business cycles economics 210c

TRANSCRIPT

GROSS DOMESTIC PRODUCT (GDP)

050

0010

000

1500

020

000

Billio

ns o

f Cha

ined

200

9 D

olla

rs

1950 1960 1970 1980 1990 2000 2010

Real GDP

Growth Theory: RGDP keeps going up over time.Business Cycle analysis: cyclical fluctuations in RGDP about thelong-run trend.

1 / 28

GDP GROWTH RATE

-50

510

15Pe

rcen

t

1950 1960 1970 1980 1990 2000 2010

Annual Change in Real GDP

2 / 28

POTENTIAL VS. ACTUAL OUTPUT

1200

013

000

1400

015

000

1600

017

000

Billio

ns o

f Cha

ined

200

9 D

olla

rs

2000 2002 2004 2006 2008 2010 2012 2014 2016

Real GDP Potential Real GDP

Real GDP and Potential Real GDP

3 / 28

WHY DO WE CARE ABOUT RECESSIONS?

Recessions appear to be costly. Just read the newspapers when we aregoing through one.

Micro studies suggest very large income losses when laid off in arecession (e.g., Oreopoulus, von Wachter, Heisz, 2012; Guvenen,Ozkan, Song, 2014).

Belief that recessions could be prevented or, at least, mitigated.

Theoretically interesting: why are we operating inside the PPF? Ordid the PPF shift inward? If so, why?

4 / 28

METHODOLOGICAL APPROACH

Measurement

Model

Model evaluation

Policy implications

5 / 28

SOME FACTS ABOUT US RECESSIONS

How the National Bureau of Economic Research (NBER) identifies U.S.recessions:

We identify a month when the economy reached a peak ofactivity and a later month when the economy reached a trough.The time in between is a recession, a period when the economyis contracting. The following period is an expansion. Economicactivity is below normal or diminished for some part of therecession and for some part of the following expansion as well.

Simple Stylized Facts:

1 Recessions are varied in length and depth

2 Recessions are unpredictable

3 Recessions are becoming less frequent

6 / 28

SOME FACTS ABOUT US RECESSIONS

Recessions across time:

1854-1919:16 cycles: 4.1 years per cycleAverage length of recession: 22 months

1919-1945:6 cycles: 4.3 years per cycleAverage length of recession: 18 months

1945-present:11 cycles: 6.1 years per cycleAverage length of recession: 11 months

7 / 28

RECESSIONS IN THE USA SINCE WWII

Year and quarter ofpeak in real GDP

Number ofquarters until

trough in real GDP

Change in realGDP, peak to

trough

1948:4 2 -1.7%1953:2 3 -2.6%1957:3 2 -3.7%1960:1 3 -1.6%1970:3 1 -1.1%1973:4 5 -3.2%1980:1 2 -2.2%1981:3 2 -2.9%1990:2 3 -1.4%2000:4 1 -0.3%2008:2 4 -3.8%

8 / 28

WHAT HAPPENS DURING A RECESSION

Key things to look for:

1 Co-movement of variables (pro-cyclical vs counter-cylical)

2 Lead-lag patterns

Key variables we care about:

1 Real GDP

2 Consumption and Investment

3 Prices

4 Unemployment

5 Nominal Interest Rates

6 Real Wages

9 / 28

INVESTMENT IS MUCH MORE VOLATILE THAN

CONSUMPTION-2

00

2040

60Pe

rcen

t

1950 1960 1970 1980 1990 2000 2010

Consumption Investment

Annual Change in Real Consumption and Investment

10 / 28

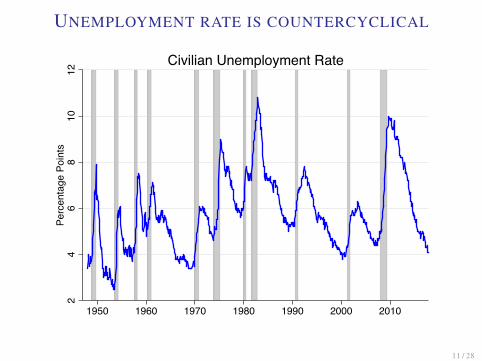

UNEMPLOYMENT RATE IS COUNTERCYCLICAL

24

68

1012

Perc

enta

ge P

oint

s

1950 1960 1970 1980 1990 2000 2010

Civilian Unemployment Rate

11 / 28

INFLATIONS RISES BEFORE AND FALLS DURING/AFTER

RECESSIONS-5

05

1015

Percent

1950 1960 1970 1980 1990 2000 2010

Inflation

12 / 28

SECTORAL COMOVEMENT

-20

-10

010

20Pe

rcen

t

1950 1960 1970 1980 1990 2000 2010

Construction ServicesNondurable Durable

Sectoral Comovement

13 / 28

PRODUCTIVITY

-20

24

68

Perc

ent

1950 1960 1970 1980 1990 2000 2010

Annual Change in Productivity

14 / 28

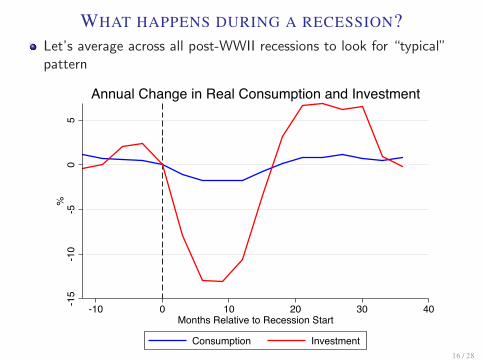

WHAT HAPPENS DURING A RECESSION?Let’s average across all post-WWII recessions to look for “typical”pattern

-4-2

02

%

-10 0 10 20 30 40Months Relative to Recession Start

Annual Change in Real GDP

15 / 28

WHAT HAPPENS DURING A RECESSION?Let’s average across all post-WWII recessions to look for “typical”pattern

-15

-10

-50

5%

-10 0 10 20 30 40Months Relative to Recession Start

Consumption Investment

Annual Change in Real Consumption and Investment

16 / 28

WHAT HAPPENS DURING A RECESSION?Let’s average across all post-WWII recessions to look for “typical”pattern0

.51

1.5

22.

5%

Poi

nts

Rel

ativ

e to

Rec

essi

on S

tart

-10 0 10 20 30 40Months Relative to Recession Start

Civilian Unemployment Rate

17 / 28

WHAT HAPPENS DURING A RECESSION?Let’s average across all post-WWII recessions to look for “typical”pattern

-2.5

-2-1

.5-1

-.50

% R

elat

ive

to R

eces

sion

Sta

rt

-10 0 10 20 30 40Months Relative to Recession Start

Inflation

18 / 28

WHAT HAPPENS DURING A RECESSION?Let’s average across all post-WWII recessions to look for “typical”pattern

-4-3

-2-1

0%

Poi

nts

Rel

ativ

e to

Rec

essi

on S

tart

-10 0 10 20 30 40Months Relative to Recession Start

Nominal Interest Rate

19 / 28

WHAT HAPPENS DURING A RECESSION?Let’s average across all post-WWII recessions to look for “typical”pattern

-.50

.51

1.5

%

-10 0 10 20 30 40Months Relative to Recession Start

Annual Change in Real Compensation per Hour

20 / 28

WHAT HAPPENS DURING A RECESSION?

Source: Guvenen, Ozkan, Song, 2014.

21 / 28

WHAT HAPPENS DURING A RECESSION?

Source: Guvenen, Ozkan, Song, 2014.

22 / 28

TYPICAL PATTERN

1 Real GDP declines.

2 Consumption growth slows and investment declines a lot.

3 Inflation is rising before recessions and falls gradually duringrecessions.

4 Unemployment goes up about 2 percentage points, and declinesslowly.

5 Nominal interest rates rise before the recession, but fall rapidly duringa recession.

6 Real wages decline slightly.

7 Higher incidence of large negative income shocks.

23 / 28

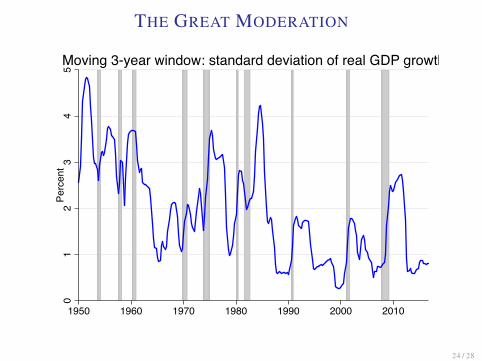

THE GREAT MODERATION

01

23

45

Perc

ent

1950 1960 1970 1980 1990 2000 2010

Moving 3-year window: standard deviation of real GDP growth

24 / 28

POSSIBLE EXPLANATIONS

1 Luck

2 Better policies (more aggressive response to inflation, reduce the levelof inflation)

3 Better inventory management

4 Decline in unionization

5 Redistribution of jobs

6 Banking deregulation

25 / 28

SUMMARY OF BUSINESS CYCLE FACTS

1 Business cycles do not exhibit any simple regular or cyclical pattern.

2 Sectoral outputs and most macroeconomic variables co-move over thebusiness cycle.

3 Fluctuations are distributed very unevenly across components ofoutput:

I consumption is 50% less volatile than output

I labor and output are approximately equally volatile - investment is2.5-3 times more volatile than output

4 Rises and falls in output are frequently observed. However,contractions are faster than expansions.

5 Aggregate volatility seems to have been falling/low.

6 Idiosyncratic volatility does not vary with business cycle, but skewnessincreases in recessions.

26 / 28

“BIG QUESTIONS” IN BUSINESS CYCLES

1 What are the shocks causing business cycles?

2 What are the propagation/amplification mechanisms behind shocks?

3 What is the relationship between business cycles and long-run growth?

4 What is the cost of business cycles?

5 What policy can reduce the cost?

27 / 28

OUR GOAL:

1 Build a model of the economy that can simultaneously explain thebehavior of RGDP, inflation, UE,...

2 Use this model to shed light on what causes recessions and thebusiness cycle.

3 Once we’ve identified the types of shocks that can cause businesscycle fluctuations, we can use the model to figure out howpolicy-makers can/should respond to economic fluctuations.

28 / 28