broadband access network options - at … · broadband access network options r. e. wagner april...

TRANSCRIPT

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 2

Broadband access network optionsOutline of the presentation

• Introduction to access networks

• Drivers and trends in access deployments

• Access network architecture options

• Network solutions of advantage to the optics industry

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 3

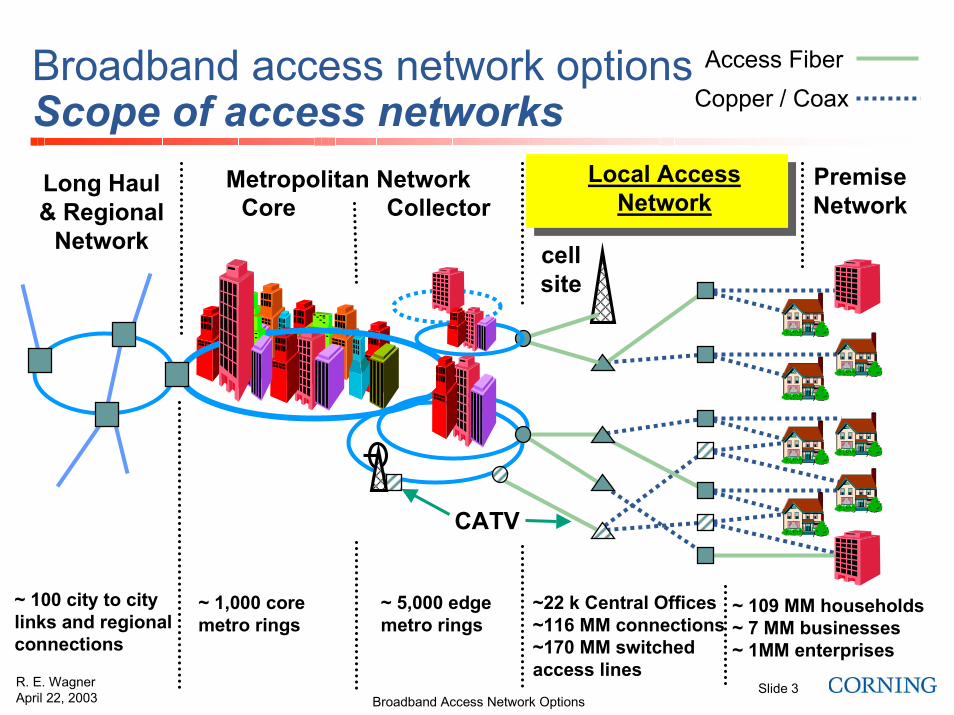

Broadband access network optionsScope of access networks

PremiseNetwork

~ 109 MM households~ 7 MM businesses~ 1MM enterprises

Core

~ 1,000 coremetro rings

Metropolitan NetworkLong Haul& Regional

Network

~ 100 city to citylinks and regionalconnections

Local AccessNetwork

~22 k Central Offices~116 MM connections~170 MM switchedaccess lines

cellsite

Collector

~ 5,000 edgemetro rings

CATV

Access FiberCopper / Coax

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 4

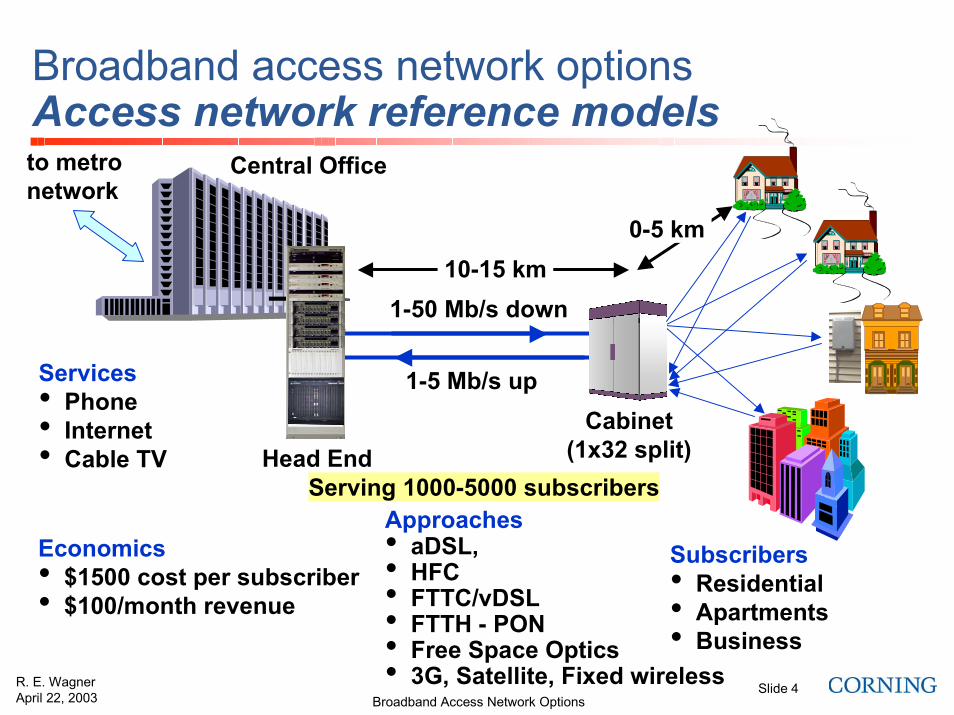

Broadband access network optionsAccess network reference models

1-50 Mb/s down

1-5 Mb/s upServices• Phone• Internet• Cable TV Head End

Central Office

Subscribers• Residential• Apartments• Business

10-15 km 0-5 km

Cabinet(1x32 split)

Economics• $1500 cost per subscriber• $100/month revenue

to metronetwork

Serving 1000-5000 subscribersApproaches• aDSL,• HFC• FTTC/vDSL• FTTH - PON• Free Space Optics• 3G, Satellite, Fixed wireless

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 5

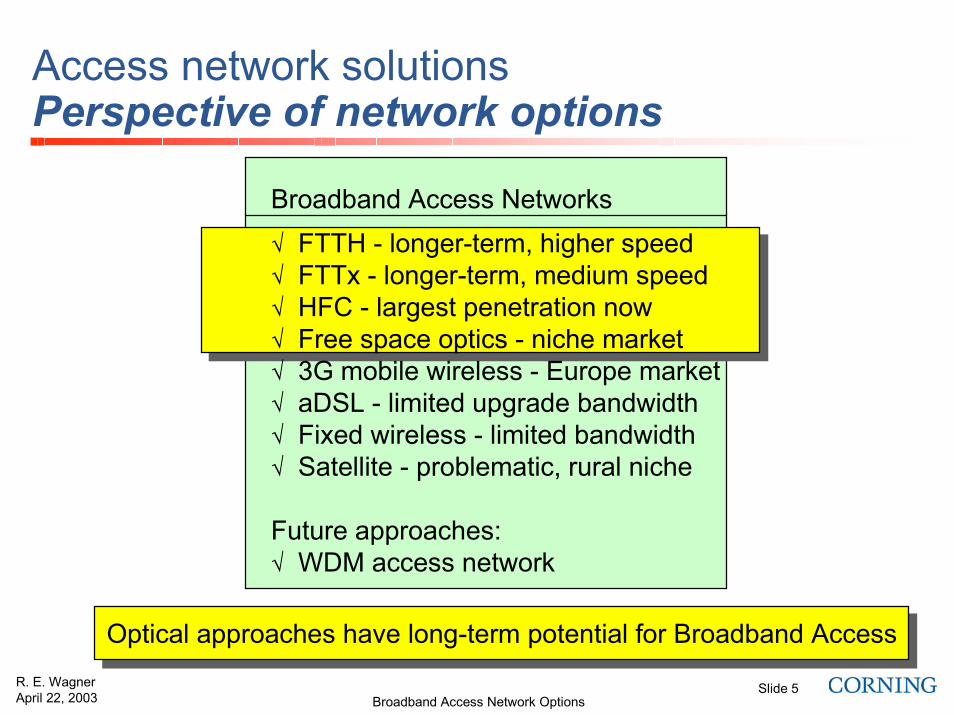

Access network solutionsPerspective of network options

Broadband Access Networks

� FTTH - longer-term, higher speed� FTTx - longer-term, medium speed� HFC - largest penetration now� Free space optics - niche market� 3G mobile wireless - Europe market� aDSL - limited upgrade bandwidth� Fixed wireless - limited bandwidth� Satellite - problematic, rural niche

Future approaches:� WDM access network

Optical approaches have long-term potential for Broadband AccessOptical approaches have long-term potential for Broadband Access

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 6

Broadband access network optionsOutline of the presentation

• Introduction to access networks

• Drivers and trends in access deployments

• Access network architecture options

• Network solutions of advantage to the optics industry

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 7

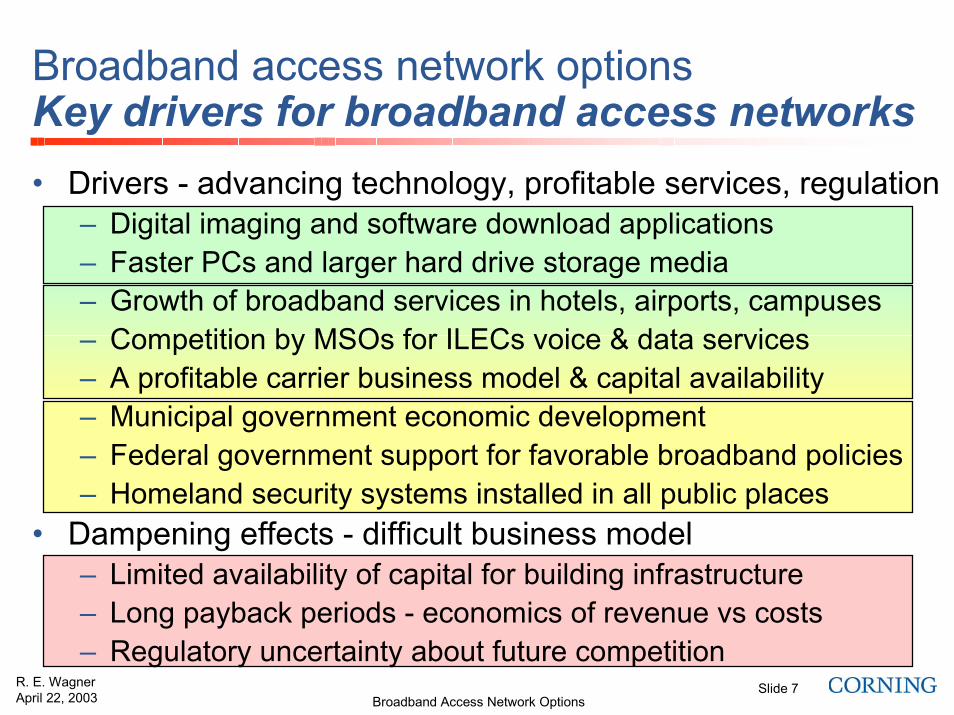

Broadband access network optionsKey drivers for broadband access networks• Drivers - advancing technology, profitable services, regulation

– Digital imaging and software download applications– Faster PCs and larger hard drive storage media– Growth of broadband services in hotels, airports, campuses– Competition by MSOs for ILECs voice & data services– A profitable carrier business model & capital availability– Municipal government economic development– Federal government support for favorable broadband policies– Homeland security systems installed in all public places

• Dampening effects - difficult business model– Limited availability of capital for building infrastructure– Long payback periods - economics of revenue vs costs– Regulatory uncertainty about future competition

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 8

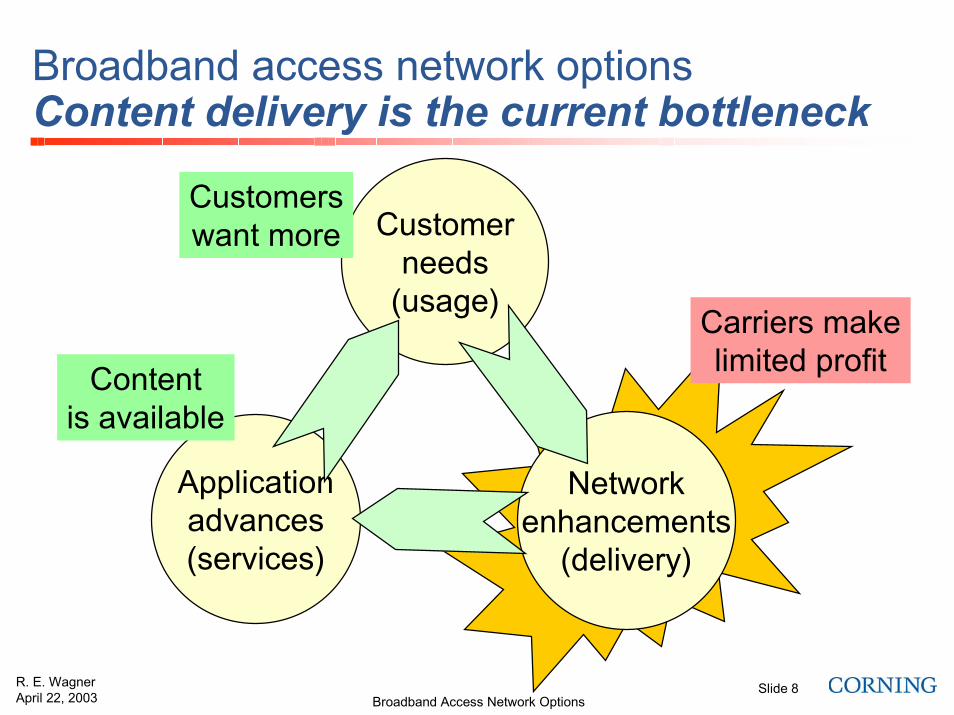

Broadband access network optionsContent delivery is the current bottleneck

Customerneeds

(usage)

Applicationadvances(services)

Networkenhancements

(delivery)

Customerswant more

Carriers makelimited profitContent

is available

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 9

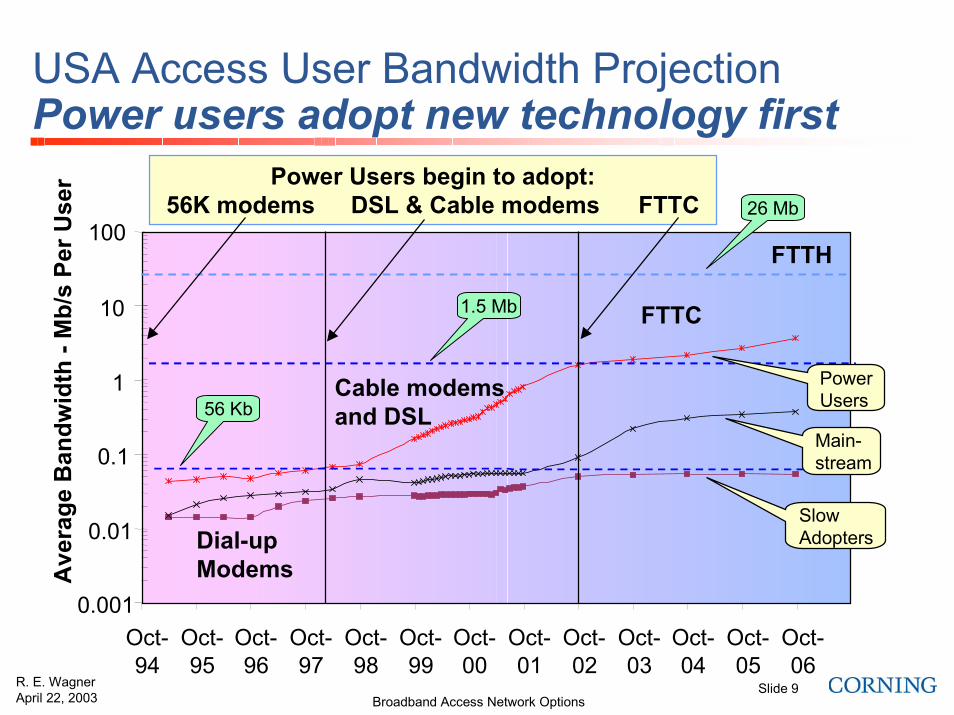

USA Access User Bandwidth ProjectionPower users adopt new technology first

Power Users begin to adopt: 56K modems DSL & Cable modems FTTC

0.001

0.01

0.1

1

10

Oct-94

Oct-95

Oct-96

Oct-97

Oct-98

Oct-99

Oct-00

Oct-01

Oct-02

Oct-03

Oct-04

Oct-05

Oct-06

Ave

rage

Ban

dwid

th -

Mb/

s Pe

r Use

r

PowerUsers

Main-stream

SlowAdopters

56 Kb

1.5 Mb

26 Mb100

Dial-upModems

Cable modemsand DSL

FTTC

FTTH

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 10

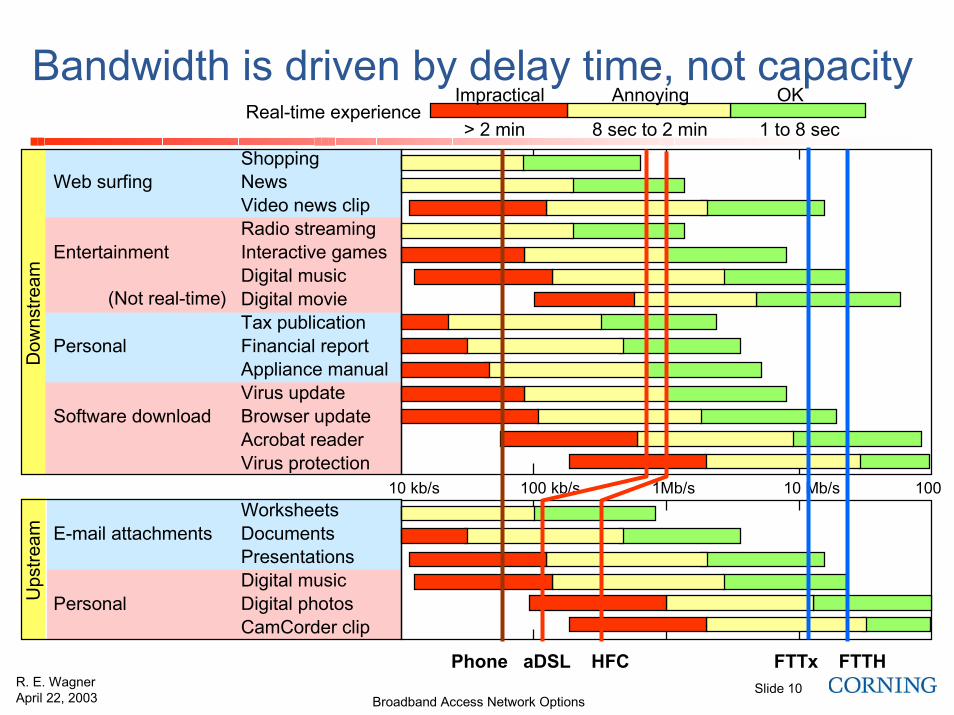

Bandwidth is driven by delay time, not capacity

Web surfing

Entertainment

Personal

Software download

E-mail attachments

Personal

ShoppingNewsVideo news clipRadio streamingInteractive gamesDigital musicDigital movieTax publicationFinancial reportAppliance manualVirus updateBrowser updateAcrobat readerVirus protection

WorksheetsDocumentsPresentationsDigital musicDigital photosCamCorder clip

10 kb/s 100 kb/s 1Mb/s 10 Mb/s 100

> 2 min 8 sec to 2 min 1 to 8 sec

Impractical Annoying OK

Phone aDSL HFC FTTx FTTH

Ups

tream

Dow

nstre

am

(Not real-time)

Real-time experience

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 11

Monthly revenue trends by segmentRevenue growth does not match bandwidth

$10

$100

$1,000

$10,000

$100,000

100 1000 10000 100000 1000000

Rev

enue

per

Mon

th

Dial-Up Modem

Local Phone

Total Phone

DSL

Cable TV

Sprint Wireless

2Way Direct PC

iDSL

DSL (business)

OSI

WWP

T1

Ameritech DS3(45Mbps)Ameritech OC3(155Mbps)

10 kbps

100 kbps

1 Mbps 10 Mbps

100 Mbps

1 Gbps

Residential Trend

ILEC Trendfor private lines

Ethernet Trend

Revenuematches

Bandwidth

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 12

Broadband access network optionsOutline of the presentation

• Introduction to access networks

• Drivers and trends in access deployments

• Access network architecture options

• Network solutions of advantage to the optics industry

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 13

Broadband access network optionsaDSL and FTTC/vDSL

Remote terminal - Power needed

CO

aDSL1-7 Mbps

12Kft

T1 - T3 < 5 milesOC-3 - 12 > 5 miles

vDSL (aka FTTC)13-52 Mbps

6Kft

OC-3 - 48Any distance

DLC (Cu)NGDLC (Fiber)

aDSL1-7 Mbps

12Kft

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 14

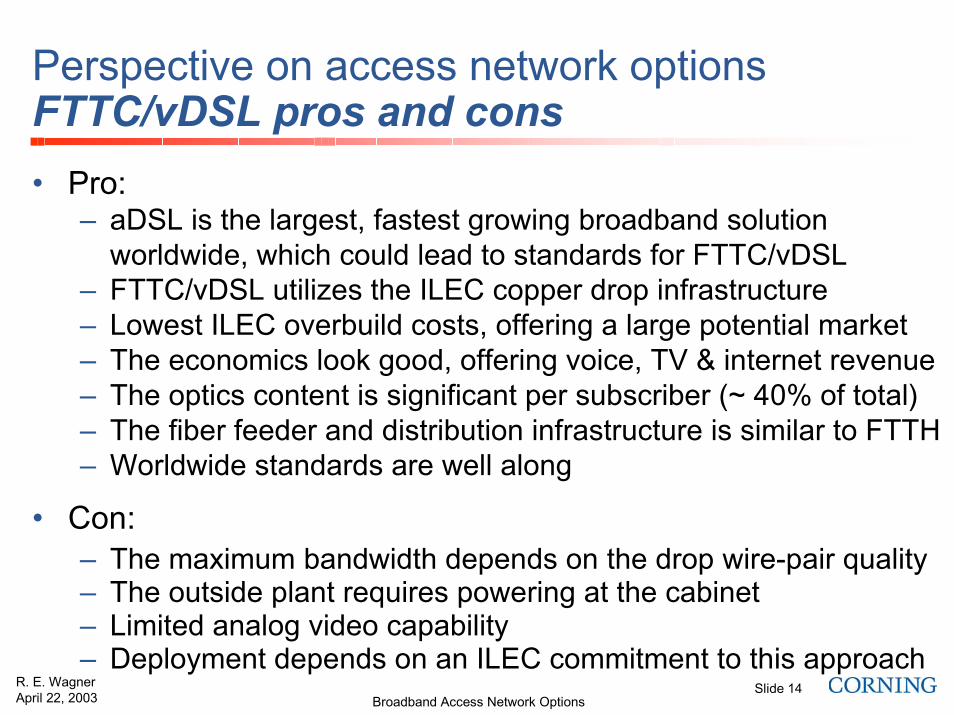

Perspective on access network optionsFTTC/vDSL pros and cons• Pro:

– aDSL is the largest, fastest growing broadband solutionworldwide, which could lead to standards for FTTC/vDSL

– FTTC/vDSL utilizes the ILEC copper drop infrastructure– Lowest ILEC overbuild costs, offering a large potential market– The economics look good, offering voice, TV & internet revenue– The optics content is significant per subscriber (~ 40% of total)– The fiber feeder and distribution infrastructure is similar to FTTH– Worldwide standards are well along

• Con:– The maximum bandwidth depends on the drop wire-pair quality– The outside plant requires powering at the cabinet– Limited analog video capability– Deployment depends on an ILEC commitment to this approach

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 15

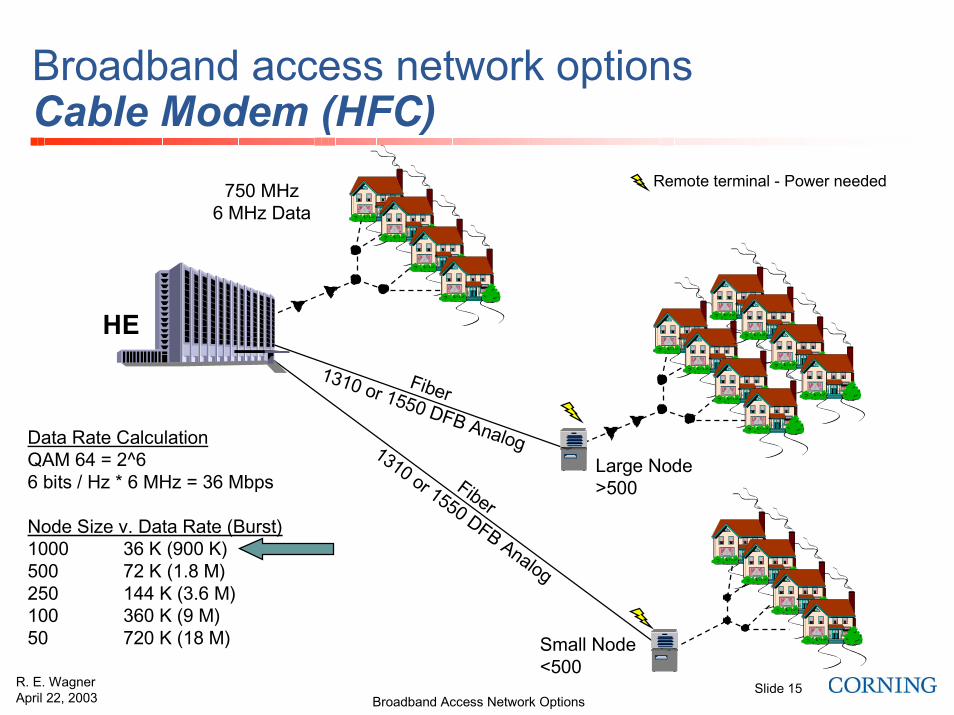

Broadband access network optionsCable Modem (HFC)

Data Rate CalculationQAM 64 = 2^66 bits / Hz * 6 MHz = 36 Mbps

Node Size v. Data Rate (Burst)1000 36 K (900 K)500 72 K (1.8 M)250 144 K (3.6 M)100 360 K (9 M)50 720 K (18 M)

HE

750 MHz6 MHz Data

Fiber1310 or 1550 DFB Analog

Large Node>500

Small Node<500

Fiber

1310 or 1550 DFB Analog

Remote terminal - Power needed

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 16

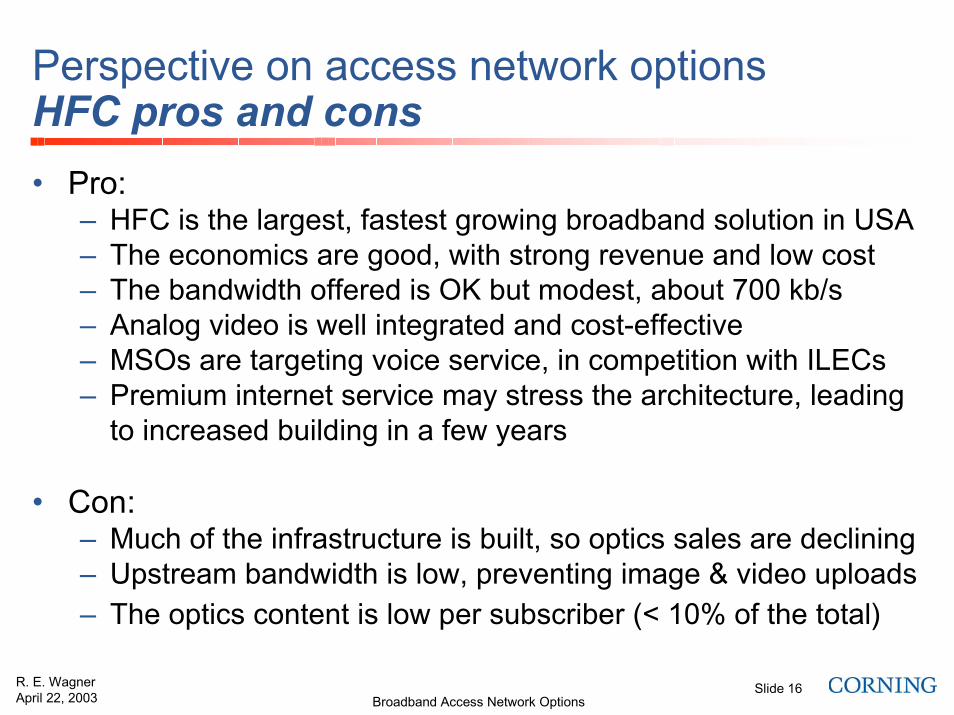

Perspective on access network optionsHFC pros and cons• Pro:

– HFC is the largest, fastest growing broadband solution in USA– The economics are good, with strong revenue and low cost– The bandwidth offered is OK but modest, about 700 kb/s– Analog video is well integrated and cost-effective– MSOs are targeting voice service, in competition with ILECs– Premium internet service may stress the architecture, leading

to increased building in a few years

• Con:– Much of the infrastructure is built, so optics sales are declining– Upstream bandwidth is low, preventing image & video uploads– The optics content is low per subscriber (< 10% of the total)

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 17

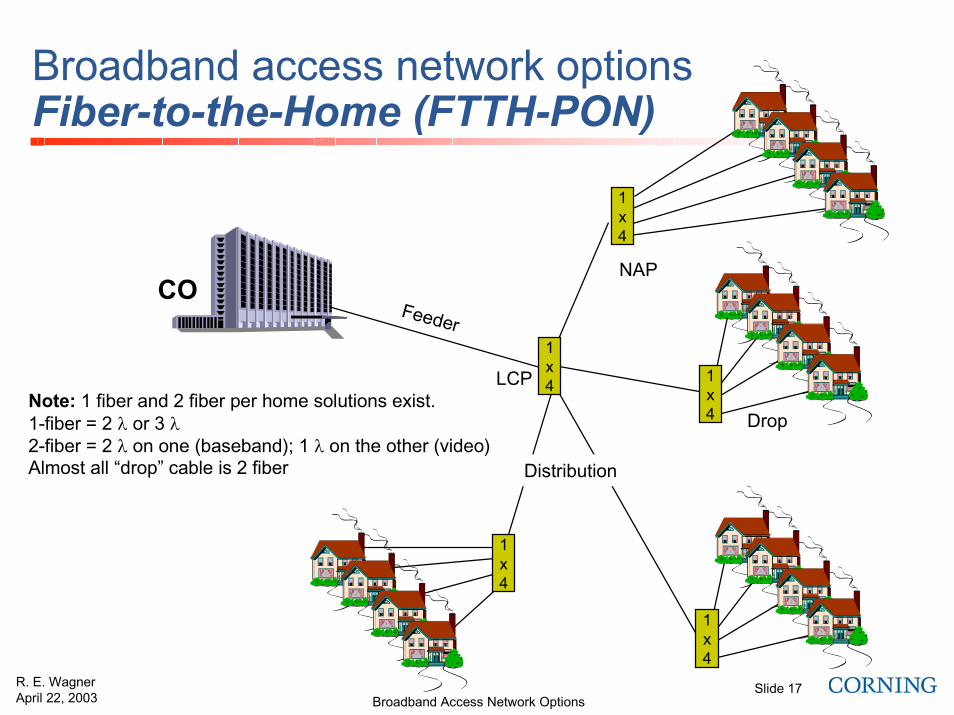

Broadband access network optionsFiber-to-the-Home (FTTH-PON)

CO

1x4

1x4

1x4

1x4

1x4

Distribution

Feeder

Drop

LCP

NAP

Note: 1 fiber and 2 fiber per home solutions exist.1-fiber = 2 � or 3 �2-fiber = 2 � on one (baseband); 1 � on the other (video)Almost all “drop” cable is 2 fiber

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 18

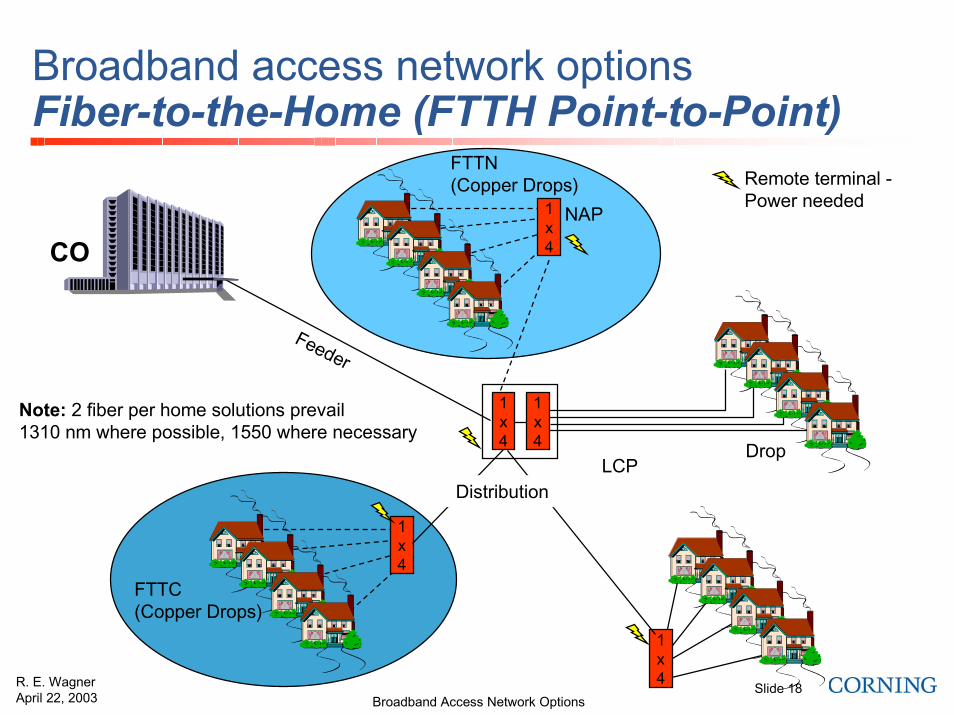

Broadband access network optionsFiber-to-the-Home (FTTH Point-to-Point)

Remote terminal -Power needed

Note: 2 fiber per home solutions prevail1310 nm where possible, 1550 where necessary

CO

1x4

Feeder

Drop

1x4

NAP

FTTN(Copper Drops)

1x4

FTTC(Copper Drops)

1x4

1x4

LCPDistribution

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 19

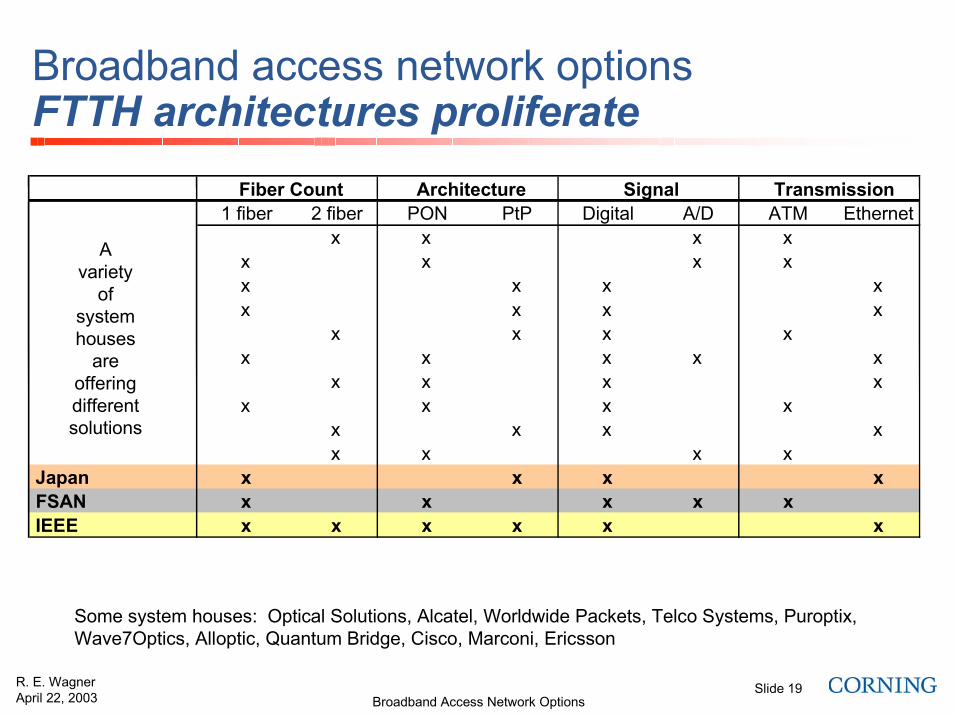

Broadband access network optionsFTTH architectures proliferate

1 fiber 2 fiber PON PtP Digital A/D ATM Ethernet

Avariety

ofsystemhouses

areofferingdifferentsolutions

x x x xx x x xx x x xx x x x

x x x xx x x x x

x x x xx x x x

x x x xx x x x

Japan x x x xFSAN x x x x xIEEE x x x x x x

Fiber Count Architecture Signal Transmission

Some system houses: Optical Solutions, Alcatel, Worldwide Packets, Telco Systems, Puroptix,Wave7Optics, Alloptic, Quantum Bridge, Cisco, Marconi, Ericsson

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 20

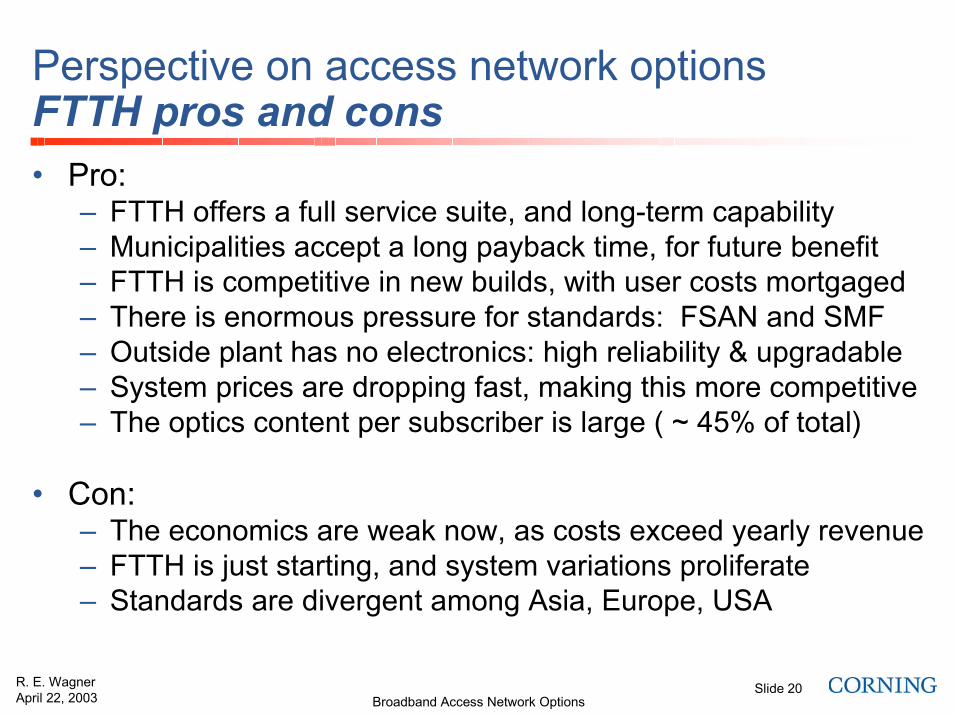

Perspective on access network optionsFTTH pros and cons• Pro:

– FTTH offers a full service suite, and long-term capability– Municipalities accept a long payback time, for future benefit– FTTH is competitive in new builds, with user costs mortgaged– There is enormous pressure for standards: FSAN and SMF– Outside plant has no electronics: high reliability & upgradable– System prices are dropping fast, making this more competitive– The optics content per subscriber is large ( ~ 45% of total)

• Con:– The economics are weak now, as costs exceed yearly revenue– FTTH is just starting, and system variations proliferate– Standards are divergent among Asia, Europe, USA

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 21

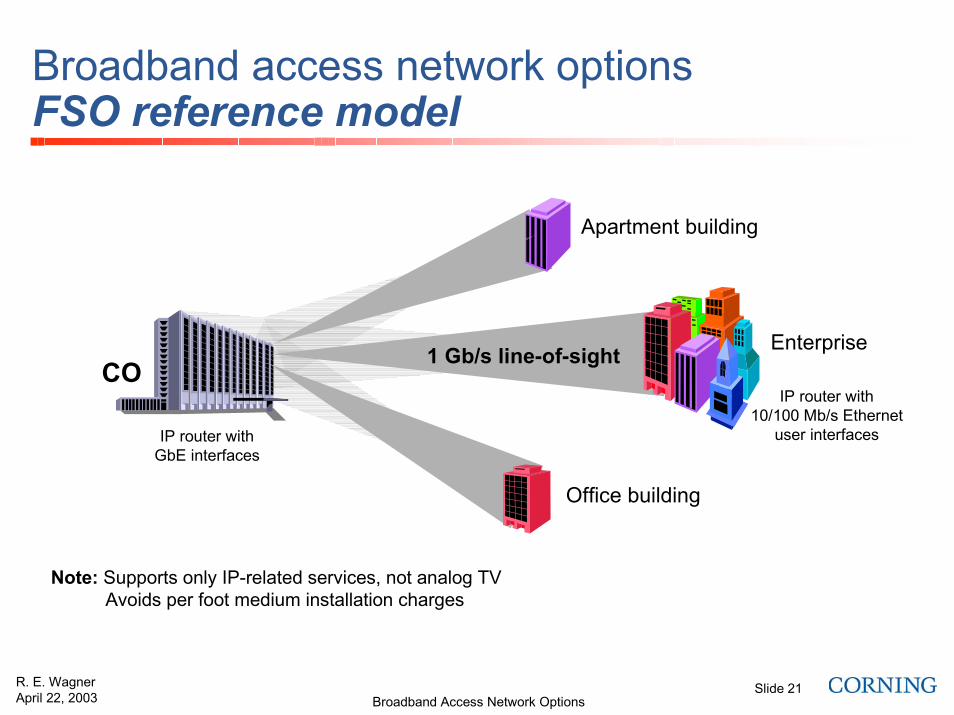

Broadband access network optionsFSO reference model

Note: Supports only IP-related services, not analog TVAvoids per foot medium installation charges

COEnterprise1 Gb/s line-of-sight

Office building

Apartment building

IP router withGbE interfaces

IP router with10/100 Mb/s Ethernet

user interfaces

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 22

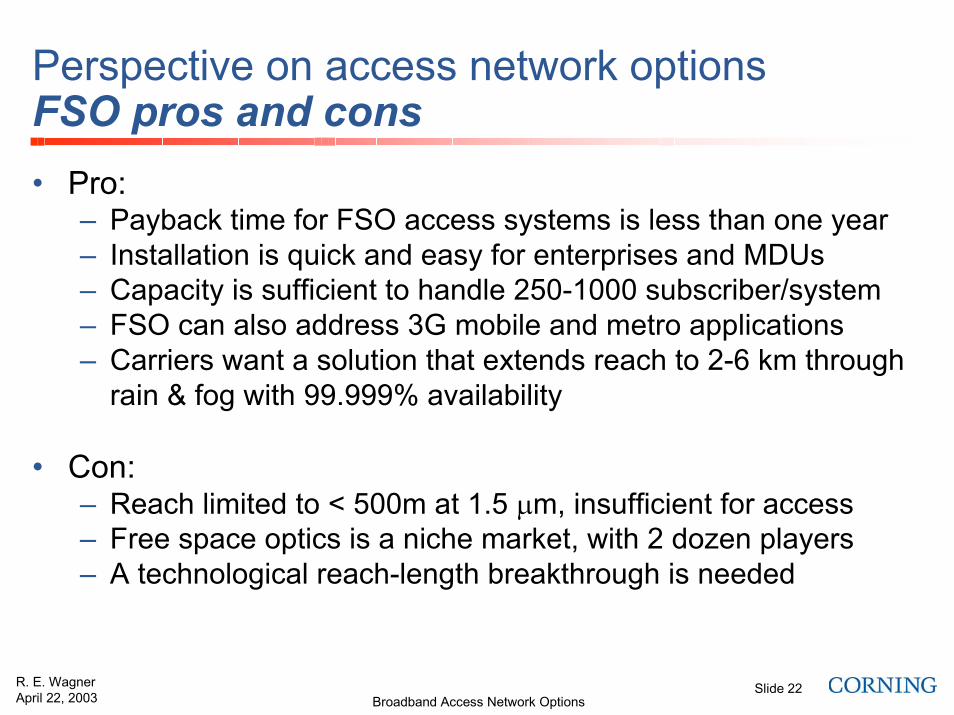

Perspective on access network optionsFSO pros and cons• Pro:

– Payback time for FSO access systems is less than one year– Installation is quick and easy for enterprises and MDUs– Capacity is sufficient to handle 250-1000 subscriber/system– FSO can also address 3G mobile and metro applications– Carriers want a solution that extends reach to 2-6 km through

rain & fog with 99.999% availability

• Con:– Reach limited to < 500m at 1.5 �m, insufficient for access– Free space optics is a niche market, with 2 dozen players– A technological reach-length breakthrough is needed

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

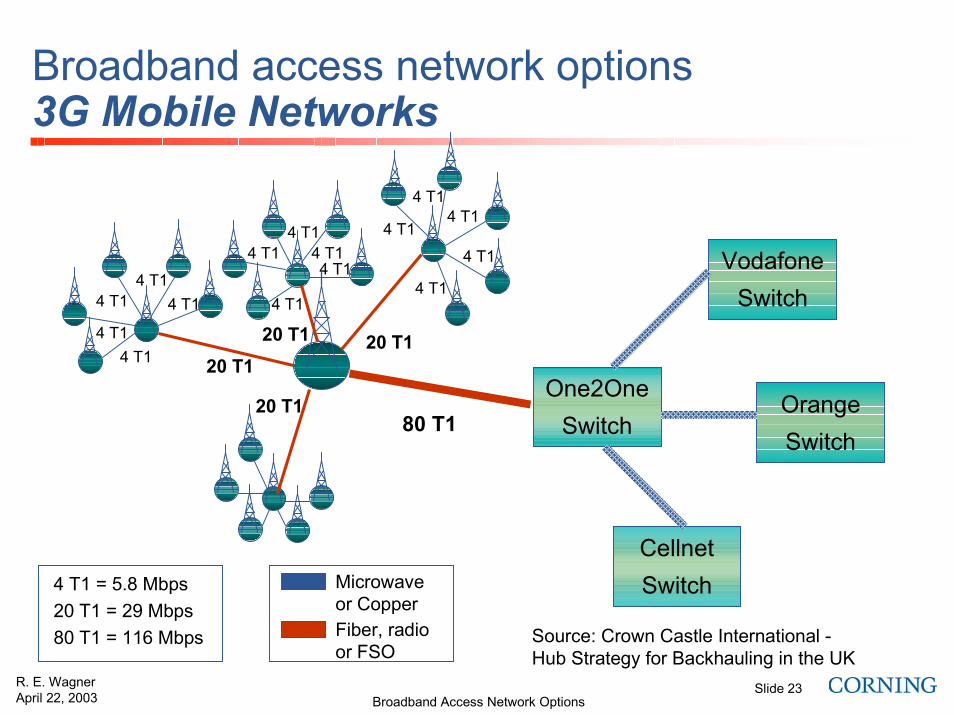

Slide 23

4 T14 T1

4 T14 T1

4 T1

4 T1 20 T120 T1

20 T1

20 T14 T1

4 T14 T1

4 T14 T1

4 T1

4 T14 T1

4 T1

Broadband access network options3G Mobile Networks

One2OneSwitch

VodafoneSwitch

OrangeSwitch

CellnetSwitch

80 T1

Source: Crown Castle International -Hub Strategy for Backhauling in the UK

4 T1 = 5.8 Mbps20 T1 = 29 Mbps80 T1 = 116 Mbps

Microwaveor CopperFiber, radioor FSO

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 24

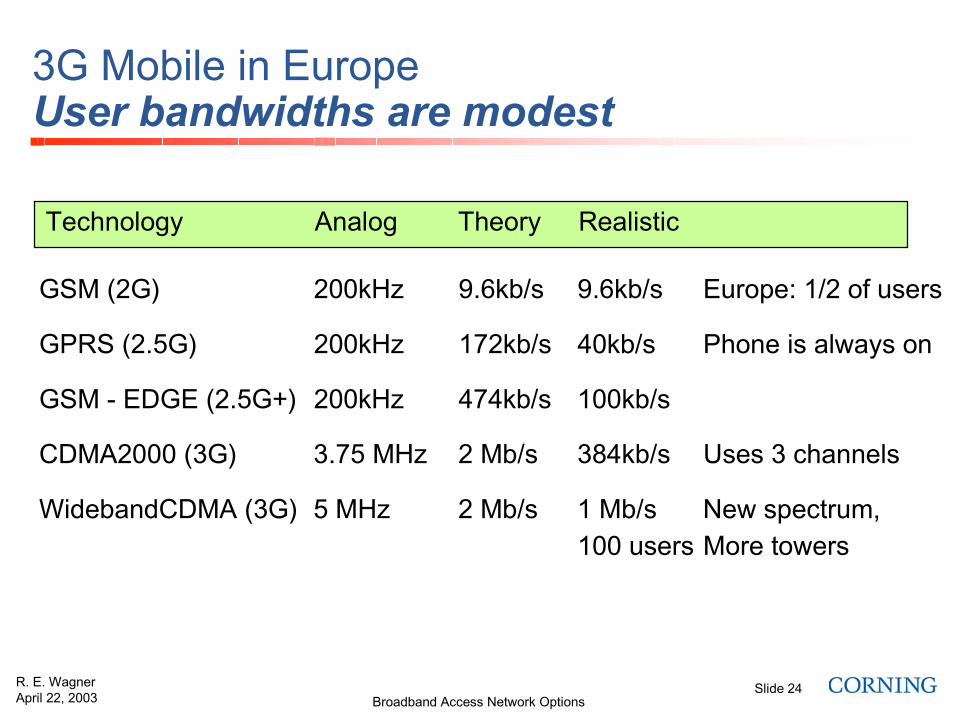

3G Mobile in EuropeUser bandwidths are modest

GSM (2G) 200kHz 9.6kb/s 9.6kb/s Europe: 1/2 of users

GPRS (2.5G) 200kHz 172kb/s 40kb/s Phone is always on

GSM - EDGE (2.5G+) 200kHz 474kb/s 100kb/s

CDMA2000 (3G) 3.75 MHz 2 Mb/s 384kb/s Uses 3 channels

WidebandCDMA (3G) 5 MHz 2 Mb/s 1 Mb/s New spectrum,100 users More towers

Technology Analog Theory Realistic

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 25

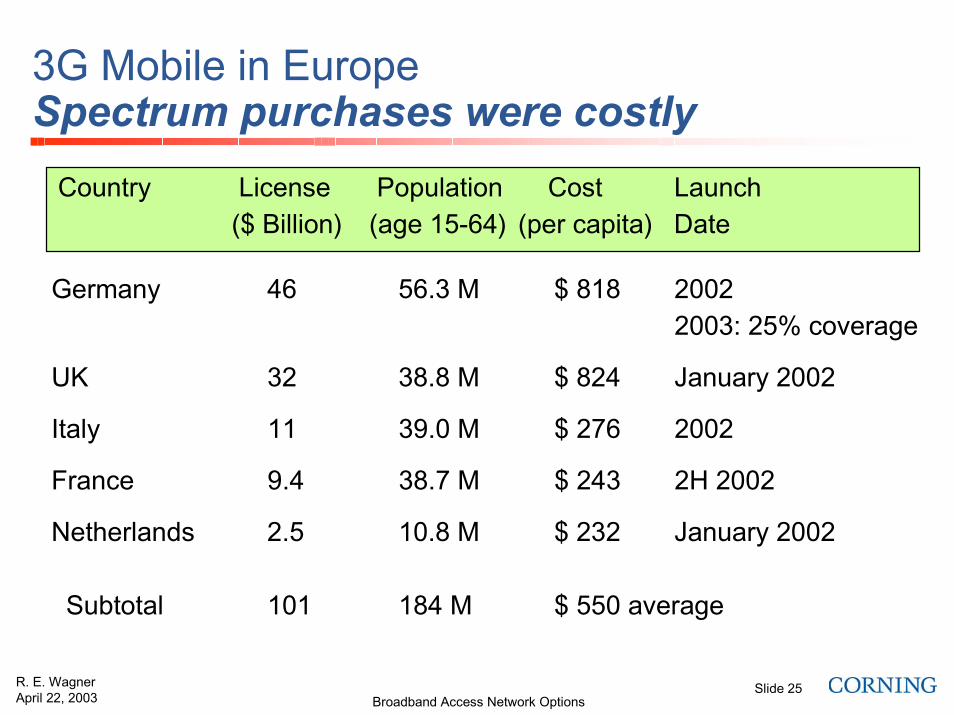

3G Mobile in EuropeSpectrum purchases were costly

Germany 46 56.3 M $ 818 20022003: 25% coverage

UK 32 38.8 M $ 824 January 2002

Italy 11 39.0 M $ 276 2002

France 9.4 38.7 M $ 243 2H 2002

Netherlands 2.5 10.8 M $ 232 January 2002

Subtotal 101 184 M $ 550 average

Country License Population Cost Launch($ Billion) (age 15-64) (per capita) Date

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 26

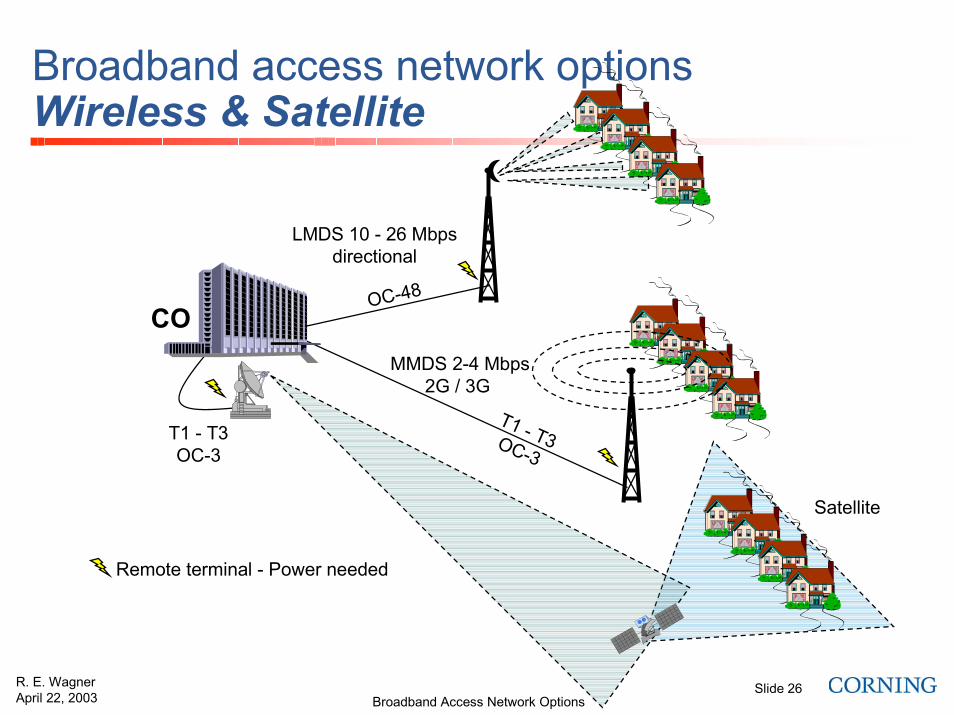

Broadband access network optionsWireless & Satellite

CO

LMDS 10 - 26 Mbpsdirectional

T1 - T3OC-3

MMDS 2-4 Mbps2G / 3G

OC-48

T1 - T3OC-3

Remote terminal - Power needed

Satellite

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 27

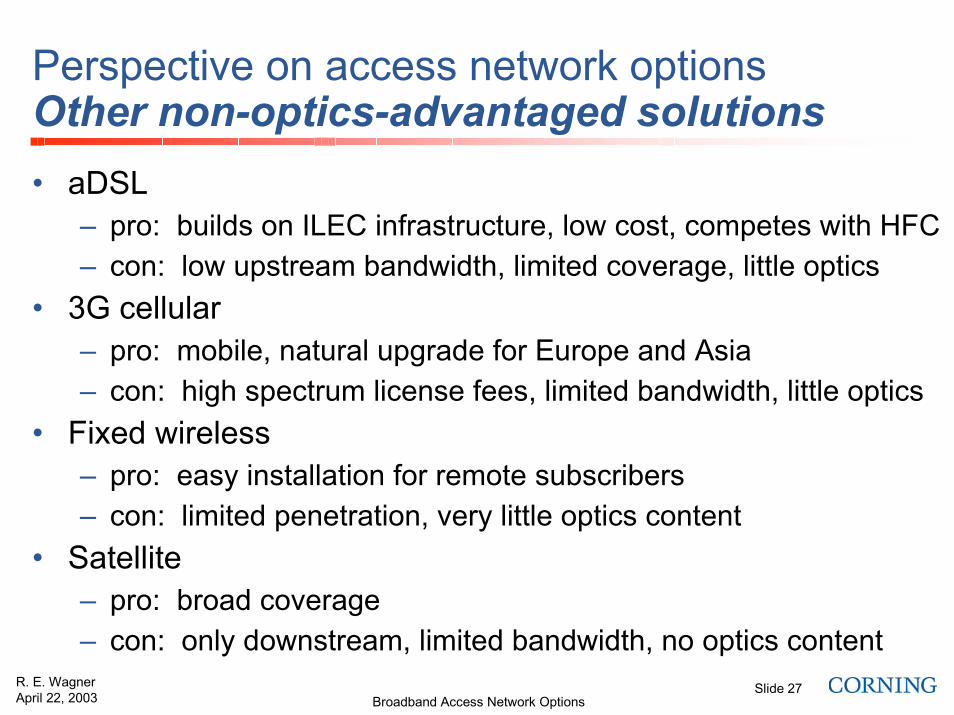

Perspective on access network optionsOther non-optics-advantaged solutions• aDSL

– pro: builds on ILEC infrastructure, low cost, competes with HFC– con: low upstream bandwidth, limited coverage, little optics

• 3G cellular– pro: mobile, natural upgrade for Europe and Asia– con: high spectrum license fees, limited bandwidth, little optics

• Fixed wireless– pro: easy installation for remote subscribers– con: limited penetration, very little optics content

• Satellite– pro: broad coverage– con: only downstream, limited bandwidth, no optics content

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 28

Broadband access network optionsOutline of the presentation

• Introduction to access networks

• Drivers and trends in access deployments

• Access network architecture options

• Network solutions of advantage to the optics industry

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 29

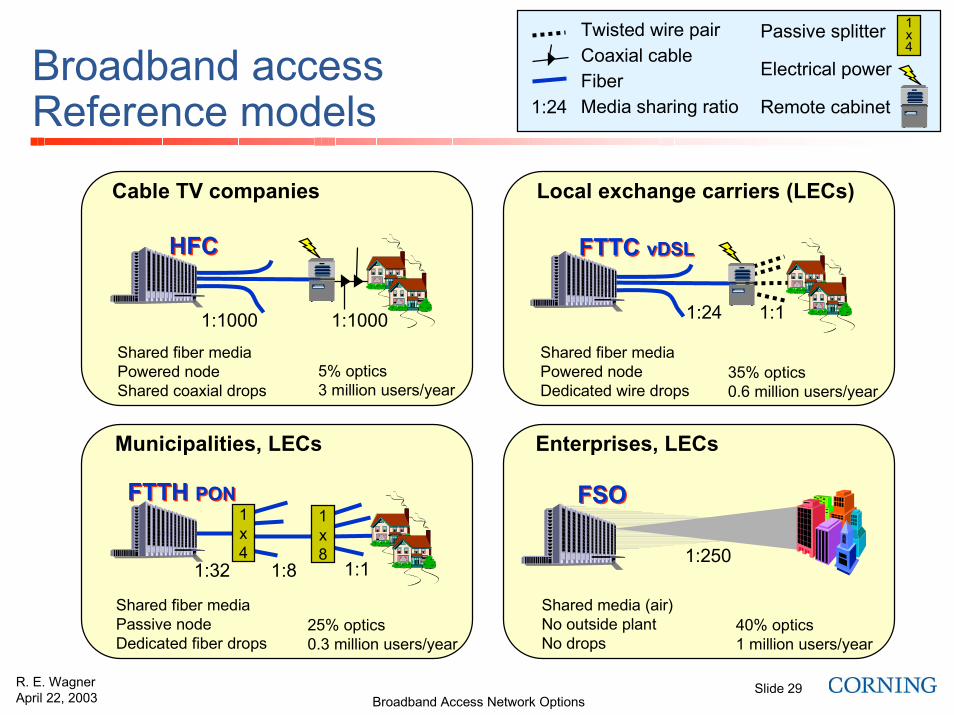

Broadband accessReference models 1:24

1x4

Twisted wire pairCoaxial cableFiberMedia sharing ratio

Passive splitter

Electrical power

Remote cabinet

1:1000 1:1000

HFCHFC

Shared fiber mediaPowered nodeShared coaxial drops

Cable TV companies

1:24 1:1

FTTC vDSLFTTC vDSL

Shared fiber mediaPowered nodeDedicated wire drops

Local exchange carriers (LECs)

1x8

1x4

1:11:81:32

FTTH PONFTTH PON

Shared fiber mediaPassive nodeDedicated fiber drops

Municipalities, LECs

FSOFSO

1:250

Shared media (air)No outside plantNo drops

Enterprises, LECs

5% optics3 million users/year

40% optics1 million users/year

25% optics0.3 million users/year

35% optics0.6 million users/year

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 30

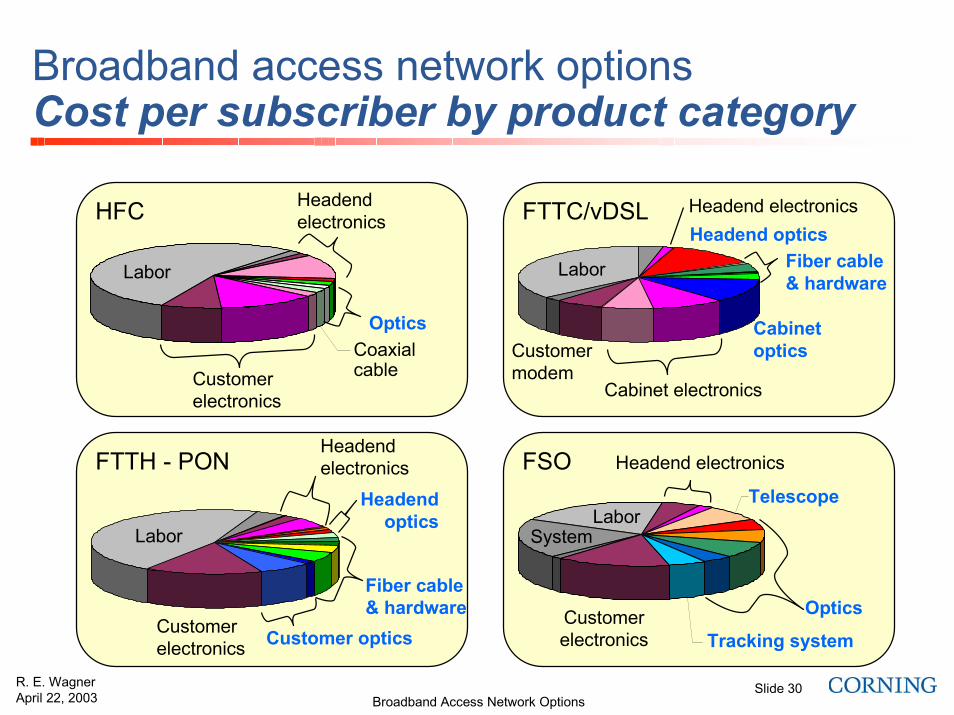

Broadband access network optionsCost per subscriber by product category

HFC Headendelectronics

OpticsCoaxialcableCustomer

electronics

Labor

FTTC/vDSL Headend electronicsHeadend optics

Fiber cable& hardware

Cabinetoptics

Cabinet electronics

Customermodem

Labor

FSO Headend electronics

Telescope

Optics Tracking system

Customerelectronics

SystemLabor

FTTH - PONHeadendelectronics

Headendoptics

Fiber cable& hardware

Customer opticsCustomerelectronics

Labor

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 31

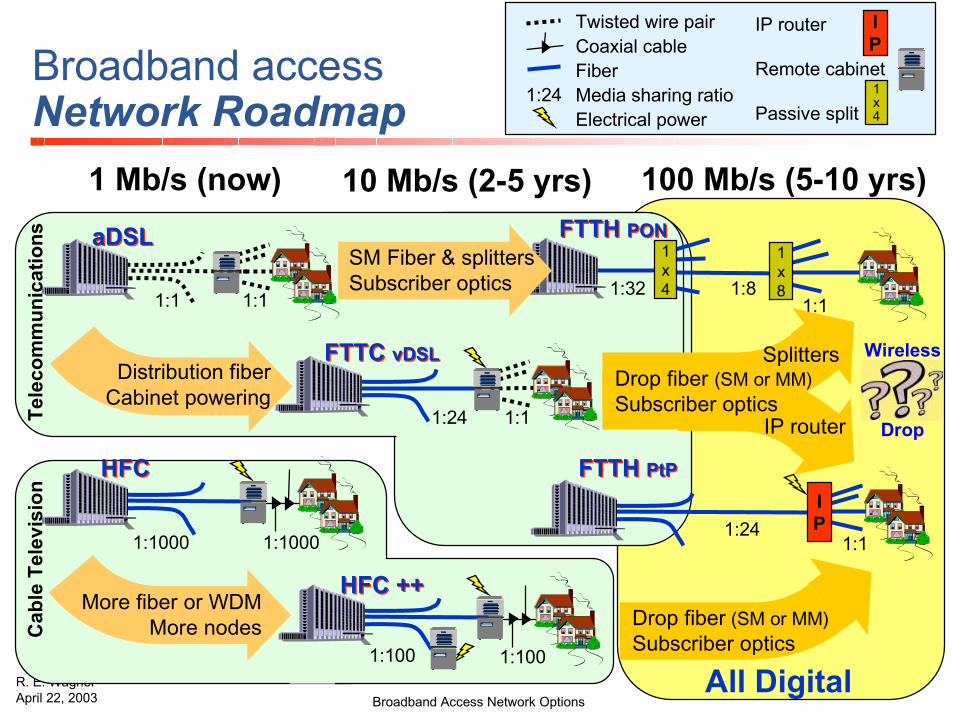

Broadband accessNetwork Roadmap

1:1

1:24 1:1

1x8

1x4

1:11:81:32

1:1000 1:1000

IP1:24

1:1

1:24

IP

1x4

Twisted wire pairCoaxial cableFiberMedia sharing ratioElectrical power

IP router

Remote cabinet

Passive split

Distribution fiberCabinet powering

More fiber or WDMMore nodes

SM Fiber & splittersSubscriber optics

Drop fiber (SM or MM)Subscriber optics

Splitters

IP router

Drop fiber (SM or MM)Subscriber optics

1 Mb/s (now) 10 Mb/s (2-5 yrs) 100 Mb/s (5-10 yrs)aDSLaDSL

HFCHFC

FTTC vDSLFTTC vDSL

FTTH PtPFTTH PtP

FTTH PONFTTH PON

All Digital

Tele

com

mun

icat

ions

Cab

le T

elev

isio

n

Wireless

Drop

1:1

HFC ++HFC ++

1:100 1:100

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 32

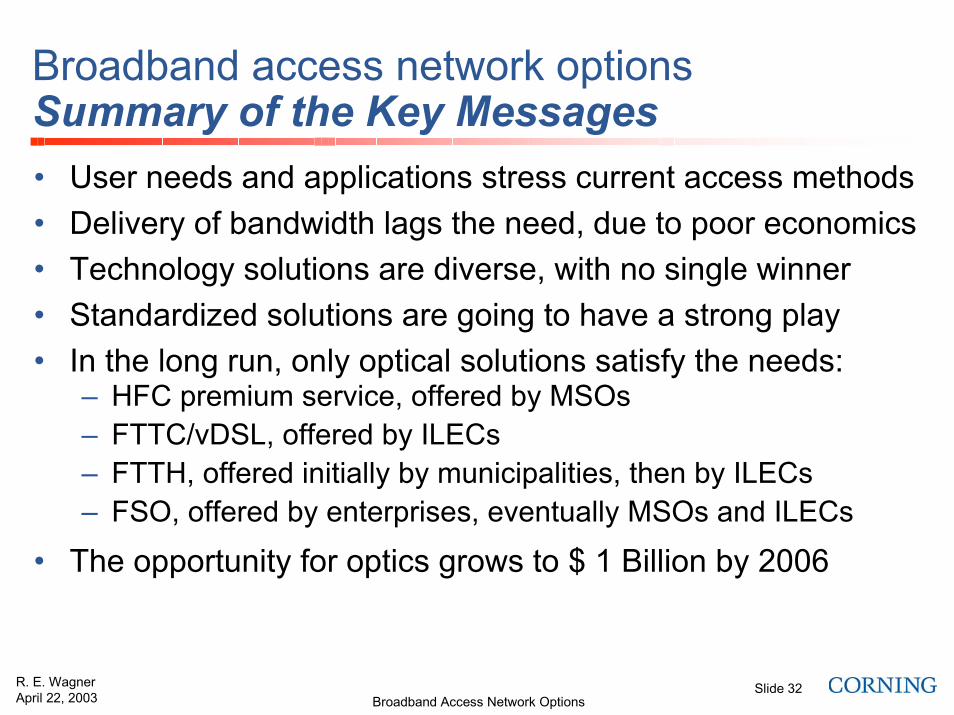

Broadband access network optionsSummary of the Key Messages• User needs and applications stress current access methods• Delivery of bandwidth lags the need, due to poor economics• Technology solutions are diverse, with no single winner• Standardized solutions are going to have a strong play• In the long run, only optical solutions satisfy the needs:

– HFC premium service, offered by MSOs– FTTC/vDSL, offered by ILECs– FTTH, offered initially by municipalities, then by ILECs– FSO, offered by enterprises, eventually MSOs and ILECs

• The opportunity for optics grows to $ 1 Billion by 2006

Broadband Access Network OptionsR. E. WagnerApril 22, 2003

Slide 33

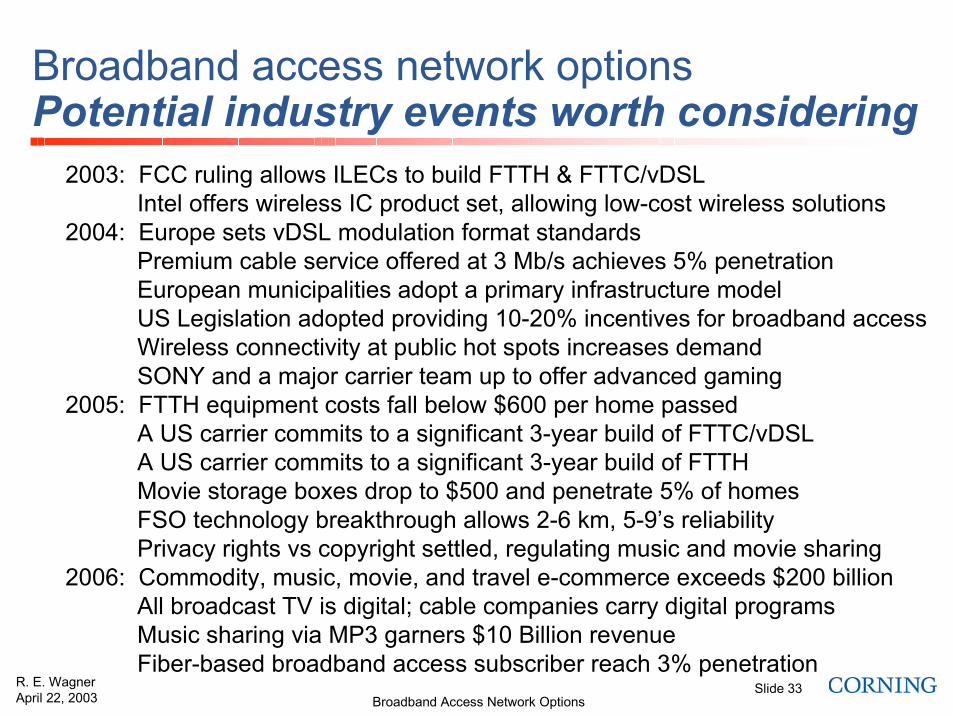

Broadband access network optionsPotential industry events worth considering

2003: FCC ruling allows ILECs to build FTTH & FTTC/vDSLIntel offers wireless IC product set, allowing low-cost wireless solutions

2004: Europe sets vDSL modulation format standardsPremium cable service offered at 3 Mb/s achieves 5% penetrationEuropean municipalities adopt a primary infrastructure modelUS Legislation adopted providing 10-20% incentives for broadband accessWireless connectivity at public hot spots increases demandSONY and a major carrier team up to offer advanced gaming

2005: FTTH equipment costs fall below $600 per home passedA US carrier commits to a significant 3-year build of FTTC/vDSLA US carrier commits to a significant 3-year build of FTTHMovie storage boxes drop to $500 and penetrate 5% of homesFSO technology breakthrough allows 2-6 km, 5-9’s reliabilityPrivacy rights vs copyright settled, regulating music and movie sharing

2006: Commodity, music, movie, and travel e-commerce exceeds $200 billionAll broadcast TV is digital; cable companies carry digital programsMusic sharing via MP3 garners $10 Billion revenueFiber-based broadband access subscriber reach 3% penetration