building a mobile banking customer experience that starts and ends with the customer

DESCRIPTION

Summary of annual mobile banking study of US banking customers. Based on 2013 study conducted during Q1. More than 3,000 participants.TRANSCRIPT

A White Paper Based On:

The ath Power Mobile Banking Study™

By Michael J. McEvoy, Managing Director

BUILDING A CUSTOMER EXPERIENCE THAT STARTS AND ENDS WITH THE CUSTOMER

MOBILE BANKING

www.athpower.com

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

Building A Customer Experience That Starts And Ends With The Customer

The ath Power Mobile Banking Study™

2

During Q1 2013, 3,201 banking customers in the US responded to an online survey by ath Power Consulting that set out to determine what factors make up an “ideal” mobile banking experience, and to uncover the impediments to producing such an experience. Through this evaluation, consumers and business owners provided information about their current mobile banking behaviors, the features and functionality they value or would like to see added, and their assessment of their current mobile banking experience.

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

BACKGROUND

KEY TAKEAWAYS

Remote Deposit Capture Approximately 1 in 3 retail customers (31%) have used RDC, a significant milestone, given that check deposit is the main reason for branch visits for many customers.

1

Voice Authentication, RecognitionNext generation capabilities will include voice authentication and voice recognition. Voice recognition would motivate 1 in 3 mobile customers to use mobile banking services more. Voice authentication would encourage more to adopt mobile banking in the first place.

2

Mobile Photo Bill PayBy helping to reduce data entry requirements for bill pay, mobile photo bill pay offers the potential for significantly reducing switching costs for customers by easing the move away from their current bank’s bill pay offering.

3

Security ConcernsAbout 2 in 5 of those who have not yet tried using mobile banking cite security concerns as a reason. Almost one-half of current mobile banking customers are similarly discouraged from using mobile services such as bill payment and funds transfers over security fears.

4

3

Mobile banking represents an opportunity for banks and others to reset the relationship with their customers. With almost 1 in 2 mobile banking customers logging in at least twice weekly, interaction with many of these customers has become more frequent. It has also become more varied as customers are being provided with new choices through mobile devices in how they manage their finances. With more frequent customer contact and more choices enabled for the customer, the mobile channel offers a unique opportunity to reset the customer relationship while improving customer experience.

INTRODUCTION

High Frequency of Logins in Mobile: Opportunities for Engagement?

Source: The 2013 ath Power Mobile Banking StudyTM

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

4

What are the main reasons why you have decided not to use mobile banking?

Why do you feel you do not need mobile banking?

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

65%

IMPEDIMENTS TO FASTER ADOPTION OF MOBILE BANKINGAlthough mobile adoption continues to grow, a number of factors are preventing faster mobile adoption. Among non-mobile banking customers possessing a device capable of accessing mobile banking, two issues are ‘standouts’ that help explain why they have yet to become mobile customers of their financial institution:

Security Concerns. About 2 in 5 (39%) of those who have not yet tried using mobile banking cite security concerns as a reason. Attacks by hackers are the biggest security concern. While banks will have difficulty in convincing this cohort that mobile banking is sufficiently safe to be trusted as a means of handling finances, rolling out and promoting additional security measures would help alleviate the fears that some have over security.

Absence of Compelling Offering. Today’s offerings are not sufficiently compelling for the 1 in 3 (31%) among non-users who say they ‘do not need’ mobile banking, most of whom prefer to use online banking for their digital banking needs. To attract online banking users, in particular, a more compelling ‘mobile’ offering is needed.

Source: The 2013 ath Power Mobile Banking StudyTM

5

Offering capabilities that are unique to mobile, such as Remote Deposit Capture (RDC), Mobile Photo Bill Pay and P2P payments will likely provide some current non-users – especially online banking customers – with sufficient motivation to migrate to the mobile channel.

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

Mobile customers are comfortable using current mobile banking capabilities and many mobile banking applications currently gain high satisfaction ratings from customers in the various ‘app’ stores. In our mobile study, slightly more than half of customers (57%) are ‘very satisfied’ with their mobile banking experience, suggesting broad customer satisfaction currently, with room for improvement. To maintain and build upon customer satisfaction ratings in an environment of rapidly inflating customer expectations, financial institutions will need to continually improve their mobile banking apps and associated capabilities.

While doing so, they could learn from the approaches taken by technology firms and other non-bank competitors. Non-bank competitors typically argue that they develop their user experience model from the customer standpoint – it all starts and ends with ‘the customer’. Banks, on the other hand, are more prone to start from the back office ‘out’, focusing more on regulatory and legacy system issues and less on the needs and wants of the end user. In practical terms, the customer may be largely forgotten as the financial institution places greater emphasis on ‘systems and processes’ than customer experience. This will need to change if financial institutions are to provide a more optimal experience for their customers.

BUILDING A ‘CUSTOMER EXPERIENCE’ THAT STARTS AND ENDS WITH THE CUSTOMER

6

Current Usage. Bank customers are readily using the capabilities provided through the mobile channel and take to new additions as they are introduced. The relatively low percentages of customers using certain functions, such as RDC, reflect the fact that many financial institutions are still rolling out their capabilities in a number of areas. Almost 2 out of 5 customers that have not used ‘remote deposit capture’ have yet to try RDC due to their bank not providing it. In fact, in both last year’s and this year’s ath Power Mobile Banking Study, RDC was the most desired capability cited by mobile users.

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

Source: The 2013 ath Power Mobile Banking StudyTM

7

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

FUTURE DIRECTIONS While customers appear broadly satisfied with current mobile banking offerings, they are ready for more, with consumer expectations above and beyond where most banks find themselves currently. In our study, customers point to a number of capabilities they would like to be able to access through mobile. Examples include capturing rewards points through mobile use and being able to use mobile devices to pay at a merchant.

For the next stage in the evolution of mobile banking, many enhancements are being developed or introduced across the industry, including:

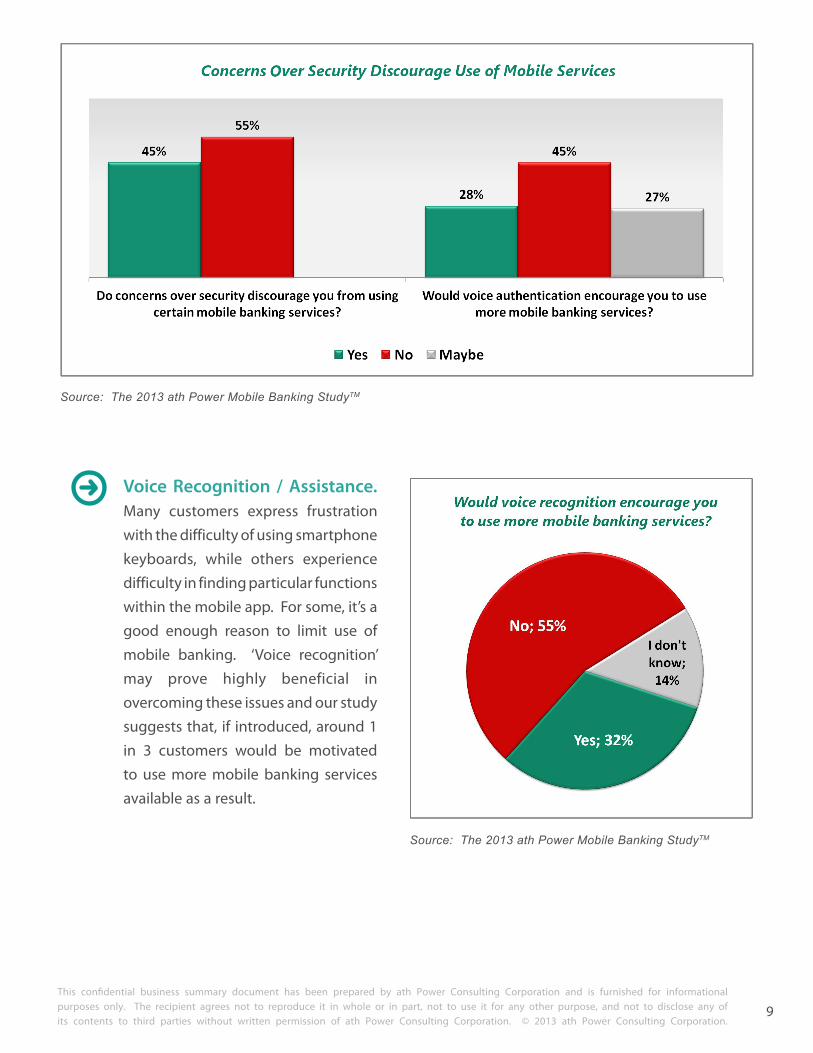

Voice Authentication. Concerns over security discourage roughly half of mobile customers from using certain mobile services, such as bill payment and funds transfers. In response, ‘voice authentication’ is among the technologies being considered by a number of financial institutions.

Source: The 2013 ath Power Mobile Banking StudyTM

8

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

Source: The 2013 ath Power Mobile Banking StudyTM

Source: The 2013 ath Power Mobile Banking StudyTM

Voice Recognition / Assistance. Many customers express frustration with the difficulty of using smartphone keyboards, while others experience difficulty in finding particular functions within the mobile app. For some, it’s a good enough reason to limit use of mobile banking. ‘Voice recognition’ may prove highly beneficial in overcoming these issues and our study suggests that, if introduced, around 1 in 3 customers would be motivated to use more mobile banking services available as a result.

9

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

Source: The 2013 ath Power Mobile Banking StudyTM

PFM Tools. Many bankers see ‘mobile’ as a means to more fully engaging with their customers and improving overall mobile adoption. For some institutions, helping customers identify and achieve their financial goals is part of that ideal, to be supported by Personal Financial Management (PFM) tools. Almost 3 in 5 customers express interest in tools which would assist them in tracking finances, setting budgets and planning their financial future.

10

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

65%

Mobile Photo Bill Pay. Mobile Photo Bill Pay (MPBP) has become available to customers at several banks, including US Bank and BBVA. As a value-added capability that is unique to mobile, MPBP is expected to encourage some current non-mobile customers to try ‘mobile’.

An important benefit which MPBP brings is the potential for avoiding the need for extensive data entry sometimes found within online banking bill pay – a prime ‘stickiness’ factor that discourages online banking customers from switching banks.

Service Trackers. ‘Trackers’ are tools that enable customers to visually track where they are within a process. An example is the Domino’s Tracker® for providing a visual status on pizza orders, from initial order to final delivery. In its most recent rendition, a link to the tracker may be pinned to the start screen on mobile devices. In financial services, a small number of institutions provide online trackers for monitoring the status of loan applications or insurance claims. A number of banks are now considering the deployment of trackers in the mobile channel, for loan applications, customer service issues, fraud claims and other potential applications. The adoption of such technologies would likely improve customer experience – provided the trackers are providing accurate and up-to-date information – and reduce customer inquiries through other, more expensive, channels.

Source: Domino’s Pizza website (https://order.dominos.com)

Clearly, exciting developments are underway in mobile banking. New capabilities that add value will likely attract additional mobile customers while encouraging existing ones to use mobile even more.

However, financial institutions must not lose sight of the customer: ‘customer experience’ matters most of all and, ultimately, will determine how mobile banking will be judged and used by the customer.

11

This confidential business summary document has been prepared by ath Power Consulting Corporation and is furnished for informational purposes only. The recipient agrees not to reproduce it in whole or in part, not to use it for any other purpose, and not to disclose any of its contents to third parties without written permission of ath Power Consulting Corporation. © 2013 ath Power Consulting Corporation.

ABOUT ATH POWER CONSULTINGath Power Consulting is the premier provider of customer experience solutions for the financial services industry, offering survey research, audit and mystery shop study, competitive intelligence, market analyses, training and development, and strategic brand planning. ath Power owns the largest panel of financial services field representatives in North America and executes more proprietary banking audits than anyone in the industry. Since 1997, our fully customizable solutions have helped improve customer retention, build brand loyalty and increase profitability, performance and market share for banking, credit card, mortgage, insurance and investment organizations across North America. To learn more, please visit www.athpower.com.

For more information on this study or any of our other solutions, please contact:Jessica Hamel +1.978.474.6464, Extension 107 [email protected]

ABOUT THE AUTHOR

Michael J. McEvoy - Managing Director

Michael J. McEvoy has over 15 years of experience consulting to many of the largest financial institutions and their technology suppliers worldwide. Prior to joining ath Power, Mike served as Principal and Head of Banking Research for Novarica, a division of Novantas. Additionally, he spent six years consulting to MasterCard and its member banks, and was also a founding analyst at both TowerGroup and MasterCard’s Purchase Street Research. He holds a Bachelors degree in mathematics and economics and a Master of Economic Science degree from University College, Cork, Ireland and an MBA from the Wharton Business School at the University of Pennsylvania. Mr. McEvoy may be reached via email at [email protected].

12