bulletin no. 2006-15 highlights of this issue of this issue ... any argument that forms w–2 ......

TRANSCRIPT

Bulletin No. 2006-15April 10, 2006

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

INCOME TAX

Rev. Rul. 2006–14, page 740.Low-income housing credit; satisfactory bond; “bondfactor” amounts for the period January through June2006. This ruling provides the monthly bond factor amountsto be used by taxpayers who dispose of qualified low-incomebuildings or interests therein during the period January throughJune 2006.

Rev. Rul. 2006–17, page 748.Frivolous tax returns; “nunc pro tunc.” This ruling empha-sizes to taxpayers, promoters, and return preparers that insert-ing the phrase “nunc pro tunc” on a return or other documentsubmitted to the Service has no legal effect and does not val-idate an invalid return, make a delinquent return timely, invali-date a signature, create a claim for refund of taxes previouslypaid, or reduce one’s federal tax liability.

Rev. Rul. 2006–18, page 743.Frivolous tax returns; only certain persons subject tofederal income tax. This ruling emphasizes to taxpayers,promoters, and return preparers that all individuals are sub-ject to federal income tax. Any argument that Forms W–2only record and report payments made to federal employees,or that only federal employees or residents of the District ofColumbia or federal territories and enclaves earn wages sub-ject to tax, has no merit and is frivolous.

Rev. Rul. 2006–19, page 749.Frivolous tax returns; use of sham trusts. This ruling em-phasizes that an individual cannot escape taxation by attribut-ing income to a purported trust. The Service will take vigor-ous enforcement action against frivolous arguments relating totrusts.

Rev. Rul. 2006–20, page 746.Frivolous tax returns; “Native American Treaty.” This rul-ing emphasizes to taxpayers, promoters, and return preparersthat there is no right to exemption from federal income taxfor Native Americans under an unspecified “Native AmericanTreaty.” Any return position based on an unspecified “NativeAmerican Treaty” has no merit and is frivolous. As a generalrule, Native Americans are subject to federal income tax justlike every other American.

Rev. Rul. 2006–21, page 745.Frivolous tax returns; reliance on Paperwork ReductionAct. This ruling emphasizes to taxpayers, promoters, and re-turn preparers that taxpayers are required to file a federal in-come tax return under section 6012 of the Code, and the reg-ulations thereunder, and that the Paperwork Reduction Act of1980 (PRA) does not relieve taxpayers of the duty to file. Anyargument that the PRA relieves the taxpayer of the duty to filean income tax return has no merit and is frivolous.

T.D. 9255, page 741.REG–164247–05, page 758.Final, temporary, and proposed regulations under section 1502of the Code provide the IRS with the authority to designate a do-mestic member of a consolidated group as a substitute agentto act as the sole agent for the group where the common par-ent is a foreign entity that is treated as a domestic corporationpursuant to section 7874(b) or as the result of a section 953(d)election.

(Continued on the next page)

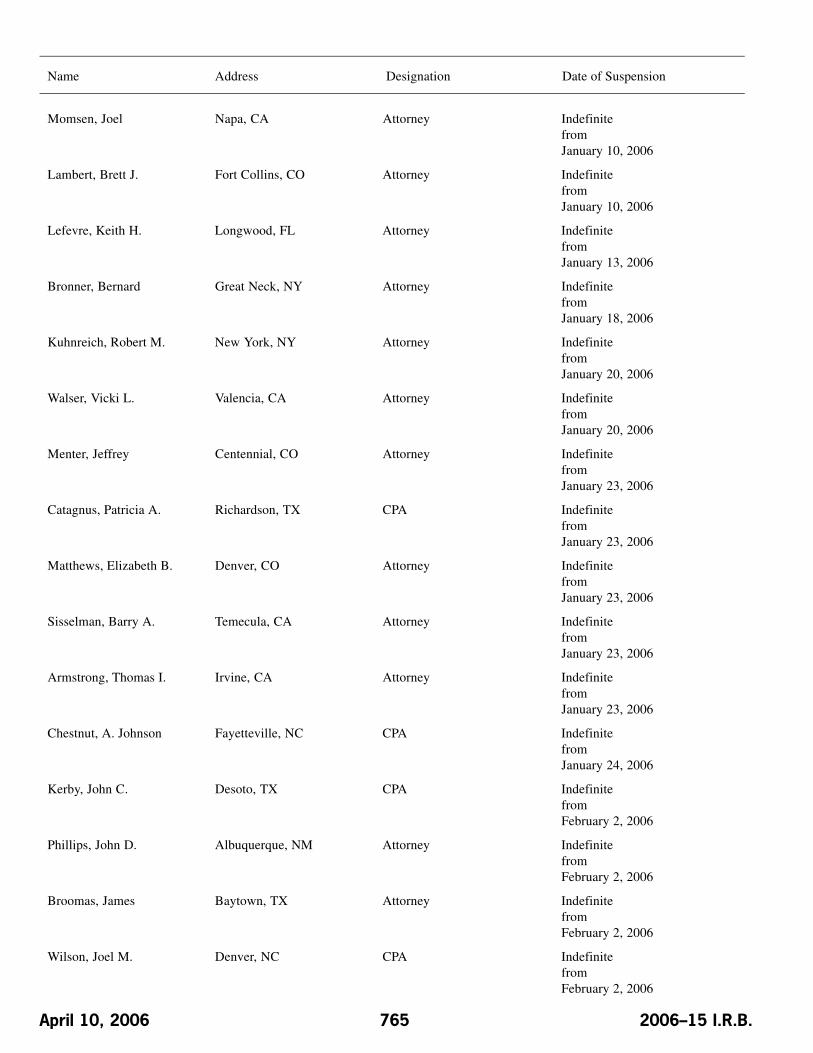

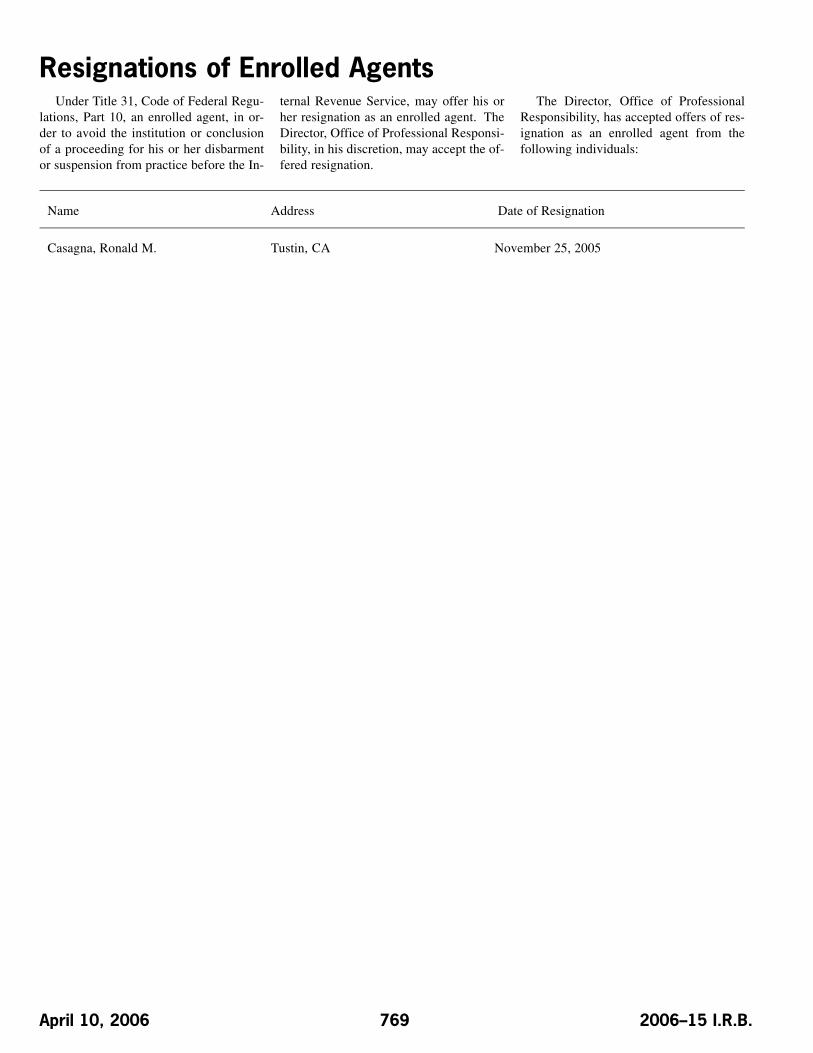

Announcements of Disbarments and Suspensions begin on page 758.Finding Lists begin on page ii.

Notice 2006–31, page 751.This notice sets out some of the most common frivolous argu-ments and schemes that taxpayers use to avoid their tax obli-gations. It also identifies civil and criminal penalties that theService may impose against taxpayers who engage in abusivetax-avoidance schemes. Notice 2005–30 modified and super-seded.

Notice 2006–33, page 754.This notice provides transition guidance on the application ofsection 409A(b) of the Code to outstanding offshore trusts as-sociated with nonqualified deferred compensation, as well asnonqualified deferred compensation arrangements providingthat assets will become restricted to the payment of benefitsunder the plan in connection with a change in the employer’sfinancial health.

ADMINISTRATIVE

Rev. Rul. 2006–17, page 748.Frivolous tax returns; “nunc pro tunc.” This ruling empha-sizes to taxpayers, promoters, and return preparers that insert-ing the phrase “nunc pro tunc” on a return or other documentsubmitted to the Service has no legal effect and does not val-idate an invalid return, make a delinquent return timely, invali-date a signature, create a claim for refund of taxes previouslypaid, or reduce one’s federal tax liability.

Rev. Rul. 2006–18, page 743.Frivolous tax returns; only certain persons subject tofederal income tax. This ruling emphasizes to taxpayers,promoters, and return preparers that all individuals are sub-ject to federal income tax. Any argument that Forms W–2only record and report payments made to federal employees,or that only federal employees or residents of the District ofColumbia or federal territories and enclaves earn wages sub-ject to tax, has no merit and is frivolous.

Rev. Rul. 2006–19, page 749.Frivolous tax returns; use of sham trusts. This ruling em-phasizes that an individual cannot escape taxation by attribut-ing income to a purported trust. The Service will take vigor-ous enforcement action against frivolous arguments relating totrusts.

Rev. Rul. 2006–20, page 746.Frivolous tax returns; “Native American Treaty.” This rul-ing emphasizes to taxpayers, promoters, and return preparersthat there is no right to exemption from federal income taxfor Native Americans under an unspecified “Native AmericanTreaty.” Any return position based on an unspecified “NativeAmerican Treaty” has no merit and is frivolous. As a generalrule, Native Americans are subject to federal income tax justlike every other American.

Rev. Rul. 2006–21, page 745.Frivolous tax returns; reliance on Paperwork ReductionAct. This ruling emphasizes to taxpayers, promoters, and re-turn preparers that taxpayers are required to file a federal in-come tax return under section 6012 of the Code, and the reg-ulations thereunder, and that the Paperwork Reduction Act of1980 (PRA) does not relieve taxpayers of the duty to file. Anyargument that the PRA relieves the taxpayer of the duty to filean income tax return has no merit and is frivolous.

Notice 2006–31, page 751.This notice sets out some of the most common frivolous argu-ments and schemes that taxpayers use to avoid their tax obli-gations. It also identifies civil and criminal penalties that theService may impose against taxpayers who engage in abusivetax-avoidance schemes. Notice 2005–30 modified and super-seded.

Notice 2006–36, page 756.Public comments are requested on recommendations for itemsthat should be included on the 2006–2007 Guidance PriorityList. Taxpayers may submit recommendations for guidanceat any time during the year. Recommendations submitted byMay 15, 2006, will be reviewed for possible inclusion on theoriginal 2006–2007 Guidance Priority List. Recommendationsreceived after May 15, 2006, will be reviewed for inclusion inthe next periodic update.

April 10, 2006 2006–15 I.R.B.

The IRS MissionProvide America’s taxpayers top quality service by helpingthem understand and meet their tax responsibilities and by

applying the tax law with integrity and fairness to all.

IntroductionThe Internal Revenue Bulletin is the authoritative instrument ofthe Commissioner of Internal Revenue for announcing officialrulings and procedures of the Internal Revenue Service and forpublishing Treasury Decisions, Executive Orders, Tax Conven-tions, legislation, court decisions, and other items of generalinterest. It is published weekly and may be obtained from theSuperintendent of Documents on a subscription basis. Bulletincontents are compiled semiannually into Cumulative Bulletins,which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform application ofthe tax laws, including all rulings that supersede, revoke, mod-ify, or amend any of those previously published in the Bulletin.All published rulings apply retroactively unless otherwise indi-cated. Procedures relating solely to matters of internal man-agement are not published; however, statements of internalpractices and procedures that affect the rights and duties oftaxpayers are published.

Revenue rulings represent the conclusions of the Service on theapplication of the law to the pivotal facts stated in the revenueruling. In those based on positions taken in rulings to taxpayersor technical advice to Service field offices, identifying detailsand information of a confidential nature are deleted to preventunwarranted invasions of privacy and to comply with statutoryrequirements.

Rulings and procedures reported in the Bulletin do not have theforce and effect of Treasury Department Regulations, but theymay be used as precedents. Unpublished rulings will not berelied on, used, or cited as precedents by Service personnel inthe disposition of other cases. In applying published rulings andprocedures, the effect of subsequent legislation, regulations,

court decisions, rulings, and procedures must be considered,and Service personnel and others concerned are cautionedagainst reaching the same conclusions in other cases unlessthe facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisions ofthe Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions and Other Related Items, and Subpart B, Leg-islation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references to thesesubjects are contained in the other Parts and Subparts. Alsoincluded in this part are Bank Secrecy Act Administrative Rul-ings. Bank Secrecy Act Administrative Rulings are issued bythe Department of the Treasury’s Office of the Assistant Sec-retary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative indexfor the matters published during the preceding months. Thesemonthly indexes are cumulated on a semiannual basis, and arepublished in the last Bulletin of each semiannual period.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

2006–15 I.R.B. April 10, 2006

Part I. Rulings and Decisions Under the Internal Revenue Codeof 1986Section 42.—Low-IncomeHousing Credit

Low-income housing credit; satisfac-tory bond; “bond factor” amounts forthe period January through June 2006.This ruling provides the monthly bond fac-tor amounts to be used by taxpayers whodispose of qualified low-income buildingsor interests therein during the period Jan-uary through June 2006.

Rev. Rul. 2006–14

In Rev. Rul. 90–60, 1990–2 C.B.3, the Internal Revenue Service provided

guidance to taxpayers concerning the gen-eral methodology used by the TreasuryDepartment in computing the bond factoramounts used in calculating the amount ofbond considered satisfactory by the Secre-tary under § 42(j)(6) of the Internal Rev-enue Code. It further announced that theSecretary would publish in the InternalRevenue Bulletin a table of bond factoramounts for dispositions occurring duringeach calendar month.

Rev. Proc. 99–11, 1999–1 C.B. 275,established a collateral program as an al-ternative to providing a surety bond fortaxpayers to avoid or defer recapture of

the low-income housing tax credits under§ 42(j)(6). Under this program, taxpayersmay establish a Treasury Direct Accountand pledge certain United States Treasurysecurities to the Internal Revenue Serviceas security.

This revenue ruling provides in Table1 the bond factor amounts for calculatingthe amount of bond considered satisfactoryunder § 42(j)(6) or the amount of UnitedStates Treasury securities to pledge in aTreasury Direct Account under Rev. Proc.99–11 for dispositions of qualified low-in-come buildings or interests therein duringthe period January through June 2006.

Table 1Rev. Rul. 2006–14

Monthly Bond Factor Amounts for Dispositions ExpressedAs a Percentage of Total Credits

Calendar Year Building Placed in Serviceor, if Section 42(f)(1) Election Was Made,

the Succeeding Calendar Year

Month ofDisposition

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Jan ’06 16.49 30.74 43.01 53.65 62.94 64.28 65.95 67.76 69.76 72.19 74.98Feb ’06 16.49 30.74 43.01 53.65 62.94 64.14 65.81 67.62 69.61 72.03 74.80Mar ’06 16.49 30.74 43.01 53.65 62.94 64.00 65.67 67.47 69.46 71.89 74.63Apr ’06 16.49 30.74 43.01 53.65 62.94 63.87 65.53 67.33 69.32 71.73 74.46May ’06 16.49 30.74 43.01 53.65 62.94 63.73 65.40 67.20 69.18 71.58 74.30Jun ’06 16.49 30.74 43.01 53.65 62.94 63.61 65.27 67.06 69.05 71.44 74.15

Table 1 (cont’d)Rev. Rul. 2006–14

Monthly Bond Factor Amounts for Dispositions ExpressedAs a Percentage of Total Credits

Calendar Year Building Placed in Serviceor, if Section 42(f)(1) Election Was Made,

the Succeeding Calendar Year

Month ofDisposition

2003 2004 2005 2006

Jan ’06 78.01 81.02 83.60 83.98Feb ’06 77.81 80.77 83.28 83.98Mar ’06 77.61 80.53 83.00 83.98Apr ’06 77.42 80.32 82.76 83.98May ’06 77.25 80.12 82.54 83.98Jun ’06 77.08 79.93 82.35 83.98

2006–15 I.R.B. 740 April 10, 2006

For a list of bond factor amounts ap-plicable to dispositions occurring duringother calendar years, see: Rev. Rul. 98–3,1998–1 C.B. 248; Rev. Rul. 2001–2,2001–1 C.B. 255; Rev. Rul. 2001–53,2001–2 C.B. 488; Rev. Rul. 2002–72,2002–2 C.B. 759; Rev. Rul. 2003–117,2003–2 C.B. 1051; Rev. Rul. 2004–100,2004–2 C.B. 718; and Rev. Rul. 2005–67,2005–43 I.R.B. 771.

DRAFTING INFORMATION

The principal author of this revenueruling is David McDonnell of the Officeof Associate Chief Counsel (Passthroughsand Special Industries). For further in-formation regarding this revenue ruling,contact Mr. McDonnell at (202) 622–3040(not a toll-free call).

Section 1502.—Regulations26 CFR 1.1502–77: Agent for the group.

T.D. 9255

DEPARTMENT OFTHE TREASURYInternal Revenue Service26 CFR Part 1

Agent for a ConsolidatedGroup With Foreign CommonParent

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final and temporary regula-tions.

SUMMARY: This document contains tem-porary regulations under section 1502 thatprovide the IRS with the authority to des-ignate a domestic member of the consol-idated group as a substitute agent to actas the sole agent for the group where aforeign entity is the common parent. Theregulations affect corporations that join inthe filing of a consolidated Federal in-come tax return where the common par-ent of the consolidated group is a foreignentity that is treated as a domestic corpo-ration pursuant to section 7874(b) of theInternal Revenue Code (Code) or as theresult of a section 953(d) election. Thetext of these temporary regulations also

serves as the text of the proposed regu-lations (REG–164247–05) set forth in thenotice of proposed rulemaking on this sub-ject in this issue of the Bulletin.

DATES: Effective Date: These regulationsare effective March 14, 2006.

Applicability Dates: These regulationsapply to taxable years for which the duedate (without extensions) for filing returnsis after March 14, 2006. The applicabilityof these regulations will expire on or be-fore March 10, 2009.

FOR FURTHER INFORMATIONCONTACT: Stephen R. Cleary, (202)622–7750, (not a toll-free number).

SUPPLEMENTARY INFORMATION:

Background and Explanation ofProvisions

Section 1504(b)(3) of the Internal Rev-enue Code of 1986 (Code) excludes for-eign corporations from the definition of“includible corporation.” As a result, a for-eign entity generally cannot be a memberof a consolidated group. In certain cases,section 7874 treats a foreign entity as a do-mestic corporation and section 953(d) al-lows a foreign insurance company to makean election to be treated as a domestic cor-poration. As a result, a foreign entity couldbe the common parent or a subsidiary ofa consolidated group if it is treated as adomestic corporation under either section7874(b) or section 953(d).

Under §1.1502–77(a)(1)(i) of the regu-lations, the common parent for a consoli-dated return year is generally the sole agent(agent for the group) that is authorized toact in its own name with respect to all mat-ters relating to the tax liability for that con-solidated return year for each member ofthe group, and any successor of a mem-ber (as defined in §1.1502–77(a)(1)(iii)).The common parent’s agency for a con-solidated return year generally continuesuntil the common parent ceases to exist,regardless of whether any subsidiaries inthat year cease to be members of the group,whether the group files a consolidated re-turn in any later year, or whether the com-mon parent ceases to be the common par-ent or a member of the group in a later year.Section 1.1502–77(d) provides rules fordesignating a substitute agent if the com-mon parent’s existence terminates.

The IRS and Treasury Department be-lieve that it may not always be practicalor efficient for tax administration to havea foreign entity act as the agent for thegroup. Accordingly, where a foreign entityis the common parent because it is treatedas a domestic corporation by reason of sec-tion 7874 or a section 953(d) election (aForeign Common Parent), the temporaryregulations provide the IRS with the au-thority to designate a domestic member ofthe group to be the sole agent (a DomesticSubstitute Agent) even though the group’scommon parent continues in existence.

These temporary regulations provideflexibility in the method of communicationthe IRS may use to designate a DomesticSubstitute Agent, allowing notification bymail or by faxed transmission. In addition,these regulations provide specificity forthe determination of the effective date ofthe designation of a Domestic SubstituteAgent: the designation is effective on theearliest of the 14th day following the dateof a mailing, the 4th day following a faxedtransmission, or the date the Commis-sioner receives written confirmation of thedesignation by a duly authorized officer ofthe designated agent, within the meaningof section 6062.

Special Analyses

It has been determined that these tem-porary regulations are not a significant reg-ulatory action as defined in Executive Or-der 12866. Therefore, a regulatory as-sessment is not required. It has been de-termined, pursuant to 5 U.S.C. 553(b)(B),that good cause exists for dispensing withthe notice and public comment proceduresand that, pursuant to 5 U.S.C. 553(d)(3),good cause exists to dispense with a de-layed effective date. The regulations arenecessary to allow the IRS to avoid po-tentially serious tax administration prob-lems that may arise when a foreign entity isthe agent for a consolidated group, and toprovide immediate guidance to taxpayersregarding the IRS’ authority to designatea substitute agent for the group in such acase. For applicability of the RegulatoryFlexibility Act (5 U.S.C. chapter 6), referto the Special Analysis section of the No-tice of Proposed Rulemaking published inthis issue of the Bulletin. Pursuant to sec-tion 7805(f) of the Code, these temporaryregulations will be submitted to the Chief

April 10, 2006 741 2006–15 I.R.B.

Counsel for Advocacy of the Small Busi-ness Administration for comment on theirimpact on small business.

Drafting Information

The principal author of these regula-tions is Stephen R. Cleary of the Officeof Associate Chief Counsel (Corporate).Other personnel from the Treasury Depart-ment and the IRS participated in their de-velopment.

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR part 1 is amendedas follows:

PART 1—INCOME TAXES

Paragraph 1. The authority citation forpart 1 is amended by adding entries in nu-merical order to read as follows:

Authority: 26 U.S.C. 7805 * * *Section 1.1502–77T also issued under

26 U.S.C. 1502 * * *Par. 2. Section 1.1502–77 is amended

by adding and reserving paragraph (i) andadding paragraph (j) to read as follows:

§1.1502–77 Agent for the group.

* * * * *(i) [Reserved](j) Designation by Commissioner if

common parent is treated as a domesticcorporation under section 7874 or section953(d) [Reserved]. For further guidance,see §1.1502–77T(j).

Par. 3. Section 1.1502–77T is added toread as follows:

§1.1502–77T Agent for the group(temporary).

(a) through (i) [Reserved]. For furtherguidance, see §1.1502–77(a) through (i).

(j) Designation by Commissioner ifcommon parent is treated as a domesticcorporation under section 7874 or section953(d)—(1) In general. If the commonparent is an entity created or organizedunder the law of a foreign country and istreated as a domestic corporation by reasonof section 7874 (or regulations thereun-der) or a section 953(d) election (a ForeignCommon Parent), the Commissioner may

at any time, with or without a requestfrom any member of the group, designateanother member of the group to act as theagent for the group (a Domestic SubstituteAgent) for any taxable year for which thedue date (without extensions) for filingreturns is after March 14, 2006 and theForeign Common Parent would other-wise be the agent for the group. For eachsuch year, the Domestic Substitute Agentwill be the sole agent for the group eventhough the Foreign Common Parent re-mains in existence. The Foreign CommonParent ceases to be the agent for the groupwhen the Commissioner’s designation ofa Domestic Substitute Agent becomes ef-fective. The Commissioner may designatea Domestic Substitute Agent for the termof a single taxable year, multiple years, oron a continuing basis.

(2) Domestic Substitute Agent. The Do-mestic Substitute Agent, by designation orby succession, shall be a domestic corpora-tion described in §1.1502–77(d)(1)(i)(A)(determined without regard to section7874, a section 953(d) election, section269B, or section 1504(d)).

(3) Designation by the Commissioner.The Commissioner will notify the Domes-tic Substitute Agent in writing by mail orfaxed transmission of the designation. TheDomestic Substitute Agent’s designationis effective on the earliest of the 14th dayfollowing the date of a mailing, the 4th dayfollowing a faxed transmission, or the datethe Commissioner receives written confir-mation of the designation by a duly au-thorized officer of the Domestic Substi-tute Agent (within the meaning of section6062). The Domestic Substitute Agentmust give notice of its designation to theForeign Common Parent and each corpo-ration that was a member of the groupduring any part of any consolidated re-turn year for which the Domestic Substi-tute Agent will be the agent. A failureof the Domestic Substitute Agent to notifythe Foreign Common Parent or any mem-ber of the group does not invalidate thedesignation. The Commissioner will senda copy of the notification to the ForeignCommon Parent, and if applicable, to anyDomestic Substitute Agent the designationreplaces; a failure to send a copy of the no-tification does not invalidate the designa-tion.

(4) Term of agency—(i) In general. Ifthe Commissioner designates a Domestic

Substitute Agent for a taxable year, theDomestic Substitute Agent will remain theagent for such year until the group ceasesto exist or the Domestic Substitute Agentceases to exist, ceases to be a member ofthe group, is replaced by a successor, or isreplaced by the Commissioner. This de-signee remains the agent for such year re-gardless of whether one or more corpora-tions that were members of the group dur-ing any part of such year cease to be mem-bers of the group, whether the group filesa consolidated return for any subsequentyear, or, except as provided by paragraphs(j)(4)(iv)(B) and (j)(4)(v) of this section,whether the group remains in existencewith a new common parent in any subse-quent year.

(ii) Agency of Domestic SubstituteAgent upon termination of the group. Ifthe Domestic Substitute Agent is the agentfor the group for a year in which the groupterminates, the Domestic Substitute Agentshall be the agent for that taxable year(and any prior taxable year for which itis the agent for the group) so long as theDomestic Substitute Agent continues itscorporate existence unless it is replacedby a successor or a new designee by theCommissioner.

(iii) Replacement of §1.1502–77(d)(1)agent. If, pursuant to §1.1502–77(d)(1),the common parent of the group designatesa Foreign Common Parent as the agent forthe group for any taxable year, the Com-missioner may, at any time, designate aDomestic Substitute Agent to replace theForeign Common Parent, even if the Com-missioner approved the terminating com-mon parent’s designation.

(iv) Group continues with a new com-mon parent—(A) Year the new commonparent becomes the common parent. Ifsubsequent to a transaction to which sec-tion 7874 applies or a section 953(d) elec-tion, the group remains in existence witha new common parent and such new com-mon parent is a domestic corporation (de-termined without regard to section 7874, asection 953(d) election, or section 269B),such new common parent will become theagent for the group with respect to the en-tire consolidated return year (including theportion of the year preceding the date onwhich the new common parent became thecommon parent)) and the former Domes-tic Substitute Agent will no longer be theagent for the group for any part of that year.

2006–15 I.R.B. 742 April 10, 2006

(B) Years preceding the year the newcommon parent becomes the common par-ent. If after the Commissioner’s designa-tion of a Domestic Substitute Agent thegroup remains in existence with a newcommon parent, and such new commonparent is a domestic corporation (deter-mined without regard to section 7874, asection 953(d) election, or section 269B),the Commissioner may designate the newcommon parent as the agent for the groupfor any of the group’s prior taxable years(for which the due date (without exten-sions) for filing returns is after March 14,2006) in which the new common parentwas a member of the group. For this pur-pose, the new common parent is treated ashaving been a member of the group for anytaxable year it is primarily liable for thegroup’s income tax liability.

(v) Replacement of Domestic SubstituteAgent by the Commissioner. The Commis-sioner may at any time, with or withouta request from any member of the group,designate a replacement for a DomesticSubstitute Agent (or a successor to suchagent).

(5) Deemed §1.1502–77(d) designa-tion—(i) Section 1.1502–78 adjustments.If the Commissioner designates a Domes-tic Substitute Agent under this paragraph(j), it will be treated as a designation of asubstitute agent under §1.1502–77(d) forthe purposes of §1.1502–78.

(ii) Default Substitute Agent. If theDomestic Substitute Agent goes out ofexistence and has a single successor that iseligible to be a Domestic Substitute Agent,such successor becomes the DomesticSubstitute Agent and is treated as a defaultsubstitute agent under §1.1502–77(d)(2).See §1.1502–77(d)(4) regarding the con-sequences of the successor’s failure tonotify the Commissioner of its status asa default substitute agent. The defaultsubstitute agent shall use procedures insection 9 of Rev. Proc. 2002–43, 2002–2C.B. 99, or a corresponding provision ofa successor revenue procedure for noti-fication. (See §601.601(d)(2)(ii) of thischapter.)

(6) Request that IRS designate a Do-mestic Substitute Agent—(i) Originaldesignation. If the common parent of thegroup is a Foreign Common Parent, andthe IRS has not designated a DomesticSubstitute Agent, one or more membersof the group may request the IRS to make

a designation for taxable years for whichthe due date (without extensions) for fil-ing returns is after March 14, 2006. Suchrequest is deemed to be a request under§1.1502–77(d)(3)(i). Members of thegroup shall use the procedures in section10 of Rev. Proc. 2002–43, 2002–2 C.B.99, or a corresponding provision of a suc-cessor revenue procedure for this purpose.(See §601.601(d)(2)(ii) of this chapter.)

(ii) Request that IRS replace a pre-viously designated substitute agent. Ifthe IRS designates a Domestic SubstituteAgent pursuant to this paragraph (j), oneor more members of the group may re-quest that the IRS replace the designatedDomestic Substitute Agent with anothermember (or successor to another mem-ber). Such a request is deemed to be arequest pursuant to §1.1502–77(d)(3)(ii).Members of the group shall use the proce-dures in section 11 of Rev. Proc. 2002–43,2002–2 C.B. 99, or a corresponding pro-vision of a successor revenue procedurefor this purpose. (See §601.601(d)(2)(ii)of this chapter.)

(7) Effective Date. This paragraph (j)applies to taxable years for which the duedate (without extensions) for filing returnsis after March 14, 2006. The applicabilityof this paragraph (j) expires on or beforeMarch 10, 2009.

Mark E. Matthews,Deputy Commissioner forServices and Enforcement.

Approved March 9, 2006.

Eric Solomon,Acting Deputy Assistant

Secretary of the Treasury (Tax Policy).

(Filed by the Office of the Federal Register on March 9, 2006,4:15 p.m., and published in the issue of the Federal Registerfor March 14, 2006, 71 F.R. 13001)

Section 3401.—Definitions26 CFR 31.3401(c)–1: Employee.(Also Section 3401(a)–1.)

Frivolous tax returns; only certainpersons subject to federal income tax.This ruling emphasizes to taxpayers, pro-moters, and return preparers that all indi-viduals are subject to federal income tax.Any argument that Forms W–2 only recordand report payments made to federal em-ployees, or that only federal employees or

residents of the District of Columbia orfederal territories and enclaves earn wagessubject to tax, has no merit and is frivolous.

Rev. Rul. 2006–18

PURPOSE

The Service is aware that some taxpay-ers are claiming that only federal employ-ees and persons residing in Washington,D.C. or federal territories and enclavesare subject to federal tax. These tax-payers may attempt to avoid their fed-eral tax liability by submitting a Form4852 (Substitute for W–2, Wage and TaxStatement, or Form 1099-R, DistributionsFrom Pensions, Annuities, Retirement orProfit-Sharing Plans, IRAs, InsuranceContracts, etc.) to the Internal RevenueService with a zero on the line for theamount of wages received. These taxpay-ers may also file tax returns showing noincome and claiming a refund for withheldincome taxes. The Service is also awarethat some promoters market a book, pack-age, kit or other materials that claim toshow taxpayers how they can avoid pay-ing income taxes based on this and othermeritless arguments.

This revenue ruling emphasizes to tax-payers, promoters, and return preparersthat all individuals are subject to fed-eral income tax. This revenue rulingalso provides that the terms “employee”and “wages” carry the meanings givento them in the Internal Revenue Code,regulations, and publications of the Inter-nal Revenue Service. Under the InternalRevenue Code, wages include any com-pensation received due to the performanceof services as an employee, and the termemployee includes any individual forwhom the legal relationship between theindividual and the person for whom theindividual performs services is the legalrelationship of employer and employee.All wages are included in gross income forpurposes of determining federal incometax liability, and are also subject to federalemployment taxes. Any argument thatForms W–2 only record and report pay-ments made to federal employees, or thatonly federal employees or residents of theDistrict of Columbia or federal territoriesand enclaves earn wages subject to tax,has no merit and is frivolous.

April 10, 2006 743 2006–15 I.R.B.

The Service is committed to identify-ing taxpayers who attempt to avoid theirfederal tax obligations by taking frivolouspositions. The Service will take vigorousenforcement action against these taxpayersand against promoters and return prepar-ers who assist taxpayers in taking thesefrivolous positions. Frivolous returnsand other similar documents submittedto the Service are processed through theService’s Frivolous Return Program. Aspart of this program, the Service deter-mines whether taxpayers who have takenfrivolous positions have filed all requiredtax returns, and computes the correctamount of tax and interest due, and deter-mines whether civil or criminal penaltiesshould apply. The Service also determineswhether civil or criminal penalties shouldapply to return preparers, promoters,and others who assist taxpayers in tak-ing frivolous positions, and recommendswhether an injunction should be soughtto halt these activities. Other informationabout frivolous tax positions is availableon the Service website at www.irs.gov.

ISSUE

Whether only federal employees andpersons residing in Washington, D.C. orfederal territories and enclaves are subjectto federal income and employment taxes.

FACTS

Taxpayer A either 1) requests, by sub-mitting a Form W–4, Employee’s With-holding Allowance Certificate, that his em-ployer not withhold any amount of fed-eral tax from wages earned, or 2) preparesa Form 4852 (Substitute for W–2) show-ing no wages received. In addition, tax-payer A either fails to file a return, orfiles a return with zero income claimingall withholding as a refund. Taxpayer Aclaims that he is not an “employee” anddoes not receive “wages” subject to federalincome tax, as those terms are as definedin the Internal Revenue Code. Taxpayer Acontends that the federal government canonly legally demand an “income” tax fromfederal employees and persons residing inWashington, D.C. or federal territories andenclaves. Therefore, Taxpayer A claimsthat he does not have to pay “income”taxes — which Taxpayer A asserts also in-clude employment taxes such as Federal

Insurance Contributions Act (FICA) taxes— to the federal government.

LAW AND ANALYSIS

Section 3401(a) provides that “wages”include all remuneration for services per-formed by an employee for his employer.Section 3121(a) provides a similar defi-nition of wages for FICA tax purposes.The argument that only federal employ-ees and persons residing in Washington,D.C. or federal territories and enclaves aresubject to tax is based on a misinterpre-tation of section 3401(c), which defines“employee” and states that the term “in-cludes an officer, employee or elected of-ficial of the United States, a State, or anypolitical subdivision thereof . . . .” Section31.3401(c)–1 of the Employment Tax Reg-ulations provides that the term “employee”includes every individual performing ser-vices if the relationship between that in-dividual and the person for whom he per-forms such services is the legal relation-ship of employer and employee. Section7701(c) states that the use of the word “in-cludes” “shall not be deemed to excludeother things otherwise within the meaningof the term defined.” Thus, the word “in-cludes” as used in the definition of “em-ployee” under § 3401(c) is a term of en-largement, not of limitation. Courts haverecognized that federal employees and of-ficials are among those within the defini-tion of “employee,” which also includesprivate citizens. See Sullivan v. UnitedStates, 788 F.2d 813, 815 (1st Cir. 1986)(contention that taxpayer was not an “em-ployee” is meritless, section 3401(c) doesnot limit withholding to the persons listedtherein); United States v. Latham, 754F.2d 747, 750 (7th Cir. 1985) (under sec-tion 3401(c), the category of “employee”includes privately employed wage earn-ers; the word “includes” is a term of en-largement not of limitation, and the ref-erence to certain entities or categories isnot intended to exclude all others); Pabonv. Commissioner, T.C. Memo. 1994–476(1994) (taxpayer’s frivolous position thatshe was not subject to tax because she wasnot an employee of the federal or state gov-ernments warranted sanctions of $2,500).

The employment tax withholding pro-visions do not affect whether wages aregross income. Section 61 provides thatcompensation for services is includable in

gross income. Whether the compensationfor services is in the form of wages, orin some other form, is irrelevant. Theamount is still subject to income tax. Allemployees, not just federal employees andthose living in federal territories and en-claves, are subject to income and employ-ment taxes.

HOLDING

Federal income tax laws do not applysolely to federal employees and persons re-siding in the District of Columbia, or fed-eral territories and enclaves, and any con-trary contention is frivolous. The terms“employee” and “wages” as used by theInternal Revenue Code apply to all em-ployees, unless specifically exempted bythe Internal Revenue Code. The incometax withholding provisions do not affectwhether an amount is gross income.

CIVIL AND CRIMINAL PENALTIES

The Service will challenge the claims ofindividuals who attempt to avoid or evadetheir federal tax liability. In addition toliability for the tax due plus statutory in-terest, taxpayers who fail to file valid re-turns or pay tax based on the argumentthat Forms W–2 only record and reportpayments made to federal workers, or thatonly federal employees or residents of fed-eral territories and enclaves earn wages,face substantial civil and criminal penal-ties. Potentially applicable civil penaltiesinclude: (1) the section 6662 accuracy-re-lated penalties, which are generally equalto 20 percent of the amount of tax thetaxpayer should have paid; (2) the sec-tion 6663 penalty for civil fraud, which isequal to 75 percent of the amount of taxesthe taxpayer should have paid; (3) a $500penalty imposed under section 6702 whenthe taxpayer files a document that purportsto be a return but that contains a frivolousposition or suggests a desire by the tax-payer to delay or impede the administra-tion of Federal income tax laws; (4) thesection 6651 additions to tax for failure tofile a return, failure to pay the tax owed,and fraudulent failure to file a return; and(5) a penalty of up to $25,000 under sec-tion 6673 if the taxpayer makes frivolousarguments in the United States Tax Court.

Taxpayers relying on this frivolous po-sition also may face criminal prosecution

2006–15 I.R.B. 744 April 10, 2006

under: (1) section 7201 for attempting toevade or defeat tax, the penalty for which isa significant fine and imprisonment for upto 5 years; (2) section 7203 for willful fail-ure to file a return, the penalty for whichis a significant fine and imprisonment forup to a year; (3) section 7206 for makingfalse statements on a return, statement, orother document, the penalty for which is asignificant fine and imprisonment for up to3 years.

Persons, including return preparers,who promote this frivolous position andthose who assist taxpayers in claiming taxbenefits based on frivolous positions mayface civil and criminal penalties and alsomay be enjoined by a court pursuant tosections 7407 and 7408. Potential penal-ties include: (1) a $250 penalty undersection 6694 for each return or claim forrefund prepared by an income tax returnpreparer who knew or should have knownthat the taxpayer’s position was frivolous(or $1,000 for each return or claim forrefund if the return preparer’s actionswere willful, intentional or reckless); (2) apenalty under section 6700 for promotingabusive tax shelters; (3) a $1,000 penaltyunder section 6701 for aiding and abettingthe understatement of tax; and (4) criminalprosecution under section 7206, for whichthe penalty is a significant fine and impris-onment for up to 3 years, for assisting oradvising about the preparation of a falsereturn, statement or other document underthe internal revenue laws.

DRAFTING INFORMATION

This revenue ruling was authored by theoffice of the Associate Chief Counsel (Pro-cedure and Administration), Administra-tive Provisions and Judicial Practice Di-vision. For further information regardingthis revenue ruling, contact that office at(202) 622–7950 (not a toll-free call).

Section 6012.—PersonsRequired to Make Returnsof Income26 CFR § 1.6012–1(a): Individuals required to makereturns of income.(Also: 44 U.S.C. § 3501, et seq.)

Frivolous tax returns; reliance on Pa-perwork Reduction Act. This ruling em-phasizes to taxpayers, promoters, and re-

turn preparers that taxpayers are requiredto file a federal income tax return undersection 6012 of the Code, and the regu-lations thereunder, and that the PaperworkReduction Act of 1980 (PRA) does not re-lieve taxpayers of the duty to file. Any ar-gument that the PRA relieves the taxpayerof the duty to file an income tax return hasno merit and is frivolous.

Rev. Rul. 2006–21

PURPOSE

The Service is aware that some tax-payers are attempting to reduce their fed-eral income tax liability by contending thatthey are not required to file an income taxreturn because of the Paperwork Reduc-tion Act of 1980, Pub. L. No. 96–511, 94Stat. 2812 (codified at 44 U.S.C. § 3501,et seq.) (“PRA”). The PRA was enacted,among other reasons, to limit federal agen-cies’ information requests in order to min-imize the paperwork burden for the pub-lic. The “public protection” provision ofthe PRA provides that no person shall besubject to any penalty for failing to main-tain or provide information to any agencyif the information collection request in-volved does not display a current controlnumber assigned by the Office of Man-agement and Budget (“OMB”). 44 U.S.C.§ 3512. Taxpayers who attempt to relyon the PRA contend that they are not re-quired to file a Form 1040, U.S. IndividualIncome Tax Return, because the instruc-tions and regulations associated with theForm 1040 do not display an OMB con-trol number. The Service is also aware thatsome promoters, including return prepar-ers, market a package, kit or other mate-rials, advising or recommending that tax-payers take this frivolous position.

This revenue ruling emphasizes to tax-payers, promoters and return preparers thattaxpayers are required to file a federal in-come tax return under section 6012 of theInternal Revenue Code, and the regula-tions thereunder, and that the PRA doesnot relieve taxpayers of the duty to file.Any argument that the PRA relieves thetaxpayer of the duty to file an income taxreturn has no merit and is frivolous.

The Service is committed to identi-fying taxpayers who attempt to avoidtheir federal tax obligations by takingfrivolous positions. The Service will

take vigorous enforcement action againstthese taxpayers and against promotersand return preparers who assist taxpay-ers in taking these frivolous positions.Frivolous returns and other similar doc-uments submitted to the Service are pro-cessed through the Service’s FrivolousReturn Program. As part of this program,the Service confirms whether taxpayerswho take frivolous positions have filedall of their required tax returns, computesthe correct amount of tax and interest due,and determines whether civil or crimi-nal penalties should apply. The Servicealso determines whether civil or criminalpenalties should apply to return prepar-ers, promoters, and others who assisttaxpayers in taking frivolous positions,and recommends whether an injunctionshould be sought to halt these activities.Other information about frivolous tax po-sitions is available on the Service websiteat www.irs.gov.

ISSUE

Whether taxpayers may avoid theirobligation to file federal income tax re-turns based on the PRA.

FACTS

Taxpayer A fails to file a federal incometax return, contending that it is not possibleto comply with the filing requirement ofInternal Revenue Code section 6012, be-cause the Commissioner has not suppliedan information collection request form thatcomplies with the PRA.

LAW AND ANALYSIS

No law allows taxpayers to avoid theirobligation under the Internal RevenueCode to file a federal tax return through re-liance on the PRA. Courts repeatedly haverejected PRA-based arguments on a num-ber of alternative grounds. Some courtshave simply noted that the PRA applies toforms themselves, not to the instructions,and, because the Form 1040 does have acontrol number, there is no PRA viola-tion. Other courts have held that Congresscreated the duty to file federal income taxreturns in section 6012(a) and “Congressdid not enact the PRA’s public protectionprovision to allow OMB to abrogate anyduty imposed by Congress.” United Statesv. Neff, 954 F.2d 698, 699 (11th Cir. 1992);

April 10, 2006 745 2006–15 I.R.B.

see also Salberg v. United States, 969 F.2d379, 383 (7th Cir. 1992) (affirming con-viction for tax evasion and failing to filea return, rejecting claims under the PRA);United States v. Holden, 963 F.2d 1114,1116 (8th Cir. 1992) (affirming convictionfor failing to file a return and rejectingargument in favor of acquittal premised onthe fact that tax instruction booklets failto comply with the PRA); United States v.Hicks, 947 F.2d 1356, 1359 (9th Cir. 1991)(affirming conviction for failing to file areturn, finding requirement to provide in-formation is required by statute, not by theService); Lonsdale v. United States, 919F.2d 1440, 1445 (10th Cir. 1990) (find-ing the PRA inapplicable to “informationcollection request” forms issued during aninvestigation of an individual to determinetax liability); United States v. Wunder,919 F.2d 34, 37 (6th Cir. 1990) (rejectingclaim of a PRA violation and affirmingconviction for failing to file a return).

HOLDING

Taxpayers are required to file a federalincome tax return under section 6012 ofthe Internal Revenue Code. The PRA doesnot relieve taxpayers of the duty to file, andany argument to the contrary has no meritand is frivolous.

CIVIL AND CRIMINAL PENALTIES

The Service will challenge the claims ofindividuals who attempt to avoid or evadetheir federal tax liabilities. In addition toliability for the tax due plus statutory inter-est, taxpayers who fail to file valid returnsor pay tax based on frivolous PRA-basedarguments face substantial civil and crim-inal penalties. Potentially applicable civilpenalties include: (1) the section 6662 ac-curacy-related penalties, which are gener-ally equal to 20 percent of the amount oftax the taxpayer should have paid; (2) thesection 6663 penalty for civil fraud, whichis equal to 75 percent of the amount oftaxes the taxpayer should have paid; (3) a$500 penalty imposed under section 6702when the taxpayer files a document thatpurports to be a return but that contains afrivolous position or suggests a desire bythe taxpayer to delay or impede the admin-istration of Federal income tax laws; (4)the section 6651 additions to tax for failureto file a return, failure to pay the tax owed,

and fraudulent failure to file a return; and(5) a penalty of up to $25,000 under sec-tion 6673 if the taxpayer makes frivolousarguments in the United States Tax Court.

Taxpayers relying on frivolous posi-tions involving the PRA also may facecriminal prosecution under: (1) section7201 for attempting to evade or defeattax, the penalty for which is a significantfine and imprisonment for up to 5 years;(2) section 7203 for willful failure to filea return, the penalty for which is a sig-nificant fine and imprisonment for up toa year; and (3) section 7206 for makingfalse statements on a return, statement, orother document, the penalty for which isa significant fine and imprisonment for upto 3 years.

Persons, including return preparers,who promote these frivolous positions andthose who assist taxpayers in claiming taxbenefits based on frivolous positions mayface civil and criminal penalties and alsomay be enjoined by a court pursuant tosections 7407 and 7408. Potential penal-ties include: (1) a $250 penalty undersection 6694 for each return or claim forrefund prepared by an income tax returnpreparer who knew or should have knownthat the taxpayer’s position was frivolous(or $1,000 for each return or claim forrefund if the return preparer’s actionswere willful, intentional or reckless); (2)a penalty of up to $1,000 under section6700 for promoting abusive tax shelters;(3) a $1,000 penalty under section 6701for aiding and abetting the understatementof tax; and (4) criminal prosecution undersection 7206, for which the penalty is asignificant fine and imprisonment for up to3 years, for assisting or advising about thepreparation of a false return, statement orother document under the internal revenuelaws.

DRAFTING INFORMATION

This revenue ruling was authored bythe Office of the Associate Chief Counsel(Procedure and Administration), Adminis-trative Provisions and Judicial Practice Di-vision. For further information regardingthis revenue ruling, contact that office at(202) 622–7950 (not a toll-free call).

Section 6662.—Impositionof Accuracy-RelatedPenalty on Underpayments

Frivolous tax returns; “Native Amer-ican Treaty.” This ruling emphasizes totaxpayers, promoters, and return preparersthat there is no right to exemption fromfederal income tax for Native Americansunder an unspecified “Native AmericanTreaty.” Any return position based on anunspecified “Native American Treaty” hasno merit and is frivolous. As a general rule,Native Americans are subject to federal in-come tax just like every other American.

Rev. Rul. 2006–20

PURPOSE

The Service is aware that some tax-payers are attempting to reduce their fed-eral tax liability by claiming tax exemptstatus based on a general “Native Ameri-can Treaty.” The Service is also aware thatsome promoters, including return prepar-ers, are advising or recommending that Na-tive American taxpayers take the frivolousposition that they are exempt from federalincome tax based on an unspecified NativeAmerican treaty. Some promoters marketa package, kit or other materials that claimto show taxpayers how they can avoid pay-ing income taxes based on these and othermeritless arguments.

This revenue ruling emphasizes to tax-payers, promoters, and return preparersthat there is no right to exemption fromfederal income tax for Native Americansunder an unspecified “Native AmericanTreaty.” Any return position based on anunspecified “Native American Treaty” hasno merit and is frivolous. As a general rule,Native Americans are subject to federal in-come tax just like every other American.

The Service is committed to identi-fying taxpayers who attempt to avoidtheir federal tax obligations by takingfrivolous positions. The Service willtake vigorous enforcement action againstthese taxpayers and against promotersand return preparers who assist taxpay-ers in taking these frivolous positions.Frivolous returns and other similar doc-uments submitted to the Service are pro-cessed through the Service’s FrivolousReturn Program. As part of this program,the Service confirms whether taxpayers

2006–15 I.R.B. 746 April 10, 2006

who take frivolous positions have filedall of their required tax returns, computesthe correct amount of tax and interest due,and determines whether civil or crimi-nal penalties should apply. The Servicealso determines whether civil or criminalpenalties should apply to return prepar-ers, promoters, and others who assisttaxpayers in taking frivolous positions,and recommends whether an injunctionshould be sought to halt these activities.Other information about frivolous tax po-sitions is available on the Service websiteat www.irs.gov.

ISSUE

Whether taxpayers may avoid theirfederal income tax liability by claimingtax exempt status based on an unspecified“Native American Treaty.”

FACTS

Taxpayer A is a Native American andreceives income from a tribal or non-tribalsource. The income paid to taxpayer A isreported on an information return (e.g., aForm 1099-MISC, Form W–2. etc.). Tax-payer A then either: 1) fails to report theincome shown on the information returnon his federal income tax return, claim-ing an erroneous exemption from federalincome tax under an unspecified “NativeAmerican Treaty,” or 2) wrongly reportsa loss offsetting the information return in-come on the “Other Income” line of hisfederal income tax return with an explana-tion that reads, “Less - Native AmericanTreaty” or “Native American Treaty.”

LAW AND ANALYSIS

Native Americans are subject to thesame income tax laws as other U.S. citi-zens unless there is an exemption explic-itly created by treaty or statute. Squire v.Capoeman, 351 U.S. 1, 6 (1956); Estateof Poletti v. Commissioner, 99 T.C. 554,557–58 (1992), aff’d, 34 F.3d 742 (9th Cir.1994); Doxtator v. Commissioner, T.C.Memo. 2005–113. Any exemption mustbe based on clear and unambiguous treatyor statutory language. Squire, 351 U.S. at6; Ramsey v. United States, 302 F.3d 1074(9th Cir. 2002); Cook v. United States,86 F.3d 1095 (Fed. Cir. 1996); Estate ofPeterson v. Commissioner, 90 T.C. 249,250 (1988). Under the Internal Revenue

Code, all individuals, including NativeAmericans, are subject to federal incometax. Section 1 imposes a tax on all taxableincome. Section 61 provides that grossincome includes all income from whateversource derived. Adjustments to income,deductions, and credits must be claimedin accordance with the provisions of theInternal Revenue Code and accompanyingTreasury regulations. Although there arecertain exemptions and other provisionsthroughout the Internal Revenue Code thatapply to Native Americans, none of theseexempt individual Native American tax-payers from federal tax. Moreover, underthe Indian Gaming Regulatory Act, anydistribution of casino gaming proceeds toindividual tribe members is also subject tofederal income tax.

Additionally, while there are numerousvalid treaties between various FederallyRecognized Indian Tribal Governmentsand the United States government, someof which may contain language providingfor narrowly defined tax exemptions, thesetreaties have limited application to spe-cific tribes. Any exemptions from federaltax are expressly stated in the language ofthe treaty. Taxpayers who are affected bysuch treaty language must be a member ofa particular tribe having a treaty and mustcite that specific treaty in claiming anyexemption. There is no general treaty thatis applicable to all Native Americans.

HOLDING

Taxpayer A made improper and un-founded claims for exemption from fed-eral income tax by either failing to reporthis income or reporting it and claimingan offsetting deduction. Any claim that ataxpayer is exempt from federal incometax due to a general “Native AmericanTreaty” is frivolous. Unless a taxpayercan cite a specific treaty or statutory lan-guage providing for exemption of incomefrom federal income tax, that taxpayer issubject to all applicable federal income taxlaws. Thus, Taxpayer A must report theincome shown on the information returnand may not report a loss or exemptionattributable to a general Native Americantreaty to offset the income received fromthe tribal organization.

CIVIL AND CRIMINAL PENALTIES

The Service will challenge the claims ofindividuals who attempt to avoid or evadetheir federal tax liability. In addition to li-ability for the tax due plus statutory inter-est, taxpayers who fail to file valid returnsor pay tax based on the argument that theyare exempt from income tax due to a gen-eral “Native American Treaty” face sub-stantial civil and criminal penalties. Poten-tially applicable civil penalties include: (1)the section 6662 accuracy-related penal-ties, which are generally equal to 20 per-cent of the amount of taxes the taxpayershould have paid; (2) the section 6663penalty for civil fraud, which is equal to75 percent of the amount of taxes the tax-payer should have paid; (3) a $500 penaltyimposed under section 6702 when the tax-payer files a document that purports to bea return but that contains a frivolous posi-tion or suggests a desire by the taxpayer todelay or impede the administration of fed-eral income tax laws; (4) the section 6651additions to tax for failure to file a return,failure to pay the tax owed, and fraudulentfailure to file a return; and (5) a penaltyof up to $25,000 under section 6673 if thetaxpayer makes frivolous arguments in theUnited States Tax Court.

Taxpayers relying on these frivolouspositions also may face criminal prosecu-tion under: (1) section 7201 for attempt-ing to evade or defeat tax, the penalty forwhich is a significant fine and imprison-ment for up to 5 years; (2) section 7203for willful failure to file a return under,the penalty for which is a significant fineand imprisonment for up to 1 year; and (3)section 7206 for making false statementson a return, statement, or other document,the penalty for which is a significant fineand imprisonment for up to 3 years.

Persons, including return preparers,who promote these frivolous positions andthose who assist taxpayers in claiming taxbenefits based on frivolous positions mayface civil and criminal penalties and alsomay be enjoined by a court pursuant tosections 7407 and 7408. Potential penal-ties include: (1) a $250 penalty undersection 6694 for each return or claim forrefund prepared by an income tax returnpreparer who knew or should have knownthat the taxpayer’s position was frivolous(or $1,000 for each return or claim forrefund if the return preparer’s actions

April 10, 2006 747 2006–15 I.R.B.

were willful, intentional or reckless); (2)a penalty of up to $1,000 under section6700 for promoting abusive tax shelters;(3) a $1,000 penalty under section 6701for aiding and abetting the understatementof tax; and (4) criminal prosecution undersection 7206, resulting in a significant fineand imprisonment for up to 3 years, forassisting or advising about the preparationof a false return statement or other docu-ment under the internal revenue laws.

DRAFTING INFORMATION

This revenue ruling was authored by theOffice of Associate Chief Counsel (Proce-dure and Administration), AdministrativeProvisions and Judicial Practice Division.For further information regarding this rev-enue ruling, contact that office at (202)622–7800 (not a toll-free call).

Section 6673.—Sanctionsand Costs Awarded byCourts

Frivolous tax returns; “nunc protunc.” This ruling emphasizes to taxpay-ers, promoters, and return preparers thatinserting the phrase “nunc pro tunc” on areturn or other document submitted to theService has no legal effect and does notvalidate an invalid return, make a delin-quent return timely, invalidate a signature,create a claim for refund of taxes previ-ously paid, or reduce one’s federal taxliability.

Rev. Rul. 2006–17

PURPOSE

The Service is aware that some taxpay-ers are attempting to reduce their federalincome tax liability by filing a returnor submitting documents to the Servicewith the phrase “nunc pro tunc” writtenor stamped on the face of the return ordocument, and asserting that the phrasehas some legal effect. The Service isalso aware that some promoters, includingreturn preparers, are advising or recom-mending that taxpayers take this frivolousposition. Some promoters market a pack-age, kit or other materials that claim toshow taxpayers how they can avoid pay-ing income taxes based on this and othermeritless arguments.

This revenue ruling emphasizes to tax-payers, promoters, and return preparersthat inserting the phrase “nunc pro tunc”on a return or other document submitted tothe Service has no legal effect and does notvalidate an invalid return, make a delin-quent return timely, invalidate a signature,create a claim for refund of taxes previ-ously paid, or reduce one’s federal tax lia-bility. Any argument that the inclusion ofthe phrase “nunc pro tunc” on a return orother document submitted to the Servicehas any legal effect has no merit and isfrivolous.

The Service is committed to identi-fying taxpayers who attempt to avoidtheir federal tax obligations by takingfrivolous positions. The Service willtake vigorous enforcement action againstthese taxpayers and against promotersand return preparers who assist taxpay-ers in taking these frivolous positions.Frivolous returns and other similar doc-uments submitted to the Service are pro-cessed through the Service’s FrivolousReturn Program. As part of this program,the Service confirms whether taxpayerswho take frivolous positions have filedall of their required tax returns, computesthe correct amount of tax and interest due,and determines whether civil or crimi-nal penalties should apply. The Servicealso determines whether civil or criminalpenalties should apply to return prepar-ers, promoters, and others who assisttaxpayers in taking frivolous positions,and recommends whether an injunctionshould be sought to halt these activities.Other information about frivolous tax po-sitions is available on the Service websiteat www.irs.gov.

ISSUE

Whether inclusion of the phrase “nuncpro tunc” on a return or other documentfiled with the Service has any legal effect.

FACTS

Some taxpayers file returns or otherdocuments with the Service that have thephrase “nunc pro tunc” stamped or writtenon the face of the return or document.These taxpayers assert that the phrase“nunc pro tunc” has some legal effect inreducing, eliminating, or altering in someway their federal income tax liability orother obligations under the tax laws.

LAW AND ANALYSIS

The phrase “nunc pro tunc,” a Latinphrase translated as “now for then,” de-notes that an act has retroactive legal effectthrough a court’s inherent power. Black’sLaw Dictionary 1097 (8th ed. 2004).When a document is signed “nunc protunc” as of a specified date, it means that athing is now done which should have beendone on the specified date. 56 Am. Jur.2d Motions, Rules, and Orders § 58, at 45(2000).

The term “nunc pro tunc” also describesa later record entry of a previous action thatis intended to have effect as of the date ofthe action itself. Black’s Law Dictionary1097. The inclusion of the phrase “nuncpro tunc” on the face of the return form orin other documents submitted to the Ser-vice has no legal effect, and does not val-idate an invalid return, make an untimelyreturn timely, invalidate a signature, cre-ate a claim for refund of taxes previouslypaid, or reduce one’s federal tax liability.

To the extent taxpayers are attemptingto validate an otherwise invalid return bywriting or stamping the phrase “nunc protunc” on the face of a return or in attacheddocuments, this phrase has no validatingeffect. For a document to qualify as a validreturn, it must contain sufficient data tocalculate tax liability, it must purport tobe a return, there must be an honest andreasonable attempt to satisfy the require-ments of the tax law, and the taxpayer mustexecute the return under penalties of per-jury. Beard v. Commissioner, 82 T.C.766 (1984), aff’d, 793 F.2d 139 (6th Cir.1986). The inclusion of the phrase “nuncpro tunc” on the face of the return formor in the attachments does not provide anyfurther information sufficient to calculatetax liability, or to satisfy any other require-ments of the tax law. Accordingly, it doesnot validate an otherwise invalid return.

HOLDING

Inclusion of the phrase “nunc pro tunc”on a return or other document submittedto the Service has no legal effect and istherefore frivolous.

CIVIL AND CRIMINAL PENALTIES

The Service will challenge the claims ofindividuals who attempt to avoid or evadetheir federal tax liability. In addition to

2006–15 I.R.B. 748 April 10, 2006

liability for the tax due plus statutory in-terest, taxpayers who fail to file valid re-turns or pay tax based on the argument thatthe inclusion of the phrase “nunc pro tunc”on the face of their return or other docu-ment submitted to the Service has some le-gal effect, face substantial civil and crim-inal penalties. Potentially applicable civilpenalties include: (1) the section 6662 ac-curacy-related penalties, which are gener-ally equal to 20 percent of the amount oftax the taxpayer should have paid; (2) thesection 6663 penalty for civil fraud, whichis equal to 75 percent of the amount oftaxes the taxpayer should have paid; (3) a$500 penalty imposed under section 6702when the taxpayer files a document thatpurports to be a return but that contains afrivolous position or suggests a desire bythe taxpayer to delay or impede the admin-istration of Federal income tax laws; (4)the section 6651 additions to tax for failureto file a return, failure to pay the tax owed,and fraudulent failure to file a return; and(5) a penalty of up to $25,000 under sec-tion 6673 if the taxpayer makes frivolousarguments in the United States Tax Court.

Taxpayers relying on these frivolouspositions also may face criminal prosecu-tion under: (1) section 7201 for attempt-ing to evade or defeat tax, the penalty forwhich is a significant fine and imprison-ment for up to 5 years; (2) section 7203for willful failure to file a return undersection 7203, the penalty for which is asignificant fine and imprisonment for upto a year; and (3) section 7206 for makingfalse statements on a return, statement, orother document, the penalty for which isa significant fine and imprisonment for upto 3 years; and (4) any other penalties pur-suant to applicable provisions of federallaw.

Persons, including return preparers,who promote these frivolous positions andthose who assist taxpayers in claiming taxbenefits based on frivolous positions mayface civil and criminal penalties and alsomay be enjoined by a court pursuant tosections 7407 and 7408. Potential penal-ties include: (1) a $250 penalty undersection 6694 for each return or claim forrefund prepared by an income tax returnpreparer who knew or should have knownthat the taxpayer’s position was frivolous(or $1,000 for each return or claim forrefund if the return preparer’s actionswere willful, intentional or reckless); (2) a

penalty under section 6700 for promotingabusive tax shelters; (3) a $1,000 penaltyunder section 6701 for aiding and abet-ting the understatement of tax; and (4)criminal prosecution under section 7206,for which the penalty is a significant fineand imprisonment for up to 3 years, forassisting or advising about the preparationof a false return or other document underthe internal revenue laws.

DRAFTING INFORMATION

This revenue ruling was authored bythe Office of the Associate Chief Counsel(Procedure and Administration), Adminis-trative Provisions and Judicial Practice Di-vision. For further information regardingthis revenue ruling, contact that office at(202) 622–7950 (not a toll-free call).

Section 6702.—FrivolousIncome Tax Return

Frivolous tax returns; use of shamtrusts. This ruling emphasizes that anindividual cannot escape taxation by at-tributing income to a purported trust. TheService will take vigorous enforcement ac-tion against frivolous arguments relating totrusts.

Rev. Rul. 2006–19

PURPOSE

The Service is aware that some tax-payers are attempting to reduce their fed-eral tax liability by filing a Form 1041,U.S. Income Tax Return for Estates andTrusts, listing income in the amount statedon their W–2, but claiming a deduction onthe return for a “fiduciary fee” in the ex-act amount of that income. These taxpay-ers then request a refund of the full amountwithheld with respect to that income.

This revenue ruling emphasizes thatan individual cannot escape taxation byattributing income to a purported trust.The Service is committed to identifyingtaxpayers who attempt to avoid their fed-eral tax obligations by taking frivolouspositions, based on arguments relatingto trusts. The Service will take vigorousenforcement action against frivolous ar-guments relating to trusts. The Serviceprocesses frivolous returns and other sim-ilar documents submitted to the Service

through the Service’s Frivolous ReturnProgram. As part of this program, theService confirms whether taxpayers whotake frivolous positions have filed all oftheir required tax returns, computes thecorrect amount of tax and interest due,and determines whether civil and criminalpenalties should apply. Other informationabout frivolous tax positions is availableon the Service website at www.irs.gov.

ISSUE

Whether taxpayers can eliminate theirfederal income tax liability by attributingincome to a trust and claiming expense de-ductions related to that trust.

FACTS

Individual taxpayer A files a Form 1041trust income tax return for the 2005 tax-able year. On it, taxpayer A lists the fullamount of income reported on his W–2,but claims a deduction for a “fiduciary fee”in the same amount. Taxpayer A requestsa refund of the full amount of withholding.

LAW AND ANALYSIS

Many frivolous trust schemes involvethe purported transfer of income and ex-penses to a trust, on the theory that the in-come and expenses then become that of thetrust. Such schemes are ignored for federaltax purposes because taxpayers cannot as-sign personal income to a trust in order toavoid tax, because such trusts are shamsfor federal tax purposes, and because thegrantor trust rules of the Internal RevenueCode (sections 671 through 679) tax the in-come to the individual grantor and not tothe trust. See, e.g., United States v. Krall,835 F.2d 711, 714 (8th Cir. 1987); UnitedStates v. Buttorff, 761 F.2d 1056, 1060–61(5th Cir. 1985).

Income is ordinarily taxed to the personwho earned it, and tax liability may not beshifted by assigning the income to anotherperson. Commissioner v. Culbertson, 337U.S. 733, 739–740 (1949); Helvering v.Eubank, 311 U.S. 122 (1940); Lucas v.Earl, 281 U.S. 111 (1930). The taxpayeris taxable on assigned income even if theincome is paid directly to a trust. Wheelerv. United States, 768 F.2d 1333 (Fed. Cir.1985); Saunders v. Commissioner, 720F.2d 871 (5th Cir. 1983); Armantrout v.Commissioner, 67 T.C. 996 (1977), aff’d,

April 10, 2006 749 2006–15 I.R.B.

570 F.2d 210 (7th Cir. 1978). Thus,assignments of personal income and ex-penses to a trust are not valid for federalincome tax purposes.

Even if the taxpayer created a validtrust under state law, the trust would be ig-nored for federal tax purposes because it isa sham. When the form of the transactionhas not, in fact, altered economic relation-ships, income is taxed according to thesubstance of the transaction. Markosianv. Commissioner, 73 T.C. 1235 (1980).This rule applies regardless of whetherthe entity has a separate existence rec-ognized under state law (see Furman v.Commissioner, 45 T.C. 360 (1966), aff’d.per curiam 381 F.2d 22 (5th Cir. 1967)),and regardless of the form of the entity,such as a trust or common law businesstrust. See Zmuda v. Commissioner, 731F.2d 1417 (9th Cir. 1984).

In addition, the grantor trust provisionsof the Internal Revenue Code require theattribution of the income and expenses ofthe trust to the individual. These provi-sions provide that all items of income, de-duction, and credit of the trust, shall beincluded in computing the taxable incomeand credits of the grantors and other per-sons who have substantial powers of own-ership or control over the trust. The powerto control the beneficial enjoyment of thecorpus or the income of the trust, the powerto borrow from or deal with the trust with-out adequate and full consideration or se-curity, the power to revoke the trust or tohave the corpus or income revert to thegrantor, the power to use the corpus orincome of the trust for the benefit of thegrantor, or similar powers, result in thetrust being ignored for federal tax purposesand all income and allowable expenses be-ing attributed to the individual grantor. Seesections 671–679; Vnuk v. Commissioner,621 F.2d 1318 (8th Cir. 1980); Rev. Rul.75–257, 1975–2 C.B. 251.

Finally, because no trust is deemed toexist for federal tax purposes, there is no

fiduciary relationship upon which trustees’fees could be predicated and there is noordinary and necessary business expensewhich could validly be claimed for suchamounts. Thus, the claimed expense fortrustees’ fees would be disallowed.

HOLDING

Individual taxpayers must file Form1040 to report earned income and may notfile Form 1041 reporting income througha trust in order to avoid federal income taxliability.

CIVIL AND CRIMINAL PENALTIES

The Service will challenge the claims ofindividuals who attempt to avoid or evadetheir federal tax liability. In addition toliability for the tax due plus statutory in-terest, taxpayers who fail to file valid re-turns or pay tax based on a frivolous ar-gument face substantial civil and crimi-nal penalties. Potentially applicable civilpenalties include: (1) the section 6662 ac-curacy-related penalties, which are gener-ally equal to 20 percent of the amount oftax the taxpayer should have paid; (2) thesection 6663 penalty for civil fraud, whichis equal to 75 percent of the amount oftaxes the taxpayer should have paid; (3) a$500 penalty imposed under section 6702when the taxpayer files a document thatpurports to be a return but that contains afrivolous position or suggests a desire bythe taxpayer to delay or impede the admin-istration of federal income tax laws; (4) thesection 6651 additions to tax for failure tofile a return, failure to pay the tax owed,and fraudulent failure to file a return; and(5) a penalty of up to $25,000 under sec-tion 6673 if the taxpayer makes frivolousarguments in the United States Tax Court.

Taxpayers relying on these frivolouspositions also may face criminal prosecu-tion under the following provisions: (1)section 7201, for attempting to evade ordefeat tax, the penalty for which is a sig-

nificant fine and imprisonment for up to 5years; (2) section 7203, for willful failureto file a return, the penalty for which is asignificant fine and imprisonment for upto 1 year; and (3) section 7206, for makingfalse statements on a return, statement, orother document, the penalty for which isa significant fine and imprisonment for upto 3 years.

Persons, including return preparers,who promote these frivolous positions andthose who assist taxpayers in claiming taxbenefits based on frivolous positions mayface civil and criminal penalties and alsomay be enjoined by a court pursuant tosections 7407 and 7408. Potential penal-ties include: (1) a $250 penalty undersection 6694 for each return or claim forrefund prepared by an income tax returnpreparer who knew or should have knownthat the taxpayer’s position was frivolous(or $1,000 for each return or claim forrefund if the return preparer’s actionswere willful, intentional or reckless); (2)a penalty of up to $1,000 under section6700 for each activity promoting abusivetax shelters; (3) a $1,000 penalty undersection 6701 for aiding and abetting theunderstatement of tax; and (4) criminalprosecution under section 7206, resultingin a significant fine and imprisonment forup to 3 years, for assisting or advisingabout the preparation of a false return orother document under the internal revenuelaws.

DRAFTING INFORMATION

This revenue ruling was authored bythe Office of the Associate Chief Counsel(Procedure and Administration), Adminis-trative Provisions and Judicial Practice Di-vision. For further information regardingthis revenue ruling, contact that office at(202) 622–7950 (not a toll-free call).

2006–15 I.R.B. 750 April 10, 2006

Part III. Administrative, Procedural, and MiscellaneousFrivolous Arguments to AvoidWhen Filing a Return or Claimfor Refund

Notice 2006–31

SECTION 1. INTRODUCTION

As April 15 approaches, the Inter-nal Revenue Service reminds taxpayersto steer clear of abusive tax-avoidanceschemes that purportedly allow them toreduce or eliminate taxes based on false orfrivolous arguments. If an idea to save ontaxes seems too good to be true, it proba-bly is.

Many abusive tax-avoidance schemesare based on frivolous arguments that theService and the courts have repeatedly re-jected. These schemes are often sold bypromoters for a substantial fee, and may besold over the Internet, through advertise-ments in newspapers and magazines and atconferences and seminars.

Section 2 of this notice sets out some ofthe most common frivolous argumentsused by these abusive tax-avoidanceschemes. The Service is committed toidentifying taxpayers who attempt toavoid their federal tax obligations bytaking frivolous positions. The Servicewill take vigorous enforcement actionagainst these taxpayers and against pro-moters and return preparers who assisttaxpayers in taking these frivolous posi-tions. Frivolous returns and other similardocuments submitted to the Service areprocessed through the Service’s FrivolousReturn Program. As part of this program,the Service confirms whether taxpayerswho take frivolous positions have filedall of their required tax returns, computesthe correct amount of tax and interest due,and determines whether civil or criminalpenalties should apply.

Section 3 of this notice identifies po-tential civil and criminal penalties forparticipation in, or promotion of, abusivetax-avoidance schemes. Taxpayers whoengage in abusive tax-avoidance schemeswill be liable for unpaid taxes and interest.In addition, the Service will impose civiland criminal penalties against taxpayerswhere appropriate. The Service also willimpose appropriate penalties and considertaking other appropriate action against

persons who promote abusive tax-avoid-ance schemes and who prepare frivolousreturns based on those schemes.

SECTION 2. COMMON FRIVOLOUSARGUMENTS

This section of this notice sets out someof the most common frivolous argumentsused by taxpayers to avoid or evade tax.This notice is not intended to be a de-scription of all frivolous arguments used toavoid or evade tax. Accordingly, the factthat an abusive tax-avoidance scheme isnot described in this notice does not meanthat it is not false and frivolous.

• “The only persons subject to federalincome and employment taxation arefederal employees and persons resid-ing in Washington, D.C., or federalterritories.” Promoters of this schemeincorrectly advise taxpayers who re-ceive wages with respect to employ-ment to file a Form 4852 (Substitutefor Form W–2, Wage and Tax State-ment, or Form 1099-R, DistributionsFrom Pensions, Annuities, Retirementor Profit-Sharing Plans, IRAs, Insur-ance Contracts, etc.) with the Serviceand, based on the above theory, includea zero on the line for the amount ofwages received. The Internal RevenueCode, however, imposes a federal in-come tax upon all United States resi-dents and citizens, not just federal em-ployees and those that reside in Wash-ington, D.C., federal territories, andfederal enclaves. The Internal Rev-enue Code also imposes employmenttax on all wages paid for employment.