century commercial bank limited ii disclosure... · €€€€€€€€€€€ risk weighted...

TRANSCRIPT

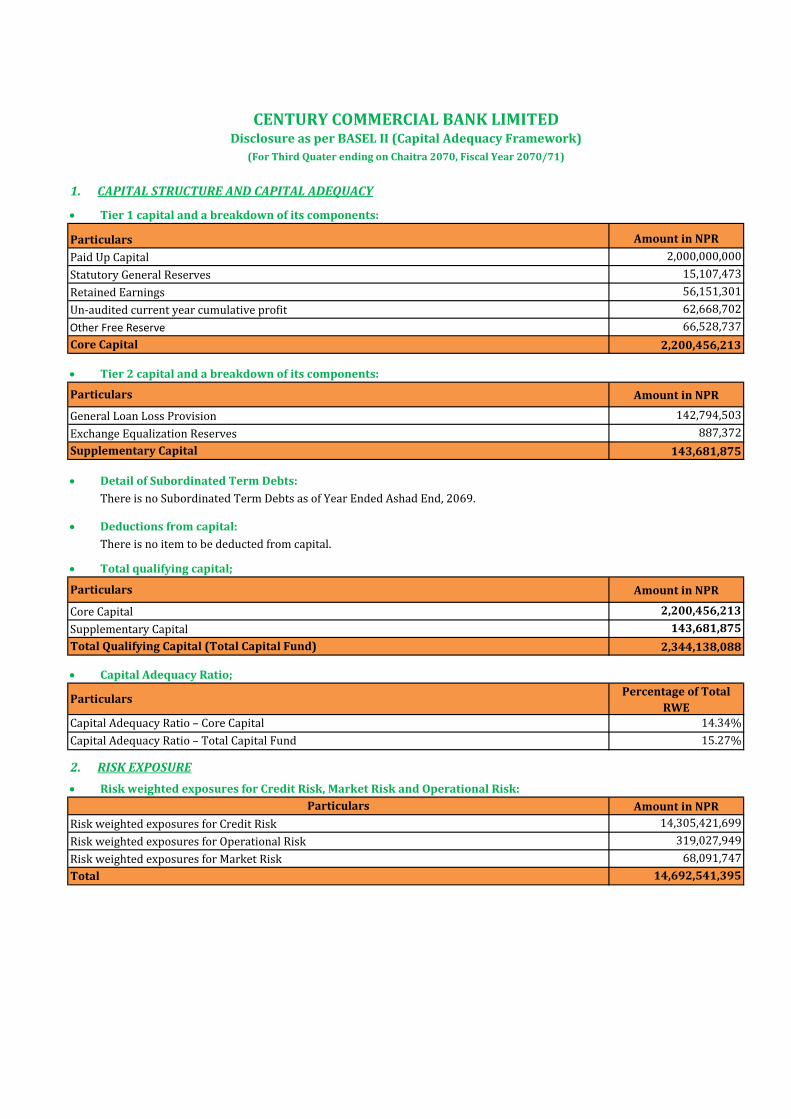

Amount in NPR

2,000,000,000

15,107,473

56,151,301

62,668,702

66,528,737

2,200,456,213

Amount in NPR

142,794,503

887,372

143,681,875

Amount in NPR

2,200,456,213

143,681,875

2,344,138,088

Percentage of Total

RWE

14.34%

15.27%

Amount in NPR

14,305,421,699

319,027,949

68,091,747

14,692,541,395

2. RISK EXPOSURE

Risk weighted exposures for Credit Risk, Market Risk and Operational Risk:

Particulars

Risk weighted exposures for Credit Risk

Risk weighted exposures for Operational Risk

Risk weighted exposures for Market Risk

Total

Capital Adequacy Ratio – Total Capital Fund

There is no Subordinated Term Debts as of Year Ended Ashad End, 2069.

Deductions from capital:

There is no item to be deducted from capital.

Total qualifying capital;

Particulars

Core Capital

Supplementary Capital

Total Qualifying Capital (Total Capital Fund)

Capital Adequacy Ratio;

Particulars

Capital Adequacy Ratio – Core Capital

Detail of Subordinated Term Debts:

Paid Up Capital

Statutory General Reserves

Retained Earnings

Un-audited current year cumulative profit

Other Free Reserve

Core Capital

Tier 2 capital and a breakdown of its components:

Particulars

General Loan Loss Provision

Exchange Equalization Reserves

Supplementary Capital

Particulars

CENTURY COMMERCIAL BANK LIMITEDDisclosure as per BASEL II (Capital Adequacy Framework)

(For Third Quater ending on Chaitra 2070, Fiscal Year 2070/71)

1. CAPITAL STRUCTURE AND CAPITAL ADEQUACY

Tier 1 capital and a breakdown of its components:

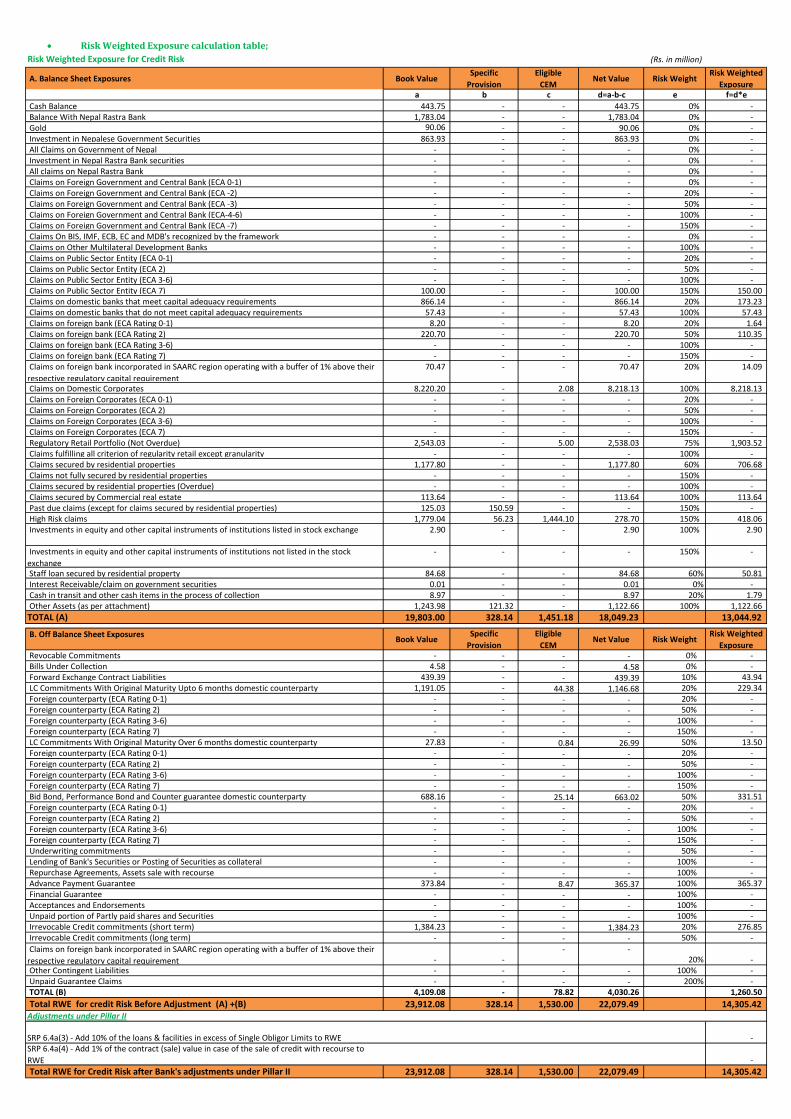

Risk Weighted Exposure calculation table;

Risk Weighted Exposure for Credit Risk (Rs. in million)

A. Balance Sheet Exposures Book ValueSpecific

Provision

Eligible

CEMNet Value Risk Weight

Risk Weighted

Exposurea b c d=a-b-c e f=d*e

Cash Balance 443.75 - - 443.75 0% - Balance With Nepal Rastra Bank 1,783.04 - - 1,783.04 0% - Gold 90.06 - - 90.06 0% - Investment in Nepalese Government Securities 863.93 - - 863.93 0% - All Claims on Government of Nepal - - - - 0% - Investment in Nepal Rastra Bank securities - - - - 0% - All claims on Nepal Rastra Bank - - - - 0% - Claims on Foreign Government and Central Bank (ECA 0-1) - - - - 0% - Claims on Foreign Government and Central Bank (ECA -2) - - - - 20% - Claims on Foreign Government and Central Bank (ECA -3) - - - - 50% - Claims on Foreign Government and Central Bank (ECA-4-6) - - - - 100% - Claims on Foreign Government and Central Bank (ECA -7) - - - - 150% - Claims On BIS, IMF, ECB, EC and MDB's recognized by the framework - - - - 0% - Claims on Other Multilateral Development Banks - - - - 100% - Claims on Public Sector Entity (ECA 0-1) - - - - 20% - Claims on Public Sector Entity (ECA 2) - - - - 50% - Claims on Public Sector Entity (ECA 3-6) - - - - 100% - Claims on Public Sector Entity (ECA 7) 100.00 - - 100.00 150% 150.00 Claims on domestic banks that meet capital adequacy requirements 866.14 - - 866.14 20% 173.23 Claims on domestic banks that do not meet capital adequacy requirements 57.43 - - 57.43 100% 57.43 Claims on foreign bank (ECA Rating 0-1) 8.20 - - 8.20 20% 1.64 Claims on foreign bank (ECA Rating 2) 220.70 - - 220.70 50% 110.35 Claims on foreign bank (ECA Rating 3-6) - - - - 100% - Claims on foreign bank (ECA Rating 7) - - - - 150% - Claims on foreign bank incorporated in SAARC region operating with a buffer of 1% above their

respective regulatory capital requirement

70.47 - - 70.47 20% 14.09

Claims on Domestic Corporates 8,220.20 - 2.08 8,218.13 100% 8,218.13 Claims on Foreign Corporates (ECA 0-1) - - - - 20% - Claims on Foreign Corporates (ECA 2) - - - - 50% - Claims on Foreign Corporates (ECA 3-6) - - - - 100% - Claims on Foreign Corporates (ECA 7) - - - - 150% - Regulatory Retail Portfolio (Not Overdue) 2,543.03 - 5.00 2,538.03 75% 1,903.52 Claims fulfilling all criterion of regularity retail except granularity - - - - 100% - Claims secured by residential properties 1,177.80 - - 1,177.80 60% 706.68 Claims not fully secured by residential properties - - - - 150% - Claims secured by residential properties (Overdue) - - - - 100% - Claims secured by Commercial real estate 113.64 - - 113.64 100% 113.64 Past due claims (except for claims secured by residential properties) 125.03 150.59 - - 150% - High Risk claims 1,779.04 56.23 1,444.10 278.70 150% 418.06 Investments in equity and other capital instruments of institutions listed in stock exchange 2.90 - - 2.90 100% 2.90

Investments in equity and other capital instruments of institutions not listed in the stock

exchange

- - - - 150% -

Staff loan secured by residential property 84.68 - - 84.68 60% 50.81 Interest Receivable/claim on government securities 0.01 - - 0.01 0% - Cash in transit and other cash items in the process of collection 8.97 - - 8.97 20% 1.79 Other Assets (as per attachment) 1,243.98 121.32 - 1,122.66 100% 1,122.66

TOTAL (A) 19,803.00 328.14 1,451.18 18,049.23 13,044.92

B. Off Balance Sheet Exposures Book Value

Specific

Provision

Eligible

CEMNet Value Risk Weight

Risk Weighted

Exposure Revocable Commitments - - - - 0% - Bills Under Collection 4.58 - - 4.58 0% - Forward Exchange Contract Liabilities 439.39 - - 439.39 10% 43.94 LC Commitments With Original Maturity Upto 6 months domestic counterparty 1,191.05 - 44.38 1,146.68 20% 229.34 Foreign counterparty (ECA Rating 0-1) - - - - 20% - Foreign counterparty (ECA Rating 2) - - - - 50% - Foreign counterparty (ECA Rating 3-6) - - - - 100% - Foreign counterparty (ECA Rating 7) - - - - 150% - LC Commitments With Original Maturity Over 6 months domestic counterparty 27.83 - 0.84 26.99 50% 13.50 Foreign counterparty (ECA Rating 0-1) - - - - 20% - Foreign counterparty (ECA Rating 2) - - - - 50% - Foreign counterparty (ECA Rating 3-6) - - - - 100% - Foreign counterparty (ECA Rating 7) - - - - 150% - Bid Bond, Performance Bond and Counter guarantee domestic counterparty 688.16 - 25.14 663.02 50% 331.51 Foreign counterparty (ECA Rating 0-1) - - - - 20% - Foreign counterparty (ECA Rating 2) - - - - 50% - Foreign counterparty (ECA Rating 3-6) - - - - 100% - Foreign counterparty (ECA Rating 7) - - - - 150% - Underwriting commitments - - - - 50% - Lending of Bank's Securities or Posting of Securities as collateral - - - - 100% - Repurchase Agreements, Assets sale with recourse - - - - 100% - Advance Payment Guarantee 373.84 - 8.47 365.37 100% 365.37 Financial Guarantee - - - - 100% - Acceptances and Endorsements - - - - 100% - Unpaid portion of Partly paid shares and Securities - - - - 100% - Irrevocable Credit commitments (short term) 1,384.23 - - 1,384.23 20% 276.85 Irrevocable Credit commitments (long term) - - - - 50% -

Claims on foreign bank incorporated in SAARC region operating with a buffer of 1% above their

respective regulatory capital requirement - - - -

20% - Other Contingent Liabilities - - - - 100% - Unpaid Guarantee Claims - - - - 200% - TOTAL (B) 4,109.08 - 78.82 4,030.26 1,260.50

Total RWE for credit Risk Before Adjustment (A) +(B) 23,912.08 328.14 1,530.00 22,079.49 14,305.42 Adjustments under Pillar II

SRP 6.4a(3) - Add 10% of the loans & facilities in excess of Single Obligor Limits to RWE - SRP 6.4a(4) - Add 1% of the contract (sale) value in case of the sale of credit with recourse to

RWE -

Total RWE for Credit Risk after Bank's adjustments under Pillar II 23,912.08 328.14 1,530.00 22,079.49 14,305.42

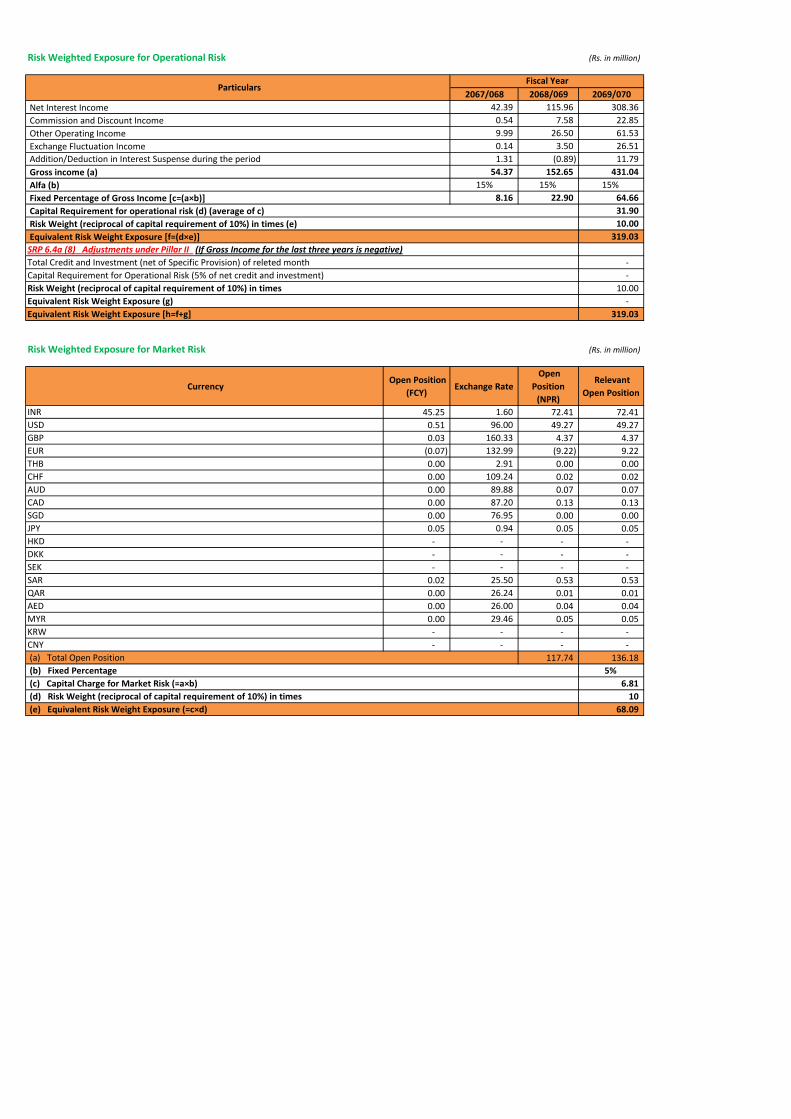

Risk Weighted Exposure for Operational Risk (Rs. in million)

2067/068 2068/069 2069/070

Net Interest Income 42.39 115.96 308.36

Commission and Discount Income 0.54 7.58 22.85

Other Operating Income 9.99 26.50 61.53

Exchange Fluctuation Income 0.14 3.50 26.51

Addition/Deduction in Interest Suspense during the period 1.31 (0.89) 11.79

Gross income (a) 54.37 152.65 431.04

Alfa (b) 15% 15% 15%

Fixed Percentage of Gross Income [c=(a×b)] 8.16 22.90 64.66

Capital Requirement for operational risk (d) (average of c) 31.90

Risk Weight (reciprocal of capital requirement of 10%) in times (e) 10.00

Equivalent Risk Weight Exposure [f=(d×e)] 319.03

SRP 6.4a (8) Adjustments under Pillar II (If Gross Income for the last three years is negative)

Total Credit and Investment (net of Specific Provision) of releted month -

Capital Requirement for Operational Risk (5% of net credit and investment) -

Risk Weight (reciprocal of capital requirement of 10%) in times 10.00

Equivalent Risk Weight Exposure (g) -

Equivalent Risk Weight Exposure [h=f+g] 319.03

Risk Weighted Exposure for Market Risk (Rs. in million)

Currency Open Position

(FCY) Exchange Rate

Open

Position

(NPR)

Relevant

Open Position

INR 45.25 1.60 72.41 72.41

USD 0.51 96.00 49.27 49.27

GBP 0.03 160.33 4.37 4.37

EUR (0.07) 132.99 (9.22) 9.22

THB 0.00 2.91 0.00 0.00

CHF 0.00 109.24 0.02 0.02

AUD 0.00 89.88 0.07 0.07

CAD 0.00 87.20 0.13 0.13

SGD 0.00 76.95 0.00 0.00

JPY 0.05 0.94 0.05 0.05

HKD - - - -

DKK - - - -

SEK - - - -

SAR 0.02 25.50 0.53 0.53

QAR 0.00 26.24 0.01 0.01

AED 0.00 26.00 0.04 0.04

MYR 0.00 29.46 0.05 0.05

KRW - - - -

CNY - - - -

(a) Total Open Position 117.74 136.18

(b) Fixed Percentage 5%

(c) Capital Charge for Market Risk (=a×b) 6.81

(d) Risk Weight (reciprocal of capital requirement of 10%) in times 10

(e) Equivalent Risk Weight Exposure (=c×d) 68.09

Particulars Fiscal Year

S.N. Claims Categories Risk Weighted Amount

1 Claims on govt. and central Bank -

2 Claims on other official entities 150,000,000

3 Claims on Banks 356,744,335

4 Claims on corporate and securities firm 8,218,125,319

5 Claims on regulatory retail portfolio 1,903,520,410

6 Claim secured by residential properties 706,677,381

7 Claims secured by commercial real state 113,637,538

8 Past due Claims -

9 High risk claims 418,056,224

10 Other Assets 1,178,163,368

11 Off Balance sheet Items 1,260,497,125

Total 14,305,421,699

Total Risk Weighted Exposure calculation table;

Amount in NPR

14,305,421,699

319,027,949

68,091,747

440,776,242

215,500,000

15,348,817,637

2,344,138,088

15.27%

Nil

* Gross 29,166,746

* Net 21,875,059

* Gross 1,000,000

* Net 500,000

* Gross 65,518,128

* Net 9,285,309

0.67%

0.22%

Last Quarter This Quarter Increase/ (Decrease)

64,302,147 29,166,746 (35,135,401)

17,430,975 1,000,000 (16,430,975)

30,256,791 65,518,128 35,261,337

Nil

Net NPA to Net Advances

Movement of Non Performing Assets

NPA Categories

Sub-Standard

Doubtful

Bad

Write off of Loans and Interest Suspense

Movements in Loan Loss Provisions and Interest Suspense:

Gross NPA to Gross Advances

Add : 3% of Total RWE due insufficient risk management system (as prescribed by NRB)

Add : 5% of Gross Income for Operational Risk (as prescribed by NRB)

Total Risk Weighted Exposure

Total Capital Fund

Total Capital to Total Risk Weighted Exposures

Amount of Non Performing Assets (NPAs) [both Gross and Net]:

Restructure Loan/Reschedule Loan

Substandard Loan

Doubtful Loan

Bad Loan

Non Performing Assets (NPAs) ratios

Risk weighted exposures for Market Risk

Risk Weighted Exposures under each of 11 categories of Credit Risk:

Particulars

Risk weighted exposures for Credit Risk

Risk weighted exposures for Operational Risk

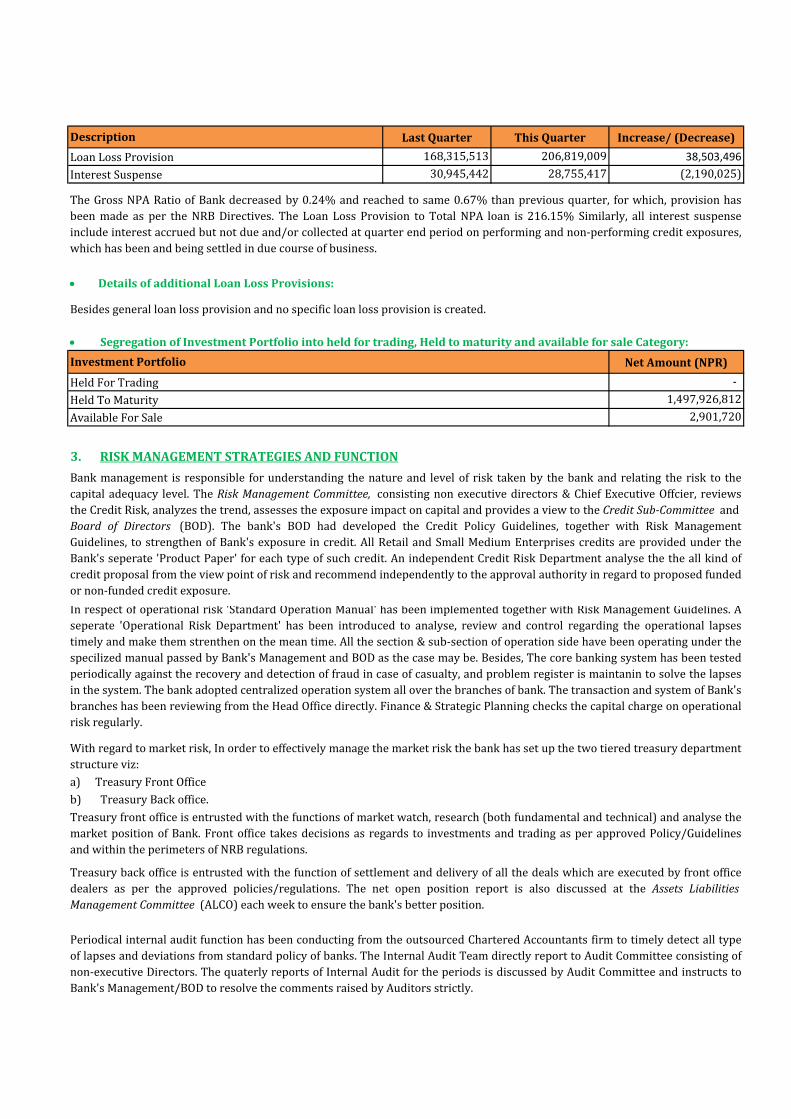

Last Quarter This Quarter Increase/ (Decrease)

168,315,513 206,819,009 38,503,496

30,945,442 28,755,417 (2,190,025)

Net Amount (NPR)

-

1,497,926,812

2,901,720

b) Treasury Back office.

Treasury front office is entrusted with the functions of market watch, research (both fundamental and technical) and analyse the

market position of Bank. Front office takes decisions as regards to investments and trading as per approved Policy/Guidelines

and within the perimeters of NRB regulations.

Treasury back office is entrusted with the function of settlement and delivery of all the deals which are executed by front office

dealers as per the approved policies/regulations. The net open position report is also discussed at the Assets Liabilities

Management Committee (ALCO) each week to ensure the bank's better position.

Besides general loan loss provision and no specific loan loss provision is created.

Periodical internal audit function has been conducting from the outsourced Chartered Accountants firm to timely detect all type

of lapses and deviations from standard policy of banks. The Internal Audit Team directly report to Audit Committee consisting of

non-executive Directors. The quaterly reports of Internal Audit for the periods is discussed by Audit Committee and instructs to

Bank's Management/BOD to resolve the comments raised by Auditors strictly.

3. RISK MANAGEMENT STRATEGIES AND FUNCTION

Bank management is responsible for understanding the nature and level of risk taken by the bank and relating the risk to the

capital adequacy level. The Risk Management Committee, consisting non executive directors & Chief Executive Offcier, reviews

the Credit Risk, analyzes the trend, assesses the exposure impact on capital and provides a view to the Credit Sub-Committee and

Board of Directors (BOD). The bank's BOD had developed the Credit Policy Guidelines, together with Risk Management

Guidelines, to strengthen of Bank's exposure in credit. All Retail and Small Medium Enterprises credits are provided under the

Bank's seperate 'Product Paper' for each type of such credit. An independent Credit Risk Department analyse the the all kind of

credit proposal from the view point of risk and recommend independently to the approval authority in regard to proposed funded

or non-funded credit exposure.

In respect of operational risk 'Standard Operation Manual' has been implemented together with Risk Management Guidelines. A

seperate 'Operational Risk Department' has been introduced to analyse, review and control regarding the operational lapses

timely and make them strenthen on the mean time. All the section & sub-section of operation side have been operating under the

specilized manual passed by Bank's Management and BOD as the case may be. Besides, The core banking system has been tested

periodically against the recovery and detection of fraud in case of casualty, and problem register is maintanin to solve the lapses

in the system. The bank adopted centralized operation system all over the branches of bank. The transaction and system of Bank's

branches has been reviewing from the Head Office directly. Finance & Strategic Planning checks the capital charge on operational

risk regularly.

With regard to market risk, In order to effectively manage the market risk the bank has set up the two tiered treasury department

structure viz:

a) Treasury Front Office

Available For Sale

Details of additional Loan Loss Provisions:

Segregation of Investment Portfolio into held for trading, Held to maturity and available for sale Category:

Investment Portfolio

Held For Trading

Held To Maturity

The Gross NPA Ratio of Bank decreased by 0.24% and reached to same 0.67% than previous quarter, for which, provision has

been made as per the NRB Directives. The Loan Loss Provision to Total NPA loan is 216.15% Similarly, all interest suspense

include interest accrued but not due and/or collected at quarter end period on performing and non-performing credit exposures,

which has been and being settled in due course of business.

Description

Loan Loss Provision

Interest Suspense