central pattana plc. - dcs-digital.com rent % of sales 29% • increase rental rate ... (crc) note...

TRANSCRIPT

Central Pattana Plc.P t D l t d I t tProperty Development and Investment

Analyst Briefing22 May 2014

CentralFestival Samui

Disclaimer

The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for share in Central Pattana Public Company Limited (“CPN” and shares in CPN, “shares”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever.

This presentation may include information which is forward-looking in nature. Forward-looking information involve known and unknown risks, uncertainties and other factors which may impact on the actual outcomes, including economic conditions in the markets in which CPN operates and general achievement of CPN business forecasts, which will cause the actual results, performance or achievements of CPN to differ, perhaps materially, from the results, performance or achievements expressed or implied in this presentation.

This presentation has been prepared by the CPN. The information in this presentation has not been independently verified. Norepresentation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the CPN or any of its agents or advisers, or any of their respective affiliates, advisers or representatives, shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

This presentation is made, furnished and distributed for information purposes only. No part of this presentation shall be relied upon directly or indirectly for any investment decision-making or for any other purposes.

This presentation and all other information, materials or documents provided in connection therewith, shall not, either in whole or in part, be reproduced, redistributed or made available to any other person, save in strict compliance with all applicable laws.

2Note: All currency figures within this presentation are presented in Thai Baht unless otherwise stated.

Agenda

► 1Q14 Overview

► Operational Performance

► Future Developments

► Financial Performance

► Future Developments

► Appendix

3

1Q14 Overview Grand Opening of CentralFestival Samuion 29 March 2014

Operations

o CentralFestival Samui was launched on 29 March 2014. with a 70% of occupancy rate on the opening date.

on 29 March 2014

o Total net leasable area (NLA) in 1Q14 was 1,177,416 sq.m. with an average occupancy rate of 95% both in Bangkok metropolitan area (BMA) and in provinces.

o 1Q14 same store effective rental rate achieved +4.5% growth YoY. (1)

Financial Highlights

1Q14

o Revenues +8% YoY

Operating profit +4% YoYo Operating profit +4% YoY

o Net profit +3% YoY

o Revenues (on same store basis) -5% YoY (2)

o Net D/E 0.45 time

Note 1: Excludes CentralWorld, CentralPlaza Ubonratchathani, CentralFestival Chiangmai and CentralFestival Hatyai. CentralFestival Samui.Note 2. Excludes CentralPlaza Ubonratchathani, CentralFestival Chiangmai and CentralFestival Hatyai. CentralFestival Samui. Same store revenue growth would have been +5% if excluded discounts given at CTW in 1Q14 together with backdated service income and the raise of service charged from tenants in 1Q13.

4

Operational Performance

5

Property Locations

Shopping Centers (10 BMA, 14 Provinces)

1 (BMA) Pure-managed (CPNRF)

Equity-owned (CPN)Existing Projects (24)

1 (BMA)

18 (9 BMA, 9 Provinces)

4 (Provinces)

1 (Province)centralcenter

g ( )

Under construction

Offices (7)

Hotels (2)

1 (Province) centralcenter

Bangkok Metropolitan Area (BMA)

Residences (2)

Shopping Centers (5 Domestic, 1 Overseas)

New Projects (6)Residences (2)

3 (BMA: Bangyai, East Ville and Salaya)

2 (Provinces: Rayong, and Nakhonratchasima)

1 (Overseas: Malaysia)

Asset Enhancements (2)Groove@CentralWorld (Expansion)

CentralPlaza Bangna (Renovation and remerchandising mix phase by phase)

6Note: As of 31 March 2014.

Leasable Area and Occupancy: Retail

As of 1Q14, CPN owns 24 premium shopping centers with average occupancy rate of 95%.

Occupancy Rate (2)Net Leasable Area(1) (sq m )Land

Freehold Leasehold Retail Department Store Total 1Q14 4Q13 1Q13

CPN in BMA 10 4 6 515,281 63,583 578,864 96% 97% 96%

No. of Projects

Occupancy Rate ( )Net Leasable Area( ) (sq.m.)Retail Properties

Land

CPN in Provinces 14 11 3 544,161 54,391 598,552 94% 97% 97%

Total Retail Properties(3) 24 15 9 1,059,442 117,974 1,177,416 95% 97% 97%

Breakdown by Rental Income Breakdown by NLA Breakdown by no. of Shopping Malls

Provincial42%

BMA55%

Provincial 45% BMA

49%Provincial

51%

BMA 10Provincial

14

7Note 1: Excludes rental agreements < 1 year, such as kiosk, carts, ATMs and coin machines. Note 2: Percentage based on leasable area. Note 3: Excludes areas transferred to CPNRF.

Leasable Area and Occupancy: Non-core Properties

Office, residential property and hotel are considered non-core businesses, complementing shopping center business and adding value to the overall project.

Net Leasable Area (sq m ) Occupancy Rate (2)Net Leasable Area (sq.m.)

orNo. of Units or Room(1) 1Q14 4Q13 1Q13

Offi i BMA(3) 5 55 102 98% 96% 95%

Non-core Properties No. of Projects

Occupancy Rate

Office in BMA(3) 5 55,102 98% 96% 95%

Residential in BMA 2 6,373 sq.m. or 61 units 70% 68% 67%

Hotel in provincial area(4) 2 561 rooms 77% 76% 81%

Revenue Breakdown

p

Office 2%

Retail

F&B 4%

Hotel 4%

Management83%

Management fee 2%

Other income 5%

8Note 1: Excludes storage.Note 2: Percentage based on leasable area.Note 3: Excludes areas transferred to CPNRF and CPNCGNote 4: Outsource the management, Pattaya (302 rooms) managed by Hilton and Udonthani (259 rooms) managed by Centara.

Occupancy rate of Hotel Business was an average of 3 months (January – March).

Rental Contract Type : By Area

• Tenants: food centers, cineplexand international brands such as

(up to 3 years)Monthly basis collection

(up to 3 years)Monthly basis collection

“McDonalds”, “KFC”• Range of percentage: 10% - 30%

of sales• With minimum guarantees

Fixed Rent

% of Sales29%

• Increase rental rate approx 5% p.a.

• Approx. 1/3 of rental contract expired every year

(up to 3 years)

Long-term Lease22%

Fixed Rent49%

expired every year

(up to 30 years)Up-front collection

• Up-front payment – realize throughout lease contract period on straight-line basis p g

Note: In addition to space rental fee, service p ,& utility fees are collected on a monthly basis

9Note: Percentage based on occupied area. Source: Company estimate as of 31 March 2014.

Effective Rental Rate (1)

Overall effective rental rate declined in 2009 – 2011 from new malls in provinces. 1Q14 same store rental grew by 4.5% YoY.

Same Store Rental Rate of Bangkok Malls(2)

1,616 1,665

1 600

1,800 (Bt/sq.m./mth)

1,447 1,499 1,484 1,455

1,519 1,600 (Bt/sq.m./mth) Same Store Rental

1,000

1,200

1,400

1,600

1,274 1,254 1,225 1,248 1,200

1,400

600

800

1,000

1Q13 1Q14

1,268 1,347 1,400

(Bt/sq.m./mth)800

1,000

2008 2009 2010 2011 2012 2013 1Q14 1Q13 1Q14

Same Store Rental Rate of Provincial Malls(2)

1,000

1,200

All Projects Malls excluded:

• CentralPlaza Ubonratchathani

600

800

1Q13 1Q14

• CentralFestival Chiangmai

• CentralFestival Hatyai

• CentralFestival Samui

• CentralWorldQ Q

10Note 1: The figures are effective rental rates for retail tenants (occupied space < 1,000 sq.m.) and net of special rental discounts.Note 2: Excludes CentralPlaza Ubonratchathani, CentralFestival Chiangmai, CentralFestival Hatyai, CentralFestival Samui, and CentralWorld.Source: Company estimate as of 31 March 2014.

Expiration of Long-term Lease Contracts(1)

Long term lease contract will be expired in each of the following years. This area will be converted to a short term contract at market rental rate which could increase the company’s revenues.

The expiration area(2)

and expiration period are shown below :

60%

26%40%

50%

20%

30% Anchor

Retail

3%

12%

2% 2% 2%4%

24%10% 14%

10%

4%0%

2014 2015 2016 2017 2018 2019 2020 ≥ 2021

11(1) Source: Company estimate as of 31 December 2013.(2) Total lease area is 192,118 sq.m. with less than 4% rental income contribution.(3) In 2015, area excludes Big C at Central Center Pattaya. The upside from short-term contract renewal is subject to the renewal of the land lease ofCentral Center Pattaya .

Future Developments

12

Domestic Expansion Net Leasable Area(sq.m.)

New Retail Properties in BMA 3 143,400

Project under construction No. of Projects

New Retail Properties in Provinces 2 88,000Total Retail Properties(3) 5 231,400

BMA PROVINCES

20142015

CentralPlaza Salaya (BMA)NLA: 33,900 sq.m.Opening in 3Q14

CentralPlaza Rayong (East)NLA: 33,000 sq.m.Opening in 2Q15

CentralPlaza Nakhonratchasima(Northeast)CentralWestGate (Bangyai)

2015 2016

(Northeast)NLA: 55,000 sq.m.Opening in 2Q16

( gy )(BMA)NLA: 75,000 sq.m.Opening in 2Q15

CentralFestival East Ville (BMA)

13Source: Company estimate as of 31 March 2014.

NLA: 34,500 sq.m.Opening in 4Q15

New Projects in Thailand (Open in 2014 - 2015)

CentralWestGateCentralPlaza RayongCentralPlaza Salaya

Investment Cost(1) 2,500 Bt. mil 2,400 Bt. mil 6,400 Bt. mil

Net Leasable Area(2) 33 900 sq m 33 000 sq m 75 000 sq mNet Leasable Area( ) 33,900 sq.m. 33,000 sq.m. 75,000 sq.m.

Parking 1,600 cars 1,500 cars 2,000 cars

Joint Developer(3) Central Department Store Robinson Department Store Central Department Store

Land Size(4) 70 i 60 i 100 iLand Size(4) 70 rais 60 rais 100 rais(Freehold & Leasehold) (Freehold) (Leasehold)

Location Nakornpathom Rayong Bangyai, NonthaburiOpening (tentative) Aug-14 2Q15 2Q15p g ( ) g

Note 1: Includes land and construction cost of shopping center and parking building. Excludes those of Central Department Store or Robinson Department Store (CRC)Note 2: Excludes CRC’s area.Note 3: Area will be developed and owned by the joint developer. However the store will serve as a magnet to draw traffic into CPN’s plaza area.Note 4: 1 rai = 1,600 sq.m.

14

New Projects in Thailand (Open in 2015 - 2016)

CentralPlaza NakhonratchasimaCentralFestival East Ville

Investment Cost(1) 3 200 Bt mil 4 000 Bt milInvestment Cost 3,200 Bt. mil 4,000 Bt. mil

Net Leasable Area(2) 34,500 sq.m. 55,000 sq.m.

Parking 1,900 cars 3,000 cars

Joint Developer(3) Central Department Store Central Department StoreJoint Developer( ) Central Department Store Central Department Store

Land Size(4) 51 rais 52 rais(Freehold & Leasehold) (Freehold)

Location Ekkamai- Ramintra NakhonratchasimaOpening (tentative) 4Q15 2Q16

Note 1: Includes land and construction cost of shopping center and parking building. Excludes those of Central Department Store or Robinson Department Store (CRC)Note 2: Excludes CRC’s area.Note 3: Area will be developed and owned by the joint developer. However the store will serve as a magnet to draw traffic into CPN’s plaza area.Note 4: 1 rai = 1,600 sq.m.

15

Overseas Expansion

South East Asia in FocusInvestment Strategies:■ Joint venture with local partners focus on retail properties

Completed JV Agreement

Potential Locations

■ To be a property manager

Thailand

Malaysia

Malaysia

VietnamShah Alam, Selangor

Malaysia

Indonesia

16

New Project in Malaysia

CentralPlaza i-City

Investment Cost ( 1 ) 5,800 Bt. mil Joint venture i-City Properties Sdn Bhd (“ICP”), an I-Berhad wholly-own subsidiaryJoint venture i City Properties Sdn Bhd ( ICP ), an I Berhad wholly own subsidiary

CPN holds 60% stake and ICP holds 40% stakeCPN will lead in the development and management of the shopping mall

Program: Shopping Center 89,700 sq.m. (NLA includes department store)L d Si 11 12 27 5 iLand Size 11.12 acres or 27.5 raisLocation i-City, Shah Alam, Selangor Darul Ehsan, MalaysiaOpening (Tentative) 4Q2016

17Note 1: Includes land and construction cost of shopping center and parking building.

Assets Enhancement

Groove@CentralWorld CentralPlaza Bangna

Groove@CentralWorld CentralPlaza BangnaGroove@CentralWorld CentralPlaza Bangna

Investment Cost 600 Bt. mil 1,400 Bt. milNet Leasable Area 7,500 sq.m. 62,000 sq.m.

( Incremental NLA 4 000 sq m ) ( Incremental NLA 4,000 sq.m.)Type Expansion Renovation and remerchandising

mix phase by phaseOpening (tentative) Dining Zone: Dec-13 Jul-14

Fashion Zone: May-14

18

Future Leasable Area & Occupancy Rate

97% 98% 96% 95% 96% 97% 96% 97% 96% 95%

90%

100%

1 600 000

1,800,000

Retail NLA (sqm)

70%

80%

90%

1 200 000

1,400,000

1,600,000

50%

60%

70%

800 000

1,000,000

1,200,000

40%

50%

600,000

800,000

2007

2008

2009

2010

2011

2012

2013

014F

015F

016F

2 2 2 2 2 2 2 20 20 20

Under study projects Under developing projects Exisitng projects % Occupancy (RHS)

Assets under management 2007 2008 2009 2010 2011 2012 2013 2014F 2015F 2016F No of project 10 11 15 15 18 20 23 25 28 33No.of project 10 11 15 15 18 20 23 25 28 33 Retail space (NLA in sqm) 697,038 761,111 967,430 964,612 1,059,910 1,121,377 1,286,125 1,354,125 1,494,125 1,686,825 Office space (NLA in sqm) 144,791 144,280 163,746 163,991 175,831 169,133 169,152 169,152 169,152 169,152 Hotel (rooms) 255 557 561 561 561 561 561 561 Residential (units) 61 61 61 61 61 61 61 61 61 61

19Source: Company estimate as at 31 December 2013.Retail space: Includes leasable area of CentralPlaza Rama 2, CentralPlaza Rama 3, and CentralPlaza Pinklao which were partially transferred to CPNRF, but still under CPN’s management.Office space: Includes leasable area of The Office @CentralWorld which was transferred to CPNCG, but still under CPN’s management.

Capital Expenditure(Bt.m

Major capital expenditure will be used to develop new projects. Financing plan for future expansion includes: cash flow from operation, bond issuance and/or project finance, and property fund vehicle.

(Bt. mil)

Actual EstimatesCPN' P j t 2013 2014 2015 2016

(Bt.mil)CPN's Projects 2013 2014 2015 2016 Under-construction Projects 9,163 7,962 3,883 1,599 Enhancement Projects 1,818 2,277 1,200 1,200 Potential Projects 764 5,757 10,771 13,666 Total CAPEX 11,745 15,996 15,854 16,466

20Source: Company estimate as of 31 December 2013.

Financial Performance

21

(Bt.mil)

Financial SummaryR i f C t lW ld

17,687

21,234

18 000

20,000

22,000

24,000

6-mth Closure of CentralPlaza Lardprao

• Reopening of CentralWorld• Relaunch of CentralPlaza Udonthani

11,755 11,38812,766

10 000

12,000

14,000

16,000

18,000 6-mth Closure of CentralWorld

5,634

3,1122,442 2,620

5,5907,345

2,1091 710

4,952

1 1252,058

6,189 6,293

1,7102 000

4,000

6,000

8,000

10,000

2,292 1,552 1,871 4,4135,991 1,7101,125 ,

0

2,000

2009 2010 2011 2012 2013 1Q14Total revenues Operating profit Net profit Net profit (Inc. non-recurring)

% YoY Growth 2009 2010 2011 2012 2013 1Q14Total revenues /1 27% (3%) 12% 39% 20% 8% Operating profit 4% (22%) 7% 113% 31% 4% Net profit 6% (32%) 21% 136% 36% 3% Net profit (inc non recurring) (77%) 83% 201% 2% 3%

Same store revenue growth would have been +5% if excluded discounts given at CTWNet profit (inc. non-recurring) (77%) 83% 201% 2% 3%

Same store revenue growth 5% 0% 9% 29% 12% (5%)

Gross Profit Margin (%) /2 43% 39% 39% 47% 50% 52%EBITDA Margin (%) /2 44% 42% 43% 50% 51% 55%

discounts given at CTW in 1Q14 together with backdated service income and the raise of service charged from tenants in 1Q13.

22Note 1: Total revenue includes rental & service, hotel operation, food & beverage, and other incomes.

Excl. interest income, share of profit from investment and reversal of impairment.Note 2: Excl. non-recurring items i.e. reversal of impairment but incl. other income .

EBITDA Margin (%) 44% 42% 43% 50% 51% 55%

Revenue Breakdown

17,687

21,234 20,000

24,000

(Bt.mil)Total revenues /1 +8% YoY or +423 Bt.mil YoY mainly driven from rent and services.Rent and services +8% YoY

• The full-quarter realization of three new

12,765

5 789 5 6348,000

12,000

16,000 The full quarter realization of three new projects launched in 2013 i.e. CentralPlazaUbonratchathani, CentralFestival Chiangmai, and CentralFestival Hatyai

• Same store revenue dropped 5% YoY.

+8% YoY-3% QoQ

5,211 5,789 5,634

0

4,000

,

2011 2012 2013 1Q13 4Q13 1Q14

Hotel +5% YoY• Higher Rev/Par of both hotels, especially at

Hilton Pattaya Hotel together with a slightly higher occupancy

Retail Office F&B Hotel Other income Management fee

FY13 Revenue breakdown

F&B sales +13% YoY• Contributions from the new food courts at the

CentralPlaza Ubonratchathani, CentralFestivalChiangmai and CentralFestival HatyaiChiangmai, and CentralFestival Hatyai.

Retail 83%

Office 2%

F&B 4%

Hotel 4%Hotel 4%

Management fee 2%

Other income 5%

23Excludes non-recurring income.Note 1: Includes revenues from residential projects and water & amusement park, and property management fees from CPNRF & CPNCG.

(Bt il)

Costs Breakdown

7 783

9,434 10,542

10,000

12,000 (Bt.mil)

Total Costs +9% YoY or +231 Bt.mil YoY.

Rent and Services 10% YoY• A rise in costs incurred by three newly opened

malls in 2013 including CentralFestival Samui7,783

4 000

6,000

8,000 malls in 2013 including CentralFestival Samuiwhich has recently opened in March 2014.

Hotel Business +3% YoY• Despite a 5% increase q-o-q in revenue given

that the supplies cost was lowered by 4 MB in

+9% YoY-3% QoQ

2,492 2,821 2,723

0

2,000

4,000

2011 2012 2013 1Q13 4Q13 1Q14

pp y1Q14 over the last quarter

F&B +8% YoY• Change in costs reflected the growth in food

and beverage sales.2011 2012 2013 1Q13 4Q13 1Q14

Retail Office F&B Hotel Others

FY13 Cost breakdown

• Increased costs incurred from new food courts launched in 2013.

Retail

Office2%

F&B6%Retail

89%6%

Hotel3%

24Note: Excludes non-recurring items.

SG&A Expenses Breakdown

2 4102,741

3,446

3,000

3,500

(Bt.mil) SG&A expenses +13% YoY or +92 Bt.mil YoYdue mainly to administrative expenses of three newly opened malls including additional personnel expense to cater for business expansion+13% YoY2,410

959 1,201

1,000

1,500

2,000

2,500 13% YoY

-33% QoQ

807

0

500

2011 2012 2013 1Q13 4Q13 1Q14

Personnel Advertising & promotion Depreciation Others

FY13 SG&A breakdownAdvertising

Personnel46%

g& Promotion

18%

DepreciationDepreciation18%

Others22%

25Note: Excludes non-recurring items.

Debt AnalysisAA- Credit Rating

Upgraded to “AA-” ratings with “Stable” outlook by TRIS Rating in 12 May 2014

All borrowings are denominated in THB

Outstanding Borrowings 19,787 Bt.mil Fixed vs. Floating Interest Rate Mix

Long-term loan24% Sh

All borrowings are denominated in THB.

24% Short-term loan28%

Long-term bond42%

Fixed89%

Floating11%

Financing Cost

Short-term bond6%

874 1,057

8134.7% 4.4% 4.3%

4.4%

4.3% 4.4% 4.3% 4 0%

5%

6%

1,000

1,200

(Bt.mil)

745 688

813

216

4.0%

2%

3%

4%

400

600

800

216 156 179

0%

1%

0

200

2009 2010 2011 2012 2013 1Q13 4Q13 1Q14

26Note: Weighted average interest rate was derived from interest expenses including interest capitalization for projects under development.

Interest expenses Weighted average cost of debt (RHS)

Capital Structure

CPN’s net D/E stood at 0.45 times, against its debt covenant of 1.75 times.

(Times)(Bt.mil)

25 900

36,824 38,564

1.20

1.40

30 000

35,000

40,000

( )

16,669 19,085

25,245 25,568

19,842 19,787 19,008 18,918 20,448

25,900

1.19 0.82 0 60

0.80

1.00

20,000

25,000

30,000

2 541 1 6324,207

1 869 2 279

0.74 0.92

1.19

0.49 0.45

0.20

0.40

0.60

5,000

10,000

15,000

2,541 1,632 945 1,869 2,279

0.000 2009 2010 2011 2012 2013 1Q14

Cash & current investment Interest bearing debts Equity Net D/ECash & current investment Interest bearing debts Equity Net D/E

27

Key Trading Statistics and Dividend

Dividend Key Trading Statistics

Key Metrics THB Key Metrics 2013 2012 2011 2010 2009 2008

Par Value 0.50

Stock Price 47.00

EPS 0 38

Par Value (THB) 0.50 0.50(3) 1.00 1.00 1.00 1.00

Dividend (THB/Share)

0.55 0.475 0.37 0.25 0.58 0.33

Dividend Paid 2 468 2 070 806 545 1 264 719EPS 0.38

P/E (x)(1) 33.52

Market Capitalization (Bt. bn) 211

Dividend Paid(Bt. mil)

2,468 2,070 806 545 1,264 719

Dividend Payout Ratio

39.2% 33%(2) 39% 48% 25%(1) 33%

Dividend policy is paid annually not less than 40% of net profit (unless there is

compelling reason against this).

Note 1: Dividend payout ratio of 25% in 2009 was derived from 40% of normal net profit and 14% of

Market Capitalization (Bt. bn) 211

Authorized Share Capital (mil. shares) 4,488

Note 1: Bloomberg’s consensus as of 31 March 2014.

gain from transferring assets into CPNRF.

Note 2: Dividend payout ratio of 33% in 2012 was derived from 40% of normal net profit and 17% of

gain from transferring assets into CPNCG.

Note 3 Par spilt to THB 0 50 per share effecti e on 7 Ma 2013

g

Note 3: Par spilt to THB 0.50 per share effective on 7 May 2013

28

Appendix

29

Statement of Financial Position

Current assets

Financial position (MB) 1Q14 % Change4Q13

Current assets

Cash and current investments 1,869 2,279 22%

Other current assets 3,630 3,302 (9%)

Total current assets 5 499 5 581 1%Total current assets 5,499 5,581 1%

Non-current assets

Investment properties (2) 53,575 55,017 3%

Leasehold rights 11 457 11 594 1%Leasehold rights 11,457 11,594 1%

Property & equipment (PP&E) 2,353 2,297 (2%)

Other non-current assets 4,655 4,658 0%

T t l N t t 72 040 73 565 2%Total Non current assets 72,040 73,565 2%

Total assets 77,539 79,146 2%

Current liabilities 15,458 15,703 2%

Non-current liabilites 25,257 24,879 (1%)

Total liabilities 40,715 40,582 (0%)

Total equities 36,824 38,564 5%

30Note1: Investment Properties are booked at cost and depreciated with the straight-line basis over the life of the assets. The estimated fair value is 115,803 Bt.mil

(2012 : 89,402 Bt.mil ), stated in the disclosure notes to the main financial statement no. 14 under “Investment Properties”.

Statement of Comprehensive Income1Q13 4Q13 1Q14 % YoY % QoQ

Change Change

Revenue from rent and services 4,424 4,829 4,793 8% (1%)

Retail 4,326 4,726 4,691 8% (1%)

Consolidated earnings (MB)

, , , ( )

Office 93 98 98 6% 0%

Other supportive businesses 5 5 4 (6%) (4%)

Revenue from hotel operation 244 244 255 5% 5%

Revenue from food and beverage 200 247 225 13% (9%) Revenue from food and beverage 200 247 225 13% (9%)

Other income(1) 344 469 361 5% (23%)

Total revenues 5,211 5,789 5,634 8% (3%) Cost of rent and services 2,250 2,552 2,466 10% (3%)

Retail 2,196 2,492 2,416 10% (3%)

Office 50 50 46 (7%) (8%)

Other supportive businesses 4 10 4 (10%) (63%)

Cost of hotel operation 78 81 80 3% (2%) Cost of hotel operation 78 81 80 3% (2%)

Cost of food and beverage 164 187 177 8% (5%)

Total costs 2,492 2,821 2,723 9% (3%)

Operating profit(1) 2,026 1,783 2,109 4% 18%

N t fit 1 656 1 750 1 710 3% (2%)Net profit 1,656 1,750 1,710 3% (2%) Normalized net profit 1,656 1,373 1,710 3% 25%

EPS (Bt) excluding non-recurring items(2) 0.37 0.31 0.38 3% 25%

31(1) Excluding other income from the reversal of allowance for impairment of assets(2) Number of shares used to calculate EPS is 4,488,000,000 shares, which is the number after the par split and the capital increase.

Operational Performance: CPNRF and CPNCG

In 1Q14, CPN Retail Growth Leasehold Property Fund (“CPNRF”) had three shopping centers and two office towers. In Sep12, CPN Commercial Growth Leasehold Property Fund (“CPNCG”) was launched and currently owns one office.

CPNRF d CPNCG d b SCB A t M t F d M Th i tiCPNRF and CPNCG are managed by SCB Asset Management, Fund Manager. Their properties are managed by CPN, Property Manager.

CPNRF P ti R i i Lif L bl A (1) Occupancy Rate (2)CPNRF Properties Remaining Life(years)

Leasable Area(1)

(sq.m.)Occupancy Rate (2)

1Q14 4Q13 1Q131. Rama 2 (Retail) 12 Years 87,691 96% 96% 99%

2. Rama 3 (Retail) 83 Years 37,255 96% 98% 98%

3 Pi kl (R t il) 11 Y 21 730 99% 100% 97%3. Pinklao (Retail) 11 Years 21,730 99% 100% 97%4. Pinklao Tower A & B (Office) 11 Years 33,760 97% 98% 97%

Total 180,436 97% 98% 98%

CPNCG Office Property Remaining Life(years)

Leasable Area(1)

(sq.m.)Occupancy Rate (2)

1Q14 4Q13 1Q13

CentralWorld (Office) 19 Years 80,585 100% 99% 99%

32Note 1: Includes rental agreements < 1 year such as kiosk, carts, ATMs and coin machines and CPN acts as the property manager.Note 2: Percentage based on leasable area.

CPN Retail Growth Leasehold Property FundCPN Retail Growth Leasehold Property Fund1st Quarter 2014 Financial Results22nd May 2014

1

Important Notice

The information contained in this presentation is for information purposes only and does not constitute an ff i it ti t ll th li it ti f ff i it ti t h b ib f it i CPN offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for units in CPN

Retail Growth Leasehold Property Fund (CPNRF and units in CPNRF, “Units”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever.

This presentation may include information which is forward-looking in nature Forward-looking information This presentation may include information which is forward looking in nature. Forward looking information involve known and unknown risks, uncertainties and other factors which may impact on the actual outcomes, including economic conditions in the markets in which CPNRF operates and general achievement of CPNRF business forecasts, which will cause the actual results, performance or achievements of CPNRF to differ, perhaps materially, from the results, performance or achievements expressed or implied in this presentation.expressed or implied in this presentation.

This presentation has been prepared by the CPNRF Property Manager. The information in this presentation has not been independently verified. No representation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the CPNRF Property Manager or CPNRF Fund Manager or any of i i f i i ffi i i i i i iits agents or advisers, or any of their respective affiliates, advisers or representatives, shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

This presentation is made, furnished and distributed for information purposes only. No part of this presentation shall be relied upon directly or indirectly for any investment decision-making or for any other presentation shall be relied upon directly or indirectly for any investment decision-making or for any other purposes.

This presentation and all other information, materials or documents provided in connection therewith, shall not, either in whole or in part, be reproduced, redistributed or made available to any other person, save in strict compliance with all applicable laws.

2

Contents

Page

1. Operations 5

2. Financial Highlights 10

3. Q&A

3

1. Operations1. Operations

Leasable Area and Occupancy

Occupancy rate of CPNRF Portfolio slightly decreased QoQ

Area (sqm) Occupancy Rate/1

Gross Area LeaseableArea

Number of Tenants/2 30 Jun 13 30 Sep 13 31 Dec 13 31 Mar 14

Rama 2 251,182 87,691 312 95.2% 95.3% 95.9% 96.1%

Rama 3 169,740 37,255 250 97.3% 97.0% 97.7% 96.7%

PinKlao (Plaza) 135,018 21,730 115 99.2% 99.1% 100.0% 99.0%

Pinklao Office Tower A&B 50,653 33,760 103 98.5% 97.6% 98.1% 97.5%

Total 606,593 180,436 780 96.7% 96.5% 97.2% 96.8%

Source: CPN Note:/1 Anchor and shop tenants only/2 Number of tenants excluding those with long-term lease with upfront rent, kiosks, carts, ATMs and coin machines as at 31 March 2014

5

New and Renewed Lease Profile

Rental rates for the 3 malls have continued to grow by 5.9%

From 1 January to 31 March 2014/1

Renewal and New Leases/1Increase / (Decrease) in

Rental Rate (p a )/3N f L A ( ) % f T t l/2 Rental Rate (p.a.)/3No. of Leases Area (sqm) % of Total/2

Rama 2 8 1,763 2.0% 6.6%

Rama 3 12 1,853 5.0% 4.9%

Pinklao (Plaza) 7 716 3.3% 4.5%

Pinklao Office Tower A & B 1 262 0.8% 12.2%

Total 28 4 594 2 5% 5 9%

Source: CPN

Total 28 4,594 2.5% 5.9%

Note:/1 Exclude rental agreements < 1 year/2 Percentage of leasable area as at 31 March 2014/3 Exclude rental agreements with revenue sharing clause

6

Lease expiry profile

Well balanced lease expiry profile

53%

50%

60%

23%

33%

17%

27% 27%22%

32%28%

40%

31%

24%26%

% 16%20%

30%

40%

Central Department

14%9% 7%

17%

0%

8%

1%

16%

0%

16%

0%

10%

20%

Apr Dec2014 2015 2016 2017 - 2024

Department Store lease expiring 2025

CDS 2025

Source: CPNNote:

Apr -Dec2014 2015 2016 2017 - 2024Rama II Rama III Pinklao (Plaza) Pinklao Office Tower A & B Total Portfolio

Note:1. Percentage of total occupied area as at 31 March 20142. Exclude rental agreements < 1 year

7

Rental Structure Profile

100%

72%

93%100%

70%80%90%

100%

d A

rea

52% 48%

28%

20%30%40%50%60%

% o

f Occ

upie

d

7%0%

0%10%20%

Rama II Rama III Pinklao (Plaza) Pinklao Office Tower A & B

Fi d R t % f S l R t

Note:

Fixed Rent % of Sales Rent

Note: 1. % of total occupied area excluding those with long-term lease with upfront rent as at 31 March 20142. % of total number of tenants excluding those with long-term lease with upfront rent, kiosks, carts, ATMs and coin machine as at 31 March 2014

8

2 Financial Highlights2. Financial Highlights

Income breakdown : 1Q14

Good performance across the three assets maintains both QoQ and YoY growths for the Fund

Fund's other income5%

Rama 239%

Rama 3

Pinklao33% THB 699mn, +1% QoQ and +7% YoY

Rama 323%

10

Profit & Loss

Net Investment Income slightly increased by 5% QoQ and 8% YoY

Unit : Baht Million 1Q14 4Q13 QoQ 1Q13 YoY

Property level

Total income 698 691 +1% 651 +7%

T t l (38) (56) 32% (40) 4%Total expenses (38) (56) -32% (40) -4%

Property management fees (86) (87) -1% (81) +7%

Net income from property level 574 548 +5% 531 +8%

Fund levelu d e eOther income 1 3 -60% 6 -79%

Fund management fee and etc. (7) (7) +1% (6) +5%

Interest expenses (4) (5) -12% (6) -24%

Net investment income 564 540 +5% 525 +8%

Net realised (loss)/gain on investments 2 (0) - - -100%

Net unrealised (loss) gains from investment 286 484 -41% (369) -

Net increase in net assets 851 1 023 17% 156 +446%Net increase in net assets 851 1,023 -17% 156 +446%

11

Balance Sheet

Unit : Baht Million except indicated Mar-14 Dec-13 QoQ

Investments in properties at fair value 18,830 18,535 +2%

Cash and near cash 996 995 +0%

Other assets 258 250 +3%

Total Assets 20,084 19,780 +2%

A/P and accrued expenses 99 99 -0%

Deposits received from customers 800 802 -0%

Loan from SCB 305 340 -10%

Other liabilities 202 712 -72%

Total Liabilities 1,406 1,953 -28%

C it l i d f ith ld 16 963 15 764 8%Capital received from unitholders 16,963 15,764 8%

Retained earnings 1,715 2,063 -17%

Net Asset Values 18,678 17,827 +5%

NAV per unit (Baht) 11 4144 10 8942 +5%NAV per unit (Baht) 11.4144 10.8942 +5%

12

Distribution Summary

Interim Dividend (16 Dec – 31 Mar 2014)(DPU of Bt 0.3600)

Unit : Baht Million except indicated 1Q14 4Q13 QoQ 1Q13 YoY

Net investment income 564 540 +5% 525 +8%

Actual distribution

via Dividend 589/2 491/1 +20% 483 +22%

Baht per unit 0.3600 0.3000 +20% 0.2949 +22%

via Par Reduction - - - - -

Baht per unit - - - - -p

Total distribution 589 491 +20% 483 +22%

Baht per unit 0.3600 0.3000 +20% 0.2949 +22%

% of Net investment income 104% 91% +13.5% 92% +12.4%

A li d di t ib ti i ld /2 9 2% 7 7% 1 5% 7 6% 1 7%

/1 Dividend paid from operating profit period from 1 Oct 2013 – 15 Dec 2013 /2 Dividend paid from operating profit period from 16 Dec 2013 – 31 Mar 2014/2 Based on unit price of 15.60 Baht as at 19 May 2014 (For the current quarter and next 9 months)

Annualised distribution yield /2 9.2% 7.7% +1.5% 7.6% +1.7%

p y ( q )

13

Shareholder Structure and Dividend

Dividend Policy• 4 times a year

Listed on the SET 23 August 2005 Units Outstanding 2,212.5M Units

DPU

4 times a year• Pay out a minimum of 90% of distributable income

Units Outstanding 2,212.5M UnitsRegistered Fund Size Baht 24,406.2M NAV (Mar 2014) Baht 11.4144

Unitholders Information(as at 21st Nov 2013) 0.8716 0.9201 0.9910 1.0230 1.1289 1.2283/1

Y2008 Y2009 Y2010 Y2011 Y2012 Y2013 1Q14 (Interim Div)

0.3600/2

THAI 88.03%

CPN 27.91%

Institution 20.35%

Individual 39.77%

FOREIGN 11 97%2008 2009 2010 2011 2012 2013/2 1Q14/4

Note: /1 2013 dividend for operating period from 1Jan - 15 Dec 2013/2 Dividend for operating period 16 Dec 2013 – 31 Mar 2014

FOREIGN 11.97%

Institution 11.93%

Individual 0.04%

Annualized Yield/3 11.17% 9.95% 8.26% 7.75% 5.94% 7.82% 8.40%

14

/3 Based on unit price as at the end of each period (For the previous 12 months)/4 Based on unit price as at 31 Mar 2014 (From 1 Jan - 31 Mar 2014)

0.04%

CPNRF Fund Structure

Land Owner Land Owner

Lease of land Lease of land90 2 9 3 Rai90-2-9.3 Rai

(Principle Leasing Contract)90-2-9.3 Rai

(Principle Leasing Contract)

Central PattanaRama 2 Co., Ltd

Central PattanaRama 3 Co., Ltd

Central Pattana Plc. (Central Plaza Pinklao)

Central Pattana Plc.

Lease of land S bl f Lease of Sublease of land

53-2-39.4 Rai20 Years

Lease of buildingand parking

20 years

Lease of land and building30 + 30 + 30

years

Sublease of land

24-02-84 Rai15 Years

Lease of shopping

complex and office building

15 years

Property Manager

15

CPN Retail Growth Leasehold Property Fund (CPNRF)

CPNRF Fund Information

Name CPN Retail Growth Leasehold Property Fund (“CPNRF”)

Property Manager Central Pattana Public Company Limited (“CPN”)Property Manager Central Pattana Public Company Limited ( CPN )

Fund Manager SCB Asset Management Company Limited

Trustee Kasikorn Bank Public Company Limited

Registrar The Siam Commercial Bank Public Company Limited

Assets CentralPlaza Rama 2, CenteralPlaza Ratchada-Rama 3, CentralPlazaPinklao, and CentralPlaza Chiangmai Airport

Type Property Fund Type I (Indefinite Life)

Total Fund Size Baht 24,406.21 MB

Fund Registered Date 11 August 2005Fund Registered Date 11 August 2005

Fund Investing Date

15 August 2005 for CentralPlaza Rama 216 August 2005 for CentralPlaza Ratchada-Rama 3

f ig

4 November 2009 for CentraPlaza Pinklao24 April 2014 for CentralPlaza Chiangmai Airport

Fund Listed Date 23 August 2005

16

Secondary Market The Stock Exchange of Thailand (“SET”)

CPN Commercial Growth Leasehold Property Fund1st Quarter 2014 Financial Results22nd May 2014

1

Important Notice

The information contained in this presentation is for information purposes only and does not constitute an ff i it ti t ll th li it ti f ff i it ti t h b ib f it i CPN offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for units in CPN

Commercial Growth Leasehold Property Fund (CPNCG and units in CPNCG, “Units”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever.

This presentation may include information which is forward-looking in nature Forward-looking information This presentation may include information which is forward looking in nature. Forward looking information involve known and unknown risks, uncertainties and other factors which may impact on the actual outcomes, including economic conditions in the markets in which CPNCG operates and general achievement of CPNCG business forecasts, which will cause the actual results, performance or achievements of CPNCG to differ, perhaps materially, from the results, performance or achievements expressed or implied in this presentation.expressed or implied in this presentation.

This presentation has been prepared by the CPNCG Property Manager. The information in this presentation has not been independently verified. No representation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the CPNCG Property Manager or CPNCG Fund Manager or any

f i i f i i ffi i i iof its agents or advisers, or any of their respective affiliates, advisers or representatives, shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

This presentation is made, furnished and distributed for information purposes only. No part of this presentation shall be relied upon directly or indirectly for any investment decision-making or for any other presentation shall be relied upon directly or indirectly for any investment decision-making or for any other purposes.

This presentation and all other information, materials or documents provided in connection therewith, shall not, either in whole or in part, be reproduced, redistributed or made available to any other person, save in strict compliance with all applicable laws.

2

Contents

Page

1. Operations 5

2. Financial Highlights 9

3. Q&A

3

1. Operations1. Operations

Leasable Area and Occupancy

Occupancy rate of CPNCG as of 31 March 2014 was 99.6%

Area (Sqm) Occupancy Rate

Gross Area Leaseable Area 31 Mar 13 30 Jun 13 30 Sep 13 31 Dec 13 31 Mar 14

The Offices @ CentralWorld 121,189 80,585 98.8% 98.0% 99.2% 98.9% 99.6%

CPNCG 121,189 80,585 98.8% 98.0% 99.2% 98.9% 99.6%

Source: CPN

5

Lease expiry profile

Well balanced lease expiry profile

37%2014

42%

13%

2016

2015

8%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

2017

Note:

The Offices @ CentralWorld

Note:1. Percentage of total occupied area as at 31 March 20142. Exclude rental agreements < 1 year

Source: CPN

6

High Quality Tenants

Anchor Tenant % f T t l L bl A /1Anchor Tenant % of Total Leasable Area /1

Nestle (Thailand) 16%Central Pattana 10%AGODA 7%Central Trading 6%Ogilvy 6%Maybank KimEng 6%FINANSIA SYRUS 4%Surv Corp 3%MSD (Thailand) 3%Philip Morris (Thailand) Limited 3%Total Area of Anchor Tenants 61%

Note: /1 Based on leasable area as at 31 March 2014

7

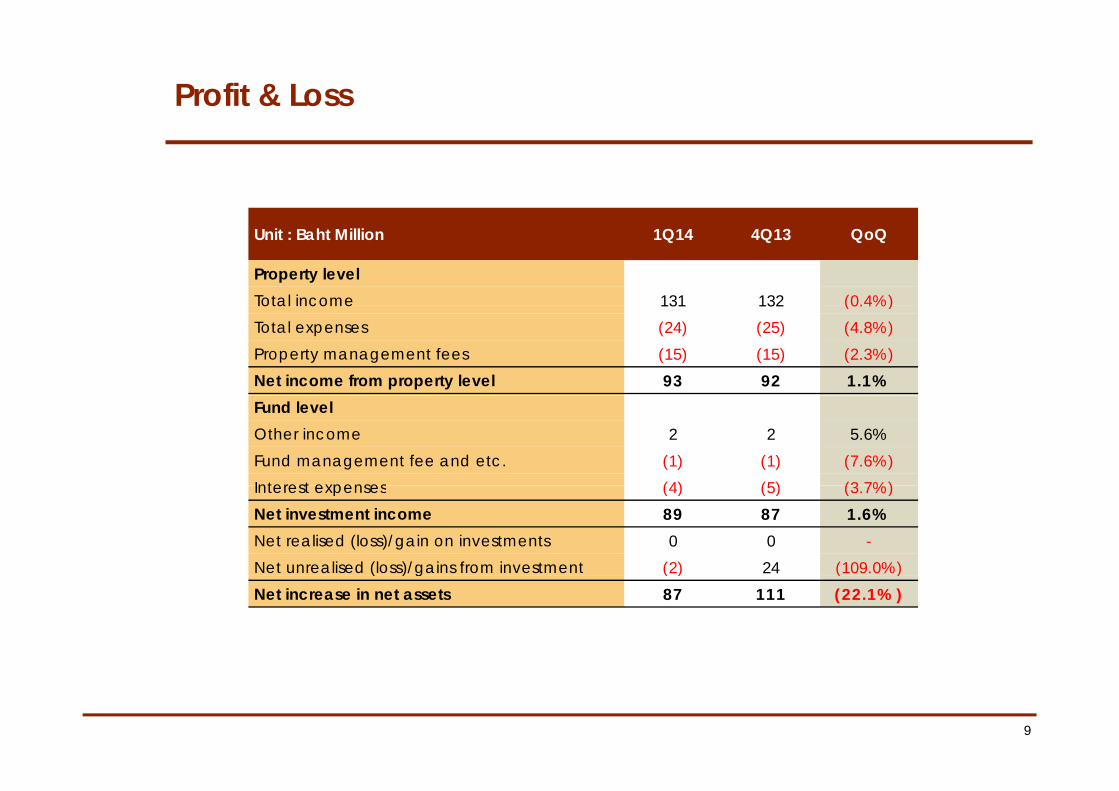

2 Financial Highlights2. Financial Highlights

Profit & Loss

Unit : Baht Million 1Q14 4Q13 QoQ

Property levelTotal income 131 132 (0.4%)Total income 131 132 (0.4%)

Total expenses (24) (25) (4.8%)

Property management fees (15) (15) (2.3%)

Net income from property level 93 92 1.1%

Fund levelOther income 2 2 5.6%

Fund management fee and etc. (1) (1) (7.6%)

Interest expenses (4) (5) (3 7%)Interest expenses (4) (5) (3.7%)

Net investment income 89 87 1.6%

Net realised (loss)/gain on investments 0 0 -

Net unrealised (loss)/gains from investment (2) 24 (109.0%)( ) g ( ) ( )

Net increase in net assets 87 111 (22.1%)

9

Balance Sheet

Unit : Baht Million except indicated Mar-14 Dec-13 QoQ

Investments in properties at fair value 5,357 5,319 0.2%

Cash and near cash 62 114 1.0%

Other assets 6 6 15.2%

Total Assets 5,424 5,438 0.7%

A/P and accrued expenses 12 25 18.2%

Deposits received from customers 167 167 0.9%

Loan from SCB 366 370 0.0%

Other liabilities 0 1 (66.8%)

Total Liabilities 545 563 0.7%

C it l i d f ith ld 4 394 4 394 0 0%Capital received from unitholders 4,394 4,394 0.0%

Retained earnings 427 481 8.3%

Net Asset Values 4,822 4,875 0.7%

NAV per unit (Baht) 11 4365 11 4272 1 3%NAV per unit (Baht) 11.4365 11.4272 1.3%

10

Distribution Summary

1Q14 4Q13 QoQUnit : Baht Million except indicated

1Q14 4Q13 QoQ

Net investment income 89 87 1.6%

Actual distribution

via Dividend 84 83 1.0%

Baht per unit 0.1960 0.1941 1.0%

via Par Reduction - - -

ht itBaht per unit - - -

Total distribution 84 83 1.0%

Baht per unit 0.1960 0.1941 1.0%

% f N t i t t i 94 4% 95 0% (0 6%)

Note:

% of Net investment income 94.4% 95.0% (0.6%)

Annualised distribution yield /1 7.7% 7.6% 1.0%

Note:/1 Based on unit price of 10.20 Baht as at 19 May 2014 (For the current quarter and next 9 months)

11

Shareholder Structure

Listed on the SET 21 Sep 2012Units Outstanding 426.64M Units

Dividend Policy• 4 times a yearUnits Outstanding 426.64M Units

Registered Fund Size Baht 4,394.4M NAV (Mar 2014) Baht 11.4365

4 times a year• Pay out a minimum of 90% of distributable income

Unitholders Information(as at 8th May 2014)

THAI 95.66%

CPN 25.00%CPN, 25%

Individual, 46%Institution 25.16%

Individual 45.50%

FOREIGN 4 34%

Institution, 29%

46%

FOREIGN 4.34%

Institution 4.22%

Individual 0.12%

12

0 %

CPNCG Fund Information

Name CPN Commercial Growth Leasehold Property Fund (“CPNRF”)

Property Manager Central Pattana Public Company Limited (“CPN”)

Fund Manager SCB Asset Management Company Limited

Trustee Kasikorn Bank Public Company Limited

Registrar The Siam Commercial Bank Public Company Limited

A t Th Offi @C t l W ldAssets The Offices@Central World

Type Property Fund Type I (Indefinite Life)

Total Fund Size THB 4,394.4 MBTotal Fund Size THB 4,394.4 MB

Fund Registered Date 13 September 2012

Fund Investing Date 14 September 2012

Fund Listed Date 21 September 2012

Secondary Market The Stock Exchange of Thailand (“SET”)

13