No Cost Components and Returns (Details)

Cost (In Rs per

Acre)

1 Land Preparation (Planking, sowing, fertilizer application etc) 810

2 Seeds (10 Kgs per acre @ Rs 120 per Kg) 1200

3

Fertilizers 1486

(a ) Basal – NPK (66 kgs @ Rs 10) 660

(b) Basal – MOP (22 Kgs @ Rs 5.5 121

© Basal – AS (22 Kgs @ Rs 7.75) 170.5

(d) 2nd

Dose – Urea (55 Kgs @ Rs 5.4) 297

(e) 3rd

Dose – Urea (44 Kgs @ Rs 5.4) 237.6

4 Pesticides (lumpsum) 500

5 Labour / machinery 3955

6 Irrigation 2700

7 Transportation (2 Trolleys @ Rs. 200/trolly) 400

Total Cost 11051.1

Return

1 Harvest of Grains (for 28 quintals / acre @ Rs 500* 14000

2 Harvest of Cobs (lumpsum) 500

3 Harvest of biomass (used as fodder & fuel) (lumpsum) 2000

Total Return 16500

Net Profit (not including the lease rent of 1 acre of land)

Only from harvest of Grains (Rs / Acre) 2948.9

If included cobs and biomass (Rs/Acre) 5448.9

Notes : * Farm gate prices during peak season

Source : IL&FS CDI Field Survey

4.3. Post Harvesting Practices and Infrastructure

The harvesting is generally done manually in the open field. Seeds are being extracted

using threshers. However, in some cases farmers are not extracting seeds immediately

after the harvest. Here they are simply storing the cobs. The important post-

production/post-harvest operations for maize are drying, grain (and seed) storage,

61

shelling, and milling. After extraction seeds are being sun-dried (on house roofs, flat

cement floors or roads, drying baskets, or plastic sheets because mechanical dryers are

not available in the villages) to reduce the moisture contents10

. Normally the seeds are

being dried for about 15 days before packing is done. After drying seeds are packed in

gunny bags and stored in sheds, storage barns, or plastic sacks at home which suffer

risk of damage due to pests and aflatoxin which makes it unsuitable to be used as raw

material for starch production. Only few farmers use fumigants like celphos to protect

the corn from grain-pest.

It is estimated that about 20-25% of the maize production is lost due to use of old and

obsolete post harvest machines and processes, open drying on floors inadequate

warehousing and grain store/bins, poor packing practices, and lack of collective

transportation facilities etc. The production loss due to poor post harvesting practices

and infrastructure affects the marketable surplus and thus the price and availability of

grain thus affecting the entire value chain in the state.

4.4. Storage and Warehousing

Most of the maize cultivators are small and medium farmers, so their grain retention

capacity is low (these farmers can‘t wait for higher prices of maize to sell their grains).

They sell most of their grains soon after harvesting to meet their essential expenses. In

maize belt of Khagaria and adjoining districts, which are flood prone, farmers sell their

grains otherwise it would be spoiled by flood water. Farmers have very limited in-

house capacity (2-10 quintals) to store their maize grains. These grains are stored in

gunny bags or wooden & earthen drum sort of pot having limited storage capacity.

Some pesticides are used to protect these grains during storage. No mass scale storage

facility is available, either in private sector or public sector. Only Gulab Bag mandi has

storage capacity of 12000-15000 MT. It has about 15 godowns each having a capacity

to store 750-1000 MT of maize. Existence of facilities of ‗Central Ware Housing

10

Shelling of maize is mostly done through mechanical shellers. Normally, big farmers own these

machines and smaller ones use it on hire basis. However, there is a provision for subsidy on purchase of

shelling machines, but only a limited number of farmers can avail benefit of this scheme due to various

factors like higher price of machine, non-transparent procedure of getting these subsidies, scheme

available for a fixed pre-determined number of machines, etc.

62

Corporation‘ or ‗Bihar State Ware Housing Corporation‘ is practically negligible in

maize producing areas. Lack of storage facility, prevent farmers from exploiting the

opportunity of good prices for their maize. It also leads to mass-transshipments of

maize grain by the traders .

4.5 Prices and Procurement

Basic staples in India including maize continue to be subjected to Minimum Support

Price (MSP) guarantees with the objective of ensuring remunerative prices to the

farmers, even out effects of seasonality, and promote agricultural diversification

although the guaranteed prices can be at times below prices prevailing in markets.

Though there is provision for MSP for maize grains, but at present there is no

procurement by the State agencies. Corn procurement by the government agency is

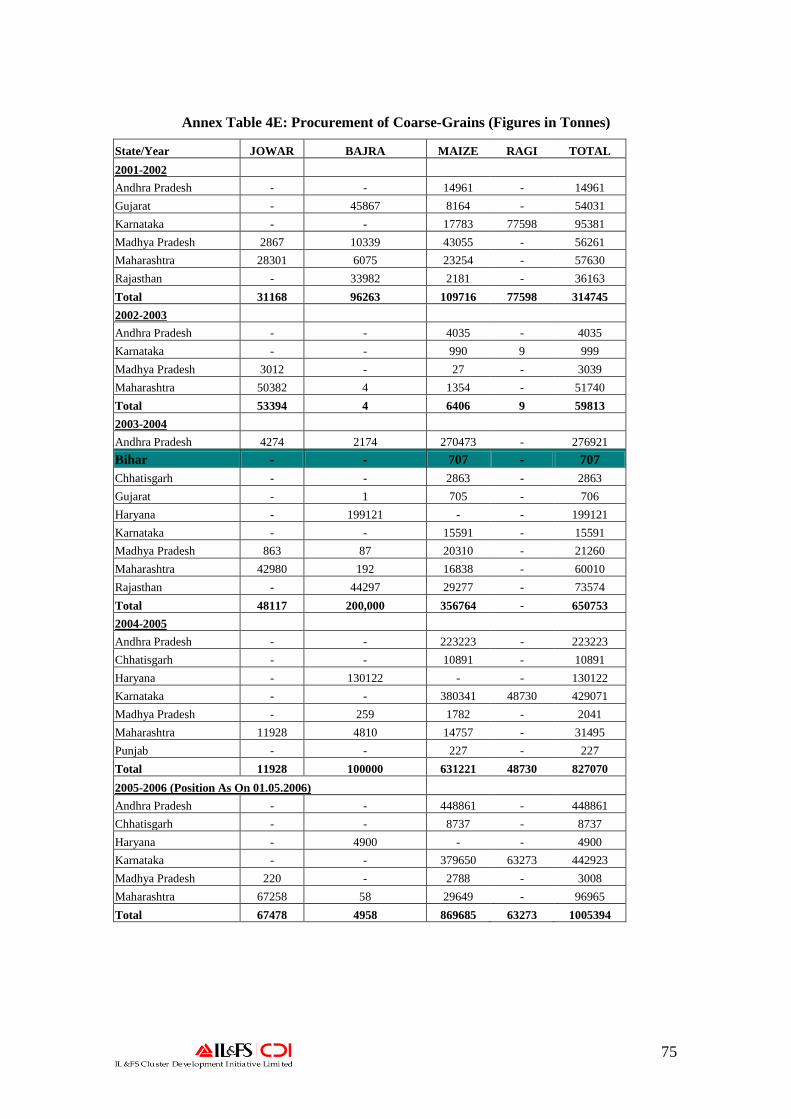

very rare (like once in five years) and that too in scanty volumes (707 MT in 2003-04)

which was just 0.2% of the total maize procurement in the country. It clearly indicates

poor procurement structure in the state (Refer to Annexure table).

In absence of any procurement by the state agencies, maize is sold in the open market

at the market prices (determined by the demand and supply forces). Prices of maize in

different grain markets of Bihar varies between Rs.500-Rs.700 per quintal, depending

upon the quality of grain (yellow flint grain is most preferred) and season from point of

view of grain trading (peak season – April to June; and lean season – December to

March). Minimum support prices act as a benchmark for open-market prices.

Table 4.8: Minimum Support Price for Maize (Rs./quintal)

2003-04 2004-05 2005-06 2006-07 2007-08

505 525 540 540 620

Source: Commission for Agricultural Costs and Pricing, Govt. of India

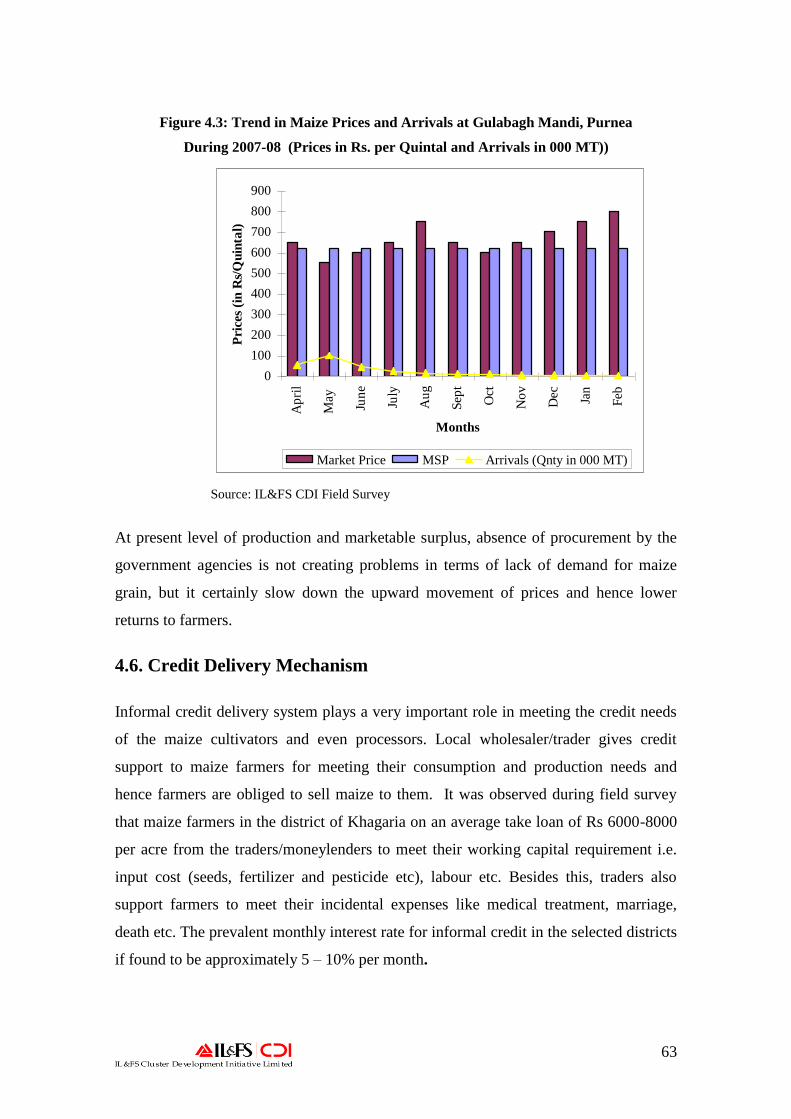

The prices in Gulab bag mandi during this year are as follows

63

Figure 4.3: Trend in Maize Prices and Arrivals at Gulabagh Mandi, Purnea

During 2007-08 (Prices in Rs. per Quintal and Arrivals in 000 MT))

0

100

200

300

400

500

600

700

800

900

Ap

ril

May

Jun

e

July

Au

g

Sep

t

Oct

No

v

Dec Jan

Feb

Months

Pri

ces

(in

Rs/

Qu

inta

l)

Market Price MSP Arrivals (Qnty in 000 MT)

Source: IL&FS CDI Field Survey

At present level of production and marketable surplus, absence of procurement by the

government agencies is not creating problems in terms of lack of demand for maize

grain, but it certainly slow down the upward movement of prices and hence lower

returns to farmers.

4.6. Credit Delivery Mechanism

Informal credit delivery system plays a very important role in meeting the credit needs

of the maize cultivators and even processors. Local wholesaler/trader gives credit

support to maize farmers for meeting their consumption and production needs and

hence farmers are obliged to sell maize to them. It was observed during field survey

that maize farmers in the district of Khagaria on an average take loan of Rs 6000-8000

per acre from the traders/moneylenders to meet their working capital requirement i.e.

input cost (seeds, fertilizer and pesticide etc), labour etc. Besides this, traders also

support farmers to meet their incidental expenses like medical treatment, marriage,

death etc. The prevalent monthly interest rate for informal credit in the selected districts

if found to be approximately 5 – 10% per month.

64

After harvesting, farmers sell maize to the moneylenders (wholesalers/traders) and loan

is settled against the value of the produce. Because of high interest rate and credit

linked product transactions, maize farmers are trapped in vicious cycle of debt and

poverty.

4.7. Marketing Channel and Infrastructure

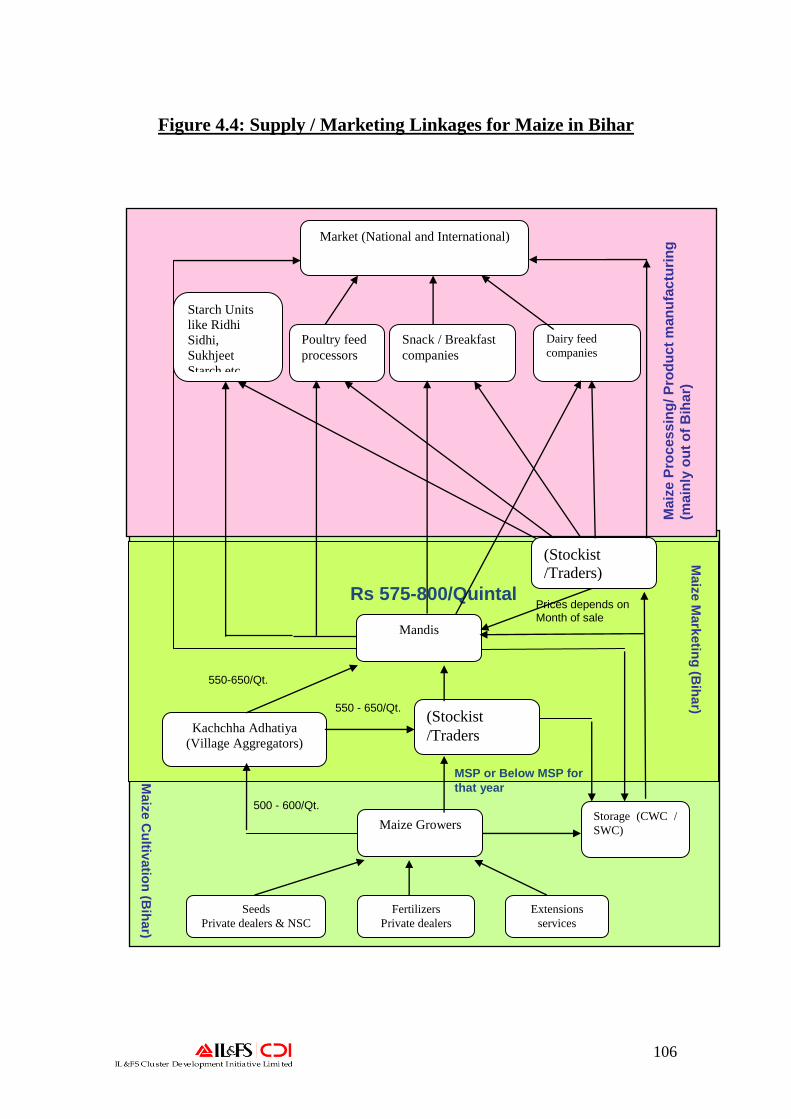

Agricultural marketing includes the movement of agricultural produce from farms

where it is produced to consumers or processors. There is free market for maize in the

state but marketing network and infrastructure remains a weak link. Maize sector is

highly unorganized with many intermediaries and farmers depend on the local village

aggregator/trader who plays an important role in procurement and marketing of the

produce. There are also some rural primary markets. Broadly two marketing channels

in maize were observed:

1. Farmer Wholesaler

2. Farmer Village Aggregator / trader Wholesaler

Feed/Starch industry Retailer Consumer

Typically, after harvest maize grains are brought to mandis (like Gulab Bag mandi in

Purnea, Khagaria etc.) by village aggregator (adhatiyas) for selling. Trade process at all

other places comprises of village level aggregation at multiple locations and then its

direct transportation to rake loading points like Khagaria etc. or is even directly sent to

customer‘s destination.

These mandis lack basic infrastructural facilities like platform for drying grains, pest-

free storage godowns, machines for weighing/sorting, public utilities, etc. Only Gulab

bag mandi in Purnea has facility to store maize to the tune of 12000-15000 MT. It has

about 15 godowns each having an average storage capacity for 750-1000 tonnes of

maize. These mandis also do not have mechanized grading except for Gulab Bag mandi

but even there the machines are not caliberated and moisture meters are found to be

faulty. There are no price display boards like it is being done in Nizamabad Mandi in

Andhra Pradesh.

65

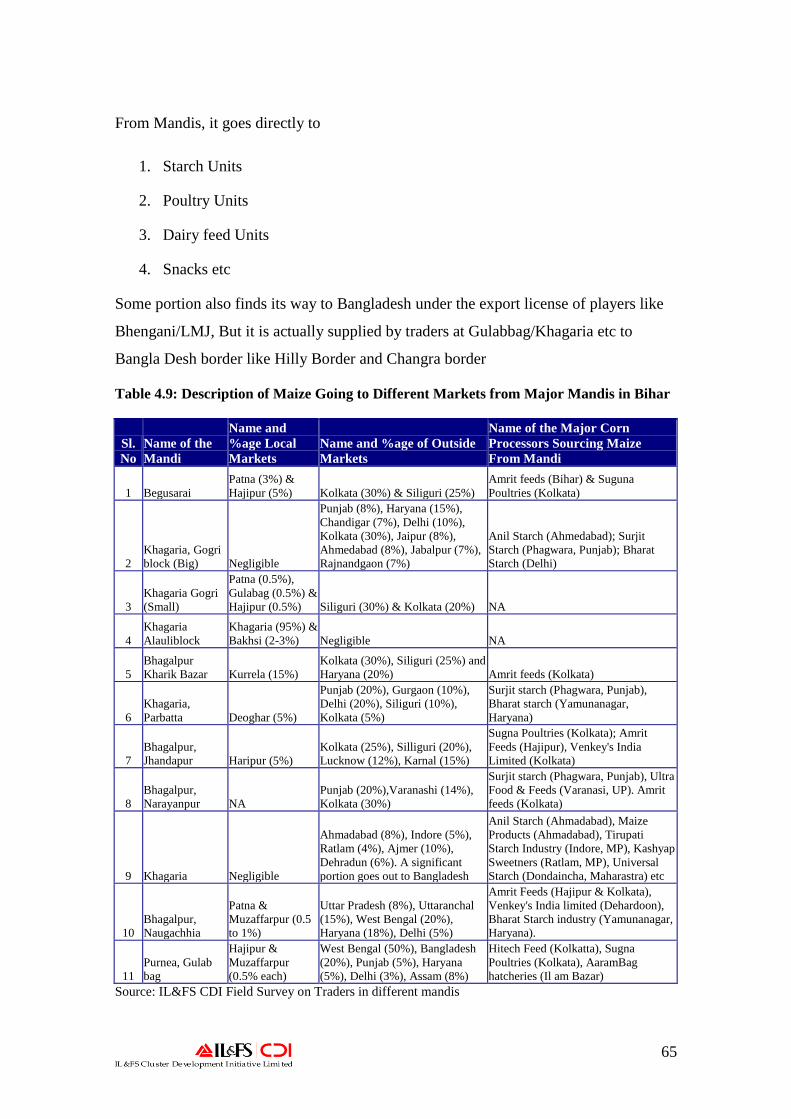

From Mandis, it goes directly to

1. Starch Units

2. Poultry Units

3. Dairy feed Units

4. Snacks etc

Some portion also finds its way to Bangladesh under the export license of players like

Bhengani/LMJ, But it is actually supplied by traders at Gulabbag/Khagaria etc to

Bangla Desh border like Hilly Border and Changra border

Table 4.9: Description of Maize Going to Different Markets from Major Mandis in Bihar

Sl.

No

Name of the

Mandi

Name and

%age Local

Markets

Name and %age of Outside

Markets

Name of the Major Corn

Processors Sourcing Maize

From Mandi

1 Begusarai

Patna (3%) &

Hajipur (5%) Kolkata (30%) & Siliguri (25%)

Amrit feeds (Bihar) & Suguna

Poultries (Kolkata)

2

Khagaria, Gogri

block (Big) Negligible

Punjab (8%), Haryana (15%),

Chandigar (7%), Delhi (10%),

Kolkata (30%), Jaipur (8%),

Ahmedabad (8%), Jabalpur (7%),

Rajnandgaon (7%)

Anil Starch (Ahmedabad); Surjit

Starch (Phagwara, Punjab); Bharat

Starch (Delhi)

3

Khagaria Gogri

(Small)

Patna (0.5%),

Gulabag (0.5%) &

Hajipur (0.5%) Siliguri (30%) & Kolkata (20%) NA

4

Khagaria

Alauliblock

Khagaria (95%) &

Bakhsi (2-3%) Negligible NA

5

Bhagalpur

Kharik Bazar Kurrela (15%)

Kolkata (30%), Siliguri (25%) and

Haryana (20%) Amrit feeds (Kolkata)

6

Khagaria,

Parbatta Deoghar (5%)

Punjab (20%), Gurgaon (10%),

Delhi (20%), Siliguri (10%),

Kolkata (5%)

Surjit starch (Phagwara, Punjab),

Bharat starch (Yamunanagar,

Haryana)

7

Bhagalpur,

Jhandapur Haripur (5%)

Kolkata (25%), Silliguri (20%),

Lucknow (12%), Karnal (15%)

Sugna Poultries (Kolkata); Amrit

Feeds (Hajipur), Venkey's India

Limited (Kolkata)

8

Bhagalpur,

Narayanpur NA

Punjab (20%),Varanashi (14%),

Kolkata (30%)

Surjit starch (Phagwara, Punjab), Ultra

Food & Feeds (Varanasi, UP). Amrit

feeds (Kolkata)

9 Khagaria Negligible

Ahmadabad (8%), Indore (5%),

Ratlam (4%), Ajmer (10%),

Dehradun (6%). A significant

portion goes out to Bangladesh

Anil Starch (Ahmadabad), Maize

Products (Ahmadabad), Tirupati

Starch Industry (Indore, MP), Kashyap

Sweetners (Ratlam, MP), Universal

Starch (Dondaincha, Maharastra) etc

10

Bhagalpur,

Naugachhia

Patna &

Muzaffarpur (0.5

to 1%)

Uttar Pradesh (8%), Uttaranchal

(15%), West Bengal (20%),

Haryana (18%), Delhi (5%)

Amrit Feeds (Hajipur & Kolkata),

Venkey's India limited (Dehardoon),

Bharat Starch industry (Yamunanagar,

Haryana).

11

Purnea, Gulab

bag

Hajipur &

Muzaffarpur

(0.5% each)

West Bengal (50%), Bangladesh

(20%), Punjab (5%), Haryana

(5%), Delhi (3%), Assam (8%)

Hitech Feed (Kolkatta), Sugna

Poultries (Kolkata), AaramBag

hatcheries (Il am Bazar)

Source: IL&FS CDI Field Survey on Traders in different mandis

66

Many of the maize growing areas trade through commodity exchanges like MCX and

NCDEX (in Mumbai) and NMC in Ahmedabad. There have been no delivery centers of

these bodies in Bihar. Recently Department of Agriculture (DoA) has allowed NCDEX

to launch the country's first spot exchange in Bihar in September-end 2007 with trading

in maize contracts.

Trade Channel and Value Chain

The following trade channel was observed in maize marketing in Bihar.

Village level aggregator — The village level aggregator operates in two ways

(depending upon his financial capability):

Trader

Commission Agent

As a trader, the aggregator buys the produce from the farmers and sells them to the

bigger traders operating at block level. The cost of transportation, packing and labour

charge is met by the aggregator. The aggregator in this case keeps a margin of around

3-5% over and above the cost incurred by him.

Whereas, as a commission agent he simply executes the order taken from the traders.

The entire cost up to the traders point, in this case, is borne by the farmer. The

commission agent in this case charges a commission up to 3% of the value of the

produce.

Commission agents at block level - In major market places such as Khagaria,

Maheshkhut, Mansi, etc commission agents are working for traders of Delhi, West

Bengal, Maharashtra on a commission of around 1.5%. These commission agents are

procuring maize from the village level aggregators and in turn supplying to the traders

operating out of major cities.

The overall trade and marketing channel is depicted in the following figure. The

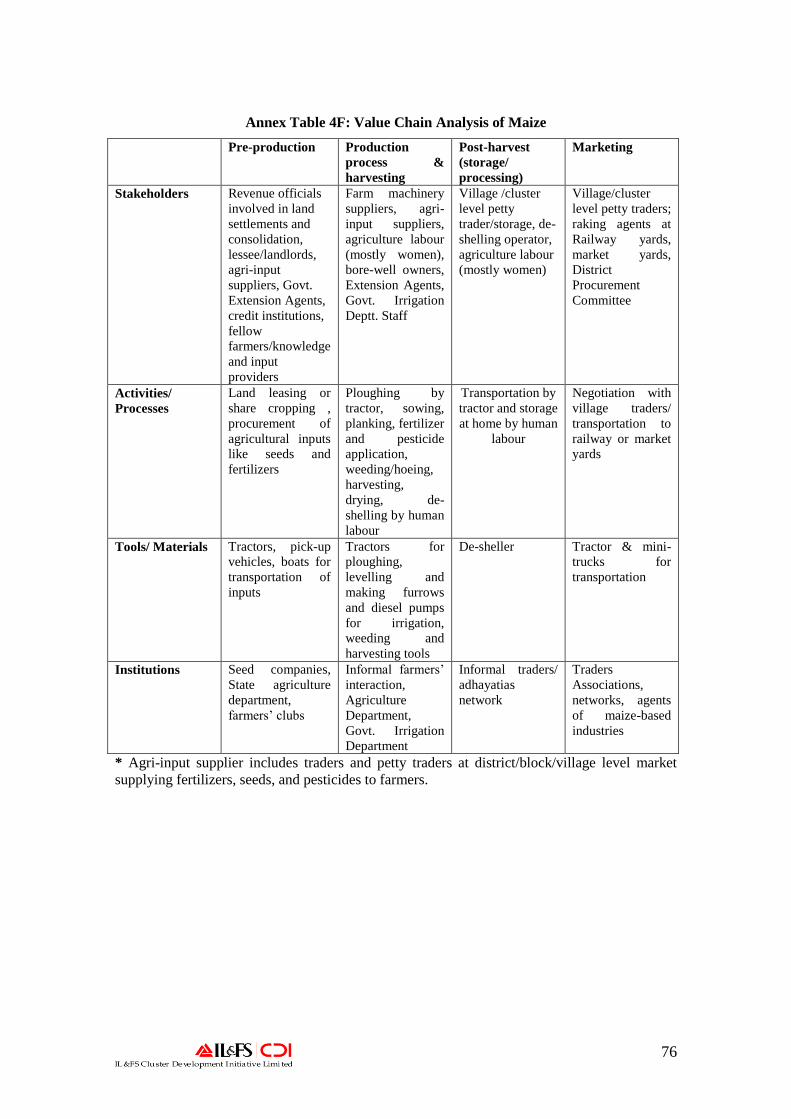

diagram of the value chain of maize in Bihar explains the way in which the maize

growers, processors and other stakeholders are linked to each other:

67

Figure 4.4: Supply / Marketing Linkages for Maize in Bihar

Plz see the attached file

68

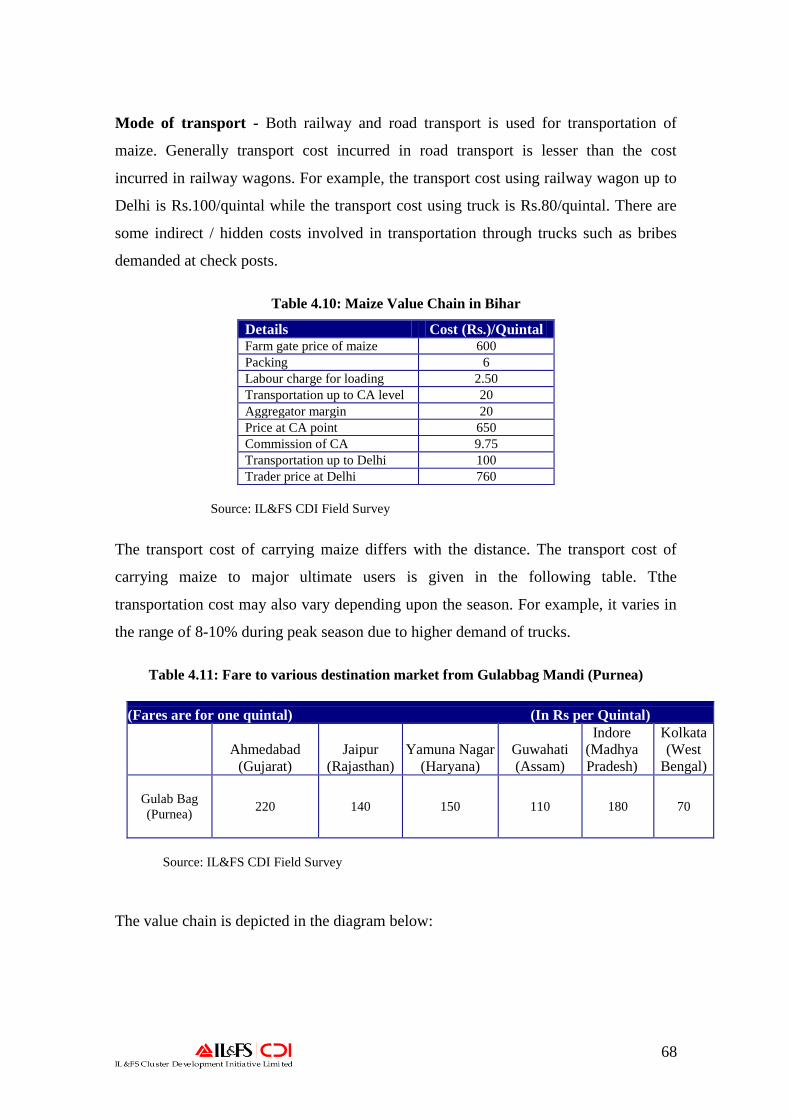

Mode of transport - Both railway and road transport is used for transportation of

maize. Generally transport cost incurred in road transport is lesser than the cost

incurred in railway wagons. For example, the transport cost using railway wagon up to

Delhi is Rs.100/quintal while the transport cost using truck is Rs.80/quintal. There are

some indirect / hidden costs involved in transportation through trucks such as bribes

demanded at check posts.

Table 4.10: Maize Value Chain in Bihar

Details Cost (Rs.)/Quintal Farm gate price of maize 600

Packing 6

Labour charge for loading 2.50

Transportation up to CA level 20

Aggregator margin 20

Price at CA point 650

Commission of CA 9.75

Transportation up to Delhi 100

Trader price at Delhi 760

Source: IL&FS CDI Field Survey

The transport cost of carrying maize differs with the distance. The transport cost of

carrying maize to major ultimate users is given in the following table. Tthe

transportation cost may also vary depending upon the season. For example, it varies in

the range of 8-10% during peak season due to higher demand of trucks.

Table 4.11: Fare to various destination market from Gulabbag Mandi (Purnea)

(Fares are for one quintal) (In Rs per Quintal)

Ahmedabad

(Gujarat)

Jaipur

(Rajasthan)

Yamuna Nagar

(Haryana)

Guwahati

(Assam)

Indore

(Madhya

Pradesh)

Kolkata

(West

Bengal)

Gulab Bag

(Purnea) 220 140 150 110 180 70

Source: IL&FS CDI Field Survey

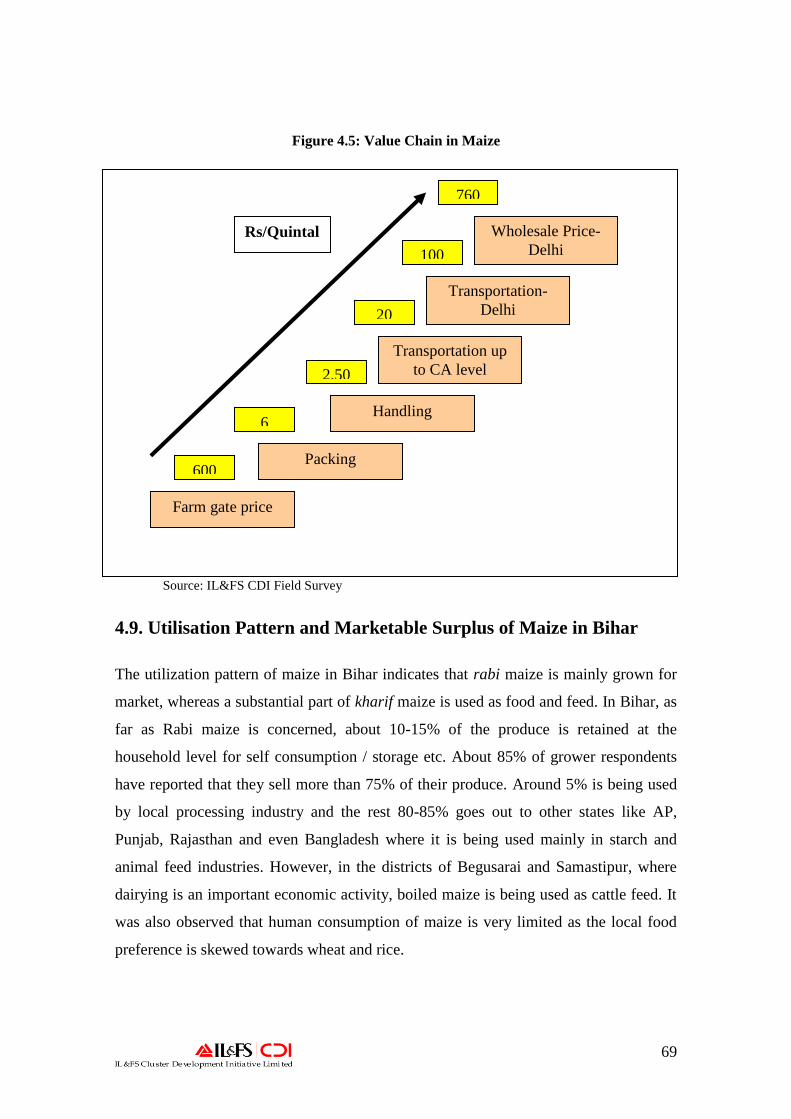

The value chain is depicted in the diagram below:

69

Figure 4.5: Value Chain in Maize

Source: IL&FS CDI Field Survey

4.9. Utilisation Pattern and Marketable Surplus of Maize in Bihar

The utilization pattern of maize in Bihar indicates that rabi maize is mainly grown for

market, whereas a substantial part of kharif maize is used as food and feed. In Bihar, as

far as Rabi maize is concerned, about 10-15% of the produce is retained at the

household level for self consumption / storage etc. About 85% of grower respondents

have reported that they sell more than 75% of their produce. Around 5% is being used

by local processing industry and the rest 80-85% goes out to other states like AP,

Punjab, Rajasthan and even Bangladesh where it is being used mainly in starch and

animal feed industries. However, in the districts of Begusarai and Samastipur, where

dairying is an important economic activity, boiled maize is being used as cattle feed. It

was also observed that human consumption of maize is very limited as the local food

preference is skewed towards wheat and rice.

Farm gate price

Packing

Handling

Transportation up

to CA level

Transportation-

Delhi

Wholesale Price-

Delhi