2013-01 measuring performance in the public sector responses

TRANSCRIPT

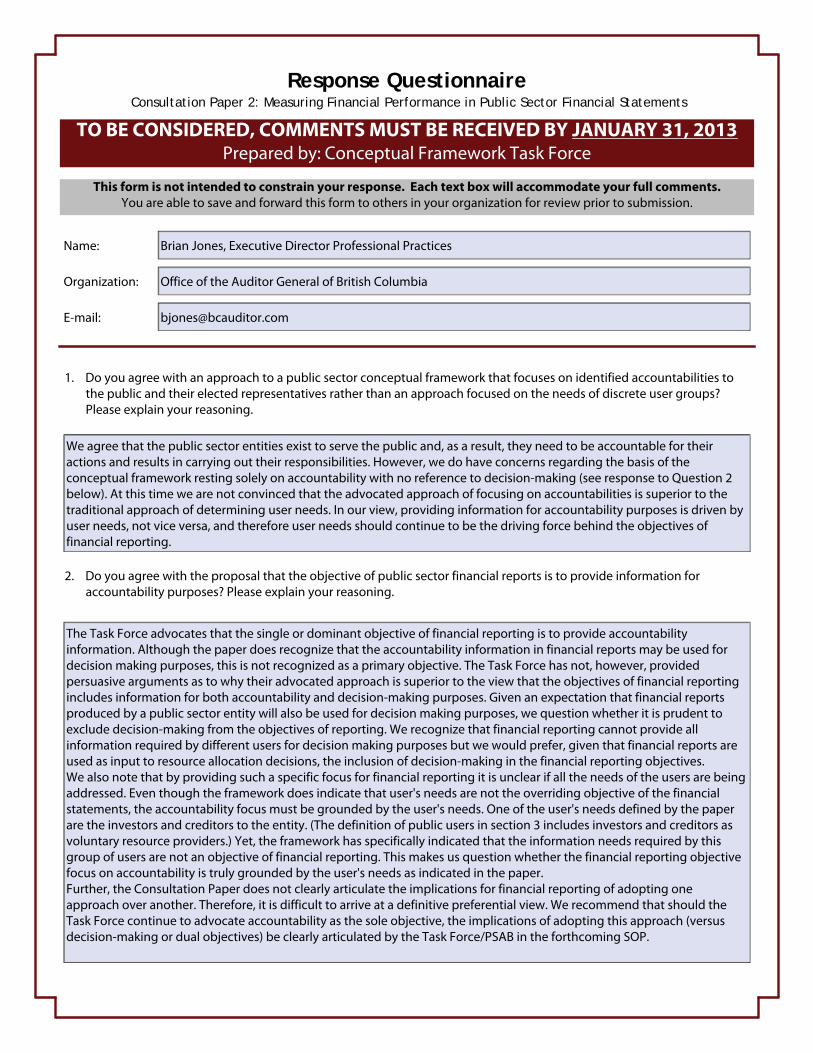

Response Questionnaire Consultation Paper 2: Measuring Financial Performance in Public Sector Financial Statements

TO BE CONSIDERED, COMMENTS MUST BE RECEIVED BY JANUARY 31, 2013 Prepared by: Conceptual Framework Task Force

This form is not intended to constrain your response. Each text box will accommodate your full comments. You are able to save and forward this form to others in your organization for review prior to submission.

Name: Trevor Seibel

Organization: District of Coldstream

E-mail: [email protected]

1. Do you agree with an approach to a public sector conceptual framework that focuses on identified accountabilities to the public and their elected representatives rather than an approach focused on the needs of discrete user groups? Please explain your reasoning.

No I do not. For local governments, Accountabilities to the public and their elected representatives is a very subjective topic. Too much is being asked of the financial statements to consider "accountability" topics, which are most likely politically motivated.

2. Do you agree with the proposal that the objective of public sector financial reports is to provide information for accountability purposes? Please explain your reasoning.

No, I do not. The purpose of the financial statements is to provide a clear, objective reporting of the financial results of the municipality. In BC, Municipalities already produce an Annual Report which considers the goals and objectives of the municipality. This is more than sufficient to address the accountability factors for the community. They should NOT be included in the financial statements.

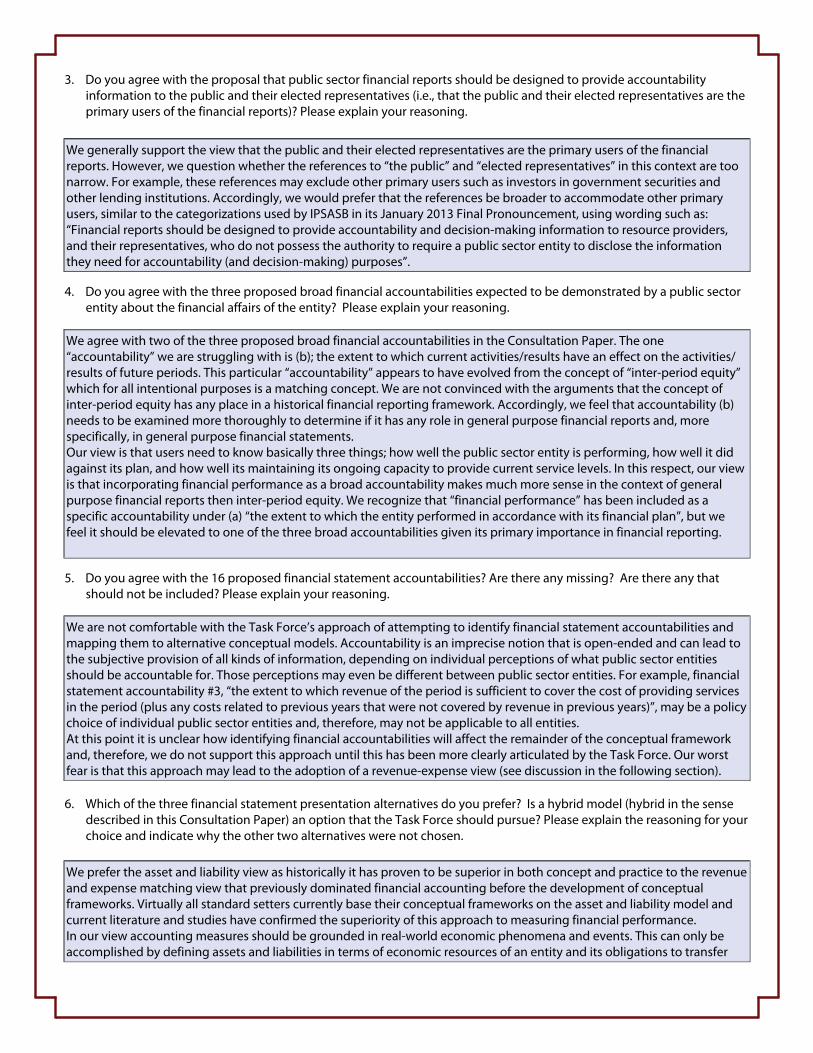

3. Do you agree with the proposal that public sector financial reports should be designed to provide accountability information to the public and their elected representatives (i.e., that the public and their elected representatives are the primary users of the financial reports)? Please explain your reasoning.

No I do not. In BC the primary users of local government financial statements are the Municipal Finance Authority and the Provincial Government. The elected representatives and the public are a secondary user of the financial statements.

4. Do you agree with the three proposed broad financial accountabilities expected to be demonstrated by a public sector entity about the financial affairs of the entity? Please explain your reasoning.

No I do not. The first principle deals with comparison of results in accordance with the financial plan. We already do this in that the budget to actual information is provided within the financial statements. As well, the Annual Report goes into more analysis of the projects and the financial plan implications. The impact of current results on future periods is subjective. Financial statements report historical information and NOT what might happen in the future. The financial condition of the entity should NOT be addressed in the financial statements. This is better served in the Annual Report.

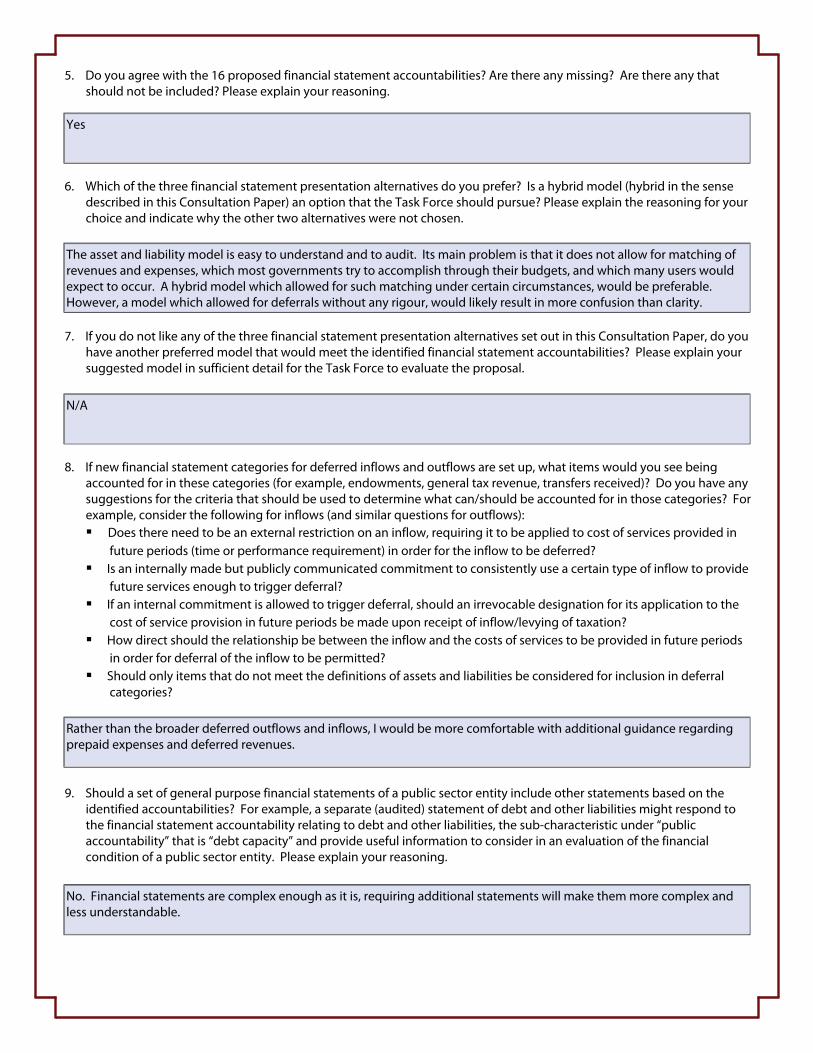

5. Do you agree with the 16 proposed financial statement accountabilities? Are there any missing? Are there any that should not be included? Please explain your reasoning.

I DISAGREE with #1,3,5,6. All the other points are reasonable.

6. Which of the three financial statement presentation alternatives do you prefer? Is a hybrid model (hybrid in the sense described in this Consultation Paper) an option that the Task Force should pursue? Please explain the reasoning for your choice and indicate why the other two alternatives were not chosen.

The Current model (Asset/Liability) is the MOST appropriate for local governments. The other 2 alternatives do not serve any direct purpose for local governments.

7. If you do not like any of the three financial statement presentation alternatives set out in this Consultation Paper, do you have another preferred model that would meet the identified financial statement accountabilities? Please explain your suggested model in sufficient detail for the Task Force to evaluate the proposal.

The Asset/Liability model works just fine.

8. If new financial statement categories for deferred inflows and outflows are set up, what items would you see being accounted for in these categories (for example, endowments, general tax revenue, transfers received)? Do you have any suggestions for the criteria that should be used to determine what can/should be accounted for in those categories? For example, consider the following for inflows (and similar questions for outflows): Does there need to be an external restriction on an inflow, requiring it to be applied to cost of services provided in

future periods (time or performance requirement) in order for the inflow to be deferred? Is an internally made but publicly communicated commitment to consistently use a certain type of inflow to provide

future services enough to trigger deferral? If an internal commitment is allowed to trigger deferral, should an irrevocable designation for its application to the

cost of service provision in future periods be made upon receipt of inflow/levying of taxation? How direct should the relationship be between the inflow and the costs of services to be provided in future periods

in order for deferral of the inflow to be permitted? Should only items that do not meet the definitions of assets and liabilities be considered for inclusion in deferral

categories?

No comment as these will not be an issue when the current model is retained.

9. Should a set of general purpose financial statements of a public sector entity include other statements based on the identified accountabilities? For example, a separate (audited) statement of debt and other liabilities might respond to the financial statement accountability relating to debt and other liabilities, the sub-characteristic under “public accountability” that is “debt capacity” and provide useful information to consider in an evaluation of the financial condition of a public sector entity. Please explain your reasoning.

No they shouldn't. General purposes financial statements are just that...general purpose!! They should not attempt to address accountability issues for the elected representatives.

GENERAL COMMENTS

These changes appear to be brought about due to issues at the senior levels of government with their legislation. The proposed changes will create undue hardship and pressures (downloading) on local governments with no significant benefit to the users of local government financial statements.

Click here to submit

Response Questionnaire Consultation Paper 2: Measuring Financial Performance in Public Sector Financial Statements

TO BE CONSIDERED, COMMENTS MUST BE RECEIVED BY JANUARY 31, 2013 Prepared by: Conceptual Framework Task Force

This form is not intended to constrain your response. Each text box will accommodate your full comments. You are able to save and forward this form to others in your organization for review prior to submission.

Name: Terry Martens, CGA

Organization: City of Armstrong, BC

E-mail: [email protected]

1. Do you agree with an approach to a public sector conceptual framework that focuses on identified accountabilities to the public and their elected representatives rather than an approach focused on the needs of discrete user groups? Please explain your reasoning.

Yes. By having each public sector group address the same set of accountabilities, better consistency is achieved.

2. Do you agree with the proposal that the objective of public sector financial reports is to provide information for accountability purposes? Please explain your reasoning.

Yes. This really is the only reason that such reports are created and distributed for a public sector organization.

3. Do you agree with the proposal that public sector financial reports should be designed to provide accountability information to the public and their elected representatives (i.e., that the public and their elected representatives are the primary users of the financial reports)? Please explain your reasoning.

Yes, so long as performance measures and other accountability results are sufficiently objective in their calculation/determination. It is recognized that some professional judgement and estimating is normal for financial statement items; however, relying too much on subjective data to create more of a "warm apple pie" type of report is dangerously turning financial statements into something they're not intended to be.

4. Do you agree with the three proposed broad financial accountabilities expected to be demonstrated by a public sector entity about the financial affairs of the entity? Please explain your reasoning.

I agree with the first and third broad accountability. The second accountability would be nice to report to the public but is subject to too much uncertainty in calculating the actual results.

5. Do you agree with the 16 proposed financial statement accountabilities? Are there any missing? Are there any that should not be included? Please explain your reasoning.

Yes. There is merit to all 16 accountabilities being dealt with in the financial statements. A suggested additional accountability would be the position of reserve funds and the change in reserve balances during the reporting period. This

would provide somewhat of a context to dealing with Accountability number 5 (consumption of TCA). However, this is not the best medium to deal with accountability - see Answer #9 and the general comments below.

6. Which of the three financial statement presentation alternatives do you prefer? Is a hybrid model (hybrid in the sense described in this Consultation Paper) an option that the Task Force should pursue? Please explain the reasoning for your choice and indicate why the other two alternatives were not chosen.

The Asset & Liability Perspective alternative is preferred. I am not in favour of the other two models due to the uncertainties of accurately reporting the correct resource inflows and outflows. The current format is already nearly impossible for the average citizen to understand. Period inflow & outflow adjustments only add to the complexity of the statements and make the current situation worse.

7. If you do not like any of the three financial statement presentation alternatives set out in this Consultation Paper, do you have another preferred model that would meet the identified financial statement accountabilities? Please explain your suggested model in sufficient detail for the Task Force to evaluate the proposal.

8. If new financial statement categories for deferred inflows and outflows are set up, what items would you see being accounted for in these categories (for example, endowments, general tax revenue, transfers received)? Do you have any suggestions for the criteria that should be used to determine what can/should be accounted for in those categories? For example, consider the following for inflows (and similar questions for outflows): Does there need to be an external restriction on an inflow, requiring it to be applied to cost of services provided in

future periods (time or performance requirement) in order for the inflow to be deferred? Is an internally made but publicly communicated commitment to consistently use a certain type of inflow to provide

future services enough to trigger deferral? If an internal commitment is allowed to trigger deferral, should an irrevocable designation for its application to the

cost of service provision in future periods be made upon receipt of inflow/levying of taxation? How direct should the relationship be between the inflow and the costs of services to be provided in future periods

in order for deferral of the inflow to be permitted? Should only items that do not meet the definitions of assets and liabilities be considered for inclusion in deferral

categories?

Although I am not in agreement with deferred inflows and outflows, if it were enacted, only externally restrictions should trigger deferral. Internal policies, bylaws, and proclamations can easily be changed or reversed by various means (i.e. a change in government or change in majority of Council). Thus, an internally triggered deferral would need to be corrected if the internal restriction that triggered the deferral were to change. The complexity of reconciling such changes would add to the complexity of the deferral process.

9. Should a set of general purpose financial statements of a public sector entity include other statements based on the identified accountabilities? For example, a separate (audited) statement of debt and other liabilities might respond to the financial statement accountability relating to debt and other liabilities, the sub-characteristic under “public accountability” that is “debt capacity” and provide useful information to consider in an evaluation of the financial condition of a public sector entity. Please explain your reasoning.

No. If accountability is an issue, legislation should be changed forcing governments to issue separate public performance reports - apart from the financial statements. For example, if the Province created a legislated requirement for all local governments in its jurisdiction to regularly publish accountability documents, I believe that more of the general public would be interested in actually reading them since they would likely be more informal than audited financial statements. The result would be greater accountability. Changing accounting standards is not going to achieve this goal since the statements will be too complicated to understand.

GENERAL COMMENTS

I am a little surprised that PSAB is even considering this change. In my opinion, PSAB is somewhat overstepping its scope. Leave the accountability issue with legislation.

Click here to submit

Formulaire de réponse Document de consultation 2 : La mesure de la performance financière dans les états financiers du secteur public

Ce formulaire ne vise pas à restreindre votre réponse. Chaque boîte de texte acceptera l'intégralité de vos commentaires. Vous pouvez sauvegarder le formulaire et l'envoyer, pour examen, à d'autres personnes de votre organisation avant de le soumettre.

Nom : JEAN MONFET

Organisation : Ministère des Affaires municipales, des Régions et de l'Occupation du territoire

Courriel : [email protected]

POUR ÊTRE PRIS EN CONSIDÉRATION, LES COMMENTAIRES DEVRONT ÊTRE REÇUS D'ICI LE 31 JANVIER 2013 Préparé par le Groupe de travail sur le cadre conceptuel

1. Êtes-vous d'accord pour que le cadre conceptuel pour le secteur public soit axé sur des responsabilités redditionnelles identifiées envers le public et ses représentants élus, plutôt que sur les besoins de divers groupes distincts d'utilisateurs? Veuillez expliquer votre raisonnement.

Nous sommes en accord avec cette orientation considérant que le public est un fournisseur de ressources des gouvernements ainsi qu'un bénéficiaire de leurs services. Il est ainsi légitime de positionner le public comme utilisateur de premier plan et d'accorder le cadre conceptuel en fonction des responsabilités redditionnelles envers cet utilisateur.

2. Êtes-vous d'accord avec la proposition voulant que l'objectif des rapports financiers du secteur public soit de fournir des informations à des fins de responsabilité redditionnelle? Veuillez expliquer votre raisonnement.

Nous sommes en accord avec cet objectif, le mandat des entités du secteur public étant de servir le public, il importe que les entités démontrent subséquemment de quelle façon ce mandat a été accompli.

3. Êtes-vous d'accord avec la proposition que les rapports financiers du secteur public devraient être conçus pour rendre des comptes au public et à ses représentants élus (autrement dit, que le public et ses représentants élus sont les principaux utilisateurs des rapports financiers)? Veuillez expliquer votre raisonnement.

Nous sommes en accord avec cette proposition. Voir réponse à la question 1 question ci-haut.

4. Êtes-vous d'accord avec les trois grands objectifs redditionnels proposés pour la reddition de comptes financière des entités du secteur public? Veuillez expliquer votre raisonnement.

Nous sommes en accord avec les trois grands objectifs redditionnels proposés, à l'effet que les entités du secteur public doivent rendre compte de la mesure dans laquelle elles se sont conformées à leur plan financier, de la mesure dans laquelle les activités ou les résultats actuels ont un effet sur les activités ou les résultats des périodes futures et de la condition financière de l'entité.

5. Êtes-vous d'accord avec les 16 éléments de reddition de comptes proposés pour les états financiers? Y en aurait-il d'autres à ajouter? Y en aurait-il à retrancher? Veuillez expliquer votre raisonnement.

Nous sommes en accord avec ces 16 éléments de reddition de comptes et ne voyons aucun autre élément à retrancher ou

à ajouter.

6. Lequel des trois modèles de présentation des états financiers préférez-vous? Le Groupe de travail devrait-il continuer à explorer l'option d'un modèle hybride (au sens donné à ce terme dans le Document de consultation)? Veuillez expliquer les raisons de votre choix et indiquer pourquoi vous n'avez pas retenu les deux autres modèles.

Nous préférons le statu quo. Dans un premier temps, le statu quo rencontre plus d'éléments de reddition de comptes que le modèle basé sur l'approche résultat. Également, considérant que nous sommes d'accord avec le fait que les rapports financiers du secteur public devraient être conçus pour rendre des comptes au public et à ses représentants élus, nous considérons que le statu quo procure pour ces deux utilisateurs un plus haut niveau de compréhension de l'information que le modèle hybride proposé. Les utilisateurs des rapports financiers des municipalités ayant déjà dû apprivoiser de nombreux changements aux états financiers au cours des dernières années, il serait inadéquat de changer pour un modèle dont l'articulation des états financiers entre eux ne serait pas complète, rendant davantage complexe la compréhension de l'information financière.

7. Si vous n'aimez aucun des trois modèles présentés dans le Document de consultation, y a-t-il un autre modèle de présentation des états financiers que vous préféreriez qui permettrait de s'acquitter des obligations redditionnelles identifiées? Veuillez expliquer le modèle que vous suggérez suffisamment en détail pour que le Groupe de travail puisse évaluer votre proposition.

S/O

8. Si l'on introduisait dans les états financiers les catégories de «revenus reportés» et de «charges reportées», quels éléments envisageriez-vous d'inclure dans ces catégories (par exemple, les dotations, les rentrées fiscales générales, les transferts reçus)? Avez-vous des suggestions quant aux critères à utiliser pour déterminer ce qui peut ou ce qui devrait être inclus dans ces catégories? Pensez par exemple aux critères suivants pour les revenus (et à des critères similaires pour les charges) : Pour qu'un revenu soit reporté, faudrait-il qu'il fasse l'objet d'une affectation externe imposant qu'il soit utilisé

pour défrayer des services à fournir dans des périodes futures (critère de la période d'utilisation)? Un engagement interne, mais rendu public, d'affecter de façon constante un certain type de revenu à des

services futurs serait-il suffisant pour déclencher le report?Si un engagement interne était suffisant pour déclencher le report, faudrait-il qu'une décision irrévocable

d'affecter les fonds au coût des services à fournir dans des périodes futures soit prise au moment de la réception des revenus/de la levée des impôts?

Jusqu'à quel point faudrait-il une relation directe entre un revenu et le coût des services à fournir dans des périodes futures pour que le report du revenu soit autorisé?

Faudrait-il que seuls les éléments qui ne répondent pas à la définition d'actif ou de passif puissent être candidats au report?

Considérant l'approche statu quo retenue, les revenus et les charges reportés inscrits à l'état de la situation financière devraient être ceux qui répondent à la définition d'actif ou de passif, ceci permettant de conserver la cohérence de l'ensemble du modèle.

9. Les états financiers à usage général d'une entité du secteur public devraient-ils comprendre d'autres états visant à répondre aux objectifs redditionnels identifiés? Par exemple, un état (vérifié) distinct de la dette et des autres passifs pourrait répondre à l'obligation d'informer le public sur la capacité d'endettement d'une entité du secteur public, et fournir des informations utiles pour évaluer la condition financière de cette dernière. Veuillez expliquer votre raisonnement.

Nous ne croyons pas que l'ajout d'autres états soit requis. Les notes et les tableaux complémentaires faisant partie intégrante des états financiers fournissent déjà l'information supplémentaire nécessaire aux lecteurs. Il faut éviter de noyer les lecteurs dans un excès d'information.

COMMENTAIRES GÉNÉRAUX

Je suis en accord avec les réponses proposées.

Cliquez ici pour soumettre

Response Questionnaire Consultation Paper 2: Measuring Financial Performance in Public Sector Financial Statements

TO BE CONSIDERED, COMMENTS MUST BE RECEIVED BY JANUARY 31, 2013 Prepared by: Conceptual Framework Task Force

This form is not intended to constrain your response. Each text box will accommodate your full comments. You are able to save and forward this form to others in your organization for review prior to submission.

Name: Stuart Barr, Assistant Auditor General

Organization: Office of the Auditor General of Canada

E-mail: [email protected]

1. Do you agree with an approach to a public sector conceptual framework that focuses on identified accountabilities to the public and their elected representatives rather than an approach focused on the needs of discrete user groups? Please explain your reasoning.

Yes, we agree with an approach focused on identified accountabilities to the public and their elected representatives. In our view, public accountability is the overriding characteristic of public sector entities and providing information to demonstrate such accountability is the primary objective of public sector reporting. Agreeing with this approach does not necessarily entail a disagreement with an approach focused on the needs of discrete user groups because both approaches would in our view likely result in similar conclusions. As articulated in this CP, “an accountability objective still requires consideration of to whom a public sector entity is accountable and for what...thus, the accountabilities remain grounded in, rather than divorced from, user needs but they are not driven solely by user needs”.

2. Do you agree with the proposal that the objective of public sector financial reports is to provide information for accountability purposes? Please explain your reasoning.

Yes, see response to Question 1 above.

3. Do you agree with the proposal that public sector financial reports should be designed to provide accountability information to the public and their elected representatives (i.e., that the public and their elected representatives are the primary users of the financial reports)? Please explain your reasoning.

Yes, we agree with this view. The public and their elected representatives are the primary users of the financial reports. While other parties may use public sector financial reports for various reasons, we believe that general purpose financial reports are intended to meet the common information needs of a potentially wide range of users. Therefore, special interest groups and their representatives would not meet this premise given each special interest group would have its own specialized information needs. Consequently, while general purpose financial reports may provide information useful to other parties, they are not prepared with their specific needs in mind.

4. Do you agree with the three proposed broad financial accountabilities expected to be demonstrated by a public sector entity about the financial affairs of the entity? Please explain your reasoning.

Yes, we agree with the three proposed broad financial accountabilities expected to be demonstrated by a public sector

entity. a) the extent to which the entity performed in accordance with its financial plan Actual-to-budget reporting is important to demonstrate whether government organizations raised revenues and funds within their mandate and did not overspend authorities or enter into unauthorized transactions (debt, capital, etc). b) the extent to which current activities/results have an effect on the activities/results of future periods Affordability of additional spending measured through net debt (liabilities less financial assets) helps users understand the levels of future taxation or other revenue required to fund past transactions and events (such as spending). c) the state of the financial condition of the entity Since government capital spending may not focus on maximizing financial return, capital spending and its effect on net debt must be highlighted in the financial statements. Therefore, another indicator of a government’s financial position is its accumulated surplus / deficit (net debt plus non-financial assets). The tangible capital assets and other non-financial assets of a government form part of its financial position and are important because they are the resources available to and deployed by the government to accomplish its objectives (i.e. they represent “prepaid service potential”). Therefore both the net debt of the government and the accumulated surplus / deficit measures should be reported on the statement of financial position as they represent different perspectives of the government's financial position.

5. Do you agree with the 16 proposed financial statement accountabilities? Are there any missing? Are there any that should not be included? Please explain your reasoning.

Yes, we agree with the 16 proposed financial statement accountabilities.

6. Which of the three financial statement presentation alternatives do you prefer? Is a hybrid model (hybrid in the sense described in this Consultation Paper) an option that the Task Force should pursue? Please explain the reasoning for your choice and indicate why the other two alternatives were not chosen.

Given that none of the three financial statement presentation alternatives meets all the identified financial statement accountabilities and that each of the alternatives has its respective benefits and drawbacks, it is difficult to conclude that one alternative is clearly superior to another. On balance, the Office prefers the Asset and Liability model because it is logical, defensible, and it addresses qualitative characteristics of financial information that are important to users. While we support the Asset and Liability model, we are concerned by the wide variation in preparer interpretation and application of the PSAB definitions of liabilities, especially in the context of the new section on government transfers. PSAB should consider ways to address these concerns by reviewing and refining as appropriate the current liability definition, and developing application guidance for areas requiring significant judgement to assess whether liability criteria have been met. We do not support the hybrid model because we have significant concerns with the potential lack of articulation between the statements. Internal consistency between financial statements is important to make them understandable and meaningful to readers. We are also concerned by the high risk that the financial statements will become complex as additional information and reconciliations will be required to articulate relationships between the statements.

7. If you do not like any of the three financial statement presentation alternatives set out in this Consultation Paper, do you have another preferred model that would meet the identified financial statement accountabilities? Please explain your suggested model in sufficient detail for the Task Force to evaluate the proposal.

N/A

8. If new financial statement categories for deferred inflows and outflows are set up, what items would you see being accounted for in these categories (for example, endowments, general tax revenue, transfers received)? Do you have any suggestions for the criteria that should be used to determine what can/should be accounted for in those categories? For example, consider the following for inflows (and similar questions for outflows): Does there need to be an external restriction on an inflow, requiring it to be applied to cost of services provided in

future periods (time or performance requirement) in order for the inflow to be deferred? Is an internally made but publicly communicated commitment to consistently use a certain type of inflow to provide

future services enough to trigger deferral? If an internal commitment is allowed to trigger deferral, should an irrevocable designation for its application to the

cost of service provision in future periods be made upon receipt of inflow/levying of taxation? How direct should the relationship be between the inflow and the costs of services to be provided in future periods

in order for deferral of the inflow to be permitted? Should only items that do not meet the definitions of assets and liabilities be considered for inclusion in deferral

categories?

We recognize that significant concerns have been expressed by the user community regarding volatility in annual surplus/deficit resulting from the current conceptual framework, and that a compromise may be required to satisfactorily address these concerns. Should PSAB choose to introduce deferred inflows/outflows, our preference would be the establishment of tight rules around deferred inflows and outflows to ensure rigour and consistency and minimize the risk of inappropriate usage of these categories. When establishing these rules, PSAB should consider at a minimum the work of IPSASB, which includes the following key points: • Deferral should only be limited to non-exchange transactions with stipulations on the reporting period in which they are to be used. • Multi-year grants with no substantive performance obligation or return provision would only quality for deferral if the period over which those resources can be used is documented and recorded in an agreement. Our preference would also be that only inflows externally restricted to fund costs of future periods should qualify for deferral. Endowments and government transfers could fall in this category.

9. Should a set of general purpose financial statements of a public sector entity include other statements based on the identified accountabilities? For example, a separate (audited) statement of debt and other liabilities might respond to the financial statement accountability relating to debt and other liabilities, the sub-characteristic under “public accountability” that is “debt capacity” and provide useful information to consider in an evaluation of the financial condition of a public sector entity. Please explain your reasoning.

We would be very cautious about adding additional statements. Additional statements may not be required to meet identified accountabilities – for example, debt capacity is currently captured in the statement of financial position and preparers are required to disclose adequate information about the nature and terms of a government's liabilities (PS 1201.046). The inclusion of additional statements is an area of judgement where different standard-setters have taken different approaches to certain accountability objectives. For example, budget to actual comparisons under PSAS are reported in the statement of operations and the statement of net debt (PS 1201.128), whereas under IPSAS entities are given a choice to report either as a separate additional financial statement or as a budget column in the financial statements (IPSAS 1.21). Another example relates to reporting unrealized valuation changes from the results of operations; PSAS currently prescribes the use of a separate statement of remeasurement gains and losses to report unrealized valuation changes (PS 1201.092) whereas IPSAS requires all resulting exchange differences be recognized as a separate component of net assets/equity (IPSAS 4.44 c)). While a model with additional statements may be manageable if a common understanding of messages and interrelationships is made, at one point too many statements may result in more complicated financial reporting process without increasing the understandability of the information.

GENERAL COMMENTS

We support the the Conceptual Framework Task Force in its efforts to review of the PSAB conceptual framework and the concepts underlying financial performance in the public sector. While this consultation paper includes a total of nine questions, the most significant ones in our view relate to identifying the preferred financial statement presentation alternative (question 6) and setting rules around accounting for deferred inflows and outflows should they be allowed (question 8). Given that none of the three financial statement presentation alternatives meets all the identified financial statement accountabilities and that each of the alternatives has its respective benefits and drawbacks, it is difficult to conclude that one alternative is clearly superior to another. On balance, for the reasons identified in our detailed response, the Office has a preference for the Asset and Liability model. Should PSAB introduce deferred inflows / outflows, the Office would support the establishment of tight rules around their use to ensure rigour and consistency and minimize the risk of inappropriate usage of these categories. When establishing these rules, PSAB should consider at a minimum the work of IPSASB.

Click here to submit

Response Questionnaire Consultation Paper 2: Measuring Financial Performance in Public Sector Financial Statements

TO BE CONSIDERED, COMMENTS MUST BE RECEIVED BY JANUARY 31, 2013 Prepared by: Conceptual Framework Task Force

This form is not intended to constrain your response. Each text box will accommodate your full comments. You are able to save and forward this form to others in your organization for review prior to submission.

Name: Claude D. Carter, FCA

Organization: CCC Inc.

E-mail: [email protected]

1. Do you agree with an approach to a public sector conceptual framework that focuses on identified accountabilities to the public and their elected representatives rather than an approach focused on the needs of discrete user groups? Please explain your reasoning.

Yes. Although I still believe that those governments owe money to (debenture holders, pension plan members, etc.) are equally relevant users of public sector financial reporting. These groups may have more of an interest in government's ability to meet its existing obligations than some in the general public and elected representatives.

2. Do you agree with the proposal that the objective of public sector financial reports is to provide information for accountability purposes? Please explain your reasoning.

Yes, but not at the exclusion of all other purposes. Valuation and the ability to meet existing obligations or to sustain levels of service should be of interest to most FS users. I suspect that such is still covered by the identified accountabilities, but maybe not as predominantly.

3. Do you agree with the proposal that public sector financial reports should be designed to provide accountability information to the public and their elected representatives (i.e., that the public and their elected representatives are the primary users of the financial reports)? Please explain your reasoning.

No. I believe those that government's have financial obligations (e.g., debenture holders, pension plan members) could also be considered primary users.

4. Do you agree with the three proposed broad financial accountabilities expected to be demonstrated by a public sector entity about the financial affairs of the entity? Please explain your reasoning.

Yes, but I have a lingering discomfort about the central role that a government's financial plan or budget - something that is not necessarily developed using a generally accepted framework or set of standards/principles established after due process/diligence like PSAS - is afforded in the broad financial accountabilities. I know there is no way to get around it, but wouldn't it be great if the budget community in the Canadian public sector could at least identify and codify its key principles and practices. The reality is that government financial plans and budgets are not subject to independent assurance reporting like financial statements.

5. Do you agree with the 16 proposed financial statement accountabilities? Are there any missing? Are there any that should not be included? Please explain your reasoning.

Yes

6. Which of the three financial statement presentation alternatives do you prefer? Is a hybrid model (hybrid in the sense described in this Consultation Paper) an option that the Task Force should pursue? Please explain the reasoning for your choice and indicate why the other two alternatives were not chosen.

#1 - Asset and Liability

7. If you do not like any of the three financial statement presentation alternatives set out in this Consultation Paper, do you have another preferred model that would meet the identified financial statement accountabilities? Please explain your suggested model in sufficient detail for the Task Force to evaluate the proposal.

n/a

8. If new financial statement categories for deferred inflows and outflows are set up, what items would you see being accounted for in these categories (for example, endowments, general tax revenue, transfers received)? Do you have any suggestions for the criteria that should be used to determine what can/should be accounted for in those categories? For example, consider the following for inflows (and similar questions for outflows): Does there need to be an external restriction on an inflow, requiring it to be applied to cost of services provided in

future periods (time or performance requirement) in order for the inflow to be deferred? Is an internally made but publicly communicated commitment to consistently use a certain type of inflow to provide

future services enough to trigger deferral? If an internal commitment is allowed to trigger deferral, should an irrevocable designation for its application to the

cost of service provision in future periods be made upon receipt of inflow/levying of taxation? How direct should the relationship be between the inflow and the costs of services to be provided in future periods

in order for deferral of the inflow to be permitted? Should only items that do not meet the definitions of assets and liabilities be considered for inclusion in deferral

categories?

9. Should a set of general purpose financial statements of a public sector entity include other statements based on the identified accountabilities? For example, a separate (audited) statement of debt and other liabilities might respond to the financial statement accountability relating to debt and other liabilities, the sub-characteristic under “public accountability” that is “debt capacity” and provide useful information to consider in an evaluation of the financial condition of a public sector entity. Please explain your reasoning.

GENERAL COMMENTS

Click here to submit

Response Questionnaire Consultation Paper 2: Measuring Financial Performance in Public Sector Financial Statements

TO BE CONSIDERED, COMMENTS MUST BE RECEIVED BY JANUARY 31, 2013 Prepared by: Conceptual Framework Task Force

This form is not intended to constrain your response. Each text box will accommodate your full comments. You are able to save and forward this form to others in your organization for review prior to submission.

Name: Office of the Comptroller, Province of New Brunswick

Organization: Government of New Brunswick

E-mail: [email protected]

1. Do you agree with an approach to a public sector conceptual framework that focuses on identified accountabilities to the public and their elected representatives rather than an approach focused on the needs of discrete user groups? Please explain your reasoning.

We agree with the approach that focuses on identified accountabilities to the public and their elected representatives. The private sector has users that are more financially sophisticated (e.g. investors and creditors) and there are both fewer and more clearly identified user needs for the information which together make it appropriate to design a framework around users and user needs. However, in the Public Sector, we agree that there are far more user groups, users that are less financially sophisticated, and user needs that are more difficult to outline. In addition, certain user groups/needs could be missed if they were the only items identified and used as the approach to a conceptual framework especially given the challenges with user needs studies.

2. Do you agree with the proposal that the objective of public sector financial reports is to provide information for accountability purposes? Please explain your reasoning.

We agree that the objective of public sector financial reports is to provide information for accountability purposes. Governance, performance, stewardship and sustainability should be the objectives of the public sector financial reports and guide the overall conceptual framework.

3. Do you agree with the proposal that public sector financial reports should be designed to provide accountability information to the public and their elected representatives (i.e., that the public and their elected representatives are the primary users of the financial reports)? Please explain your reasoning.

We agree that public sector financial reports should be designed to provide accountability information to the public and their elected representatives. Because the information is prepared for the public, we feel it is very important to ensure the statements are understandable. The current financial statements are already complex for most users, even for those with a reasonable understanding of economic activities and accounting. Therefore, we feel any changes made should clarify the statements not increase their complexity.

4. Do you agree with the three proposed broad financial accountabilities expected to be demonstrated by a public sector entity about the financial affairs of the entity? Please explain your reasoning.

We agree with the three proposed broad financial accountabilities.

5. Do you agree with the 16 proposed financial statement accountabilities? Are there any missing? Are there any that should not be included? Please explain your reasoning.

We need to have additional information regarding the 16 proposed financial statement accountabilities. We agree with the accountabilities but want to know what each accountability means and what the implications are on specific standards.

6. Which of the three financial statement presentation alternatives do you prefer? Is a hybrid model (hybrid in the sense described in this Consultation Paper) an option that the Task Force should pursue? Please explain the reasoning for your choice and indicate why the other two alternatives were not chosen.

We prefer the Asset & Liability (A&L) Model for the following reasons: 1) it meets 14/16 of the outlined accountabilities; 2) users are familiar with the current model and we feel the hybrid model would increase the complexity of the statements; 3) the R&E model would increase volatility and subjectivity to the statements and the deferred inflows/outflows would increase complexity; 4) the A&L model reflects the true economic reality and decisions of government; 5) it would be easier to make changes to the existing A&L model as opposed to creating a new one. Therefore, would like PSAB to consider reviewing the A&L model and possibly making some changes (For example: review the definition of a liability and address the issue of volatility); 6) there may or may not be both unrealized and realized gains & losses. We feel that this is yet to be determined. 7) hybrid model introduces another statement and this would increase complexity. We felt it was very difficult to make a choice on one of the new models without numerical examples, some additional information regarding the financial statement accountabilities (and their impact on existing standards), and proposed rules and examples for the deferred inflows/outflows. The hybrid model does meet most of the outlined accountabilities, improve budget to actual comparisons and focuses on realized performance as opposed to anticipated performance. However, we don't feel we have sufficient information to choose the hybrid model and are also concerned that it would not be understandable to users. We feel the R&E model would introduce too much subjectivity to the statements and lead to inconsistent application of the standards across jurisdictions.

7. If you do not like any of the three financial statement presentation alternatives set out in this Consultation Paper, do you have another preferred model that would meet the identified financial statement accountabilities? Please explain your suggested model in sufficient detail for the Task Force to evaluate the proposal.

N/A

8. If new financial statement categories for deferred inflows and outflows are set up, what items would you see being accounted for in these categories (for example, endowments, general tax revenue, transfers received)? Do you have any suggestions for the criteria that should be used to determine what can/should be accounted for in those categories? For example, consider the following for inflows (and similar questions for outflows): Does there need to be an external restriction on an inflow, requiring it to be applied to cost of services provided in

future periods (time or performance requirement) in order for the inflow to be deferred? Is an internally made but publicly communicated commitment to consistently use a certain type of inflow to provide

future services enough to trigger deferral? If an internal commitment is allowed to trigger deferral, should an irrevocable designation for its application to the

cost of service provision in future periods be made upon receipt of inflow/levying of taxation? How direct should the relationship be between the inflow and the costs of services to be provided in future periods

in order for deferral of the inflow to be permitted? Should only items that do not meet the definitions of assets and liabilities be considered for inclusion in deferral

categories?

We need additional information regarding deferred inflows and outflows with specific criteria that outlines how they will be used in the models with numerics attached. If deferred inflows and outflows were introduced to the financial statements, we would have to ensure that rules would be developed to prevent introducing subjectivity into the statements. For example, if inflows do not have to be externally restricted in order to be deferred, there could be very inconsistent application of the standards and a lot of subjectivity introduced. The deferred inflows/outflows would need to be restricted to certain non-exchange transactions with stipulations outlining the reporting period in which they are used.

9. Should a set of general purpose financial statements of a public sector entity include other statements based on the identified accountabilities? For example, a separate (audited) statement of debt and other liabilities might respond to the financial statement accountability relating to debt and other liabilities, the sub-characteristic under “public accountability” that is “debt capacity” and provide useful information to consider in an evaluation of the financial condition of a public sector entity. Please explain your reasoning.

We do not feel that this is necessary as sufficient information can be obtained from the A&L model statements to evaluate the condition of the entity. In addition, adding another statement will increase the complexity for users.

GENERAL COMMENTS

Click here to submit

Response Questionnaire Consultation Paper 2: Measuring Financial Performance in Public Sector Financial Statements

TO BE CONSIDERED, COMMENTS MUST BE RECEIVED BY JANUARY 31, 2013 Prepared by: Conceptual Framework Task Force

This form is not intended to constrain your response. Each text box will accommodate your full comments. You are able to save and forward this form to others in your organization for review prior to submission.

Name: Gregory MacBeth

Organization: Office of the Auditor General of Manitoba

E-mail: [email protected]

1. Do you agree with an approach to a public sector conceptual framework that focuses on identified accountabilities to the public and their elected representatives rather than an approach focused on the needs of discrete user groups? Please explain your reasoning.

We do not agree that the general purpose financial statements should focus on the public and elected officials at the exclusion of discreet user groups. For accountability and decision making purposes, service recipients and service providers will also need information for decisions making purposes.

2. Do you agree with the proposal that the objective of public sector financial reports is to provide information for accountability purposes? Please explain your reasoning.

Yes. However, we prefer IPSASB's accountability and decision making proposal. The CFTF already recognizes decision making as a subset of accountability. Considering both would be consistent with our answer in question #1.

3. Do you agree with the proposal that public sector financial reports should be designed to provide accountability information to the public and their elected representatives (i.e., that the public and their elected representatives are the primary users of the financial reports)? Please explain your reasoning.

Yes. However, information needs by other user groups should be considered. The focus should be on knowledgeable readers.

4. Do you agree with the three proposed broad financial accountabilities expected to be demonstrated by a public sector entity about the financial affairs of the entity? Please explain your reasoning.

Yes.

5. Do you agree with the 16 proposed financial statement accountabilities? Are there any missing? Are there any that should not be included? Please explain your reasoning.

Yes. However, it is not necessary to demonstrate accountability of all the characteristics in one set of financial statements. Other accountability documents could be prepared.

6. Which of the three financial statement presentation alternatives do you prefer? Is a hybrid model (hybrid in the sense described in this Consultation Paper) an option that the Task Force should pursue? Please explain the reasoning for your choice and indicate why the other two alternatives were not chosen.

Of the three alternatives, we prefer the asset and liability model. The focus is on a government's ability to finance its activities, meet its financial obligations and provide service. Although the revenue and expense model has a valid objective of providing accountability information on the cost of services provided in the period and revenue applicable for the period, we have concern on the determination of how to allocate revenue to the appropriate period. We believe the hybrid model would be too confusing to the readers because there would be different conceptual frameworks for the statement of financial position and statement of operations plus a new statement introduced.

7. If you do not like any of the three financial statement presentation alternatives set out in this Consultation Paper, do you have another preferred model that would meet the identified financial statement accountabilities? Please explain your suggested model in sufficient detail for the Task Force to evaluate the proposal.

PSAB should seriously consider the adoption of IPSASB's model. International consistency is important.

8. If new financial statement categories for deferred inflows and outflows are set up, what items would you see being accounted for in these categories (for example, endowments, general tax revenue, transfers received)? Do you have any suggestions for the criteria that should be used to determine what can/should be accounted for in those categories? For example, consider the following for inflows (and similar questions for outflows): Does there need to be an external restriction on an inflow, requiring it to be applied to cost of services provided in

future periods (time or performance requirement) in order for the inflow to be deferred? Is an internally made but publicly communicated commitment to consistently use a certain type of inflow to provide

future services enough to trigger deferral? If an internal commitment is allowed to trigger deferral, should an irrevocable designation for its application to the

cost of service provision in future periods be made upon receipt of inflow/levying of taxation? How direct should the relationship be between the inflow and the costs of services to be provided in future periods

in order for deferral of the inflow to be permitted? Should only items that do not meet the definitions of assets and liabilities be considered for inclusion in deferral

categories?

The categories set up should be consistent with the IPSASB model.

9. Should a set of general purpose financial statements of a public sector entity include other statements based on the identified accountabilities? For example, a separate (audited) statement of debt and other liabilities might respond to the financial statement accountability relating to debt and other liabilities, the sub-characteristic under “public accountability” that is “debt capacity” and provide useful information to consider in an evaluation of the financial condition of a public sector entity. Please explain your reasoning.

General purpose financial statements could include other statements but information about specific accountabilities could also be included in notes or schedules.

GENERAL COMMENTS

I am replying on behalf of the Office of the Auditor General - Manitoba. My comments are from the perspective of the public sector within our jurisdiction.

Click here to submit

January 31, 2013 Tim Beauchamp Director, Public Sector Accounting 277 Wellington Street West Toronto, Ontario M5V 3H2 Dear Mr. Beauchamp, RE: Consultation Paper #2 – Measuring Financial Performance in Public Sector Financial Statements Thank you for the opportunity to provide comments on the Measuring Financial Performance in Public Sector Financial Statements Consultation Paper. The Conceptual Framework project has been initiated in response to a report issued by a Joint Working Group (JWG) of select PSAB members and Deputy Ministers of Finance. Our overall impression is that the proposals in this Consultation Paper, particularly with respect to the financial statement presentation alternatives, go beyond what is required in order to deal with the concerns raised in the JWG report. We feel the seemingly simpler proposals put forward in that paper still have a large degree of merit. As a result, much of our present response revisits and re-iterates the suggestions contained in that document. One of the key issues raised in the JWG report was the disagreement with introducing fair value measurement to public sector financial reports. We are disappointed that none of the concepts in this Consultation Paper seem to address this concern. At no point does the paper discuss the appropriateness of including fair value measurement in a public sector conceptual framework. Instead, it seems to assume that the need for fair value measurement is a given. We strongly encourage the Task Force to give careful consideration to issues raised with respect to fair value measurement. Only in limited circumstances would fair value actually provide relevant information to the primary users of government financial statements. The Conceptual Framework should clearly articulate this narrow degree of applicability. In summary, we are in favor of the proposed emphasis on public accountability and the public as the primary users of financial statements. We agree with some, but not all, of the 16 proposed financial statement accountabilities. Any final list of accountabilities must be grounded in the identified needs of our primary user group. We don’t believe financial statement presentation alternatives need to be considered. Instead, we feel the needed changes can be accomplished by elaborating on certain concepts contained in the current asset-liability model.

PO Box 187 1723 Hollis Street Halifax, NS B3J 2N3 (902) 424-7021 [email protected] Department of Finance

Government Accounting

1. Do you agree with an approach to a public sector conceptual framework that focuses on identified accountabilities to the public and their elected representatives rather than an approach focused on the needs of discrete user groups? Please explain your reasoning. We agree that the framework cannot attempt to address the needs of all potential users. Discrete user groups typically have the ability to obtain the information they need through alternative means. Therefore, general purpose financial statements do not have to be designed to meet the information needs of these groups. In our view, the needs of the primary user group (public and elected representatives) should be the cornerstone on which decisions about the concepts underlying financial performance are made. We agree with an approach that focuses on identified accountabilities to the public and their elected representatives to the extent that those accountabilities are defined in response to the needs of the primary user group. It would be useful to see the degree to which the identified accountabilities align with identified user needs. More information on the results of user needs studies would allow us to provide a more thorough response to this question.

2. Do you agree with the proposal that the objective of public sector financial reports is to provide information for accountability purposes? Please explain your reasoning. Yes, we agree that the primary objective of government financial statements is to provide information for accountability purposes, specifically accountability over the management of public funds. The objective of public sector financial reports should be to meet the information needs of the primary user group. Citizens demand public accountability in two primary areas. First, they want assurance that public money is being used in a manner that reflects the priorities of the people. Second, they are concerned with the ongoing ability to receive the public services that are important to them. As such, the primary objective of public sector financial reports should be to provide the citizens with information that will help them assess the degree to which a government is meeting these accountabilities.

3. Do you agree with the proposal that public sector financial reports should be designed to provide

accountability information to the public and their elected representatives (i.e., that the public and their elected representatives are the primary users of the financial reports)? Please explain your reasoning. We agree that the public and their elected representatives are the primary users of government financial reports. As noted in the consultation paper, members of the public are often less financially sophisticated than other types of user groups. As such, the importance of understandability in a public sector conceptual framework for financial reporting cannot be under-emphasized. The conceptual framework must make it clear that understandability cannot be compromised without solid justification. The profession should not over-estimate the financial sophistication of the public and our elected officials. We must, to the extent possible, show complex matters in a simplified and understandable way. Financial accountability is a key component of the democratic process because many political platforms and promises are based on, or supported by, fiscal merit. For the public to adequately assess the degree to which the fiscal benefits are achieved, financial information must be as clear and approachable as possible.

When a proposed standard would undoubtedly impair understandability, it should proceed only if the primary user group will gain clear benefits from the information the standard intends to reveal. To provide benefits, the standard must provide a truer picture of the government’s economic reality. Standard setters must clearly demonstrate how a proposed standard will achieve this objective before incorporating it into the Public Sector Accounting (PSA) Handbook. The PSA standard on financial instruments is a case in point. We continue to argue that the public gains little benefit from seeing financial instruments, particularly derivatives, measured at fair value when there is no intention to settle these items at fair value. Derivative arrangements are designed to prevent fair value gains and losses so their substance is such that they have few to no economic consequences for the government holding them. As such, the government’s economic reality is not fairly represented by the fictitious, “moment-in-time” gains and losses that accrue at the end of a reporting period. Consequently, users are provided with complex information that is of little benefit to them and even less real financial consequence. Fair value measurement, in this context, does not provide the primary user group with the accountability information it needs.

4. Do you agree with the three proposed broad financial accountabilities expected to be

demonstrated by a public sector entity about the financial affairs of the entity? Please explain your reasoning. We agree with the three proposed broad financial accountabilities. These accountabilities appear to be a fair representation of what the public would want to know about the government’s financial matters. We further agree that financial statements can provide only a part of the information required to demonstrate the full range of these accountabilities. We continue to applaud the Task Force’s emphasis on addressing only those pieces of accountability that can reasonably be demonstrated through financial statements and the notes thereto.

5. Do you agree with the 16 proposed financial statement accountabilities? Are there any missing? Are there any that should not be included? Please explain your reasoning. We do not agree with the 16 proposed financial statement accountabilities. In particular, #6, “the separation of unrealized valuation changes from the results of operations,” should not be included. Valuation changes should only be reflected in financial statements to the extent that they represent a real economic risk to the government. When no real risk is present, these unrealized gains and losses do not provide any useful information about a government’s performance or its financial condition. When it is unlikely that items being reported at fair value will ever be settled at that value, no remeasurement to fair value should take place. If the instruments in question are likely to be settled at fair value, then changes in fair value represent a real risk to the government holding them. As a real risk, the unrealized gains or losses should flow through the statement of operations as a cost or reward of conducting business in that manner. In these circumstances, there is no need to separate unrealized from realized valuation changes. They should both be included in the Statement of Operations and used to assess government performance because they both reflect real risks the government has assumed and should be held accountable for. We are concerned that the 16 financial statement accountabilities may not be rooted in identified user needs. For example, we are not convinced that the public and their elected representatives are

interested in valuation changes that are unlikely to be realized. Before finalizing the list of financial statement accountabilities, the Task Force should confirm that these items are of true and material concern to the primary users of public sector financial reports. Information that is deemed somewhat useful, but not critical for public accountability, should be reserved for the notes to the financial statements. Finally, we would like to note that accountabilities 12 through 16 appear redundant. In our view, these concepts are already contained within accountabilities 9 through 11.

6. Which of the three financial statement presentation alternatives do you prefer? Is a hybrid model (hybrid in the sense described in this Consultation Paper) an option that the Task Force should pursue? Please explain the reasoning for your choice and indicate why the other two alternatives were not chosen. We do not believe that new financial statement presentation alternatives are necessary. Our preference is to continue with the existing model, but to address inconsistencies in the way the conceptual framework is presently interpreted. The two primary concerns relate to the liability definition in the context of non-exchange transactions and the use of fair value measurement. We believe there is room within the existing asset-liability model to deal with both of these issues. For example, the existing liability definition should be explained such that it clearly includes the moral/constructive obligation that is created when a government accepts non-exchange resources, from an external party, that are restricted for a specific purpose. In determining the degree and end to which the resources are restricted, the substance, not just the form, of the transferor’s intentions must be considered. This explanation could be contained within the conceptual framework, but would likely be a better fit within PS 3200 – Liabilities. In our view, this clarification would require a liability to be recognized when assets are received and the transferor’s intent is, in substance, for such assets to be used for a specific purpose. The liability would be settled as the assets are used as intended. Concerns raised with respect to fair value measurement can also be dealt with within the existing asset-liability model. Our present conceptual framework already acknowledges that public sector financial reports are to be “prepared primarily using the historical cost basis of measurement.” The framework could elaborate on this concept by explaining those limited situations in which fair value would be an appropriate basis of measurement. Specifically, the framework should restrict the use of fair value to those situations where the government is exposed to the real risks and benefits of fair value fluctuations. Fair value measurement should be avoided in cases where it does not represent the true economic substance of the government’s financial condition and performance. The hybrid-model is not an option that the Task Force should pursue. Financial performance and financial position are intrinsically linked and it is illogical to view them as separate, non-corresponding concepts. The introduction of a hybrid model adds complexity to financial reporting and reduces understandability for the primary user group. In our view, a new model is unnecessary because, as discussed above, the current deficiencies in PSA standards can be easily dealt with within the existing asset-liability approach.

We have not selected the revenue-expense model because we are concerned that there will be excessive subjectivity involved in assigning costs and revenues to one time period or another. We believe the existing asset-liability view, with the previously discussed amendments, will allow for more consistent reporting from one jurisdiction to the next.

7. If you do not like any of the three financial statement presentation alternatives set out in this Consultation Paper, do you have another preferred model that would meet the identified financial statement accountabilities? Please explain your suggested model in sufficient detail for the Task Force to evaluate the proposal. Our preferred approach is described in our response to question 6. It is different from the existing asset-liability alternative in that it does not meet the accountability which calls for “the separation of unrealized valuation changes from the results of operations.” However, as we’ve explained in our response to question 5, we do not believe this particular item should be included in the list of financial statement accountabilities.

8. If new financial statement categories for deferred inflows and outflows are set up, what items would you see being accounted for in these categories (for example, endowments, general tax revenue, transfers received)? Do you have any suggestions for the criteria that should be used to determine what can/should be accounted for in those categories? For example, consider the following for inflows (and similar questions for outflows):

a. Does there need to be an external restriction on an inflow, requiring it to be applied to cost of services provided in future periods (time or performance requirement) in order for the inflow to be deferred?

b. Is an internally made but publicly communicated commitment to consistently use a certain type of inflow to provide future services enough to trigger deferral?

c. If an internal commitment is allowed to trigger deferral, should an irrevocable designation for its application to the cost of service provision in future periods be made upon receipt of inflow/levying of taxation?

d. How direct should the relationship be between the inflow and the costs of services to be provided in future periods in order for deferral of the inflow to be permitted?

e. Should only items that do not meet the definitions of assets and liabilities be considered for inclusion in deferral categories?

In our view, the definitions of assets and liabilities should be used to determine if deferral is appropriate and therefore, new categories are not necessary. As described in our response to question 6, we feel that certain deferred inflows (restricted-use assets from external parties) already meet the definition of a liability. In our view, there is a claim on restricted-use assets; at minimum, a moral obligation to use them in a certain way. Once the government accepts the resources, with full knowledge of the transferor’s intentions, it has little discretion but to use the resources in the manner intended. As such that government has incurred a liability that can only be settled by using the resources in accordance with the substance of the transferor’s objectives. Deferred inflows that do not meet the liability test (e.g., resources which, in substance, have no restricted use), should be recognized as revenue. Similarly, deferred outflows that meet the definition of an asset should be recognized as such. Those that do not should be charged to expense.

9. Should a set of general purpose financial statements of a public sector entity include other statements based on the identified accountabilities? For example, a separate (audited) statement of debt and other liabilities might respond to the financial statement accountability relating to debt and other liabilities, the sub-characteristic under “public accountability” that is “debt capacity” and provide useful information to consider in an evaluation of the financial condition of a public sector entity. Please explain your reasoning. No, a set of general purpose financial statements of a public sector entity should not include other statements based on the identified accountabilities. Too much information can obscure the more important messages in a set of financial statements. It is our belief that additional statements will only serve to reduce understandability when the objective should be to improve understandability. An audited line item with required disclosures should be sufficient to meet users’ needs for accountability information with respect to debt (and other specific financial statement items). If there is reason to suspect that user needs are not adequately served by the information presently provided with respect to debt, then improved disclosures should be considered before the introduction of a new financial statement. This concludes our comments on the Measuring Financial Performance in Public Sector Financial Statements Consultation Paper. We would be pleased to discuss any questions or comments you may have with respect to this letter. To do so, please contact Jill Devanney ([email protected]), Rob Bourgeois ([email protected]), or the undersigned. Regards,

Suzanne Wile, CA Executive Director, Government Accounting Nova Scotia Department of Finance

Montréal, le 31 janvier 2013 Tim Beauchamp, directeur Comptabilité du secteur public 277, rue Wellington Ouest Toronto (Ontario) M5V 3H2 Monsieur, Vous trouverez ci-joint les commentaires du Groupe de travail technique Secteur public - Comptabilité dans le secteur public de l’Ordre des comptables professionnels agréés du Québec concernant le document de consultation « La mesure de la performance financière dans les états financiers du secteur public ». Nous vous serions reconnaissants de nous faire parvenir une copie de la traduction anglaise de nos commentaires. Veuillez prendre note que ni l’Ordre des comptables professionnels agréés du Québec, ni quelque personne que ce soit ayant participé à la préparation des commentaires ne peuvent être tenus responsables relativement à son utilisation et ils ne sont tenus à aucune garantie de quelque nature que ce soit découlant de ces commentaires, comme décrit dans le déni de responsabilité joint à la présente. Veuillez agréer, Monsieur Beauchamp, l’expression de mes sentiments distingués. Représentante du Groupe de travail technique Secteur public - Comptabilité dans le secteur public, Annie Smargiassi CPA, CA p. j. Déni de responsabilité et commentaires

DÉNI DE RESPONSABILITÉ

Les documents préparés par le Groupe de travail technique Secteur public - Comptabilité dans

le secteur public de l’Ordre des comptables professionnels agréés du Québec (Ordre) ci-après

appelés les «commentaires», sont fournis selon les conditions décrites dans la présente, pour

faire connaître leur opinion sur des énoncés de principes, des documents de consultation, des

exposés-sondages préliminaires ainsi que des exposés-sondages publiés par le Conseil des

normes comptables, le Conseil des normes d’audit et de certification, le Conseil sur la

comptabilité dans le secteur public, le Conseil sur la gestion des risques et la gouvernances et

d’autres organismes.

Les commentaires fournis par ce comité ne doivent pas être utilisés comme substitut à des

missions confiées à des professionnels spécialisés. Il est important de noter que les lois, les

normes et les règles sur lesquelles sont émis les commentaires peuvent changer en tout temps

et que, dans certains cas, les commentaires écrits peuvent être sujets à controverse.

Ni l’Ordre, ni quelque personne que ce soit ayant participé à la préparation des commentaires ne

peuvent être tenus responsables relativement à l’utilisation de ces commentaires et ils ne sont

tenus à aucune garantie de quelque nature que ce soit découlant de ces commentaires. Les

commentaires donnés ne lient pas, par ailleurs, les membres du Groupe de travail technique

Secteur public - Comptabilité dans le secteur public, l’Ordre ou, de façon plus particulière, le

Bureau du syndic de l’Ordre.

La personne qui se réfère ou utilise ces commentaires assume l’entière responsabilité de sa

démarche ainsi que tous les risques liés à l’utilisation de ceux-ci. Elle consent à exonérer

l’Ordre à l’égard de toute demande en dommages-intérêts qui pourrait être intentée par suite de

toute décision qu’elle aurait pu prendre en fonction de ces commentaires. Elle reconnaît

également avoir accepté de ne pas faire état de ces commentaires reçus via le Groupe de travail

dans les avis exprimés ou les positions prises.

COMMENTAIRES DU GROUPE DE TRAVAIL TECHNIQUE SECTEUR PUBLIC - COMPTABILITÉ DANS LE SECTEUR PUBLIC DE L’ORDRE DES COMPTABLES PROFESSIONNELS AGRÉÉS DU QUÉBEC RELATIFS AU DOCUMENT DE CONSULTATION «LA MESURE DE LA PERFORMANCE FINANCIÈRE DANS LES ÉTATS FINANCIERS DU SECTEUR PUBLIC ».

MANDAT DU GROUPE DE TRAVAIL

Le Groupe de travail technique Secteur public - Comptabilité dans le secteur public de l'Ordre des

comptables professionnels agréés du Québec a comme mandat notamment de recueillir et de

canaliser le point de vue des praticiens exerçant en cabinet et de membres œuvrant dans les affaires,

dans les services gouvernementaux, dans l'industrie et dans l'enseignement ainsi que le point de vue

d’autres personnes concernées œuvrant dans des domaines d’expertise connexes.

Pour chaque exposé-sondage ou autre document étudié, les membres du Groupe de travail

technique mettent leurs analyses en commun. Les commentaires ci-dessous reflètent les points de

vue exprimés et, sauf indication contraire, ces commentaires ont fait l'objet d'un consensus parmi les

membres du Groupe de travail ayant participés à cette analyse.

Les commentaires formulés par le Groupe de travail ne font l'objet d'aucune sanction de l'Ordre. Ils

n'engagent pas la responsabilité de celui-ci.

COMMENTAIRES GÉNÉRAUX

D’abord, les membres ont souligné le travail colossal du Groupe de travail sur le cadre conceptuel et

l’ouverture qui a été démontrée dans le document de consultation. Ils reconnaissent les efforts qui

ont été déployés dans le cadre de ce projet.

Ils suggèrent toutefois au groupe de travail de présenter des données chiffrées pour chacune des

approches. En effet, ceci permettrait de mieux comprendre les différences entre les trois approches

et de faire les liens avec les états financiers les reflétant.

Certains membres ont également précisé que le cadre conceptuel devrait être axé sur les états