cbse class 12 accountancyapsbirpur.edu.in/upload/attach/872651520860523_accounts.pdfmaterial...

TRANSCRIPT

MaterialdownloadedfrommyCBSEguide.com. 1/37

CBSEClass12ACCOUNTANCY

SamplePaper(ByCBSE)

GeneralInstructions:

Thisquestionpapercontainstwoparts-AandB.

PartAiscompulsoryforall.

PartBhastwooptions-‘AnalysisofFinancialStatements’and‘Computerised

Accounting’.

AttemptanyoneoptionofPartB.

Allpartsofaquestionshouldbeattemptedatoneplace.

PartA

(AccountingforPartnershipFirmsandCompanies)

1.SixfriendsstartedapartnershipbusinessbyinvestingRs.2,00,000each.Theydecidedto

shareprofitequally.Namethetermsbywhichtheywillbecalledindividuallyand

collectively.(1)

2.A,BandCwerepartnersinafirmsharingprofitsintheratioof3:2:1.Bwasguaranteed

aprofitofRs.2,00,000.DuringtheyearthefirmearnedaprofitofRs.84,000.Calculatethe

netamountofProfit/LosstransferredtothecapitalaccountsofAandC.(1)

3.H,PandSwerepartnersinafirmsharingprofitsintheratioof4:3:3.OnAugust1,2017,

Pdied.His20%sharewasacquiredbyHandremainingbyS.Calculatethenewprofit

sharingratio.(1)

4.Howisdissolutionofpartnershipdifferentfromdissolutionofpartnershipfirm?(1)

5.Whyareirredeemabledebenturesalsoknownasperpetualdebentures?(1)

6.Distinguishbetweensharesanddebenturesonthebasisofconvertibility.(1)

7.KKLimitedobtainedaloanofRs.10,0,000fromStateBankofIndia@9%interst.The

companyissuedRs.15,0009%debenturesinfavourofStateBankofIndiaascollateral

security.PassnecessaryJournalentriesfortheabovetransactions:(3)

MaterialdownloadedfrommyCBSEguide.com. 2/37

(i)Whencompanydecidednottorecordtheissueof9%Debenturesascollateralsecurity.

(ii)Whencompanydecidedtorecordtheissueof9%Debenturesascollateralsecurity.

8.P,QandRwerepartnerssharingprofitsintheratioof2:2:1.Thefirmclosesitsbookson

March31everyyear.OnJune30,2017,Rdied.ThefollowinginformationisprovidedonR’s

death:(3)

(i)BalanceinhiscapitalaccountinthebeginningoftheyearwasRs.6,50,000.

(ii)HewithdrewRs.60,000onMay15,2017forhispersonaluse.

Onthedateofdeathofapartnerthepartnershipdeedprovidedforthefollowing:

(a)Interestoncapital@10%perannum.

(b)Interestondrawings@12%perannum.

(c)Hisshareintheprofitofthefirmtillthedateofdeath,tobecalculatedonthebasisofthe

rateofNetProfitonSalesofthepreviousyear,whichwas25%.TheSalesofthefirmtillJune

30,2017wereRs.6,00,000.

PrepareR’sCapitalAccountonhisdeathtobepresentedtohisexecutors.

9.MMLimitedisregisteredwithanAuthorisedcapitalofRs.200Croresdividedintoequity

sharesofRs.100each.TheSubscribedandCalledupcapitalofthecompanyisRs.

10,00,00,000.Thecompanydecidedtohelptheunemployedyouthofthenaxalaffectedareas

ofAndhraPradesh,ChhattisgarhandOdishabyopening100‘SkillDevelopmentCentres’.The

companyalsodecidedtoprovidefreemedicalservicestothevillagersofthesestatesby

startingmobiledispensaries.Tomeetthecapitalexpenditureoftheseactivitiesthecompany

issued1,00,000equityshares.Theseshareswerefullysubscribedandpaid.

PresentthesharecapitalofthecompanyinitsBalanceSheet.Alsoidentifyanytwovalues

thatthecompanywantstopropagate.(3)

10.VKLimitedpurchasedmachineryfromModernEquipmentManufacturersLimited.The

companypaidthevendorsbyissueofsomeequitysharesanddebenturesandthebalance

throughanacceptanceintheirfavourpayableafterthreemonths.Theaccountantofthe

MaterialdownloadedfrommyCBSEguide.com. 3/37

companywhileJournalisingtheabovementionedtransactionsleftsomeitemsblank.You

arerequiredtofillintheblanks.(3)

VKLimited

Journal

Date Particular LFDR.Amount

(Rs.)

DR.Amount

(Rs.)

MachineryAccountDr.

To………………………………………………………

(PurchasedmachineryforRs.7,00,000from

ModernEquipmentManufacturersLimited)

ModernEquipmentManufacturersLtd.A/CDr.

LossonIssueof9%DebenturesAccountDr.

To……………………………………………………..

To……………………………………………………..

ToSecuritiesPremiumAccount

ToPremiumonRedemptionofDebenturesA/C

(IssuedRs.1,00,0009%debenturesatadiscountof

10%redeemableatapremiumof10%and50,000

equitysharesofRs.10eachissuedatapremiumof

15%)

……………………………………………….Dr.

To………………………………………………

(…………………………………………………………………………)

…………………

…………………

…………………

…………………

…………………

…………………

…………………

…………………

…………………

…………………

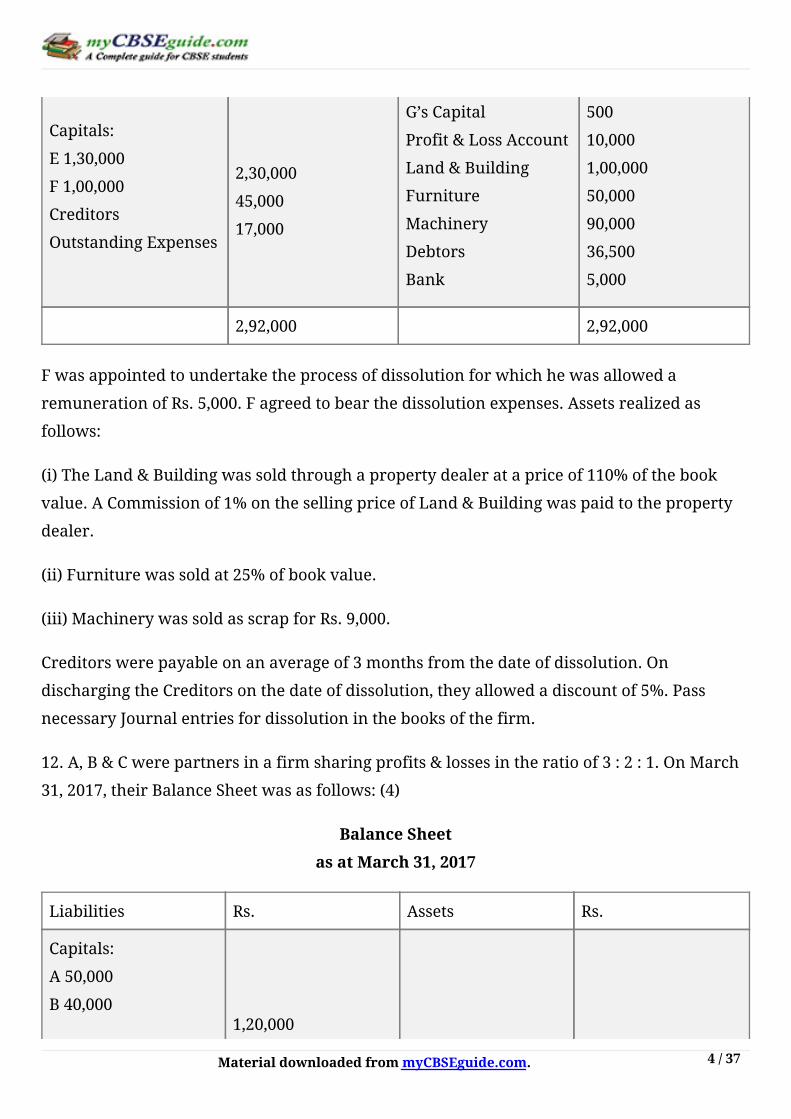

11.E,FandGwerepartnersinafirmsharingprofitsintheratioof2:2:1.OnSeptember30,

2017,theirfirmwasdissolved.Onthedateofdissolution,theBalanceSheetofthefirmwas

asfollows:(4)

BalanceSheet

AsatMarch31,2017

Liabilities Rs. Assets Rs.

MaterialdownloadedfrommyCBSEguide.com. 4/37

Capitals:

E1,30,000

F1,00,000

Creditors

OutstandingExpenses

2,30,000

45,000

17,000

G’sCapital

Profit&LossAccount

Land&Building

Furniture

Machinery

Debtors

Bank

500

10,000

1,00,000

50,000

90,000

36,500

5,000

2,92,000 2,92,000

Fwasappointedtoundertaketheprocessofdissolutionforwhichhewasalloweda

remunerationofRs.5,000.Fagreedtobearthedissolutionexpenses.Assetsrealizedas

follows:

(i)TheLand&Buildingwassoldthroughapropertydealeratapriceof110%ofthebook

value.ACommissionof1%onthesellingpriceofLand&Buildingwaspaidtotheproperty

dealer.

(ii)Furniturewassoldat25%ofbookvalue.

(iii)MachinerywassoldasscrapforRs.9,000.

Creditorswerepayableonanaverageof3monthsfromthedateofdissolution.On

dischargingtheCreditorsonthedateofdissolution,theyallowedadiscountof5%.Pass

necessaryJournalentriesfordissolutioninthebooksofthefirm.

12.A,B&Cwerepartnersinafirmsharingprofits&lossesintheratioof3:2:1.OnMarch

31,2017,theirBalanceSheetwasasfollows:(4)

BalanceSheet

asatMarch31,2017

Liabilities Rs. Assets Rs.

Capitals:

A50,000

B40,000

1,20,000

MaterialdownloadedfrommyCBSEguide.com. 5/37

C30,000

ReserveFund

Creditors

EmployeesProvident

Fund

18,000

27,000

50,000

FixedAssets

CurrentAssets

1,80,000

35,000

2,15,000 2,15,000

FromApril1,2017,theydecidedtosharefutureprofitsequally.Forthispurposethe

followingswereagreedupon:

(i)GoodwillofthefirmwasvaluedatRs.3,00,000.

(ii)FixedAssetswillbedepreciatedby10%.

(iii)Afterdoingtheaboveadjustmentsthecapitalsofthepartnerswillbeinproportionto

theirnewprofitsharingratio.ForthispurposeCurrentAccountswillbeopened.

PassnecessaryJournalentriesfortheabovetransactionsinthebooksofthefirm.

13.L,MandNarepartnersinafirmsharingprofits&lossesintheratioof2:3:5.OnApril

1,2016theirfixedcapitalswereRs.2,00,000,Rs.3,00,000andRs.4,00,000respectively.Their

partnershipdeedprovidedforthefollowing:(6)

(i)Interestoncapital@9%perannum.

(ii)InterestonDrawings@12%perannum.

(iii)Interestonpartners’loan@12%perannum.

OnJuly1,2016,LbroughtRs.1,00,000asadditionalcapitalandNwithdrewRs.1,00,000from

hiscapital.DuringtheyearL,MandNwithdrewRs.12,000,Rs.18,000andRs.24,000

respectivelyfortheirpersonaluse.OnJanuary1,2017thefirmobtainedaLoanofRs.

1,50,000fromM.TheNetprofitofthefirmfortheyearendedMarch31,2017aftercharging

interestonM’sLoanwasRs.85,000.

PrepareProfit&LossAppropriationAccountandPartnersCapitalAccount.

14.PassnecessaryJournalentriesinthebooksofPPLimitedfortheissueofdebenturesin

MaterialdownloadedfrommyCBSEguide.com. 6/37

thefollowingcases:(6)

(a)Issued5009%debenturesofRs.100eachatadiscountof6%redeemableatapremiumof

9%.

(b)IssuedRs.10,00,0009%debenturesofRs.100eachatapremiumofRs.20perdebenture

redeemableatapremiumofRs.10perdebenture.

(c)Issued3,0008%debenturesofRs.100eachatadiscountofRs.15,000redeemableata

premiumof5%.

15.OnApril1,2013,XYLimitedissuedRs.9,00,00010%debenturesatadiscountof9%.The

debenturesweretoberedeemedinthreeequalannualinstalmentsstartingfromMarch31,

2015.(6)

Prepare‘DiscountonIssueofDebentureAccount’forthefirstthreeyearsstartingfromApril

1,2013.Alsoshowyourworkingsclearly.

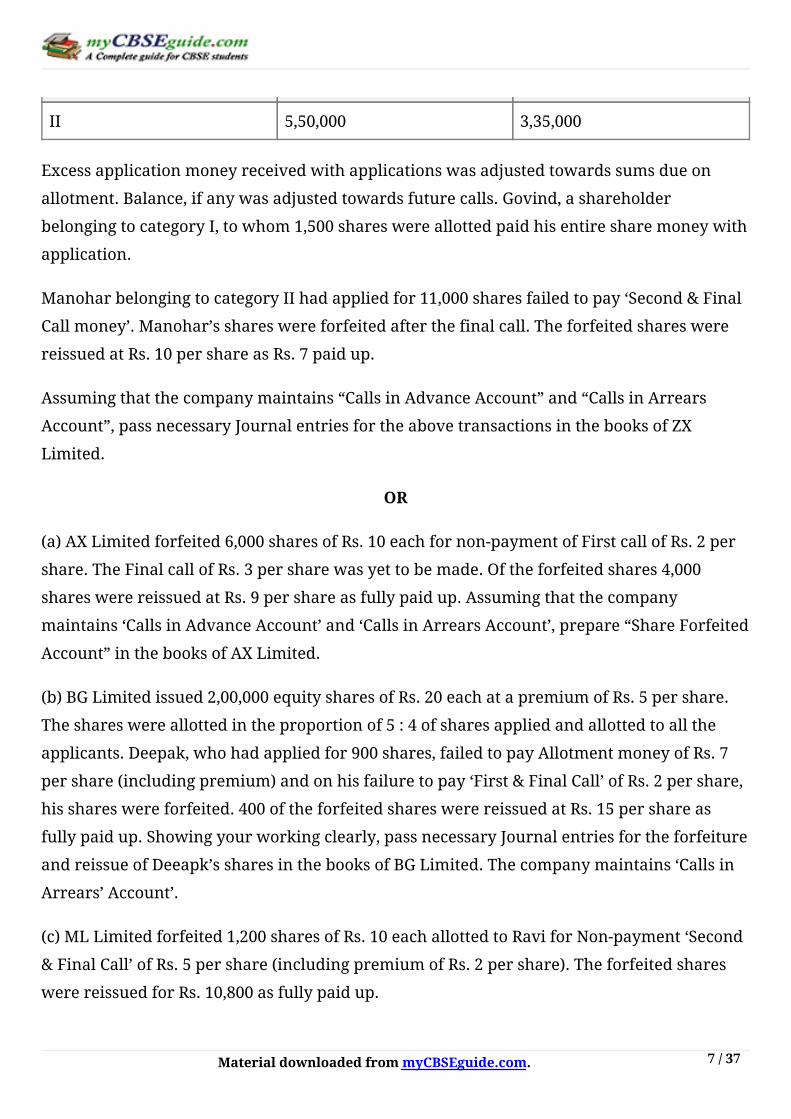

16.ZXLimitedinvitedapplicationsforissuing5,00,000EquitysharesofRs.10eachpayable

atapremiumofRs.10eachpayablewithFinalcall.Amountpersharewaspayableas

follows:(8)

Rs.

OnApplication 2

OnAllotment 3

OnFirstCall 2

OnSecond&Final

CallBalance

Applicationsfor8,00,000shareswerereceived.Applicationsfor50,000shareswererejected

andtheapplicationmoneywasrefunded.Allotmentwasmadetotheremainingapplicants

asfollows:

Category No.ofsharesApplied No.ofSharesallotted

I 2,00,000 1,50,000

MaterialdownloadedfrommyCBSEguide.com. 7/37

II 5,50,000 3,35,000

Excessapplicationmoneyreceivedwithapplicationswasadjustedtowardssumsdueon

allotment.Balance,ifanywasadjustedtowardsfuturecalls.Govind,ashareholder

belongingtocategoryI,towhom1,500shareswereallottedpaidhisentiresharemoneywith

application.

ManoharbelongingtocategoryIIhadappliedfor11,000sharesfailedtopay‘Second&Final

Callmoney’.Manohar’sshareswereforfeitedafterthefinalcall.Theforfeitedshareswere

reissuedatRs.10pershareasRs.7paidup.

Assumingthatthecompanymaintains“CallsinAdvanceAccount”and“CallsinArrears

Account”,passnecessaryJournalentriesfortheabovetransactionsinthebooksofZX

Limited.

OR

(a)AXLimitedforfeited6,000sharesofRs.10eachfornon-paymentofFirstcallofRs.2per

share.TheFinalcallofRs.3persharewasyettobemade.Oftheforfeitedshares4,000

shareswerereissuedatRs.9pershareasfullypaidup.Assumingthatthecompany

maintains‘CallsinAdvanceAccount’and‘CallsinArrearsAccount’,prepare“ShareForfeited

Account”inthebooksofAXLimited.

(b)BGLimitedissued2,00,000equitysharesofRs.20eachatapremiumofRs.5pershare.

Theshareswereallottedintheproportionof5:4ofsharesappliedandallottedtoallthe

applicants.Deepak,whohadappliedfor900shares,failedtopayAllotmentmoneyofRs.7

pershare(includingpremium)andonhisfailuretopay‘First&FinalCall’ofRs.2pershare,

hisshareswereforfeited.400oftheforfeitedshareswerereissuedatRs.15pershareas

fullypaidup.Showingyourworkingclearly,passnecessaryJournalentriesfortheforfeiture

andreissueofDeeapk’ssharesinthebooksofBGLimited.Thecompanymaintains‘Callsin

Arrears’Account’.

(c)MLLimitedforfeited1,200sharesofRs.10eachallottedtoRaviforNon-payment‘Second

&FinalCall’ofRs.5pershare(includingpremiumofRs.2pershare).Theforfeitedshares

werereissuedforRs.10,800asfullypaidup.

MaterialdownloadedfrommyCBSEguide.com. 8/37

PassnecessaryJournalentriesforreissueofsharesinthebooksofMLLimited.

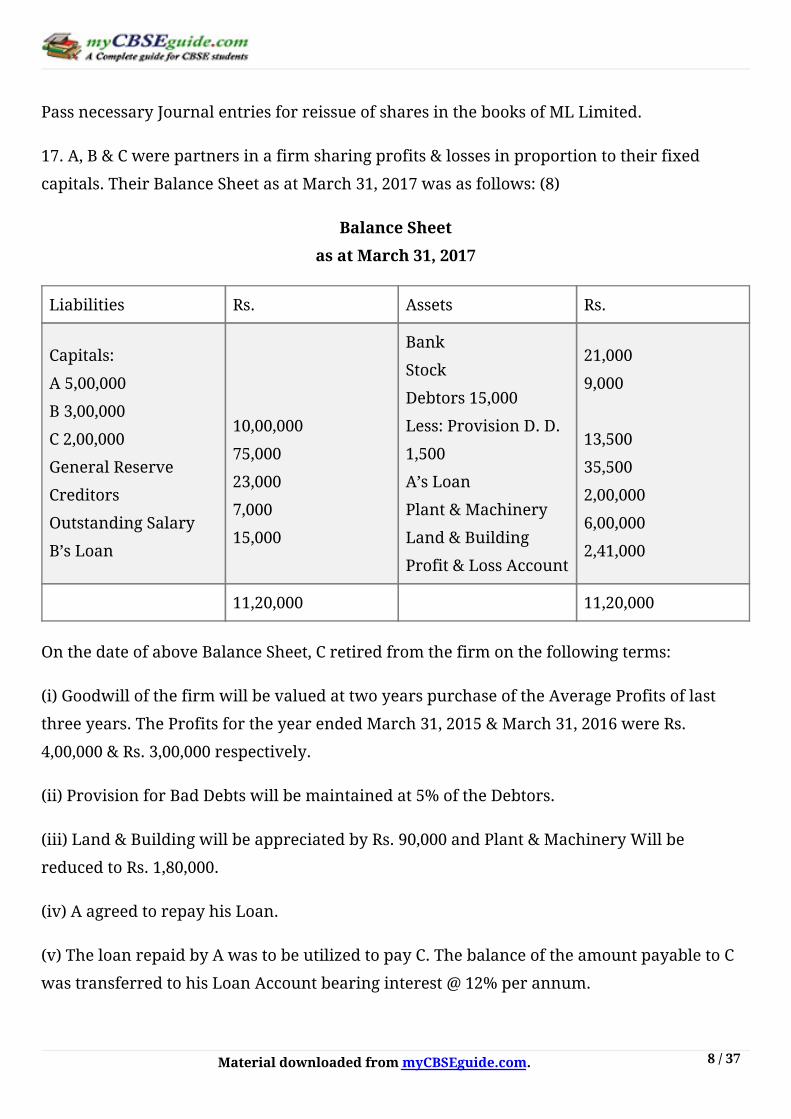

17.A,B&Cwerepartnersinafirmsharingprofits&lossesinproportiontotheirfixed

capitals.TheirBalanceSheetasatMarch31,2017wasasfollows:(8)

BalanceSheet

asatMarch31,2017

Liabilities Rs. Assets Rs.

Capitals:

A5,00,000

B3,00,000

C2,00,000

GeneralReserve

Creditors

OutstandingSalary

B’sLoan

10,00,000

75,000

23,000

7,000

15,000

Bank

Stock

Debtors15,000

Less:ProvisionD.D.

1,500

A’sLoan

Plant&Machinery

Land&Building

Profit&LossAccount

21,000

9,000

13,500

35,500

2,00,000

6,00,000

2,41,000

11,20,000 11,20,000

OnthedateofaboveBalanceSheet,Cretiredfromthefirmonthefollowingterms:

(i)GoodwillofthefirmwillbevaluedattwoyearspurchaseoftheAverageProfitsoflast

threeyears.TheProfitsfortheyearendedMarch31,2015&March31,2016wereRs.

4,00,000&Rs.3,00,000respectively.

(ii)ProvisionforBadDebtswillbemaintainedat5%oftheDebtors.

(iii)Land&BuildingwillbeappreciatedbyRs.90,000andPlant&MachineryWillbe

reducedtoRs.1,80,000.

(iv)AagreedtorepayhisLoan.

(v)TheloanrepaidbyAwastobeutilizedtopayC.ThebalanceoftheamountpayabletoC

wastransferredtohisLoanAccountbearinginterest@12%perannum.

MaterialdownloadedfrommyCBSEguide.com. 9/37

PrepareRevaluationAccount,Partners’CapitalAccountsandtheBalanceSheetofthe

reconstitutedfirm.

OR

P&Kwerepartnersinafirm.OnMarch31,2017theirBalanceSheetwasasfollows:

BalanceSheet

asatMarch31,2017

Liabilities Rs. Assets Rs.

Capitals:

P3,00,000

K2,00,000

GeneralReserve

Creditors

OutstandingExpenses

C’sLoan

Profit&LossAccount

(Profitfor2016-17)

5,00,000

1,00,000

50,000

8,000

1,20,000

55,000

Bank

Stock

Debtors22,000

Less:ProvisionD.D.

1,500

UnexpiredInsurance

SharesinKLimited

Plant&Machinery

Land&Building

18,000

19,000

20,500

5,000

65,000

1,45,500

5,60,000

8,33,000 8,33,000

OnApril1,2017,theydecidedtoadmitCasanewpartnerfor1/4thshareinprofitsonthe

followingterms:

(i)C’sLoanwillbeconvertedintohiscapital.

(ii)CwillbringhisshareofgoodwillpremiuminCash.Goodwillofthefirmwillbe

calculatedonthebasisofAverageProfitsofpreviousthreeyears.Profitsfortheyearended

March31,2015andMarch31,2016wereRs.65,000andRs.1,00,000respectively.

(iii)10%depreciationwillbechargedonPlant&MachineryandLand&Buildingwillbe

appreciatedby5%.

(iv)CapitalsofP&KwillbeadjustedonthebasisC’scapital.Actualcashwillbeboughtinor

MaterialdownloadedfrommyCBSEguide.com. 10/37

paidoffasthecasemaybe.

PassnecessaryJournalentriesonC’sadmission.

PartB

OptionI

(AnalysisofFinancialStatements)

18.Giveanytwoexamplesofcashinflowsfromoperatingactivitiesotherthancashreceipts

fromsaleofgoods&renderingofservices.(1)

19.PPLimitedisShareBrokerCompany.GGLimitedisengagedinmanufacturingof

packagedfood.PPLimitedpurchased5,000equitysharesofRs.100eachofSavitaLimited.G

GLimitedalsopurchased10,000equitysharesofRs.100eachofSavitaLimited.Forthe

purposeofpreparingtheirrespectiveCashFlowStatements,underwhichcategoryof

activitiesthepurchaseofshareswillbeclassifiedbyPPLimitedandGGLimited?(1)

20.MKLimitedisacomputerhardwaremanufacturingcompany.Whilepreparingits

accountingrecordsittakesintoconsiderationthevariousaccountingprinciplesand

maintainstransparency.Attheendoftheaccountingyear,thecompanyfollowsthe

‘CompaniesActandRules,2013’forthepreparationofitsFinancialStatements.Italso

preparesitsIncomeStatementandBalanceSheetaspertheformatprovidedinScheduleIII

totheAct.ItsFinancialStatementsdepictitsfair&truefinancialposition.Forthefinancial

yearendingMarch31,2017,theaccountantofthecompanyisnotcertainaboutthe

presentationofthefollowingitemsunderrelevantMajorHeads&SubHeads,ifany,inits

BalanceSheet:(4)

(i)SecuritiesPremiumReserve

(ii)CallsinAdvance

(iii)Stores&Spares

(a)AdvicetheaccountantofthecompanyunderwhichMajorHeadsandSubHeads,ifany,

heshouldpresenttheaboveitemsintheBalanceSheetofthecompany,

(b)Listanytwovaluesthatthecompanyisobservinginthemaintenanceofitsaccounting

recordsandpreparationofitsfinancialstatements.

MaterialdownloadedfrommyCBSEguide.com. 11/37

21.FortheyearendedMarch31,2017,NetProfitaftertaxofKXLimitedwasRs.6,00,000.

ThecompanyhasRs.40,00,00012%DebenturesofRs.100each.CalculateInterestCoverage

Ratioassuming40%taxrate.Stateitssignificancealso.WilltheInterestCoverageRatio

changeifduringtheyear2017-18,thecompanydecidestoredeemdebenturesofRs.5,00,000

andexpectstomaintainthesamerateofNetProfitandassumethattheTaxratewillnot

change.(4)

22.FollowingistheStatementofProfit&LossofXLLimitedfortheyearendedMarch31,

2017:(4)

StatementofProfit&Loss

fortheyearendedMarch31,2017

ParticularsNotesto

Accounts

2015-16

Amount(Rs.)

2016-17

Amount(Rs.)

RevenuefromOperations

Expenses:

(a)EmployeeBenefitExpenses:10%of

Revenuefrom

Operations

(b)OtherExpenses

50,00,000

10,00,000

80,00,000

12,00,000

TaxRate40%

PrepareComparativeStatementofProfit&LossofXLLimited.

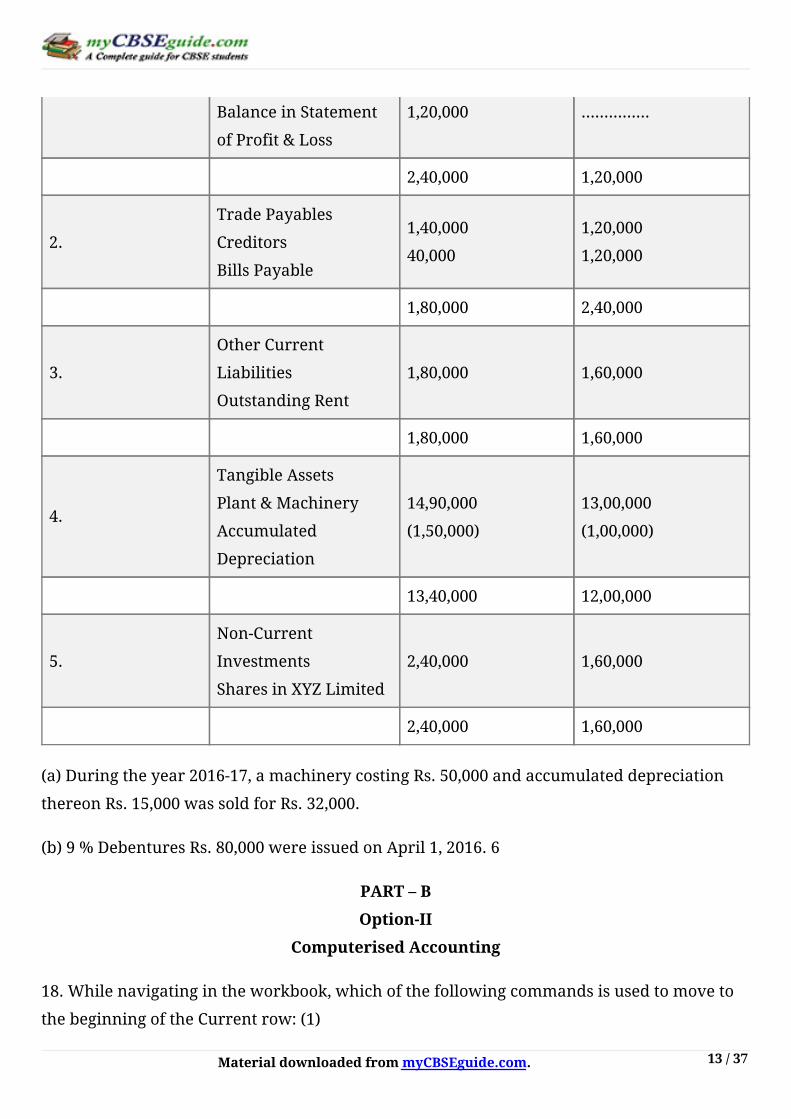

23.FromthefollowingBalanceSheetofAjantaLimitedasonMarch31,2017,prepareaCash

FlowStatement:(6)

ParticularsNote

Number

31-3-2017

(Rs.)

31-3-2016

(Rs.)

I.EquityandLiabilities

(1)Shareholders’

Funds

(a)EquityShare

MaterialdownloadedfrommyCBSEguide.com. 12/37

Capital

(b)Reservesand

Surplus

(2)Non-Current

Liabilities

Long-Term

Borrowings-9%

Debentures

(3)CurrentLiabilities

(a)TradePayables

(b)OtherCurrent

Liabilities

10,00,000

2,40,000

3,20,000

1,80,000

1,80,000

10,00,000

1,20,000

2,40,000

2,40,000

1,60,000

Total 19,20,000 17,60,000

II.Assets

(1)Non-CurrentAssets

(a)FixedAssets

TangibleAssets

(b)Non-Current

Investments

(2)CurrentAssets

(a)Inventories

(b)TradeReceivables

(c)CashandCash

Equivalents

13,40,000

2,40,000

1,20,000

1,60,000

60,000

12,00,000

1,60,000

1,60,000

1,60,000

80,000

Total 19,20,000 17,60,000

NoteofAccounts

Note

NumberParticulars

31-3-2017

(Rs.)

31-3-2016

(Rs.)

1.

ReservesandSurplus

GeneralReserve 1,20,000 1,20,000

MaterialdownloadedfrommyCBSEguide.com. 13/37

BalanceinStatement

ofProfit&Loss

1,20,000 ……………

2,40,000 1,20,000

2.

TradePayables

Creditors

BillsPayable

1,40,000

40,000

1,20,000

1,20,000

1,80,000 2,40,000

3.

OtherCurrent

Liabilities

OutstandingRent

1,80,000 1,60,000

1,80,000 1,60,000

4.

TangibleAssets

Plant&Machinery

Accumulated

Depreciation

14,90,000

(1,50,000)

13,00,000

(1,00,000)

13,40,000 12,00,000

5.

Non-Current

Investments

SharesinXYZLimited

2,40,000 1,60,000

2,40,000 1,60,000

(a)Duringtheyear2016-17,amachinerycostingRs.50,000andaccumulateddepreciation

thereonRs.15,000wassoldforRs.32,000.

(b)9%DebenturesRs.80,000wereissuedonApril1,2016.6

PART–B

Option-II

ComputerisedAccounting

18.Whilenavigatingintheworkbook,whichofthefollowingcommandsisusedtomoveto

thebeginningoftheCurrentrow:(1)

MaterialdownloadedfrommyCBSEguide.com. 14/37

a.[ctrl]+[home]

b.[pageup]

c.[Home]

d.[ctrl]+[Backspace]

19.JoinlineinthecontextofAccesstablemeans:(1)

a.Graphicalrepresentationoftablesbetweentables

b.Linesbondingthedatawithintable

c.Lineconnectingtwofieldsofatable

d.Lineconnectingtworecordsofatable

20.Enumeratethebasicrequirementsofcomputerizedaccountingsystemforabusiness

organization.(4)

21.Thegenerationofledgeraccountsisnotanecessaryconditionformakingtrialbalancein

acomputerizedaccountingsystem.Explain.(4)

22.Internalmanipulationofaccountingrecordsismucheasierincomputerizedaccounting

thaninmanualaccounting.How?(4)

23.Computerisationofaccountingdataononehandstoresvoluminousdatainasystematic

andorganizedmannerwhereasontheotherhandsuffersfromthreatsofvulnerabilityand

manipulations.Discussthesecuritymeasuresyouwouldliketoemployforsecuringthedata

fromsuchthreats.(6)

MaterialdownloadedfrommyCBSEguide.com. 15/37

CBSEClassXIIAccountancy

SamplePaper(byCBSE)

MarkingScheme

PartA

(AccountingforPartnershipFirmsandCompanies)

1.Individually:Partners

Collectively:Firm

2.NetAmountofLosstransferredto:

A’sCapitalAccount:Rs.87,000

C’sCapitalAccount:Rs.29,000

3.RatioofH,PandSis4:3:3

H’sGain=3/10X20/100=3/50

H’snewshare=H’soldshare+H’sGain

=4/10+3/50=23/50

S’sGain=3/10X80/100=12/50

S’snewshare=S’soldshare+S’sGain

=3/10+12/50=27/50

NewProfitsharingRatioofHandSis23:27

4.Solution:Incaseofdissolutionofpartnership,thefirmcontinuetodobusinessbutwitha

changedagreement.Incaseofdissolutionofpartnershipfirm,thefirmceasestoexist,the

assetsofthefirmarerealisedanditsliabilitiesaredischarged.

5.Solution:Irredeemabledebenturesarecalledperpetualdebenturesbecausethesearenot

repayableduringthelifespanofthecompany.

MaterialdownloadedfrommyCBSEguide.com. 16/37

6.Solution:Sharescannotbeconvertedintodebenturesoranyothersecuritywhereasthe

debenturescanbeconvertedintosharesifthetermssoprovide.

7.(i)

KKLimited

Journal

Date Particulars LF Dr.Amount(Rs.) Dr.Amount(Rs.)

BankAccountDr.

ToBankLoanAccount

(ObtainedloanfromStateBankof

India@9%.)

10,00,000 10,00,000

(ii)

KKLimited

Journal

Date Particulars LFDr.Amount

(Rs.)

Dr.Amount

(Rs.)

BankAccountDr.

ToBankLoanAccount

(ObtainedloanfromStateBankofIndia

@9%.)

10,00,000

10,00,000

DebentureSuspenseAccountDr.

To9%DebenturesAccount

(Issued9%Debenturesascollateral

securityin

favourofStateBankofIndia)

15,00,000

15,00,000

8.

R’sCapitalAccount

MaterialdownloadedfrommyCBSEguide.com. 17/37

Date

2017Particulars JF Amount

(Rs)

Date

2017Particulars JF Amount

(Rs)

Jun30

Jun30

Jun30

ToDrawingsA/C

ToIntereston

DrawingsA/C

ToR’sExecutor’s

A/c

60,000

900

6,35,350

Apr1

Jun

30

Jun

30

ByBalanceb/d

ByIntereston

capitalA/c

ByProfit&Loss

SuspenseA/C

6,50,000

16,250

30,000

6,96,250 6,96,250

Note:½markmaybedeductedifthedatesarenotcorrectlyrecorded.

9.

MMLimited

BalanceSheet

Asat……….

ParticularsNote

Number

CurrentYear

Rs.

PreviousYear

Rs.Crores

I.EquityandLiabilities

1.Shareholders’Funds

a)ShareCapital

1 11 10

NotestoAccounts

NoteNumber1

Particulars CurrentYearsRs.Crores

ShareCapital:

AuthorisedCapital

2,00,00,000EquitySharesofRs.100each

200

IssuedCapital

11,00,000EquitysharesofRs.100each11

MaterialdownloadedfrommyCBSEguide.com. 18/37

SubscribedCapital

SubscribedandFullypaid

11,00,000EquitysharesofRs.100each

11

10.

VKLimited

Journal

Date Particular LF DR.Amount Dr.Amount

MachineryAccountDr.

ToModernEquipmentManufacturersLimited

(PurchasedmachineryforRs.7,00,000from

ModernEquipmentManufacturersLimited)

70,000

70,000

ModernEquipmentManufacturersLtd.A/C

Dr.

LossonIssueof9%DebenturesAccountDr.

To9%DebenturesAccount

ToEquityShareCapitalAccount

ToSecuritiesPremiumAccount

ToPremiumonRedemptionofDebenturesA/C

(IssuedRs.1,00,0009%debenturesata

discountof10%redeemableatapremiumof

10%and50,000equitysharesofRs.10each

issuedatapremiumof15%)

6,65,000

20,000

1,00,000

5,00,000

75,000

10,000

ModernEquipmentManufacturersLtd.A/C

Dr.

ToBillsPayableAccount

(AcceptancegiventoModern

EquipmentManufacturersLimited)

35,000 35,000

11.

E,FandG

MaterialdownloadedfrommyCBSEguide.com. 19/37

Journal

Date Particulars LF Dr.Amount(Rs.) Dr.Amount(Rs.)

RealisationAccountDr.

ToLand&BuildingAccount

ToFurnitureAccount

ToMachineryAccount

ToDebtorsAccount

(IndividualAssetsaccountsclosedby

transferringtheirbalancesto

RealisationAccount)

2,76,500

1,00,000

50,000

90,000

36,500

CreditorsAccountDr.

OutstandingExpensesAccountDr.

ToRealisationAccount

(IndividualExternalLiabilities

Accountsclosedbytransferringtheir

balancestoRealisationAccount)

45,000

17,000

62,000

BankAccountDr.

ToRealisationAccount

(Land&Buildingrealized)

1,08,900

1,08,900

BankAccountDr.

ToRealisationAccount

(Furniturerealized)

12,500

12,500

BankAccountDr.

ToRealisationAccount

(MachinerySoldasscrap)

9,000

9,000

RealisationAccountDr.

ToBankAccount

(Creditorspaidatadiscountof5%)

42,750

42,750

RealisationAccountDr.

ToBankAccount 17,000

MaterialdownloadedfrommyCBSEguide.com. 20/37

(PaidoutstandingExpenses) 17,000

RealisationAccountDr.

ToF’sCapitalAccount

(RemunerationpaidtoFfor

undertakingdissolutionprocess)

5,000

5,000

E’sCapitalAccountDr.

F’sCapitalAccountDr.

G’sCapitalAccountDr.

ToRealisationAccount

(LossonRealisationtransferredto

partners’CapitalAccounts)

59,540

59,540

29,770

1,48,850

BankAccountDr.

ToG’sCapitalAccount

(FinalpaymentreceivedfromG)

30,270

30,270

E’sCapitalAccountDr.

F’sCapitalAccountDr.

ToBankAccount

(FinalpaymentmadetoEandF)

1,89,540

1,89,540

3,49,080

12.

A,BandC

Journal

Date Particular LF DR.Amount(Rs.) Dr.Amount(Rs.)

C’sCapitalAccountDr.

ToA’sCapitalAccount

(Treatmentofgoodwillduetochangein

profitsharingratio)

50,000

50,000

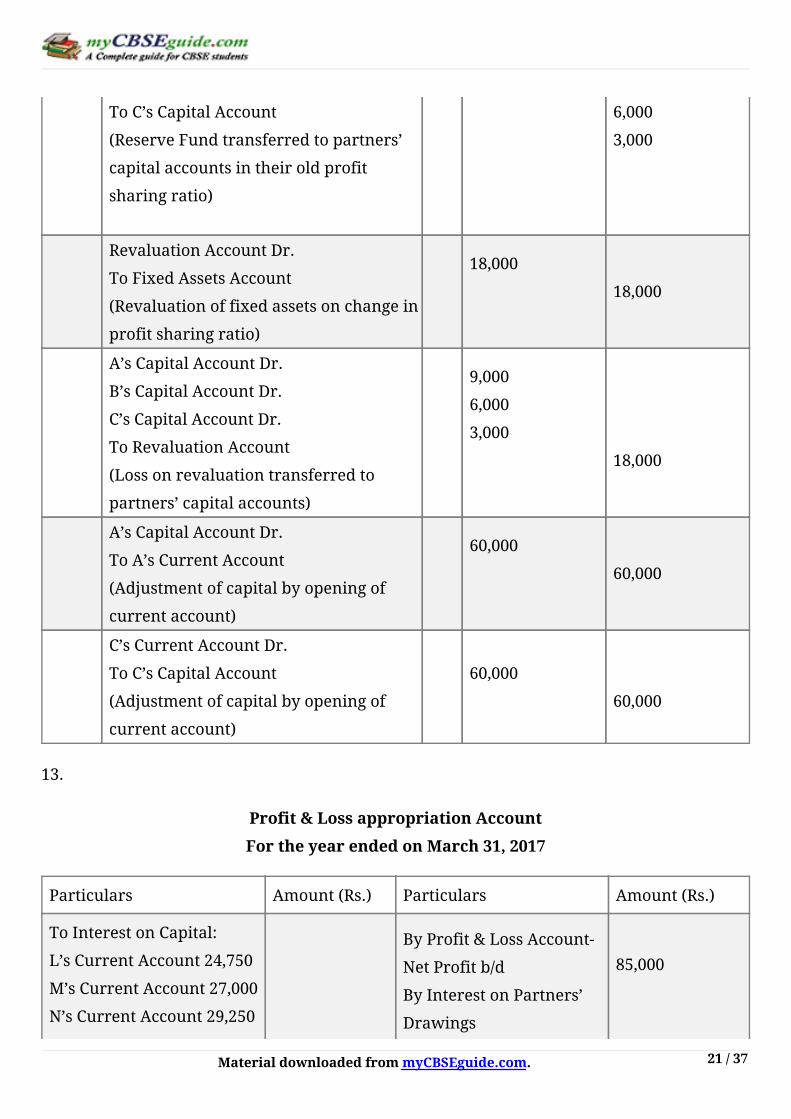

ReserveFundAccountDr.

ToA’sCapitalAccount

ToB’sCapitalAccount 18,000

9,000

MaterialdownloadedfrommyCBSEguide.com. 21/37

ToC’sCapitalAccount

(ReserveFundtransferredtopartners’

capitalaccountsintheiroldprofit

sharingratio)

6,000

3,000

RevaluationAccountDr.

ToFixedAssetsAccount

(Revaluationoffixedassetsonchangein

profitsharingratio)

18,000

18,000

A’sCapitalAccountDr.

B’sCapitalAccountDr.

C’sCapitalAccountDr.

ToRevaluationAccount

(Lossonrevaluationtransferredto

partners’capitalaccounts)

9,000

6,000

3,000

18,000

A’sCapitalAccountDr.

ToA’sCurrentAccount

(Adjustmentofcapitalbyopeningof

currentaccount)

60,000

60,000

C’sCurrentAccountDr.

ToC’sCapitalAccount

(Adjustmentofcapitalbyopeningof

currentaccount)

60,000

60,000

13.

Profit&LossappropriationAccount

FortheyearendedonMarch31,2017

Particulars Amount(Rs.) Particulars Amount(Rs.)

ToInterestonCapital:

L’sCurrentAccount24,750

M’sCurrentAccount27,000

N’sCurrentAccount29,250

ByProfit&LossAccount-

NetProfitb/d

ByInterestonPartners’

Drawings

85,000

MaterialdownloadedfrommyCBSEguide.com. 22/37

ToProfittransferredto

Partners’Current

Accounts

L1,448

M2,172

N3,620

81,000

7,240

88,240

L’sCurrentAccount720

M’sCurrentAccount1,080

N’sCurrentAccount1,440

3,240

88,240

Partner’sCapitalAccount

Date Particulars L M N Date Particulars L M N

2016

Jul1

2017

Mar

31

ToBank

Account

ToBalance

c/d

3,00,000

3,00,000

1,00,000

3,00,000

2016

Apr

1

Jul1

ByBalance

b/d

ByBank

Account

2,00,000

1,00,000

3,00,000

4,00,000

3,00,000 3,00,000 4,00,000 3,00,000 3,00,000 4,00,000

14.(6)

PPLimited

Journal

Date Particulars LFDr.Amount

Rs.

Dr.Amount

(Rs.)

(a)

(i)

BankAccountDr.

To9%DebentureApplication&Allotment

A/C

(Applicationmoneyreceivedfor5009%

Debentures)

47,000

47,000

9%DebentureApplication&AllotmentA/C

Dr.

LossonissueofDebenturesAccountDr. 47,000

MaterialdownloadedfrommyCBSEguide.com. 23/37

(ii)

To9%DebenturesAccount

ToPremiumonredemptionAccount

(Applicationmoneytransferredto9%

Debenturesaccountandrecordedlosson

issueofdebenturesandpremiumon

redemption)

7,500

50,000

4,500

(b)(i)

BankAccountDr.

To9%DebentureApplication&Allotment

A/C

(ApplicationmoneyreceivedforRs.

10,00,0009%Debentures)

12,000

12,000

(ii)

9%DebentureApplication&AllotmentA/C

Dr.

LossonissueofDebenturesAccountDr.

To9%DebenturesAccount

ToSecuritiesPremiumAccount

ToPremiumonredemptionAccount

(Applicationmoneytransferredto9%

DebenturesaccountandSecurities

PremiumReserveAccountandrecorded

lossonissueofdebenturesandpremium

onredemption)

12,00,000

1,00,000

10,00,000

2,00,000

1,00,000

(c)(i)

BankAccountDr.

To8%DebentureApplication&Allotment

A/C

(Applicationmoneyreceivedfor3,0008%

Debentures)

2,85,000

2,85,000

(ii)

8%DebentureApplication&AllotmentA/C

Dr.

LossonissueofDebenturesAccountDr.

To8%DebenturesAccount

ToPremiumonredemptionAccount

2,85,000

30,000

3,00,000

15,000

MaterialdownloadedfrommyCBSEguide.com. 24/37

(Applicationmoneytransferredto8%

Debenturesaccountandrecordedlosson

issueofdebenturesandpremiumon

redemption)

15.

DiscountonIssueof10%DebenturesAccount

Date Particulars JFAmount

(Rs)Date Particulars JF

Amount

(Rs)

2013

Apr1

To10%

Debentures

A/C

81,0002014

Mar31

By

Statement

ofProfit&

Loss

ByBalance

c/d

27,000

54,000

81,000 81,000

2014

Apr1

2015

Apr1

ToBalanceb/d

ToBalanceb/d54,000 2015Mar31

ByStatement

ofProfit&

Loss

ByBalancec/d

27,000

27,000

54,000 54,000

2015Apr1 Tobalanceb/d 27,0002016

Mar31

ByStatement

ofProfit&

Loss

ByBalancec/d

18,000

9,000

27,000 27,000

16.

MaterialdownloadedfrommyCBSEguide.com. 25/37

Journal

Date Particulars LFDr.Amount

(Rs.)

Dr.Amount

(Rs.)

BankAccountDr.

ToEquityShareApplication

Account

(Applicationmoneyreceived)

16,36,000

16,36,000

EquityShareApplicationAccount

Dr.

ToEquityShareCapitalAccount

ToEquityShareAllotment

Account

ToBankAccount

ToCallsinAdvanceAccount

(Applicationmoneytransferredto

EquityShareCapitalaccount,

EquityShareAllotmentaccount,

CallsinAdvanceaccountand

remainingamountrefunded)

16,36,000

10,00,000

5,03,500

1,10,000

22,500

EquityShareAllotmentAccount

Dr.

ToEquityShareCapitalAccount

(Allotmentmoneydueon5,00,000

15,00,000

15,00,000

BankAccountDr.

ToEquityShareAllotment

Account

(NetamountofAllotmentmoney

received)

9,96,500

9,96,500

EquityShareFirstCallAccount

MaterialdownloadedfrommyCBSEguide.com. 26/37

Dr.

ToEquityShareCapitalAccount

(FirstCallmoneydueon5,00,000

10,00,000

10,00,000

BankAccountDr.

CallsinAdvanceAccountDr.

ToEquityShareFirstCallAccount

(Firstcallmoneyreceived)

9,97,000

3,000

10,00,000

EquityShareFinalCallAccount

Dr.

ToEquityShareCapitalAccount

ToSecuritiesPremiumReserve

Account

(FinalCallmoneydueon5,00,000

includingpremiumofRs.10each)

65,00,000

15,00,000

50,00,000

BankAccountDr.

CallsinAdvanceAccountDr.

CallinArrearsAccountDr.

ToEquityShareFinalCall

Account

(Finalcallmoneyreceived)

63,89,500

19,500

91,000

65,00,000

ShareCapitalAccountDr.

SecuritiesPremiumReserve

AccountDr.

ToShareForfeitureAccount

ToCallsinArrearsAccount

(Manohar’sSharesforfeited)

70,000

70,000

49,000

91,000

BankAccountDr.

ToShareCapitalAccount

ToSecuritiesPremiumReserve

70,000

49,000

MaterialdownloadedfrommyCBSEguide.com. 27/37

Account

(ForfeitedSharesofManoharre-

issued)

21,000

ShareForfeitureAccountDr.

ToCapitalReserveAccount

(Shareforfeitedaccountin

respectof400sharestransferred

tocapitalreserveaccount)

49,000

49,000

OR

(a)

ShareforfeitureAccount

Date Particulars JFAmount

(Rs)Date Particulars JF

Amount

(Rs)

ToShare

Capital

Account

ToCapital

ReserveA/C

ToBalance

c/d

4,000

16,000

10,000

ByShare

CapitalA/C 30,000

30,000 30,000

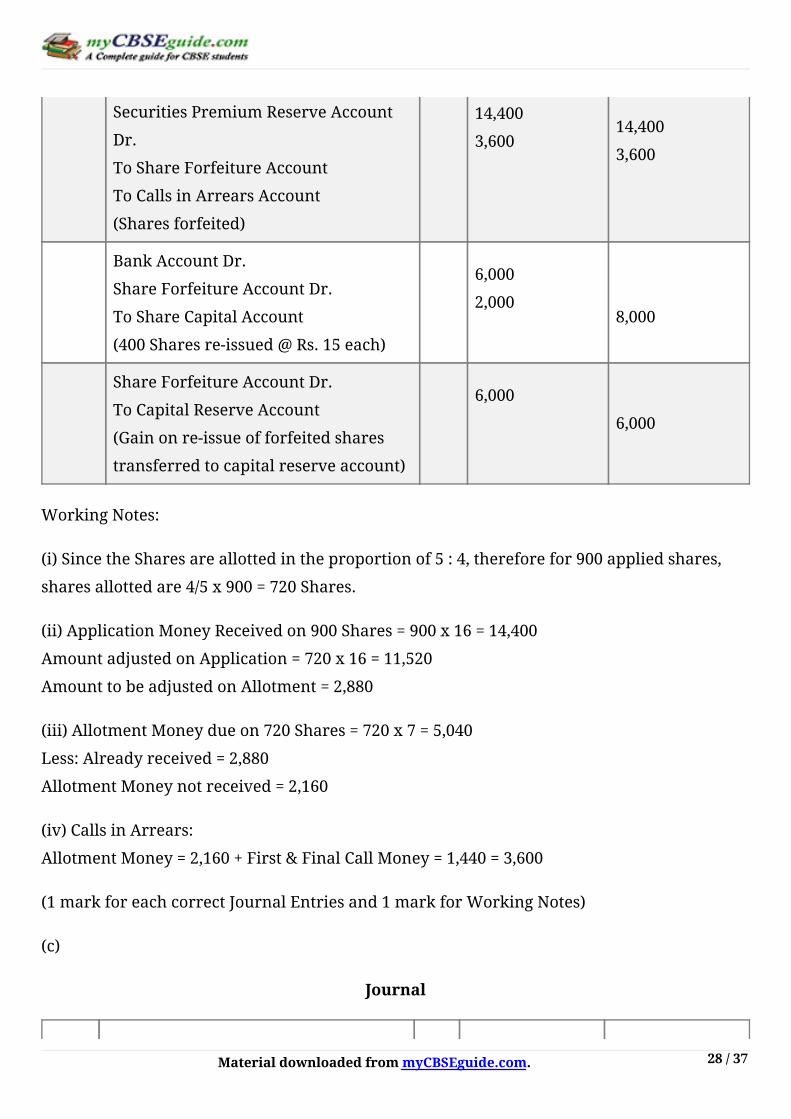

(b)

Journal

Date Particulars LF Dr.Amount(Rs.) Dr.Amount(Rs.)

ShareCapitalAccountDr.

MaterialdownloadedfrommyCBSEguide.com. 28/37

SecuritiesPremiumReserveAccount

Dr.

ToShareForfeitureAccount

ToCallsinArrearsAccount

(Sharesforfeited)

14,400

3,600

14,400

3,600

BankAccountDr.

ShareForfeitureAccountDr.

ToShareCapitalAccount

6,000

2,000

8,000

ShareForfeitureAccountDr.

ToCapitalReserveAccount

(Gainonre-issueofforfeitedshares

transferredtocapitalreserveaccount)

6,000

6,000

WorkingNotes:

(i)SincetheSharesareallottedintheproportionof5:4,thereforefor900appliedshares,

sharesallottedare4/5x900=720Shares.

(ii)ApplicationMoneyReceivedon900Shares=900x16=14,400

AmountadjustedonApplication=720x16=11,520

AmounttobeadjustedonAllotment=2,880

(iii)AllotmentMoneydueon720Shares=720x7=5,040

Less:Alreadyreceived=2,880

AllotmentMoneynotreceived=2,160

(iv)CallsinArrears:

AllotmentMoney=2,160+First&FinalCallMoney=1,440=3,600

(1markforeachcorrectJournalEntriesand1markforWorkingNotes)

(c)

Journal

MaterialdownloadedfrommyCBSEguide.com. 29/37

Date Particulars LF DR.Amount(Rs.) Dr.Amount(Rs.)

BankAccountDr.

ShareForfeitedAccountDr.

ToShareCapitalAccount

(1,200Sharesre-issuedforRs.10,800as

fullypaidup)

10,800

1,200

12,000

ShareForfeitureAccountDr.

ToCapitalReserveAccount

(Gainonre-issueofforfeitedshares

transferredtocapitalreserveaccount)

7,200

7,200

17.

RevaluationAccount

ParticularsAmount

(Rs.)Particulars

Amount

(Rs.)

ToPlant&Machinery

ToProfittransferred

toPartners’Current

Accounts

A35,375

B21,225

C14,150

20,000

70,750

ByProvisionfor

DoubtfulDebts

ByLand&Building

750

90,000

90,750 90,750

Partner’sCurrentAccounts

Date Particulars A B C Date Particulars A B C

ToC’s

Current

Account

By

Revaluation

Account

ByA’s

Current 35,375 21,225 14,150

38,250

MaterialdownloadedfrommyCBSEguide.com. 30/37

2017

Mar

31

ToProfit&

LossA/C

ToC’s

Capital

Account

38,250

1,20,500

22,950

72,300

48,200

42,150

2017

Mar

31

Account

ByB’s

Current

Account

ByGeneral

Reserve

ByBalance

c/d

37,500

85,875

22,500

51,525

22,950

15,000

1,58,750 95,250 90,350 1,58,750 95,250 90,350

Partner’sCapitalAccounts

Date Particulars A B C Date Particulars A B C

2017

Mar

31

ToBank

Account

ToC’s

Loan

Account

ToBalance

c/d

5,00,000

3,00,000

35,500

2,06,650

2017

Mar

31

ByBalance

b/d

ByC’s

Current

Account

5,00,000 3,00,000

2,00,000

42,150

5,00,000 3,00,000 2,42,150 5,00,000 3,00,000 2,42,150

BalanceSheet

AsatMarch31,2017

Liabilities Amount(Rs.) Assets Amount(Rs.)

Capitals:

A5,00,000

B3,00,000

C’sLoan

Creditors

OutstandingSalary

8,00,000

2,06,650

23,000

7,000

15,000

Bank

Stock

Debtors15,000

Less:ProvisionforD.Debts750

Plant&Machinery

Land&Building

A’sCurrentAccount

21,000

9,000

14,250

1,08,000

6,90,000

85,875

51,525

MaterialdownloadedfrommyCBSEguide.com. 31/37

B’sLoan 10,51,650 B’sCurrentAccount 10,51,650

OR

Journal

Date Particular LF Dr.Amount(Rs.) Dr.Amount(Rs.)

C’sLoanAccountDr.

ToC’sCapitalAccount

(C’sLoanaccounttransferredtohis

capitalaccount)

1,30,000

1,30,000

BankAccountDr.

ToPremiumforGoodwillAccount

(NewpartnerCbringsinhisshareof

goodwill)

17,500

17,500

PremiumforGoodwillAccountDr.

ToP’sCapitalAccount

ToK’sCapitalAccount

(PremiumforGoodwilltransferredto

oldpartners’capitalaccountsintheir

sacrificingratio)

17,500

8,750

8,750

RevaluationAccountDr.

ToPlant&MachineryAccount

(RevaluationofPlant&Machineryon

admissionofnewpartner)

14,550

14,550

Land&BuildingAccountDr.

ToRevaluationAccount

(RevaluationofLand&Buildingon

admissionofnewpartner)

28,000

28,000

RevaluationAccountDr.

ToP’sCapitalAccount

ToK’sCapitalAccount

13,450

6,725

6,725

MaterialdownloadedfrommyCBSEguide.com. 32/37

(Profitonrevaluationtransferredto

partners’capitalaccounts)

GeneralReserveAccountDr.

ToP’sCapitalAccount

ToK’sCapitalAccount

(GeneralReservetransferredto

partners’capitalaccount)

1,00,000

50,000

50,000

Profit&LossAccountDr.

ToP’sCapitalAccount

ToK’sCapitalAccount

(Profit&Lossaccounttransferredto

partners’capitalaccount)

45,000

22,500

22,500

P’sCapitalAccountDr.

K’sCapitalAccountDr.

ToBankAccount

(CashpaidtoPforadjustmentofhis

capital)

1,92,975

92,975

2,85,950

PartB

OptionI

(AnalysisofFinancialStatements)

18.Anytwoofthefollowings:

(i)Royalties

(ii)CommissionReceived

(iii)Anyotherrevenuereceipts

19.ForPPLimited:OperatingActivity½

ForGGLimited:InvestingActivity½

20.(a)

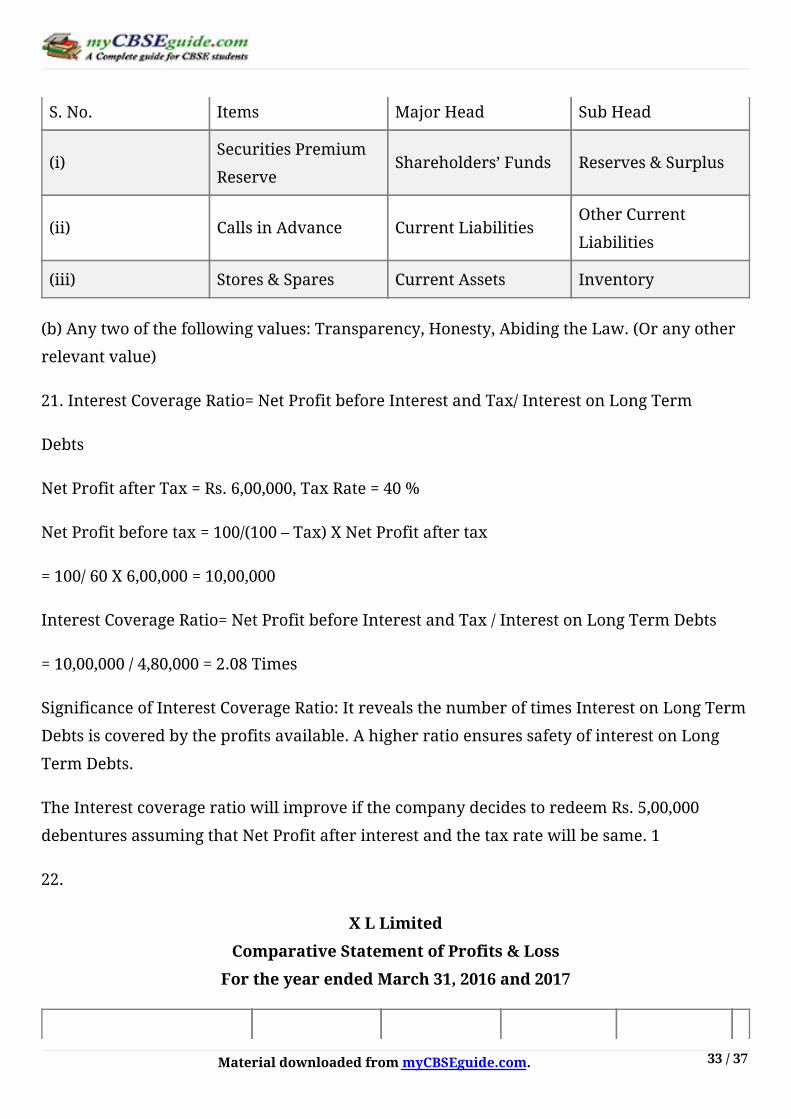

MaterialdownloadedfrommyCBSEguide.com. 33/37

S.No. Items MajorHead SubHead

(i)SecuritiesPremium

ReserveShareholders’Funds Reserves&Surplus

(ii) CallsinAdvance CurrentLiabilitiesOtherCurrent

Liabilities

(iii) Stores&Spares CurrentAssets Inventory

(b)Anytwoofthefollowingvalues:Transparency,Honesty,AbidingtheLaw.(Oranyother

relevantvalue)

21.InterestCoverageRatio=NetProfitbeforeInterestandTax/InterestonLongTerm

Debts

NetProfitafterTax=Rs.6,00,000,TaxRate=40%

NetProfitbeforetax=100/(100–Tax)XNetProfitaftertax

=100/60X6,00,000=10,00,000

InterestCoverageRatio=NetProfitbeforeInterestandTax/InterestonLongTermDebts

=10,00,000/4,80,000=2.08Times

SignificanceofInterestCoverageRatio:ItrevealsthenumberoftimesInterestonLongTerm

Debtsiscoveredbytheprofitsavailable.AhigherratioensuressafetyofinterestonLong

TermDebts.

TheInterestcoverageratiowillimproveifthecompanydecidestoredeemRs.5,00,000

debenturesassumingthatNetProfitafterinterestandthetaxratewillbesame.1

22.

XLLimited

ComparativeStatementofProfits&Loss

FortheyearendedMarch31,2016and2017

MaterialdownloadedfrommyCBSEguide.com. 34/37

Particulars 2015-16

Amount(Rs.)

2016-17

Amount(Rs.)

Absolute

Change(Rs.)

%age

Change

RevenuefromOperations

Expenses:

(a)EmployeeBenefit

Expenses:10%of

Revenuefrom

Operations

(b)OtherExpenses

NetProfitbeforeTax

Less:Tax

NetProfitafterTax

50,00,000

5,00,000

10,00,000

35,00,000

14,00,000

21,00,000

80,00,000

8,00,000

12,00,000

60,00,000

24,00,000

36,00,000

30,00,000

3,00,000

2,00,000

25,00,000

10,00,000

15,00,000

60

60

20

71.43

71.43

71.43

23.

AjantaLimited

CashFlowStatement

fortheyearended31stMarch,2014

Particulars Amount(Rs.)

I–CASHFLOWFROMOPERATINGACTIVITIES

Surplus:BalanceintheStatementofProfit&Loss

AdjustmentforNon-CashandNon-OperatingItems

Depreciation65,000

LossonsaleofMachinery3,000

InterestonDebentures28,800

OperatingProfitbeforechangesinworkingcapital

Add:DecreaseinCurrentAssetsandIncreaseinCurrent

Liabilities

Inventories40,000

OutstandingRent20,000

Creditors20,000

Less:IncreaseinCurrentAssetsandDecreaseinCurrent

Liabilities

1,20,000

96,800

2,16,800

80,000

2,16,800

(2,40,000)

2,16,800

(2,88,000)

MaterialdownloadedfrommyCBSEguide.com. 35/37

BillsPayable

CashFlowfromOperatingActivities

II-CASHFLOWFROMINVESTINGACTIVITIES

PurchaseofMachinery

SaleofMachinery

PurchaseofSharesinXYZLimited

CashFlowfromInvestingActivities

III-CASHFLOWFROMFINANCINGACTIVITIES

Issueof9%Debentures

InterestonDebentures

CashFlowfromFinancingActivities

NetCashFlow

Add:OpeningBalanceofCashandCashEquivalents

ClosingBalanceofCashandCashEquivalents

32,000

80,000

2,88,000

80,000

(28,800)

51,200

51,200

(20,000)

80,000

60,000

PlantandMachineryAccount

ParticularsAmount

(Rs.)Particulars

Amount

(Rs.)

ToBalanceb/d

ToBankAccount

13,00,000

2,40,000

ByBankAccount

ByPlant&Machinery

Account

ByStatementofProfit

&Loss

ByBalancec/d

32,000

15,000

3,000

14,90,000

15,40,000 15,40,000

AccumulatedDeprecationAccount

ParticularsAmount

(Rs.)Particulars

Amount

(Rs.)

ToPlant&Machinery

Account15,000

1,50,000

ByBalanceb/d

ByStatementofProfit

&Loss

1,00,000

65,000

MaterialdownloadedfrommyCBSEguide.com. 36/37

ToBalancec/d

1,65,000 1,65,000

Part–B

Option–II

ComputerizedAccounting

18.Sol:(c)

19.Sol:(b)

20.Sol:Thecomputerizedaccountingisonethedatabase-orientedapplicationswhereinthe

transactiondataisstoredinwell-organizeddatabase.Theuseroperatesonsuchdatabase

usingtherequiredinterfaceandalsotakestherequiredreportsbysuitabletransformations

ofstoreddataintoinformation.Therefore,thefundamentalsofcomputerizedaccounting

includeallthebasicrequirementsofanydatabase-orientedapplicationincomputers.

Accountingframework.

Itistheapplicationenvironmentofthecomputerizedaccounting.Ahealthyaccounting

frameworkintermsofaccountingprinciples,codingandgroupingstructureisapre-

condition

foranycomputerizedaccountingsystem.

Operatingprocedure.

Awell-conceivedanddesignedoperatingprocedureblendedwithsuitableoperating

environmentoftheenterpriseisnecessarytoworkwiththecomputerizedaccounting

system.

21.Incomputerizedaccountingsystem,everydaybusinesstransactionsarerecordedwith

thehelpofcomputersoftware.Logicalschemeisappliedforcodificationofaccountand

transaction.Everyaccountandtransactionisassignedauniquecode.Thegroupingof

accountsisdonefromthefirststage.

[Brieflyexplainingwhatisaccountgroupsandhierarchyofledger.]

MaterialdownloadedfrommyCBSEguide.com. 37/37

ThehierarchyofledgeraccountsismaintainedandthedataistransferredintoLedger

accountsautomaticallybythecomputer.Inordertoproduceledgeraccountsthestored

transactiondataisprocessedtoappearasclassifiedsothatsameispresentedintheformof

report.Thepreparationoffinancialstatementsisindependentofproducingthetrial

balance.

22.Internalmanipulationofaccountingrecordsismucheasierincomputerizedaccounting

duetothefollowing:

i.Defectivelogicalsequenceattheprogrammingstage

ii.Pronetohacking

23.Everyaccountingsoftwareensuresdatasecurity,safetyandconfidentiality.Therefore

every,softwareshouldprovideforthefollowing:

PasswordSecurity:Passwordisamechanism,whichenablesausertoaccessasystem

includingdata.Thesystemfacilitatesdefiningtheuserrightsaccordingto

organizationpolicy.Consequently,apersoninanorganizationmaybegivenaccessto

aparticularsetofadatawhilehemaybedeniedaccesstoanothersetofdata.

DataAudit:Thisfeatureenablesonetoknowastowhoandwhatchangeshavebeen

madeintheoriginaldatatherebyhelpingandfixingtheresponsibilityoftheperson

whohasmanipulatedthedataandalsoensuresdataintegrity.Basically,thisfeature

issimilartoAuditTrial.

DataVault:Softwareprovidesadditionalsecuritythroughdataencryption.