business ethics & financial reportingusers.metropolia.fi/~minnak/ipw/monika...

TRANSCRIPT

University of Applied Sciences St. Pölten

Business Ethics &

Financial Reporting

Monika Kovarova-Simecek

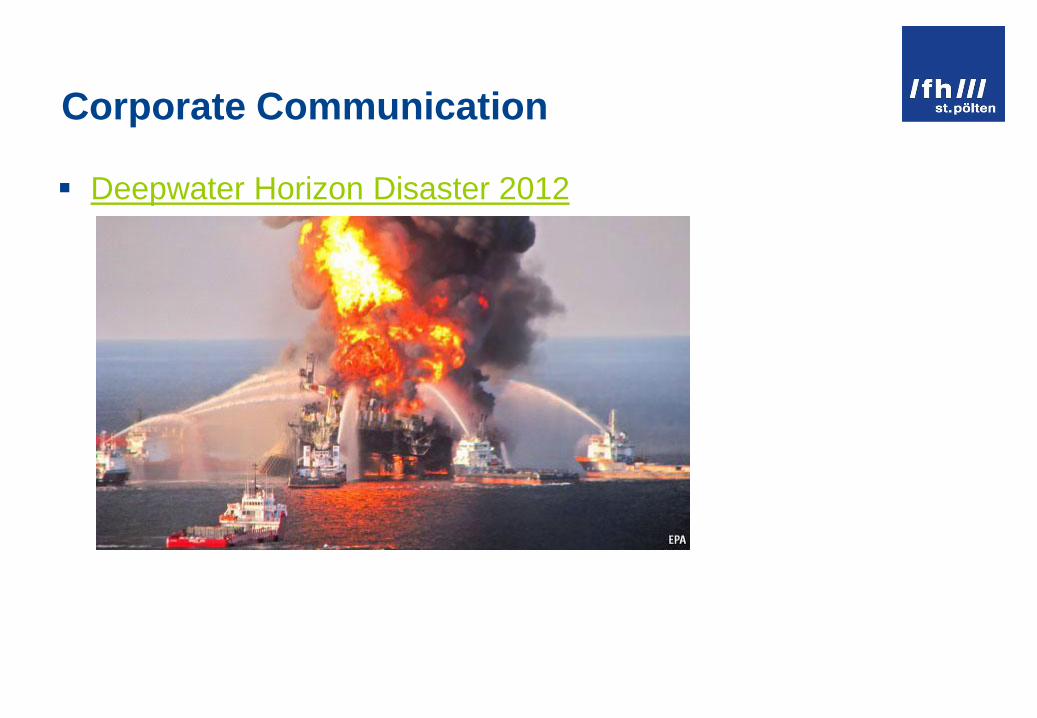

Corporate Communication

Deepwater Horizon Disaster 2012

Corporate Communication

”(…) is a set of activities involved in managing and orchestrating all internal and external communications aimed at creating

favorable point-of-view among stakeholders on which the company

depends. It is the messages issued by a corporate organization, body,

or institute to its audiences, such as employees, media, channel

partners and the general public. Organizations aim to communicate

(…) to transmit coherence, credibility and ethic.”

Riel, Cees B.M van/Fombrun, Charles J. (2007). Essentials Of Corporate Communication

What is business ethics?

Business Ethics = Corporate Responsibility

Definition along the legal debate over two questions:

Does a corporation hold a corporate responsibility for

activities of individual persons within the company?

1909 the US Supreme Court: YES

Is corporate responsibility defined by law or by what is

socially accepted in practise?

Strong resistence of business persons based upon Milton Friedman (1970): ‚ There is one and only social responsibility of business…to

use its resources and engage in acitivities desinged to increase its profits so long

as it stays within the rules of the game, which is to say, engaged in open and free

competition without deception or fraud.‘

Criminal responsibility for individuals

Fraud committed by members of the boards

Abuse of power

Demage of the company and third parties

Common case of Top Management fraud is accounting

fraud

The aftermath of legal vacuum

Case of Hooker Chemicals (1953): used Love Canal in Niagara Falls

as a dumping ground for trichlorophenal and dioxin without informing

government construsting a school at the area at the same time; years

later, chemical burns, miscarriagies, liver ailments and different types of

cancer were reported.

Case of Pinto Vehicle by Ford (1972): production despite of the

knowledge of a technical defect by which the fuel tank burst into flames

by collision.

Case of Lockheed (1972-73): payment of bribes to Japanes

government officicials to facilitate the purchase of jets Foreign Corrupt

Practises Act

Several other cases in the 1980s

Communication – Ethics – Risk

Communication Ethics

Risk

Corporate risks

Risk is fundamental to all business activity:

Risks at operating level: sales, costs, customers, suppliers,

liquidity, etc.

Risks at strategic level: political and legal risks, new technologies,

innovation, competitors, know-how etc.

Risk at human and behavioral level: the risk of

unethical behavior

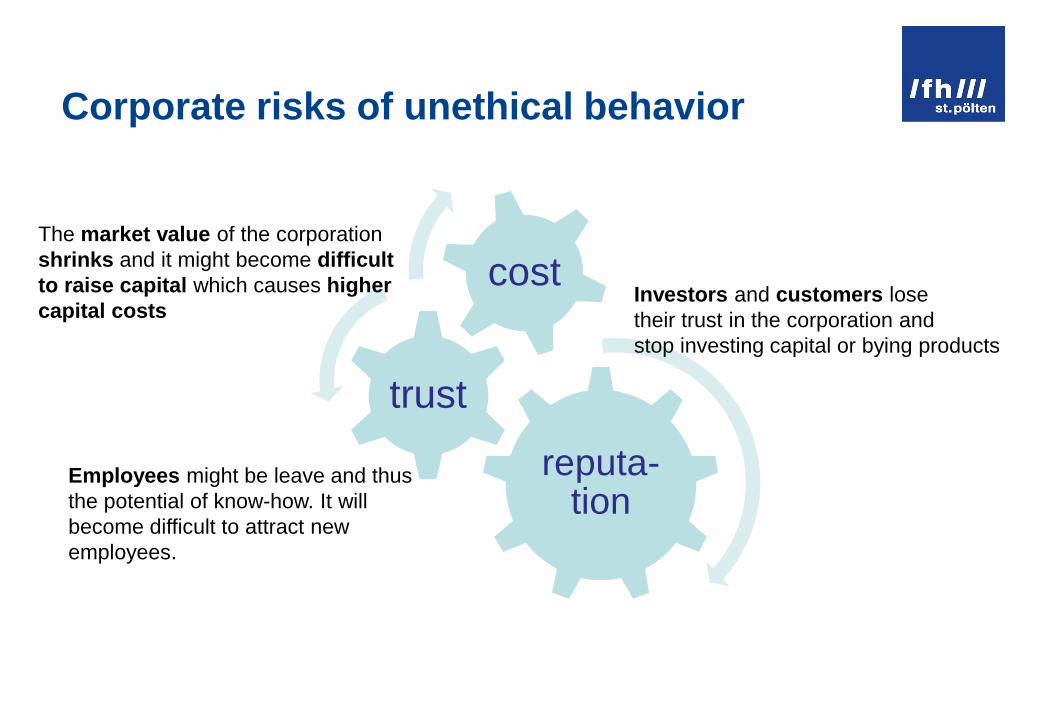

Corporate risks of unethical behavior

reputa-tion

trust

cost Investors and customers lose

their trust in the corporation and

stop investing capital or bying products

The market value of the corporation

shrinks and it might become difficult

to raise capital which causes higher

capital costs

Employees might be leave and thus

the potential of know-how. It will

become difficult to attract new

employees.

Communication as a risk of unethical

behaviour

Corporate Communication is a matter of behavior of the

company and thus of the individuals within the company.

This behavior is driven by the following factors:

Why? Reason? Motivation!

To whom? Stakeholder? Motivation!

What? Content? Motivation!

When? Time? Motivation!

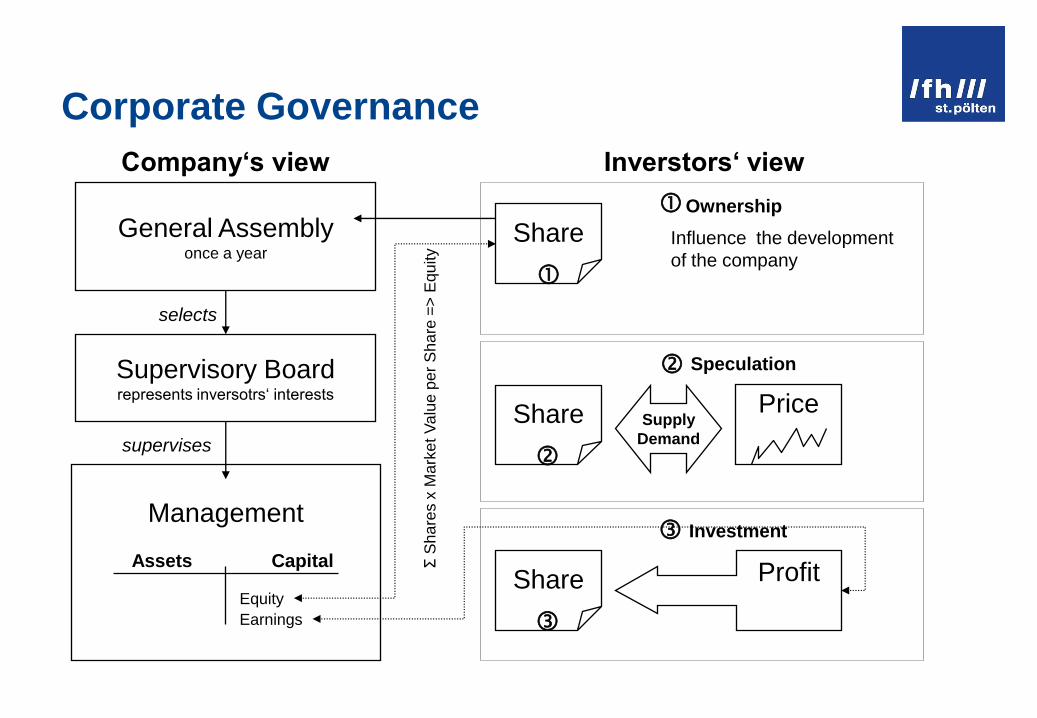

Corporate Governance

Company‘s view Inverstors‘ view

Price

General Assembly once a year

Supervisory Board represents inversotrs‘ interests

Management

Σ S

ha

res x

Ma

rket

Va

lue

pe

r S

ha

re =

> E

qu

ity

selects

supervises

Assets Capital

Equity

Share

Share Supply

Demand

Share

Earnings

Ownership

Speculation

Investment

Influence the development

of the company

Profit

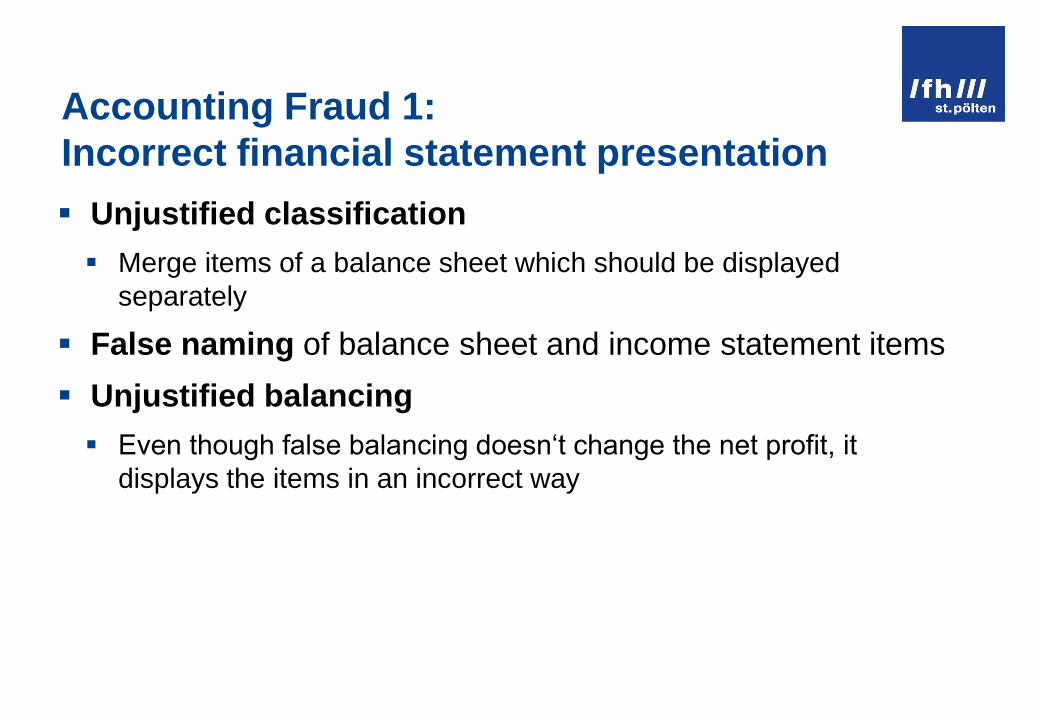

Accounting Fraud 1:

Incorrect financial statement presentation

Unjustified classification

Merge items of a balance sheet which should be displayed

separately

False naming of balance sheet and income statement items

Unjustified balancing

Even though false balancing doesn‘t change the net profit, it

displays the items in an incorrect way

Accounting Fraud 2:

Falsification of profits

Valuation fraud

overvaluation (defaulted extraordinary depreciation)

undervaluation (of provisions)

Defaulted booking of an asset or a liability

Booking of a not existing asset or a liability

Accounting Fraud 3.1:

Creativ accounting or „Window dressing“

Managers try to present the company in a better shape than it

is by:

Progressive balancing in bad times

Booking of good wills, deferred taxes and disagio

No booking of long-term provisions

Valuation of inventory with fixed and variable costs

Linear depreciation

Accounting Fraud 3.2:

Creativ accounting as „Window dressing“

Managers try to present the company in a worse shape than it

is by:

Conservative balancing in good times

Booking of provisions for expenses

Valuation of inventory with variable costs only

Declining depreciation

ENRON

The biggest case of bankruptcy based upon unethical

business

The result of abuse of power of individuals within the

company and legal vacuum

The story of ENRON

1985: after federal deregulation of natural gas pipelines, Enron was born

from the merger of Houston Natural Gas and InterNorth

In the process of the merger, Enron incurred massive debt

In order to survive, the company had to come up with a new and

innovative business strategy to generate profits and cash flow

Revolutionary solution to Enron's credit, cash and profit woes: a "gas

bank" in which Enron

would buy gas from a network of suppliers and sell it to a network of

consumers,

contractually guaranteeing both the supply and the price,

charging fees for the transactions and assuming the associated risk.

The raise of ENRON

Enron created both a new product and a new paradigm for

the industry the energy derivative

Enron Finance Corp.

dominated the market for natural gas contracts

could predict future prices with great accuracy

thereby guaranteeing superior profits

The raise of ENRON

Enron applied the „gas bank-concept“ to

the market for electric energy (1996)

other tradeable „commodities“ like coal, paper, steel, water,

weather (1997)

1999: Enron created EOL – an electronic commodities

trading Web site, handling 335bn $ in online commodity

trades in 2000

The fall of ENRON

Enron started to face various difficulties:

No appropriate accounting rules for such innovative products or

concepts

Increasing requirements on debt ratio by rating agencies such as S&Ps

Moody‘s

Increasing profit expectations of shareholders

Outstanding derivative contracts on balance sheets at the end of a

particular quarter adjustment to fair market value, booking unrealized

gains or losses to the income statement of the period.

No quoted prices upon which to base valuations for long-term futures

contracts in commodities such as gas.

Credit ratings

To satisfy credit rating agencies, Enron had to make sure,

its ROA and equity ratio is within an acceptabel range

reducing hard assets

earning increasing paper profits

using special purpose entities (SPEs)

The structure of SPEs

Enron SPEs

Bank

contributes hard assets and debt

in exchange for debt guarantees

sells hard assets

books profits

gives credit to SPEs

borrows the bank credits without

showing it up on the balance sheet

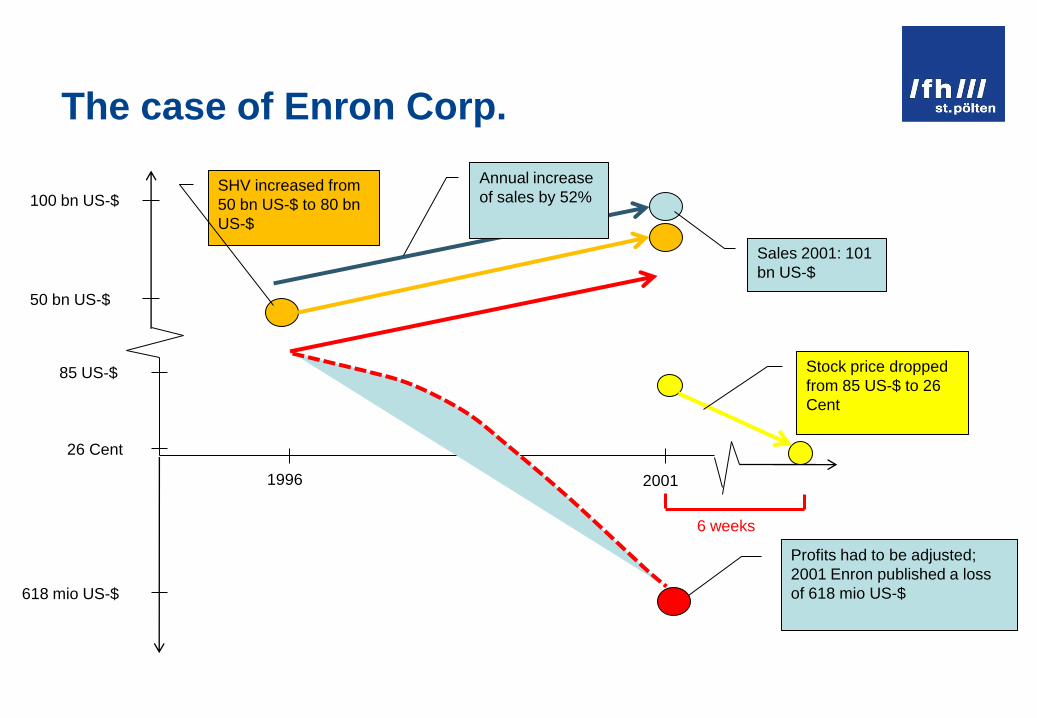

The case of Enron Corp.

100 bn US-$

50 bn US-$

85 US-$

26 Cent

1996 2001

6 weeks

Sales 2001: 101

bn US-$

SHV increased from

50 bn US-$ to 80 bn

US-$

Annual increase

of sales by 52%

Stock price dropped

from 85 US-$ to 26

Cent

618 mio US-$

Profits had to be adjusted;

2001 Enron published a loss

of 618 mio US-$

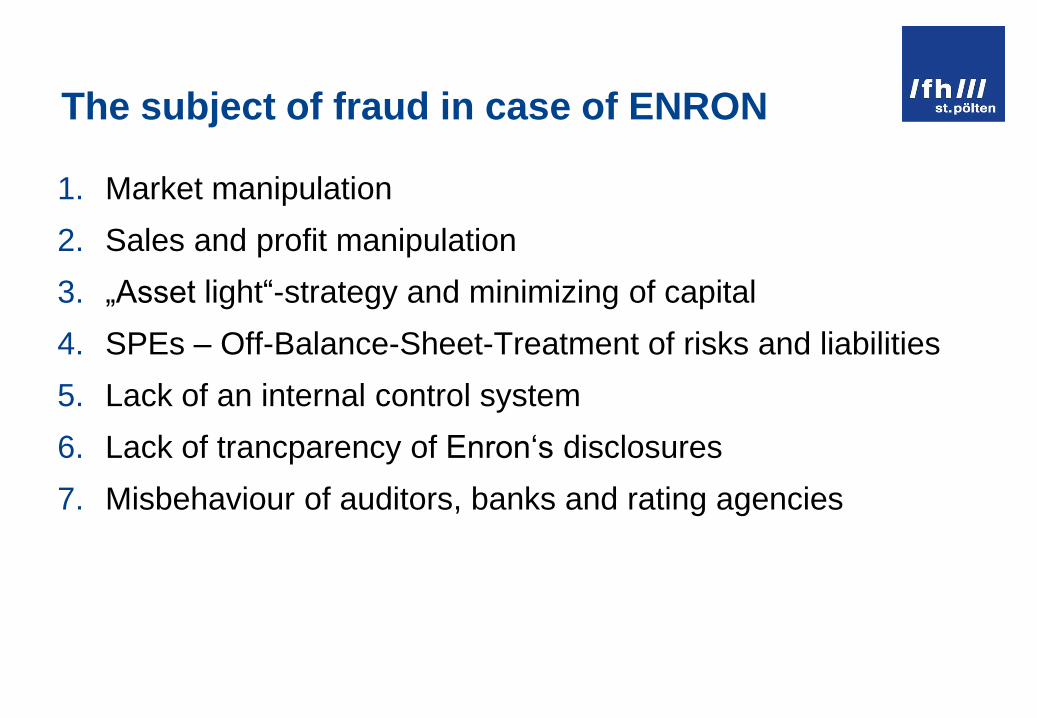

The subject of fraud in case of ENRON

1. Market manipulation

2. Sales and profit manipulation

3. „Asset light“-strategy and minimizing of capital

4. SPEs – Off-Balance-Sheet-Treatment of risks and liabilities

5. Lack of an internal control system

6. Lack of trancparency of Enron‘s disclosures

7. Misbehaviour of auditors, banks and rating agencies

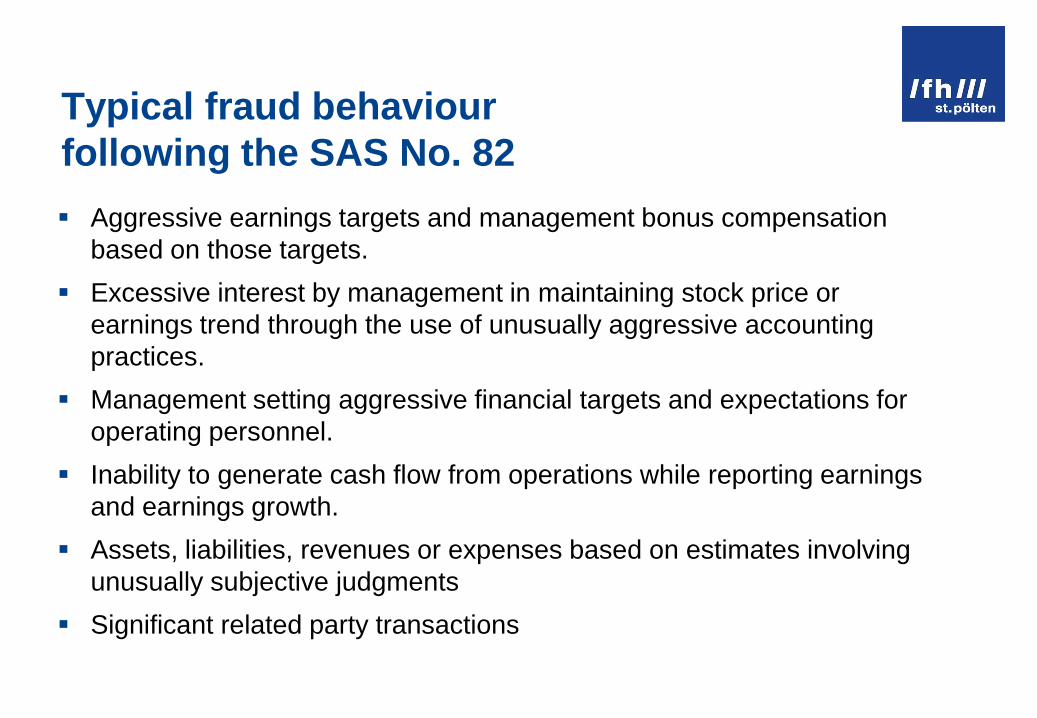

Typical fraud behaviour

following the SAS No. 82

Aggressive earnings targets and management bonus compensation

based on those targets.

Excessive interest by management in maintaining stock price or

earnings trend through the use of unusually aggressive accounting

practices.

Management setting aggressive financial targets and expectations for

operating personnel.

Inability to generate cash flow from operations while reporting earnings

and earnings growth.

Assets, liabilities, revenues or expenses based on estimates involving

unusually subjective judgments

Significant related party transactions

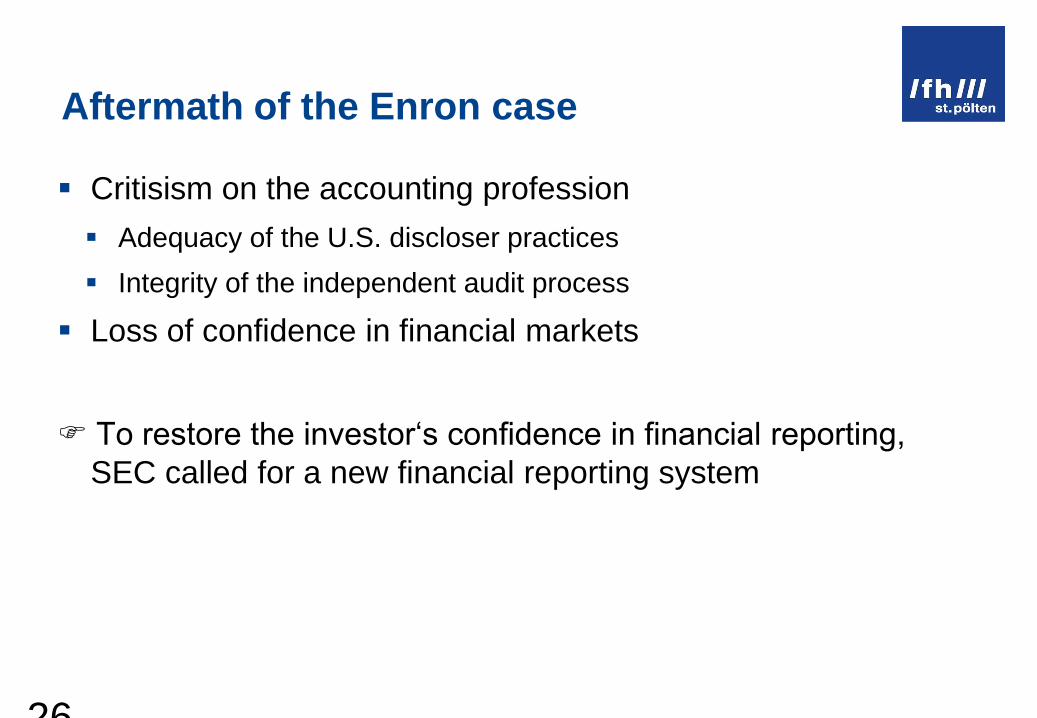

Aftermath of the Enron case

Critisism on the accounting profession

Adequacy of the U.S. discloser practices

Integrity of the independent audit process

Loss of confidence in financial markets

To restore the investor‘s confidence in financial reporting,

SEC called for a new financial reporting system

26

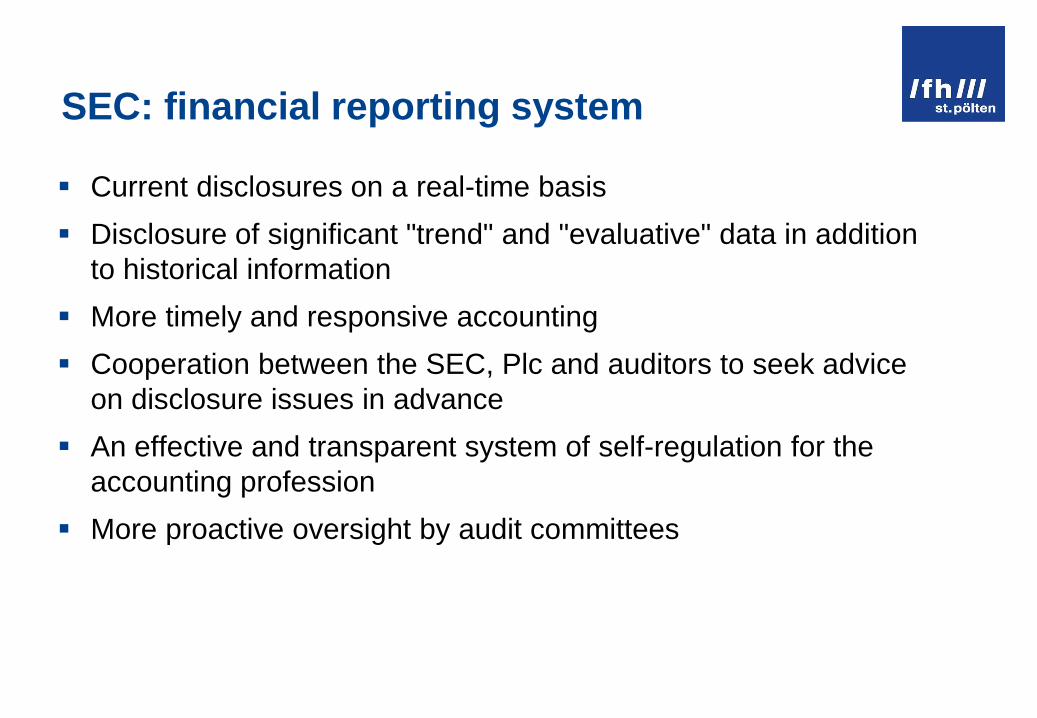

SEC: financial reporting system

Current disclosures on a real-time basis

Disclosure of significant "trend" and "evaluative" data in addition

to historical information

More timely and responsive accounting

Cooperation between the SEC, Plc and auditors to seek advice

on disclosure issues in advance

An effective and transparent system of self-regulation for the

accounting profession

More proactive oversight by audit committees

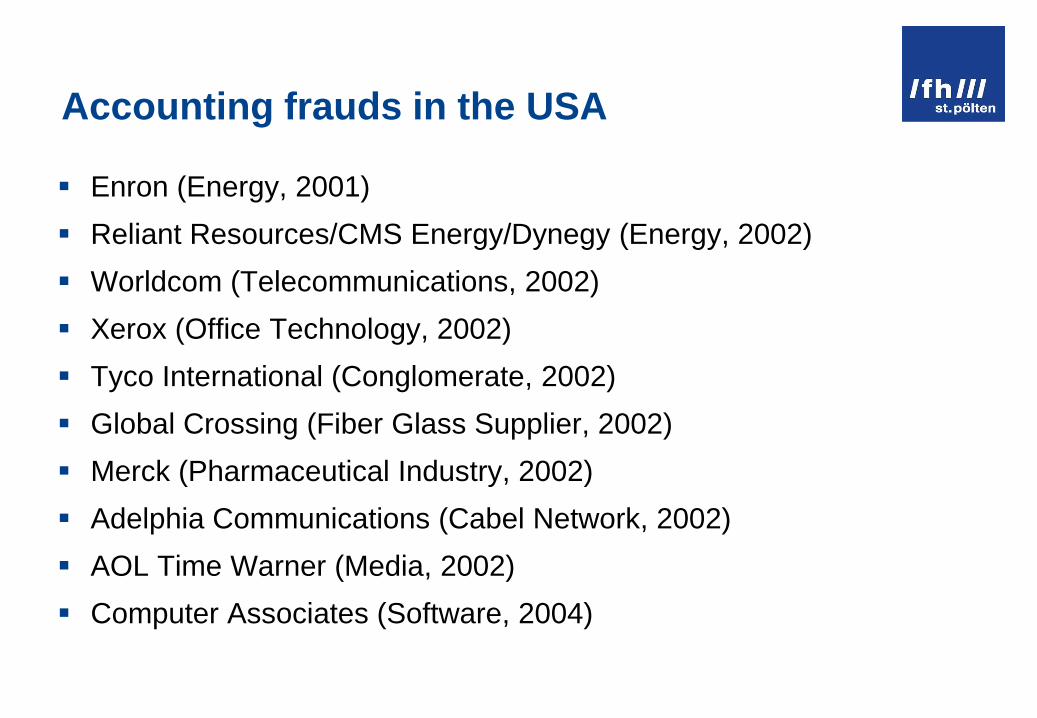

Accounting frauds in the USA

Enron (Energy, 2001)

Reliant Resources/CMS Energy/Dynegy (Energy, 2002)

Worldcom (Telecommunications, 2002)

Xerox (Office Technology, 2002)

Tyco International (Conglomerate, 2002)

Global Crossing (Fiber Glass Supplier, 2002)

Merck (Pharmaceutical Industry, 2002)

Adelphia Communications (Cabel Network, 2002)

AOL Time Warner (Media, 2002)

Computer Associates (Software, 2004)

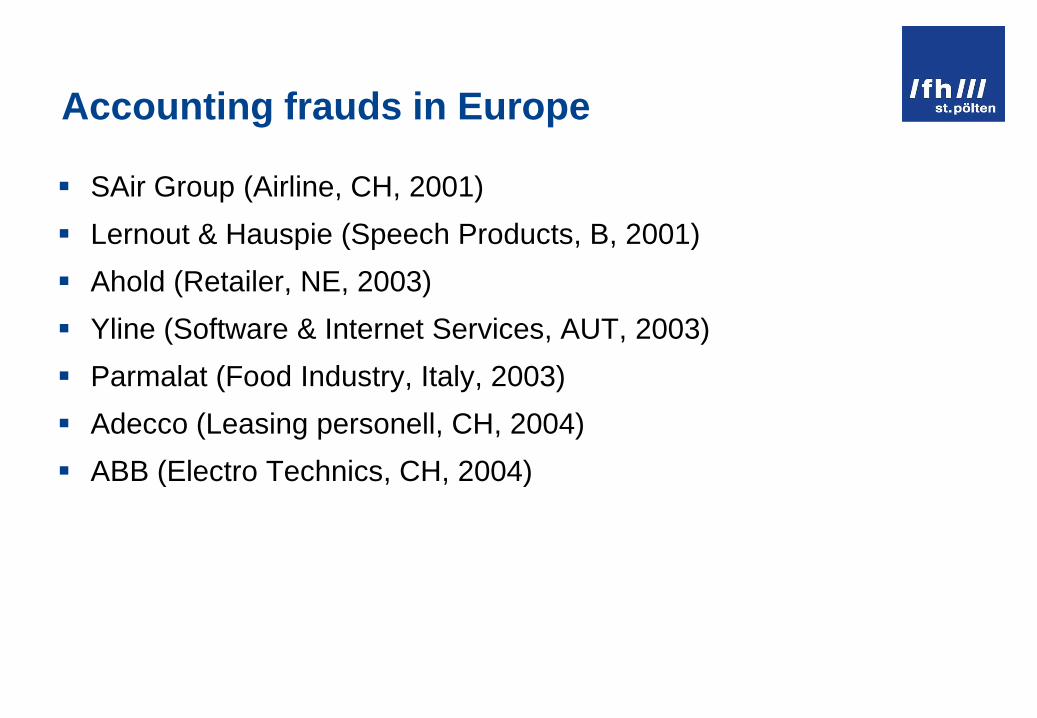

Accounting frauds in Europe

SAir Group (Airline, CH, 2001)

Lernout & Hauspie (Speech Products, B, 2001)

Ahold (Retailer, NE, 2003)

Yline (Software & Internet Services, AUT, 2003)

Parmalat (Food Industry, Italy, 2003)

Adecco (Leasing personell, CH, 2004)

ABB (Electro Technics, CH, 2004)

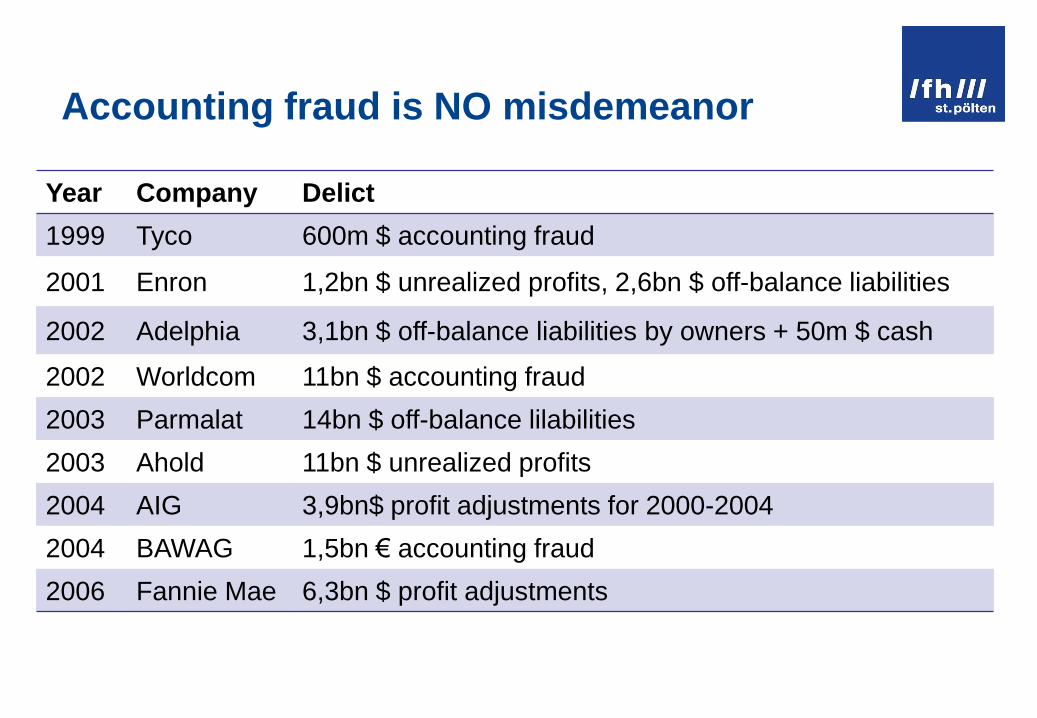

Accounting fraud is NO misdemeanor

Year Company Delict

1999 Tyco 600m $ accounting fraud

2001 Enron 1,2bn $ unrealized profits, 2,6bn $ off-balance liabilities

2002 Adelphia 3,1bn $ off-balance liabilities by owners + 50m $ cash

2002 Worldcom 11bn $ accounting fraud

2003 Parmalat 14bn $ off-balance lilabilities

2003 Ahold 11bn $ unrealized profits

2004 AIG 3,9bn$ profit adjustments for 2000-2004

2004 BAWAG 1,5bn € accounting fraud

2006 Fannie Mae 6,3bn $ profit adjustments

How to handle the risk of unethical business?

Law and regulatory frameworks are a necessary element

to reduce unethical behavior such as corruption, misleading

intransparency, fraud etc.

Corporations must apply the law and set up proper risk

management, internal control and transparency

systems to

avoid proactively the occurrence of unethical behavior

find out early enough if unethical actions is being set

prosecute criminal activities

Regulatory frameworks

Federal Corporate Sentencing Guidelines (FCSG),1991 –

establish requirements for corporate ethics programm

Environmental Protection Act, 1995

Sarbenes-Oxley-Act (SOX), 2002

increased the transparency and the accuracy of financial information

increased the independence of the outside auditors who review the

accuracy of corporate financial statements and

increased the oversight role of boards of directors

Corporate Governance Codex, Finland 2010

Being ethical is expensive…

Critisism of the current way to manage the risk of unethical

business such as

high level of bureauracy and thus deceleration of processes

high costs of transparency and documentation (compliance is reckoned

to cost 3%-5% of total sales)

But if you think, being

ethical is expensive,

try unethical.

Punishment of unethical behavior 1

At individual level - imprisonment:

Enron:

Ben Glison (Accountant) – 5 years

Adrew Fastow (CFO) – 6 years + 2 years social work

Jeff Skilling (CEO) – 24 years and 4 months

Worldcom:

Bernie Ebbers (CEO): 25 years, max. reduction of 3 years

Tyco:

Dennis Kozlowski (CEO): 8 years

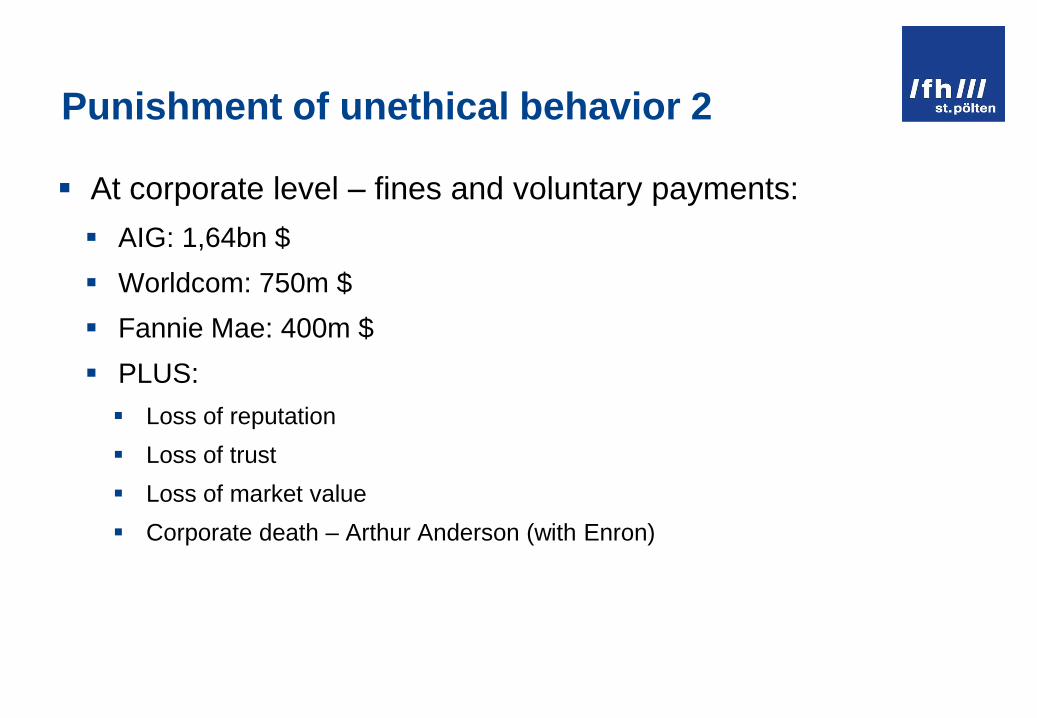

Punishment of unethical behavior 2

At corporate level – fines and voluntary payments:

AIG: 1,64bn $

Worldcom: 750m $

Fannie Mae: 400m $

PLUS:

Loss of reputation

Loss of trust

Loss of market value

Corporate death – Arthur Anderson (with Enron)

Many thanks for your attention