capitamalls asia limitedcapitamallsasia.listedcompany.com/newsroom/cma011112b.pdf · capitamalls...

TRANSCRIPT

Presentation to media and analysts *Nov 2012*

Singapore • China • Malaysia • Japan • India

Presentation to media & analysts 2 November 2012

CapitaMalls Asia Limited

Asia’s Leading Mall Developer, Owner and Manager

Presentation to media and analysts *Nov 2012*

Contents CapitaMalls Asia Overview and China

Strategy - Corporate Overview and Strengths - China Presence and Business Strategy West China Region - Overview - Chengdu - Operating Malls in West Region - New Projects in West Region North China Region - Overview - Beijing - Operating Malls in North Region - New Projects in North Region

1

Presentation to media and analysts *Nov 2012* CMA Overview and China Strategy

Presentation to media and analysts *Nov 2012*

Corporate Overview and Strengths

3

Presentation to media and analysts *Nov 2012*

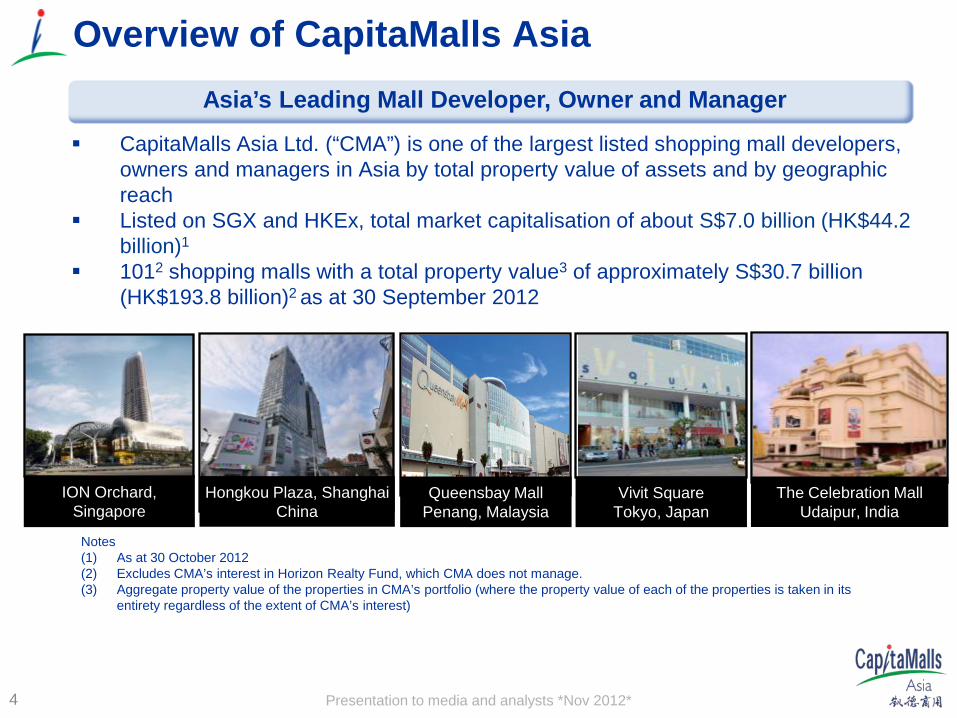

CapitaMalls Asia Ltd. (“CMA”) is one of the largest listed shopping mall developers, owners and managers in Asia by total property value of assets and by geographic reach

Listed on SGX and HKEx, total market capitalisation of about S$7.0 billion (HK$44.2 billion)1

1012 shopping malls with a total property value3 of approximately S$30.7 billion (HK$193.8 billion)2 as at 30 September 2012

Overview of CapitaMalls Asia Asia’s Leading Mall Developer, Owner and Manager

Queensbay Mall Penang, Malaysia

Vivit Square Tokyo, Japan

ION Orchard, Singapore

Hongkou Plaza, Shanghai China

The Celebration Mall Udaipur, India

Notes (1) As at 30 October 2012 (2) Excludes CMA’s interest in Horizon Realty Fund, which CMA does not manage. (3) Aggregate property value of the properties in CMA’s portfolio (where the property value of each of the properties is taken in its

entirety regardless of the extent of CMA’s interest)

4

Presentation to media and analysts *Nov 2012*

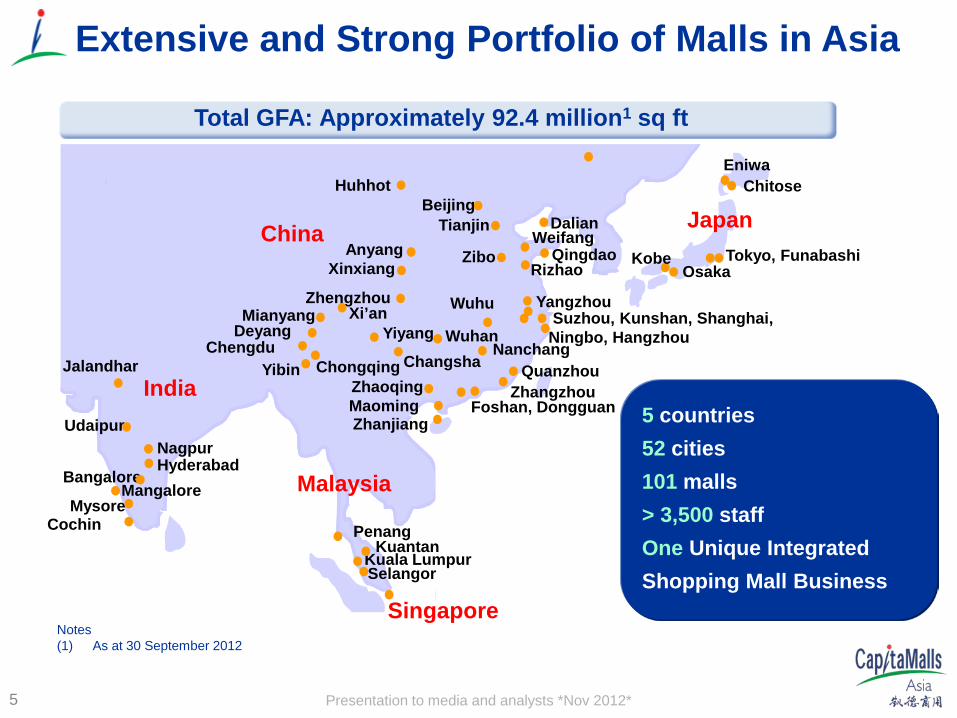

Extensive and Strong Portfolio of Malls in Asia

Total GFA: Approximately 92.4 million1 sq ft

5

India

Tokyo, Funabashi Osaka

Zhanjiang Maoming

Wuhu Suzhou, Kunshan, Shanghai, Ningbo, Hangzhou

Weifang Zibo

Beijing

Zhengzhou

Chengdu

Mianyang

China Xinxiang

Anyang

Yangzhou

Deyang

Huhhot

Foshan, Dongguan

Penang

Jalandhar

Udaipur Nagpur

Mangalore Mysore

Cochin

Bangalore Hyderabad

Tianjin

Rizhao

Yibin Chongqing

Yiyang

Changsha Quanzhou Zhangzhou

Eniwa Chitose

Xi’an

Dalian

Kobe

Wuhan

Zhaoqing

Japan

Selangor Kuala Lumpur

Malaysia

Singapore

Nanchang

5 countries 52 cities 101 malls

> 3,500 staff One Unique Integrated Shopping Mall Business

Kuantan

Qingdao

Notes (1) As at 30 September 2012

Presentation to media and analysts *Nov 2012*

From 5 Malls in 2002 to 101 Malls Today

6

Proven track record since 2002

1.8 2.7 3.1 5.2

11.3 13.3

19.4 20.4 21.9

29.4 30.7

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Sep-12

Property valuation on a 100% basis (in S$ billion)

182 659 > 3,500 Employees

Milestones

Properties 5 10 10 24 55 78 96 86 91 101

CMT listing

CRCT listing

CMA listing

CMMTlisting

CMA HK listing

Presentation to media and analysts *Nov 2012*

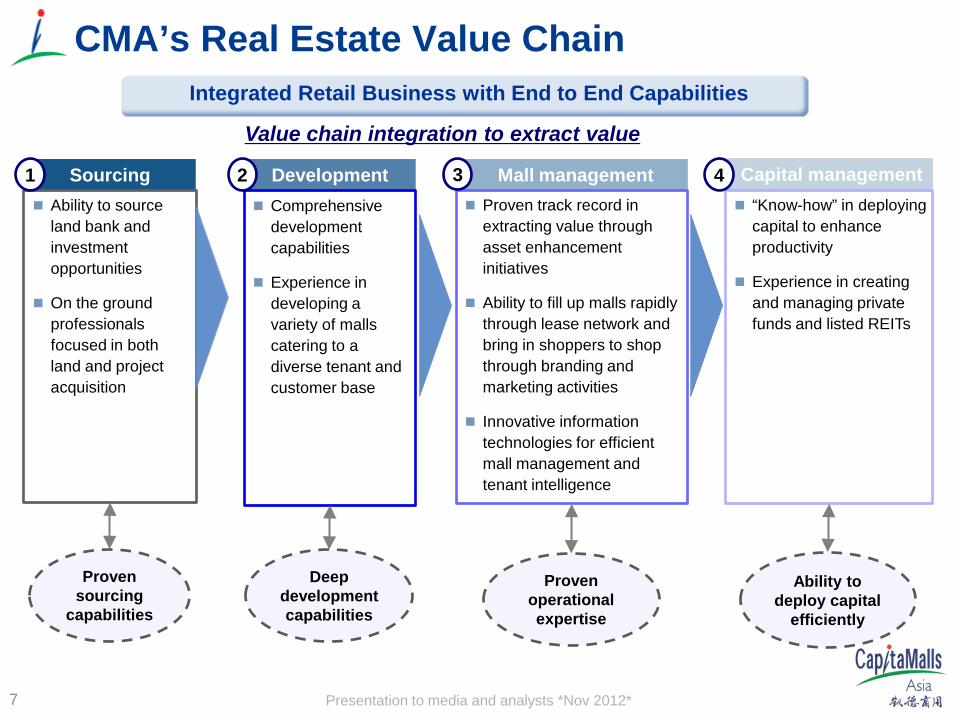

CMA’s Real Estate Value Chain Integrated Retail Business with End to End Capabilities

7

Value chain integration to extract value

Sourcing Ability to source

land bank and investment opportunities

On the ground professionals focused in both land and project acquisition

Development Comprehensive

development capabilities

Experience in developing a variety of malls catering to a diverse tenant and customer base

Capital management “Know-how” in deploying

capital to enhance productivity

Experience in creating and managing private funds and listed REITs

1

Proven sourcing

capabilities

Deep development capabilities

Ability to deploy capital

efficiently

Mall management Proven track record in

extracting value through asset enhancement initiatives

Ability to fill up malls rapidly through lease network and bring in shoppers to shop through branding and marketing activities

Innovative information technologies for efficient mall management and tenant intelligence

Proven operational expertise

2 3 4

Presentation to media and analysts *Nov 2012*

Strong Sourcing Network and Capabilities China Acquisitions in 2010, 2011 and 2012:

Designs for projects under development may be subject to change.

Shanghai

CapitaMall Tiangongyuan, Beijing

8

1

Presentation to media and analysts *Nov 2012*

Strong relationship with a wide profile of retailers including home-grown chains

and international brands

Industry-Leading Network of >10,000 Leases 2

9

Presentation to media and analysts *Nov 2012*

Attracting New Retailers Through Our International Leasing Network

In Shanghai

In Singapore

In Singapore

In Shanghai In Shanghai In Shanghai

In Penang

In Beijing

In Penang In Singapore

Highlights of New Retailers in Our Malls

10

2

Presentation to media and analysts *Nov 2012*

Partnering Our Retailers to Grow and Regionalise

11

3

• Tenant engagement programme to add value to retailers’ business • Seminars and workshops conducted by industry experts

Presentation to media and analysts *Nov 2012*

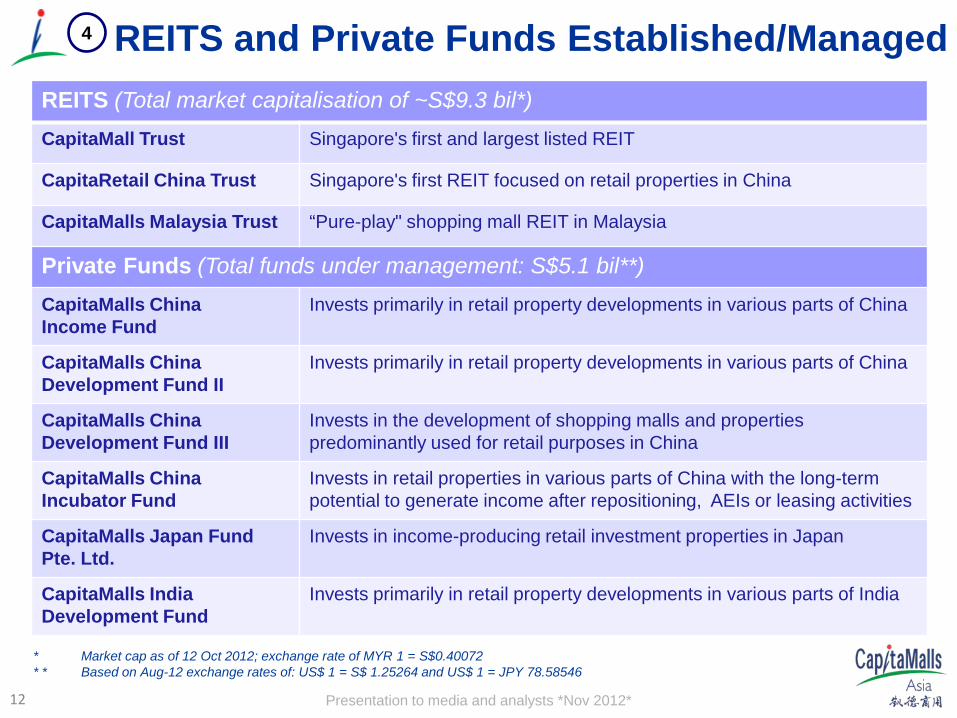

REITS and Private Funds Established/Managed 4

REITS (Total market capitalisation of ~S$9.3 bil*) CapitaMall Trust Singapore's first and largest listed REIT

CapitaRetail China Trust Singapore's first REIT focused on retail properties in China

CapitaMalls Malaysia Trust “Pure-play" shopping mall REIT in Malaysia

Private Funds (Total funds under management: S$5.1 bil**) CapitaMalls China Income Fund

Invests primarily in retail property developments in various parts of China

CapitaMalls China Development Fund II

Invests primarily in retail property developments in various parts of China

CapitaMalls China Development Fund III

Invests in the development of shopping malls and properties predominantly used for retail purposes in China

CapitaMalls China Incubator Fund

Invests in retail properties in various parts of China with the long-term potential to generate income after repositioning, AEIs or leasing activities

CapitaMalls Japan Fund Pte. Ltd.

Invests in income-producing retail investment properties in Japan

CapitaMalls India Development Fund

Invests primarily in retail property developments in various parts of India

* Market cap as of 12 Oct 2012; exchange rate of MYR 1 = S$0.40072 * * Based on Aug-12 exchange rates of: US$ 1 = S$ 1.25264 and US$ 1 = JPY 78.58546

12

Presentation to media and analysts *Nov 2012*

China Presence and Business Strategy

13

Presentation to media and analysts *Nov 2012*

CapitaMalls Asia’s Presence in China Leverage on Group Presence Since 1994

Minhang Plaza, Shanghai, China Hongkou Plaza, Shanghai, China

Raffles City Shanghai

Strong Understanding of China Retail Real Estate Market

Over 15 Years of

experience

14

Presentation to media and analysts *Nov 2012*

Malls are Strategically Located in Large Population Catchment Areas

Raffles City Beijing CapitaMall Jinniu, Chengdu CapitaMall Dongguan

CapitaMall Saihan, Huhhot CapitaMall Yuhuating, Changsha CapitaMall Qibao, Shanghai

One-stop shopping, dining and entertainment destinations within sizeable population catchment areas

Well-positioned and accessible via major transportation routes

15

Presentation to media and analysts *Nov 2012*

Suzhou

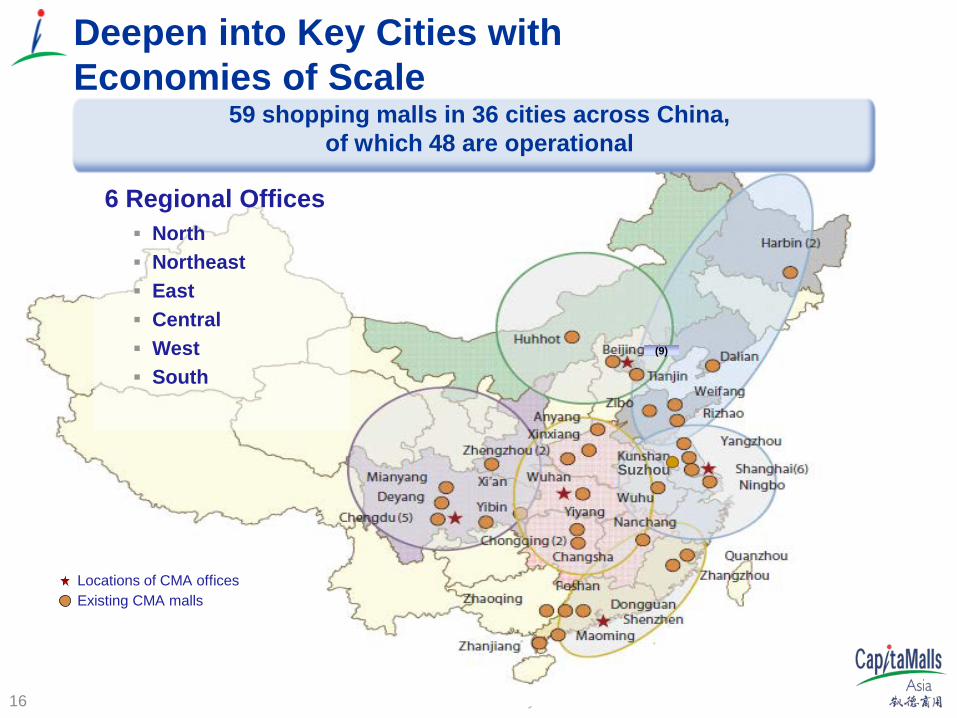

Deepen into Key Cities with Economies of Scale

59 shopping malls in 36 cities across China, of which 48 are operational

16

Existing CMA malls Locations of CMA offices

6 Regional Offices North Northeast East Central West South

(9)

Presentation to media and analysts *Nov 2012*

3

5,950 6,718 7,641

8,921

10,849

13,268

15,700

18,123

2004 2005 2006 2007 2008 2009 2010 2011

2

Rising Disposable Income per Capita (RMB) Creating Stimulus for Consumption

RMB Bil

9,422 10,493 11,759

13,786 15,781

17,175 19,109

21,810

2004 2005 2006 2007 2008 2009 2010 2011

RMB

30.9% 35.8%

42.5% 47.0% 51.1% 55.0% 58.6% 61.9%

1995 2000 2005 2010 2015 2020 2025 2030

Increasing Urbanisation – Projected to reach 61.9% in 2030 1

Strong Potential for Shopping Mall Sector in China, especially in Tier 2 and 3 cities

Retailers Continue to Enjoy Strong Sales

China Fundamentals Remain Strong

Source: National Bureau of Statistics of China

Source: United Nations Source: National Bureau of Statistics of China

17

Presentation to media and analysts *Nov 2012*

Chengdu

Anyang Mall

Zhengzhou Xinxiang

Chongqing

Foshan

Coastal Cities

Wuhan

Shenzhen

Zhengzhou

Chengdu

Inland Plants

Changsha

Tianjin

Beijing

Shanghai

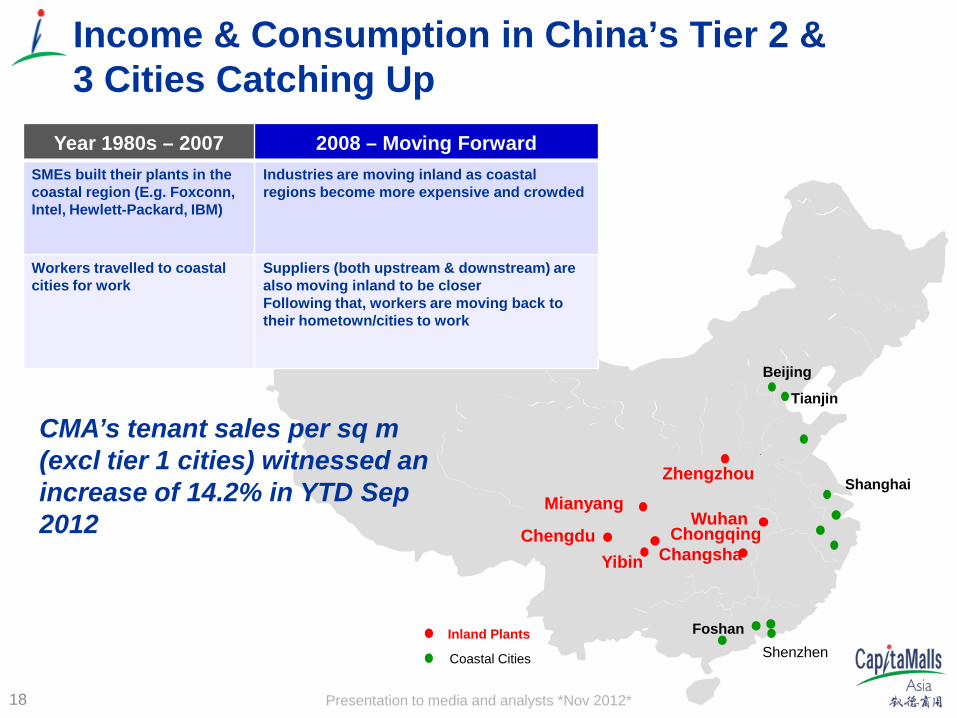

Year 1980s – 2007 2008 – Moving Forward SMEs built their plants in the coastal region (E.g. Foxconn, Intel, Hewlett-Packard, IBM)

Industries are moving inland as coastal regions become more expensive and crowded

Workers travelled to coastal cities for work

Suppliers (both upstream & downstream) are also moving inland to be closer Following that, workers are moving back to their hometown/cities to work

CMA’s tenant sales per sq m (excl tier 1 cities) witnessed an increase of 14.2% in YTD Sep 2012

Mianyang

Yibin

Income & Consumption in China’s Tier 2 & 3 Cities Catching Up

18

Presentation to media and analysts *Nov 2012*

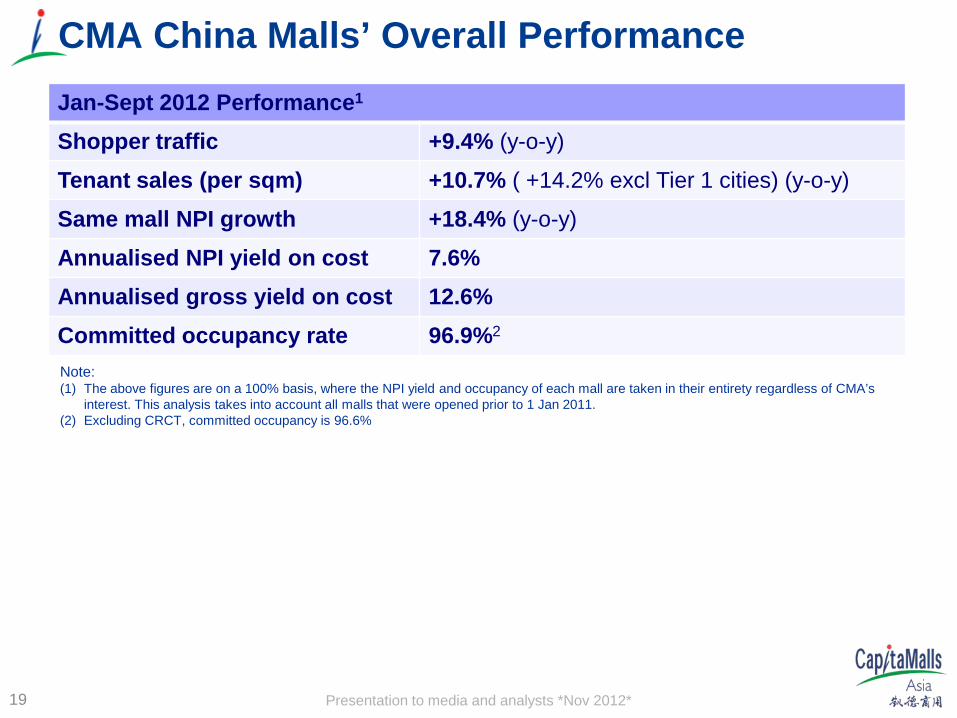

CMA China Malls’ Overall Performance

19

Jan-Sept 2012 Performance1 Shopper traffic +9.4% (y-o-y)

Tenant sales (per sqm) +10.7% ( +14.2% excl Tier 1 cities) (y-o-y)

Same mall NPI growth +18.4% (y-o-y) Annualised NPI yield on cost 7.6%

Annualised gross yield on cost 12.6%

Committed occupancy rate 96.9%2

Note: (1) The above figures are on a 100% basis, where the NPI yield and occupancy of each mall are taken in their entirety regardless of CMA’s

interest. This analysis takes into account all malls that were opened prior to 1 Jan 2011. (2) Excluding CRCT, committed occupancy is 96.6%

Presentation to media and analysts *Nov 2012*

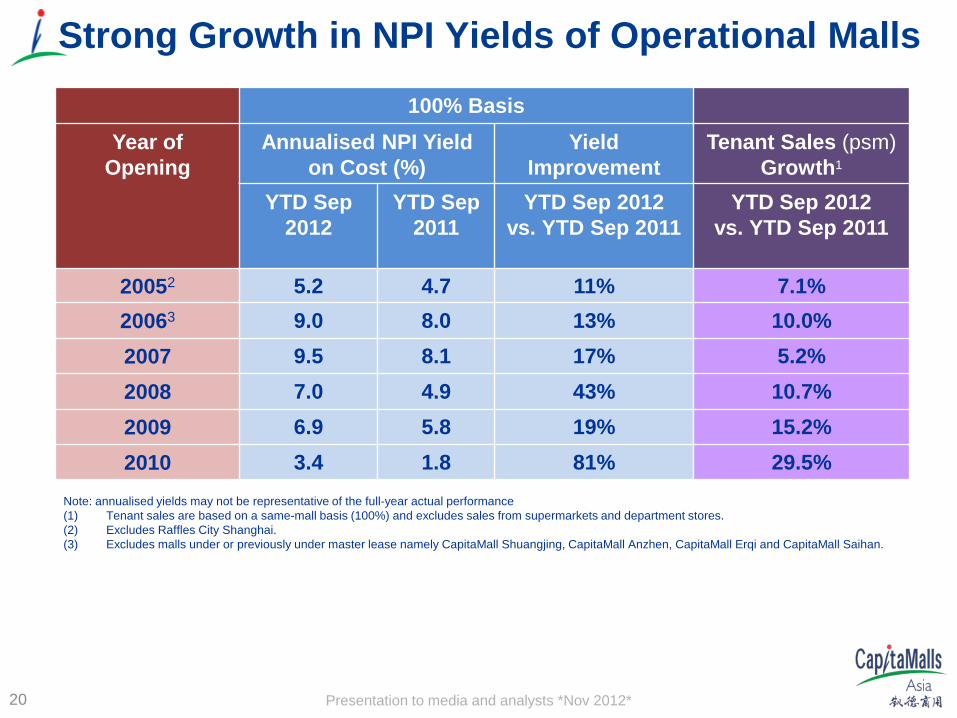

Strong Growth in NPI Yields of Operational Malls

20

100% Basis

Year of Opening

Annualised NPI Yield on Cost (%)

Yield Improvement

Tenant Sales (psm) Growth1

YTD Sep 2012

YTD Sep 2011

YTD Sep 2012 vs. YTD Sep 2011

YTD Sep 2012 vs. YTD Sep 2011

20052 5.2 4.7 11% 7.1% 20063 9.0 8.0 13% 10.0% 2007 9.5 8.1 17% 5.2% 2008 7.0 4.9 43% 10.7% 2009 6.9 5.8 19% 15.2%

2010 3.4 1.8 81% 29.5% Note: annualised yields may not be representative of the full-year actual performance (1) Tenant sales are based on a same-mall basis (100%) and excludes sales from supermarkets and department stores. (2) Excludes Raffles City Shanghai. (3) Excludes malls under or previously under master lease namely CapitaMall Shuangjing, CapitaMall Anzhen, CapitaMall Erqi and CapitaMall Saihan.

Presentation to media and analysts *Nov 2012* 21 West China Region CapitaMall Jinniu, Chengdu, China

Presentation to media and analysts *Nov 2012*

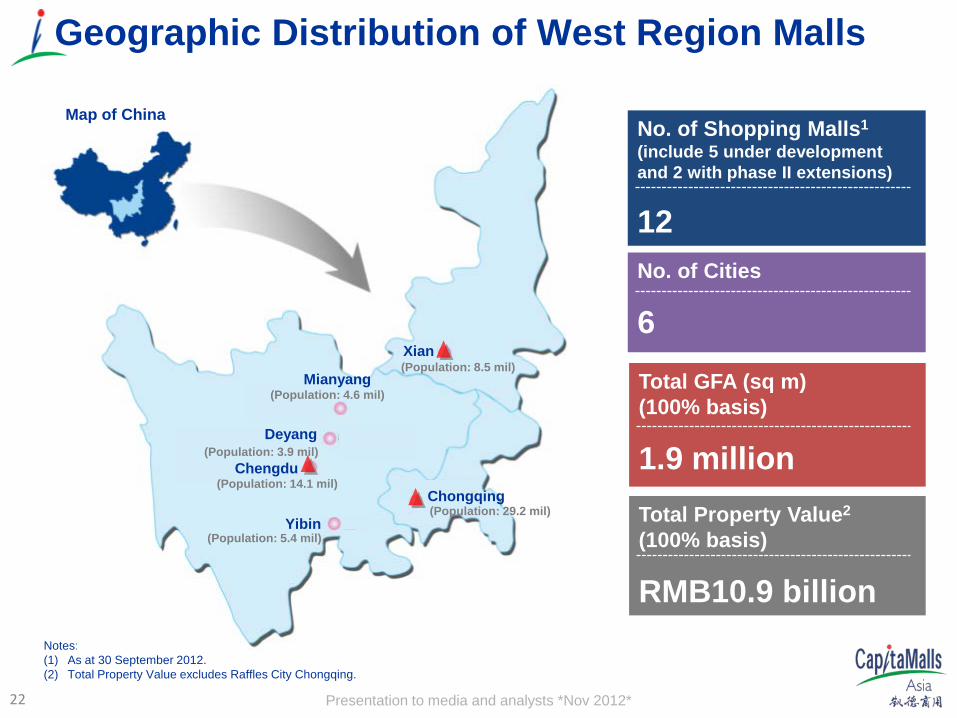

Geographic Distribution of West Region Malls

No. of Shopping Malls1 (include 5 under development and 2 with phase II extensions)

12 No. of Cities

6 Total GFA (sq m) (100% basis)

1.9 million Total Property Value2 (100% basis)

RMB10.9 billion Notes: (1) As at 30 September 2012. (2) Total Property Value excludes Raffles City Chongqing.

Map of China

Mianyang

Chengdu

Deyang

Yibin

Chongqing

Xian

(Population: 4.6 mil)

(Population: 14.1 mil)

(Population: 8.5 mil)

(Population: 5.4 mil)

(Population: 29.2 mil)

(Population: 3.9 mil)

22

Presentation to media and analysts *Nov 2012*

Chengdu

23

Presentation to media and analysts *Nov 2012* 24

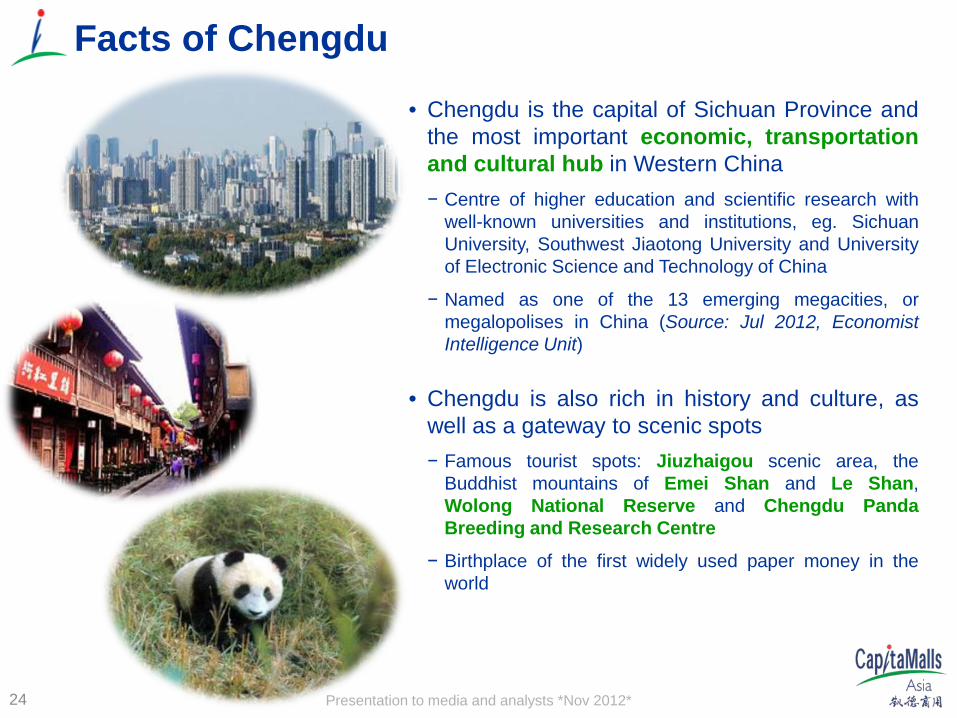

Facts of Chengdu

• Chengdu is the capital of Sichuan Province and the most important economic, transportation and cultural hub in Western China − Centre of higher education and scientific research with

well-known universities and institutions, eg. Sichuan University, Southwest Jiaotong University and University of Electronic Science and Technology of China

− Named as one of the 13 emerging megacities, or megalopolises in China (Source: Jul 2012, Economist Intelligence Unit)

• Chengdu is also rich in history and culture, as well as a gateway to scenic spots − Famous tourist spots: Jiuzhaigou scenic area, the

Buddhist mountains of Emei Shan and Le Shan, Wolong National Reserve and Chengdu Panda Breeding and Research Centre

− Birthplace of the first widely used paper money in the world

Presentation to media and analysts *Nov 2012*

Excellent Connectivity Around the World

Source: Chengdu Shuangliu International Airport, Chengdu Metro.

25

Extensive Transportation Network that Enhances Chengdu’s Accessibility

Chengdu Shuangliu International Airport

Air

High-speed Railway Railway Highway

Chengdu Highway

• 3 national highways that links Sichuan Province to Shanxi Province, Tibet and Yunnan Province

• 8 expressways to Chongqing, Mianyang, Leshan, Ya’an, Dazhou and Dujiangyan

• 5th busiest airport in China & handled 29 million passengers in 2011 (12.6% increase from 2010)

• Flights to 92 domestic and 19 international destinations, including Amsterdam, New Delhi, Bangalore, Mumbai, Singapore, Hong Kong, Macao, Tokyo, Seoul, etc.

• High-speed railway: − Chengdu-Dujiangyan high speed railway

(completed) − Shanghai–Wuhan–Chengdu high speed

railway (2013) − Chengdu-Chongqing high speed railway

(2014) − Xian-Chengdu high speed railway (2014)

Metro

• Existing subway lines 1 & 2 • Planning subway lines 3 – 7 to be operational by 2017 • Expected to carry 13.1 million passengers per day by 2020

Presentation to media and analysts *Nov 2012*

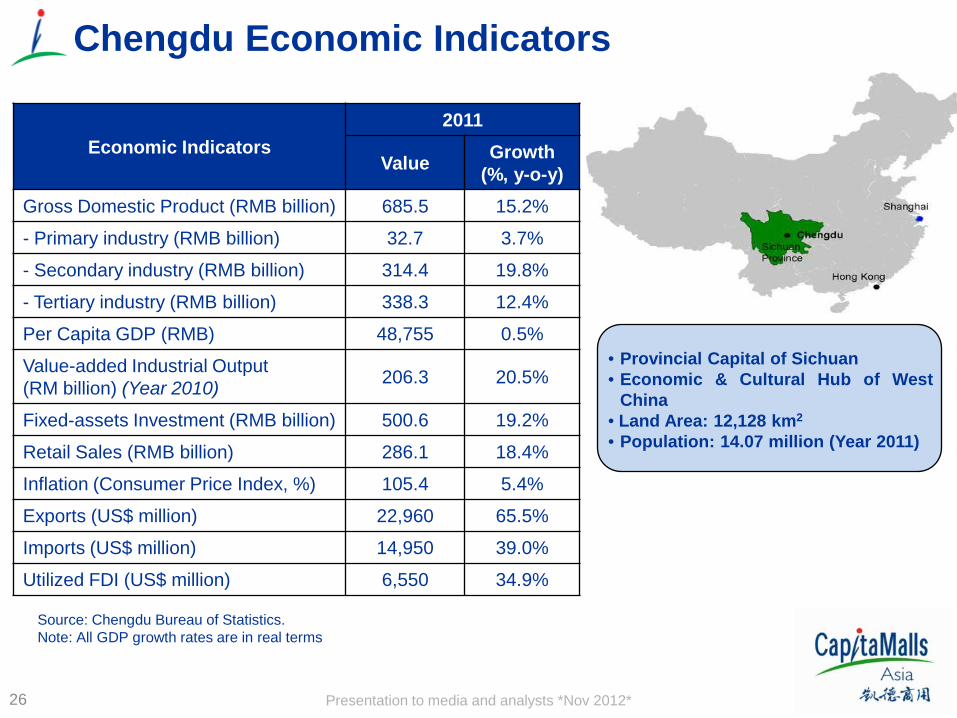

Chengdu Economic Indicators

Economic Indicators 2011

Value Growth (%, y-o-y)

Gross Domestic Product (RMB billion) 685.5 15.2%

- Primary industry (RMB billion) 32.7 3.7%

- Secondary industry (RMB billion) 314.4 19.8%

- Tertiary industry (RMB billion) 338.3 12.4%

Per Capita GDP (RMB) 48,755 0.5%

Value-added Industrial Output (RM billion) (Year 2010) 206.3 20.5%

Fixed-assets Investment (RMB billion) 500.6 19.2%

Retail Sales (RMB billion) 286.1 18.4%

Inflation (Consumer Price Index, %) 105.4 5.4%

Exports (US$ million) 22,960 65.5%

Imports (US$ million) 14,950 39.0%

Utilized FDI (US$ million) 6,550 34.9%

Source: Chengdu Bureau of Statistics. Note: All GDP growth rates are in real terms

26

• Provincial Capital of Sichuan • Economic & Cultural Hub of West

China • Land Area: 12,128 km2

• Population: 14.07 million (Year 2011)

Presentation to media and analysts *Nov 2012* 27

Chengdu Population Growth

Source: Chengdu Bureau of Statistics Note: Total population includes long-stay residents

2007 2008 2009 2010 2011 Population (m) 12.53 12.71 12.87 14.05 14.07 % Growth - 1.4% 1.3% 9.2% 0.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.50

12.00

12.50

13.00

13.50

14.00

14.50

mill

ion

Presentation to media and analysts *Nov 2012*

Source: Statistical bureau of various cities

Chengdu: One of China’s Fastest Growing Cities

28

100%

150%

200%

250%

2005 2006 2007 2008 2009 2010 2011

Per Capita GDP

RMB 2005 2006 2007 2008 2009 2010 2011

Beijing 45,993 52,054 61,274 66,797 70,452 75,943 80,394

Shanghai 49,649 54,858 62,041 66,932 69,164 76,074 82,560

Chengdu 19,670 22,445 26,849 31,203 35,215 48,510 48,755

100%

150%

200%

250%

300%

2005 2006 2007 2008 2009 2010 2011

GDP

RMB bil 2005 2006 2007 2008 2009 2010 2011

Beijing 689 772 901 1,049 1,187 1,378 1,600

Shanghai 914 1,030 1,200 1,370 1,505 1,717 1,920

Chengdu 238 277 332 394 450 555 685

Average GDP growth of 19.3%, above China’s average of 9.2%

Presentation to media and analysts *Nov 2012*

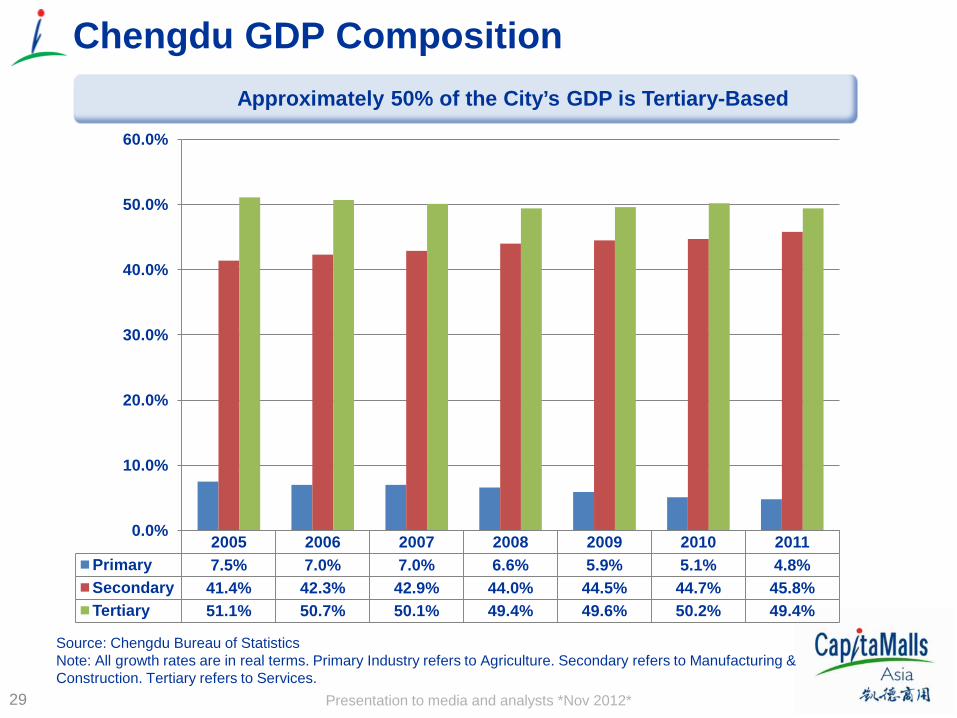

Chengdu GDP Composition

Source: Chengdu Bureau of Statistics Note: All growth rates are in real terms. Primary Industry refers to Agriculture. Secondary refers to Manufacturing & Construction. Tertiary refers to Services.

29

2005 2006 2007 2008 2009 2010 2011 Primary 7.5% 7.0% 7.0% 6.6% 5.9% 5.1% 4.8% Secondary 41.4% 42.3% 42.9% 44.0% 44.5% 44.7% 45.8% Tertiary 51.1% 50.7% 50.1% 49.4% 49.6% 50.2% 49.4%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Approximately 50% of the City’s GDP is Tertiary-Based

Presentation to media and analysts *Nov 2012*

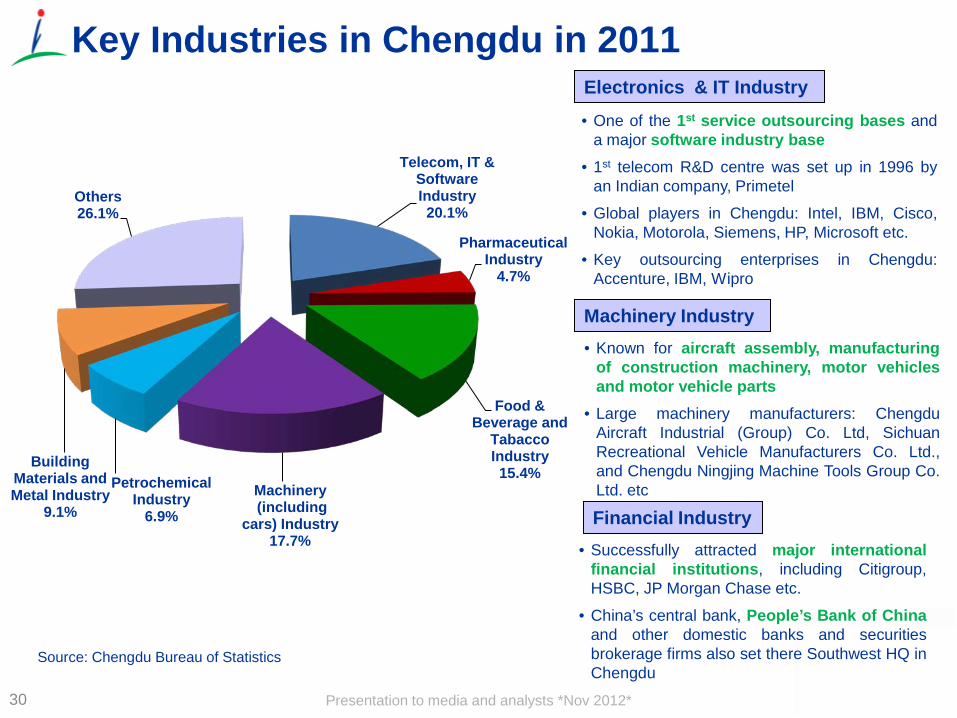

Key Industries in Chengdu in 2011

Source: Chengdu Bureau of Statistics

30

Telecom, IT & Software Industry 20.1%

Pharmaceutical Industry

4.7%

Food & Beverage and

Tabacco Industry 15.4%

Machinery (including

cars) Industry 17.7%

Petrochemical Industry

6.9%

Building Materials and Metal Industry

9.1%

Others 26.1%

• One of the 1st service outsourcing bases and a major software industry base

• 1st telecom R&D centre was set up in 1996 by an Indian company, Primetel

• Global players in Chengdu: Intel, IBM, Cisco, Nokia, Motorola, Siemens, HP, Microsoft etc.

• Key outsourcing enterprises in Chengdu: Accenture, IBM, Wipro

Electronics & IT Industry

Financial Industry

Machinery Industry • Known for aircraft assembly, manufacturing

of construction machinery, motor vehicles and motor vehicle parts

• Large machinery manufacturers: Chengdu Aircraft Industrial (Group) Co. Ltd, Sichuan Recreational Vehicle Manufacturers Co. Ltd., and Chengdu Ningjing Machine Tools Group Co. Ltd. etc

• Successfully attracted major international financial institutions, including Citigroup, HSBC, JP Morgan Chase etc.

• China’s central bank, People’s Bank of China and other domestic banks and securities brokerage firms also set there Southwest HQ in Chengdu

Presentation to media and analysts *Nov 2012*

Source: Statistical bureau of various cities

Chengdu: One of China’s Fastest Growing Cities

31

RMB bil 2005 2006 2007 2008 2009 2010 2011

Beijing 291 330 384 465 531 623 690

Shanghai 298 338 387 458 517 607 678

Chengdu 101 116 136 162 205 242 286

RMB 2005 2006 2007 2008 2009 2010 2011

Beijing 17,653 19,978 21,989 24,725 26,738 29,073 32,903

Shanghai 18,645 20.668 23,623 26,675 28,838 31,838 36,230

Chengdu 11,359 12,789 14,849 16,943 18,659 20,836 23,932

Stronger Disposable Income Per Capita & Retail Sales Growth

Disposable Income Per Capita

100%

120%

140%

160%

180%

200%

220%

2005 2006 2007 2008 2009 2010 2011

Retail Sales

100%

150%

200%

250%

300%

2005 2006 2007 2008 2009 2010 2011

Presentation to media and analysts *Nov 2012*

1 金牛 Jinniu

2 沙湾 Shawan

来福士 Raffles City 3

4 天府 Tianfu

Chengdu Major Micro-Markets

Source: CBRE

5

魅力城 Meilicheng

Major Office Areas 1. CBD 2. South Renmin Road

Major Retail Areas 3. Chunxi Road 4. Yanshikou

Major Luxury Residential Areas 5. Qingshuihe-Shuangnan 6. Zijing 7. Dongdajie-Wangjiang 8. South New City 9. Jianshe Road

Major Industrial Areas 10. Chengdu HIDZ1 (West Park) 11. Chengdu HIDZ1 (South Park) 12. Chengdu ETDZ2

Notes: (1) Refers to High-tech Industrial Development Zone. (2) Refers to Economic & Technological Development Zone.

CMA Projects in Chengdu

32

Presentation to media and analysts *Nov 2012*

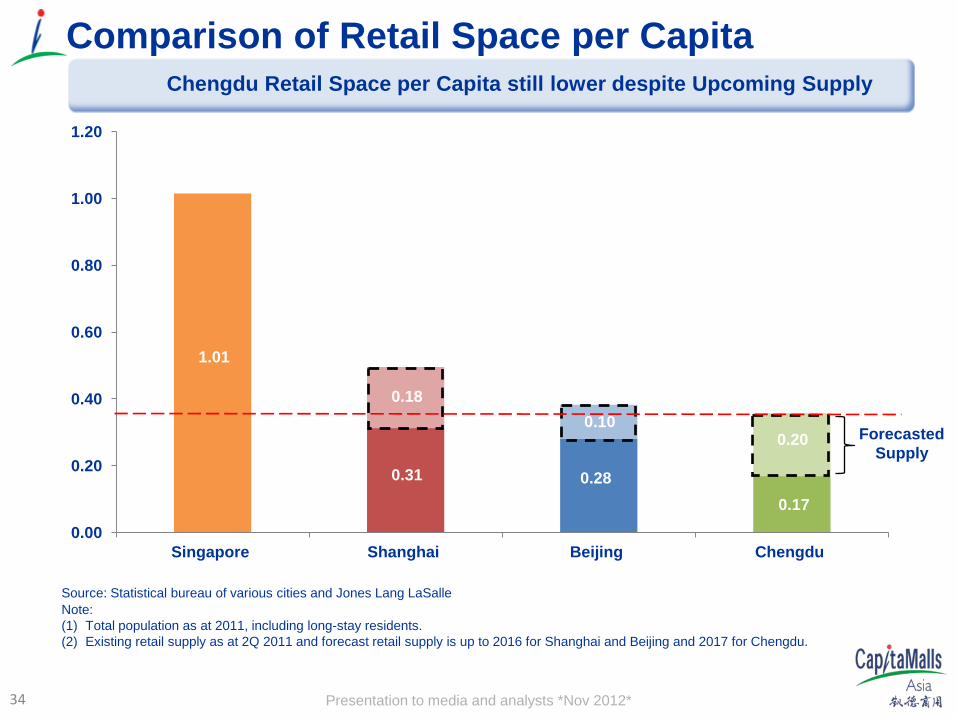

Chengdu Retail Supply and Retail Space Per Capita

Source: Chengdu Bureau of Statistics and Jones Lang LaSalle and Cushman & Wakefield Note: Population includes long-stay residents and population growth from 2012 to beyond 2014 is based on a 2.2% increase

per annum.

33

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

0 100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000 900,000

1,000,000 1,100,000 1,200,000 1,300,000 1,400,000

Ret

ail S

pace

per

Cap

ita

Ret

ail G

FA (s

q m

)

Total Departmental Store Supply Total Shopping Mall Supply Retail Space Per Capita

Presentation to media and analysts *Nov 2012*

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Singapore Shanghai Beijing Chengdu

0.31

0.18 0.10

Comparison of Retail Space per Capita

Note: (1) Total population as at 2011, including long-stay residents. (2) Existing retail supply as at 2Q 2011 and forecast retail supply is up to 2016 for Shanghai and Beijing and 2017 for Chengdu.

0.28 0.17

Forecasted Supply

Source: Statistical bureau of various cities and Jones Lang LaSalle

1.01

0.20

Chengdu Retail Space per Capita still lower despite Upcoming Supply

34

Presentation to media and analysts *Nov 2012*

Operating Malls in West Region

35

Presentation to media and analysts *Nov 2012*

2.4% 2.7%

5.3%

7.1%

8.7%

2007 2008 2009 2010 2011

Net Property Income Yield1 Occupancy

Opened in Sep 2006

Case Study: Opening of CapitaMall Jinniu

Capital Value (RMB’ million)

Challenges faced in the first 2 years due to entry into new market

92%

95%

99% 100% 100%

2007 2008 2009 2010 2011

Note: Refers to net property income yield on cost.

363 364 394 415

455

2007 2008 2009 2010 2011

36

Presentation to media and analysts *Nov 2012*

752 884

1,033

2009 2010 2011

9,213 11,372

14,998 16,606 16,270

2007 2008 2009 2010 2011

Shopper Traffic (‘000) Tenants’ Sales per sq m1 (RMB)

CAGR: 15.3% p.a. CAGR: 17.2% p.a.

We Persevered & Grew Our Business

Note: Excludes supermarket GTO sales. 37

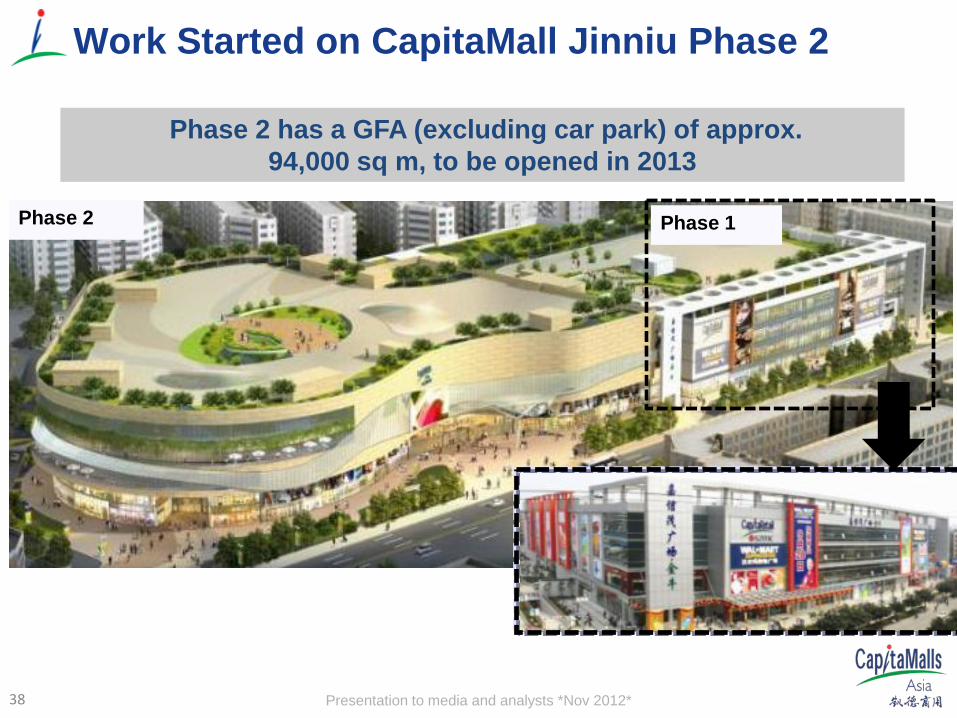

Presentation to media and analysts *Nov 2012* 38

Phase 1 Phase 2

Work Started on CapitaMall Jinniu Phase 2

Phase 2 has a GFA (excluding car park) of approx. 94,000 sq m, to be opened in 2013

Presentation to media and analysts *Nov 2012* 39

CapitaMall Jinniu Positioning Largest One-Stop Shopping Mall in Jinniu District

Positioned as a Mid-High End Mall with a Target Catchment of approx. 800,000 population (5 km radius)

• Existing Tenants in Jinniu Phase 1:

• Potential Prospects for Jinniu Phase 2:

Presentation to media and analysts *Nov 2012* 40

Key Statistics: CapitaMall Jinniu Phase I Opening Date: September 2006

Location: Jinniu district in Chengdu’s northwest, amidst government buildings, high-end residences and reputable schools

GFA (excluding car park)

~57,800 sq m

NLA ~48,400 sq m

No. of Floors 5 (including 1 basement)

No. of Car park spaces

390

Key retailers: Walmart, KFC, Pizza Hut, Watsons, CSC,Vero Moda, DQ, New Dynamic Institute, Highwave Sports, Belle, Basic House, Mind Bridge, I’M DAVID

CapitaMall Jinniu, Chengdu (Phase I)

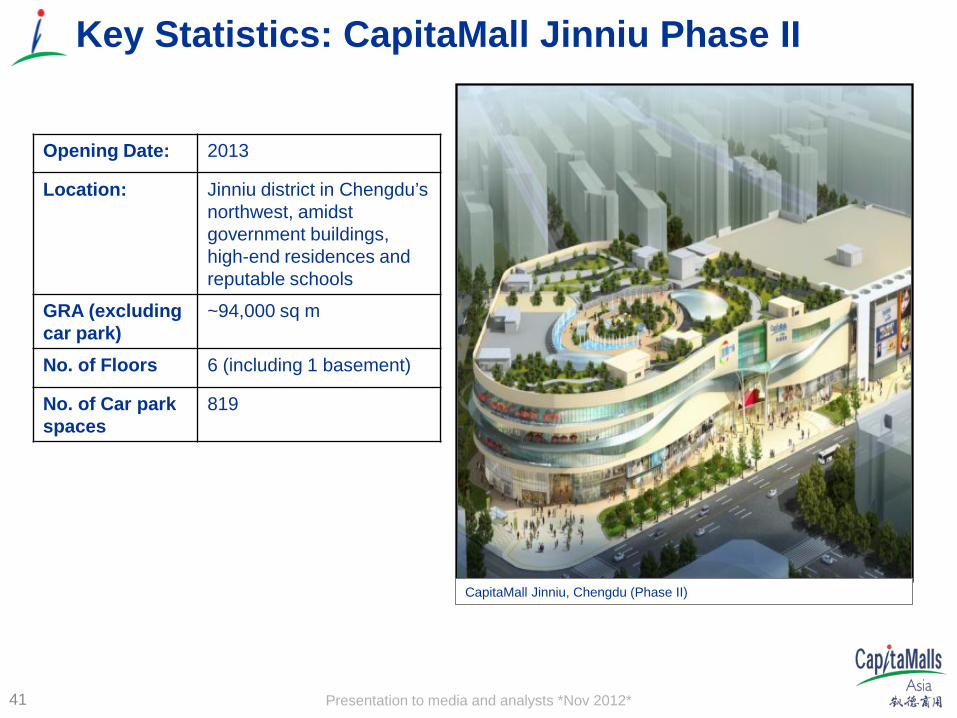

Presentation to media and analysts *Nov 2012* 41

Opening Date: 2013

Location: Jinniu district in Chengdu’s northwest, amidst government buildings, high-end residences and reputable schools

GRA (excluding car park)

~94,000 sq m

No. of Floors 6 (including 1 basement)

No. of Car park spaces

819

Key Statistics: CapitaMall Jinniu Phase II

CapitaMall Jinniu, Chengdu (Phase II)

Presentation to media and analysts *Nov 2012* 42

Key Statistics: CapitaMall Shawan

Opening date September 2009

Location Within Shawan’s economic centre and the city’s Second Ring Road

GFA (excluding car park)

~38,600 sq m

NLA ~26,700 sq m No. of floors 5 (including 1 basement)

No. of car park spaces

268

Key retailers Century Mart Supermarket, Zi Jin Cinema, Starbucks, KFC, Mannings, Ajisen Ramen, Highwave Sports, Jack & Jones, Vero Moda, Only

Presentation to media and analysts *Nov 2012*

Key Statistics: CapitaMall Shapingba

43

Opening date: April 2008

Location: At the core of Chongqing commercial district and opposite Chongqing’s North train station

GFA (excluding car park)

~41,900 sq m

NLA ~26,900 sq m

No. of floors 7 (including 2 basements)

Key retailers Sephora, Haagen Dazs, Yonghui Supermarket, Guess, Pizza Hut, KFC, Watsons, Esprit, Cache Cache, Adidas, Lee, Vero Moda, Jack Jones, G200, Baby Fox

Presentation to media and analysts *Nov 2012* 44

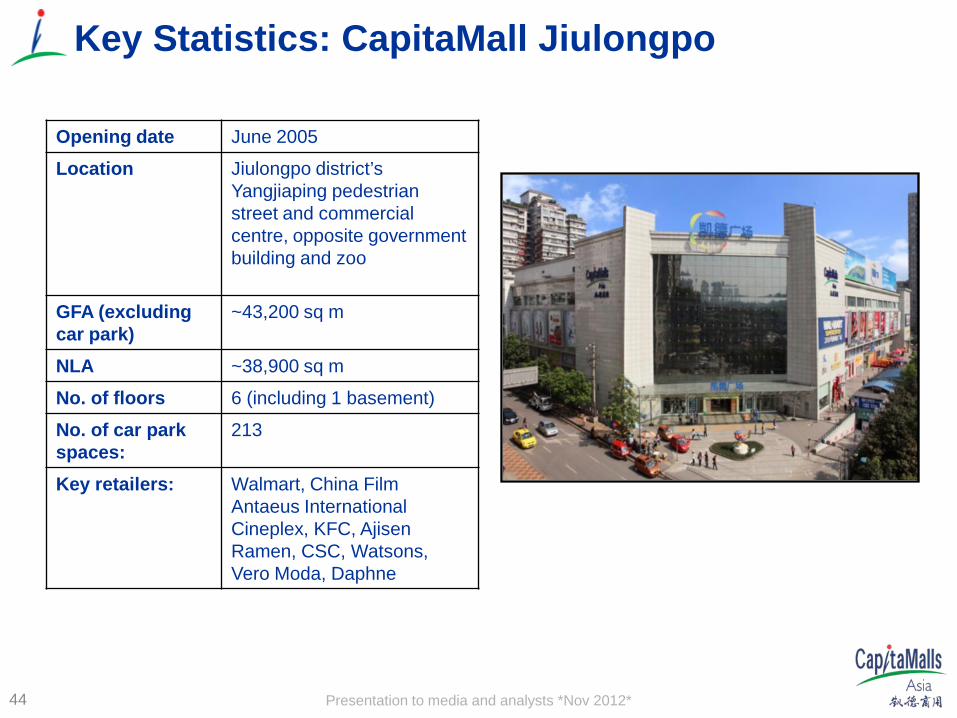

Key Statistics: CapitaMall Jiulongpo

Opening date June 2005

Location Jiulongpo district’s Yangjiaping pedestrian street and commercial centre, opposite government building and zoo

GFA (excluding car park)

~43,200 sq m

NLA ~38,900 sq m

No. of floors 6 (including 1 basement)

No. of car park spaces:

213

Key retailers: Walmart, China Film Antaeus International Cineplex, KFC, Ajisen Ramen, CSC, Watsons, Vero Moda, Daphne

Presentation to media and analysts *Nov 2012*

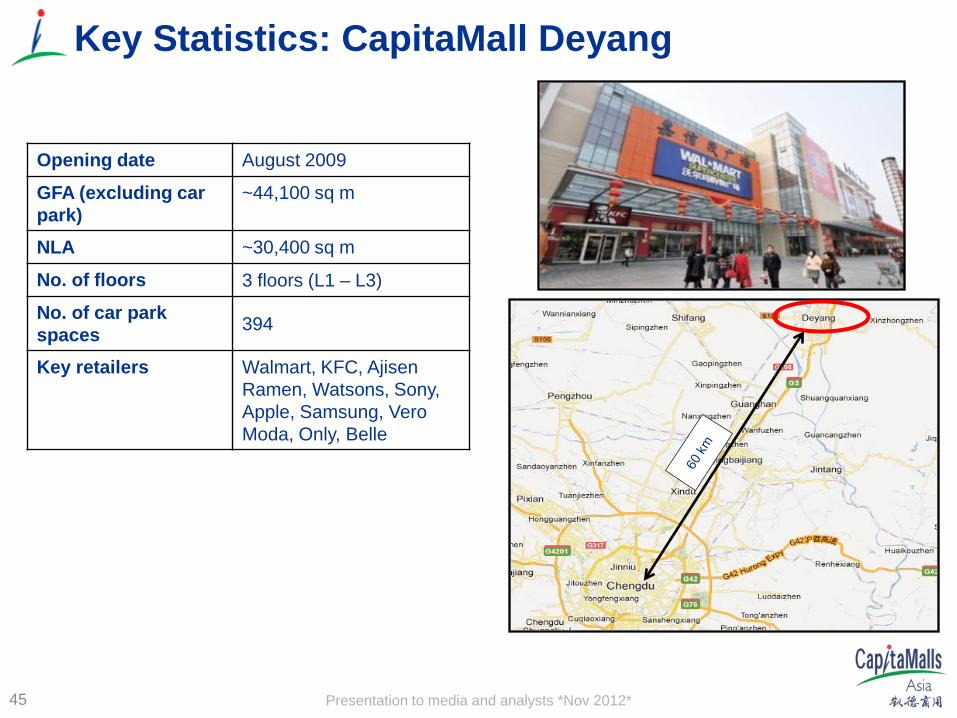

Key Statistics: CapitaMall Deyang

45

Opening date August 2009

GFA (excluding car park)

~44,100 sq m

NLA ~30,400 sq m

No. of floors 3 floors (L1 – L3)

No. of car park spaces 394

Key retailers Walmart, KFC, Ajisen Ramen, Watsons, Sony, Apple, Samsung, Vero Moda, Only, Belle

Presentation to media and analysts *Nov 2012*

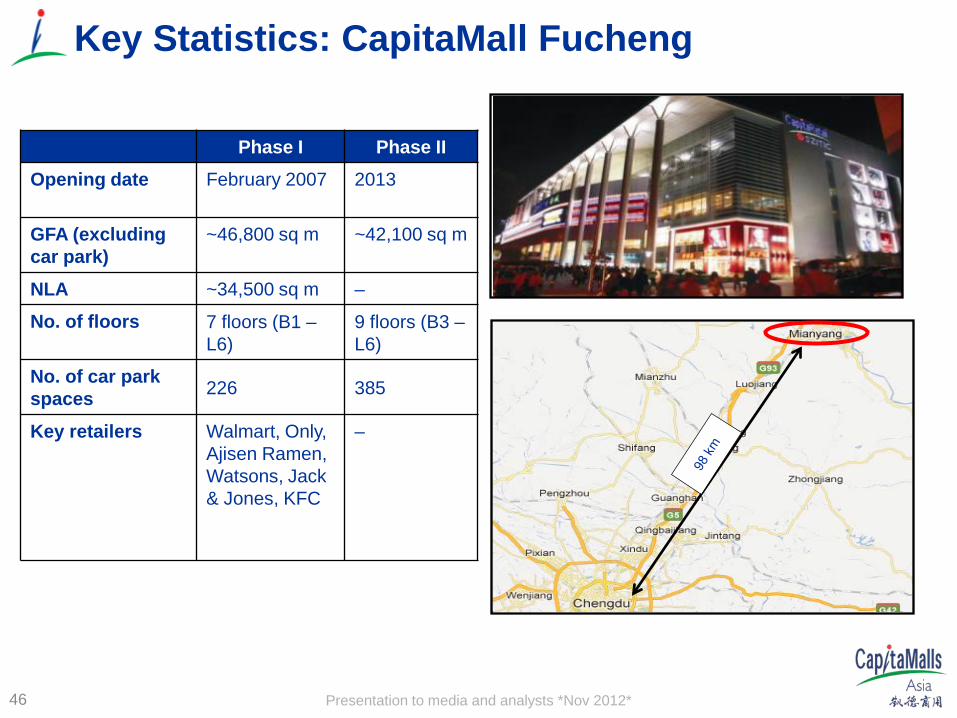

Key Statistics: CapitaMall Fucheng

46

Phase I Phase II Opening date February 2007 2013

GFA (excluding car park)

~46,800 sq m ~42,100 sq m

NLA ~34,500 sq m –

No. of floors 7 floors (B1 – L6)

9 floors (B3 – L6)

No. of car park spaces 226 385

Key retailers Walmart, Only, Ajisen Ramen, Watsons, Jack & Jones, KFC

–

Presentation to media and analysts *Nov 2012*

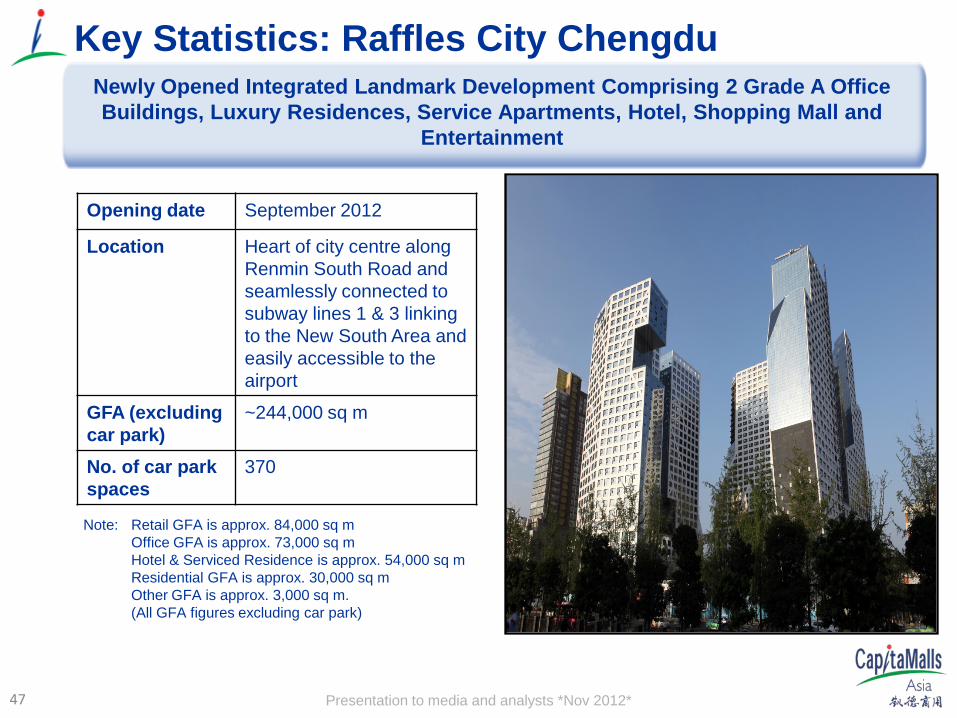

Key Statistics: Raffles City Chengdu

Opening date September 2012

Location Heart of city centre along Renmin South Road and seamlessly connected to subway lines 1 & 3 linking to the New South Area and easily accessible to the airport

GFA (excluding car park)

~244,000 sq m

No. of car park spaces

370

Newly Opened Integrated Landmark Development Comprising 2 Grade A Office Buildings, Luxury Residences, Service Apartments, Hotel, Shopping Mall and

Entertainment

Note: Retail GFA is approx. 84,000 sq m Office GFA is approx. 73,000 sq m Hotel & Serviced Residence is approx. 54,000 sq m Residential GFA is approx. 30,000 sq m Other GFA is approx. 3,000 sq m. (All GFA figures excluding car park)

47

Presentation to media and analysts *Nov 2012*

New Projects in West Region

48

Presentation to media and analysts *Nov 2012*

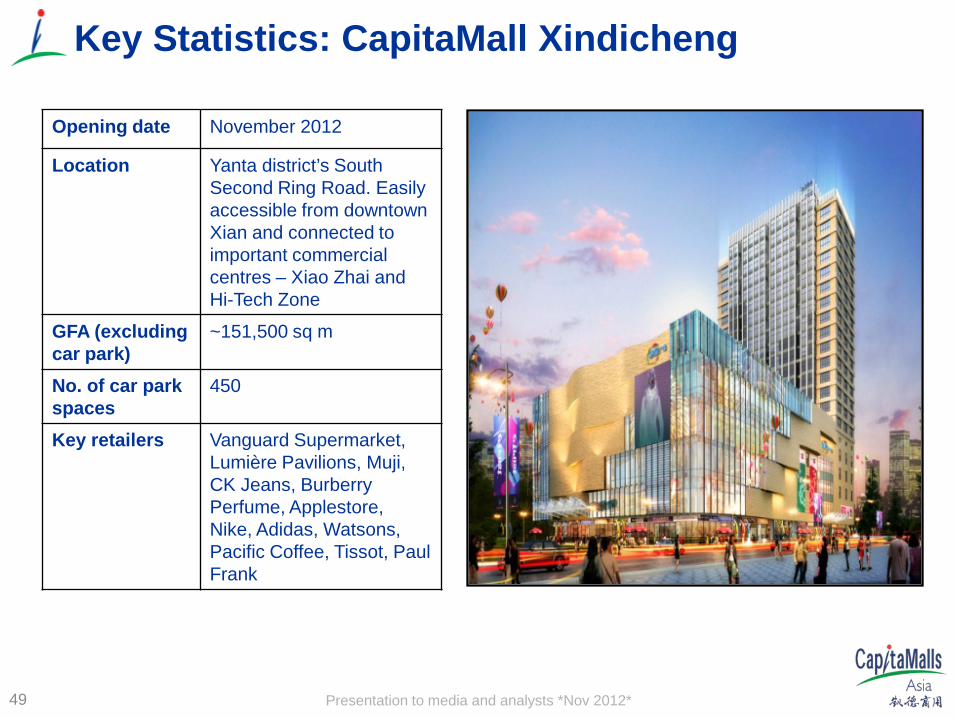

Key Statistics: CapitaMall Xindicheng

49

Opening date November 2012

Location Yanta district’s South Second Ring Road. Easily accessible from downtown Xian and connected to important commercial centres – Xiao Zhai and Hi-Tech Zone

GFA (excluding car park)

~151,500 sq m

No. of car park spaces

450

Key retailers Vanguard Supermarket, Lumière Pavilions, Muji, CK Jeans, Burberry Perfume, Applestore, Nike, Adidas, Watsons, Pacific Coffee, Tissot, Paul Frank

Presentation to media and analysts *Nov 2012* 50

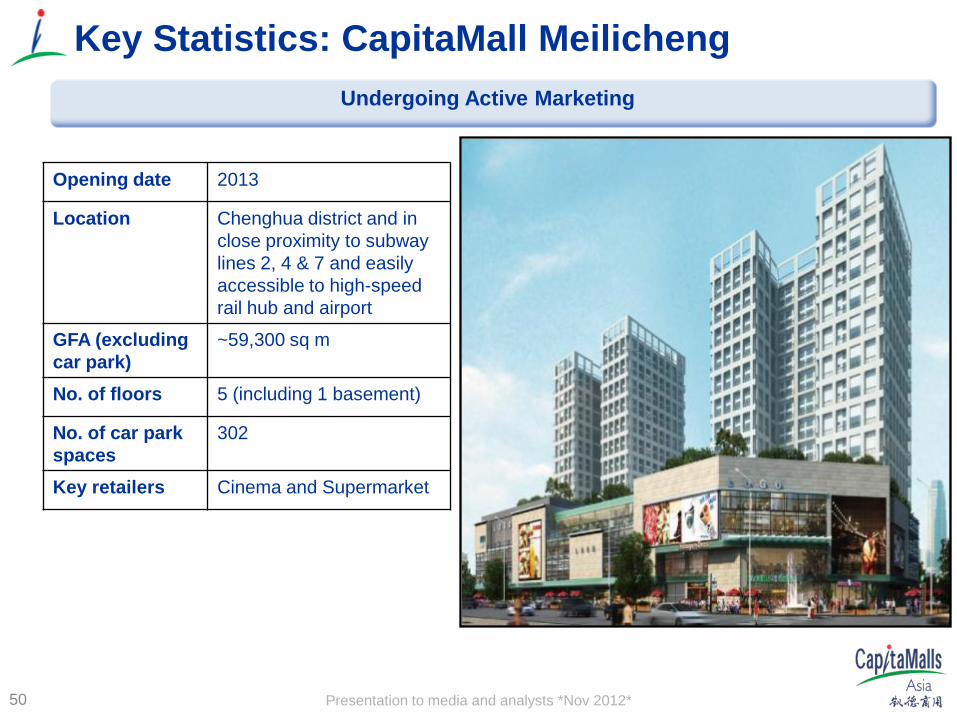

Key Statistics: CapitaMall Meilicheng

Opening date 2013

Location Chenghua district and in close proximity to subway lines 2, 4 & 7 and easily accessible to high-speed rail hub and airport

GFA (excluding car park)

~59,300 sq m

No. of floors 5 (including 1 basement)

No. of car park spaces

302

Key retailers Cinema and Supermarket

Undergoing Active Marketing

Presentation to media and analysts *Nov 2012* 51

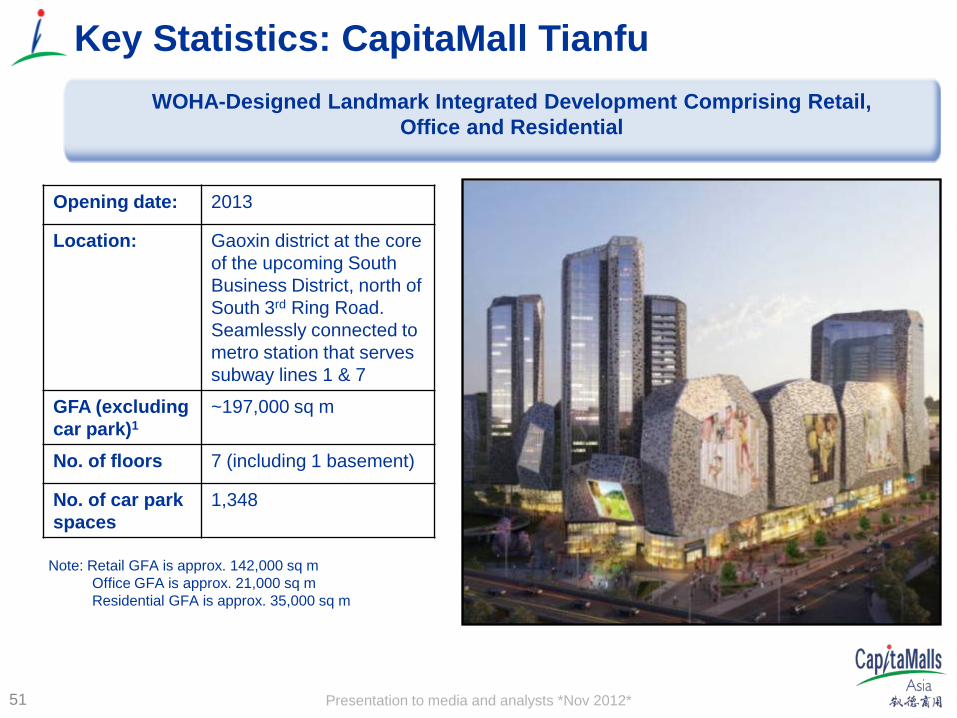

Key Statistics: CapitaMall Tianfu

Opening date: 2013

Location: Gaoxin district at the core of the upcoming South Business District, north of South 3rd Ring Road. Seamlessly connected to metro station that serves subway lines 1 & 7

GFA (excluding car park)1

~197,000 sq m

No. of floors 7 (including 1 basement)

No. of car park spaces

1,348

Note: Retail GFA is approx. 142,000 sq m Office GFA is approx. 21,000 sq m Residential GFA is approx. 35,000 sq m

WOHA-Designed Landmark Integrated Development Comprising Retail, Office and Residential

Presentation to media and analysts *Nov 2012* 52

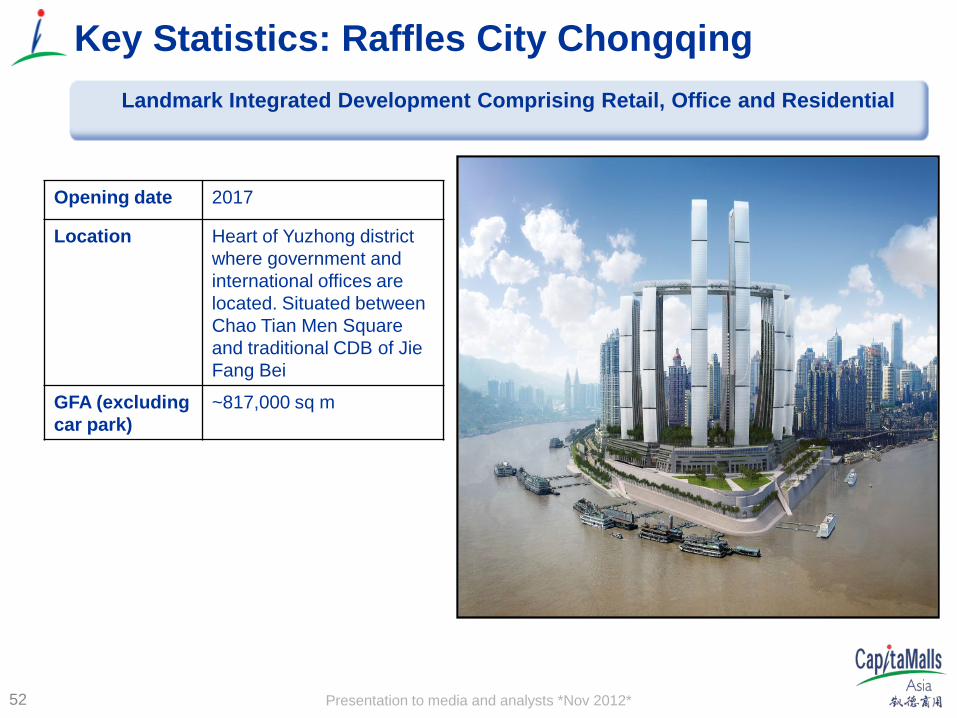

Key Statistics: Raffles City Chongqing

Opening date 2017

Location Heart of Yuzhong district where government and international offices are located. Situated between Chao Tian Men Square and traditional CDB of Jie Fang Bei

GFA (excluding car park)

~817,000 sq m

Landmark Integrated Development Comprising Retail, Office and Residential

Presentation to media and analysts *Nov 2012* Raffles City Beijing, Beijing, China North China Region

Presentation to media and analysts *Nov 2012*

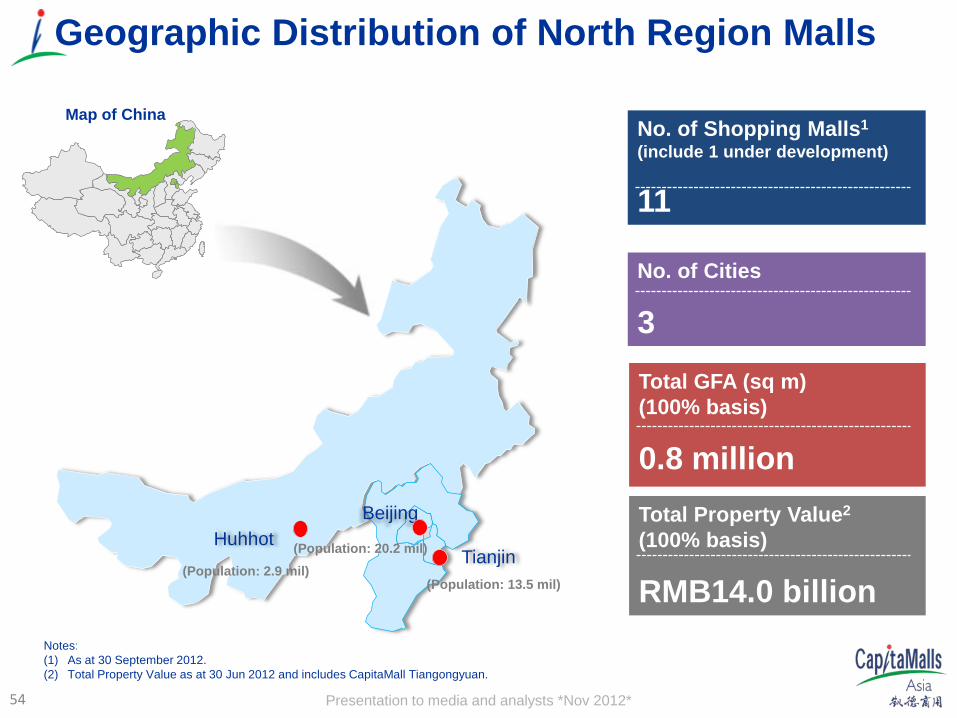

Geographic Distribution of North Region Malls

No. of Shopping Malls1 (include 1 under development)

11

No. of Cities

3 Total GFA (sq m) (100% basis)

0.8 million Total Property Value2 (100% basis)

RMB14.0 billion Notes: (1) As at 30 September 2012. (2) Total Property Value as at 30 Jun 2012 and includes CapitaMall Tiangongyuan.

Map of China

Tianjin

Beijing Huhhot

(Population: 2.9 mil) (Population: 20.2 mil)

(Population: 13.5 mil)

54

Presentation to media and analysts *Nov 2012*

Beijing

55

Presentation to media and analysts *Nov 2012* 56

Facts of Beijing

• The capital of China • The political and cultural centre • The largest retail market • Highly educated workforce and large

graduate population • Key Statistics:

Total population .20.2 million Disposable Income RMB 32,903 Per Capita Total retail sales RMB 690 billion for 2011:

Presentation to media and analysts *Nov 2012*

Beijing Economic Snapshot

• Economic Fundamentals – strong growth pace at heart of nation – 2011: GDP achieved 8.1% growth, expect strong growth momentum in 2012.

– Per capita GDP reached RMB80,394.

– Per capita urban disposable income reached RMB32,903, an increase of 13.2% over the

previous year.

– Retail sales of consumer goods crossed RMB690 billion, ranked 1st in China, ahead of Shanghai.

• Beijing Suburb Development Plan – Background: Beijing had 20m population at end of 2011, one of the most populated cities in

the world, driven by the fast-pace economic growth.

– Beijing New Town Development Plan (2007): Channel priority development emphasis to 5 suburban districts (Daxing, Tongzhou, Shunyi, Changping & Fangshan).

– Beijing South Area Development Plan (2009) Accelerate economic development towards southern Beijing, including:

(a) investing RMB290 billion in infrastructure, (b) building Daxing MRT line to connect to city centre, (c) endorsing Beijing’s 2nd international airport site in Daxing.

57

Presentation to media and analysts *Nov 2012* 58

Beijing MRT Route Map

Presentation to media and analysts *Nov 2012*

CMA Presence in Beijing

59

① CapitaMall Xizhimen

② CapitaMall Wangjing

③ Raffles City Beijing

④ CapitaMall Crystal

⑤ CapitaMall Cuiwei

⑥ CapitaMall Anzhen

⑦ CapitaMall Shuangjing

⑧ CapitaMall Taiyanggong

⑨ CapitaMall Tiangongyuan

2 8

7

6

1

5 4 3

Beijing Map

N Existing Beijing Portfolio

Beijing city-north relatively congested

Bei

jing

city

-wes

t rel

ativ

ely

hilly

reg

ion B

eijing CB

D extending eastbound

Beijing city-south being promoted for development emphasis

9

Under development site in Beijing

Presentation to media and analysts *Nov 2012*

Operating Malls in North Region

60

Presentation to media and analysts *Nov 2012*

8.7% 8.9% 9.3% 9.8% 11.4%

2007 2008 2009 2010 2011

Case Study: CapitaMall Wangjing, Beijing

7.4 7.6 7.9 8.7 9.5

2007 2008 2009 2010 2011

Shopper traffic (mil)

CAGR 7%

805 1,018 1,006 1,320 1,573

2007 2008 2009 2010 2011

Tenant sales psm (RMB/sqm/m)

CAGR 18%

NPI yield (On cost)

Valuation (RMB mil)

1,193 1,220 1,239 1,362 1,506

2007 2008 2009 2010 2011

Gross Yield 16.2%

11%

16%

61

Presentation to media and analysts *Nov 2012*

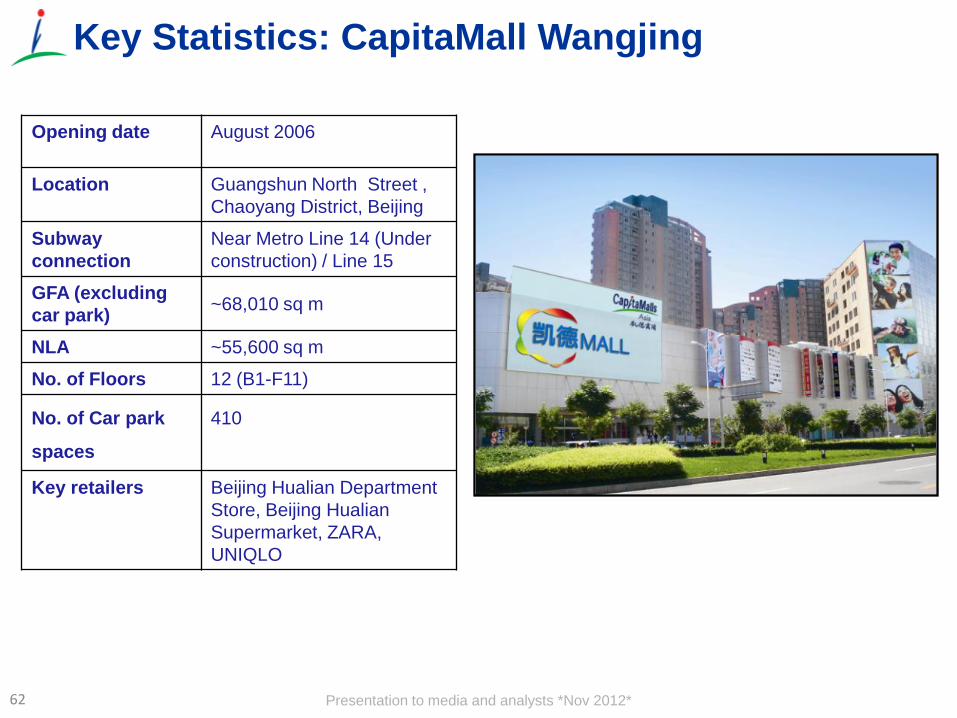

Opening date August 2006

Location Guangshun North Street , Chaoyang District, Beijing

Subway connection

Near Metro Line 14 (Under construction) / Line 15

GFA (excluding car park) ~68,010 sq m

NLA ~55,600 sq m

No. of Floors 12 (B1-F11)

No. of Car park

spaces

410

Key retailers Beijing Hualian Department Store, Beijing Hualian Supermarket, ZARA, UNIQLO

Key Statistics: CapitaMall Wangjing

62

Presentation to media and analysts *Nov 2012*

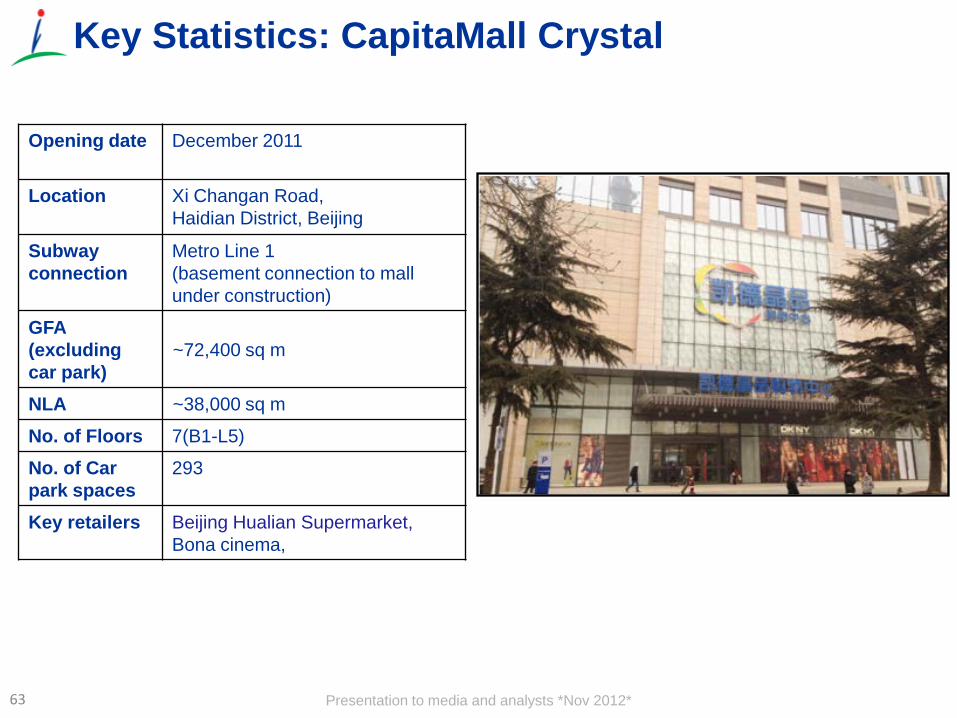

Opening date December 2011

Location Xi Changan Road, Haidian District, Beijing

Subway connection

Metro Line 1 (basement connection to mall under construction)

GFA (excluding car park)

~72,400 sq m

NLA ~38,000 sq m

No. of Floors 7(B1-L5)

No. of Car park spaces

293

Key retailers Beijing Hualian Supermarket, Bona cinema,

Key Statistics: CapitaMall Crystal

63

Presentation to media and analysts *Nov 2012*

Opening date July 2012

Location Taiyanggongzhong Road , Chaoyang District, Beijing

Subway connection

Metro Line 10

GFA (excluding car park) ~83,700 sq m

NLA ~42,500 sq m

No. of Floors 7 (B2-F5)

No. of Car park

spaces

783

Key retailers Beijing Hualian Supermarket, Hai Di Lao Hotpot,

Key Statistics: CapitaMall Taiyanggong

64

Presentation to media and analysts *Nov 2012*

Opening date April 2010

Location Cuiwei Road, Haidian District, Beijing

Subway connection Near Metro Line 1 Wanshoulu station (1KM) Gongzhufen station(1.2KM)

GFA (excluding car park) ~56,100 sq m

NLA ~35,000 sq m

No. of Floors 5 (B1-F4)

No. of Car park spaces

416

Key retailers Beijing Hualian Supermarket, Hai Di Lao Hotpot

Key Statistics: CapitaMall Cuiwei

65

Presentation to media and analysts *Nov 2012*

Key Statistics: CapitaMall Xizhimen

Opening date October 2007

Location Xizhimenwai Road , Xichen District, Beijing

Subway Connection

Metro Line 2/4/13

GFA (excluding car park) ~83,000 sq m

NLA ~51,000 sq m

No. of Floors 8 (B2-F6)

Key retailers Beijing Hualian Supermarket, Watsons, KFC

66

Presentation to media and analysts *Nov 2012*

Opening date April 2009

Location Dongzhimen South Street, Dongcheng District, Beijing

Subway Connection

Metro Line 2

GFA (excluding car park) ~111,000 sq m

NLA ~90,300 sq m

No of Floors 7 (B2-F5)

No. of Car park

spaces

455

Key retailers Beijing Hualian Supermarket, Guess, Han Na Shan BBQ

Key Statistics: Raffles City Beijing

67

Presentation to media and analysts *Nov 2012*

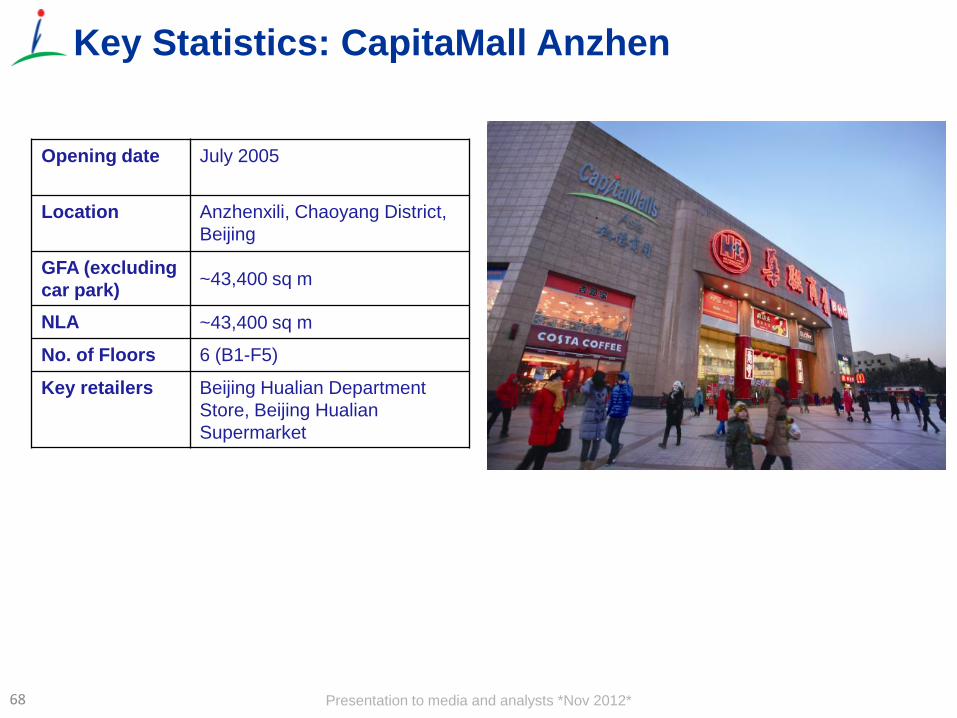

Opening date July 2005

Location Anzhenxili, Chaoyang District, Beijing

GFA (excluding car park) ~43,400 sq m

NLA ~43,400 sq m

No. of Floors 6 (B1-F5)

Key retailers Beijing Hualian Department Store, Beijing Hualian Supermarket

Key Statistics: CapitaMall Anzhen

68

Presentation to media and analysts *Nov 2012*

Opening date March 2004

Location Guangqu Road, Chaoyang District, Beijing

GFA (excluding car park) ~49,500 sq m

NLA ~49,500 sq m

No. of Floors 4 (B1-F3)

No. of Car park

spaces

334

Key retailers Carrefour, B&Q

Key Statistics: CapitaMall Shuangjing

69

Presentation to media and analysts *Nov 2012*

Opening date December 2008

Location Nan Bei Avenue, Hexi District,Tianjin

GFA (excluding car park) ~59,300 sq m

NLA ~40,700 sq m

No. of Floors 5 (B1-F4)

No. of Car park

spaces

436

Key retailers e-mart supermarket, Xing Mei Cinema

Key Statistics: CapitaMall TianjinOne

70

Presentation to media and analysts *Nov 2012*

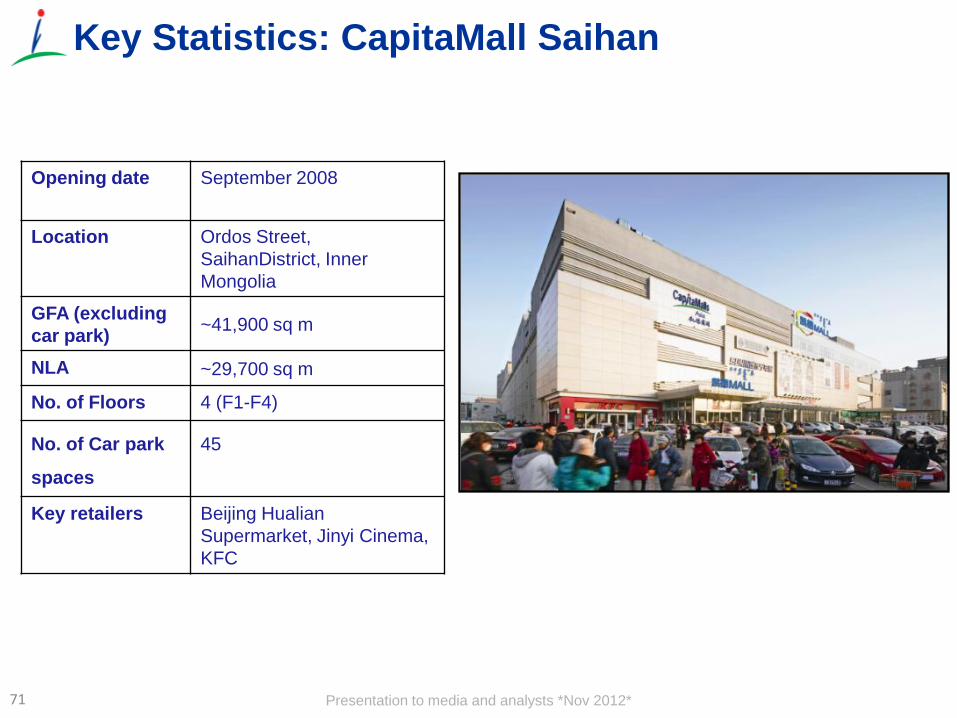

Opening date September 2008

Location Ordos Street, SaihanDistrict, Inner Mongolia

GFA (excluding car park) ~41,900 sq m

NLA ~29,700 sq m

No. of Floors 4 (F1-F4)

No. of Car park

spaces

45

Key retailers Beijing Hualian Supermarket, Jinyi Cinema, KFC

Key Statistics: CapitaMall Saihan

71

Presentation to media and analysts *Nov 2012*

New Projects in North Region

72

Presentation to media and analysts *Nov 2012*

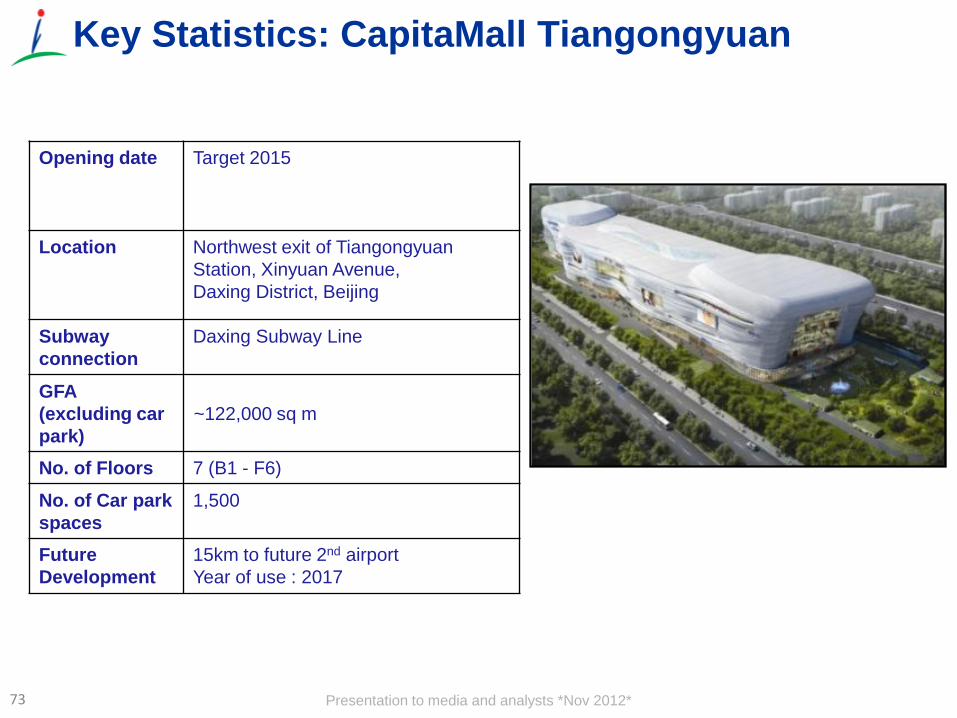

Opening date Target 2015

Location Northwest exit of Tiangongyuan Station, Xinyuan Avenue, Daxing District, Beijing

Subway connection

Daxing Subway Line

GFA (excluding car park)

~122,000 sq m

No. of Floors 7 (B1 - F6)

No. of Car park spaces

1,500

Future Development

15km to future 2nd airport Year of use : 2017

Key Statistics: CapitaMall Tiangongyuan

73

Presentation to media and analysts *Nov 2012*

Thank you