business strategy - daniel serranodaniel-serrano.com/documents/serrano_daniel_zipcar_m2.pdf ·...

TRANSCRIPT

Business Strategy

Team 2Monica De LezaetaDaniel SerranoHugh BowenDaniel ShovlinAdam Chapman

Wheels when you want them

1Tuesday, May 4, 2010

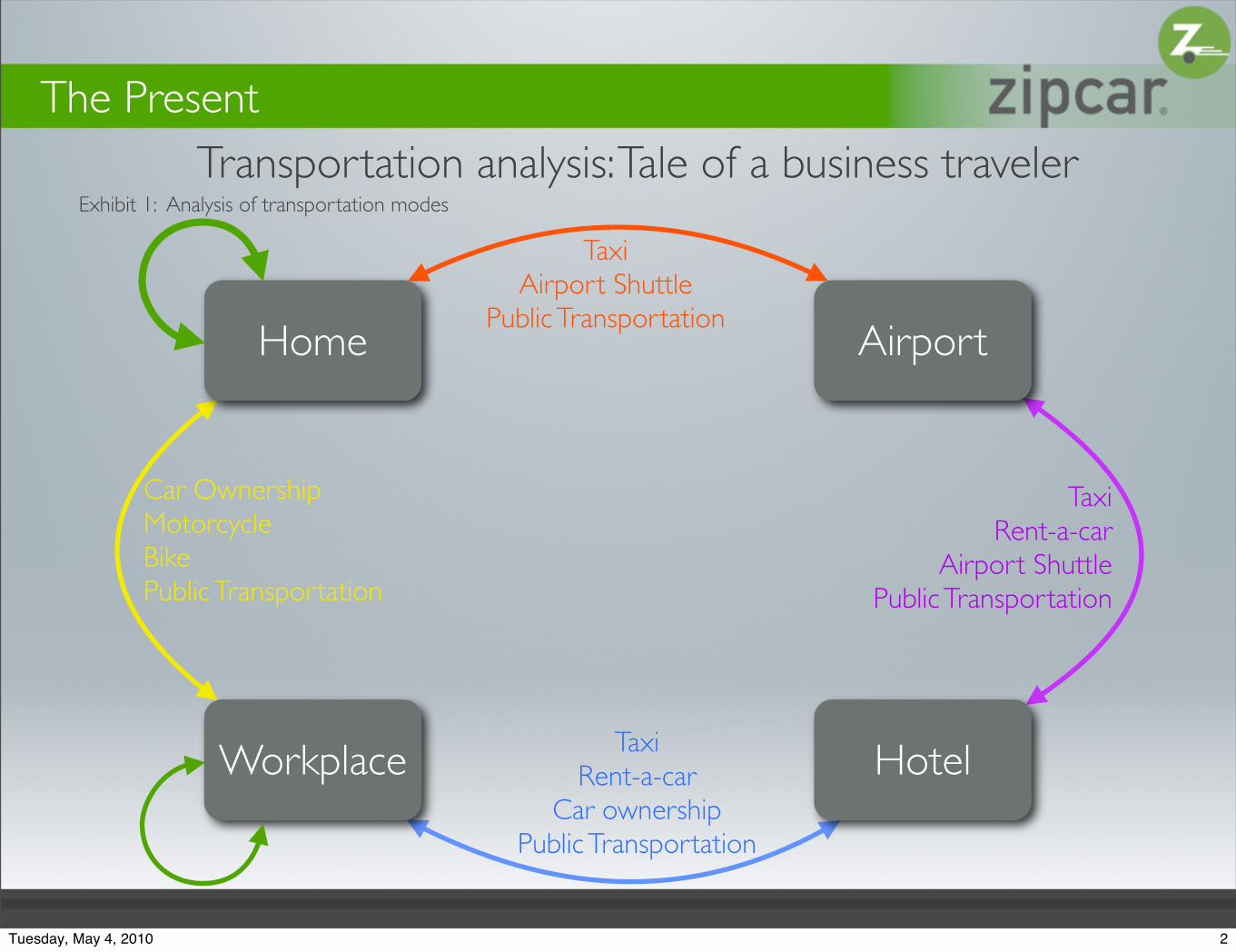

Home

HotelWorkplace

Airport

Car OwnershipMotorcycleBikePublic Transportation

TaxiRent-a-car

Airport ShuttlePublic Transportation

TaxiAirport Shuttle

Public Transportation

TaxiRent-a-car

Car ownershipPublic Transportation

The Present Transportation analysis: Tale of a business traveler

Exhibit 1: Analysis of transportation modes

2Tuesday, May 4, 2010

Home

HotelWorkplace

Airport

Car OwnershipMotorcycleBikePublic Transportation

TaxiRent-a-car

Airport ShuttlePublic Transportation

TaxiAirport Shuttle

Public Transportation

TaxiRent-a-car

Car ownershipPublic Transportation

The Present Transportation analysis: Tale of a business traveler

Exhibit 1: Analysis of transportation modes

2Tuesday, May 4, 2010

Transportation analysis: Tale of a business traveler

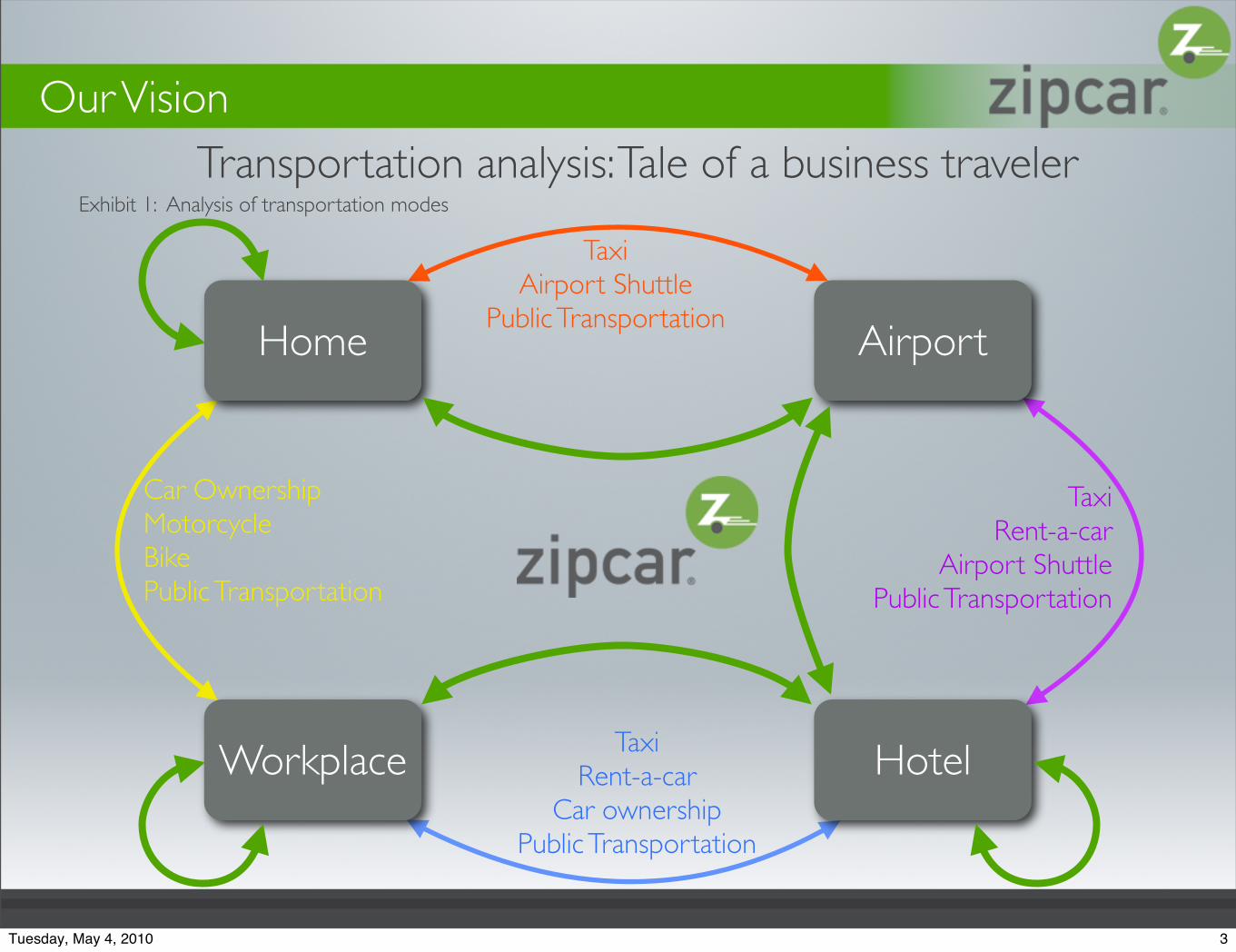

Home

HotelWorkplace

Airport

Car OwnershipMotorcycleBikePublic Transportation

TaxiRent-a-car

Airport ShuttlePublic Transportation

TaxiAirport Shuttle

Public Transportation

TaxiRent-a-car

Car ownershipPublic Transportation

Our Vision

Exhibit 1: Analysis of transportation modes

3Tuesday, May 4, 2010

Vision & Mission Statement

Vision“Be the Premier Global Car-Sharing Service provider offering and integrated transportation system solution.”

Mission“Strengthen the Zipcar brand in the United States and expand the Zipcar presence into Europe and Asia by leveraging core competencies, providing excellent customer service, capitalizing on proprietary technology and aggressively pursuing strategic partnerships.”

4Tuesday, May 4, 2010

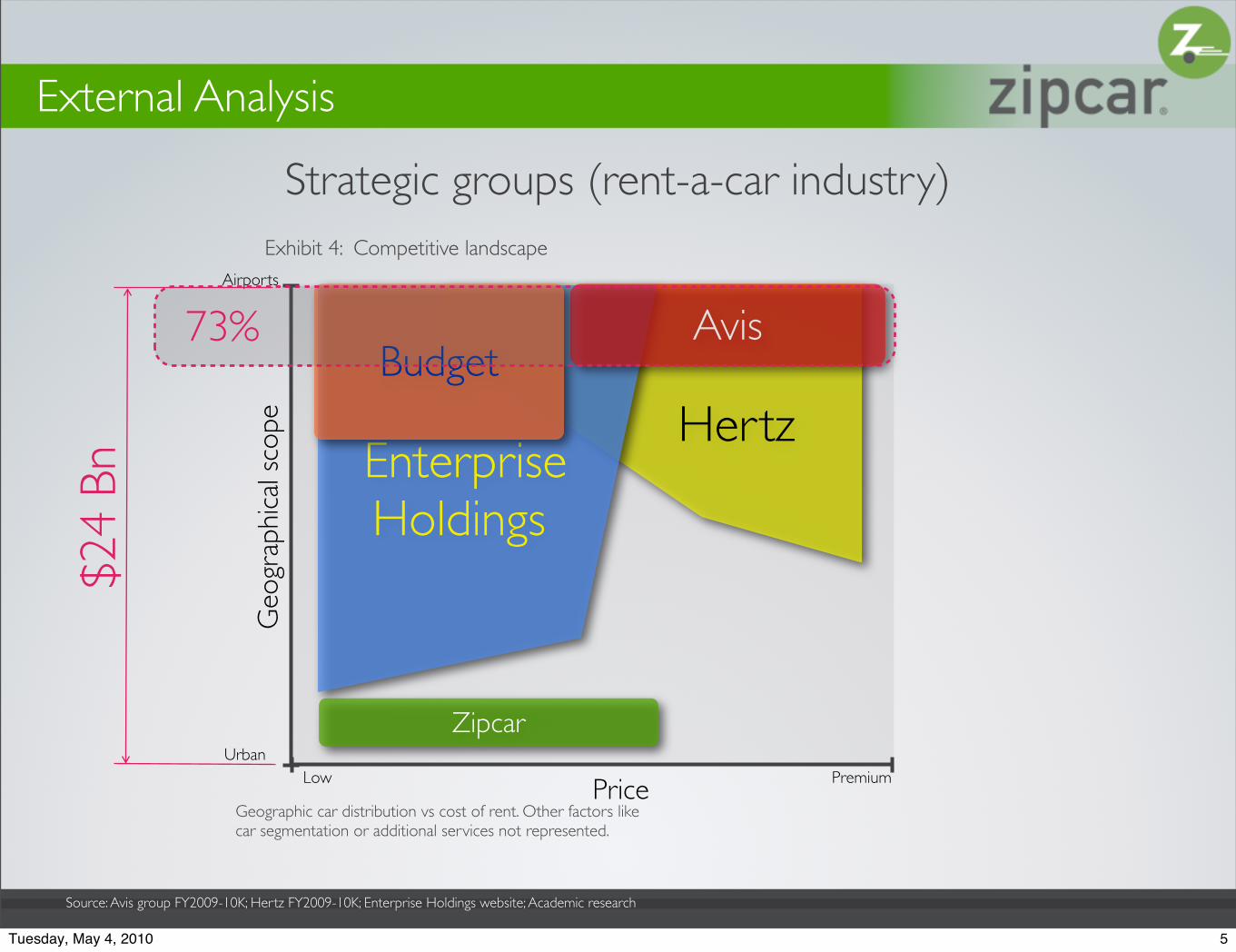

Strategic groups (rent-a-car industry)

Hertz

Airports

Urban

Geo

grap

hica

l sco

pe

PriceLow Premium

Exhibit 4: Competitive landscape

Geographic car distribution vs cost of rent. Other factors like car segmentation or additional services not represented.

Enterprise Holdings

AvisBudget

Zipcar

73%

External Analysis $2

4 Bn

Source: Avis group FY2009-10K; Hertz FY2009-10K; Enterprise Holdings website; Academic research

5Tuesday, May 4, 2010

Strategic groups (rent-a-car industry)

Airports

Urban

Geo

grap

hica

l sco

pe

PriceLow Premium

Exhibit 4: Competitive landscape

Geographic car distribution vs cost of rent. Other factors like car segmentation or additional services not represented.

HertzEnterprise Holdings

AvisBudget

Zipcar

73%

External Analysis $2

4 Bn

Source: Avis group FY2009-10K; Hertz FY2009-10K; Enterprise Holdings website; Academic research

5Tuesday, May 4, 2010

Ostrich Strategy

6Tuesday, May 4, 2010

Competitive Analysis

7Tuesday, May 4, 2010

SUBSTITUTESCar ownership

Taxi Co.Motorcycles

eBikesPublic Transportation

POTENTIAL ENTRANTSRent A Car Companies

Automobile ManufacturersGovernments

NGOs

INDUSTRY COMPETITORSConnect by Hertz

WeCarMint

CAR2GO

SUPPLIERS

BUYERS

Porter’s 5 Forces

8Tuesday, May 4, 2010

Potential entrants: Threat of Entry

Sources of barriers to entry:• Capital requirements: high cost of capital

• Economies of scale: high volumes to be competitive

• Absolute cost advantages: access to low cost raw materials

• Product differentiation: brand recognition, consumer loyalty

• Access to channels of distribution

• Government & legal barriers: patents

• Retaliation

POTENTIAL ENTRANTSRent A Car Companies

Automobile ManufacturersGovernments/NGO

Porter’s 5 Forces

9Tuesday, May 4, 2010

Rivalry between established competitors:

Factors that may affect the prices:• Concentration: Small number, low price

changes

• Diversity of competitors: different price structures

• Product Differentiation: avoid commoditization

• Excess of capacity: may force price reduction

• Cost conditions: fixed/variable costs

INDUSTRY COMPETITORSConnect by Hertz

WeCarMint

CAR2GO

Porter’s 5 Forces

10Tuesday, May 4, 2010

High

Low

Flex

ibilit

y ne

eded

Distance of travelLow High

Source: Adapted from Schwartz, Joachim. Presentation at Car-Free Cities Working Group seminar, London, 1999.

Public Transportation

Taxi

Bike

Car-rental

Exhibit 3: Relationship to other modes of transportation

Zipcar

External Analysis

Alternatives to traditional automobile

11Tuesday, May 4, 2010

High

Low

Flex

ibilit

y ne

eded

Distance of travelLow High

Source: Adapted from Schwartz, Joachim. Presentation at Car-Free Cities Working Group seminar, London, 1999.

Public Transportation

Taxi

Bike

Car-rental

Exhibit 3: Relationship to other modes of transportation

Zipcar

External Analysis

Alternatives to traditional automobile

11Tuesday, May 4, 2010

POTENTIAL ENTRANTSRent A Car Companies

Automobile ManufacturersGovernments

NGOs

INDUSTRY COMPETITORSConnect by Hertz

WeCarMint

CAR2GO

COMPLEMENTSeBikes

Public TransportationAirport Shuttles

SUPPLIERS

BUYERS

Porter’s 6 Forces

Adapted from: Robert M. Grant (2010) “Contemporary Strategy Analysis 7th Ed”

SUBSTITUTESCar ownership

Taxi Co.Motorcycles

eBikesPublic Transportation

Airport Shuttles

12Tuesday, May 4, 2010

POTENTIAL ENTRANTSRent A Car Companies

Automobile ManufacturersGovernments

NGOs

INDUSTRY COMPETITORSConnect by Hertz

WeCarMint

CAR2GOCOMPLEMENTS

eBikesPublic Transportation

Airport Shuttles

SUPPLIERS

BUYERS

Porter’s 6 Forces

Adapted from: Robert M. Grant (2010) “Contemporary Strategy Analysis 7th Ed”

SUBSTITUTESCar ownership

Taxi Co.Motorcycles

eBikesPublic Transportation

Airport Shuttles

12Tuesday, May 4, 2010

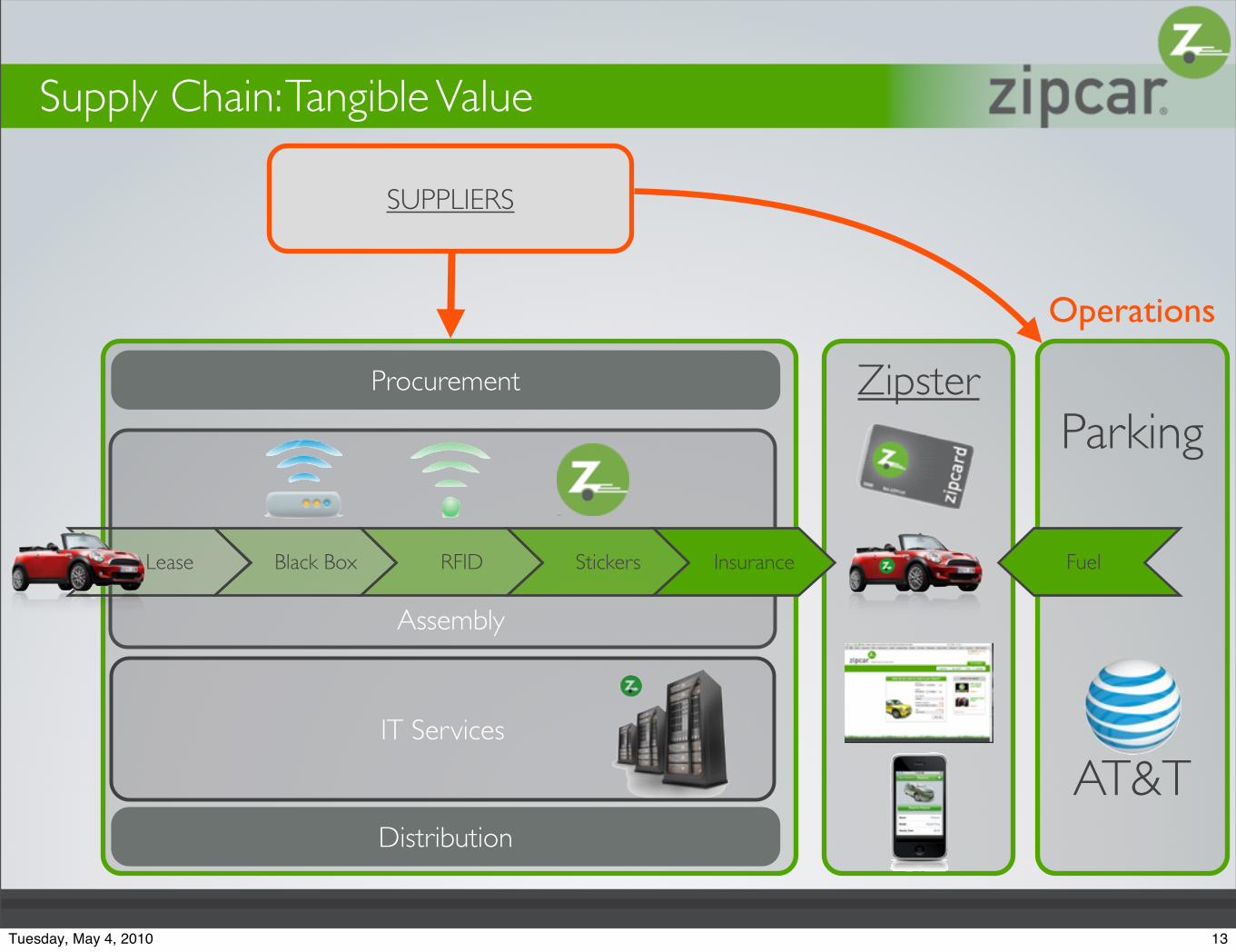

Supply Chain: Tangible Value

InsuranceStickersRFIDBlack BoxLease

SUPPLIERS

Procurement

Distribution

Operations

Assembly

IT Services

ZipsterParking

Fuel

AT&T

13Tuesday, May 4, 2010

Supply Chain: Intangible Value

Inbound logistics Operations

Outbound logistics

Marketing & Sales

Service

• Green movement• Member benefits “Partnerships”• Cost saving

• Availability• Affordability• Customization• Support• Hassle free

• Car Network• Maintenance• Customer Service

Added value to customers

BUYERS

14Tuesday, May 4, 2010

Supply Chain: Intangible Value

Inbound logistics Operations

Outbound logistics

Marketing & Sales

Service

• Green movement• Member benefits “Partnerships”• Cost saving

• Availability• Affordability• Customization• Support• Hassle free

• Car Network• Maintenance• Customer Service

Added value to customers

Improvement

BUYERS

14Tuesday, May 4, 2010

Recap of primary strategies

#1 Leverage brand recognition to create stronger partnerships

#3 Increase convenience by enhancing technology

#2 Increase university campus presence

#4 Expansion in suburban areas of dense cities

#5 Evolve the business model

#7 Expansion to suburban areas of dense cities

#6 Expansion to main european cities

#9 Capital investments

#11 Market securities investments

#12 Competitive advantage or Entry barriers

#10 Partnerships

Recap of SWOT

From Strengths From Weaknesses

From Opportunities From Threats

Business Growth

Entry barriers#8 Exploit Fast Fleet

15Tuesday, May 4, 2010

Strategy Objective:“Increase our competitive advantage by improving the positioning of our product while reducing our cost structure”

Differentiation:Extended car network

Cost Leadership:Reduced parking costs

Competitive Advantage Strategic Alliance

Strategic Competitive Advantage

Tangible + Intangible Differentiation for a longer period of time

Pursued Strategy

16Tuesday, May 4, 2010

ZIPCAR HILTON ALLIANCEZipcar Benefits:•Added parking locations near high

density population with short term transportation needs

•Access to the community surrounding the hotel parking locations

•Broader distribution to more suburban areas

•New clientele base•Segmented clientele for car selection•Inroad to airports and competition

with rent-a-cars•Inroad to Europe

Hilton Benefits:

•Increased convenience and amenities

for the hotel customer

•Revenue from Zipcar membership

•Increased advertising through Zipcar

channels

• Increased Competitive Differentiation

•Capitalization on “Green Movement”

Pursued Strategy

17Tuesday, May 4, 2010

THE MEMBERSHIP CARDTangible benefits for our members

• Reward points• All-in-one card

•Unlocks your car•Unlocks your room

• Might include American Express

Strategy Implementation

18Tuesday, May 4, 2010

INTEGRATED SEARCHTangible benefits for our partner

• Extended Hilton brand exposure• Direct Zipcar’s customers to Hilton

• Seamless reservation process

Strategy Implementation

19Tuesday, May 4, 2010

•Zipcar Locations

Strategy: Tactics

Our Tactic: First Stage

20Tuesday, May 4, 2010

Strategy: Tactics

Our Tactic: First Stage

•Zipcar + Hilton Locations

•Zipcar +Hilton + Airports124 Hotels19 Airpots

20Tuesday, May 4, 2010

Financial Projections

0K

1K

2K

3K

4K

5K

6KHotel Strategy

# o

f Car

s

0K25K50K75K

100K125K150K175K200K

Year

0

Year

1 -

Q1

Q2

Q3

Q4

Year

2-Q

1

Q2

Q3

Q4

Year

3-Q

1

Q2

Q3

Q4

Year

4-Q

1

Q2

Q3

Q4

Year

5-Q

1

Q2

Q3

Q4

# o

f Mem

bers

Total # Members Organic Total # Members Hotel

Exhibit 4: Car and Membership growth

21Tuesday, May 4, 2010

Financial Projections

0K

1K

2K

3K

4K

5K

6KHotel Strategy

# o

f Car

s

0K25K50K75K

100K125K150K175K200K

Year

0

Year

1 -

Q1

Q2

Q3

Q4

Year

2-Q

1

Q2

Q3

Q4

Year

3-Q

1

Q2

Q3

Q4

Year

4-Q

1

Q2

Q3

Q4

Year

5-Q

1

Q2

Q3

Q4

# o

f Mem

bers

Total # Members Organic Total # Members Hotel

harvesting

Exhibit 4: Car and Membership growth

21Tuesday, May 4, 2010

Financial Projections

Financial Facts:

•First positive cashflow: Year2-Q2

•Breakeven Point: Year3-Q1

•NPV @ 12%: $39M

•IRR: 26.7%

•Initial investment: $4.5M-$15M

-$8M

$0M

$8M

$15M

$23M

$30M

Year

0

Year

1 -

Q1

Q2

Q3

Q4

Year

2-Q

1

Q2

Q3

Q4

Year

3-Q

1

Q2

Q3

Q4

Year

4-Q

1

Q2

Q3

Q4

Year

5-Q

1

Q2

Q3

Q4

Hotel Strategy: Quarterly Financial projections

Profit Total Cost Revenue

Exhibit 5: Zipcar - Hilton Alliance. Zipcar Projections

22Tuesday, May 4, 2010

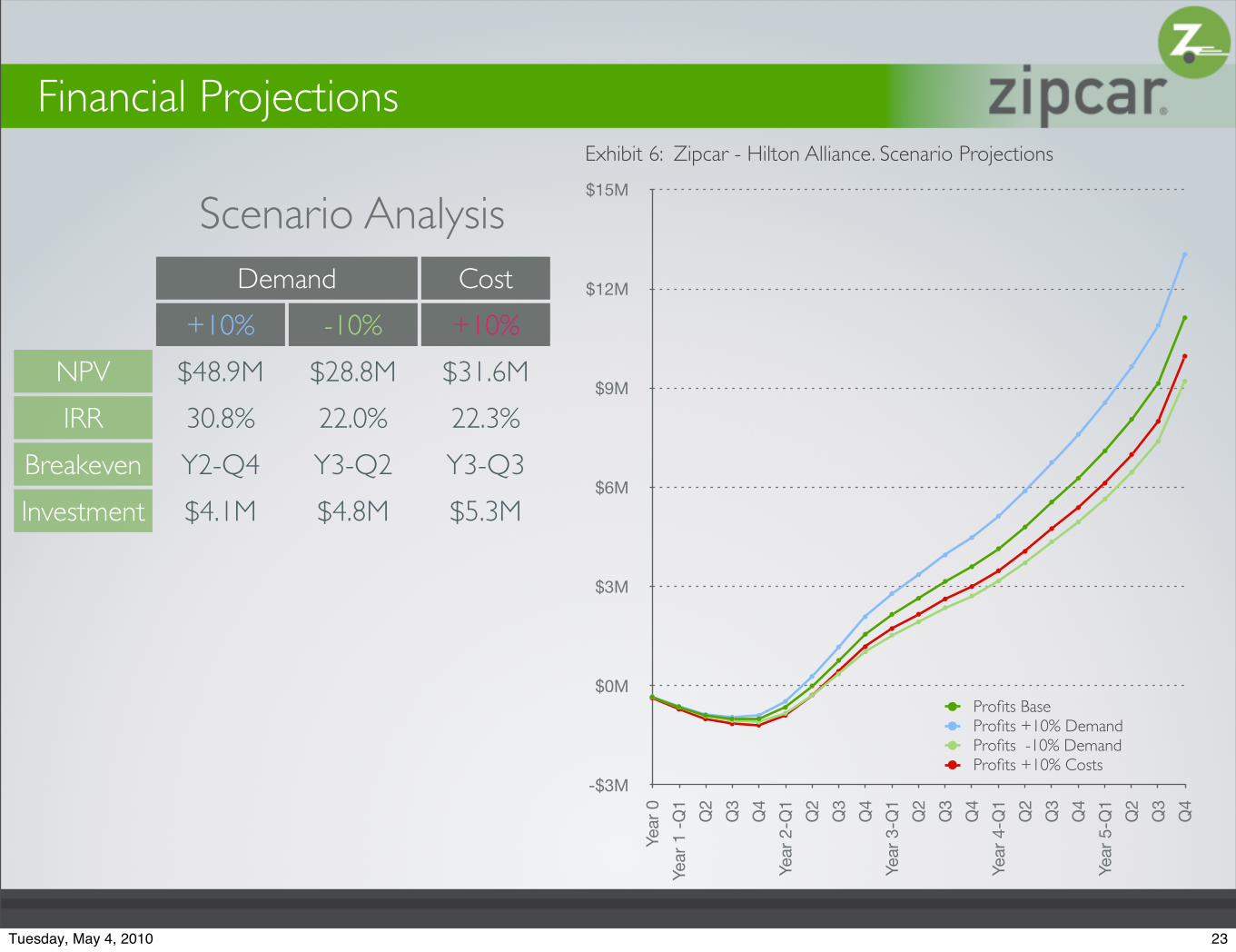

Scenario Analysis

Financial Projections

DemandDemand Cost

+10% -10% +10%

NPV

IRR

Breakeven

Investment

$48.9M $28.8M $31.6M

30.8% 22.0% 22.3%

Y2-Q4 Y3-Q2 Y3-Q3

$4.1M $4.8M $5.3M

-$3M

$0M

$3M

$6M

$9M

$12M

$15M

Year

0

Year

1 -

Q1

Q2

Q3

Q4

Year

2-Q

1

Q2

Q3

Q4

Year

3-Q

1

Q2

Q3

Q4

Year

4-Q

1

Q2

Q3

Q4

Year

5-Q

1

Q2

Q3

Q4

Profits Base Profits +10% DemandProfits -10% DemandProfits +10% Costs

Exhibit 6: Zipcar - Hilton Alliance. Scenario Projections

23Tuesday, May 4, 2010

The new Zipcar world:3,375 New Hotels30+ New Airports

24Tuesday, May 4, 2010

Wheels when you want them

THANK YOU25Tuesday, May 4, 2010

Wheels when you want them

&aq

THANK YOU25Tuesday, May 4, 2010

0%

25%

50%

75%

100%

Q1 Q2 Q3 Q4 Q5 Q6 Q7 Q8 Q9 Q10 Q11 Q12 Q13 Q14 Q15 Q16

Adoption rates - Assumption

Adoption Rate Organic (Base case)Adoption Rate HotelsAdoption Rate Organic Not previous presence (Base case)Adoption Rate HOTELS Not previous presence (Base case)

Backup: Financial Projections

Other assumptions:Members per car (objective): 40Revenue per car per year : $18.000Reduced services from Hilton:

•Parking slots: 100%

•Maintenance: 25%

Revenue stream to Hilton:•Membership fees of members captured in their

hotels: ($25 each)

•10% Revenue of traffic originated from their captures.

Exhibit 7: Zipcar - Hilton Alliance. Zipcar Projections

26Tuesday, May 4, 2010

$0M

$0.25M

$0.5M

$0.75M

$1M

$1.25M

$1.5M

Year 0 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4

Hilton: Financial Projections

Parking costHilton Deductions (parking+25% service)Hilton Profit Total

Excerpt:

NPV of Hilton Revenue:

$5.6M

NPV of Parking Cost:

$6.5M

Cost of opportunity for Hilton:

$0.9M

Backup: Hilton Financials

Exhibit 8: Zipcar - Hilton Alliance. Hilton Projections

27Tuesday, May 4, 2010

Year 0 Year 1 -Q1 Q2 Q3 Q4 Year 2-Q1 Q4 Year 3-Q1 Q4 Year 4-Q1 Q4 Year 5-Q1 Q4Members x Car (objective) 40Revenues# New Hotels 47 47 47 47 55 55 84 84 167 167 425 425 0# Cars x Hotel 4 4 4 4 4 4 3 3 2 2 1 1 0# New Cars 188 188 188 188 220 220 252 252 334 334 425 425 0Aggregated # cars 188 376 564 752 972 1192 1884 2136 2974 3308 4401 4826 5676

# Members x Car (organic) 3.825 6.12 11.73 17.85 36.975 68.85 87.975 119.85 138.975 170.85# Members x Car (hotel) 0.95625 1.53 2.9325 4.4625 8.2875 12.75 12.75

Members Organic (hidden calculations)Total # Members Organic 564 1466 3196 5828 10592 30696 36472 52859 59367 82144 91064 121954Members Hotel (hidden calculations)Total # Members Hotel 141 367 799 1457 2685 8070 9776 15227 17472 25298 28351 38890Total # Members Organic + Hotel 705 1833 3995 7285 13277 38766 46248 68086 76839 107442 119415 160844Members rate (Real/Objective) 9.38% 12.19% 17.71% 24.22% 34.15% 59.38% 61.37% 64.48% 64.59% 67.56% 67.83% 70.84%Revenue x car/yearRevenue x car/quarter (maximum @ 40users) $ 1,128,000 $ 2,256,000 $ 3,384,000 $ 4,512,000 $ 5,832,000 $ 9,792,000 $ 11,304,000 $ 15,840,000 $ 17,844,000 $ 23,856,000 $ 26,406,000 $ 34,056,000

Revenue 0 $ 105,750 $ 274,950 $ 599,250 $ 1,092,750 $ 1,991,550 $ 5,814,900 $ 6,937,200 $ 10,212,900 $ 11,525,850 $ 16,116,300 $ 17,912,250 $ 24,126,600Revenue w/out Hotel $ 84,600 $ 219,900 $ 479,400 $ 874,200 $ 1,588,800 $ 4,604,400 $ 5,470,800 $ 7,928,850 $ 8,905,050 $ 12,321,600 $ 13,659,600 $ 18,293,100Revenue from Hotel $ 21,150 $ 55,050 $ 119,850 $ 218,550 $ 402,750 $ 1,210,500 $ 1,466,400 $ 2,284,050 $ 2,620,800 $ 3,794,700 $ 4,252,650 $ 5,833,500Increase rate Hotel/Overall 20.0% 20.0% 20.0% 20.0% 20.2% 20.8% 21.1% 22.4% 22.7% 23.5% 23.7% 24.2%Increase rate Hotel/Organic 25% 25% 25% 25% 25% 26% 27% 29% 29% 31% 31% 32%

Hilton Profit (Fee based $50 x new member) 3525 28200 54050 82250 149800 226075 187050 193975 218825 275750 299325 370275Hilton Porfit (Hotel Revenue Margin) $ 2,115 $ 5,505 $ 11,985 $ 21,855 $ 40,275 $ 121,050 $ 146,640 $ 228,405 $ 262,080 $ 379,470 $ 425,265 $ 583,350Hilton Profit Total $ 5,640 $ 33,705 $ 66,035 $ 104,105 $ 190,075 $ 347,125 $ 333,690 $ 422,380 $ 480,905 $ 655,220 $ 724,590 $ 953,625Hilton NPV of Profit $ 5,575,881

CostsLeasing $ 225,600 $ 451,200 $ 676,800 $ 902,400 $ 1,166,400 $ 1,430,400 $ 2,260,800 $ 2,563,200 $ 3,568,800 $ 3,969,600 $ 5,281,200 $ 5,791,200 $ 6,811,200Access $ 23,502 $ 47,004 $ 70,506 $ 94,008 $ 121,510 $ 149,012 $ 235,519 $ 267,021 $ 371,780 $ 413,533 $ 550,169 $ 603,298 $ 709,557Parking $ 36,660 $ 73,320 $ 109,980 $ 146,640 $ 189,540 $ 232,440 $ 367,380 $ 416,520 $ 579,930 $ 645,060 $ 858,195 $ 941,070 $ 1,106,820Insurance $ 79,902 $ 159,804 $ 239,706 $ 319,608 $ 413,110 $ 506,612 $ 800,719 $ 907,821 $ 1,263,980 $ 1,405,933 $ 1,870,469 $ 2,051,098 $ 2,412,357Maintenance $ 18,798 $ 37,596 $ 56,394 $ 75,192 $ 97,190 $ 163,184 $ 188,381 $ 263,974 $ 297,370 $ 397,560 $ 440,056 $ 567,543Fuel $ 55,836 $ 111,672 $ 167,508 $ 223,344 $ 288,684 $ 484,704 $ 559,548 $ 784,080 $ 883,278 $ 1,180,872 $ 1,307,097 $ 1,685,772Total Operational Cost $ 365,664 $ 805,962 $ 1,246,260 $ 1,686,557 $ 2,189,096 $ 2,704,338 $ 4,312,305 $ 4,902,492 $ 6,832,543 $ 7,614,774 $ 10,138,465 $ 11,133,820 $ 13,293,249Hilton Operational Cost $ 0 $ 5,640 $ 33,705 $ 66,035 $ 104,105 $ 190,075 $ 347,125 $ 333,690 $ 422,380 $ 480,905 $ 655,220 $ 724,590 $ 953,625Hilton Deductions (parking+25% service) $ (36,660) $ (78,020) $ (119,379) $ (160,739) $ (208,338) $ (256,738) $ (408,176) $ (463,615) $ (645,923) $ (719,403) $ (957,585) $ (1,051,084) $ (1,248,706)Total Costs $ 329,004 $ 733,582 $ 1,160,585 $ 1,591,854 $ 2,084,863 $ 2,637,676 $ 4,251,254 $ 4,772,567 $ 6,609,000 $ 7,376,277 $ 9,836,100 $ 10,807,326 $ 12,998,168

Profit $ (329,004) $ (627,832) $ (885,635) $ (992,604) $ (992,113) $ (646,126) $ 1,563,646 $ 2,164,633 $ 3,603,900 $ 4,149,573 $ 6,280,200 $ 7,104,924 $ 11,128,432GM -594% -322% -166% -91% -32% 27% 31% 35% 36% 39% 40% 46%Cumulative profit (aggregatted cash flows) $ (329,004) $ (956,836) $ (1,842,471) $ (2,835,075) $ (3,827,188) $ (4,473,313) $ (2,135,387) $ 29,246 $ 9,444,542 $ 13,594,115 $ 30,237,815 $ 37,342,739 $ 65,676,094

NPV $ 38,911,928IRR 26.68%Investment needed $ 4,473,313The HIlton advantage (Fees instead of parking)The HIlton advantage (Fees instead of parking) $ (31,020) $ (39,615) $ (43,945) $ (42,535) $ 535 $ 28,885 $ (33,690) $ (92,420) $ (99,025) $ (120,100) $ (133,605) $ (153,195)Hilton NPV of advantage $ (911,113)Hilton NPV of Parking $ 6,486,994

Backup: Financial ProjectionsQ2-3 hidden on Y2-5 to add clarity

28Tuesday, May 4, 2010

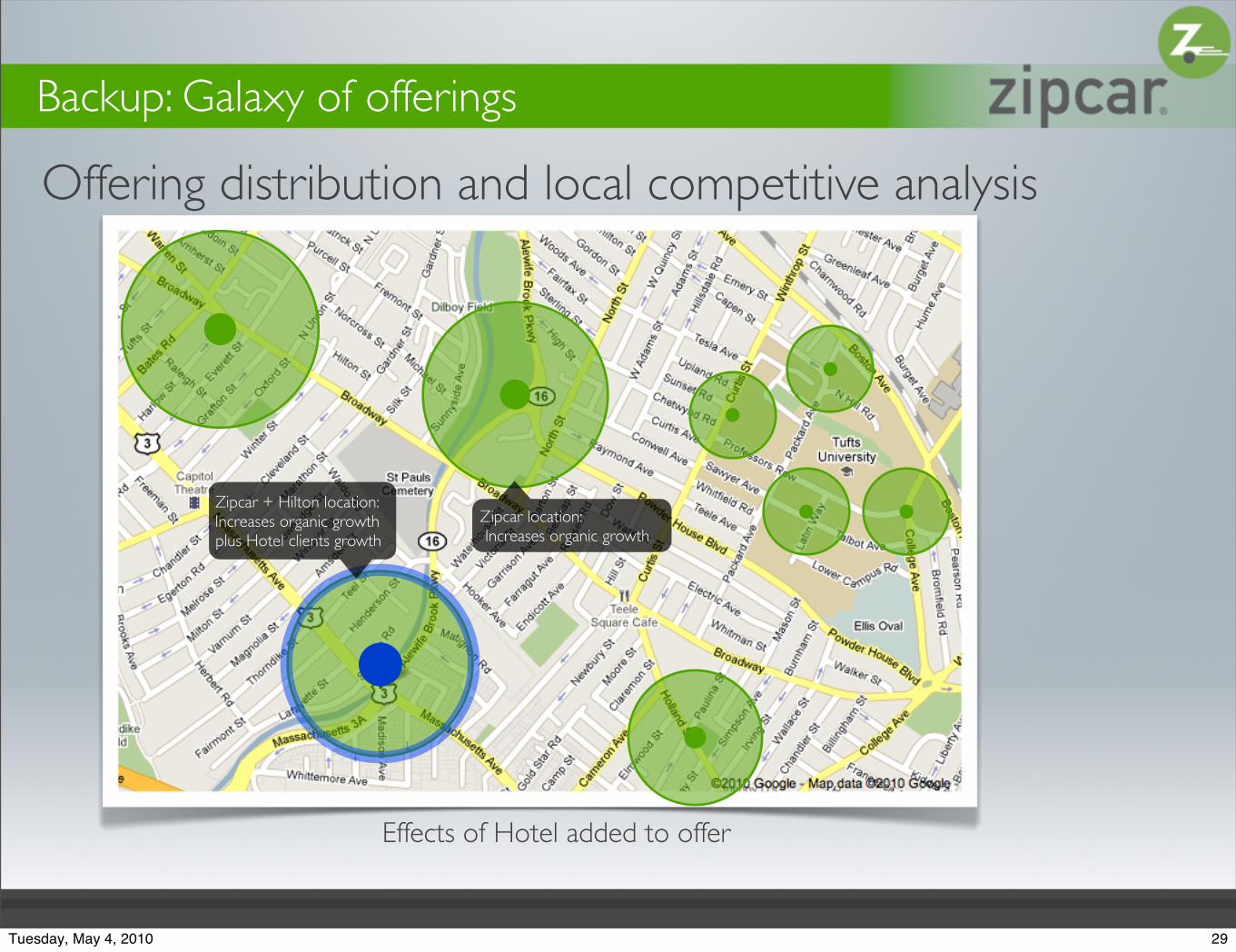

Offering distribution and local competitive analysis

Effects of Hotel added to offer

Backup: Galaxy of offerings

Zipcar location: Increases organic growth

Zipcar + Hilton location:Increases organic growthplus Hotel clients growth

29Tuesday, May 4, 2010

Backup: Process Analysis

Use of FMEA to analyze the process and find service improvements and hidden value

30Tuesday, May 4, 2010