building resource consumption accounting...

TRANSCRIPT

1

Back to Basics in Management Accounting: Resource Consumption

Accounting

CAPT Larry R. White, CMA, CFM, CPA, CGFM

Commanding Officer, USCG Finance Center

Anton van der MerwePrinciple, Alta Via Consulting, LLC

2

Back to Basics: RCAFoundational Management Accounting Concepts

RCA Overview

RCA Go To Market

What Happened During The Incubation Phase

The Road Forward

3

What is Enterprise Optimization?

• To Maximize Revenue or Mission Outcomes

• To Minimize Cost or Redeploy Financial Resources

Decisions On the Use of:

• Existing Resources and Capabilities; or

• Incremental Changes

4

What is Management Accounting’s Contribution to

Enterprise Optimization?• Decision Support, Planning and Control Over the

Value Creating Operations of the Firm

By doing what?• Modeling… the Organization’s Operations &

Costs• Providing Insight into Future Outcomes… Usually

with Invested Resources or Incremental Changes

5

What Causes Costs?

Resources (also creates any revenues!)

Inputs ResourcePool

Output

Another ResourcePool (s)Or Final

Product/Service

Support or

Production

ResourceQuantities

and Activities/Processes

LaborMachinesMaterial

IT Resources

6

What Are the Primary Characteristics of Resources?

• Capability– Quality or Qualitative Characteristics

• Cost – Cost Structure– Cost Behavior

• Capacity– Quantity They Provide

7

How Do We Define Capacity?• Productive• Non-Productive• Idle/Excess

More Questions:• Who is Responsible for Idle & Excess Capacity? • What can Allocations of Idle & Excess Capacity

Do to Costs?

8

Cost Concepts

Operational

Fixed Variable

“Relevant Range”

Which Cost Concepts Must Form the Basis for Cost Modeling?

Decision Support

UnavoidableAvoidable

Opportunity Cost

9

What Types of Decisions Are Needed for Enterprise Optimization?

Too Many, Too Diverse, Too SituationalImpossible to Categorize

10

What Constitutes an Effective Model of Operations & Costs?

Key Principles:• Causality• Responsiveness• Work or Process Visibility

Resource Divisibility is Necessary to Identify and Assess Cost Avoidability

Insight into Resource Divisibility is the Key to Effective Decision Support Information!

11

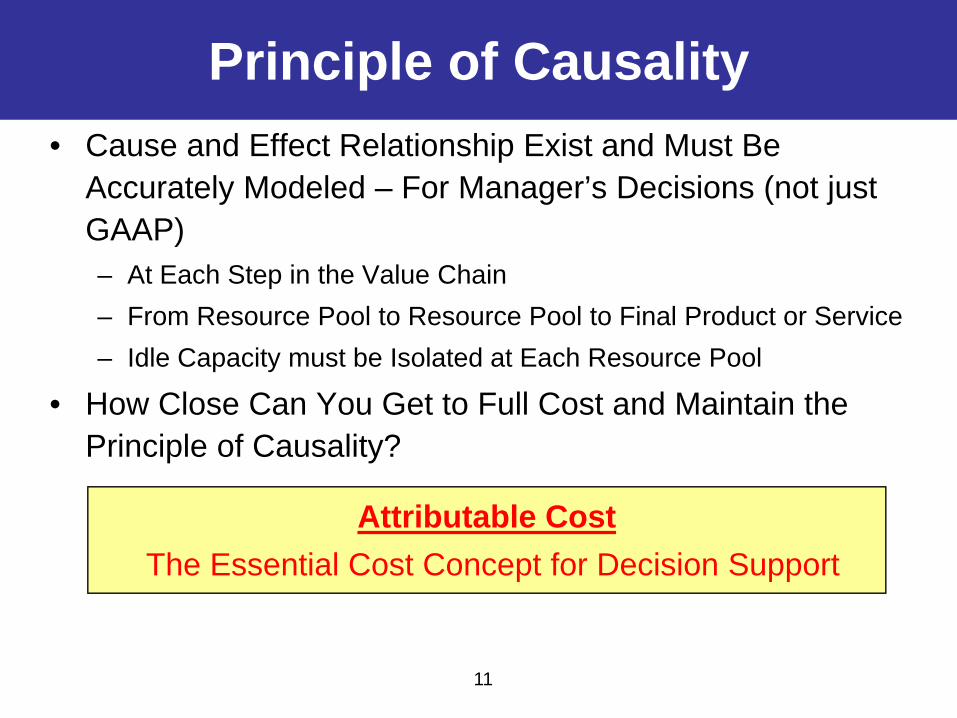

Principle of Causality• Cause and Effect Relationship Exist and Must Be

Accurately Modeled – For Manager’s Decisions (not just GAAP)– At Each Step in the Value Chain – From Resource Pool to Resource Pool to Final Product or Service– Idle Capacity must be Isolated at Each Resource Pool

• How Close Can You Get to Full Cost and Maintain the Principle of Causality?

Attributable CostThe Essential Cost Concept for Decision Support

12

Principle of Responsiveness

Product A Product B

Service 1 Service 2 Service 3

Total Volume

$’s

Change in Total $’s Due to a Change in

Total Volume

Fixed Cost

Variable Cost

Product A Product B

Service 1 Service 2 Service 3

Output

Inputs

Output

Inputs

Output

Inputs

Output

Inputs

Output

Inputs

Traditional: Total Cost to Total Volume

Value Chain Modeling of Resource Pools

13

What is Responsiveness?• Consumption Behavior must Respond to Causal

Relationships– Fixed Responsiveness– Proportional Responsiveness

• Integrity of Resource Quantities and their Costs are Maintained – Requires Careful design of Resource Pools– Each Resource Pool must provide Discrete, Homogeneous

Resource/Capability

• Clear Insights into Organizational, Product Line, Batch, & Unit level Cost Behaviors is Always Available in the Data

Provides Resource Divisibility Insights

14

Traditional Income Statement vs.Multiple Margin P&L

+ Revenue- Cost of Goods Sold= Gross Margin- G&A- Depreciation- Interest= Net Income before Tax- Taxes= Net Income

+ Revenue- Product Proportional Cost= Contribution Margin- Product Fixed Cost= Product Gross Margin- Non-Product Proportional Costs= Margin 3- Non-Product Fixed Cost= Margin 4- Excess/Idle Capacity Costs= Margin 5

15

Principle of WorkInsights into Process Effectiveness

Without the Work Principle:

Resource Pool A Product 123Planned Output: 1,000 Hrs

Actual Output: 1,100 HrsInputs:

Using the Work Principle:

Product 123Inputs:

Resource Pool APlanned Output: 1,000 Hrs

Actual Output: 1,100 Hrs

Pool A 1,100 Hrs

Setups (Qty 10) 300 HrsRun Machine 800 Hrs

Setups

Run Machine

16

Back to Basics: RCAFoundational Management Accounting Concepts

RCA Overview

RCA Go To Market

What Happened During The Incubation Phase

The Road Forward

17

4 Stages of Cost Management & Performance Measurement Systems*• Stage 1 - Inadequate for Financial reporting

• Stage 2 - Financial-reporting Driven

• Stage 3 – Stand-alone

• Stage 4 - Integrated Cost Management, Financial Reporting and Performance Measurement

*Kaplan, R. S. & Cooper, R. (1997). Cost and Effect, Harvard Business School Press: Boston, MA.

18

What is Resource Consumption Accounting?

• RCA Inherits Core Principles from German Cost Management (GPK)– GPK is a Well Developed Standard Costing

System– Principles Applied in Practice since the Late

1940’s– Principles Implemented by 3,000+ Companies

• RCA Integrates– Activity-based Costing and Throughput Concepts

• RCA Creates an Integrated Economic Model of Operations for Decision Making– Enterprise Optimization– Principle Based– Highlights Resource Divisibility

RCA

Resource view

Advantages

Process viewAdvantages

GPK ABC

Capacity Analysis and Management

Process Analysis and Management

Capacity-Focused

Activity-Focused

19

RCA: The Fundamental DifferenceOperational Integration

• Breaking the “Tapestry Syndrome”• Stop Trying to Get Management Accounting Information

from the Financial Accounting General Ledger

Source Document: Goods Receipt

Qty

$’s

Raw Material xxx kgs

Raw Material $ xx.xx

Traditional Practice

Quantity Flows

Value Flows

Source Document: Goods ReceiptFor Raw Material A123

Material A123 xx kgs $yy.yyItem Qty Amount

Value Chain Integration

Quantity Flows

Value Flows

Source Document: Goods Receipt

Qty

$’s

Raw Material xxx kgs

Raw Material $ xx.xx

Source Document: Goods ReceiptFor Raw Material A123

Material A123 xx kgs $yy.yyItem Qty Amount

20

Traditional Income Statement vs.Multiple Margin P&L

+ Revenue- Cost of Goods Sold= Gross Margin- G&A- Depreciation- Interest= Net Income before Tax- Taxes= Net Income

+ Revenue- Product Proportional Cost= Contribution Margin- Product Fixed Cost= Product Gross Margin- Non-Product Proportional Costs= Margin 3- Non-Product Fixed Cost= Margin 4- Excess/Idle Capacity Costs= Margin 5

21

What is Resource Consumption Accounting?

Pillar 1: Focus on Resources & their Consumption• Understand your Resources & Their Consumption… Understand Cost• Provides a Framework for Capacity Management

Pillar 2: Quantity Structure for Resource Consumption• Operational Quantities Drive Costs• Model the Operation & Use of Resources….then Apply Cost• Enables Resource Capacity Management• Demonstrates Causality of Value Chain Relationships

Pillar 3: Recognizing the Inherent and Changing Nature of Costs• Resource Pools Start with an Inherent Cost Structure• As Resources are Consumed, the Nature of their Costs Change• Costs that are Initially Proportional by Nature can Change from Proportional to

Fixed Based on Consumption Patterns• Value Chain Modeling of Resource Cost Responsiveness

22

Product Support Cost

S: Ancillary Production Equipment

S: AdministrationHuman Resources

& Accounting

S: Quality Assurance

RP: Dryer (Hours)Capacity: 100Output Qty: 100

S: Plant Engineering and

Maintenance

RP: Plant Maintenance (Maint. Labor)Capacity: 30,000Output Qty: 30,000

P: Extrusion Line

RP: Extrusion Labor (Labor hours)Capacity; 32,000Output Qty: 30,000

Product P & L’s

Department

Resource PoolAbbreviated RP

Activity

RP: Chiller (Hours)Capacity: 50,000Output Qty: 50,000 Perfor

m

AccountingPerform

Admin

QA

Testing

Legend

S-Support

P- Production

Common Fixed Costs

Product

Returns

RP: Extrusion Machine1(Machine hours)Capacity; 17,520Output Qty: 10,000

RCA Storyboard

Manufacturing Costs

Budgeted Products

RP: QA Labor(Labor hours)Capacity: 14,000Output Qty: 14,000

RP: Admin Labor(Labor hours)Capacity: 17,000Output Qty: 17,000

Perform

HR

23

Plant Maintenance Resource Pool Output Measure: Maintenance Labor HourOutput Quantity: 20,000 Hours

Primary Costs Fixed Proportional

Technician Wages -$ 600,000$

Supervisor Salary 80,000$ -$

General Material 12,000$ 100,000$

Depreciation: Shop Equipment 50,000$ -$

142,000$ 700,000$

Secondary Costs

Resource Pool Output Fixed Qty Prop Qty

Utilities MW-Hrs 40 160 6,000$ 24,000$

Activity/Process Driver Fixed Qty Prop Qty

HR: Benefits Adjustments # Adjusts 22 0 1,100$ -$ Purchase: Gen Materials # PO's 10 200 500$ 10,000$

7,600$ 34,000$

Total Resource Pool Costs 149,600$ 734,000$

Unit Cost Rates (/20,000 Hrs) 7.48 36.70

RCA Information

24

For Enterprise Optimization RCA Provides:

• Operational View of Organization• Fixed and Proportional Nature of Cost

-Costs are Better Understood, -Responsibility for Costs is Clearer

• Variance Analysis• Target Cost Determination• Multi-level and Multi-dimensional Contribution Margin /

Profitability Reporting• Capacity Utilization Information• Planning, Forecasting, and Simulation

-Model is Reversible/Invertible for Calculations

25

Back to Basics: RCAFoundational Management Accounting Concepts

RCA Overview

RCA Go To Market

What Happened During The Incubation Phase

The Road Forward

26

A Challenging Marketplace• Multiple Philosophies, Approaches, Techniques:

Activity-Based Costing, Lean Accounting, Theory of Constraints, etc.

• Multiple Failed Attempts for Operational Decision Support Information

• Inconsistent Usage of Basic Principles by the Various Options (Avoidable/Unavoidable, Fixed/Variable, etc.)

• NOISE – What To Do for What Purpose?• Manager Confusion is at an All Time High

27

A Challenging Marketplace

• Low Level of Knowledge About Management Accounting– Compared With Financial Accounting

• Cluttered, Undisciplined Market for Management Accounting Solutions– High Failure Rate– No Reliable Standards

• Investments in Management Accounting Systems Considered High Risk.

28

The Normal Marketplace

• First Mover Advantage: The Early Bird Gets the Worm… and Benefits from It.

29

Managers & The MA Marketplace

• Instead: The Early Bird Gets Eaten by The Worm… and the Other Birds Take Their Investment Dollars Elsewhere.

30

RCA In The Marketplace • Although RCA’s Core Principles Are Well Proven (Over

3,000 Implementations) They Are Unfamiliar to the U.S. Market

• Other Approaches Have Been Down This Road In The U.S. and Highlighted What Needs to Be Avoided e.g., A Lack of Standards, A Free-For-All by Consultants and Software Vendors

• One Is Dealing With A Highly Skeptical Punch-drunk Decision Maker That Is At Least Twice Bitten and Now Thrice Shy

31

The Tipping Point Methodology • The Realities of the Marketplace Required A Different Approach to

Rolling RCA Out• The Tipping Point Approach Was Adopted and Will Comprise Three

Phases:

2001 2008 ??

INCUBATIONPhase 1

COMMUNITYPhase 2

MARKET WIDEPhase 3

32

Back to Basics: RCAFoundational Management Accounting Concepts

RCA Overview

RCA Go To Market

What Happened During The Incubation Phase

The Road Forward

33

Incubation Phase Activities• The RCA Interest Group at CAM-I Comprised Users,

Practitioners and Academia• The Incubation Phase Was A Validation (Kicking the

Tires) Period• Involved A Number of Case Studies Targeting Diverse

Business Environments e.g., For Profit & Not For Profit, Manufacturing & Service, Commercial & Government

• A Number of Research Projects into GPK was Undertaken Through IMA’s FAR (Foundation for Applied Research)

34

RCA Case Studies

Manufacturer: Clopay• A Global Plastics Extrusion Manufacturer of Plastic Film

Sheet Products for Medical & Hygiene Markets

• Used A Traditional Standard Costing System

• Experienced Fluctuating Product Costs when Volume and Mix Changes Occurred

• New More Efficient Machines Were Under Utilized and Old Fully Depreciated Machines Were Being Targeted for Extra Volume

35

RCA Case StudiesAircraft Maintenance: Air Engines• A Global Service Provider that Specializes in the Repair

and Overhaul of Jet Engines

• Unpredictable Demand and Workload e.g., the Extent of Work On An Engine Is Only Known Once the Engine is Disassembled and Inspected

• Require a Solution that Could Dynamically Accommodate Fluctuating Resource Demand

• Could not Provide Customers with Motivation for Overhead Charges on Their Invoices

36

RCA Case StudiesHospital: St Anonymous• A Community Based Not for Profit Hospital – the Case

Focused on the Outpatient Surgery Center (OSC)• Did Not Have Sufficient Insight Into Their Costs to be

able to Negotiate MediCare and MediAid Reimbursements

• Wanted to Understand which Surgical Procedures in the OSC Were Making and Losing Money

• Constructed the OSC with Two Additional Operating Room Shells and Wanted to Understand the Impact on Support Resource and Their Capacity

37

RCA Case StudiesUniversity: UAMS• A $1 Billion Medical Sciences University that is Primarily

State Funded But Also Gets Federal and Private Research Grants

• Being Funding Driven, Did Not Have A Management Accounting System

• Did Not Understand Student Costs – Whether They Were Cross Subsidizing Out of State Students and How to Justify Their Funding Needs to the State

• University Would Not Be Able to Sustain Its Stated Missions at the Current Rate of Medical Cost Increases –Lacked Insight Into Resource Usage and Costs

38

Back to Basics: RCAFoundational Management Accounting Concepts

RCA Overview

RCA Go To Market

What Happened During The Incubation Phase

The Road Forward

39

The Community Phase

INCUBATIONPhase 1

COMMUNITYPhase 2

MARKET WIDEPhase 3

40

The Community Phase

• The Community Phase Will Be Structured Around the:

INCUBATIONPhase 1

COMMUNITYPhase 2

MARKET WIDEPhase 3

41

RCA Institute Objectives

• Improve Management Accounting Knowledge and Practice– Focus on Decision Support for Enterprise Optimization

• Build A Highly Structured and Disciplined RCA Community– Create Standard Body of Knowledge and Standards of Practice– Initial Objective is 150-200 Highly Skilled Practitioners (The

Tipping Point)– Provide A Professional Structure that Minimizes Risk to RCA

Adopters

42

The RCA Institute Will…

• Be A Non-profit Entity • Seek An Affiliation with the Executive Education Branch of

A Top-Flight University (Negotiations Underway)• Responsible for Training of Practitioners and Adopters• Provide A Number of Products and Services to Mitigate

Adopter Risk e.g., Certification, Assurance Services• Sponsor Research into RCA Implementation and Long-

term Use• Serve to Raise RCA Awareness and Fulfill Advocacy and

Outreach Roles

43

RCA Support & Quality Assurance• Institute Membership

– Corporate & Individual

• Certification– Specialist, Practitioner, Master

– Software Products

• Implementation Review/Assurance

• Support Adopting Organizations & Practitioner Expertise

• Adopter Internal Use Reviews– Evaluations of An Organization’s Effectiveness Using and

Maintaining RCA

44

Individual Training CoursesProduct Name Product Description

Product Purpose

Competency Level

RCA-T101 The Current Management Accounting Landscape Introduction RCA Specialist

RCA-T102 RCA Terminology and Principles Introduction RCA Specialist

RCA-T201 Introduction to RCA Conceptual Design & Modeling Competency RCA Specialist

RCA-C001 Case Model: No Pain Case Competency RCA Specialist

RCA-T202 An Introduction to RCA Decision Support Competency RCA Practitioner

RCA-T301 Advanced RCA Conceptual Design and Modeling Competency RCA Practitioner

RCA-T302 Effective Enterprise Management – RCA Adopted Competency RCA Practitioner

RCA-M101 Methodology Training Mastery RCA Master

RCA-T401 RCA Certification Mastery RCA Master

RCA-D101 RCA Overview Decision Maker

RCA-D102 RCA Decision Support Decision Maker

45

Launch Date: 1 August 2008

Website: www.RCAInstitute.org

Interview: Cost Management magazineJuly/August Edition

46

Back to Basics: RCA

Questions?

Thank You