canada's financial sector: responses to the global …...1 canada’s financial sector:...

TRANSCRIPT

1

Canada’s Financial Sector: Responses to the Global Crisis

To the Colombian Banking Association Cartagena, Colombia

10 July 2009Paul Jenkins

Senior Deputy Governor

2

Contents

• Introduction

• Structure of Financial Regulation

• Key Lessons From Canada

• The Forward Agenda

Cover Photo Credit: D. Neuman http://www.flickr.com/photos/dneuman/

3

PresenterPresenter’s title

Introduction

4

Building on a strong, coherent policy framework

• Credible monetary policy framework•Conventional•Unconventional

• Sound fiscal management

• Systemwide financial stability focus•Liquidity facilities•Risk assessment (Financial System Review)

• Financial sector’s management of risk

• Credible and sound regulatory environment

5

Rate of return of Canadian banksAverage return on equity (ROE)

-20

-15

-10

-5

0

5

10

15

20

25

Canada United States ContinentalEurope

UnitedKingdom

2007 2008Source: Bloomberg and banks’ financial statements

%

6

Funding spreads

Conditions in short-term funding markets have improved*

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09

Basis points

0

50

100

150

200

250

300

350

400

Canada United States Euro zone United Kingdom

Source: Bloomberg

* The difference between 3-month interbank offered rates and their respective overnight index swaps: for the United States and the United Kingdom, LIBOR; for the Euro zone, EURIBOR; and for Canada, CDOR.

7

Relatively conservative risk appetite of Canadian banks

2007Q2 2007Q3 2007Q4 2008Q1 2008Q2 2008Q3 2008Q4 2009Q10%

10%

20%

30%

40%

50%

60%

Canada United States Continental Europe United Kingdom

Source: Bloomberg and banks' financial statements

Cumulative writedowns as a share of shareholders' equity

8

Need for liquidity extension lower in Canada

Total public sector liquidity extension

0%

5%

10%

15%

20%

25%

U.S. Euro Zone U.K. Canada Canada (includingIMPP)

0%

2%

4%

6%

8%

10%Ratio to GDP (lhs)

Ratio to Banking System (rhs)

Note: Liquidity extension refers to central banks' liquidity provision operations, as w ell as foreign currency sw aps w ith other central banks, but excludes outright securities purchases.IMPP: Insured Mortgage Purchase Program provides for governement purchases of insured mortgage pools.

Sources: Bank of Canada, U.S. Federal Reserve, Bank of England and European Central Bank

9

PresenterPresenter’s title

Structure of Financial Regulation

10

Four features

•Regulatory framework

•Market structure and product design

•Principled, reliance‐based supervision

•Risk‐based prudential regulation

See also: “Lessons for banking reform: A Canadian perspective,” by Carol Ann Northcott, Graydon Paulin, Mark White, Central Banking, Volume 19, Number 4.

11

Regulatory framework

• Independent, clearly mandated agencies

•Opportunities for regulatory arbitrage constrained

•Good inter‐agency communications

•Structured settings for discussion and information sharing

12

Regulatory frameworkFinancial Institutions Supervisory Committee (FISC)Members• Office of the Superintendent of Financial Institutions (OSFI): Chair• Bank of Canada• Canada Deposit Insurance Corporation (CDIC)• Department of Finance• Financial Consumer Agency of Canada (FCAC)Purpose• Share information regarding condition of financial institutions• Discuss and analyze developments as they relate to financial

institutions• Coordinate intervention in a troubled institution

13

Market structure and product design

• Banking system dominated by a handful of systemically important institutions• Extensive, nationwide retail distribution networks•Diversified through wholesale and international operations

• Three internationally active insurance companies

• Wide range of smaller (domestic and international) institutions

• Only about 30 per cent of mortgages in Canada are securitized

• Banks retain a degree of risk on their balance sheets

14

Principled, reliance‐based supervision

• Adaptable, less open to arbitrage, as banks use own judgement and must prove compliance

• OSFI has substantial discretion to issue guidance

• Comprehensive, risk‐based methodology – applied on a consolidated basis

• Guide to Intervention promotes awareness and transparency

Risk‐based prudential regulationCanadian capital requirements are higher than Basel II:

Major Canadian banks also maintain a sizable buffer above OSFI’s requirements of 7% Tier 1 and 10% total

15Total capital ratio Tier 1 capital ratio

Source: OSFI

16

Risk‐based prudential regulationOSFI also imposes an upper limit on bank leverage

17

OSFI requires high-quality capital: Tier 1 must be made up ofcommon shares and retained earnings

Risk‐based prudential regulation

Common shares Retained earnings

Preferred shares (eligible for Tier 1) Hybrid capital

Source: OSFI

18

PresenterPresenter’s title

Key Lessons from Canada

19

Canadian bank capital well managed

2000Q1 2001Q1 2002Q1 2003Q1 2004Q1 2005Q1 2006Q1 2007Q1 2008Q1 2009Q17.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

Canada United States Continental Europe United Kingdom

Source: Bloomberg and banks' financial statements

Tier 1 capital ratio

20

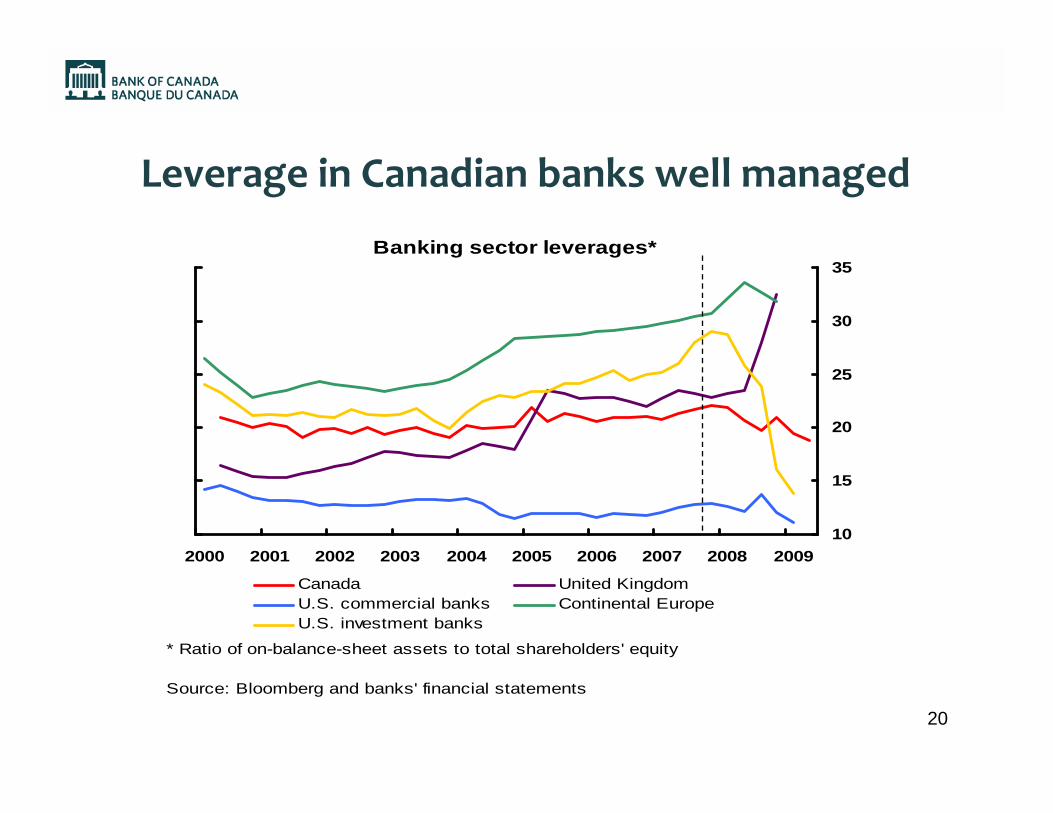

Leverage in Canadian banks well managed

Banking sector leverages*

2000 2001 2002 2003 2004 2005 2006 2007 2008 200910

15

20

25

30

35

Canada United KingdomU.S. commercial banks Continental EuropeU.S. investment banks

* Ratio of on-balance-sheet assets to total shareholders' equity

Source: Bloomberg and banks' financial statements

21

More conservative housing market (1)

Canada United States

Source: Statistics Canada, U.S. Federal Reserve

Mortgage debt as a per cent of nominal GDP

25

35

45

55

65

75

85

95

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Canada USSources: Statistcs Canada, U.S. Federal Reserve

Mortgage debt as a per cent of nominal GDP

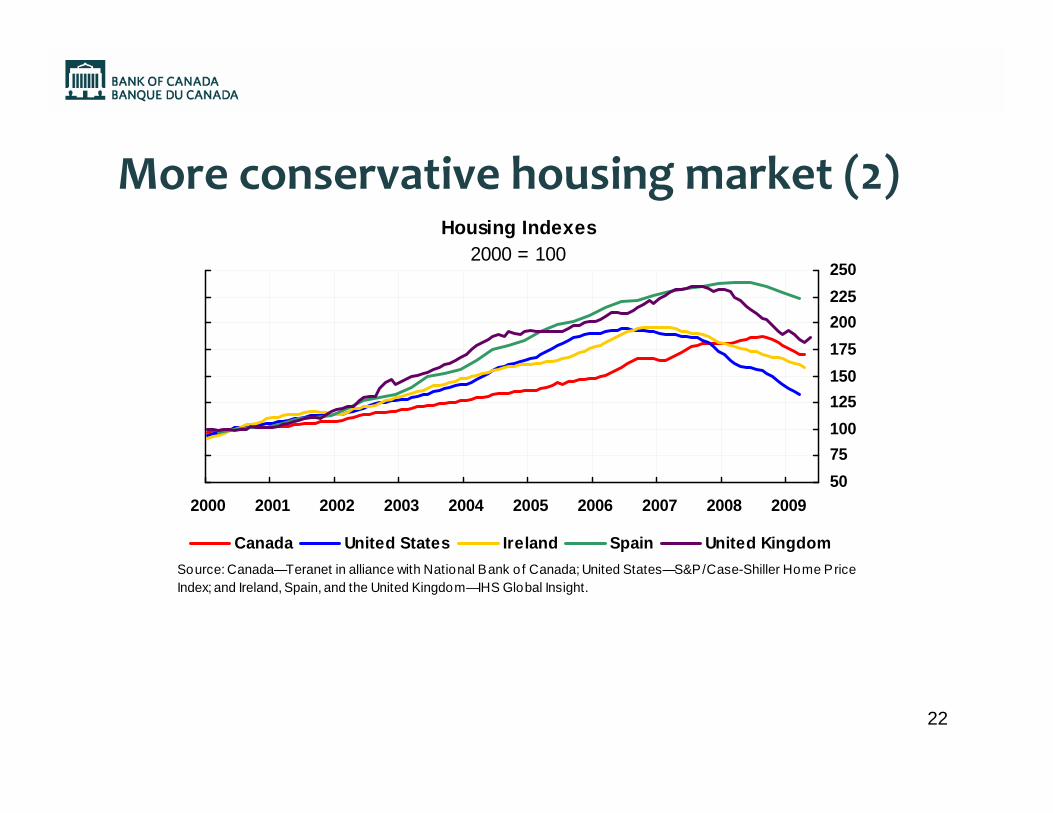

22

More conservative housing market (2)Housing Indexes

2000 = 100

2000 2001 2002 2003 2004 2005 2006 2007 2008 20095075100125150175200225250

Canada United States Ireland Spain United KingdomSource: Canada—Teranet in alliance with National Bank o f Canada; United States—S&P/Case-Shiller Home Price Index; and Ireland, Spain, and the United Kingdom—IHS Global Insight.

23

Mortgage market: Key reasons Canada didn’t have same stresses in housing market as in U.S. (1)

• Banks required to have insurance on mortgages if purchaser has loan‐to‐value ratio over 80%

• CMHC, a federal agency, has explicit sovereign guarantee and is largest insurance provider

• Lenders relying on private mortgage insurers receive government guarantee of losses (from insurer failure) above 10% of original mortgage

• Canadian market for non‐prime mortgages has been limited and ended for banks in 2008 when CMHC ceased insuring such mortgages

24

Mortgage market: Key reasons Canada didn’t have same stresses in housing market as in U.S. (2)

• Mortgagors personally liable for loan

• Mortgage interest not tax deductible

• Most mortgages originated by banks for own balance sheets and, as a result, higher underwriting standards are applied

• Securitization of mortgages primarily for liquidity rather than risk transfer

25

The Forward Agenda

26

Four key elements

•Continuously open markets

•Sustainable securitization

•Bank capital requirements

•Macroprudential approach to regulation

27

Continuously open markets

•Core funding markets should be made more efficient and less susceptible to extreme price movements

•Crisis clearly exacerbated by seizure of interbank and repo markets

•Robust and efficient financial system needs interbank, commercial paper, and repo markets that are continuously open, even under stress

•Ensure robust infrastructure

28

Sustainable securitization

• Transparency should be increased so that risk can be identified more effectively and priced more efficiently

• Models and data underlying securities could be published

• Skin in the game (keep similar products or first loss)

29

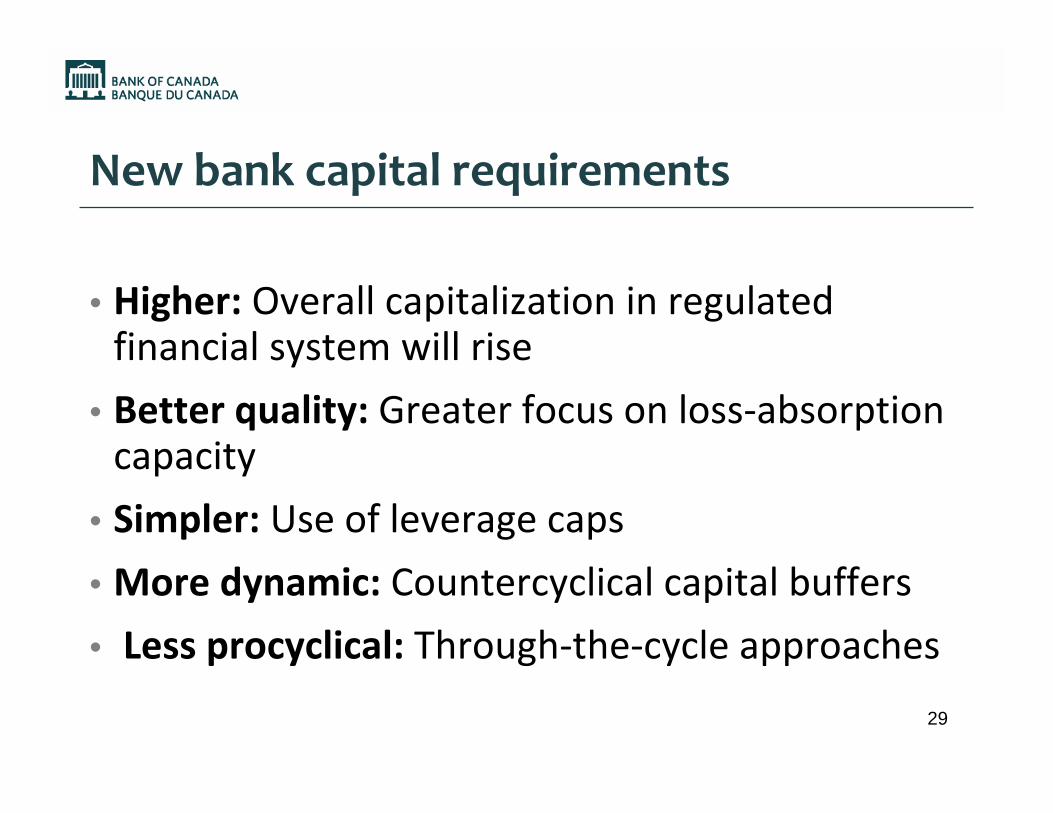

New bank capital requirements

•Higher: Overall capitalization in regulated financial system will rise

•Better quality: Greater focus on loss‐absorption capacity

•Simpler: Use of leverage caps

•More dynamic: Countercyclical capital buffers

• Less procyclical: Through‐the‐cycle approaches

30

Macroprudential approach to regulation

• Not enough for prudential regulators to adopt new measures within their current frameworks

• Need for oversight of the system as a whole—including both systemically important institutions and systemically important markets

• Macroprudential surveillance: Identify buildup of risks to financial system

• Macroprudential regulation: Strengthen resilience of financial system

31