by jeffrey n. barnes, cpa, macc oral defense slides in partial fulfillment

DESCRIPTION

Organizational Leadership and Ethical Climate in Utah’s Certified Public Accounting Profession (20-minute Presentation Slides). by Jeffrey N. Barnes, CPA, MAcc Oral Defense Slides in Partial Fulfillment of Requirements for the Degree Doctor of Business Administration - PowerPoint PPT PresentationTRANSCRIPT

Organizational Leadership and Ethical Climate in Utah’s

Certified Public Accounting Profession(20-minute Presentation Slides)

byJeffrey N. Barnes, CPA, MAcc

Oral Defense Slides in Partial Fulfillment of Requirements for the Degree

Doctor of Business Administration

UNIVERSITY OF PHOENIX

February 2013

Chapter 1, Introduction

• CPAs are critically involved with assuring fair presentation of financial statements.

• Fraudulent financial reporting continues (Arens, Elder, & Beasley, 2012; Apostolou & Crumbley, 2007).

• Foundations of fraudulent behavior are rooted in sociological, psychological, and moral-development theories (Albrecht, Romney, Cherrington & Roe, 1982).

Chapter 1, IntroductionSignificance of the Problem

• Accounting profession to benefit from the study by,

– understanding current state of organizational leadership,– finding confirmatory or disconfirmatory evidence that

leadership correlates to ethical perceptions, – determining if religiosity and regulatory influence relate to

leadership and ethical climate perceptions, and– designing leadership training interventions.

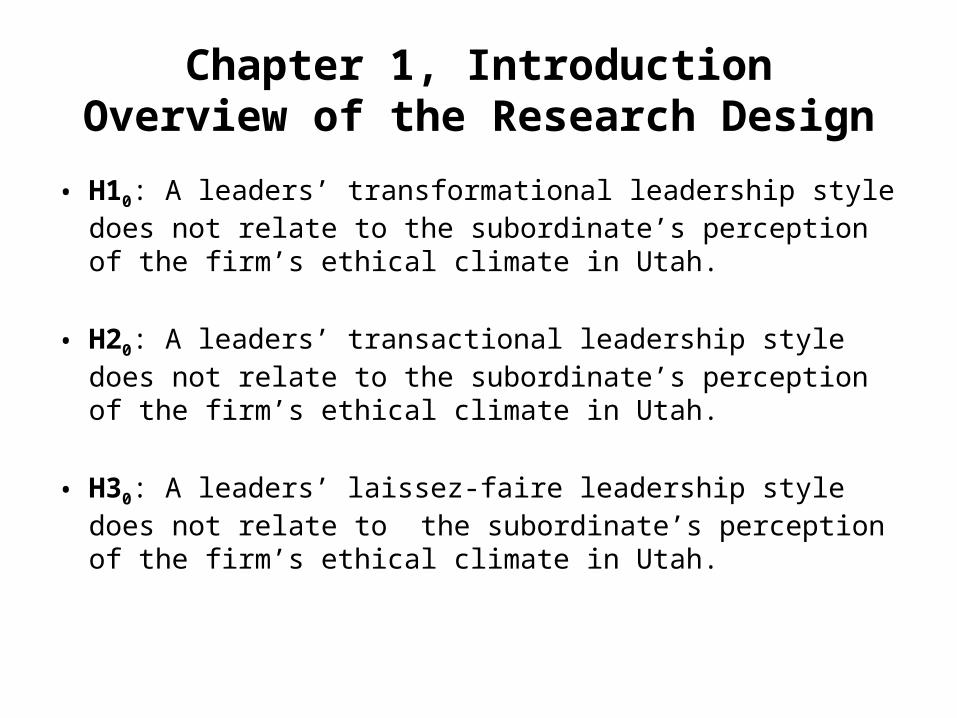

Chapter 1, IntroductionOverview of the Research Design

• H10: A leaders’ transformational leadership style does not relate to the subordinate’s perception of the firm’s ethical climate in Utah.

• H20: A leaders’ transactional leadership style does not relate to the subordinate’s perception of the firm’s ethical climate in Utah.

• H30: A leaders’ laissez-faire leadership style does not relate to the subordinate’s perception of the firm’s ethical climate in Utah.

Chapter 1, IntroductionOverview of the Research Design

• H40: Known exogenous regulatory/punishment factors, as perceived by subordinates, do not relate to the subordinate’s perception of the firm’s ethical climate and immediate leadership in Utah.

• H50: The degree of service or church attendance does not relate to the subordinates’ perception of the firm’s ethical climate and immediate leadership in Utah.

• Alternate hypotheses, for each of the null hypotheses, suggest that relationships exists

Chapter 1, IntroductionOverview of the Research Design

Chapter 2, Review of LiteratureIntroduction

• The current study,

– explains previous research related to leadership and ethical climate, which is sparse in the accounting profession,

– provides secondary evidence regarding regulatory controlling subordinate effect, and

– provides secondary evidence regarding the nascent emerging positive subordinate effects of religiosity.

Chapter 2, Review of LiteratureDocumentation

Category of Documentation Number Percentage

2006 to present 123 44.2%

Prior 2006 154 55.8%

All references 277 100.0%

Founding or extending theorists 41 14.8%

Empirical research 83 30.0%

Peer-reviewed articles 198 71.5%

Books 57 20.6%

Dissertations/unpublished research 4 1.4%

Official websites 18 6.5%

Chapter 2, Review of LiteratureSummary

• Both the lack of empirical research into the public accounting profession and the possible insights correlative influence these two moderating variables could provide and substantiate the additional needed empirical studies regarding the current state of accounting firms’ ethical climate structure and the prevailing leadership style typically exhibited.

Chapter 2, Review of LiteratureSummary

• An organization’s ethical climate, is founded on the collective foundation of it individuals moral and ethics philosophies. These moral and ethical philosophies are related to the five empirically derived ethical climate types found within organizations.

• Organizational leadership shapes and is shaped by the organization’s ethical climate. Potentially affecting the public accountants’ perceptions of organizational leadership and ethical climate are two potential moderating variables, which are awareness of regulatory statutes and personal religiosity, respectively.

Chapter 3: MethodTheoretical Model Design

Known Exogenous Regulatory/Punishment

Factors(MV: H4)

1 FSGO Scale

(FSGO Survey, 12 Questions)

Subordinates' Perception of

5 Ethical Climate Scales(DV)

(ECQ Survey, 26 Questions)

Extent of Religiosity/Compassionate

Service(MV: H5)

1 Scale

(REL Survey, 4 Questions)

Superiors'Leadership Style(IV: H1, H2, H3)

9 Leadership Scales

(MLQ Survey, 45 Questions)

Legend:

DV Dependent VariableIV Independent VariableMV Moderating (Intervening) VariableH Hypothesis

Figure 2. Statistical Integrated Leadership & Ethical Climate Framework

H1, H2, H3

H4 H4

H5 H5

Chapter 3: MethodInstrumentation

• Four instruments were used in this research study, the

– Multifactor Leadership Questionnaire (MLQ), or standard MLQ, or also known as the MLQ 5X short, by Avolio and Bass (2004),

– Ethical Climate Questionnaire (ECQ), by Victor and Cullen (1987, 1988),

– Understanding of Federal Sentencing Guidelines for Organizations, by researcher (2012), and

– Religiosity, by researcher (2012).

Chapter 3: MethodPopulation

• In 2010, approximately 1,175 certified public accountants (CPAs), in the practice of public accounting, in the State of Utah and members of the Utah Association of Certified Public Accountants (UACPA, 2009).

• There were 469 separate physical CPA firm offices in Utah at the time of the study, many with below five CPAs. Of the 469 firms, only 41 firms with five or more CPAs exist (UACPA, 2009).

• 11 CPA firms provided written permission to contact organization personnel, via email, for the administration of the electronic survey of this research study.

Chapter 3: MethodData Collection (Cont.)

• The original request was sent on February 7, 2012, the second request was sent on February 18, 2012, and the third and last request was sent March 13, 2012.

• The 257 email addresses, at the time the survey was administered, there was provided 236 continuing valid prospective respondents. The reduction of 21 emails represented natural attrition from the firms. The number of survey participants was 103 from a target population of 236, providing a 43.6% response rate.

Chapter 3: MethodResearcher Error with ECQ Instrument (Cont.)

Proper Ethical Climate Questionnaire Scale and Scale Used in This Study Proper ECQ Measurement Scale

Measurement Scale of this Study

0—Completely false 1—Completely false 1—Mostly false 2—Mostly false 2—Somewhat false 3—Somewhat false 3—Somewhat true 4—Mostly true 4—Mostly true 5—Completely true 5—Completely true

Chapter 3: MethodResearcher Error with ECQ Instrument (Cont.)

• According to Bart Victor, Ph.D. (personal communication, August 2, 2012), who is one the originators of the Ethical Climate Questionnaire (Victor and Cullen, 1988), this study’s collected data would expect to still be meaningful. He provided the following guidance,

. . . the data collection need not be reperformed; to address the scale error in the ‘Methods’ section of the dissertation; to state that the existing data means, variances, and correlations are meaningful and reportable; to suggest that the scale errors do not cause a systemic or universal disqualifying error, because the recorded survey respondents’ impressions about the perceived ethical climate types are still valid; to not transform the data, thus, to use the existing data as is; and to check for similar intercorrelations and reliability.

Chapter 3: MethodCorrelation Analysis

Guilford Interpretation of the Magnitude of Significant Correlations

Absolute Value of Rho (r)

Interpretation

< .20 Slight, almost no relationship

.20 - .39 Low correlation, definite but small relationship

.40 – .69 Moderate correlation, substantial relationship

.70 – .89 High correlation, strong relationship

.90 – 1.00 Very high correlation, very dependable relationship Source: Van Aswegen & Engelbrecht, 2009, p. 5.

Chapter 3: MethodANOVA Analysis

• Prior to running the ANOVA analyses, assumptions for ANOVA were tested. The assumptions for normality were tested, which ascertain that the scores be normally distribution around the mean of the dependent variable. Histograms were developed for all the dependent variable ethical climate types.

• Also tested was the homogeneity of variance, which requires that the groups have equal variances in the population. Scatterplots of dependent variable’s various ethical climate types were constructed to determine the absence of heteroscedasticity. Both histograms and scatterplot tests were performed visually.

Chapter 3: MethodANOVA Analysis (Cont.)

• ANOVA analysis was performed for those correlative relationships with statistical significance. ANOVA or analysis of variance provided the F-crit statistic (F-test, F) , R2, and significance.

Chapter 3: MethodUnivariate Analysis

• Statistical analysis also treated the demographic categories, with sufficient subsample size, as independent variables.

• Running univariate analysis of variances between the demographic independent variable and the leadership independent variable to the ethical climate’s dependent variables was performed. Those relationships that demonstrated significant relationships were reported

Chapter 4: ResultsStatistical Analyses

• Findings for Hypothesis 1—Transformational Leadership’s Relationship to Ethical Climates

• Findings for Hypothesis 2—Transactional Leadership’s Relationships to Ethical Climates

• Findings for Hypothesis 3—Laissez-faire Leadership’s Relationships to Ethical Climates

• Findings for Hypothesis 4—Regulatory Influence Relationships to Leadership and Ethical Climates

• Findings for Hypothesis 5—Religiosity’s Relationships to Leadership and Ethical Climates

• Limited Cross-sectional Statistical Analysis• Post Hoc Power and Effect Size Analysis

Chapter 4: ResultsFindings for Hypothesis 1--Correlations

Transformational (IV)

Caring (DV)

Lawcode

(DV)

Rules (DV)

Instrumental

(DV)

Independence

(DV)

Pearson Correlation .411 .282 .402 -.525 .093 Significance (2-tailed), p-value .000** .004** .000** .000** .349 N 103 103 103 103 103

Chapter 4: ResultsFindings for Hypothesis 1--ANOVA

Model

Sum of Squares

df

Mean Square

F-test

R2

Sig.

Regression 28.873 1 28.873 8.718 .079 .004** Residual 334.486 101 3.312 Total 363.359 102

Model

Sum of Squares

df

Mean Square

F-test

R2

Sig.

Regression 187.525 1 187.525 20.550 .169 .000** Residual 921.678 101 9.126 Total 1109.204 102

Model

Sum of Squares

df

Mean Square

F-test

R2

Sig.

Regression 72.129 1 72.129 19.504 .162 .000** Residual 373.521 101 3.698 Total 445.650 102

Model

Sum of Squares

df

Mean

Square

F-test

R2

Sig.

Regression 648.221 1 648.221 38.361 .268 .000** Residual 1706.692 101 16.898 Total 2354.913 102

Transformation Leadership to Caring Ethical Climate

Transformation Leadership to Lawcode Ethical Climate

Transformation Leadership to Rules Ethical Climate

Transformation Leadership to Instrumental Ethical Climate

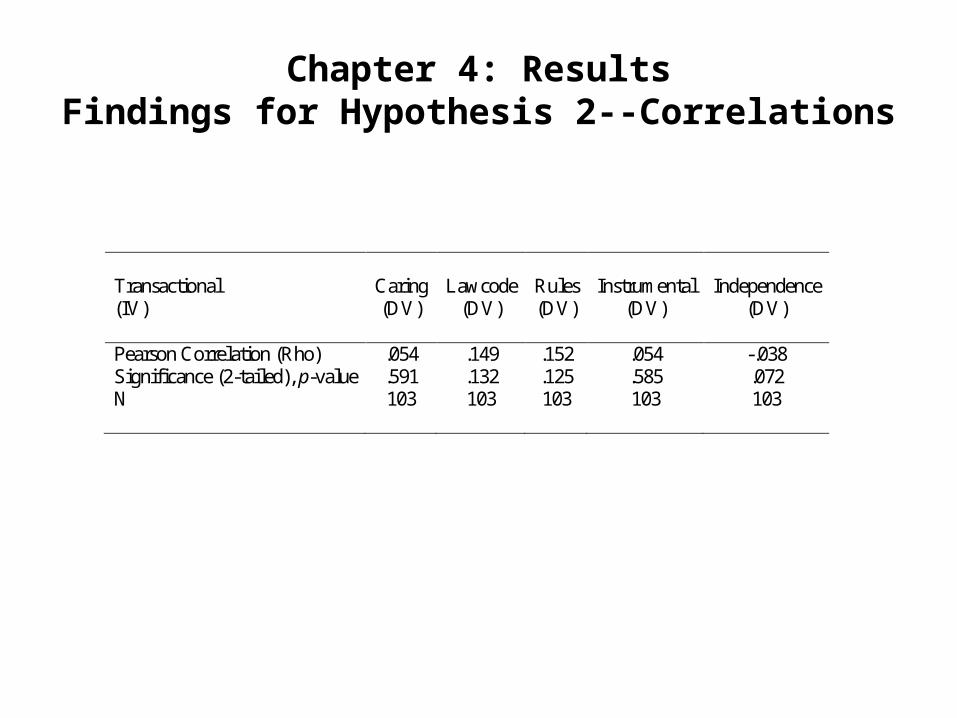

Chapter 4: ResultsFindings for Hypothesis 2--Correlations

Transactional (IV)

Caring (DV)

Lawcode

(DV)

Rules (DV)

Instrumental

(DV)

Independence

(DV)

Pearson Correlation (Rho) .054 .149 .152 .054 -.038 Significance (2-tailed), p-value .591 .132 .125 .585 .072 N 103 103 103 103 103

Chapter 4: ResultsFindings for Hypothesis 3--Correlations

Laissez-faire (IV)

Caring (DV)

Lawcode

(DV)

Rules (DV)

Instrumental

(DV)

Independence

(DV)

Pearson Correlation (Rho) -.073 -.143 -.237 .247 .010 Significance (2-tailed), p-value .462 .151 .016* .012* .919 N 103 103 103 103 103

Chapter 4: ResultsFindings for Hypothesis 3--ANOVA

Model

Sum of Squares

df

Mean Square

F-test

R2

Sig.

Regression 24.995 1 24.995 6.001 .056 .016* Residual 420.655 101 4.165 Total 445.650 102

Model

Sum of Squares

df

Mean Square

F-test

R2

Sig.

Regression 143.840 1 143.840 6.570 .061 .012* Residual 2211.073 101 21.892 Total 2354.913 102

Laissez-faire Leadership to Rules Ethical Climate

Laissez-faire Leadership to Instrumental Ethical Climate

Chapter 4: ResultsFindings for Hypothesis 4—Correlations

FSGO Understanding (IV)

Caring (DV)

Lawcode (DV)

Rules (DV)

Instrumental (DV)

Independence (DV)

Pearson Correlation -.002 .220 .165 -.284 .048 Significance, (2-tailed), p-value .990 .129 .257 .048* .742 N 49 49 49 49 49

Chapter 4: ResultsFindings for Hypothesis 5--Correlations

REL Religiosity (IV)

Caring (DV)

Lawcode

(DV)

Rules (DV)

Instrumental

(DV)

Independence

(DV)

Pearson Correlation (Rho) -.091 -.043 -.084 .021 -.110 Significance (2-tailed), p-value .363 .669 .401 .831 .268 N 103 103 103 103 103

Chapter 4: ResultsCross-sectional Analyses

• To understand the significant interaction between gender (or with

any other demographic independent variable), and transformational leadership (or any

other independent variable), on the caring ethical climate type perception (or

any other dependent variable), the transformational leadership (or any other independent

variable) was grouped into those scoring higher than one standard deviation (+1SD) and those scoring lower than one standard deviation (-1SD) and plotted with gender (or with any other demographic independent variable).

Chapter 4: ResultsLimited Cross-sectional Statistical Analysis

Gender/Transformational Leadership to Caring Ethical Climate

Category D2(Gender)

Frequency

Female (1) 29Male (2)Total

74103

Source

Type III Sum Of Squares

df

Mean Square

F

Sig.

Corrected Model 254.542a 3 84.847 9.828 .000 Intercept 1506.910 1 1506.910 174.553 .000 Gender (D2) 59.265 1 59.265 6.865 .010 Transformational 28.464 1 28.464 3.297 .072 Gender (D2) * Transformational

48.949

1

48.949

5.670

.019*

Error 854.662 99 8.633 Total 63303.000 103 Corrected Total 1109.204 102

Chapter 4: ResultsLimited Cross-sectional Statistical Analysis

(Cont.)

Service Function/Transformational Leadership to Lawcode Ethical Climate

Category D8(Service Function)

Frequency

Assurance (1) 61Tax (2)Total

3596

Source Type III Sum Of Squares

df

Mean Square

F

Sig.

Corrected Model 50.463 a 3 16.821 5.297 .002 Intercept 1348.360 1 1348.360 424.591 .000 Assurance and Tax (D8) 20.225 1 20.225 6.369 .013 Transformational 14.507 1 14.507 4.568 .035 Assurance and Tax (D8) * Transformational

16.339

1

16.339

5.145

.026*

Error 292.162 92 3.176 Total 30802.000 96 Corrected Total 342.625 95

Chapter 4: ResultsLimited Cross-sectional Statistical Analysis (Cont.)

Service Function/Transformational Leadership to Rules Ethical Climate

Category D8(Service Function)

Frequency

Assurance (1) 61Tax (2)Total

3596

Source

Type III Sum Of Squares

df

Mean

Square

F

Sig.

Corrected Model 89.824 a 3 29.941 8.524 .000 Intercept 1069.929 1 1069.929 304.592 .000 Assurance and Tax (D8) 26.019 1 26.019 7.407 .008 Transformational 35.826 1 35.826 10.199 .002 Assurance and Tax (D8) * Transformational Error Total Corrected Total

23.310

1

23.310

6.636

.012*

323.165 92 3.513 28191.000 96

412.990 95

Chapter 4: ResultsLimited Cross-sectional Statistical Analysis (Cont.)

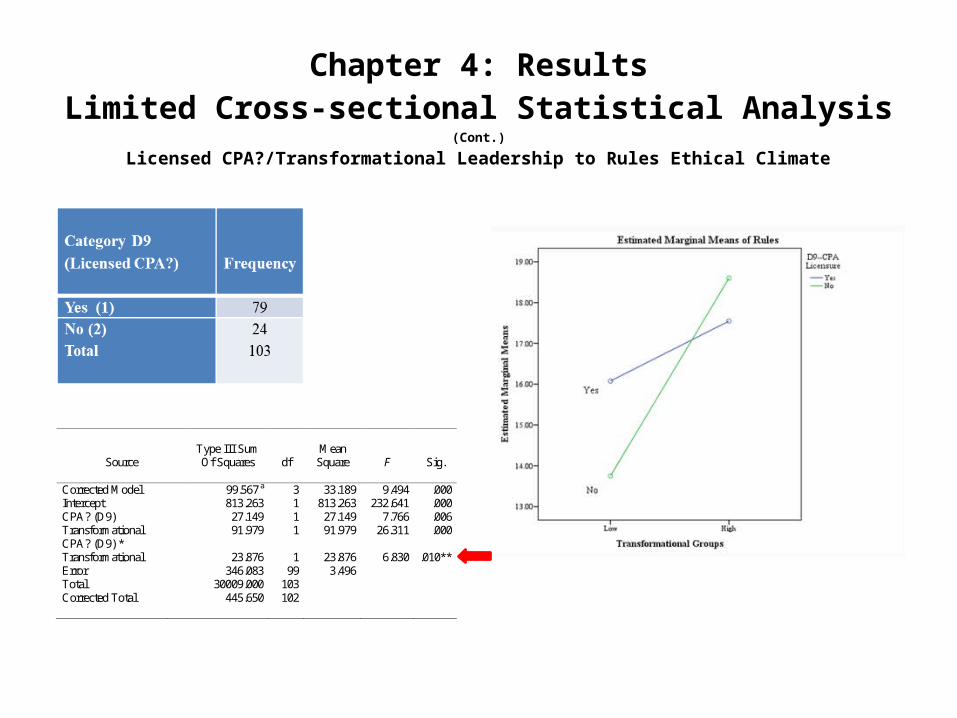

Licensed CPA?/Transformational Leadership to Rules Ethical Climate

Source

Type III Sum Of Squares

df

Mean

Square

F

Sig.

Corrected Model 99.567 a 3 33.189 9.494 .000 Intercept 813.263 1 813.263 232.641 .000 CPA? (D9) 27.149 1 27.149 7.766 .006 Transformational 91.979 1 91.979 26.311 .000 CPA? (D9) * Transformational

23.876

1

23.876

6.830

.010**

Error 346.083 99 3.496 Total 30009.000 103 Corrected Total 445.650 102

Chapter 4: ResultsLimited Cross-sectional Statistical Analysis (Cont.)

Firm Size/Transformational Leadership to Lawcode Ethical Climate

Category D11(Firm Size)

Frequency

Regional 32Local, large 25+ 50Local, small 20Total 102

Source

Type III Sum Of Squares

df

Mean Square

F

Sig.

Corrected Model 69.601 a 3 23.200 7.819 .000 Intercept 147.678 1 147.678 49.769 .000 Firm Size (D11) 6.100 1 6.100 2.056 .155 Transformational 23.938 1 23.938 8.067 .005 Firm Size (D11) * Transformational

13.106

1

13.106

4.417

.038*

Error 293.758 99 2.967 Total 33269.000 103 Corrected Total 363.359 102

Chapter 4: ResultsLimited Cross-sectional Statistical Analysis (Cont.)

Licensed CPA?/Transactional Leadership to Rules Ethical Climate

Source

Type III Sum Of Squares

df

Mean

Square

F

Sig.

Corrected Model 32.366 a 3 10.789 2.584 .058 Intercept 684.151 1 684.151 163.885 .000 Transactional 19.079 1 19.079 4.570 .035 CPA? (D9) 20.518 1 20.518 4.915 .029 CPA? (D9) * Transactional

17.359

1

17.359

4.158

.044*

Error 413.284 99 4.175 Total 30009.000 103 Corrected Total 445.650 102

Chapter 4: ResultsLimited Cross-sectional Statistical Analysis (Cont.)

Years with Firm/Lassiez-faire Leadership to Lawcode Ethical Climate

Category D7(Years with firm)

Frequency

0 – 2 183 – 45 – 1010+ years

273226

Total 103

Source

Type III Sum Of Squares

df

Mean

Square

F

Sig.

Corrected Model 66.219 a 7 9.460 3.024 .006 Intercept 5937.012 1 5937.012 1898.146 .000 LFL 4.082 1 4.082 1.305 .256 Time with Firm (D7) 40.450 3 13.483 4.311 .007 Time with Firm (D7) * LFL

38.792

3

12.931

4.134

.008**

Error 297.141 95 3.128 Total 33269.000 103 Corrected Total 363.359 102

Chapter 4: ResultsPost Hoc Power and Effect Size Analysis

Hypothesis

Alpha

P-value

df

Post

Hoc

Power

(eta2)

Effect

Size

H1, Transformational to Caring .05 .000** 102 .92 .53

H1, Transformation to Lawcode .05 .004* 102 .86 .54

H1, Transformation to Rules .05 .000** 102 .93 .56

H1, Transformation to Instrumental .05 .000** 102 .93 .56

H3, Laissez-faire to Rules .05 .016* 102 .71 .18

H3, Laissez-faire to Instrumental .05 .012* 102 .73 .17

H4, Understanding FSGO to Instrumental .05 .048* 48 .51 .33

Post Hoc Power and Effect Size Analysis

Chapter 5: Conclusions and RecommendationsFrequency Means of Leadership Recognized

Frequency Means of Leadership Style Recognized

Leadership Style

Mean

Std. Dev.

Transformational 2.53 0.626 Transactional 1.89 0.369 Laissez-faire 1.31 0.647

MLQ Frequency Key: 0.0 = Not at all, 1.0 – Once in a while,2.0 = Sometimes, 3.0 = Fairly often, and 4.0 = Frequently, if not always

Chapter 5: RecommendationsChange Leadership Behavior and Attributes

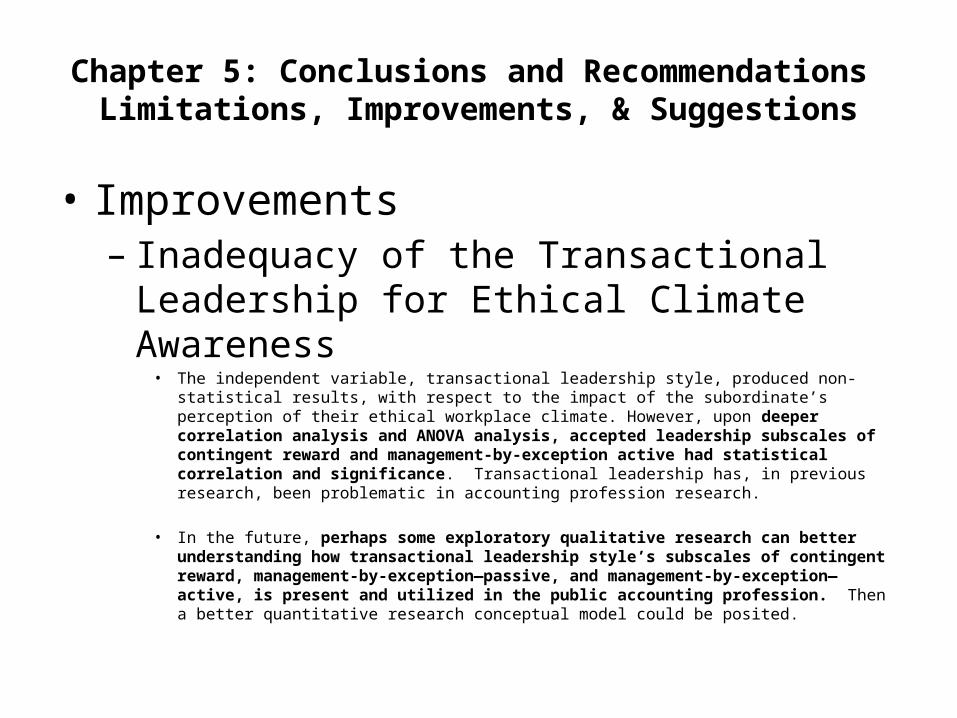

Chapter 5: Conclusions and Recommendations Limitations, Improvements, & Suggestions

• Improvements– Inadequacy of the Transactional Leadership for

Ethical Climate Awareness• The independent variable, transactional leadership style, produced non-statistical results, with respect to the

impact of the subordinate’s perception of their ethical workplace climate. However, upon deeper correlation analysis and ANOVA analysis, accepted leadership subscales of contingent reward and management-by-exception active had statistical correlation and significance. Transactional leadership has, in previous research, been problematic in accounting profession research.

• In the future, perhaps some exploratory qualitative research can better understanding how transactional leadership style’s subscales of contingent reward, management-by-exception—passive, and management-by-exception—active, is present and utilized in the public accounting profession. Then a better quantitative research conceptual model could be posited.

Chapter 5: Conclusions and Recommendations Limitations, Improvements, & Suggestions

• Suggestions for Future Research• First, with appropriate corrections for the ECQ Survey instrument, this study can be replicated in other

professional public accounting jurisdictions. The accumulation of future replications can add to the aggregating of a larger, robust sample, perhaps leading to a meta-analysis.

• Second, better religiosity construct development can be pursued.

• Third, further research opportunities. For example, – why in Utah do women’s employment percentages nearly shrink in half, over time? – Why do men represent a higher percentage in the accounting profession’s senior positions? – What are the social factors creating a “glass ceiling” effect in Utah’s public accounting profession? – Why does the public accounting profession continue to appear unattractive to minority persons?

• Fourth, can better process-based management philosophies, with leadership training interventions, further bend the Utah public accounting leadership culture more toward transformational leadership, less towards transactional, and the eradication of laissez-faire leadership?

• Fifth, could accounting firms that improve their transformational leadership practices, – heighten the subordinates’ perception to the more preferred ethical climate types (i.e., caring, lawcode, and rules) ?– earn higher employee satisfaction, experience less professional staff turnover, and increase profitability?

References

Provided in the separate chapter PowerPoint presentations