canada superior court province of …documentcentre.eycan.com/eycm_library/quebecor world...

TRANSCRIPT

CANADA S U P E R I O R C O U R T PROVINCE OF QUÉBEC Commercial Division DISTRICT OF MONTRÉAL COURT NO: 500-11-032338-085

Designated tribunal under the Companies’ Creditors Arrangement Act1

IN THE MATTER OF THE PLAN OF

COMPROMISE OR ARRANGEMENT OF QUEBECOR WORLD INC. AND VARIOUS SUBSIDIARIES AS LISTED IN SCHEDULE “A”

DEBTORS - and - ERNST & YOUNG INC. MONITOR

11th REPORT OF THE MONITOR – JULY 21, 2008

INTRODUCTION AND BACKGROUND

1. On January 21, 2008 this Court, sitting as designated tribunal under the Companies’ Creditors Arrangement Act (“CCAA”)1, issued an order at the request of Quebecor World Inc. (“QWI”) and certain of its affiliates (collectively, the “Petitioners” or “Debtors”) declaring that the Petitioners are debtor companies to which the CCAA applies, granting certain relief to them while they prepare a plan of arrangement pursuant to the CCAA, and appointing Ernst & Young Inc. as monitor (“EYI” or “Monitor”). The initial order of the Court, which governs these proceedings, was modified on January 31, February 19, April 21, and May 9, 2008 (the “Initial Order”).

2. Contemporaneously, all of the Petitioners other than QWI (the “U.S. Debtors”) asked for and received relief under Chapter 11 of the U.S. Bankruptcy Code2 (the “Code”).

3. The orders granted by this Court and by the Bankruptcy Court of the Southern District of New York together with the relief provided under the CCAA and the Code3 (collectively the “Orders”) provide, among other things, for a stay of proceedings against the Debtors while they prepare a restructuring plan.

4. Early on in the course of the restructuring proceedings (“Proceedings”), a concern was expressed both in Canada and in the United States by several creditors, namely the Official Committee of Unsecured Creditors (“UCC”) appointed in the proceedings under the Code, and various other ad hoc committees appointed by the bondholders and the banking syndicate

1 Companies’ Creditors Arrangement Act (“CCAA”), R.S.C. 1985, c. C-36, as amended. 2 U.S. Code, title 11, chapter 11. 3 Section §362 of the U.S. Bankruptcy Code.

Page 2

(collectively, the “Committees”), regarding the extent and complexity of transactions amongst the companies in the Quebecor World group of companies (“QWG”), transactions that may have occurred between QWG and a few related or affiliated parties, and certain transactions that occurred before the date of inception of the Proceedings.

5. As a result of these concerns and the discussions held with the advisors to the Committees, it was decided that it would be appropriate for the Monitor to undertake a review of those transactions and report thereon. The work to be performed by the Monitor in this regard is described in the Second Report of the Monitor to this Court, dated February 14, 2008 (the “Second Report”), at paragraph 63 thereof. For purposes of convenience for the reader, this paragraph is reproduced hereinbelow:

“63. The Monitor has received requests from advisors for each of the Ad Hoc Committees to conduct a factual investigation of information concerning the status of the inter-company accounts of Quebecor World group (the “Group”). As a result, the Monitor will prepare a narrative report which will address the topics set forth below. The Ad Hoc Committees have requested that the Monitor’s report does not render any opinion or analysis, as the report is being commissioned as an efficient methodology for the multiple interested parties to receive the facts regarding topics set forth below. The Ad Hoc Committees have requested that the Monitor’s report not be binding on any party and shall not constitute evidence of the subject matter contained therein, and have indicated that each of the Ad Hoc Committees reserves its respective rights to use, or not use, the Monitor’s report and to form and advocate any position based thereon.

63.1 an overview of the nature of the inter-company transactions that occur within the Group;

63.2 preliminarily, an accounting of the financial position of the more significant legal entities involved in the inter-company transactions, as at (or close to) the filing date (information on additional entities will be provided should any of the Ad Hoc Committees so request);

63.3 a description of the transactions and inter-company flows from the use of the pre-petition credit facility and the issuance of public and private debt securities of QWI and subsidiaries;

63.4 an analysis of the use of proceeds derived from issuance of the 4.875% Senior Notes due 2008, 6.125% of Senior Notes due 2013, 9.75% Senior Notes due 2015, and 8.75% Senior Notes due 2016 and the related documentation on inter-company flows, including the mirror notes;

63.5 a listing of the inter-company balances, as recorded by the Company among the Quebecor World group legal entities as at January 21, 2008;

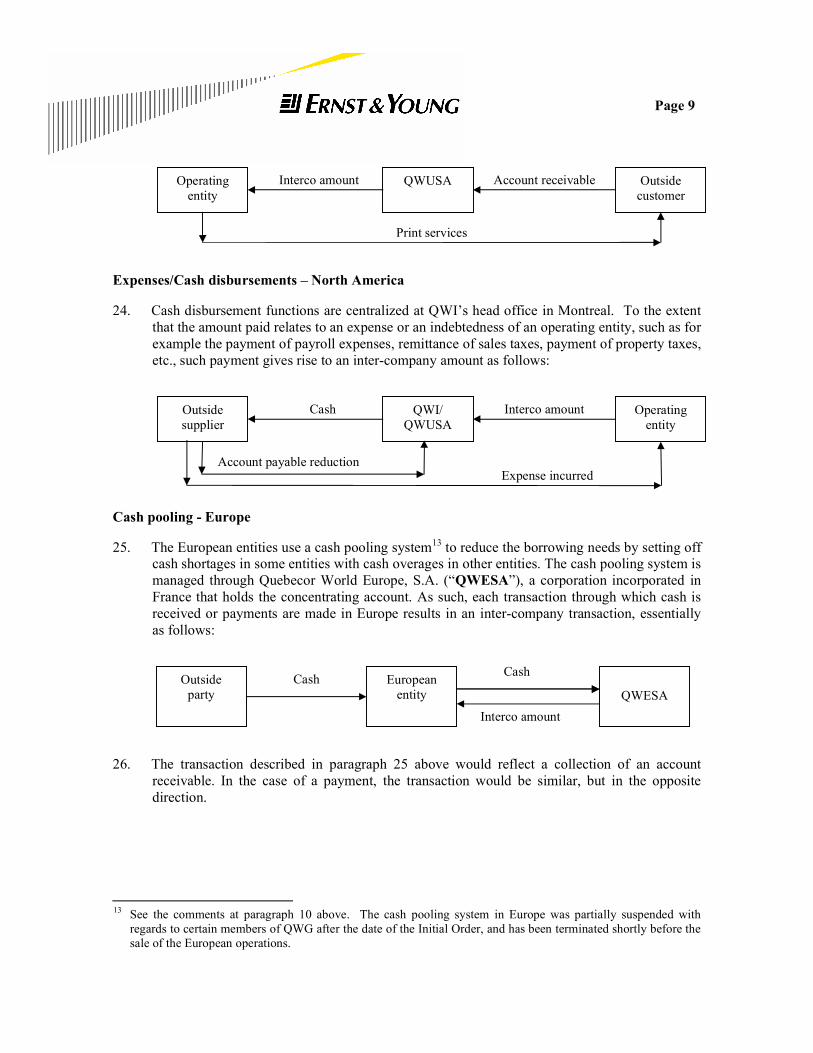

63.6 a summary of the procedures implemented by QWI to track post-petition inter-company transactions between the Petitioners and among the entire Group;

63.7 a summary of the nature of inter-company transactions between QWI, Quebecor Inc. and Quebecor Media Inc., the balances between those entities as of the filing date and the current procedures in place to track post-petition transactions; and

Page 3

63.8 a factual description of the transactions through which approximately $370 million of private notes were repaid in October, 2007, which resulted in an increase in the indebtedness due to the Bank Syndicate and in the security provided to the bank group.”

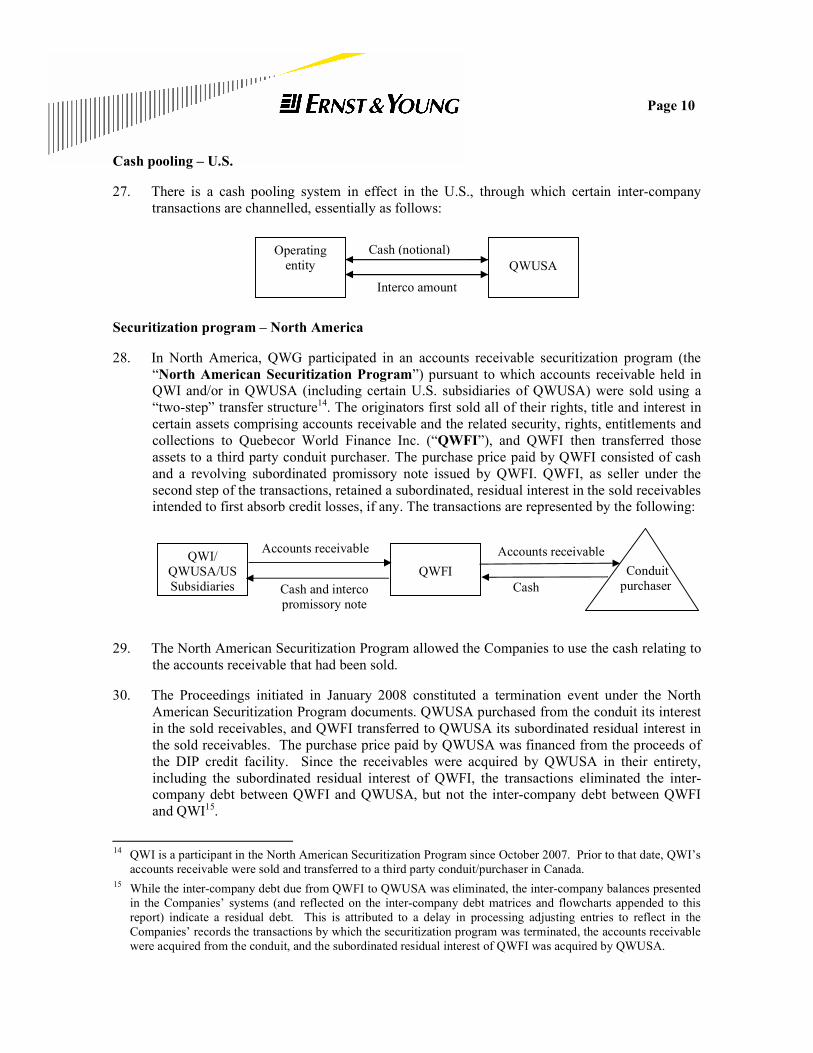

6. The Monitor has made progress in respect of the work contemplated in paragraph 63 of the Second Report. However this work is not yet completed, due to a number of factors, including in particular:

6.1. The complexity of the corporate structure and the very high level of interaction between the affiliates. QWG comprised approximately 180 entities as at January 21, 2008, including approximately 10 in Canada, 95 in the U.S., 20 in Latin America and 50 in Europe.

6.2. The fact that financial information systems are complex and cumbersome.

6.3. The fact that the employees who could assist the Monitor in performing this review had a very heavy workload requiring them to direct their attention to other high priority projects, such as preparing and coordinating the compilation of information required for the statutory forms required in the proceedings under the Code and the CCAA; preparing monthly operating reports and other information required in the proceedings under the Code and the CCAA; reporting obligations in connection with the Interim Financing (“DIP Financing”) approved in the context of the Proceedings; compiling information required in the context of the negotiations for the sale of the European operations4, and compiling information to respond to the high volume of requests for information formulated by the Committees, all of which needs to be addressed in addition to the accounting department’s regular workload.

7. More specifically, the portion of the work that is not yet completed to a level satisfactory to the Monitor relates to the preparation of financial statements showing the financial position of the more significant entities (paragraph 63.2 of the Second Report) and a summary of the transactions between the entities of QWG and Quebecor Inc. (“QI”), Quebecor Media Inc. (“QMI”), and other parties or persons affiliated to QI or QMI.

8. As the Monitor considers the work on the other aspects sufficiently advanced, subject to additional queries or clarifications from this Court or from the Committees, as the case may be, and in view of the fact that additional time will be required before the Monitor can be in a position to report on the information referred to in paragraph 7 above, the Monitor thought it would be appropriate to issue this interim report on the findings to date (the “Report”) 5. The content of the Report is presented under the following categories:

4 See the 8th Report of the Monitor, dated June 10, 2008. 5 The reader should not infer from this comment that the information herein on the inter-company balances or that

the financial statements prepared on an entity by entity basis will contain precise information regarding the inter-company balances. In view of the fact that the accounting process necessarily involves estimates, that errors can always be made in recording transactions and that some transactions are not allocated to individual entities, as is explained in this Report, the information presented in connection with the inter-company balances, both herein and in the financial statements that will be prepared on an entity by entity basis can never be perfectly accurate but reflect the best available estimate of the inter-company balances and is thought to be a fair representation of the amounts due between the entities.

Page 4

INTRODUCTION AND BACKGROUND .............................................................................. 1

TERMS OF REFERENCE ........................................................................................................ 5

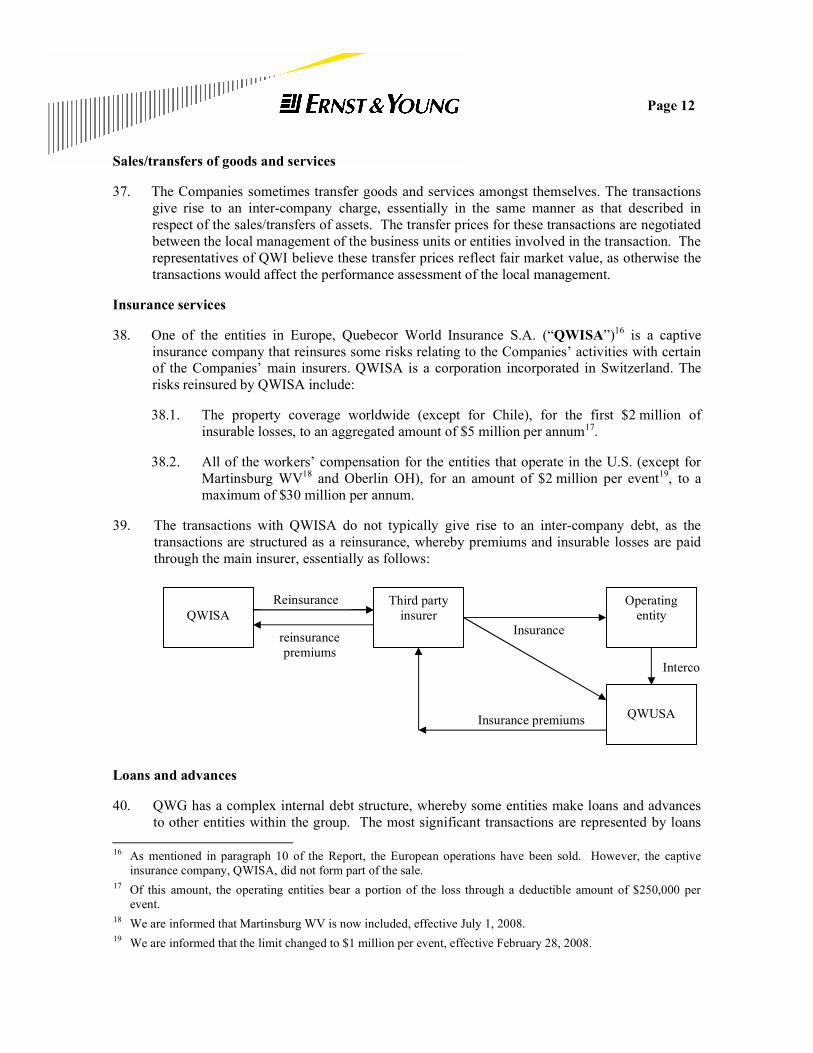

DISCLAIMER........................................................................................................................... 5

STRUCTURE OF QWG ........................................................................................................... 6

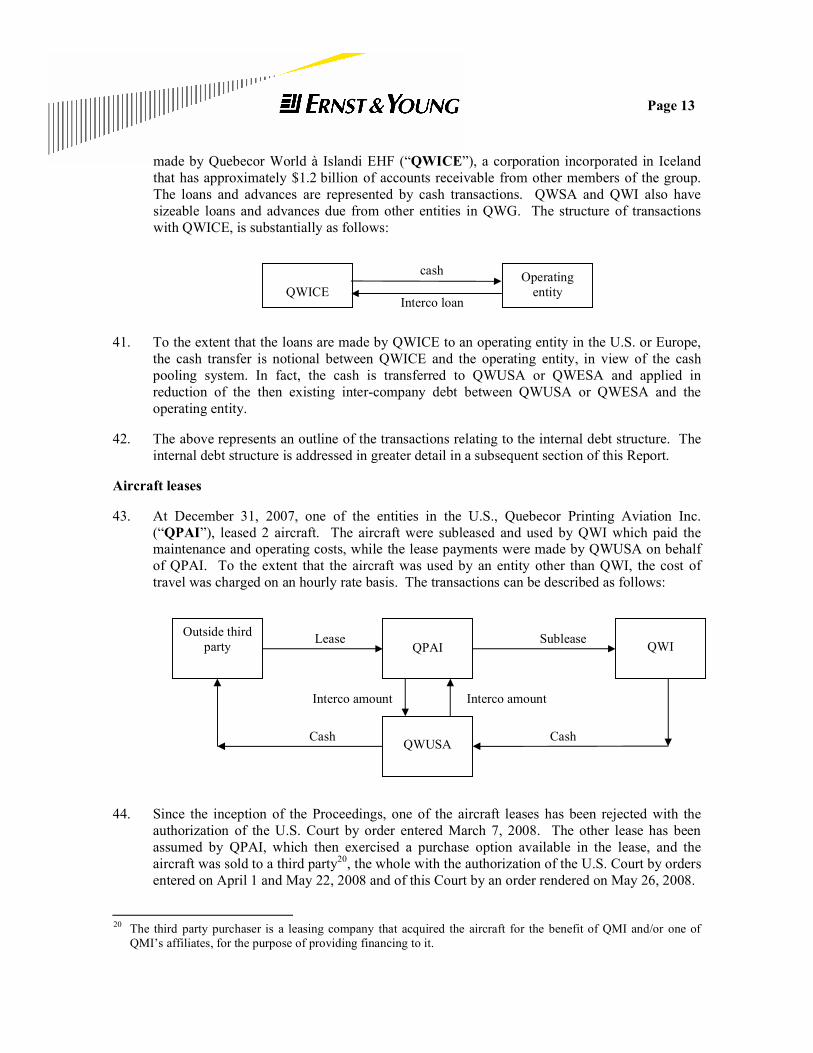

NATURE OF THE INTER-COMPANY TRANSACTIONS THAT OCCUR WITHIN QWG ......................................................................................................................... 6

Purchase transactions ........................................................................................................ 7 Sale transactions – U.S...................................................................................................... 8 Expenses/Cash disbursements – North America............................................................... 9 Cash pooling - Europe....................................................................................................... 9 Cash pooling – U.S. ........................................................................................................ 10 Securitization program – North America........................................................................ 10 Allocation of common expenses ..................................................................................... 11 Royalties.......................................................................................................................... 11 Sales/transfers of assets................................................................................................... 11 Sales/transfers of goods and services .............................................................................. 12 Insurance services ........................................................................................................... 12 Loans and advances ........................................................................................................ 12 Aircraft leases ................................................................................................................. 13 Leasing transactions........................................................................................................ 14 Financing vehicles – public debt..................................................................................... 14

INTERNAL DEBT STRUCTURE.......................................................................................... 15

INTER-COMPANY DEBT..................................................................................................... 16

TRACKING INTER-COMPANY TRANSACTIONS ........................................................... 17

ANALYSIS OF THE USE OF PROCEEDS FROM SENIOR NOTES ................................. 18 Senior notes due in 2008 and 2013 ................................................................................. 18 Senior notes due in 2015................................................................................................. 19 Senior notes due in 2016................................................................................................. 20 Senior debentures due in 2027 ........................................................................................ 21

EXTERNAL DEBT STRUCTURE ........................................................................................ 22

REPAYMENT OF PRIVATE NOTES IN OCTOBER 2007 ................................................. 22 Private notes issued on July 15, 2000 ............................................................................. 22 Balance outstanding in October 2007 ............................................................................. 23 Note repayment in October 2007 .................................................................................... 23 Source of funds ............................................................................................................... 24

OVERALL COMMENTS AND CONCLUSION................................................................... 26

Page 5

TERMS OF REFERENCE

9. In this Report:

The capitalized terms not defined herein are as defined in the Initial Order or in the previous reports of the Monitor.

“Dollars” or “$”: U.S. currency, unless specified otherwise.

“QWI” or “Company”: Quebecor World Inc., the parent company of the various corporations/entities in the Quebecor World group of companies.

“QWG” or “Companies”: The various corporations, partnerships, limited liability companies, limited partnerships, or other legal persons that are part of the Quebecor World group, including QWI. For greater clarity, QWG includes only QWI and those entities that are direct or indirect subsidiaries of QWI, and does not include QI, QMI or other entities related to QI or QMI.

“Debtors” or “Petitioners”: QWI and various entities amongst QWG that are applicants in the proceedings in Canada under the CCAA and/or in the proceedings in the U.S. under chapter 11 of the Code. Conversely, the term “Non-Petitioner” will be used to describe an entity that is part of QWG but is not an applicant in the proceedings under the CCAA and/or the Code.

The terms inter-company balances, amounts, loans, advances, notes, etc. are used interchangeably. Some of the transactions are documented through loan agreements or notes, and some transactions merely result in the recording of an advance, receivable or payable between the entities of QWG. The description of a transaction in this Report should not be interpreted as inferring the manner in which a transaction is documented, solely based on the terminology used.

10. This Report refers to the corporate structure, transactions, inter-company balances, etc. as they existed as at December 31, 2007 or on the dates specified herein, as the case may be. The structure is subject to change, in particular (but without limitation) as a result of the insolvency proceedings initiated in the United Kingdom in respect of the affiliates in the U.K.6, as a result of the sale of the European operations7, and as a result of various other restructuring initiatives being implemented by the Companies.

DISCLAIMER

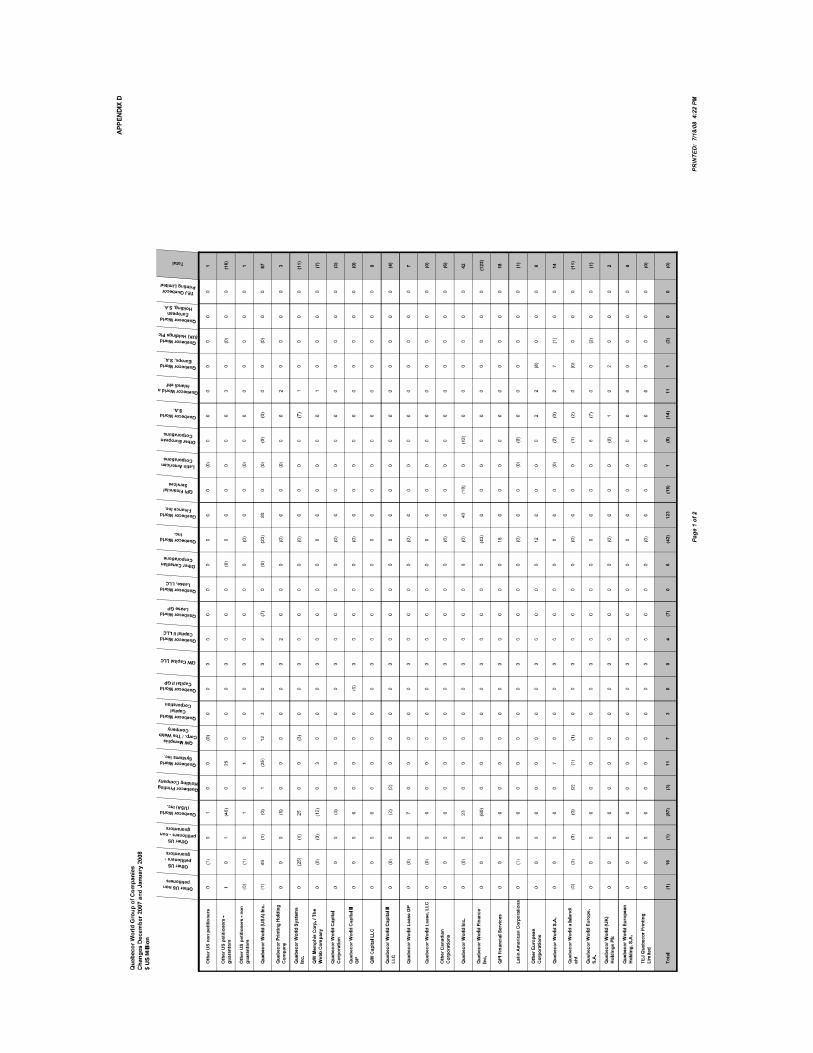

11. In preparing this Report, the Monitor has relied upon unaudited financial information, company records, company prepared financial information and projections, discussions with management and employees of QWG, and information from various other sources.

6 See the 3rd Report of the Monitor, dated April 1, 2008 and the 5th Report of the Monitor, dated May 6, 2008. 7 See note 4 above.

Page 6

While we reviewed various documents and believe that the information herein provides a fair summary of the transactions as presented to us or as reflected in the documents presented to us, such work does not constitute an audit or verification of such information for accuracy, completeness, or compliance with generally accepted accounting principles. Accordingly, EYI expresses no opinion or other form of assurance in respect of such information.

In the course of our mandate, we have assumed the integrity and truthfulness of the information and explanations presented to us, within the context in which it was presented. To date, nothing has come to our attention which would cause us to question the reasonableness of this assumption.

Finally, we have requested that management bring to our attention any significant matters which were not addressed in the course of our specific inquiries. Accordingly, this Report is based solely on the information (financial or otherwise) made available to us.

This Report has been prepared for the use of this Court as general information relating to the Companies and their operations. Given the nature of EYI’s mandate, this information is preliminary only and is subject to change as the mandate progresses.

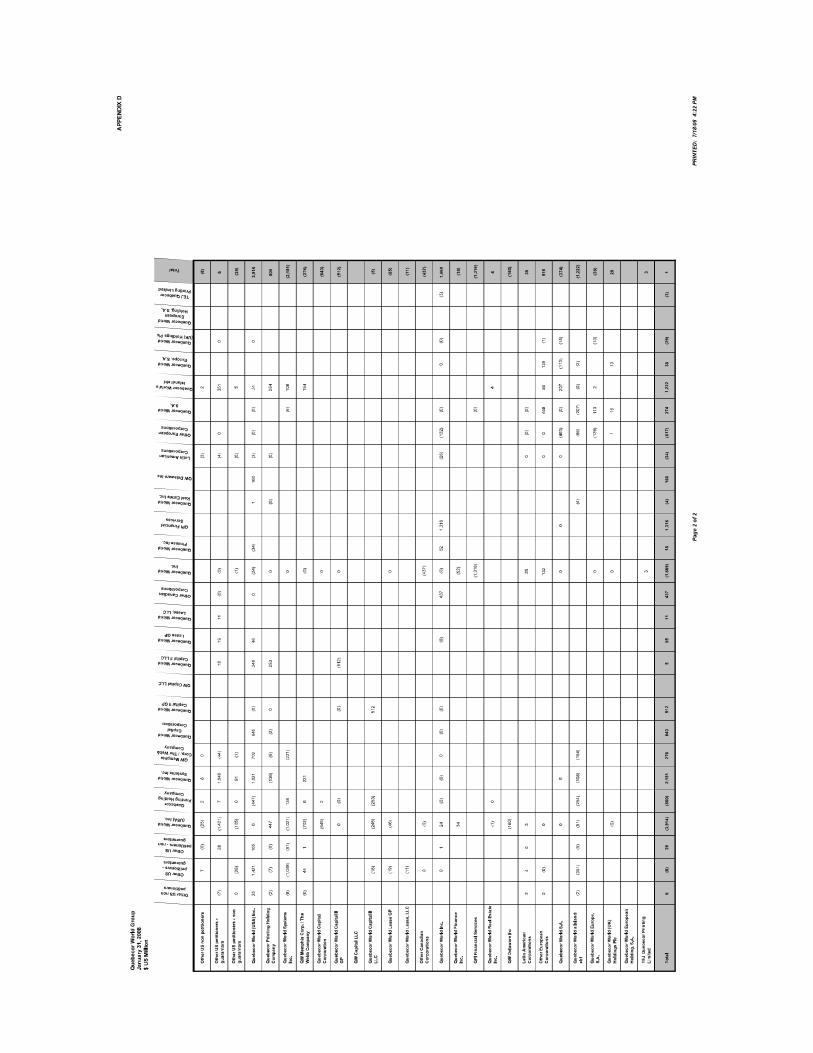

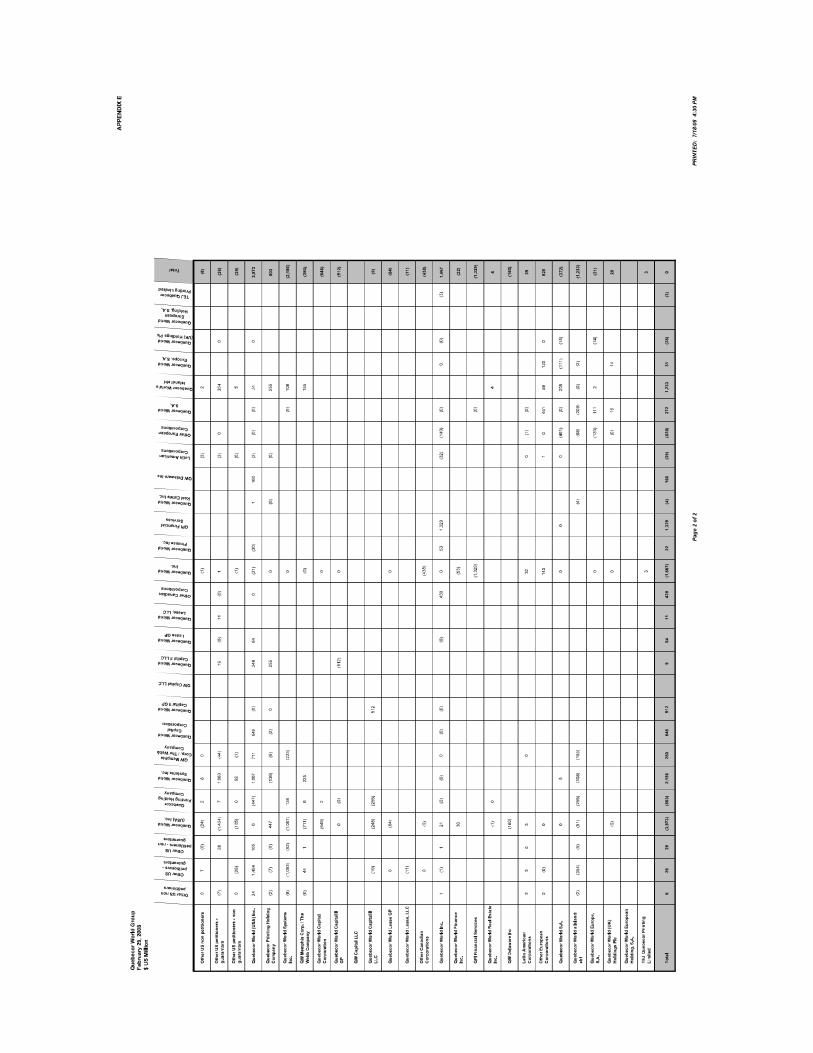

STRUCTURE OF QWG

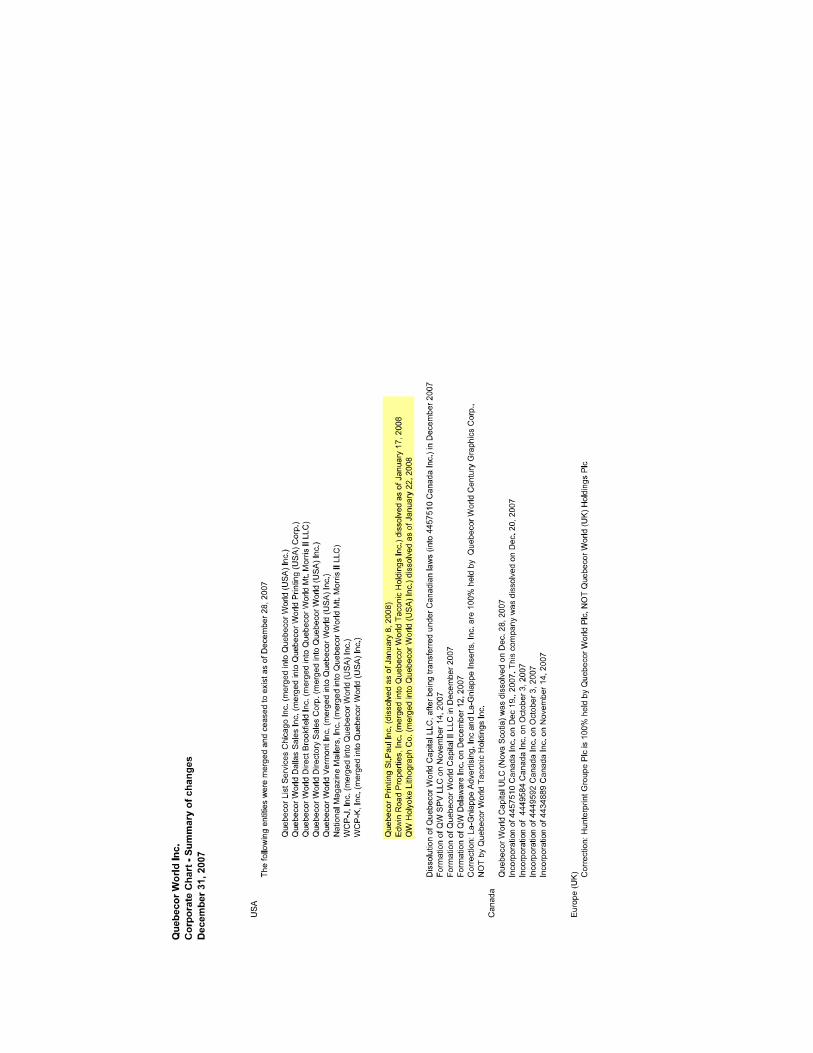

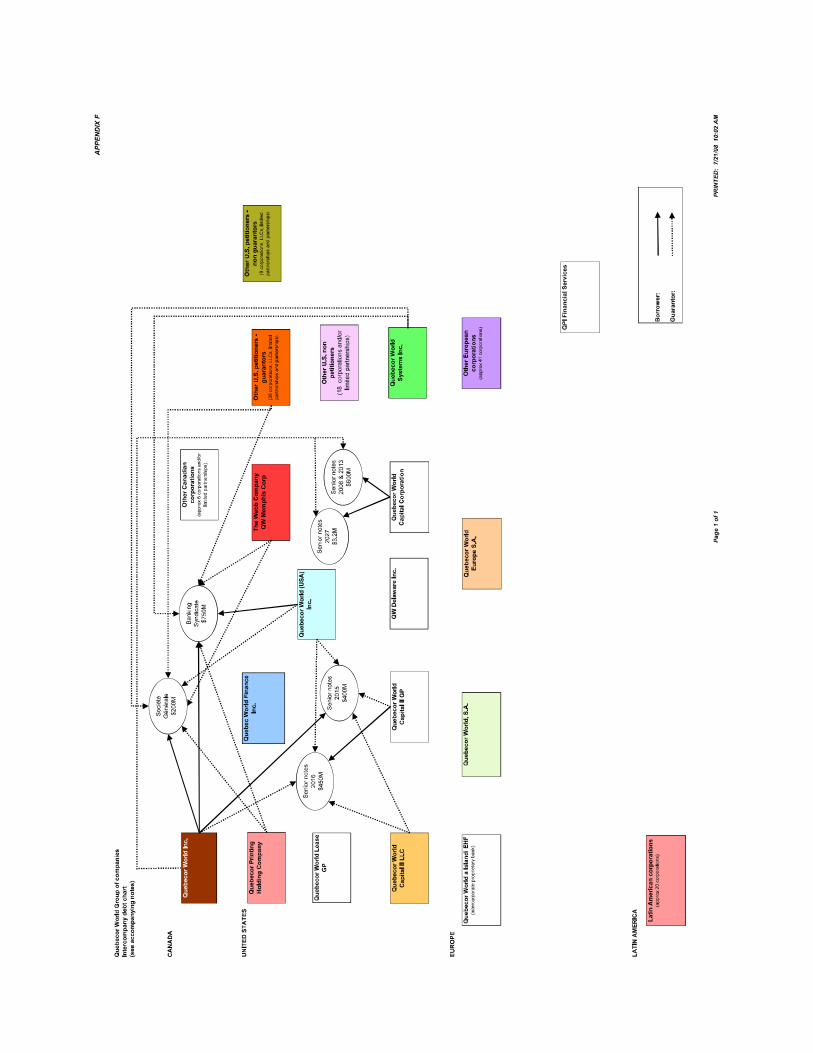

12. A corporate chart indicating the relationship between the various entities forming QWG, the geographical location of the entities and their branches, is presented as Appendix A. The corporate chart indicates the status of QWG as of December 31, 2007.

NATURE OF THE INTER-COMPANY TRANSACTIONS THAT OCCUR WITHIN QWG

13. The Companies’ administrative functions are significantly centralized in a few main locations. The information systems are complex and cumbersome, and are designed to provide management with information based on business units8. The administrative processes put in place to manage the business are such that a large number of commercial transactions, including transactions with outside third parties, can give rise to inter-company transactions.

14. The Companies’ operations are segregated based on the following business units, namely: magazine, retail insert group, catalogues, book services, directories and direct mail services.

15. The Companies have operations in North America9, Europe10 and Latin America9. Due to the corporate structure and international operations, some inter-company transactions result from financing vehicles11 and/or local legal requirements12.

8 Substantially, the Companies’ systems provide information based on business units for reporting on the

operations, and on a consolidated basis for external reporting purposes. Obtaining information on a legal entity basis is difficult, as the Companies’ systems do not easily accommodate this level of reporting, since the Companies have seen limited needs thus far for detailed entity by entity information. The Companies have started adapting their systems to extract information based on legal entities, in addition to the other levels of reporting that are more relevant to management.

9 Mexico is considered as part of Latin America for purposes of the corporate structure.

Page 7

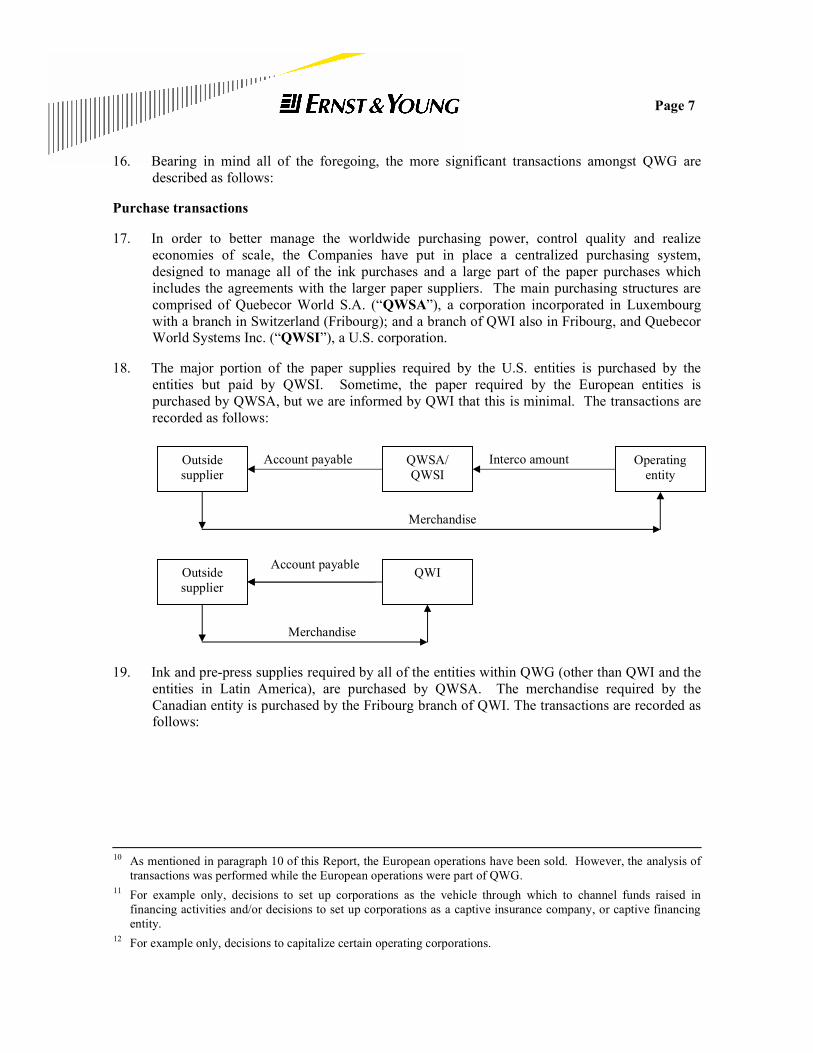

16. Bearing in mind all of the foregoing, the more significant transactions amongst QWG are described as follows:

Purchase transactions

17. In order to better manage the worldwide purchasing power, control quality and realize economies of scale, the Companies have put in place a centralized purchasing system, designed to manage all of the ink purchases and a large part of the paper purchases which includes the agreements with the larger paper suppliers. The main purchasing structures are comprised of Quebecor World S.A. (“QWSA”), a corporation incorporated in Luxembourg with a branch in Switzerland (Fribourg); and a branch of QWI also in Fribourg, and Quebecor World Systems Inc. (“QWSI”), a U.S. corporation.

18. The major portion of the paper supplies required by the U.S. entities is purchased by the entities but paid by QWSI. Sometime, the paper required by the European entities is purchased by QWSA, but we are informed by QWI that this is minimal. The transactions are recorded as follows:

19. Ink and pre-press supplies required by all of the entities within QWG (other than QWI and the entities in Latin America), are purchased by QWSA. The merchandise required by the Canadian entity is purchased by the Fribourg branch of QWI. The transactions are recorded as follows:

10 As mentioned in paragraph 10 of this Report, the European operations have been sold. However, the analysis of

transactions was performed while the European operations were part of QWG. 11 For example only, decisions to set up corporations as the vehicle through which to channel funds raised in

financing activities and/or decisions to set up corporations as a captive insurance company, or captive financing entity.

12 For example only, decisions to capitalize certain operating corporations.

Outside supplier

QWSA/ QWSI

Operating entity

Account payable Interco amount

Merchandise

Outside supplier

QWI

Merchandise

Account payable

Page 8

20. With regards to the purchases that are made by the U.S. operating entities directly, the transactions are recorded through an inter-company entry in the records of Quebecor World (U.S.A.) Inc. (“QWUSA”) as follows:

21. The prices charged by QWSA are intended to reflect arm’s length pricing and are supported by transfer pricing documentation prepared by external consultants. The recording of accounts payable and payment of amounts on behalf of affiliates by QWUSA and QWSI do not have a profit component.

22. The transactions as described above reflect the usual manner in which they are recorded. In compiling financial information on an entity by entity basis while preparing the statements of assets and liabilities used in connection with the proceedings under the Code, the Companies made certain adjustments to some of the inter-company transactions that could be identified, in order to reallocate the accounts payable due to an outside supplier to the entity that had in fact ordered the merchandise. These adjustments were processed as at December 31, 2007 and an equivalent adjustment was processed as at January 31, 2008. This adjustment is reflected in the inter-company account balances referred to in this Report.

Sale transactions – U.S.

23. In the U.S., sale transactions give rise to inter-company transactions, in view of the fact that the trade accounts receivable are pooled with those of QWUSA. The transactions are recorded as follows:

Outside supplier

QWSA Operating entity

Account payable Interco amount

Merchandise

Outside supplier

QWI

Merchandise

Account payable

Outside supplier

QWUSA Operating entity

Account payable Interco amount

Merchandise

Page 9

Expenses/Cash disbursements – North America

24. Cash disbursement functions are centralized at QWI’s head office in Montreal. To the extent that the amount paid relates to an expense or an indebtedness of an operating entity, such as for example the payment of payroll expenses, remittance of sales taxes, payment of property taxes, etc., such payment gives rise to an inter-company amount as follows:

Cash pooling - Europe

25. The European entities use a cash pooling system13 to reduce the borrowing needs by setting off cash shortages in some entities with cash overages in other entities. The cash pooling system is managed through Quebecor World Europe, S.A. (“QWESA”), a corporation incorporated in France that holds the concentrating account. As such, each transaction through which cash is received or payments are made in Europe results in an inter-company transaction, essentially as follows:

26. The transaction described in paragraph 25 above would reflect a collection of an account receivable. In the case of a payment, the transaction would be similar, but in the opposite direction.

13 See the comments at paragraph 10 above. The cash pooling system in Europe was partially suspended with

regards to certain members of QWG after the date of the Initial Order, and has been terminated shortly before the sale of the European operations.

European entity

QWESA

Interco amount

Cash Outside party

Cash

Outside supplier

QWI/ QWUSA

Operating entity

Cash Interco amount

Account payable reduction Expense incurred

Operating entity

QWUSA Outside customer

Interco amount Account receivable

Print services

Page 10

Cash pooling – U.S.

27. There is a cash pooling system in effect in the U.S., through which certain inter-company transactions are channelled, essentially as follows:

Securitization program – North America

28. In North America, QWG participated in an accounts receivable securitization program (the “North American Securitization Program”) pursuant to which accounts receivable held in QWI and/or in QWUSA (including certain U.S. subsidiaries of QWUSA) were sold using a “two-step” transfer structure14. The originators first sold all of their rights, title and interest in certain assets comprising accounts receivable and the related security, rights, entitlements and collections to Quebecor World Finance Inc. (“QWFI”), and QWFI then transferred those assets to a third party conduit purchaser. The purchase price paid by QWFI consisted of cash and a revolving subordinated promissory note issued by QWFI. QWFI, as seller under the second step of the transactions, retained a subordinated, residual interest in the sold receivables intended to first absorb credit losses, if any. The transactions are represented by the following:

29. The North American Securitization Program allowed the Companies to use the cash relating to the accounts receivable that had been sold.

30. The Proceedings initiated in January 2008 constituted a termination event under the North American Securitization Program documents. QWUSA purchased from the conduit its interest in the sold receivables, and QWFI transferred to QWUSA its subordinated residual interest in the sold receivables. The purchase price paid by QWUSA was financed from the proceeds of the DIP credit facility. Since the receivables were acquired by QWUSA in their entirety, including the subordinated residual interest of QWFI, the transactions eliminated the inter-company debt between QWFI and QWUSA, but not the inter-company debt between QWFI and QWI15.

14 QWI is a participant in the North American Securitization Program since October 2007. Prior to that date, QWI’s

accounts receivable were sold and transferred to a third party conduit/purchaser in Canada. 15 While the inter-company debt due from QWFI to QWUSA was eliminated, the inter-company balances presented

in the Companies’ systems (and reflected on the inter-company debt matrices and flowcharts appended to this report) indicate a residual debt. This is attributed to a delay in processing adjusting entries to reflect in the Companies’ records the transactions by which the securitization program was terminated, the accounts receivable were acquired from the conduit, and the subordinated residual interest of QWFI was acquired by QWUSA.

QWFI

Cash and interco promissory note

Cash Conduit purchaser

Accounts receivable Accounts receivable QWI/ QWUSA/US Subsidiaries

Operating entity

QWUSA

Interco amount

Cash (notional)

Page 11

Allocation of common expenses

31. Some expenses are incurred on behalf of several entities. As an example only, the head office administrative functions and professional fees are allocated periodically based on formulas that are reviewed by outside professionals in order to comply with transfer pricing and income tax expense deductibility rules.

32. The allocation of expenses is performed amongst the Companies through inter-company charges and/or a management fee expense, and covers expenses such as information technology (“IT”), selling, general and administrative expenses (“SG&A”) and purchase volume discounts.

33. In the U.S., some common expenses are not reallocated through inter-company charges. Examples of transactions that should give rise to an inter-company reallocation but that are not would include the payment of income taxes. Based on our discussions with representatives of QWI, we believe the potential adjustments relating to these common expenses cannot be quantified.

Royalties

34. In addition to the responsibility for recording certain accounts payable relating to certain purchases made by U.S. operating entities and issuing payments for these accounts payable, QWSI owns and manages certain of the intangible property of QWG in the U.S.. The intangible property consists of the rights to the paper supply contracts, and the names and trademarks associated with the Quebecor World name. The entities in the U.S. are charged (every quarter) a royalty for the use of the intellectual or intangible property.

Sales/transfers of assets

35. The Companies sometimes transfer assets amongst themselves. This may occur when contracts are transferred from one production unit to another or when new equipment is installed and the previously used equipment is transferred to an entity that can still use the older or less sophisticated equipment. The transfer price is intended to reflect the fair market value of the assets transferred when a cross-border transfer takes place and their net book value when the transfers are between entities in the same country. The transactions by which equipment is transferred or sold amongst the Companies give rise to an inter-company charge, essentially as follows:

36. The inter-company balances created through these transactions are settled through the cash pooling systems (referred to earlier herein) by a notional cash transfer, or are settled in cash when the assets are transferred between regions.

Operating entity

Operating entity

equipment

Interco amount

Page 12

Sales/transfers of goods and services

37. The Companies sometimes transfer goods and services amongst themselves. The transactions give rise to an inter-company charge, essentially in the same manner as that described in respect of the sales/transfers of assets. The transfer prices for these transactions are negotiated between the local management of the business units or entities involved in the transaction. The representatives of QWI believe these transfer prices reflect fair market value, as otherwise the transactions would affect the performance assessment of the local management.

Insurance services

38. One of the entities in Europe, Quebecor World Insurance S.A. (“QWISA”)16 is a captive insurance company that reinsures some risks relating to the Companies’ activities with certain of the Companies’ main insurers. QWISA is a corporation incorporated in Switzerland. The risks reinsured by QWISA include:

38.1. The property coverage worldwide (except for Chile), for the first $2 million of insurable losses, to an aggregated amount of $5 million per annum17.

38.2. All of the workers’ compensation for the entities that operate in the U.S. (except for Martinsburg WV18 and Oberlin OH), for an amount of $2 million per event19, to a maximum of $30 million per annum.

39. The transactions with QWISA do not typically give rise to an inter-company debt, as the transactions are structured as a reinsurance, whereby premiums and insurable losses are paid through the main insurer, essentially as follows:

Loans and advances

40. QWG has a complex internal debt structure, whereby some entities make loans and advances to other entities within the group. The most significant transactions are represented by loans

16 As mentioned in paragraph 10 of the Report, the European operations have been sold. However, the captive

insurance company, QWISA, did not form part of the sale. 17 Of this amount, the operating entities bear a portion of the loss through a deductible amount of $250,000 per

event. 18 We are informed that Martinsburg WV is now included, effective July 1, 2008. 19 We are informed that the limit changed to $1 million per event, effective February 28, 2008.

reinsurance premiums

Operating entity

Insurance

QWUSA

Interco

Insurance premiums

QWISA

Third party insurer

Reinsurance

Page 13

made by Quebecor World à Islandi EHF (“QWICE”), a corporation incorporated in Iceland that has approximately $1.2 billion of accounts receivable from other members of the group. The loans and advances are represented by cash transactions. QWSA and QWI also have sizeable loans and advances due from other entities in QWG. The structure of transactions with QWICE, is substantially as follows:

41. To the extent that the loans are made by QWICE to an operating entity in the U.S. or Europe, the cash transfer is notional between QWICE and the operating entity, in view of the cash pooling system. In fact, the cash is transferred to QWUSA or QWESA and applied in reduction of the then existing inter-company debt between QWUSA or QWESA and the operating entity.

42. The above represents an outline of the transactions relating to the internal debt structure. The internal debt structure is addressed in greater detail in a subsequent section of this Report.

Aircraft leases

43. At December 31, 2007, one of the entities in the U.S., Quebecor Printing Aviation Inc. (“QPAI”), leased 2 aircraft. The aircraft were subleased and used by QWI which paid the maintenance and operating costs, while the lease payments were made by QWUSA on behalf of QPAI. To the extent that the aircraft was used by an entity other than QWI, the cost of travel was charged on an hourly rate basis. The transactions can be described as follows:

44. Since the inception of the Proceedings, one of the aircraft leases has been rejected with the authorization of the U.S. Court by order entered March 7, 2008. The other lease has been assumed by QPAI, which then exercised a purchase option available in the lease, and the aircraft was sold to a third party20, the whole with the authorization of the U.S. Court by orders entered on April 1 and May 22, 2008 and of this Court by an order rendered on May 26, 2008.

20 The third party purchaser is a leasing company that acquired the aircraft for the benefit of QMI and/or one of

QMI’s affiliates, for the purpose of providing financing to it.

Operating entity

QWICE

cash

Interco loan

QPAI

Outside third party

Cash

Lease

QWUSA

Interco amount

Sublease

Interco amount

Cash

QWI

Page 14

Leasing transactions

45. One of the entities in the U.S., Quebecor World Lease GP (“QWLGP”), leases equipment that is used by the Companies based on subleases, on terms substantially similar to those of the master lease. The monthly transactions are recorded essentially as follows:

Financing vehicles – public debt

46. Some of the public debt was raised by entities created as financing vehicles. Quebecor World Capital II GP (“QWC2GP”) and Quebecor World Capital Corporation (“QWCC”) are examples of such vehicles.

47. In the case of QWC2GP, the structure is the result of a modification made in December 2007. The resulting effect of the modification is that amounts are due by Quebecor World Capital II LLC (“QWC2LLC”) to QWC2GP, and amounts are, in turn, owed to QWC2LLC by QWUSA, Quebecor World RAI Inc. (“QWRAI”) and Quebecor Printing Holding Company (“QPHC”), the U.S. holding corporation and parent company of QWUSA. The transaction can be described essentially as follows:

We point out that in the above diagram, the transfers of cash occurred between Quebecor World Capital LLC (“QWCLLC”), a predecessor entity in the transaction before the modification made in December 2007. The transfers of cash between QWCLLC and QPHC and QWRAI are only notional, in view of the cash pooling system.

48. In the case of QWCC, the amounts are owed by QWUSA and the transactions can be described as follows:

QWUSA QWCC cash

Interco loan

Non interest bearing note

QWC2LLC QPHC QWC2GP

QWUSA

Loans/notes

Cash / notes

QWRAI

QWLGP Operating entity Sublease

Interco amount

Outside third party

Cash

Master Lease

QWUSA

Cash Interco amount

Page 15

49. The above represents an outline of the types of transactions that occur in the context of the issuance of public debt. The financing transactions that apply to the debt presently outstanding are described in greater detail in this Report, under the heading “analysis of the use of proceeds from senior notes”.

INTERNAL DEBT STRUCTURE

50. The current financing structure involves QWICE, a corporation in Iceland that makes loans and advances to the various entities in QWG based on financing needs. This structure was put in place in February 2001, through an initial capital contribution of $125 million from QWI. This capital contribution was contemporaneous with an issuance of preferred shares (series 4) by QWI which yielded proceeds of CDN$200 million (approximately $130 million).

51. The funds received by QWICE from said initial capitalization were loaned to various entities in the U.S.

52. Additional transfers of funds by QWI were made to capitalize QWICE during 2001, the most significant of which is represented by a series of transactions between October and December 2001, by which:

52.1. QWUSA borrowed monies externally.

52.2. Some of the U.S. entities, namely QWUSA and QPHC, were de-capitalized through dividends, resulting in an aggregate dividend payment of $1 billion to QWI.

52.3. A portion of the funds received by QWI through the dividend, or approximately $850 million thereof, was used to capitalize QWICE. The remainder of the $1 billion dividend was used to repay $118 million in external debt owing by QWI and for general corporate purposes.

52.4. QWICE then made loans and advances to various operating entities and to QPHC in the U.S.

52.5. The funds borrowed by QPHC from QWICE were used to re-capitalize QWUSA, and these funds were then used to repay the monies that had been borrowed from external sources.

53. In all, approximately $1.3 billion was transferred to QWICE to capitalize it in 2001, and these funds were loaned to the various entities in QWG. The loan portfolio of QWICE as at December 31, 2001 indicates loans totalling $1.3 billion, as follows:

$000'sQPHC 652,000 QWUSA 247,376 QWSI 91,000 U.S. operating entities 327,393

1,317,769

Page 16

54. We understand that the funds that were made available for loans and advances for the QWG are limited to the funds from this initial capitalization of $1.3 billion in 2001, plus the interest earned by QWICE on the loans and advances, less an amount of approximately $250 million withdrawn by QWI in December 2006 through a de-capitalization of QWICE.

55. Over time, the funds from the initial capitalization and interest thereon were redistributed amongst QWG based on the financing needs of the individual operating entities.

56. The loan portfolio of QWICE at December 31, 2007 can be summarized as follows:

Loan Total amountQPHC 250,000 251,889 QWUSA 50,000 50,338 QWSI 105,985 106,709 European entities 285,878 290,499 U.S. operating entities 507,780 511,092

1,199,643 1,210,527

$000's

57. The internal debt structure currently in place is not the first time QWG sets up such a structure. We were informed that a similar structure had been put in place previously through an entity incorporated in Ireland, QPI Financial Services Inc. (“QPI”) (a wholly-owned subsidiary of QWI), but that structure was abandoned. There still exists a large inter-company loan of approximately CDN$1.3 billion payable by QWI to QPI as a remnant of that financing structure. We understand that although QPI was incorporated in Ireland, it is now a corporation resident in Canada for tax purposes.

58. We are informed that neither QWICE nor QPI has any external debt.

59. In addition to the internal financing structure through QWICE and the former structure through QPI, the Companies have an internal financing structure through the Swiss branch of QWSA that was used to provide funding to some of the European operating entities. This structure is no longer used as a financing structure as a result of the sale of the European operations referred to in paragraph 10 above.

INTER-COMPANY DEBT

60. Appendix B is a schedule that outlines, in the form of a matrix, the inter-company debt as at December 31, 2007, by category of entities, isolating the more significant entities which act as a cornerstone for the inter-company transactions21.

61. To visualize the flow of inter-company debt, a chart presenting information extracted from the above-mentioned schedule is attached as Appendix C. The information is essentially the same as that presented in the matrix (Appendix B), shown in a flow chart format, although inter-company amounts of less than $20 million have been omitted, to avoid clutter.

21 See the comments at note 5 above.

Page 17

62. We have been unable to obtain complete and updated information on the inter-company balances as at January 20, 2008. In our discussions with representatives of the Companies’ accounting group, we were informed that due to limitations in the Companies’ information systems, the only information that could be generated would consist of a pro-rata calculation between the inter-company balances as at December 31, 2007 and those as at January 31, 2008. This might be a fair basis of estimating on-going transactions such as sales and purchases, but would yield questionable results with respect to punctual transactions such as transfers of equipment or transfers of cash or the transaction by which the securitization program was terminated. In view of the foregoing, we consider that it is impractical to try and compile information as at January 20, 2008.

TRACKING INTER-COMPANY TRANSACTIONS

63. Since the inception of the Proceedings on January 21, 2008, the operations of QWG have been carried out substantially on the same basis as they had been before, subject to the reporting obligations pursuant to the Orders and the DIP Financing agreement. As mentioned in the description of the nature of transactions in paragraphs 13 to 48 of this Report, substantially all transactions, whether between the members of QWG or with an outside third party, trigger an inter-company transaction.

64. In essence, the high level of interrelation between the various entities and the volume of transactions make it difficult, if not impossible, to track the transactions between the affiliates on a transaction by transaction basis, and it is therefore necessary to monitor the inter-company transactions from a broader perspective of investigating changes in inter-company account balances after the fact, if these are considered significant.

65. In an effort to limit their impact, the employees have been sensitized to the problem of inter-company transfers or transactions and have been asked to be vigilant and to consult extensively with the Monitor and with the Companies’ legal counsel where a transaction is identified that could have an impact on inter-company balances, to assess whether the transaction is permissible and to seek authorization for the transaction, as the case may be.

66. A model was developed to extract information from the Companies’ systems in order to calculate the month to month changes in the inter-company balances. The model provides information that should help the Companies’ personnel identify, track and investigate large changes in inter-company balances.

67. Appendix D and E outline the inter-company debt as at January 31 and February 29, 2008 and the reported changes from month to month, from December 31, 2007 to February 29, 200822. This information is presented in the same format as that of the Appendix referred to in paragraph 60.

22 See the comments at note 5 above.

Page 18

ANALYSIS OF THE USE OF PROCEEDS FROM SENIOR NOTES

Senior notes due in 2008 and 2013

68. The Company issued senior notes in March 2004 (“2008-13 Notes”), comprised of the following:

Due date Rate $000'sNovember 15, 2008 4.875% 200,000 November 15, 2013 6.125% 400,000

600,000

69. The 2008-13 Notes were issued by QWCC as issuer, and are guaranteed by QWI.

70. The 2008-13 Notes were issued under a final prospectus dated January 28, 2004. The 2008-13 Notes did not generate cash proceeds, but were issued merely to exchange notes issued in November 2003 as a private placement with essentially identical notes registered under the Securities Act23 and freely tradable by persons not affiliated with QWI.

71. The notes replaced by these 2008-13 Notes were issued in November 2003 through a private placement under a confidential offering memorandum. Upon receipt of the funds in November 2003, these funds were transferred by QWCC to QWUSA through the issuance of notes that mirror the characteristics of the notes issued by QWCC24.

72. The issuance of the private notes in November 2003 generated proceeds of $593 million.

73. Following the issuance of the 2008-13 Notes, the following debt was retired:

Due date Rate Face value Call PriceNovember 15, 2008 8.375% 258,000 268,000 February 15, 2009 7.750% 300,000 312,000

558,000 580,000

$000's

74. According to the information presented in the Company’s financial statements, the retired debt had originally been issued by World Color Press, prior to its acquisition by the Company in 1999.

23 U.S. Code, Title 15, chapter 2A. 24 We point out that while “mirror” notes exist in an amount of $600 million, as a note issued by QWUSA to

QWCC to mirror the characteristics of the debt due by QWCC to external noteholders, the records of the Companies do not reflect that exact amount as the inter-company amount due from QWUSA to QWCC, in view of previous transactions, notes relating to the senior debentures due in 2027 (addressed in a subsequent section of this Report), grid notes, etc. The amount presented as due from QWUSA as at December 31, 2007 is $642 million.

Page 19

75. The stated intention was to benefit from lower interest rates. The early redemption of the notes and the issuance of the private placement were approved by a resolution of the Board of Directors of QWI on October 23, 2003.

76. The redemption amount for the retired debt was paid by wire transfers made primarily on November 12 and December 3, 2003. A small portion of the notes were redeemed in February, 2004.

Senior notes due in 2015

77. In December 2006 the Company issued $400 million of 9.75% notes due January 15, 2015 (“2015 Notes”). The 2015 Notes were issued by QWI and are guaranteed by QWUSA, QWCLLC and Quebecor World Capital ULC (“QWCULC”). The 2015 Notes were issued by way of private placement under a confidential offering memorandum dated December 13, 2006.

78. Some of the guarantors were replaced in December 2007, further to internal financing restructuring.

79. Based on the information presented to us, the internal financing restructuring did not involve any transfer of funds. The net effect of the transactions through which the internal financing was restructured, was that QWC2GP became a guarantor of the obligations of QWI under the 2015 Notes (due to the liquidation of QWCULC into QWC2GP), and QWC2LLC became a guarantor of the obligations of QWI under the 2015 Notes (due to the liquidation of QWCLLC into QWC2GP, and after the creation of QWC2LLC, a transfer to QWC2LLC of the assets and an assumption of the liabilities previously attributable to QWCLLC).

80. The stated projected use of the proceeds in the offering memorandum was to repurchase up to $125 million of senior notes, to repay in full $150 million of the 7.75% senior debentures due in January 2007, to repay borrowings under the credit facility and to use the remainder for general corporate purposes.

81. The Companies entered into a series of separate transactions contemporaneously with the issuance of the 2015 Notes which extended over a period of several days in late December 2006. The financial transactions included (not necessarily in this order)25:

81.1. The issuance of the 2015 Notes, generating net proceeds of approximately $393 million.

81.2. Additional borrowings of approximately $416 million on a short term basis.

81.3. A series of transfers of funds of $150 million, through QPHC, then through QWUSA, and ultimately a transfer of $155 million to QWCC. The transfers of funds from QWI to QPHC and to QWUSA consisted of capitalization transactions and the transfer from QWUSA to QWCC was a loan repayment.

25 We are advised by representatives of the Companies that the transactions represent separate transactions and

should not be considered necessarily as being a consequence of one another, or that the funds used in a transaction were provided by another transaction.

Page 20

81.4. Funds were then used by QWCC to repay approximately $155 million in senior debentures (i.e. $150 million in capital plus accrued interest of approximately $5 million) that had been issued by QWCC. These were 7.25% senior debentures due in January 2007.

81.5. A transfer of funds from QWI to QWICE of approximately $266 million, to repay a loan of CDN$308 million.

81.6. Transfers of funds totalling $257 million from QWICE to QWI, to de-capitalize QWICE.

81.7. A transfer of funds from QWICE to QWSA and then subsequently to Helio Charleroi S.A., (“Helio”), an affiliate in Belgium, of approximately €12 million (or $16 million) to fund capital expenditure requirements.

81.8. A repayment of short term borrowings of approximately $500 million.

82. In summary, the series of transactions had the following effect: a new issuance of debt comprised of the 2015 Notes, for $400 million, the capitalization of QPHC and QWUSA, by $150 million, the early repayment of the internal debt of QWUSA and of the external debt of QWCC, for $150 million in capital plus accrued interest, the recapitalization of QWICE with approximately $257 million, funding for Helio of approximately $16 million, a repayment of the borrowings under the credit facility for approximately $85 million, and approximately $145 million in cash flow. The early repayment of the external debt (by 17 days) was to provide an improvement in the debt to equity ratio covenant.

Senior notes due in 2016

83. In March 2006 the Company issued $450 million of 8.75% notes due March 15, 2016 (“2016 Notes”). The 2016 Notes were issued by QWCULC and are guaranteed by QWI, QWUSA and QWCLLC. The 2016 Notes were issued by way of a private placement under a confidential offering memorandum dated March 1, 2006. The net proceeds generated by the issuance of the 2016 Notes totalled approximately $443.8 million.

84. The stated projected use of the proceeds, in the confidential offering memorandum, was to repay in full the 7.20% senior notes due March 28, 2006, in the principal amount of $250 million, and for general corporate purposes.

85. The funds generated through the issuance of the 2016 Notes in December 2006 were intended to be channelled through an efficient internal financing structure. To put in place the structure, the funds were transferred through a combination of loans and advances and capitalizations, from QWCULC to QWC2GP, then to QWCLLC, and then to QPHC and QWUSA.

86. This structure was amended in December 2007. The modification to this internal financing structure is the same as that described in paragraphs 78 and 79 of this Report. As mentioned in paragraph 79, this change did not involve any transfer of funds.

Page 21

87. The Companies entered into a series of separate transactions contemporaneously with the issuance of the 2016 Notes, the end result of which can be summarized as follows (not necessarily in this order)26:

87.1. The funds were raised through the issuance of the 2016 Notes, generating proceeds of approximately $443.8 million.

87.2. An equivalent amount was transferred from QWCULC to QWC2GP as a loan.

87.3. An equivalent amount, together with an amount equivalent to a capital contribution of $50 million that had been made primarily by QWI to capitalize QWC2GP, was then transferred to QWCLLC as a capital contribution.

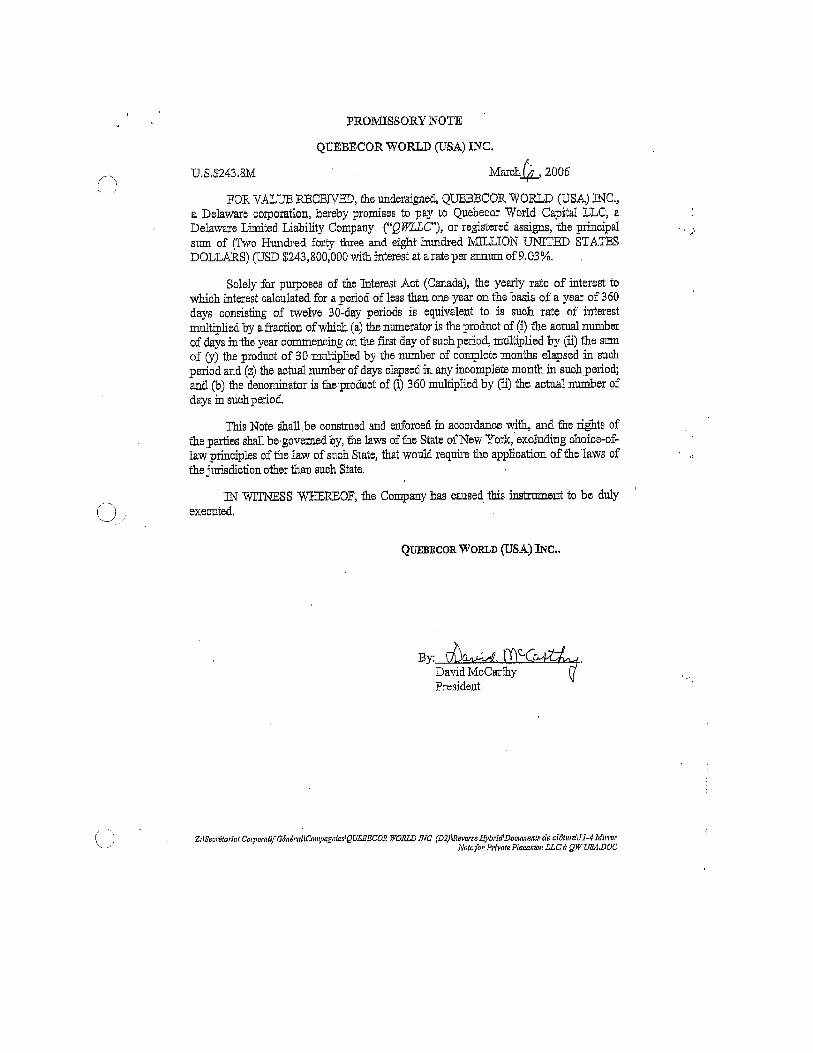

87.4. Funds were then loaned to QPHC ($250 million)27 and to QWUSA ($243.8 million)28. The notes issued to QWCLLC by QPHC and QWUSA as evidence of the debt are attached as Appendix G.

87.5. QWUSA transferred funds to QWCC to repay a loan of $250 million owing by QWUSA to QWCC.

87.6. QWCC repaid the maturing 7.20% senior notes that had been issued in March 2001.

87.7. The remainder of the funds were used as working capital, although funds transited through QWICE and triggered a series of inter-company transactions (consisting in part of loans and in part of capitalizations), before being returned in part by QWICE by way of a loan to QWI ($230 million) and in part by a transfer from the Fribourg branch of QWI to QWI ($20 million).

Senior debentures due in 2027

88. In 1997 the Company issued $150 million of 6.5% debentures due August 1, 2027 (“2027 Notes”). The 2027 Notes were issued by Quebecor Printing Capital Corporation (now QWCC) and are guaranteed by Quebecor Printing Inc. (now QWI). The 2027 Notes were issued under a prospectus dated January 15, 1997 and a supplementary prospectus dated July 29, 1997. The net proceeds generated by the issuance of these 2027 Notes totalled approximately $148.6 million.

89. The stated projected use of the proceeds in the prospectus was to repay a portion of the indebtedness under the revolving bank credit facilities.

90. The 2027 Notes were redeemable at the option of the noteholder at par on August 1, 2004. Most of the noteholders tendered their notes for redemption, and the balance outstanding of these notes is $3.2 million.29

26 See note 25 above. 27 As mentioned earlier in this Report, the transfer of funds to QPHC is notional only, in view of the cash pool

arrangements.

Page 22

EXTERNAL DEBT STRUCTURE

91. Appendix F outlines the external debt structure of the Companies in respect of credit facility with the banking syndicate, the equipment financing facility with Société Générale (Canada) and the senior notes issued by the Companies and becoming due in 2008, 2013, 2015, 2016 and 2027.

REPAYMENT OF PRIVATE NOTES IN OCTOBER 2007

Private notes issued on July 15, 2000

July 2000 transactions

92. The Company issued private notes in 2000, comprised of the following:

Series Due date Rate US$000'sA July 15, 2010 8.42% 175,000 B July 15, 2012 8.52% 75,000 C September 15, 2015 8.54% 91,000 D September 15, 2020 8.69% 30,000

371,000

93. The notes were issued by QWCC and upon receipt these funds were transferred to Quebecor World Capital GP (“QWCGP”) through the issuance of notes that mirror the characteristics of the notes issued by QWCC. The funds were then re-transferred amongst some of the Companies in a series of loans and/or loan repayment transactions, with the funds eventually being advanced to Quebecor Printing (U.S.A.) Holdings Inc. (now QWUSA) as part of the cash pool arrangements.

94. The notes were issued by QWCC based on two Note Purchase Agreements dated July 12, 2000 and September 12, 2000 respectively. Under the Note Purchase Agreements, the notes were issued by QWCC and are guaranteed by QWI and by QWUSA.

November 2003 transactions

95. The issuance of mirror notes by QWCGP in 2000 and the series of contemporaneous transactions among some of the Companies through a series of loans and/or loan repayments, until the funds were ultimately transferred to QWUSA, represented the set-up of an internal financing structure.

96. This structure was unwound in November 2003. The manner in which it was unwound was as follows: Essentially, funds circulated from QWUSA, through some of the Companies, through QWCGP, and finally to QWCC in repayment of the mirror notes, which were then cancelled.

28 In a separate contemporaneous transaction, an advance of $6.7 million was made by QWCLLC to QWRAI,

through the same financing structure. 29 See the comments at note 24.

Page 23

The funds were then re-transferred by QWCC to QWUSA by way of a loan, for which QWUSA issued new notes payable to QWCC, also referred to as “mirror notes”, on terms substantially the same as the old mirror notes.

97. This transaction in November 2003 did not affect the notes issued to the noteholders, but only affected the internal debt structure of the Companies by reallocating loans and advances amongst the affiliates as a result of the internal financing restructuring.

Balance outstanding in October 2007

98. The Note Purchase Agreements provide for the possibility of repurchasing the notes before their maturity date by payment of a redemption amount represented by the principal amount, accrued interest and an applicable “Make Whole” payment. The audited financial statements for fiscal 2006 indicate that a portion of the notes were redeemed on December 29, 2006, as follows:

Series Due date RateIssued Redeemed Balance

A July 15, 2010 8.42% 175,000 3,500 171,500 B July 15, 2012 8.52% 75,000 15,000 60,000 C September 15, 2015 8.54% 91,000 36,000 55,000 D September 15, 2020 8.69% 30,000 - 30,000

371,000 54,500 316,500

US$000's

Note repayment in October 2007

99. On September 27, 2007, pursuant to a resolution of the Board of Directors of QWI, a decision was made to redeem the remaining outstanding series A, B, C and D notes on October 29, 2007.

100. The certificate issued to the noteholders indicates that the aggregate redemption amount was $376 million. Notwithstanding the fact that the notes were issued by QWCC, the payment of the redemption amount was made by QWUSA. The documented agreements between QWCC and QWUSA regarding the re-purchase and redemption of the notes are represented by an agreement dated September 28, 2007 and a letter dated October 29, 2007, through which QWCC transfers to QWUSA the rights and obligations relating to the redemption of the notes, QWUSA acquires the notes for an amount equivalent to the redemption amount, and QWUSA surrenders the notes to QWCC for cancellation, in consideration of the cancellation of an equivalent debt due by QWUSA to QWCC.

101. We understand that the equivalent debt is represented by the “mirror” notes that had been issued by QWUSA in December 2003.

102. Notwithstanding the fact that the documentation appended to the Note Purchase Agreements specifies a distinct separate banking information for each of the noteholders as the payment routing instruction, the redemption amount was paid as a single payment to CIBC Mellon as a result of an agreement through which CIBC Mellon acts as Registrar, Transfer Agent and Paying Agent for this debt issue.

Page 24

103. The redemption amount was paid by a single wire transfer of $376 million paid to CIBC Mellon Trust Company on October 29, 2007.

Source of funds

104. The Companies did not issue new debt to refinance the October 2007 note repayment described above, but decided to use the funds made available under their operating line of credit with the banking syndicate.

105. The request for a draw under the credit facility to pay the redemption amount was effected by letters to the Royal Bank of Canada (the administrative agent for the banking syndicate) (“RBC”) dated August 31, September 14 and September 19, 2007.

106. The credit agreement between the Companies and the banking syndicate contained restrictions as to the use of funds. In September 2007, section 3.6 of the credit agreement provided that:

3.6 Purposes of Advances

The Credit Facilities shall be used by the Borrowers for general corporate purposes, including, without limitation, ongoing working capital and operations requirements, commercial paper back-up and, subject to the terms and conditions hereof, to provide funding for Acquisitions, Investments and capital expenditures. No Swingline Loan shall be used to refinance any outstanding Swingline Loan.

107. The credit agreement was modified in October 2007 and section 3.6 was modified as follows to allow the note repayment under certain terms and conditions described below:

3.6 Purposes of Advances

The Credit Facilities shall be used by the Borrowers for general corporate purposes, including, without limitation, ongoing working capital and operations requirements, commercial paper back-up and, subject to the terms and conditions hereof, to provide funding for Acquisitions, Investments and capital expenditures, but excluding for the purposes of financing any share redemption (including, without limitation, redemption of QWI’s Series 5 Cumulative Redeemable First Preferred Shares) or for the purposes of financing any principal repayments of Indebtedness (other than scheduled instalments, the payments owed at scheduled and unscheduled maturity up to an aggregate amount of US$50,000,000 or the redemption in full of the Private Notes).

Notwithstanding the foregoing, until such time as the Private Notes have been redeemed in full, (i) the Credit Facilities may be used for any of the purposes described in the preceding paragraph up to a maximum amount of US$400,000,000; and (ii) the initial Borrowing under the Credit Facilities in excess of US$400,000,000 shall be used solely for the purpose of Borrowings to be used exclusively for the proposed redemption, in full, of the Private Notes.

108. The modification described above, together with the contemporaneous waivers of the financial ratio covenants under the syndicated credit agreement and a cross-default under the private notes, allowed a draw under the credit facility for the purpose of paying the redemption amount of the private notes. The draw under the credit facility occurred on October 29, 2007.

Page 25

109. The amount drawn under the RBC credit facility increased from $132.5 million as of October 28, 2007 to a peak level of $726.9 million as of January 1, 2008, and then decreased slightly to $676.3 million as of January 20, 2008.

110. As part of the modifications to and the waivers under the credit agreement, QWI undertook the following:

110.1. To provide a guarantee of the indebtedness by each of the North American subsidiaries (except for few specific entities and entities considered to have a negligible amount of operating assets and EBITDA).

110.2. To provide security by way of a pledge of the shares held by The Webb Company and QWUSA in QW Memphis Corp.

110.3. To provide security by way of a pledge of the shares held by QPHC in QWUSA.

110.4. To provide security by way of first ranking security interest in the personal and real property of QW Memphis Corp. (other than the accounts receivable that may be subject to the North American Securitization Program, and a specific parcel of real property located in Covington, TN).

110.5. To provide security by way of a first ranking security interest over all inventories of QWI and its subsidiaries in North America.

110.6. To reduce the aggregate commitment of the bank syndicate to $750 million as of October 1, 2007 and $500 million as of July 1, 2008 (the latter having become moot as a result of the Proceedings).

111. We understand that the guarantees and security agreements referred to in paragraphs 110.1 to 110.4 were executed, as well as the security interest over the inventory of QWI. However, the security interest in the inventories of the North American subsidiaries (other than QW Memphis Corp) was not executed and delivered. While QWG undertook to provide this security by the end of March 2008, these Proceedings intervened.

112. The credit agreement between QWI, QWUSA and Société Générale (Canada) provides that Société Générale (Canada) is to benefit from guarantees and security similar to those granted to the banking syndicate, on a pari passu basis, and, accordingly, similar security and guarantees were also provided to Société Générale (Canada).

113. By virtue of the security agreements, the security is limited in aggregate to an amount of $170 million (other than expenses and interest as expressly provided for in paragraph 39 of the Initial Order). The security is for the benefit of the banking syndicate and for the benefit of Société Générale (Canada) and is subject to a pari passu sharing agreement. Limitations on the amount of security or secured obligations were required in order to comply with restrictions on granting liens contained in certain senior notes and debentures described above, at the time the agreements were executed.

Page 26

OVERALL COMMENTS AND CONCLUSION

114. The present Report addresses the matters referred in paragraphs 63.1, 63.3 to 63.6 and 63.8 of the Second Report of the Monitor, dated February 14, 2008. Barring a request by the Court for additional information or clarification of the matters addressed herein, the Monitor considers the work, as it relates to that portion of the information requests on inter-company transactions and balances, as completed.

All of which is respectfully submitted this 21st day of July 2008.

ERNST & YOUNG INC. In its capacity as the Monitor appointed by the Court in the matter of the proposed arrangement of Quebecor World Inc. et al.

Per: Murray A. McDonald, CA, CIRP President

H:\Clients\CorpFin\Q\Quebecor World Restructuring -QWI\22-01 Reports-Rapports\11th report - Report on Intercos\QWI - Report on Interco tx Jul21 08 final.doc

IN THE MATTER OF THE COMPANIES’ CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED

AND IN THE MATTER OF A PLAN OF COMPROMISE OR ARRANGEMENT OF

QUEBECOR WORLD INC. ET AL

U.S. SUBSIDIARIES INCLUDED IN THE CCAA PROCEEDINGS

SCHEDULE “A”

Quebecor Printing Aviation Inc. Quebecor Printing Holding Company Quebecor World (USA) Inc. Quebecor World Arcata Corp. Quebecor World Atglen Inc. Quebecor World Atlanta II LLC Quebecor World Book Services LLC Quebecor World Buffalo Inc. Quebecor World Capital Corporation Quebecor World Capital II GP Quebecor World Capital II LLC Quebecor World Century Graphics Corporation Quebecor World Dallas II Inc. Quebecor World Dallas, L.P. Quebecor World DB Acquisition Corp. Quebecor World Dittler Brothers Inc. Quebecor World Dubuque Inc. Quebecor World Eusey Press Inc. Quebecor World Fairfield Inc. Quebecor World Great Western Publishing Inc. Quebecor World Hazleton Inc. Quebecor World Infiniti Graphics Inc. Quebecor World Johnson & Hardin Co. Quebecor World KRI Inc. Quebecor World Krueger Acquisition Corp. Quebecor World Lease GP Quebecor World Lease LLC

Quebecor World Lincoln Inc. Quebecor World Logistics Inc. Quebecor World Loveland Inc. Quebecor World Magna Graphic Inc. Quebecor World Memphis LLC Quebecor World Mid-South Press Corporation Quebecor World Mt. Morris II LLC Quebecor World Nevada II LLC Quebecor World Nevada Inc. Quebecor World Northeast Graphics Inc. Quebecor World Olive Branch Inc. Quebecor World Pendell Inc. Quebecor World Petty Printing Inc. Quebecor World Printing (USA) Corp. Quebecor World Rai Inc. Quebecor World Retail Printing Corporation Quebecor World San Jose Inc. Quebecor World Systems Inc. Quebecor World Taconic Holdings Inc. Quebecor World Up / Graphics Inc. Quebecor World Waukee Inc. QW Memphis Corp. QW New York Corp. The Webb Company WCP-D, Inc. WCZ, LLC