bulletin d’information - gouv · bulletin d’information 2001-6 july 5, 2001 subject: broadening...

TRANSCRIPT

BULLETIN D’INFORMATION22000011--66

JJuullyy 55,, 22000011

Subject: Broadening of the tax credit for musical productions todramatic performances and comedy shows andclarifications concerning the fiscal policy applicable toindividuals and to businesses

This information bulletin describes the application details of the broadening of therefundable tax credit for musical productions to dramatic performances and comedyshows.

It also provides a full description of the application details of many more technical fiscalmeasures concerning personal income tax, corporate income tax and consumptiontaxes.

The following changes are made, in particular, regarding corporate taxes:

— the calculation of the refundable tax credit for Québec film or televisionproduction is simplified;

— the application of the tax holiday for manufacturing SMEs in remote resourceregions is clarified;

— two activity sectors are added to the refundable tax credit for processing activitiesin the resource regions and its application is extended in some cases.

In the consumption taxes sector, new measures are introduced to enhance compliancewith the tax rules in the garment industry. In addition, the application of the specific taxon lodging of $2 per overnight stay will be extended to two other tourist regions, namelyCharlevoix and Outaouais regions.

- 2 -

For information concerning these matters, contact the Secteur du droit fiscal et de lafiscalité at (418) 691-2236.

The French and English versions of this bulletin are available at the ministère desFinances website at: www.finances.gouv.qc.ca

Paper copies are also available, on request, from the Direction des communications, at(418) 691-2233.

BBuulllleettiinn dd’’iinnffoorrmmaattiioonn 22000011--66

Broadening of the tax credit for musical productions to dramaticperformances and comedy shows and clarifications concerning thefiscal policy applicable to individuals and to businesses

1. MEASURES CONCERNING INDIVIDUALS ........................................................1

1.1 Confirmation of the right of an individual making support payments to claima tax credit regarding the child whose custody he shares ....................................1

1.2 Possibility of spreading out the taxation of a lump-sum pay equity paymentmade by certain municipal employers...................................................................2

1.3 Broadening of fiscal measures relating to property with undeniableecological value ....................................................................................................4

1.3.1 Recognition of the government of Canada as donee .................................5

1.3.2 Eligibility of certain property located outside Québec.................................5

1.4 Tax benefits granted to the office of a political division of a foreign state .............7

1.5 Introduction of a deduction for foreign producers................................................10

1.6 Clarification of the fiscal policy relating to allowances for the use of a motorvehicle.................................................................................................................12

1.7 Obligation to file an information return regarding certain contractualpayments and amounts paid as subsidies ..........................................................14

1.7.1 Reporting of certain contractual payments paid by governmentdepartments and budget-funded bodies...................................................14

1.7.2 Information return regarding subsidies.....................................................16

2. MEASURES CONCERNING BUSINESSES ......................................................17

2.1 Measures concerning culture..............................................................................17

2.1.1 Refundable tax credit for Québec film or television production ................17

- 2 -

2.1.2 Refundable tax credit for musical productions .........................................26

2.1.3 Refundable tax credit for sound recordings..............................................29

2.1.4 Change to the period within which expenditures giving rise torefundable tax credits relating to the cultural field must be paid...............31

2.2 Clarifications concerning the tax holiday for small and medium-sizemanufacturing enterprises in remote resource regions.......................................32

2.3 Streamlining measure regarding the eligibility certificate for the refundabletax credit for the Vallée de l'aluminium ...............................................................34

2.4 Streamlining measure regarding the eligibility certificate for the refundabletax credit for Gaspésie and certain maritime regions of Québec ........................36

2.5 Changes to the refundable tax credit for processing activities in theresource regions .................................................................................................37

2.6 Refundable tax credits for scientific research and experimentaldevelopment .......................................................................................................38

2.7 Streamlining of the notion of qualified corporation and clarification of thenotion of qualified business for the purposes of certain refundable taxcredits .................................................................................................................39

2.8 Change to the special tax applicable to environmental trusts .............................41

2.9 Streamlining of rules regarding the transfer of property with no immediatetax impact ...........................................................................................................42

2.10 Additional items allowing a financial institution to claim a deduction forinvestments regarding investments in a corporation engaging in thesecurities trade ...................................................................................................45

2.11 Adjustments concerning activities performed in the course of operating aninternational financial centre with participants in the investor immigrantprogram ..............................................................................................................47

2.12 Increase in available floor space in certain designated sites ..............................49

- 3 -

3. MEASURES CONCERNING CONSUMPTION TAXES .....................................52

3.1 Measures to enhance compliance with the tax rules in the garment industry .....52

3.2 Application of the specific tax on lodging in the Charlevoix and Outaouaistourist regions .....................................................................................................54

3.3 Clarification concerning the information and documents that may be soughtby a formal demand ............................................................................................55

4. MEASURES CONCERNING HARMONIZATION...............................................57

4.1 Notice of Ways and Means Motion of March 16, 2001 .......................................57

4.2 Department of Finance Canada news release of April 12, 2001.........................61

APPENDIX

1. MEASURES CONCERNING INDIVIDUALS

1.1 Confirmation of the right of an individual making support payments toclaim a tax credit regarding the child whose custody he shares

Under the tax legislation, a taxpayer may claim, for a taxation year, a non-refundabletax credit regarding a child of whom he is the father or mother, provided in particularthat the child, at any time during the year, ordinarily lived with him and was hisdependant.

In the event that many taxpayers claim a tax credit regarding the same child, the taxlegislation stipulates that they must agree to share the amount of the tax credit betweenthem. Failing an agreement, the Minister of Revenue may set the amount each of thesetaxpayers can deduct in calculating his tax otherwise payable.

However, since taxation year 1986, the law stipulates a special rule to prevent ataxpayer who makes support payments for the maintenance of a spouse or a child fromclaiming, in certain circumstances, a tax credit (a deduction prior to 1988) regarding theperson for whose benefit the support payment is made.

From 1986 to 1996, the main objective of this special rule was to prevent a taxpayerfrom both claiming regarding his spouse or his child, for a taxation year after the one inwhich his union failed, a deduction for the support payment he had paid for themaintenance of either of these persons and a personal exemption or a tax credit, as thecase may be, regarding the same person. However, the rule did not have the effect ofdenying this possibility to a taxpayer whose child was covered by joint custody.

In addition, although support payments for children were made exempt from tax in 1997,this special rule was maintained to prevent an individual making a support payment forthe maintenance of a spouse or a child from claiming, for a taxation year after the one inwhich his union failed, a tax credit regarding his spouse or a child not covered byshared custody.

- 2 -

While the fiscal policy seeks to allow taxpayers sharing custody of their children to claima tax credit for dependent children, it is possible, in view of the wording of the legislativeprovision setting out the special rule, that a tribunal may decide that the Minister ofRevenue may not, in the absence of an agreement between the parents sharingcustody of a child, distribute between them the amount of the tax credit claimedregarding the child if one of the parents makes, at a regular frequency during the entireyear, a support payment for the child’s maintenance.

Considering that the tax legislation stipulates that a child must, as a general rule,ordinarily live with the taxpayer claiming the tax credit in his regard and that the value ofthis tax credit must be divided between all the taxpayers claiming such a tax credit, andthat the number of orders stipulating shared custody of children continues to increase,the special rule applicable to individuals making support payments for the maintenanceof a child no longer appears necessary.

Furthermore, since the wording of the legislative provision granting a tax credit for aspouse was also amended in 1997 to stipulate that a taxpayer is entitled to an amountfor a person who, at any time during the year, is his spouse if, at that time, he providesfor the needs of such person from whom he does not live separate and apart becauseof the failure of their union, there is no longer any reason for the special rule applicableto individuals making support payments for the maintenance of a spouse.

The tax legislation will therefore be amended to eliminate, as of taxation year 2001, thespecial rule applicable to individuals making support payments for the maintenance of aspouse or a child. Furthermore, for non-prescribed taxation years prior to 2001, the taxlegislation will be clarified to confirm that the individual making a support paymentregarding whose custody he shares may, if he satisfies the conditions otherwisestipulated, claim a tax credit regarding such child.

1.2 Possibility of spreading out the taxation of a lump-sum pay equitypayment made by certain municipal employers

Generally, employers covered by the Pay Equity Act must, no late than November 21,2001, pay the first pay adjustments required to reach pay equity, and may spread thepayment of a pay adjustment amount over a maximum of four years.

- 3 -

For some employers, namely municipalities or other municipal bodies affected by areorganization, special rules were stipulated in the Act respecting municipal territorialorganization to, in particular, postpone the date at which they must make the payadjustments required to reach pay equity.

By the deadline specifically applicable under these rules, these employers must, inaccordance with the provisions stipulated in the Act respecting municipal territorialorganization, make a lump-sum payment, in lieu of the amount of pay adjustment thatwould normally have been due to be paid for hours worked since November 21, 2001, ifthe date of payment of the pay adjustments had not been postponed.

Under the tax rules, the full amount of the lump-sum pay adjustment payment must beincluded in calculating the income from an office or employment for the taxation year inwhich it is received, even if part of this payment relates to prior taxation years.

Furthermore, this lump-sum pay adjustment payment is not eligible for the incomeaveraging mechanism stipulated in the tax system and which allows an individual to paythe tax relating to certain retroactive payments, such as income from an office oremployment received pursuant to a judgement or other arbitration ruling or supportpayment arrears, as if it had been received in the course of the year to which it relates.

Because of the progressive nature of the tax rates, the individual receiving a lump-sumpay adjustment payment paid in accordance with the special pay equity rules stipulatedin the Act respecting municipal territorial organization, may be disadvantaged comparedto an individual whose employer is not covered by these rules, since he will have to paya higher tax burden regarding a pay adjustment required to reach pay equity.

In the interests of fairness to individuals in such a situation, the tax legislation will beamended to make the lump-sum pay adjustment payment that will be paid inaccordance with the special pay equity rules stipulated in the Act respecting municipalterritorial organization eligible for the averaging mechanism for retroactive lump-sumpayments.

In this way, individuals will avoid paying, regarding a lump-sum pay adjustment paymentrequired to reach pay equity, more tax than they would have had to pay had thepayment been received and taxed steadily over each of the years in which it waspayable.

- 4 -

This change will apply regarding lump-sum pay adjustment payments received afterDecember 31, 2001.

1.3 Broadening of fiscal measures relating to property with undeniableecological value

The tax system stipulates various tax relief measures to encourage taxpayers to makegifts that contribute to the protection and development of Québec’s ecological heritage.

Briefly, these tax relief measures consist of a deduction in calculating taxable income ora non-refundable tax credit depending on whether the donor is a corporation or anindividual, respectively, and a reduction by half of the inclusion rate of the capital gainthat may result from the alienation, by donation, of ecological property.

To give rise to this tax relief, the gift must be made to the Québec government, aQuébec municipality or a registered charity whose mission in Québec is recognized bythe Minister of the Environment, and consist of any of the following properties:

— land located in Québec, whose fair market value is certified by the Minister of theEnvironment and which, in the Minister’s view, has undeniable ecological value;

— a real servitude, whose fair market value is certified by the Minister of theEnvironment, that encumbers the whole or part of a land located in Québec andwhich, in the Minister’s view, has undeniable ecological value and is consented infavour of a land belonging to one of the donees listed above.

In general, the fair market value of the property, as certified by the Minister of theEnvironment, must be used in calculating the deduction or non-refundable tax credit forgifts, as the case may be, and constitutes the proceeds of alienation of the property forthe purposes of determining the capital gain or loss that may result from its donation.

When the property is a real servitude, the capital gain or loss must, in addition, bedetermined using a special rule designed to establish the adjusted cost base of theservitude by deeming a certain amount in this regard, so as to attribute to it a portion ofthe adjusted cost base of the land it encumbers.

- 5 -

1.3.1 Recognition of the government of Canada as donee

Under existing rules, a taxpayer who donates to the government of Canada land locatedin Québec and having undeniable ecological value or who consents a real servitudeencumbering such land in favour of land belonging to the government of Canada, maynot claim the tax relief specific to ecological gifts.

In some circumstances, the government of Canada appears to be the entity in the bestposition to receive the gift of such property because, for example, the property islocated near a natural site belonging to it.

Amendments will accordingly be made to the tax legislation to recognize, for thepurposes of the tax relief relating to ecological gifts, the government of Canada as adonee eligible to receive a gift of land located in Québec and having undeniableecological value or a real servitude encumbering such land, it being understood, in thelatter case, that the real servitude must be consented in favour of land belonging to thegovernment of Canada.

These changes will apply regarding a gift of such property made after the day ofpublication of this information bulletin.

1.3.2 Eligibility of certain property located outside Québec

Currently, the gift must involve property located in Québec to give rise to the tax reliefrelating to ecological gifts.

This rule was implemented in agreement with the objectives of protecting anddeveloping Québec’s ecological heritage pursued by these fiscal measures.

In certain specific cases, such as the protection of a wildlife species consideredendangered or vulnerable by the government, the gift of property located in a regionbordering Québec may, just as the gift of property located in Québec, help to protectand develop the ecological heritage of Québec.

- 6 -

Consequently, amendments will be made to the tax legislation so that the gift of certainproperty located outside Québec in favour of a recognized donee may, like the gift ofproperty located in Québec and subject to the same conditions and restrictions, giverise to the application of the tax relief relating to ecological gifts.

More particularly, the property located outside Québec that may, in the event of theirdonation, give rise to the application of this tax relief, is as follows:

— land located outside Québec in a border region, if the following conditions aremet:

– the fair market value of the land is certified by the Minister of theEnvironment;

– in the Minister’s view, the land has undeniable ecological value and itspreservation and conservation are important for the protection anddevelopment of Québec’s ecological heritage;

— a real servitude encumbering the whole or part of land located outside Québec ina border region and which constitutes, in the view of the Minister of theEnvironment, land with undeniable ecological value and whose preservation andconservation are important for the protection and development of Québec’secological heritage, if the following conditions are met:

– the fair market value of the servitude is certified by the Minister of theEnvironment;

– the servitude is consented in favour of land belonging to a recognizeddonee.

The following entities will be recognized as donees:

— a government, municipality or other public body exercising government functions;

— a registered charity one of whose major missions is, in the view of the Minister ofthe Environment of Canada, the conservation and protection of Canada’senvironmental heritage and which is approved, in relation to the gift consented toit, by the Minister of the Environment of Québec.

- 7 -

For greater clarity, in general, the fair market value of the property as certified by theMinister of the Environment will be used in the calculation of the deduction or thenon-refundable tax credit for gifts, as the case may be, and will constitute the proceedsof alienation of such property for the purposes of determining the capital gain or lossthat may result from its donation.

Furthermore, when the donated property is a real servitude, its adjusted cost base mustbe determined according to the same procedures that currently obtain regarding suchproperty encumbering land located in Québec.

Lastly, a taxpayer may only claim a deduction in calculating his taxable income or anon-refundable tax credit for gifts, as the case may be, regarding a gift of propertylocated outside Québec, if he provides the Minister of Revenue with the certifications ofthe Minister of the Environment concerning the fair market value of such property andthe undeniable ecological value of the land and the importance of its preservation andconservation for the protection and development of Québec’s ecological heritage. Whenthe gift is made in favour of a registered charity, the taxpayer must also provide theMinister of Revenue with the approval of such charity given in writing by the Minister ofthe Environment in relation to such gift.

These changes will apply regarding to a gift of property located outside Québec madeafter the day of publication of this information bulletin.

1.4 Tax benefits granted to the office of a political division of a foreign state

Although the Québec government has not declared itself bound by the ViennaConvention on Diplomatic Relations and the Vienna Convention on Consular Relations,it generally recognizes that the provisions of these conventions are minimum standardsregarding privileges and immunity.

Accordingly, Québec's tax regulations provide members of diplomatic missions andconsular posts as well as members of their families with a variety of tax benefits that gobeyond what is stipulated in these agreements.

- 8 -

More specifically, the members of a consular post, other than an honorary consularofficer, who are neither Canadian citizens nor permanent residents, currently benefit,provided they do not carry on a business in Québec or hold any office or employmentthere other than their function with the government they represent, from an exemption ofduties imposed under the Taxation Act and a refund of consumption taxes imposed by alaw of Québec regarding a moveable good or a service.

Furthermore, provided they satisfy certain conditions, the members of the families ofmembers of a consular post enjoy the same tax benefits as the latter.

In addition, Québec’s tax regulations stipulate that a foreign government is exempt fromany municipal or school real estate tax on an immovable it owns, if such immovable isrecognized by the Minister of International Relations as intended exclusively for consularpurposes, and from any personal tax or municipal compensation it could be required topay because it is the owner, lessee or occupant of such an immovable, except thoselevied separately and collected in payment of services rendered.

For many years now, the Québec government has hosted the DélégationWallonie-Bruxelles on its territory. Since the functions performed in Québec by thisdelegation are broadly comparable to those of a consular post, the Québec governmenthas granted the office of this delegation, its delegate and the members of his familyadvantages similar to those accorded a consular post and the persons connected to it.

Considering that it is appropriate to extend this preferred treatment to other delegationsor representations of a political division of a foreign state that the Québec governmentmay host on its territory, the existing regulations will be amended to grant the office of apolitical division of a foreign state and the persons with a connection to it the same taxbenefits as those granted to consular posts and the persons with a connection to them,provided such office is recognized as carrying out in Québec functions broadlycomparable to those of a consular post.

To benefit from this preferred tax treatment, the office of a political division of a foreignstate must be recognized by the Minister of Finance upon recommendation by theMinister of International Relations.

For the purposes of such recognition, a province, state or similar division of a foreignstate will be considered a political division of a foreign state.

- 9 -

More specifically, the Regulation respecting fiscal privileges granted to members of adiplomatic mission or consular post and to the members of their families, will beamended to stipulate that the office of a political division of a foreign state recognized ascarrying out in Québec functions broadly comparable to those of a consular post, maybenefit from an exemption or a refund, as the case may be, of consumption taxesimposed under a law of Québec regarding a good or a service, subject to the sameconditions and restrictions as those currently imposed on an international governmentorganization that has reached an agreement with the Québec government.

This regulation will also be amended to stipulate that persons with a connection to suchan office, i.e. members of such office who are neither Canadian citizens nor permanentresidents of Canada and the members of their families, may benefit, subject to the sameconditions and restrictions, from tax benefits relating to income tax and consumptiontaxes granted to consular officers and consular employees as well as to members oftheir families.

For greater clarity, the members of the office of a political division of a foreign state whoare employees in the administrative or technical departments of such office will beconsidered similar to consular employees.

Furthermore, the Regulation respecting the municipal and school tax system applicableto the governments of the other provinces, foreign governments and internationalbodies, will be amended to stipulate that the government of a political division of aforeign state will be exempt from any municipal or school real estate tax on animmovable it owns if such immovable is recognized by the Minister of InternationalRelations as intended exclusively for purposes broadly comparable with consularpurposes, and from any personal tax or municipal compensation it could be required topay because it is the owner, lessee or occupant of such an immovable, except thoselevied separately and collected in payment of services rendered.

These regulatory amendments will confirm the preferred treatment currently granted tothe Délégation Wallonie-Bruxelles, its delegate and members of his family.

In addition, it is also appropriate to recognize, for the purposes of these measures, theReprésentation du Gouvernement de l’État de la Bavière, which the Québecgovernment hosts on its territory.

- 10 -

The latter will be able to benefit, retroactive to January 1, 1999, from the exemptionsgranted by the Regulation respecting the municipal and school tax system applicable tothe governments of the other provinces, foreign governments and international bodies,and may obtain a refund of consumption taxes imposed under a law of Québec that ithas paid since the same date.

Furthermore, the members of this Représentation and the members of their families willbenefit, subject to the same conditions and restrictions, from the tax benefits grantedunder the Regulation respecting fiscal privileges granted to members of a diplomaticmission or consular post and to the members of their families to persons with aconnection to a consular post, as of taxation year 2001 in the case of income tax, andas of August 1, 2001 in the case of consumption taxes.

1.5 Introduction of a deduction for foreign producers

In recent years, various players have made substantial efforts to attract foreign filmproductions to Québec.

These efforts have in particular led to the installation of top-quality infrastructures andthe supply of highly sophisticated technical services in 2D and 3D animation and digitalvisual effects, that have made Québec a choice location for shooting foreign filmproductions.

To support these efforts and stimulate job creation in this sector of the economy, thegovernment introduced, in the March 31, 1998 Budget Speech, the refundable tax creditfor film production services, which generally gives rise to tax assistance of 11%regarding certain Québec labour expenditures incurred in the course of shooting aneligible foreign production.

To ensure that Québec maintains its competitive position regarding foreign filmproductions and to further encourage such productions to come to Québec, anothertype of tax assistance will be provided as of taxation year 2001, so that payments aneligible individual receives for services provided in Québec as producer, as part of aneligible production, will be non-taxable in his hands.

- 11 -

In general, such tax assistance will consist of a deduction in calculating the taxableincome of the eligible individual or, if applicable, in calculating his income earned inQuébec and his income earned in Canada, depending on whether or not the provisionsof Part II of the Taxation Act are applicable for the purposes of calculating his income.

❏ Eligible individual

For the purposes of this measure for a given taxation year, the expression "eligibleindividual" means an individual who, as a matter of fact, has not resided in Canada atany time of the given year.

❏ Eligibility conditions

To benefit from this tax relief for a taxation year, the eligible individual must haveworked, during the year, as a producer as part of an eligible production, as certified in acertificate issued, for the year, by the Société de développement des entreprisesculturelles (SODEC) and enclosed with his tax return for such year.

In general, SODEC will recognize as a producer, an individual who is responsible fordecision-making throughout the development of the project and the production of a film.

The notion of eligible production will have essentially the same meaning as the meaningadopted for the purposes of the refundable tax credit for film production services,without the criterion designed to avoid an accumulation of tax credits. Consequently,SODEC will recognize a given production as an eligible production according to thesame criteria as those it already uses to certify a production for the purposes ofobtaining this tax credit.

Briefly, a production will be recognized as an eligible production, if, in particular, itsatisfies certain minimum cost rules and does not fall into a category of productionexcluded from the application of the refundable tax credit for Québec film or televisionproduction.

- 12 -

❏ Calculation details of the deduction

An eligible individual whose income, for a taxation year, is calculated without taking intoaccount the provisions of Part II of the Taxation Act because he is deemed to reside inQuébec all year having sojourned there for one or more periods totalling at least183 days and who, according to the certificate issued for such year by SODEC, works,during the year, as a producer as part of an eligible production, may deduct, incalculating his taxable income for the year, an amount equal to the excess:

— of all the amounts each of which represents a payment, including a wage orsalary, received for services supplied in Québec as part of the eligible productionand which were included in the calculation of his income for the year; over

— all the amounts deducted in calculating his income for the year and which mayreasonably be considered attributable to such services.

In the case where the provisions of Part II of the Taxation Act apply for calculating theincome of an eligible individual for a taxation year, this deduction will be reflected in thecalculation of his income earned in Québec and of his income earned in Canada.

❏ Income tax source deductions

This new deduction for foreign producers will automatically be taken into account incalculating income tax source deductions for any payment made after the date ofpublication of this information bulletin.

1.6 Clarification of the fiscal policy relating to allowances for the use of amotor vehicle

Under the current tax legislation, an individual is not required to include in thecalculation of his income reasonable allowances for the use of a motor vehicle hereceives from his employer to travel in the performance of his duties.

- 13 -

In this regard, the legislation stipulates that the allowance an individual receives for theuse of a motor vehicle in relation to his office or employment or in the course thereof, isdeemed not to be reasonable when the measurement of the use of the vehicle, for thepurposes of the allowance, is not made solely on the basis of the number of kilometrestravelled by the vehicle during such use in relation with the office or employment of theindividual or in the course thereof.

By relying on this legislative presumption, the ministère du Revenu du Québec (MRQ)considers that when an employer pays an allowance of a fixed amount that is not basedon the number of kilometres actually travelled by the employee, this allowance istaxable and must be included in calculating the various contributions payable by anemployer on his payroll. However, the employee who receives such allowance may, ifhe satisfies certain conditions, deduct, in calculating his income, the amounts he spentfor the use of his motor vehicle.

The position of the MRQ, which is intended to reflect current fiscal policy, has recentlybeen called into question by the Québec Court of Appeal. In a decision handed down onDecember 18, 2000,1 the Court of Appeal substantially restricted the scope of thepresumption stipulated in the Taxation Act by stating that this presumption simplyrequires that the mileage travelled by the sole basis of reference in the measurementused to determine the amount allocated as an allowance.

Taking the view that the position of the MRQ resulted in transforming the concept ofallowance into a refund of expenses, the Court of Appeal considered that such anallowance set on the basis of the estimated mileage travelled annually according to anextrapolation of the actual kilometres travelled by employees during a reference period,could be reasonable.

Since this decision runs against fiscal policy, the legislation will be amended to specifythat an allowance will be deemed not to be reasonable if the measurement of the use ofthe motor vehicle, for the purposes of such allowance, was not made solely on the basisof the number of kilometres actually travelled by the motor vehicle during its use inrelation with the office or employment of an individual or in the course thereof.

1 Sous-ministre du Revenu du Québec v. Ville de Beauport (file 200-09-002160-981).

- 14 -

This change will apply by declaration. However, it will not apply regarding casespending before the courts on the day of publication of this information bulletin, or tonotices of objection served on the Minister of Revenue no later than such day, when thereasonable nature of an allowance for the use of a motor vehicle was contested no laterthan that day in such cases or such notices, and the grounds of the objection are theitems covered by this change.

1.7 Obligation to file an information return regarding certain contractualpayments and amounts paid as subsidies

The current tax regulations stipulate an obligation to file returns with the Minister ofRevenue of Québec regarding various information necessary for the establishment ofassessments stipulated by the Taxation Act and to forward, if applicable, a copy of suchreturns to any person they concern.

Since it has been shown that taxpayers comply more readily with the tax legislationwhen information returns are filed regarding amounts paid to them, new measures willbe implemented as of 2002 to encourage taxpayers to better comply with the tax laws,and make the tax system fairer.

1.7.1 Reporting of certain contractual payments paid by governmentdepartments and budget-funded bodies

Québec’s economy includes a growing number of self-employed workers and smallunincorporated businesses. In the absence of information returns and sourcewithholdings regarding amounts paid under a contractual relationship, non-compliancewith the tax laws is on the rise.

To improve compliance with the tax laws, the departments of the Québec governmentand the budget-funded bodies listed in Schedule 1 of the Financial Administration Actwill be required to file an information return regarding any person or partnership towhom an amount, other than an excluded amount, is paid directly or indirectly (i.e.credited to his account), during a particular calendar year after 2001, for delivery ofservices by him or on his behalf or both as such and for the sale or rental of goods.

- 15 -

In this regard, the expression "excluded amount" means the following amounts:

— an amount paid, wholly or almost wholly, during the year for the sale or rental ofgoods;

— an amount regarding which another information return must be filed for the yearin accordance with Québec's tax regulations;

— an amount that does not have to be included in calculating the income of itsrecipient, if the latter is an employee of a government department orbudget-funded body;

— an amount paid for the delivery of services outside Canada to a recipient whowas not a resident of Canada at the time of such delivery;

— an amount paid to person whose identity must be protected;

— an amount paid to a government or to a government corporation.

However, no statement need be produced by a government department orbudget-funded body regarding amounts paid, other than an excluded amount, during agiven year to a person or partnership for the delivery of services by him or on his behalfor both as such and for the sale or rental of goods, if the total of such amounts thus paidduring the year is less than $1 000.

For greater clarity, in every case where a information return must be filed regarding acontractual payment made by a government department or budget-funded body to aperson or a partnership, the latter must in particular must provide such entity with hisidentification number, namely his social insurance number if such person is anindividual, or his Québec enterprise number otherwise.

Government departments and budget-funded bodies must forward the informationreturns to the Minister of Revenue no later than the last day of February each yearregarding the preceding calendar year. These entities must also provide each person orpartnership regarding which a return must be filed for a year with a copy of the portionof the return that concerns it no later than the date on which such return must be filedwith the Minister of Revenue.

- 16 -

1.7.2 Information return regarding subsidies

Under the current tax legislation, subsidies received by a taxpayer may, as the casemay be, reduce the cost or the capital cost of an asset, reduce the amount of adisbursement or an expenditure or constitute income for the taxpayer.

To improve compliance with the tax legislation, the Regulation respecting the TaxationAct will be amended to stipulate that any entity responsible for the payment of a subsidywill be required to file an information return indicating the amounts paid as such, duringa particular calendar year after 2001, to a person or partnership.

In this regard, the expression "subsidy" will include government transfer payments,other than the amounts paid to contribute to the funding of public bodies, the health andeducation networks and the municipal sector, but will not include an amount regardingwhich another information return must be filed for the year in accordance with Québec'stax regulations.

The entities responsible for the payment of subsidies must forward the informationreturns to the Minister of Revenue no later than the last day of February each yearregarding the preceding calendar year. These entities must also provide each person orpartnership regarding which a return must be filed for a year with a copy of the portionof the return that concerns it no later than the date on which such return must be filedwith the Minister of Revenue.

- 17 -

2. MEASURES CONCERNING BUSINESSES

2.1 Measures concerning culture

The government bolsters the development of cultural industries with a number ofrefundable tax credits that sustain the activities of Québec businesses. To maintain taxassistance for businesses operating in the cultural field and ensure compliance with theobjectives of the tax credits allowed in this regard, adjustments will be made to the taxcredit for Québec film or television production, to the tax credit for musical productionsand to the tax credit for sound recordings. Lastly, technical clarifications will be made toall tax credits relating to the cultural field, regarding the period within which theexpenditures giving rise to these tax credits must be paid.

2.1.1 Refundable tax credit for Québec film or television production

The refundable tax credit for Québec film or television production applies to labourexpenditures incurred by a corporation that produces a Québec film, as this expressionis defined in the Regulation respecting the recognition of a film as a Québec film. Thistax credit generally corresponds to 33 �% of the eligible labour expenditures incurred toproduce the film.

However, the labour expenditures that give rise to the refundable tax credit for film ortelevision production may not exceed 45% of the production expenses of the film, sothat the tax assistance generally may not exceed 15% of such expenses.

In the latter regard, the tax legislation allows various amounts to be included incalculating the production expenses of a film, even though no amount has actually beenincurred.

In recent months, the ministère des Finances, working with various stakeholders, hasstudied the changes that should be made to simplify the rules for calculating therefundable tax credit for Québec film and television production.

- 18 -

This process, and the representations made by members of the industry, has led to theconclusion that a structural change to this tax credit, using labour expenditures as thesole parameter for the calculation, without the cap based on production expenses, couldcause instability to the financial structure of film or television productions.

In this context, changes will be made to the refundable tax credit for film and televisionproduction to simplify the calculation. In particular, the cap based on productionexpenses will be retained in the calculation of the tax credit, but changes will be maderegarding the components of production expenses. These changes will be prospectivein scope.

In addition, changes favourable to the film and television industry, and retroactive inscope, will be made to ensure that the objective of the fiscal policy is met, in particularconcerning productions for which an application for an advance ruling has been filedwith the Société de développement des entreprises culturelles (SODEC), or for whichan application for final certification has been filed with SODEC if no application for anadvance ruling has been filed, no later than August 31, 2001.

❏ Simplification of the calculation of the production expenses of a film

Currently, a portion of the production expenses of a film can consist of producer’s feesand general administration expenses deemed incurred, as well as amountsrepresenting the value of the use, without consideration, of goods or services.

More specifically, the tax legislation allows the eligibility, as production expenses, of anamount as producer’s fees and an amount as general administration expenses each ofwhich is equal to the greater of the expenses actually incurred or 10% of the total ofshooting expenses and post-production expenses. However, the total of the producer’sfees and the general administration expenses may not exceed 25% of the total shootingexpenses and post-production expenses.

The tax legislation also allows the eligibility, as production expenses, of an amountequal to the fair market value of the use, without consideration, of goods or services inthe course of the production of a film.

- 19 -

— Withdrawal of amounts deemed incurred as producer’s fees andgeneral administration expenses

To simplify the calculation of the tax credit for film or television production and toprovide members of the industry with greater predictability of the amount of the taxcredit in their financial structure, the tax legislation will be amended so that only theamounts actually incurred for the production of a film are included in the calculation ofthe production expenses of the film.

More specifically, the tax legislation will be amended so that the production expenses ofa film no longer contain an amount deemed incurred as producer’s fees and an amountdeemed incurred as general administration expenses each of which corresponds to10% of the total of the shooting expenses and the post-production expenses.Accordingly, amounts as producer’s fees and as general administration expenses maybe included in the calculation of the production expenses of a film only if they have beenactually incurred for the production of the film.

— Withdrawal of the value of the use, without consideration, ofgoods or services

Furthermore, the tax legislation will be amended so that the value of the use, withoutconsideration, of goods or services, may no longer be included in the calculation of theproduction expenses of a film.

— Expenses directly attributable to the production of a film

As a consequence of these changes, no reference will henceforth be made to theexpenses relating to the shooting and post-production stages of a film in establishingthe amount of production expenses of the film. Accordingly, the production expenses ofa film will include solely the expenses actually incurred that are directly attributable tothe production of the film.

In this regard, some expenses, for instance expenses relating to sub-titling or dubbing afilm, financial expenses or legal expenses, may be incurred after the trial print or thedate of recording the master tape of the film, and still constitute expenses directlyattributable to the production of the film. Accordingly, such expenses should berecognized in the calculation of the production expenses of a film, provided suchexpenses would not have been incurred had the film not been produced.

- 20 -

– Obligation to pay production expenses

Furthermore, currently, in the calculation of the production expenses of a film, the taxlegislation only stipulates the obligation for the corporation to incur such expenses butnot to pay them, while stipulating that the labour expenditures giving rise to the taxcredit must be paid. Since the amount of tax assistance provided by this tax creditdepends on both labour expenditures and the total of the production expenses directlyattributable to the production of a film, henceforth any expenditure included in theproduction expenses of a film must be incurred and paid before a corporation can claima tax credit in this regard.

For greater clarity, production expenses incurred in the course of the production of afilm but not paid before a corporation claims this tax credit in relation to a given taxationyear, will not be included in the calculation of the cap based on production expenses toestablish the amount of the tax credit for such given taxation year, but may be in relationto a subsequent taxation year provided they have been paid before the corporationclaims this tax credit for such subsequent taxation year.

In view of the above, the tax legislation will be amended so that the productionexpenses of a film include solely the expenses directly attributable to the production ofthe film, that are incurred during the period running from the screenplay to thepost-production of the film, or within a longer period considered reasonable by theMinister of Revenue, and that are paid by the production corporation, subject to thefollowing section regarding the eligibility of part of the acquisition cost of an asset,before the corporation claim this tax credit.

– Eligibility of part of the acquisition cost of an asset

In this regard, the tax legislation will also be amended to specify that the productionexpenses directly attributable to the production of a film include a portion of theacquisition cost of assets belonging to the production corporation, and that it uses in thecourse of the production of a film.

The portion of the acquisition cost of such assets that may be included in the productionexpenses of a film will correspond to the portion of the accounting depreciation of suchassets, for a year, relating to the use the corporation has made of its assets, in suchyear, in the course of the production of the film.

- 21 -

For greater clarity, all the amounts thus included in the production expenses of severalfilms, in relation to a given asset, must not exceed the total accounting depreciation ofsuch asset.

– Extension beyond post-production of the period duringwhich expenses may be incurred for the production of a film

Furthermore, the period following the post-production of a film, within which the Ministerof Revenue may recognize certain expenditures as production expenses of a film, maynot exceed the date of the application for final certification of the film with SODEC.

As a corollary to this change conferring on the Minister of Revenue the power torecognize certain expenditures as production expenses of a film after thepost-production of the film, an amendment will be made to the tax legislation so that thelabour expenditures incurred in the course of production of a film and giving rise to thistax credit may also be incurred within a longer period, considered reasonable by theMinister of Revenue, than the period running from the screenplay to the post-productionof the film, subject to the limit described above relating to the date of the application forfinal certification of the film.

Accordingly, for illustration purposes, expenses relating to the sub-titling of a film thatare incurred by a corporation in the course of the production of the film, after the trialprint or the date of recording of the master tape of the film, but before the date of theapplication for final certification of the film with SODEC, may be recognized by theMinister of Revenue as labour expenditures and production expenses of the film, if allthe conditions otherwise applicable for the purposes of the tax credit are satisfied.

— Advantage, benefit or refund reducing the financial charge ofthe production corporation

In some circumstances, the financial charge of a corporation in relation to a film it hasproduced may be reduced when, for instance, it obtains a benefit, an advantage or arefund from a third party, or if it alienates an asset belonging to it that it used in thecourse of the production of the film.

- 22 -

So that the expenses directly attributable to the production of a film reflect the financialcharge actually borne by a corporation, the tax legislation will be amended so that, for agiven taxation year for which such corporation claims this tax credit, the productionexpenses of the film are reduced, subject to the amounts of government andnon-government assistance otherwise prescribed for the purposes of the tax credit, bythe amount of any advantage, benefit or refund the corporation has obtained, is entitledto obtain or may reasonably expect to obtain, no later than the filing deadline applicableto it for such given taxation year, whether in the form of compensation, guarantee ofproceeds of alienation of an asset that exceeds the fair market value of such asset, or inany other form or in any other way.

Furthermore, the portion of the proceeds of the alienation of an asset relating to aportion of the cost of acquisition of such asset that has already been included in theproduction expenses of a film will be considered an advantage.

For greater clarity, when the portion of the acquisition cost of an asset belonging to acorporation is included in the production expenses of a film the corporation hasproduced2, the portion of the proceeds of the alienation of such asset in excess of theportion of the acquisition cost of such asset that has not been depreciated in the courseof the production of the film, will be considered an advantage.

For illustration purposes, for a given film, if an asset belonging to a corporation hasbeen used by the corporation and an amount of $10, representing depreciation of 10%of such asset ($100 * 10%), has been included up to $5 in the calculation of theproduction expenses of the film and of another film respectively, and such asset isresold at $100 no later than the filing deadline applicable to the corporation for thetaxation year in which it claims this tax credit regarding the given film, an amount of$5 must be deducted in the calculation of the production expenses of the given film.

— Limit on the amount of production expenses

As mentioned above, the tax legislation stipulates that the total of the producer’s feesand general administration expenses relating to a film may not exceed 25% of the totalshooting expenses and post-production expenses of the film.

2 As mentioned above, the portion of the acquisition cost of an asset, in such circumstances,

corresponds to the portion of the accounting depreciation of such asset, for a year, relating to theuse made by the corporation of such asset, in such year, in the course of the production of thefilm.

- 23 -

Given the changes that will be made to the tax legislation regarding the expensesactually incurred that are directly attributable to the production of a film, and morespecifically concerning the lack of reference to the shooting and post-production stagesof a film, the tax legislation will be amended so that this 25% limit is withdrawn.

However, to prevent amounts substantially greater than the standards generallyrecognized by the industry from being included in the calculation of the productionexpenses of a film, the tax legislation will be amended so that the Minister of Revenuemay refuse to recognize, as production expenses of a film, any amount included in theproduction expenses of the film that he considers unreasonable compared to industrystandards.

— Increase in cap based on production expenses

Because of the changes made to the components of the production expenses of a film,the tax legislation will be amended to raise the cap based on the production expensesof a film, in order to maintain the amount of tax assistance currently provided by this taxcredit.

Accordingly, the rate of the cap based on the production expenses of a film will beincreased to 50%.

❏ Application date

These changes will apply regarding a film or television production for which anapplication for an advance ruling is filed with SODEC after August 31, 2001.

❏ Clarification concerning the notion of producer’s fees and generaladministration expenses

Regarding film or television productions for which an application for an advance ruling isfiled with SODEC after the day of publication of this information bulletin, thesimplifications to the calculation of the tax credit, and more specifically regarding theamounts relating to producer’s fees and to general administration expenses, will havethe effect of resolving the differences in interpretation that have arisen between theministère du Revenu and members of the film industry.

- 24 -

Furthermore, to ensure that the objective of the fiscal policy underlying this tax credit isalso satisfied for prior years, more specifically regarding the portion of the productionexpenses of a film that may consist of an amount of producer’s fees and an amount ofgeneral administration expenses deemed incurred, changes will be made to the taxlegislation to specify the notions of producer’s fees and of general administrationexpenses.

More specifically, the tax legislation will be amended to specify that the producer’s feesand general administration expenses incurred for the production of a film and which aredirectly attributable to the production of the film, such as for example, the expenses of aproduction office, secretarial expenses relating to the screenplay, the fees of theproduction manager and those of the production accountant, fees relating to thenegotiation of actors' contracts, insurance expenses as well as expenses for auditsrequired by investors, must be included in the calculation of the total shooting expensesand post-production expenses of a film.

Furthermore, the tax legislation will be amended so that some expenses, for instanceexpenses relating to the sub-titling or dubbing of a film, financial expenses or legalexpenses, incurred after the trial print or the date of recording the master tape of thefilm, and that are directly attributable to the production of the film, may be included inthe calculation of the production expenses of the film.

More specifically, the tax legislation will be amended so that the production expensesdirectly attributable to the production of a film, that are incurred in the course of theproduction of the film after the trial print or the date of recording the master tape of thefilm, within a period considered reasonable by the Minister of Revenue, are included inthe calculation of the production expenses of the film.

In this regard, the period within which the Minister of Revenue may recognize certainexpenditures as production expenses of a film may not exceed the nearer of the dayfollowing twelve months after the date of the trial print or of the recording the mastertape of the film, or the day of the application for final certification of the film withSODEC.

These changes will apply regarding productions for which an application for an advanceruling is filed with SODEC, or for which an application for final certification is filed withSODEC if no application for an advance ruling has been filed, no later than August 31,2001.

- 25 -

They also apply regarding a taxation year for which a corporation has benefited fromthis tax credit regarding a production, except regarding taxation years prescribed theday of publication of this information bulletin. Lastly, these changes will apply regardinga taxation year for which a notice of objection, an appeal or a waiver of prescription hasbeen duly served on the Minister of Revenue, before day of publication of thisinformation bulletin.

❏ Document to enclose with the application for final certification of aQuébec film or television production

According to the Regulation respecting the recognition of a film as a Québec film, anapplication for final certification regarding a Québec film or television production mustbe filed with SODEC within the twelve months following the date of recording the mastertape or trial print of such production.

In addition, according to this regulation, one of the Québec content criteria of a Québecfilm or television production consists of a minimum percentage of expenses incurred forsuch a production that must be paid to Quebecers or to corporations with anestablishment in Québec.

Accordingly, the final certification of a film depends partly on the production expenses ofthe film that are paid to Quebecers or to corporations with an establishment in Québec.

As mentioned above in this information bulletin, an amendment will be made to the taxlegislation to require that the production expenses of a film be paid before a corporationmay claim a tax credit for film and television production, since the amount of taxassistance provided by this tax credit depends in part on the production expenses of afilm.

In this context, an amendment to the same effect will be made to the Regulationrespecting the recognition of a film as a Québec film, to require that the productionexpenses of a film be paid before a corporation may file an application for finalcertification of a film with SODEC.

- 26 -

More specifically, the regulation will be amended so that a corporation is required toenclose with its application for final certification of a film an audited report on the costs,or a review engagement report if the final cost of the production of the film is less than$250 000, certifying that a minimum of 95% of the production expenses of the film waspaid before the day of such application for final certification.

This change will apply regarding a film or television production for which an applicationfor final certification is filed with SODEC after the day of publication of this informationbulletin.

2.1.2 Refundable tax credit for musical productions

The refundable tax credit for musical productions was introduced to support theactivities of businesses operating in show business. Briefly, an eligible corporation can,under certain conditions, claim a refundable tax credit equal to 33 �% of the labourexpenditures it incurs for the purposes of producing an eligible production.

However, the labour expenditures giving rise to this tax credit may not exceed 45% ofthe production expenses of the production, so that the tax assistance may not exceed15% of such expenses. In addition, the tax credit granted for an eligible production maynot exceed $300 000.

To be eligible for the refundable tax credit for musical productions, at least 75% of ashow must consist of songs or instrumental music, based on timing, with the exceptionof a concert, a song cycle or the interpretation of a dramatic work set to music, with orwithout spoken dialogue. In addition, a show must not be an excluded show. For thispurpose, an excluded show is a circus show, an aquatic or ice show, a benefitperformance or a gala.

The production must also satisfy Québec content criteria stipulated in a point scale.Under this point scale, a production must obtain a minimum of three out of a maximumof five points based on the place of residence of the creative personnel who participatedin the production of the show, at the end of the taxation year preceding the beginning ofthe production work of the show.

- 27 -

Work done in recent months has led to the conclusion that broadening this tax credit tocomedy shows and dramatic performances would be positive for these sectors of theQuébec cultural industry, in particular by allowing comedy shows to face foreigncompetition and by supporting the production and diffusion of dramatic performances.

❏ Modification to the eligibility criterion based on the percentage ofsinging content of a show

In this context, the eligibility criterion that at least 75% of a show must consist of songsor instrumental music, based on timing, with the exeption of a concert, a song cycle orthe interpretation of a dramatic work set to music, with or without spoken dialogue, willbe withdrawn.

Henceforth, a show will be eligible provided SODEC has issued a certificate for itattesting that it is a musical show, a dramatic performance, a comedy show, a mime ora magic show.

For greater clarity, a show will continue to be an excluded show if it is a circus show, anaquatic or ice show, a benefit performance or a gala.

- 28 -

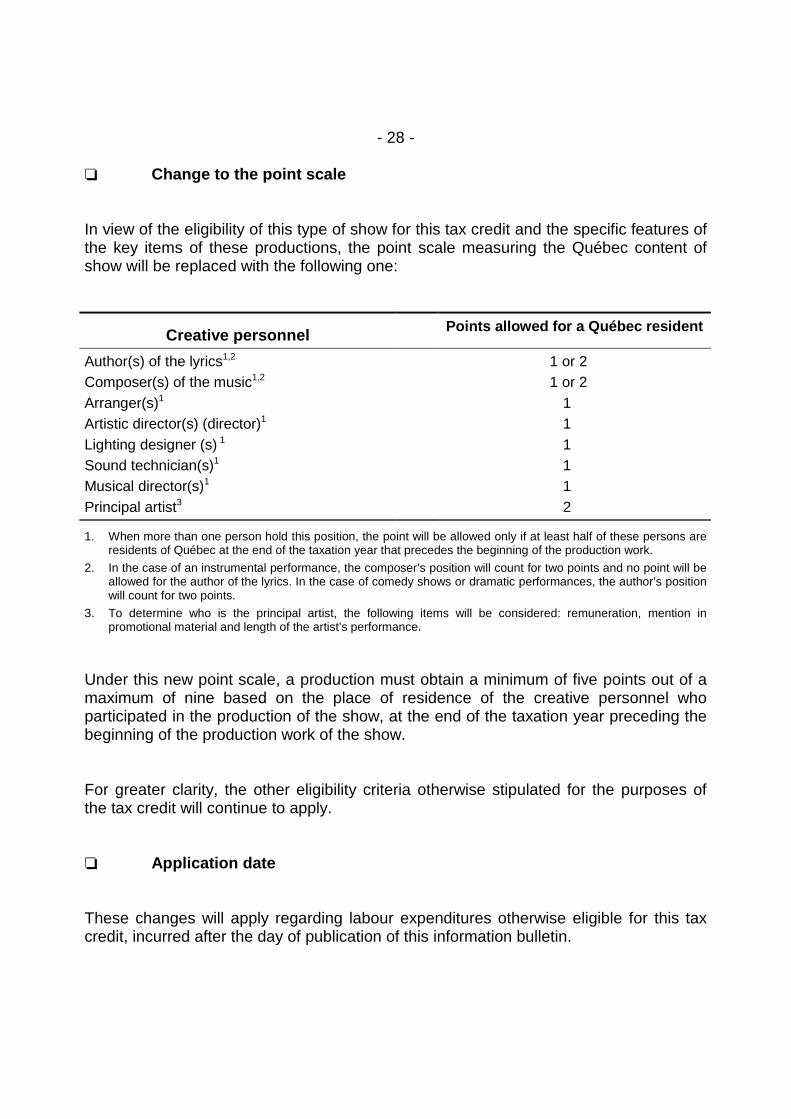

❏ Change to the point scale

In view of the eligibility of this type of show for this tax credit and the specific features ofthe key items of these productions, the point scale measuring the Québec content ofshow will be replaced with the following one:

Creative personnel Points allowed for a Québec resident

Author(s) of the lyrics1,2 1 or 2Composer(s) of the music1,2 1 or 2Arranger(s)1 1Artistic director(s) (director)1 1Lighting designer (s) 1 1Sound technician(s)1 1Musical director(s)1 1Principal artist3 2

1. When more than one person hold this position, the point will be allowed only if at least half of these persons areresidents of Québec at the end of the taxation year that precedes the beginning of the production work.

2. In the case of an instrumental performance, the composer’s position will count for two points and no point will beallowed for the author of the lyrics. In the case of comedy shows or dramatic performances, the author’s positionwill count for two points.

3. To determine who is the principal artist, the following items will be considered: remuneration, mention inpromotional material and length of the artist’s performance.

Under this new point scale, a production must obtain a minimum of five points out of amaximum of nine based on the place of residence of the creative personnel whoparticipated in the production of the show, at the end of the taxation year preceding thebeginning of the production work of the show.

For greater clarity, the other eligibility criteria otherwise stipulated for the purposes ofthe tax credit will continue to apply.

❏ Application date

These changes will apply regarding labour expenditures otherwise eligible for this taxcredit, incurred after the day of publication of this information bulletin.

- 29 -

2.1.3 Refundable tax credit for sound recordings

Like the refundable tax credit for musical productions, the refundable tax credit forsound recordings enables an eligible corporation, under certain conditions, to receive arefundable tax credit equal to 33 �% of the labour expenditures it incurs for thepurposes of producing an eligible sound recording.

However, the labour expenditures giving rise to this tax credit may not exceed 45% ofthe production expenses of the production, so that the tax assistance may not exceed15% of such expenses. In addition, the tax credit granted for an eligible sound recordingmay not exceed $50 000.

To be eligible for the refundable tax credit for sound recordings, at least 60% of aproduction must consist of musical content, based on timing. The sound recording mustalso satisfy Québec content criteria stipulated in a point scale to the same effect asthose stipulated for the refundable tax credit for musical productions, except that theposition of musical or artistic director must be replaced by that of director.

Given that the refundable tax credit for musical productions is being broadened toinclude comedy shows and that shows are often recorded, the refundable tax credit forsound recordings will also be changed, so that this type of production is eligible for thistax credit.

Accordingly, the criterion that at least 60% of the content of a sound recording must bemusical content, based on timing, will no longer apply regarding a sound recording,provided SODEC has issued a certificate for it attesting that it is a sound recordingconsisting of a comedy show.

- 30 -

Furthermore, to reflect the actual situation of the recording industry, the point scalemeasuring the Québec content of a sound recording will be replaced with the followingone:

Creative personnel Points allowed for a Québec resident

Author(s) of the lyrics1,2 1 or 2Composer(s) of the music1,2 1 or 2Artistic director(s)1 1Musical director(s)1 1Director(s)1 1Arranger(s)1 1Sound engineer(s)1 1Principal artist3 2

1. When more than one person hold this position, the point will be allowed only if at least half of these persons areresidents of Québec at the end of the taxation year that precedes the beginning of the production work.

2. In the case of instrumental performances the composer’s position will count for two points and no point will beallowed for the author of the lyrics. In the case of comedy shows, the author’s position will count for two points.

3. To determine who is the principal artist, the following items will be considered: remuneration, mention inpromotional material and length of the artist’s performance.

Under this new point scale, a sound recording must obtain a minimum of five points outof a maximum of nine based on the place of residence of the creative personnel whoparticipated in the production of the sound recording, at the end of the taxation yearpreceding the beginning of the recording work.

For greater clarity, the other eligibility criteria otherwise stipulated for the purposes ofthe tax credit will continue to apply.

❏ Application date

These changes will apply regarding labour expenditures otherwise eligible for this taxcredit, incurred after the day of publication of this information bulletin.

- 31 -

2.1.4 Change to the period within which expenditures giving rise to refundabletax credits relating to the cultural field must be paid

For the purposes of the refundable tax credit for film and television production, and forthe purposes of the other refundable tax credits in the cultural field that have beenstructure on the basis of this tax credit, the labour expenditures giving rise to these taxcredits must in particular be paid in the taxation year in which they are incurred or withinthe 60 days following the end of such taxation year.

This period within which these expenditures must be paid is specific to the refundabletax credits relating to the cultural field. In general, the expenditures giving rise to thevarious refundable tax credits stipulated in the tax legislation must be paid before thesetax credits are claimed, which implies that a period of many months may elapsefollowing the end of the taxation year in which such expenditures were incurred. Therefundable tax credits may be claimed no later than a year after the deadline for filingthe tax return for the taxation year during which such expenditures were incurred.

In this context, to standardize the refundable tax credits of the cultural field with all therefundable tax credits otherwise stipulated in the tax legislation, the legislation will beamended to withdraw, for the purposes of all the refundable tax credits relating to thecultural field, the requirement that the expenditures giving rise to these tax credits bepaid in the taxation year in which they are incurred or within the 60 days following theend of such taxation year.

Henceforth, like the other refundable tax credits, it will suffice that the expendituresgiving rise to the various refundable tax credits relating to the cultural field have beenpaid at the time the tax credit is claimed, subject to the conditions otherwise applicableto each of these tax credits.

This change will apply regarding a taxation year of a corporation ending after the day ofpublication of this information bulletin.

- 32 -

2.2 Clarifications concerning the tax holiday for small and medium-sizemanufacturing enterprises in remote resource regions

A ten-year tax holiday was introduced in the March 29, 2001 Budget Speech tomanufacturing small and medium-size enterprises in remote resource regions, tostimulate economic development of these regions where the employment situation isthe most difficult.

Accordingly, in general, a corporation all of whose activities consist mainly in carryingon a manufacturing or processing business in one of these regions may claim a taxholiday with respect to income tax, the tax on capital and the employer contribution tothe Health Services Fund (HSF).

❏ Clarification concerning manufacturing and processing activities

Since the tax legislation does not define manufacturing and processing, the ordinarymeaning of these words and jurisprudence must be relied upon to determine whether acorporation carries out such activities.

Accordingly, the notion of manufacturing generally refers to the creation of something(for instance, making or assembling a machine) or the shaping, from something, of anobject (for instance, manufacturing a part to be included in a machine).

The notion of processing generally refers to the technique of preparation, manipulation,or any other activity designed to produce a physical or chemical transformation in aproduct, an article or a substance, other than the transformation resulting from thenatural growth process.

Manufacturing and processing activities are generally carried out by companies in thesecondary sector of the economy, i.e. companies in the manufacturing sector. However,jurisprudence has already established that some activities performed by corporations inthe tertiary sector, i.e. the sector consisting of service companies, could constitutemanufacturing and processing activities.

- 33 -

To avoid any ambiguity and to better reflect the objective of the tax holiday, namely tostrengthen the manufacturing sector, the notion of manufacturing or processingcompany will be clarified.

More specifically, for the purposes of the tax holiday, the activities performed by acorporation all of whose activities consist mainly in supplying services may not beconsidered as manufacturing or processing activities.

To this end, activities relating to the wholesale and retail trade, as well as lodging andrestaurant services, will be considered services. For example, a corporation all of whoseactivities consist mainly in preparing meals and beverages ordered by customers forimmediate consumption on site or outside the establishment will not be eligible for thetax holiday.

This clarification applies as of March 30, 2001.

❏ Relief measure regarding the existence of an establishment outside aremote resource region

For the purposes of the tax holiday, a corporation must only have establishments, withinthe meaning of the Taxation Act, in remote resource regions. Essentially, the purpose ofthis condition is to ensure that the tax holiday is granted only regarding activitiesgenerated in the remote resource regions.

It often happens that a corporation assigns salespeople to various points of sale thatmay be located outside a remote resource region. The criterion requiring establishmentsonly in these regions may then appear constraining, if the revenue generated by thesalespeople results from activities performed in a remote resource region. Furthermore,this criterion may also be restrictive for a corporation whose head office is outside aremote resource region, but not its manufacturing or processing activities.

Accordingly, the condition that the corporation must maintain establishments only in aremote resource region will be streamlined regarding these two situations.

- 34 -

More specifically, this streamlining measure will apply to the situation in which acorporation is deemed to have an establishment outside a remote resource region,because it carries on a business there through an employee, an agent or a mandatarywho has general authority to contract for the corporation or who disposes of a stock ofgoods belonging to the latter and used to regularly fill orders he receives. Thisstreamlining measure will also apply to the situation in which a corporation maintains itshead office outside a remote resource region, the head office being understood as theestablishment where the corporation’s legal, administrative and management activitiesare concentrated.

In these two situations, when all or substantially all of a corporation’s payroll, for ataxation year, is attributable to employees who work in an establishment located in aremote resource region, such corporation will then be deemed to have establishmentsonly in such remote resource region during such taxation year.

To that end, payroll will be determined according to the wages incurred by thecorporation in the taxation year, regarding its employees. The wages that must beconsidered for each employee include director’s fees, bonuses, performance premiums,commissions, remuneration for work done in excess of normal work hours and taxablebenefits that must be included in calculating the employee's income.

This streamlining measure applies as of March 30, 2001.

2.3 Streamlining measure regarding the eligibility certificate for therefundable tax credit for the Vallée de l'aluminium

A refundable tax credit was introduced for the Vallée de l'aluminium in the March 14,2000 Budget Speech. Certain clarifications were made on December 21, 20003

concerning the notion of manufacturing. Lastly, in the March 29, 2001 Budget Speech,the application details of the tax credit were harmonized with those of the tax credit forprocessing activities in the resource regions, to standardize the measures forprocessing activities in the regions.

3 Ministère des Finances du Québec, Bulletin d’information 2000-10.

- 35 -

Briefly, the refundable tax credit for the Vallée de l'aluminium is granted regarding theincrease in payroll attributable to eligible employees of an eligible corporation operatingin the Saguenay−Lac-Saint-Jean administrative region, for five consecutive calendaryears.

To be considered eligible, the corporation must, however, carry on a certified business,i.e. a business regarding which an eligibility certificate has been issued byInvestissement Québec.

Under the current rules, Investissement Québec cannot issue an eligibility certificateregarding a business if, in its view, the business is the continuation of a certifiedbusiness for which an eligibility certificate has previously been issued.

However, these rules may impede the recovery of businesses in the case, amongothers, where a corporation wants to acquire the assets of a bankrupt corporation thatalready holds an eligibility certificate.

Consequently, the current terms and conditions will be streamlined to allowInvestissement Québec to issue an eligibility certificate regarding a business, even if itis the continuation of a certified business or of a part of a certified business for which aneligibility certificate has previously been issued. In such a case, the expiry of theeligibility certificate will be set from the reference calendar year of the corporation thatheld the first certificate.

For greater clarity, the rules already stipulated concerning business continuations willapply to adjust the amount of the increase in payroll of an eligible corporation when,during a given calendar year, the activities another eligible corporation performed in theSaguenay−Lac-Saint-Jean region decrease or cease and, by the same token, theactivities regarding the certified business commence or increase in scope, in anestablishment of such eligible corporation located in the Saguenay−Lac-Saint-Jeanregion.

- 36 -