centre for new and emerging markets number 30 manuela...

TRANSCRIPT

CENTRE FOR NEW AND EMERGING MARKETS

Discussion Paper Series Number 30

Ownership, Competition and Enterprise Performance

Saul Estrin , London Business School

Manuela Angelucci, University College London

March 2003

Contact details: Anna M Malaczynska Tel: +44 (0)20 7706 6964 Fax: +44 (0)20 7724 8060 www.london.edu/cnem © London Business School, 2003

Non - Technical Summary

In this paper, we use the data from a large enterprise-level survey of Russia to explore the

impact of private ownership and competition on the performance of firms. The transition

process at the enterprise level entailed two major policy initiatives – the creation of a private

sector via privatisation; and the establishment of markets, through price and trade

liberalisation, as the main mechanism for resource allocation. The latter implies an increase

in the competitive pressure faced by incumbent firms. Our aim in this paper is to explore

whether and in what ways enterprise performance was influenced in Russia by privatisation

and by the increase of competition in the marketplace.

The study uses our survey questionnaire of 437 Russian industrial firms in 2000 to develop

measures of ownership, competition and performance. In the transition context, the

traditional focus on state versus private ownership from the western literature has to be

broadened to take account of widespread insider ownership. We are able to compare majority

ownership stakes in 2000 with those at the time of privatisation, in order to follow the

evolution of ownership structure. We find that there have been important changes in

ownership; there has been a major decline in insider and state ownership and an increase in

outsider ownership. Within the group of insider ownership, managers have been increasing

their stake at the expense of workers.

Our measures of competition are perceptual, being the response by senior managers to

questions about the number of significant competitors faced in this marketplace. We define

domestic competition as being high if there are more than five competitors, medium if the

number is between 3 and 5 and low in the case of monopoly and duopoly. The proportions of

firms in the three categories are around 63%, 28% and 10% respectively, which suggests most

Russian firms feel themselves to have a significant degree of competition in their home

market. However, imports are found to be an important source of competition by only 37%

of firms.

Our empirical analysis explores the relationship between ownership, competition and various

measures of enterprise performance. We find clear differences between private and state

owned firms in terms of their restructuring activity, though not between insider and outsider

owned firms. Ownership is not found to influence more traditional measures of economic

performance such as the profitability or productivity however. This is consistent with other

2

surveys of Russian enterprises, and suggests that it is, as yet, still too early to judge the impact

of privatisation in Russia, perhaps because of measurement error or because privatisation took

place before the other relevant capital market institutions were properly developed.

We were also unable to identify any impact of competitive pressures on enterprise behaviour

using financial or economic measures of performance. This is consistent with the results

concerning ownership, highlights issues concerning the quality of Russian quantitative data.

Such data were severely affected at the time the sample was taken by the consequences of the

1998 crash. However, in almost all the measures of managerial activity, including deep

restructuring, defensive restructuring and investment intentions, we identify a positive impact

from the pressures of domestic competition, and sometimes also from import competition.

The findings therefore do emphasise the importance of price and trade liberalisation for the

transition process.

3

ABSTRACT

The literature suggests that competitive forces should be an important element in improving

enterprise performance in transition economies, especially when combined with private

ownership. However, empirical evidence on these issues for Russia has as yet not been

convincing. Our findings are consistent with the literature in being unable to identify clear

differences in performance between insider and outsider owned firms. However, we do find

evidence that competitive pressures influence qualitative indicators of managerial activity,

including deep restructuring and investment intentions.

JEL Classification Numbers: D21, L10, G30

Keywords: corporate governance, competition, firm performance

4

1. Introduction

In this paper, we use the data from our Russia survey to explore the impact of competition on

the performance of firms. The transition process at the enterprise level entailed two major

policy initiatives – the creation of a private sector via privatisation as well as de novo private

enterprise entry and growth; and the establishment through price and trade liberalisation of

markets as the main mechanism for resource allocation (see e.g. World Bank (1996, 2002)).

The latter implies an increase in the competitive pressure faced by incumbent firms and this

may affect enterprise behaviour. Our aim in this paper is to explore whether and in what

ways enterprise performance was influenced in Russia by this increase of competition in the

marketplace, and to identify if other factors acted to consolidate this impact.

There is a growing Western literature, at both a theoretical and empirical level, about the

ways that competition might enhance company performance, (see e.g. Nalebuff and Stiglitz

(1983), Aghion, Harris and Vickers (1997), Nickell (1996), Nickell, Nicolitsas, Dryden

(1997)). The evidence suggests that, at least in the UK, competition has acted to enhance

total factor productivity, though in the context of effective financial markets and shareholder

control. The issue is more complicated in transition countries because, for example,

“restructuring” may be a more important indicator of enterprise performance in the short run

than factor productivity (see Roland (2000), Linz and Krueger (1998)). Moreover, standard

models about the impact of competition assume that the enterprise sector is privately owned

and that budget constraints on firms are hard, including an effective bankruptcy threat. Such

conditions have not often been satisfied in any transition economy until recently (see e.g.

EBRD (2002)) and as the other papers in this issue indicate, certainly did not pertain in Russia

at the time of our survey. Nonetheless, considerable empirical work has been undertaken on

the issue for transition economies (see Djankov and Murrell (2002)), and this suggests that

“product market competition has been a major force behind improvement in enterprise

productivity in transition economies” (Djankov and Murrell (2002)). But clear differences

have emerged concerning how competition affects firms in Central and Eastern Europe and

the CIS; in the latter, import competition is rarely significant but domestic competition is

sometimes found to have a significant effect on company performance. In Central and

Eastern Europe, import competition has been crucial.

Our approach in this paper is more descriptive than in some of the previous studies. Our

survey does not contain information on market structure and its changes. Moreover, the

Russian market is at best only partially integrated, so that one would need to account for

regional as well as sectoral factors in the measurement of competition (see Brown and Earle

5

(2001)), and our dataset, with 11 oblasts and 6 (2 digit) sectors does not contain sufficient

observations for such an approach. However, the data set is rich in information about a

variety of performance measures, and has very interesting perceptual indicators of intensity of

competition from domestic firms and from abroad. Our approach is therefore to explore

empirically the relationship between a variety of performance measures and the “intensity” of

competition, taking account of ownership where possible.

The paper is organised as follows. In the following section we briefly summarise hypotheses

and describe the nature of data with respect to ownership, competition and performance. The

relationship between these variables is presented in the third section, and conclusions drawn

in the fourth.

2. Enterprise Performance and Competition in Transition

It is almost an article of faith for economists that competition is a force for “good”; but this

conclusion derives from welfare economics, and refers primarily to the impact of competition

on the allocation of resources. The effects of competition on the performance of individual

firms are less clear-cut; a Schumpeterian perspective suggests that monopoly power might

enhance innovation and growth, and Chamberlin’s model of monopolistic competition

characterises inefficiency via “excessive” competitive entry. Only quite recently have the

issues for individual enterprise performance begun to be systematically evaluated (see

Holmstrom (1982), Hart (1983), Nalebuff and Stiglitz (1983)). It is widely believed that

competition acts to create a downward pressure on company costs and provides incentives for

efficient organisation, while monopoly is associated with organisational slack and an “easy

life”. Competition is seen as a means to reduce capital-inefficiency within the firm (see

Djankov and Murrell (2002)). Holmstrom (1982), for example, shows that, because of the

greater opportunities for comparison of performance, incentive schemes to motivate

managerial effort will generate sharper incentives, the more players are involved.

Competition makes the monitoring of managerial performance more effective because

unobserved performance or productivity schemes are likely to be correlated across firms

operating in the same industry, and hence managerial effort will rise as the number of firms in

the industry increases.

These arguments seem to have particular force in the transition context. It is arguable that

failure to align owners’ and managers’ incentives and the consequences for company

performance was one of the critical failings of central planning (see Ellman (1989)), and this

6

explains the crucial role of privatisation (handing over monitoring and evaluation of

managerial effort to capital markets) and of price and trade liberalisation (by creating

competitive pressure on firms) during transition (see Blanchard et al (1991)). It is therefore

very important to evaluate whether competition has had the expected effect on managerial

effort, and therefore company performance.

However, the economic and institutional environment of many transition countries is not the

same as that for which the hypotheses discussed above were derived. For example, many

firms remained state-owned (see Bennett, Estrin and Maw (2001)) and it is not clear that

enhanced competition is sufficient to engender improved managerial effort in state-owned

firms. For this reason, Earle and Estrin (1998) explore competition and ownership effects

simultaneously; a method which we repeat in this paper. It is also unclear whether pressures

on managerial incentives from market competition can operate effectively in an environment

of soft budget constraints (see Schaffer (1998)). This implies that, if we fail to isolate any

impact of competition on enterprise performance, one interpretation might be the way

managerial incentives are distorted by the behaviour of the financial system (see Commander,

Dolinskaya and Mumssen (2002)).

3. Measures of Ownership, Competition and Performance

Our study therefore relies on measures of ownership, competition and performance.

Commencing with the former, one would normally seek to distinguish primarily between state

and private ownership (see e.g.Vickers and Yarrow (1988)). There exists an enormous

theoretical and empirical literature (see e.g. Megginson and Netter (2001) for a survey) which

suggests that privately owned firms will perform better, in the sense of total factor

productivity as well as financial measures, than their state-owned counterparts. Djankov and

Murrell (2002) survey the considerable empirical literature on these issues for transition

economies and reach exactly the same conclusion for the economics of Central and Eastern

Europe. However, they remain more circumspect at this stage for Russia and other countries

of the former Soviet Union (see also Estrin and Wright (1999)). An important reason for the

problematic impact of privatisation in much of the CIS has been the very high level of insider

ownership (see Earle and Estrin (1997)). The theory suggests that the privatisation to insiders

may not have the desired effects on managerial effort and enterprise performance (see Earle,

Estrin and Leshchenko (1996)), and Djankov and Murrell (2002) interpret the paucity of

significant results about the positive impact of private ownership on performance in the CIS

as resulting from both the poor quality of the privatisation (widespread insider ownership) and

the relatively weak development of supporting institutions (see EBRD (2000)). An important

7

aspect of our survey is therefore to investigate whether ownership patterns have been

evolving away from insider control towards outsiders in the years since privatisation.

Our survey allows us to explore whether the pattern of ownership was changing in Russia in

the four or five years post privatisation, as was predicted by for example Boycko, Shleifer and

Vishny (1995). We are able to distinguish between all three of the main categories of owner

– insiders (managers plus workers), the state (Federal and Regional Government) and

outsiders (the remainder, including Investment Funds, Banks, other firms and private

individuals). Unfortunately ownership questions were found to be sensitive by our

interviewees, eliciting many more missing values than other questions. Hence, we are not

usually able to break down the ownership categories any further without considerable loss of

information. The only exception is for insiders; in two thirds of firms, it is possible to break

the category down into workers and managers.

Table 1 Ownership by Majority Shareholding Group

At time of

privatisation

On January 1st 2000

Number of

firms

% of firms Number of

firms

% of firms

Insider-owned 279 79.3 217 59.5

Outsider-owned 31 8.8 112 30.7

State-owned 25 7.1 13 3.6

No overall ownership 17 4.8 23 6.3

Total 352 100.0 365 100.0

Source: Author’s calculations

In Table 1, we categorise firms according to groups that own the majority of shares (greater

than 50%). The proportion of firms in each category does not change greatly if we use

alternative indicators of majority shareholder e.g. dominant shareholder (largest single

shareholding group) or a lower majority shareholder threshold (>40%, >35%). The survey

confirms the findings of other studies (see e.g. Estrin and Wright (1999)) that insiders held the

vast majority of shares in privatised firms immediately post-privatisation. Outsiders

controlled a mere 9 % of firms in our survey; a similar proportion to that is identified in other

studies (see e.g. Earle and Estrin, 1997)). However, the small fraction of majority state

shareholding merely reflects our sampling strategy of looking at privatised enterprises (see

8

Appendix to this special issue)1. An important indicator of the evolution of reform is the

changing ownership pattern. If secondary capital markets are effective and liquid, one would

expect to see a significant shift from insider to outsider ownership and this is confirmed by

the data in Table 1. This suggests that, even before the reforms following 1998, outsiders had

been buying shares from insiders to obtain majority control. Insiders had lost majority control

in more than 55 firms, some 15% of the total and 21% of insider firms, while outsiders had

gained majority control in 75 firms, more than double the number that group controlled

originally, mainly from insiders but also from the state dominated category. The period from

around the mid–1990’s until 2000 therefore appears to have been one in which there were

important changes in the underlying pattern of control, in ways that might have favoured

improved corporate governance.

In Table 2, we explore the changing pattern of ownership more thoroughly, using information

about average shareholdings held by each group. The table includes information about the

number of firms upon which the measures are based, which varies depending on the category

of owner, because of missing values. Although there has been a decline in shareholdings by

insiders overall, Table 2 indicates (on a smaller sample) that this masks a large decline in

worker ownership but an increase in share ownership by managers. Managers have increased

their stake by almost 30% since privatisation. The evolution in dominant ownership we saw

in Table 1 is explained by the fact that outsider ownership has doubled since privatisation and

now accounts for about one third of shares, almost as much as workers and considerably more

than managers. Though relying on an even smaller proportion of the sample, we can add the

following about outsiders. About half of the shares in the hands of outsiders are under the

ownership of other Russian firms, with the rest divided between banks and investment

companies, foreign firms, and ‘others’. Outsider ownership is also closely correlated with

concentrated ownership: 38 percent of outsider-owned firms had 2-3 shareholders controlling

50 percent or more of the shares, versus only 7 percent of insider-owned firms. This suggests

that outsiders may have been more effective in addressing corporate governance issues in

firms where they control majority stakes. It could also reflect selection bias by outsiders,

who only invest in firms where they can purchase significant stakes. Outsiders tend to hold

small stakes in firms that remain insider-controlled; the average outsider shareholding in

1 The fact that there are hardly any majority state-owned firms in our sample arises because

Russian sources define a firm to be privatised if any of its shares have been sold, rather than

when a majority have been sold. Retained stated shareholding was actually rather high in

Russia at the time when most firms were privatised (see Bennett, Estrin and Maw (2001)).

9

insider-owned firms is only 11 percent, versus the 24 percent shares owned by insiders in

outsiders-owned firms.

Table 2 Change in Share Ownership by Major Category

At time of

privatisation

On January 1st 2000 Change

Number

of firms

% of

shares

Number

of firms

% of

shares

Number

of firms

% of

shares

Insiders, of which: 351 71.8 364 62.3 339 -9.5

Managers 216 12.7 229 17.7 201 3.8

Workers 216 54.0 229 34.5 201 -19.9

Outsiders 351 16.0 364 32.0 339 16.1

State 351 12.2 364 5.7 339 -6.6

Source: Authors’ calculations

Our measures of competition are perceptual, being the responses by senior managers to

questions about the number of significant competitors faced in “their market place” (regional,

national or global)2. We use two measures of competition – domestic competition and import

competition – because transition theory has stressed the role of trade in increasing competitive

pressures on firms (see e.g. World Bank (1996)). Domestic competition is defined as “high”

if there are more than five competitors in the same market; “medium” if the number of

competing firms is between 3 and 5; and “low” in the case of monopoly and duopoly3. We

find the proportion of firms in the three categories to be 62.7%, 27.5% and 9.7% respectively.

Thus the survey indicates that most Russian firms face a significant degree of competition in

their relevant markets; a finding echoing previous studies (see e.g. Earle and Estrin (1998)

and Brown and Earle (2001)).

2 The bulk of firms in our survey define their market in regional or national Russian terms.

For almost every firm the percentage of sales derived from Krai/oblast or Russian Federal

level exceeds 50%. In the entire sample of 437 firms, only 13 sell primarily abroad. 3 The relevant geographical dimension is employed at all times. If a firm competes on the

“market” only at the krai/oblast level, then only its krai/oblast competitors are counted, etc.

10

The only measure of foreign competition is a categorical variable showing whether or not

firms face significant competition from imports. Imports are found to be a significant source

of competition in the market by only 37% of firms; rather a low proportion given that the

regional composition of our sample includes many of the main conurbations. In Table 3, we

present cross-tabulations of the two measures. It can be seen that a significant proportion of

Russian firms face high domestic and import competition; more than 25% of the total in the

sample. In contrast, only 7% of firms face little competition in their relevant markets, either

from domestic or foreign competitors. Moreover, import competition plays some role in

limiting firms in areas of higher domestic monopoly power – 28% of firms facing medium

domestic competition and 25% of firms facing low domestic competition instead face

significant import competition. Thus, competitive pressures on firms in Russia are perhaps

higher than one might expect, at least in the relatively industrial and open oblasts chosen for

this survey.

Table 3 Distribution of Firms According to Domestic and Foreign Competition

Categories

Import competition Domestic competition

1=yes 0=no 1

high

2

medium

3

low

Total

0 144 (60%) 75 (72%) 28 (75%) 247

1 103 (40%) 31 (28%) 9 (25%) 143

Total 247 106 37 390

Source: Authors’ calculations

The survey allows us to explore the robustness of our competition measures by comparing

firms’ responses on the number of competitors to their estimate of the demand impact of

price change. Respondents are asked what the likely demand impact of a 10 percent price

increase of their major product would be. We find 62.2% of high-competition firms expect a

sales drop greater than 10 percent, and only 38.2% have a price elasticity of demand less than

unity. The equivalent values for low and medium competition enterprises are 35.5 percent

and 64.5 percent respectively. The differences are significant at the 95 % level. This pattern

strengthens our confidence in the categorisation of competitive pressures faced by firms.

11

The Western literature on enterprise performance tends to concentrate on total factor

productivity (see e.g. Nickell (1996)) or financial indicators such as return on equity (see e.g.

Megginson and Netter (2001)). There are great difficulties in using the same indicators in

transition economies, not least because of problems with accounting standards, measurement

of capital and reliability of profit data (see Commander et al (1996) for a discussion in the

Russian context). In this study, we have followed the literature (see e.g. Frydman et al

(1999)) in using a variety of measures including productivity, profitability, investment rates

and restructuring. The latter is of particular importance since it measures managerial

activities to alter the performance of the firm that may or may not in the short term be

associated with financial measures of company performance (see Estrin and Rosevear

(1999)). Restructuring is notoriously difficult to measure, and we addressed the issue in the

design of the survey by asking managers a number of questions about their restructuring

activities, ranging from the introduction of new products and services or quality enhancing

innovation to sale or leasing out real estate and the shedding of excess labour. Managers were

asked to categorise their activities up to 1999: (1) engaged in a specific activity in 1997, 1998

and/or 1999 (answered separately); (2) didn’t engage in the activity 1997-99 because it was

already done; (3) didn’t engage in it because firm never needed to do it; or (4) should have

engaged in it but have not done so. There are a number of ways of combining these data into

summary measures but for this initial exercise we focus on the simplest possible one: whether

the firm chose to engage in restructuring activity at all between 1997 and 1999.

12

Table 4 Deep and Defensive Restructuring Deep

restructuring

Total

number

of firms

% of firms

engaged in

restructuring in

1997-99

Defensive

restructuring

Total

number

of firms

% of firms

engaged in

restructuring in

1997-99

Introduction of new

products and

services

435 54.9 Liquidation of

unprofitable products

426 46.0

Moves to new

markets

423 75.7 Cuts in social

provision

425 52.7

Improved marketing 428 71.7 Shedding excess

labour

431 56.1

Energy-saving

innovation

420 53.6 Sale or leasing-out of

excess equipment

431 45.0

Labour and

material-saving

innovation

425 52.0 Sale or leasing-out of

real estate

428 47.7

Quality-raising

innovation

423 66.7

Source: Authors’ calculations

Table 4 presents the percentages of firms that engaged in various restructuring measures in

1997-99, grouping measures under the headings of “deep restructuring” (e.g., introducing new

products or moving into new markets) and “defensive restructuring” (e.g., labour shedding or

liquidating plant or product lines).

Many observers have found it useful to divide restructuring into activities that are primarily

reactive, and those which suggest that the firm is making the internal changes required to

permit it to function effectively in a market environment (see Estrin, Gelb and Singh (1995),

Roland (2000)). In this paper, we adopt the classification proposed by Carlin et al (2001) and

divide restructuring activities into “deep” and “defensive”. The percentage of firms engaged

at all during the sample period in each of the major restructuring activities in presented in

Table 4. It can be seen the defensive activities are on average rather less common than deep

ones, which might at first seem an encouraging finding. Indeed, it could indicate a sequence

13

in restructuring whereby defensive restructuring measures had already been undertaken and

deeper ones were now underway. However this is not entirely convincing, given the

relatively poor state of Russian industry in this period. The high mean values could also

reflect optimistic evaluations of their own performance by our respondents. In our later work,

we therefore concentrate on the relative ranking of firms in terms of restructuring and on the

time path of restructuring activity.

Following Carlin et al. (2001), we have gone on in later work to condense these measures of

restructuring into composite deep and defensive restructuring indices using the method of

principal components. In both cases, the eigenvector of the first principal component

provides the weights to be applied to the component restructuring indices when constructing

the composite index. The method also allows a check of whether a composite index is

sensible, i.e., whether it is measuring some underlying deep or defensive restructuring

activity. In the case of the deep restructuring composite index, the first principal component

(out of six) explains 38 percent of the variance in the six deep restructuring indices; the next

most important component explains less than half of that. Similarly, the first principal

component for the five defensive restructuring activities explains 36 percent of the variance.

4 The Impact of Ownership and Competition on Performance

In the section, we first explore the interaction between competition, ownership and a number

of important control variables. We then go on to investigate how competition, interacted with

ownership, affects a variety of indicators of enterprise performance.

4.1 Ownership and Performance

Commencing with ownership, the literature suggests that enterprise performance was not

greatly influenced by ownership per se in Russia in the early years of transition (see e.g.

Djankov and Murrell (2002)). In this paper, our focus will be on the interactions between

state ownership and competition and their effects on enterprise performance. As noted

above, one would not necessarily expect the prediction about the enhanced performance

of firm operating in a more competitive product market environment to carry over to

environments where the enterprise in question was state-owned. Moreover, one would

expect state ownership to exacerbate the tendencies to inefficiency and slack engendered

by monopoly power.

14

Because the Russian privatisation process led to such an unusual structure of ownership,

with relatively few outside owners of the type typical in Western economies, the literature

has also addressed the issue of how different forms of majority ownership have affected

company performance. This issue is peripheral to our main theme, because there are no

obvious reasons for expecting fundamental differences in terms of the impact on company

performance between the interactions of competition with insider and outsider ownership.

However, for the sake of completeness, we present some findings on the performance–

ownership question4. Our approach is to compare performance in insider and outsider

owned firms using a large variety of performance measures – value added per worker,

change in productivity, employment growth, investment rates, export shares and the two

composite measures of restructuring. The findings are reported in Table 5. We note that

insider owned firms have slightly higher productivity and export shares, and slightly

smaller (fall in) employment and investment share. They also undertook slightly more

deep restructuring and slightly less defensive restructuring. The fall in productivity

growth is larger in outsider than insider owned firms. However, none of these differences

is statistically significant at even the 90% level. Hence we conclude that our survey

confirms the findings of numerous other studies about Russia: that in 1999 ownership

changes had not yet begun to have a significant effect on company performance (see

Djankov and Murrell (2002)).

Table 5 The Effect of Ownership on Performance, 1997-1999 Value

Added/

worker

Real

Productivity

Growth

Employment

Growth

Investment

Rates (I/K)

Export

Share

Restructuring

Index

Deep Defensive

Total 65.8 -3.7 -7.5 7.4 4.4 61.9 49.0

Insider

Owned

62.7 -1.8 -9.3 6.2 4.8 62.2 49.5

Outsider

Owned

64.9 -3.2 -9.9 7.8 4.3 61.4 55.8

Source: Author’s calculations

4 The ownership structure may to some extent be endogenous, if the ?actors who control the privatization process (e.g. insiders) select ownership on the basis of performances. It is in principle very hard to address this problem using cross-section data. However, our data set contains information about ownership back to the time of privatization, which is likely to be exogenous to current performance. Our findings are not significantly affected if we use initial ownership structure rather than current ownership structure.

15

The relationship between ownership and competition will depend on the sequence and

method of privatisation chosen. One could imagine, for example, that governments

seeking to maximise revenue would sell profitable firms first (see e.g. Gupta, Ham and

Svejnar (2000)) and hence one might be expect a positive correlation between private

ownership and monopoly power. Alternatively, the authorities might seek to retain firms

with significant monopoly power in state hands, in order to develop regulatory

mechanisms or to share in the monopoly profits , while disposing of firms operating in a

more competitive environment. The cross-tabulations between state and private

ownership on the one hand, and the two indicators of competition on the other, are

contained in Table 6. Some groups are small because, as noted above, the sample

contains relatively few majority state-owned firms, but it can be seen that there are almost

no state owned firms in the low competitive category. This is consistent with the view

that the state chose to privatise firms with significant domestic monopoly power, though

import competition does not appear to have entered their calculations.

Table 6 Ownership of Firms and Competition Level

Domestic competition Import competition

1 2 3 high medium low

Total 0 1 Total

No Yes

State owned 8 2 1 11 10 3 13

Private owned 205 92 33 350 207 124 331

Total 215 94 34 343 217 129 346

Source: Authors’ calculations

It is also important to explore the regional and sectoral pattern of competition in our

sample. In fact, the variation in our perceptual measures within region is comparable to

that between regions, and differences are not statistically significant The only region

where high levels of domestic competition are more common are Krasroyansk, and

perhaps slightly in the more isolated centres such as Perm. Unsurprisingly, rather more

16

firms in Moscow and Moscow region have reported import competition than in other

regions (more than 50% as against less than 40% in the sample as a whole). There is also

no significant relationship between the available indicator of the firm’s sector, measured

at the two-digit level, and our measure of domestic competition. Around 10% of firms in

every sector indicate that they have low levels of competition, except for machine tools

and metal working where the proportion is closer to 20%, though the difference is not

statistically significant. Import competition is found to be slightly but significantly

higher in light industry and chemicals.

4.2 The Impact of Competition on Performance

In this section, we explore the relationship between the performance of the firm –

measured by restructuring, productivity, financial performance and investment – and the

two measures of competition. In the regression analysis, we control for firm size,

industry, location and ownership structure.

4.2.1 Competition and Restructuring

As noted above, the questionnaires report information on fifteen possible reforms, asking

whether they have been implemented between 1997 and 1999, and, if not exploring some

possible reasons for it. We now seek to use the richness of the measures more fully.

Therefore, in addition to dividing the activities into deep and defensive restructuring, we

investigate the intensity of restructuring:

- continuous, if the firm has restructured constantly between 1997 and 1999

- one-off, for firms which have undertaken the various reforms once between 1997

and 1999

- missed, if reforms were needed but could not be implemented.

The indices range between zero and one. Hence, a firm that has undertaken all the deep

reforms every year between 1997 and 1999 will have the maximum score of one in its

deep, continuous” index5. The results are reported in Table 7. First, the data confirm

5 The use of more than one measure is advisable because none is devoid of ambiguity.

Continuous restructuring might be seen both as a sign of “virtuous behaviour” and a failure to

succeed at the first time. Exactly the opposite can be said of the one-off index. The third

indicator could be biased because the incentive not to admit the failure to implement

necessary reforms (and to provide wrong information instead) is quite high.

17

that firms engage more in deep than defensive reforms. For the latter, companies have

undertaken less than half of the reforms they were asked about, and less than a quarter of

them continuously. The equivalent values for deep reforms are all significantly higher.

Firms have undertaken 60 percent of them at least once between 1997 and 1999, of

which more than one half have been done continuously.

Table 7 Restructuring Indices and Competition

Domestic competition Foreign competition

High Medium Low Yes no

Deep, continuous .363

(.319)

.382

(.329)

.286

(.309)

.402

(.318)

.341

(.324)

Deep, one off .630

(.285)

.635

(.289)

.564

(.321)

No difference

Deep, missed No difference (overall mean = .160)

Defensive, continuous .244

(.264)

.220

(.251)

.190

(.207)

.247

(.263)

.230

(.256)

Defensive, one off .488

(.306)

.519

(.287)

.460

(.275)

.518

(.308)

.482

(.291)

Defensive, missed .032

(.089)

.040

(.089)

.040

(.092)

No difference

(overall mean = .037)

Note: Standard deviations are in parentheses.

Group-specific mean values are reported only when the differences are significant

Source: Authors’ calculations

Table 7 also provides evidence of a positive association between deep restructuring and

competition, both domestic and foreign. Firms in highly and medium competitive

domestic markets restructure more than those in concentrated environments, both

intermittingly and continuously. The same applies to firms facing import competition.

Turning to defensive reforms, we once again see more restructuring in almost every

category in firms with high rather than low domestic competition and foreign

competition. However, foreign competition does not seem to affect missed restructuring,

whether deep or defensive. Thus the raw data seem to indicate that the predicted

relationship between competition pressure and restructuring does hold in Russia in the

sample period. However, the small size of the mean differences between competition

18

groups suggests the need for further work. Our approach is to use regression analysis,

estimating the following model:

R = f(DC, IC, size, sector, ownership, region) (1)

where R is a measure of restructuring, DC and IC are dummy variables for our measures

of domestic and international competition respectively, firm size is measured by

employment and ownership by a dummy variable for majority state ownership. We

include firm size because we wish to allow for the possibility of economies of scale in

restructuring. Industry dummies control for demand and technical differences between

firms, and regional dummies for local demand and institutional factors.

We run separate regressions for each of the six restructuring variables (deep restructuring,

continuous (C), one-off (OF) and Missed (M) and the same three groups for defensive

restructuring). We also report regressions in which competition is interacted with

ownership to test the complementary effects discussed above. The results are summarised

in Table 8, which reports the sign of the significant coefficients in each of the twelve

regressions6. The regressions confirm the findings of table 7 that competition is

influencing restructuring. Firms in highly concentrated markets engage in less deep

restructuring (both continuous and one-off) than highly competitive ones, and to some

extent in less defensive restructuring as well. Firms facing medium competition miss

more reforms. There are also some private ownership effects. Defensive restructuring is

positively correlated with state ownership and a significant interaction of ownership with

competition is found. Thus the regressions broadly confirm our hypotheses about the

impact of competition on restructuring, and the significant joint role of private ownership.

6 The regressions are available in an Appendix to this paper.

19

Table 8 Competition and Restructuring — Regression Analysis — Significant Coefficients

Deep restructuring Defensive restructuring

C C+I OF OF+I M M+I C C+I OF OF+I M M+I

State +

DC-Med

dom

+ + - - + +

DC-Lo

dom

- - - - - -

IC

Med*state - +

Lo* state

IC* state - + +

Note: C = continuous restructuring

OF = one-off restructuring

M = missed restructuring

I = interactions

Signs are reported if coefficients are significant at the 10 % level or above

Med dom = medium domestic competition dummy

Lo dom = low domestic competition dummy

State = dummy for majority state ownership

Source: Authors’ calculations

4.2.2. Competition, Productivity and Profitability

The quantitative data in our survey are problematic because of poor accounting standards, the

high levels of inflation over the period, and firms either misreporting or failing to report certain

variables, e.g. profits. Despite this, we attempted to estimate a variety of regressions of the form,

Performance = f (DC, IC, size, sector, region, ownership) (2)

with and without interaction effects between competition and ownership. For the performance

indicators, we used three measures of productivity: the inverse of capital productivity (capacity

utilisation, measured as the current quantity of output over the maximum physical output of the

equipment), sales per worker and value added per worker. The results are not reported however,

because the equations themselves were not statistically significant competition was not found to

have a significant effect on capacity utilisation in either level or rate of change form, nor on any

of the measures of labour productivity. Moreover, no significant ownership effects were

identified, and there were no significant interactions.

Predictions about the impact of competition on profitability are more complex because monopoly

power is associated with greater price-cost margins. (See Nickell (1996)). We estimated a series

of equations with the form of equation (2), using rate of return on equity (ROE), profits/capital

stock and profits/sales as the dependent variable. As for the other quantitative performance

equations, we were unable to identify any competition effects and the equations themselves were

not significant, and hence are not reported7. Given the data problems, it is unclear whether these

findings indicate that competition and ownership are not yet affecting quantitative measures of

productivity and profitability or that measurement error has prevented us from isolating a

significant effect.

4.4.3 Competition and Innovation

Schumpeter hypothesised that competition would hinder investment and innovation, and our data

offer a way to test that hypothesis. We have information on the investment activity, and can thus

explore the relationship between competition and the timing of major investments. If competition

shortens the innovation cycle, then the higher is monopoly power, the lower is the probability of a

firm having recently (since August 1998) undertaken a major investment. Conversely, if

7 The regressions are available in an Appendix to this paper.

17

monopoly power provides a financially more secure environment for investment, and relaxes

financial constraints on the firm, the impact will go the other way.

We regress a binary variable, coded one if such an investment occurred since 1998 against

competition, controlling once again for industry, firm size, region and ownership. The results are

reported in Table 9. In the basic model (without interactions) we find no significant effect from

domestic competition but that foreign competition significantly increases the probability of

investment. As expected, state-ownership reduces investment but the effect is not quite

statistically significant. The results are strengthened once interactions are included. Foreign

competition increases the probability of investment, especially when the firm is privately owned.

Once again, we find that competition enforces rather than hinders company performance in this

important aspect of restructuring.

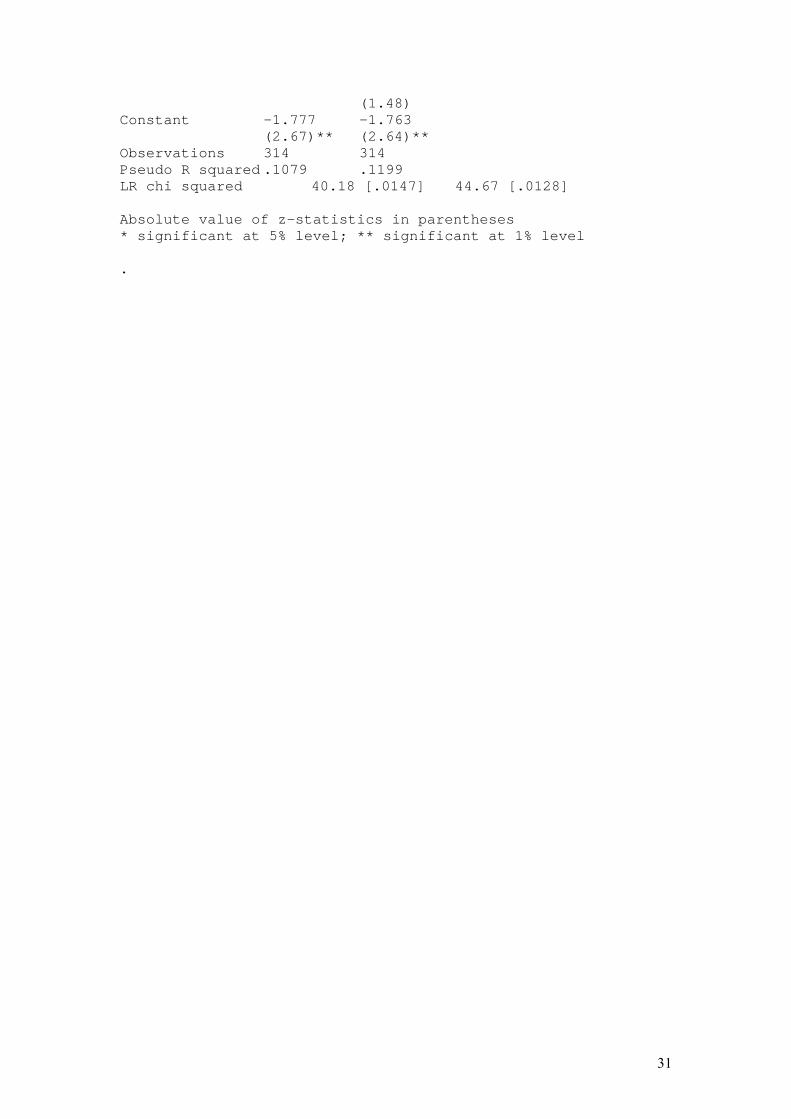

Table 9 Logistic Regressions of Probability of Undertaking Major Investment in Fixed

Capital Since August 1998

Probability of undertaking

investment

Basic model Interactions

Controls for:

Size

Region Not significant Not significant

Industry

State ownership - (p-value=0.111) Not significant

Domestic competition:

Medium Not significant Not significant

Low Not significant Not significant

Foreign competition:

Yes .549 (p-value=0.065) .745 (p-value=0.022)

Interaction of state ownership and

foreign competition

--- -.042 (p-value=0.097)

Source: Authors’ calculations

18

5 Conclusions

The literature has suggested that competition will be an important element in the transition process,

especially when combined with privatisation so that the former links between the enterprise sector and

the state are weakened (see Blanchard et al (1991), Stiglitz (1999)). However, empirical evidence to

date for Russia and the CIS countries has not strongly supported these hypotheses; ownership effects

have been difficult to identify in previous surveys and the evidence about the import of competition,

especially import competition, has been decidedly mixed (see Djankov and Murrell (2002)).

Our survey, which uses data from Russian enterprises several years after privatisation, allows us to

revisit these issues at a time when firms could have begun to address internally the difficulties raised

in a dramatic fashion by the liberalisation strategy from 1992 and mass privatisation after 1993.

Sufficient time should have elapsed by 1999 for us to be able to begin to discern fundamental

behavioural changes from the statistical noise generated by the shocks to the economic environment

caused by the reforms from 1992-1994. On the other hand, our sample period includes the year of the

economic crash in 1998, which seems likely to distort a number of our variables. In particular,

nominal variables determined largely on the demand scale, like sales or value added, will be

influenced by the decline in domestic demand in 1998/9, and measurement error could be increased

by the higher inflation rates post-1998, especially given the inadequacy of disaggregated price and

cost deflators in Russia.

These phenomena help us to explain some of the main results in this paper. We do identify clear

behavioural differences between majority state owned and private firms, especially with respect to

restructuring activity. However, along with much of the literature, we continue to be unable to

identify clear differences in performance between insider and outsider owned firms. There are a

number of possible interpretations for this. One is that insider ownership is not as damaging in the

short term in Russia as economic theory might suggest, because information asymmetries yield

advantages to incumbent managers; because of selection effects whereby managers and workers were

able to purchase “better” firms; and because in a context of managerial scarcity, the best managers are

concentrated in insider owned firms where they can obtain a higher share of the rewards from

successful company performance. Capital market weaknesses may also make it much harder for

outsiders to impose effective corporate governance. It may also still be too early to judge the impact

of privatisation on performance. There clearly has been a reallocation of shareholding since the

initial privatisations, with a move to outsider stakes and increased concentration of ownership. In the

longer term, this may have profound effects on company performance, but they are not yet visible in

our data set.

19

The thrust of this paper has been about the impact of competition upon enterprise performance. The

findings have been encouraging and emphasise the importance of price and trade liberalisation for the

transition process. We have been unable to identify any impact of competition using financial and

economic measure of performance, but as noted above such data were severely affected at the time the

sample was taken by the consequences of the 1998 crash. However, in almost all measures of

managerial activity, including deep restructuring, defensive restructuring and investment intentions,

we identify a positive impact from domestic competition, and sometimes also from import

competition.

However, the paper confirms the view that transition reforms cannot be undertaken piecemeal because

their impact is complementary. In particular, competition has a more emphatic effect on performance

in majority privately owned firms than in stat owned ones. Privatisation and liberalisation activities,

including trade policies, therefore need to go hand in hand.

20

References

Aghion, Philippe, Christopher Harris and John Vickers. 1997. “Competition and Growth with Step-by-Step Innovation: An Example,” European Economic Review 41, p.771-782.

Bennett, John, Saul Estrin and James Maw. 2001. “Mass Privatisation and Partial State Ownership of Firms in Transition Economics.” CEPR Discussion Paper no.2895, London: CEPR.

Blanchard, Olivier, Rudiger Dornbusch, Paul Krugman, Richard Layard, and Lawrence Summers. 1991. Reform in Eastern Europe, Cambridge, Mass.: MIT Press.

Boycko, Maxim, Andrei Shleifer and Robert Vishny. 1995. Privatizing Russia. Cambridge, Mass.: MIT Press.

Brown, David and John Earle. 2001. “Privatization, Competition and Reform Strategies: Theory and Evidence from Russian Enterprise Panel Data,” CEPR Discussion Paper no.2758, London: CEPR.

Carlin, Wendy, Steven Fries, Mark Schaffer and Paul Seabright. 2001. “Competition and Enterprise Performance in Transition Economies: Evidence from a Cross-Country Survey,” WDI Working Paper no. 376, Michigan: William Davidson Institute.

Commander, Simon, Qimiao Fan and Mark Schaffer, (eds.). 1996. Enterprise Restructuring and Economic Policy in Russia. Washington: World Bank.

Commander, Simon, Irina Dolinskaya and Christian Mumssen. 2002. “Determinants of Barter in Russia: An Empirical Analysis,” Journal of Development Economics, 67 (2), p.275-307.

Djankov, Simeon, and Peter Murrell. 2002. “Enterprise Restructuring: a Quantitative Survey,” Journal of Economic Literature 40 (3), p.739-792.

Frydman, Roman, Cheryl Gray, M. Hessel and Andrzej Rapaczynski. 1999. “When Does Privatization Work? The Impact of Private Ownership on Corporate Performance in the Transition Economies,” Quarterly Journal of Economics 114 (4), p. 1153-1191.

EBRD. 2000. Transition Report 2000: Employment, Skills and Transition, London: EBRD.

EBRD. 2002. Transition Report 2002: Agriculture and Rural Transition, London: EBRD.

21

Earle, John, Saul Estrin and Larisa Leshchenko. 1996. “Ownership Structures, Patterns of Control, and Enterprise Behavior in Russia,” in Commander, S., Q. Fan and M. Schaffer (eds), Enterprise Restructuring and Economic Policy in Russia, Washington: World Bank.

Earle, John and Saul Estrin. 1997. “After Voucher Privatization: The Structure of Corporate Ownership in Russian Manufacturing Industry,” CEPR Discussion Paper no.1736, London: CEPR.

Earle, John and Saul Estrin. 1998. “Privatization, Competition and Budget Constraints: Disciplining Enterprises in Russia,” Working Paper no.128, Stockholm: Stockholm Institute of Transition Economics.

Ellman, Michael. 1989. Socialist Planning. Cambridge: Cambridge University Press.

Estrin, Saul, Alan Gelb and Inderjit Singh (1995), “Shocks and Adjustment by Firms in Transition: A Comparative Study,” Journal of Comparative Economics 21(2), p. 131-153.

Estrin, Saul and Mike Wright. 1999. “Corporate Governance in the Former Soviet Union: An Overview,” Journal of Comparative Economics 27(3), p.398-421.

Estrin, Saul and Adam Rosevear. 1999. “Enterprise Performance and Ownership: The Case of Ukraaine,” European Economic Review, 43(4), p. 1125-1136.

Gupta, Nadini, John Ham and Jan Svejnar. 2000. “Priorities and Sequencing in Privatization:

Theory and Evidence from the Czech Republic,” The William Davidson Institute and the

University of Michigan Business School, mimeo.

Hart, Oliver. 1083. “The Market Mechanism as an Incentive Scheme,” Bell Journal of Economics, 14, p. 366-82.

Holmstrom, Bengt. 1982. “Moral Hazard in Teams,” Bell Journal of Economics, 13, p. 324-40.

Linz, Susan and Gary Krueger. 1998. “Enterprise Restructuring in Russia’’ Transition Economy: Formal and Informal Mechanisms,” Comparative Economic Studies 40(2), p. 5-52.

Megginson, William, and Jeffry Netter. 2001. “From State to Market: A Survey of Empirical Studies on Privatization,” Journal of Economic Literature, 39 (2), p. 321-389.

Nalebuff, Barry and Joseph Stiglitz. 1983. “Prizes and Incentives: Towards a General Theory of Compensation and Competition,” Bell Journal of Economics, 14(1), 21-43.

22

Nickell, Stephen. 1996. “Competition and Corporate Performance,” Journal of Political Economy 104(4), p.724-746.

Nickell, Stephen, Daphne Nicolitsas and Neil Dryden. 1997. “What Makes Firms Perform Well?” European Economic Review 41, p. 783-96.

Roland, Gerard. 2000. Transition and Economics: Politics, Markets and Firms. London: MIT Press.

Schaffer, Mark. 1998. “Do Firms in Transition Economies Have Soft Budget Constraints? A Reconsideration of Concepts and Evidence,” Journal of Comparative Economics 26, p. 62-79.

Stiglitz, Joseph. 1999. “Whither Reform?” 1999 ABCDE Conference. Washington D.C.: World Bank.

Vickers, John and George Yarrow. 1988. Privatization: An Economic Analysis. Cambridge Mass.: MIT Press.

Vickers, John. 1994. Concepts of Competition. Oxford: Clarendon.

World Bank. 1996. World Development Report: From Plan to Market. Washington, DC:

Oxford University Press.

World Bank. 2002. Transition: The First Ten Years. Washington, DC: World Bank.

23

Appendix

Saul Estrin and Manuela Angelucci

24

Table A1 Number of Enterprises: Coverage in terms of Size and Industry*

GOSCOMSTAT/Survey: Number of enterprises by industry&size

Industry code

Total GKS**

Total Survey

Survey/ GKS %

Size group1,

GKS

Size group1,

Surv

Survey/ GKS %

Size group2,

GKS

Size group2,

Surv

Survey/ GKS %

Size group3,

GKS

Size group3,

Surv

Survey/ GKS %

Total Industry 10 25446 10772 2273 2137

Selected industries 20104 437 2.2 8862 147 1.7 1789 139 7.8 1510 139 9.2

Chemicals 13 644 56 8.7 257 9 3.5 68 16 23.5 179 31 17.3 Machinery 14 6445 108 1.7 2694 29 1.1 661 25 3.8 873 54 6.2 Wood 15 2702 66 2.4 1188 37 3.1 252 16 6.3 141 13 9.2 Stone&clay 16 2060 72 3.5 1231 24 1.9 177 29 16.4 50 19 38.0 Light 17 3038 72 2.4 1071 28 2.6 211 33 15.6 130 11 8.5 Food 18 5215 63 1.2 2421 20 0.8 420 20 4.8 137 23 16.8

* Size Group 1: =>100 <=500; Size Group 2: > 500 <=1000; Size Group 3 >1000 <=5000 ** Goskomstat data refers only to medium and large enterprises Source: Authors’ calculations

25

Table A1 Restructuring Indices — Deep Restructuring (1) (2) (3) (4) (5) (6) Moscow reg -0.175 -0.175 -0.084 -0.086 0.033 0.036 (2.31)* (2.30)* (1.23) (1.26) (0.63) (0.67) St Petersburg -0.221 -0.223 -0.099 -0.090 0.048 0.045 (2.66)** (2.66)** (1.31) (1.19) (0.82) (0.76) St Petersburg reg 0.016 0.014 -0.032 -0.025 0.098 0.097 (0.11) (0.09) (0.24) (0.18) (0.95) (0.94) Nizhny novgorod -0.101 -0.102 0.035 0.037 0.004 0.006 (1.37) (1.37) (0.52) (0.54) (0.09) (0.11) Samara -0.114 -0.116 -0.034 -0.031 0.036 0.036 (1.36) (1.36) (0.45) (0.40) (0.61) (0.60) Ekaterinburg -0.182 -0.183 -0.067 -0.067 0.042 0.044 (2.44)* (2.42)* (0.99) (0.98) (0.79) (0.83) Perm -0.309 -0.311 -0.145 -0.139 0.079 0.078 (3.67)** (3.65)** (1.90) (1.81) (1.34) (1.31) Novosibirsk -0.369 -0.370 -0.261 -0.262 0.192 0.198 (4.82)** (4.75)** (3.76)** (3.74)** (3.58)** (3.63)** Volgograd -0.315 -0.315 -0.190 -0.195 0.193 0.197 (3.77)** (3.74)** (2.50)* (2.56)* (3.28)** (3.35)** Chelyabinsk -0.310 -0.309 -0.014 -0.016 -0.091 -0.087 (2.42)* (2.40)* (0.12) (0.14) (1.01) (0.97) Omsk -0.228 -0.229 -0.130 -0.127 0.127 0.127 (2.38)* (2.37)* (1.50) (1.46) (1.88) (1.87) q7==13 -0.196 -0.199 -0.063 -0.050 0.044 0.044 (1.78) (1.75) (0.63) (0.49) (0.57) (0.55) Mach. Buil. & Metal. 0.126 0.126 0.121 0.125 -0.078 -0.081 (2.10)* (2.07)* (2.22)* (2.29)* (1.86) (1.91) Wood & paper 0.069 0.069 -0.034 -0.035 -0.012 -0.009 (0.95) (0.95) (0.52) (0.53) (0.23) (0.18) Stone & clay -0.019 -0.019 -0.044 -0.046 0.023 0.025 (0.28) (0.28) (0.74) (0.76) (0.48) (0.54) Light ind 0.072 0.073 0.055 0.048 -0.090 -0.084 (1.11) (1.12) (0.93) (0.81) (1.97) (1.81) Food ind 0.103 0.104 0.127 0.120 -0.094 -0.089 (1.52) (1.52) (2.06)* (1.96) (1.97) (1.87)

26

Table A1 Restructuring Indices — Deep Restructuring (cont.) 501-1000 0.046 0.045 0.047 0.053 -0.032 -0.036 (1.06) (1.04) (1.21) (1.35) (1.06) (1.19) >1000 0.172 0.171 0.068 0.074 -0.023 -0.027 (3.66)** (3.61)** (1.60) (1.74) (0.69) (0.82) State share -0.001 -0.002 -0.002 0.000 0.001 0.000 (1.03) (0.96) (1.35) (0.03) (0.93) (0.07) Med. Dom. Comp. -0.003 -0.004 -0.030 -0.036 0.055 0.062 (0.07) (0.08) (0.79) (0.90) (1.91) (1.99)* Low Dom. Comp. -0.122 -0.126 -0.095 -0.078 0.023 0.022 (1.98)* (1.86) (1.70) (1.28) (0.52) (0.46) Foreign Comp. 0.013 0.008 0.000 0.026 0.026 0.008 (0.36) (0.21) (0.00) (0.69) (0.98) (0.29) For comp*state sh 0.001 -0.004 0.003 (0.28) (1.74) (1.59) Low Dom comp*state sh 0.001 -0.003 0.000 (0.15) (0.83) (0.17) Med Dom comp*state sh 0.000 0.001 -0.002 (0.04) (0.42) (0.61) Constant 0.433 0.436 0.656 0.643 0.134 0.138 (5.49)** (5.41)** (9.17)** (8.86)** (2.42)* (2.45)* Observations 316 316 316 316 316 316 R-squared 0.23 0.23 0.20 0.21 0.17 0.17 Absolute value of t-statistics in parentheses * significant at 5% level; ** significant at 1% level > .>

27

Table A2 Restructuring Indices — Defensive Restructuring (1) (2) (3) (4) (5) (6)

Moscow reg -0.064 -0.063 0.005 0.004 0.017 0.018 (0.95) (0.93) (0.07) (0.05) (0.71) (0.74) St Petersburg 0.083 0.077 0.118 0.109 0.007 0.009 (1.12) (1.03) (1.43) (1.33) (0.27) (0.33) St Petersburg reg 0.043 0.036 0.047 0.041 0.069 0.071 (0.33) (0.28) (0.33) (0.29) (1.49) (1.51) Nizhny novgorod -0.160 -0.163 -0.112 -0.116 0.038 0.040 (2.44)* (2.46)* (1.53) (1.58) (1.63) (1.68) Samara -0.018 -0.021 0.048 0.042 -0.005 -0.004 (0.24) (0.28) (0.57) (0.51) (0.20) (0.14) Ekaterinburg -0.101 -0.102 -0.049 -0.045 0.031 0.031 (1.52) (1.52) (0.67) (0.61) (1.32) (1.28) Perm -0.062 -0.067 0.026 0.017 0.008 0.011 (0.82) (0.89) (0.32) (0.20) (0.30) (0.39) Novosibirsk -0.109 -0.111 0.013 0.010 0.059 0.061 (1.61) (1.60) (0.18) (0.13) (2.43)* (2.48)* Krasnoyarsk -0.076 -0.074 0.091 0.095 0.027 0.027 (1.02) (0.99) (1.11) (1.15) (1.02) (1.01) Volgograd -0.204 -0.203 0.059 0.069 -0.026 -0.028 (1.79) (1.77) (0.47) (0.54) (0.65) (0.69) Chelyabinsk -0.152 -0.154 -0.094 -0.091 0.005 0.005 (1.78) (1.80) (0.99) (0.96) (0.17) (0.15) Omsk -0.038 -0.049 0.173 0.185 0.016 0.014 (0.38) (0.48) (1.59) (1.66) (0.47) (0.38) Mach. Buil. & Metal. 0.060 0.058 0.010 0.015 -0.016 -0.018 (1.12) (1.08) (0.17) (0.25) (0.86) (0.95) Wood & paper -0.001 -0.001 -0.032 -0.022 -0.019 -0.021 (0.02) (0.02) (0.45) (0.31) (0.82) (0.90) Stone & clay -0.072 -0.071 -0.140 -0.138 0.018 0.018 (1.21) (1.20) (2.14)* (2.11)* (0.85) (0.85) Light ind 0.078 0.082 0.013 0.026 -0.018 -0.021 (1.36) (1.41) (0.20) (0.40) (0.90) (1.00) Food ind -0.011 -0.008 -0.089 -0.083 -0.010 -0.011 (0.19) (0.13) (1.33) (1.24) (0.47) (0.51)

28

Table A2 Restructuring Indices — Defensive Restructuring (cont.) 501-1000 0.003 0.000 0.011 0.009 -0.026 -0.026 (0.07) (0.01) (0.27) (0.22) (1.87) (1.87) >1000 0.022 0.018 0.013 0.007 -0.007 -0.006 (0.52) (0.43) (0.27) (0.16) (0.47) (0.43) State share 0.001 0.000 0.000 -0.002 0.001 0.001 (1.17) (0.18) (0.05) (0.88) (1.33) (1.52) Med. Dom. Comp. -0.071 -0.069 0.003 -0.008 0.022 0.027 (1.94) (1.75) (0.08) (0.18) (1.68) (1.88) Low Dom. Comp. -0.098 -0.112 -0.053 -0.047 0.019 0.018 (1.80) (1.87) (0.88) (0.71) (0.99) (0.83) Foreign Comp. -0.030 -0.045 0.042 0.015 -0.007 -0.003 (0.89) (1.25) (1.15) (0.38) (0.63) (0.26) For comp*state sh 0.003 0.004 -0.001 (1.05) (1.58) (0.66) Low Dom comp*state sh 0.002 -0.001 0.000 (0.64) (0.16) (0.17) Med Dom comp*state sh 0.000 0.002 -0.001 (0.09) (0.66) (0.86) Constant 0.333 0.343 0.527 0.535 0.029 0.027 (4.75)** (4.81)** (6.77)** (6.78)** (1.15) (1.06) Observations 316 316 316 316 316 316 R-squared 0.12 0.13 0.10 0.11 0.09 0.09 Absolute value of t-statistics in parentheses > * significant at 5% level; ** significant at 1% level > .

29

Table A3 Probability of Undertaking Investment in Fixed Capital Inv Interactions Moscow reg -0.482 -0.586 (0.80) (0.96) St Petersburg 0.015 -0.041 (0.02) (0.06) St Petersburg reg 0.174 0.106 (0.16) (0.10) Nizhny novgorod 0.038 -0.060 (0.07) (0.11) Samara -0.782 -0.836 (1.13) (1.21) Ekaterinburg 0.563 0.512 (1.01) (0.92) Perm -0.591 -0.748 (0.84) (1.03) Novosibirsk -0.939 -1.117 (1.46) (1.71) Krasnoyarsk -1.007 -1.127 (1.38) (1.54) Volgograd -0.670 -0.748 (0.66) (0.74) Chelyabinsk -0.764 -0.796 (0.95) (0.98) Omsk -0.658 -0.697 (0.70) (0.74) Mach. Buil. & Metal. 0.285 0.339 (0.57) (0.66) Wood & paper 0.531 0.525 (0.86) (0.84) Stone & clay 1.077 1.040 (1.97)* (1.89) Light ind 0.089 0.023 (0.16) (0.04) Food ind 1.434 1.412 (2.65)** (2.59)** 501-1000 0.376 0.447 (1.02) (1.20) >1000 0.877 0.949 (2.24)* (2.39)* State share -0.018 -0.013 (1.60) (0.89) Med. Dom. Comp. 0.078 -0.114 (0.24) (0.32) Low Dom. Comp. -0.236 -0.265 (0.44) (0.45) Foreign Comp. 0.550 0.746 (1.84) (2.30)* For comp*state sh -0.043 (1.66) Low Dom comp*state sh -0.001 (0.02) Med Dom comp*state sh 0.043

(1.48) Constant -1.777 -1.763 (2.67)** (2.64)** Observations 314 314 Pseudo R squared .1079 .1199 LR chi squared 40.18 [.0147] 44.67 [.0128] Absolute value of z-statistics in parentheses * significant at 5% level; ** significant at 1% level .

31

Table A4 Capital Vintage Kvntg Interactions Moscow reg -15.694 -15.712 (2.33)* (2.32)* St Petersburg -12.786 -13.031 (1.72) (1.74) St Petersburg reg -16.585 -16.784 (1.27) (1.28) Nizhny novgorod -12.159 -12.270 (1.85) (1.84) Samara -11.878 -12.026 (1.59) (1.60) Ekaterinburg -15.470 -15.387 (2.32)* (2.30)* Perm -10.910 -11.174 (1.45) (1.47) Novosibirsk -23.243 -23.322 (3.42)** (3.36)** Krasnoyarsk -12.592 -12.490 (1.69) (1.67) Volgograd -2.107 -1.904 (0.18) (0.17) Chelyabinsk -13.388 -13.376 (1.57) (1.56) Omsk -17.150 -17.072 (1.75) (1.69) Mach. Buil. & Metal. -8.013 -7.944 (1.50) (1.47) Wood & paper 3.443 3.635 (0.54) (0.56) Stone & clay -4.985 -4.940 (0.84) (0.83) Light ind -1.323 -1.015 (0.23) (0.17) Food ind 16.378 16.557 (2.71)** (2.72)** 501-1000 1.598 1.512 (0.42) (0.39) >1000 3.473 3.320 (0.83) (0.79) State share -0.176 -0.222 (1.54) (1.43) Med. Dom. Comp. -1.673 -1.877 (0.46) (0.47) Low Dom. Comp. 1.023 0.966 (0.19) (0.16) Foreign Comp. -0.841 -1.592 (0.25) (0.44) For comp*state sh 0.120 (0.49) Low Dom comp*state sh 0.016 (0.05) Med Dom comp*state sh 0.041

32

(0.13) Constant 37.039 37.340 (5.27)** (5.21)** Observations 316 316 R-squared 0.14 0.14 F statistics 2.06 [.0036] 1.81 [.0106] Absolute value of t-statistics in parentheses * significant at 5% level; ** significant at 1% level .

33

Table A5 Equipment Utilisation — Levels and First Difference

K%age Interactions dK%age

Interactions

Moscow reg. 3.016 2.918 9.024 8.932 (0.47) (0.45) (3.30)** (3.25)** St Petersburg -6.827 -6.122 0.255 0.023 (0.97) (0.86) (0.08) (0.01) St Petersburg reg -5.440 -4.731 -3.174 -3.511 (0.44) (0.38) (0.60) (0.66) Nizhny novgorod -2.645 -2.405 0.410 0.198 (0.42) (0.38) (0.15) (0.07) Samara -9.986 -9.652 -1.194 -1.364 (1.40) (1.35) (0.39) (0.45) Ekaterinburg -9.503 -9.451 -2.397 -2.513 (1.50) (1.49) (0.89) (0.92) Perm -4.870 -4.272 1.623 1.314 (0.68) (0.59) (0.53) (0.42) Novosibirsk -3.408 -3.327 0.452 0.119 (0.53) (0.51) (0.16) (0.04) Krasnoyarsk -19.119 -19.388 -2.350 -2.482 (2.70)** (2.73)** (0.77) (0.81) Volgograd -3.847 -3.964 7.042 6.944 (0.35) (0.36) (1.52) (1.49) Chelyabinsk -10.021 -9.715 3.104 2.953 (1.23) (1.19) (0.90) (0.85) Omsk -26.818 -25.581 -7.919 -8.553 (2.87)** (2.67)** (1.99)* (2.09)* Mach. Buil. & Metal. 2.215 2.482 4.160 4.155 (0.44) (0.49) (1.90) (1.88) Wood & paper 5.772 5.776 0.107 -0.004 (0.95) (0.94) (0.04) (0.00) Stone & clay 2.223 2.162 -0.043 -0.149 (0.40) (0.38) (0.02) (0.06) Light ind 0.793 0.355 1.157 1.102 (0.14) (0.06) (0.49) (0.46) Food ind 10.992 10.543 -0.818 -0.812 (1.91) (1.83) (0.33) (0.33) 501-1000 6.225 6.618 0.895 0.873 (1.70) (1.80) (0.57) (0.55) >1000 -0.014 0.417 -3.138 -3.160 (0.00) (0.10) (1.84) (1.84) State share -0.143 -0.022 -0.077 -0.110 (1.31) (0.15) (1.65) (1.73) Med. Dom. Comp. -4.843 -5.096 1.116 0.828 (1.39) (1.35) (0.75) (0.51) Low Dom. Comp. 2.766 4.311 -0.532 -1.297 (0.53) (0.76) (0.24) (0.53) Foreign Comp. -1.664 0.182 -0.888 -1.083 (0.53) (0.05) (0.66) (0.73) For comp*state sh -0.306 0.021

34

(1.31) (0.21) Low Dom comp*state sh -0.231 0.102 (0.76) (0.78) Med Dom comp*state sh 0.054 0.060 (0.18) (0.46) Constant 57.662 56.541 4.618 5.083 (8.62)** (8.31)** (1.62) (1.74) Observations 316 316 314 314 R-squared 0.10 0.11 0.15 0.16 F statistics 1.42 [.0990] 1.34 [.1313] 2.28 [.0009] 2.03 [.0028] Absolute value of t-statistics in parentheses * significant at 5% level; ** significant at 1% level >

35

Table A6 Production Function

Basic model Interactions

lWva lWva

lemp 0.150 0.156

(2.51)* (2.59)*

lWk_n 0.105 0.104

(1.83) (1.81)

Moscow reg. -0.390 -0.403

(1.94) (1.99)*

St Petersburg -0.400 -0.397

(1.74) (1.72)

St Petersburg reg. -0.711 -0.725

(1.66) (1.68)

Nizhny novgorod -0.478 -0.493

(2.41)* (2.46)*

Samara -0.591 -0.599

(2.61)** (2.63)**

Ekaterinburg -0.447 -0.458

(2.23)* (2.26)*

Perm -0.630 -0.648

(2.72)** (2.76)**

Novosibirsk -0.507 -0.533

(2.46)* (2.55)*

Krasnoyarsk -0.697 -0.714

(3.13)** (3.19)**

Volgograd -0.798 -0.807

(2.34)* (2.36)*

Chelyabinsk -0.383 -0.389

(1.49) (1.51)

Omsk -0.840 -0.866

(2.86)** (2.85)**

Mach. Buil. & Metal. -0.304 -0.293

(1.89) (1.80)

Wood & paper -0.287 -0.293

(1.47) (1.49)

36

Stone & clay -0.146 -0.154

(0.82) (0.86)

Light ind. -0.439 -0.451

(2.54)* (2.59)*

Food ind. 0.469 0.463

(2.53)* (2.49)*

State share -0.001 -0.001

(0.18) (0.14)

Med. Dom. Comp. 0.020 -0.017

(0.18) (0.14)

Low Dom. Comp. -0.041 -0.069

(0.25) (0.38)

Foreign comp. 0.030 0.056

(0.29) (0.50)

For comp*state sh -0.006

(0.76)

Low Dom comp*state sh 0.003

(0.33)

Med Dom comp*state sh 0.008

(0.85)

Constant 3.099 3.081

(6.47)** (6.36)**

Observations 303 303

R-squared 0.22 0.22

F( 23, 279) = 3.38 [.0000] 3.02 [.0000]

Absolute value of t-statistics in parentheses

* significant at 5% level; ** significant at 1% level

37

Table A7 Labour Productivity — Levels and First Difference

Ws_n Interactions dWs_n

Interactions

Moscow reg. -56.130 -56.040 0.076 0.080

(1.96) (1.95) (0.74) (0.78)

St Petersburg -49.017 -49.772 -0.159 -0.157

(1.56) (1.57) (1.42) (1.39)

St Petersburg reg. -60.728 -61.177 -0.179 -0.172

(1.00) (1.00) (0.83) (0.80)

Nizhny novgorod -70.083 -70.324 -0.096 -0.091

(2.51)* (2.49)* (0.97) (0.91)

Samara -62.557 -62.903 -0.233 -0.232

(1.95) (1.95) (2.05)* (2.03)*

Ekaterinburg -64.101 -64.132 -0.225 -0.216

(2.26)* (2.24)* (2.23)* (2.13)*

Perm -106.356 -107.067 -0.244 -0.240

(3.32)** (3.29)** (2.11)* (2.06)*

Novosibirsk -87.955 -87.967 -0.267 -0.261

(3.00)** (2.96)** (2.54)* (2.46)*

Krasnoyarsk -110.857 -110.538 -0.421 -0.413

(3.51)** (3.47)** (3.74)** (3.66)**

Volgograd -75.481 -75.303 -0.067 -0.053

(1.56) (1.55) (0.39) (0.30)

Chelyabinsk -76.338 -76.634 -0.171 -0.163

(2.10)* (2.10)* (1.30) (1.23)

Omsk -68.062 -69.277 -0.223 -0.182

(1.63) (1.60) (1.51) (1.19)

Mach. Buil. & Metal. -58.049 -58.332 0.143 0.150

(2.55)* (2.54)* (1.73) (1.80)

Wood & paper -20.390 -20.380 -0.010 0.005

(0.74) (0.74) (0.10) (0.05)

Stone & clay -26.436 -26.277 -0.111 -0.107

(1.05) (1.03) (1.21) (1.16)

Light ind. -64.141 -63.585 0.062 0.076

(2.60)** (2.55)* (0.70) (0.85)

38

Food ind. 169.324 169.792 0.027 0.033

(6.54)** (6.52)** (0.29) (0.36)

501-1000 12.977 12.565 0.037 0.035

(0.79) (0.76) (0.62) (0.59)

>1000 37.667 37.231 -0.007 -0.016

(2.10)* (2.05)* (0.11) (0.24)

State share -0.119 -0.248 -0.002 -0.002

(0.24) (0.38) (1.20) (1.02)

Med. Dom. Comp -14.971 -14.817 -0.072 -0.067

(0.96) (0.87) (1.28) (1.11)

Low Dom. Comp -34.619 -36.056 -0.076 -0.042

(1.44) (1.39) (0.88) (0.46)

Foreign comp. 5.879 3.802 0.023 0.004

(0.41) (0.24) (0.45) (0.07)

For comp*state sh 0.334 0.004

(0.32) (1.03)

Low Dom comp*state sh 0.232 -0.005

(0.16) (0.98)

Med Dom comp*state sh -0.035 -0.001

(0.03) (0.26)

Constant 223.280 224.444 0.678 0.668

(7.46)** (7.35)** (6.33)** (6.15)**

Observations 310 310 307 307

R-squared 0.39 0.39 0.15 0.15

F statistics 7.83 [.0000] 6.86 [.0000] 2.15

[.0021] 1.97 [.0040]

Absolute value of t-statistics in parentheses

* significant at 5% level; ** significant at 1% level

39

Table A8 Return on Equity — Levels and First Difference

ROE Interactions dROE Interactions

Moscow reg. 0.045 0.038 -0.540 -0.355

(0.75) (0.64) (0.15) (0.10)

St Petersburg -0.054 -0.051 -1.100 -0.980

(0.79) (0.74) (0.27) (0.24)

St Petersburg reg -0.044 -0.052 -0.133 0.165

(0.35) (0.42) (0.02) (0.02)

Nizhny novgorod -0.058 -0.065 1.227 1.472

(0.99) (1.10) (0.35) (0.42)

Samara -0.058 -0.063 -2.524 -2.339

(0.86) (0.93) (0.62) (0.57)

Ekaterinburg -0.105 -0.109 -0.321 -0.179

(1.77) (1.83) (0.09) (0.05)

Perm -0.088 -0.099 0.094 0.426

(1.31) (1.46) (0.02) (0.10)

Novosibirsk -0.101 -0.116 -0.982 -0.598

(1.66) (1.88) (0.27) (0.16)

Krasnoyarsk -0.161 -0.170 6.820 7.009

(2.47)* (2.59)* (1.76) (1.80)

Volgograd -0.024 -0.026 -19.580 -19.456

(0.25) (0.27) (3.33)** (3.29)**

Chelyabinsk -0.109 -0.109 0.823 0.886

(1.43) (1.43) (0.18) (0.19)

Omsk -0.255 -0.259 2.883 3.396

(2.99)** (2.94)** (0.57) (0.65)

Mach. Buil. & Metal. 0.015 0.023 1.038 0.985

(0.31) (0.47) (0.36) (0.34)

Wood & paper 0.058 0.058 0.989 1.109

(1.01) (1.01) (0.29) (0.32)

Stone & clay 0.012 0.007 4.923 5.076

(0.23) (0.13) (1.55) (1.59)

Light ind. 0.045 0.040 0.839 0.952

(0.87) (0.77) (0.27) (0.30)

Food ind. 0.119 0.117 -2.910 -2.865

40

(2.15)* (2.11)* (0.88) (0.86)

501-1000 0.058 0.064 -0.280 -0.343

(1.69) (1.85) (0.14) (0.17)

>1000 0.046 0.048 -0.318 -0.372

(1.20) (1.28) (0.14) (0.16)

State share 0.0008 0.0003 0.079 0.100

(0.08) (0.03) (1.31) (1.25)

Med. Dom. Comp 0.016 -0.006 2.148 2.646

(0.48) (0.17) (1.11) (1.26)

Low Dom. Comp -0.007 -0.014 -0.801 -0.277

(0.14) (0.26) (0.27) (0.09)

Foreign comp. 0.026 0.036 -0.140 -0.121

(0.87) (1.11) (0.08) (0.06)

For comp*state sh -0.002 0.019

(1.05) (0.15)

Low Dom comp*state sh 0.001 -0.076

(0.17) (0.41)

Med Dom comp*state sh 0.005 -0.107

(1.63) (0.63)

Constant 0.130 0.136 -1.179 -1.593

(1.98)* (2.04)* (0.30) (0.40)

Observations 291 291 287 287

R-squared 0.12 0.13 0.11 0.11

F statistics 1.61 [.0406] 1.55 [.0467] 1.38

[.1197] 1.23 [.2111]

Absolute value of t-statistics in parentheses

* significant at 5% level; ** significant at 1% level

41

Table A9 Profit/Sales Ratio — Levels and First Difference

P/S Interactions dP/S Interactions

Moscow reg. 0.018 0.017 0.014 0.015

(0.50) (0.47) (0.40) (0.41)

St Petersburg 0.018 0.021 -0.028 -0.026

(0.44) (0.50) (0.71) (0.64)

St Petersburg reg 0.087 0.089 0.025 0.028

(1.12) (1.14) (0.33) (0.37)

Nizhny novgorod -0.003 -0.003 -0.059 -0.057

(0.08) (0.08) (1.67) (1.62)

Samara -0.016 -0.016 0.000 0.001

(0.39) (0.38) (0.00) (0.03)

Ekateringburg -0.024 -0.022 -0.039 -0.035

(0.66) (0.59) (1.10) (0.98)

Perm -0.034 -0.033 -0.008 -0.005

(0.83) (0.79) (0.19) (0.13)

Novosibirsk -0.024 -0.026 -0.030 -0.030

(0.63) (0.68) (0.80) (0.79)

Krasnoyarsk -0.066 -0.067 -0.017 -0.015

(1.63) (1.63) (0.42) (0.39)

Volgograd -0.036 -0.029 -0.013 -0.004

(0.54) (0.44) (0.21) (0.06)

Chelyabinsk -0.008 -0.003 0.019 0.023

(0.16) (0.07) (0.40) (0.50)

Omsk -0.188 -0.170 -0.158 -0.135

(3.50)** (3.08)** (3.02)** (2.51)*

Mach. Buil. & Metal. -0.003 0.002 -0.023 -0.019

(0.10) (0.07) (0.79) (0.63)

Wood & paper -0.016 -0.011 -0.021 -0.015

(0.44) (0.30) (0.60) (0.42)

Stone & clay -0.019 -0.021 -0.023 -0.024

(0.59) (0.64) (0.70) (0.72)

Light ind. -0.025 -0.023 0.002 0.006

(0.79) (0.73) (0.08) (0.21)

Food ind. 0.003 0.002 -0.052 -0.051

42

(0.08) (0.06) (1.57) (1.55)

501-1000 0.051 0.053 0.015 0.016

(2.39)* (2.48)* (0.70) (0.77)

>1000 0.066 0.065 -0.010 -0.012

(2.83)** (2.79)** (0.45) (0.53)

State share -0.0001 0.00003 -0.0003 -0.0001

(0.30) (0.04) (0.57) (0.22)

Med. Dom. Comp 0.017 0.011 -0.005 -0.007

(0.84) (0.50) (0.23) (0.35)

Low Dom. Comp 0.003 0.018 -0.019 0.001

(0.11) (0.55) (0.61) (0.03)

Foreign comp -0.003 -0.001 0.019 0.017

(0.15) (0.02) (1.05) (0.86)

For comp*state sh -0.0003

0.001

(0.24) (0.38)

Low Dom comp*state sh -0.002 -0.003

(1.25) (1.62)

Med Dom comp*state sh 0.001 0.000

(0.67) (0.28)

Constant 0.078 0.073 0.050 0.044

(2.01)* (1.86) (1.33) (1.16)

Observations 306 306 303 303

R-squared 0.14 0.15 0.10 0.11

F statistics 2.01 [.0047] 1.86[.0079] 1.30

[.1643] 1.27 [.1728]

Absolute value of t-statistics in parentheses

* significant at 5% level; ** significant at 1% level

43

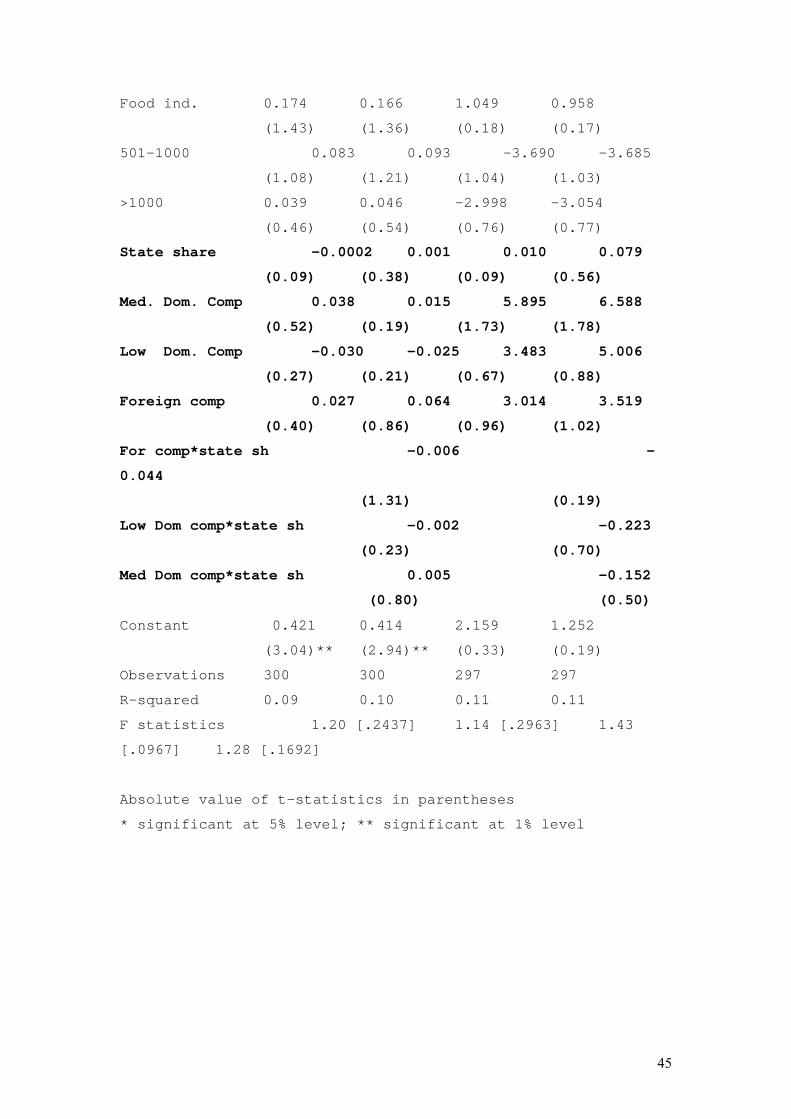

Table A10 Profit/Capital Ratio — Levels and First Difference

P/K Interactions dP/K Interactions

Moscow reg. 0.110 0.102 0.681 0.910

(0.83) (0.77) (0.11) (0.15)

St Petersburg -0.029 -0.014 1.583 2.029

(0.19) (0.09) (0.22) (0.28)

St Petersburg reg -0.063 -0.067 3.379 3.957

(0.23) (0.24) (0.26) (0.30)

Nizhny novgorod -0.046 -0.050 0.898 1.347

(0.35) (0.38) (0.15) (0.22)

Samara -0.189 -0.190 -4.111 -3.752

(1.28) (1.29) (0.60) (0.54)

Ekaterinburg -0.037 -0.042 -5.198 -4.966

(0.28) (0.32) (0.85) (0.81)

Perm -0.042 -0.044 -14.108 -13.406

(0.28) (0.29) (1.99)* (1.87)

Novosibirsk -0.105 -0.120 0.585 1.124

(0.78) (0.88) (0.09) (0.18)

Krasnoyarsk -0.233 -0.245 3.604 3.789

(1.60) (1.68) (0.53) (0.56)

Volgograd -0.130 -0.134 -2.393 -2.065

(0.55) (0.57) (0.22) (0.19)

Chelyabinsk -0.081 -0.080 -0.482 -0.123

(0.49) (0.48) (0.06) (0.02)

Omsk -0.305 -0.299 -3.119 -1.704

(1.59) (1.51) (0.35) (0.19)

Mach. Buil. & Metal. -0.115 -0.103 -1.386 -1.374

(1.09) (0.97) (0.28) (0.27)

Wood & paper 0.033 0.033 -18.992 -18.758

(0.26) (0.26) (3.16)** (3.09)**

Stone & clay -0.180 -0.187 -1.519 -1.427

(1.54) (1.59) (0.27) (0.26)

Light ind. -0.151 -0.164 -2.568 -2.537

(1.32) (1.42) (0.48) (0.47)

44

Food ind. 0.174 0.166 1.049 0.958

(1.43) (1.36) (0.18) (0.17)

501-1000 0.083 0.093 -3.690 -3.685

(1.08) (1.21) (1.04) (1.03)

>1000 0.039 0.046 -2.998 -3.054