british meat exports: situation and...

TRANSCRIPT

British meat exports: situation and perspectivesJ.P. Garnier, AHDB Exports

Agenda

• Changing times

• Brexit: practical implications for UK meat exports

• What is happening with the market, current trade

and export perspectives for pork, lamb and beef

• Export perspectives 2016-21

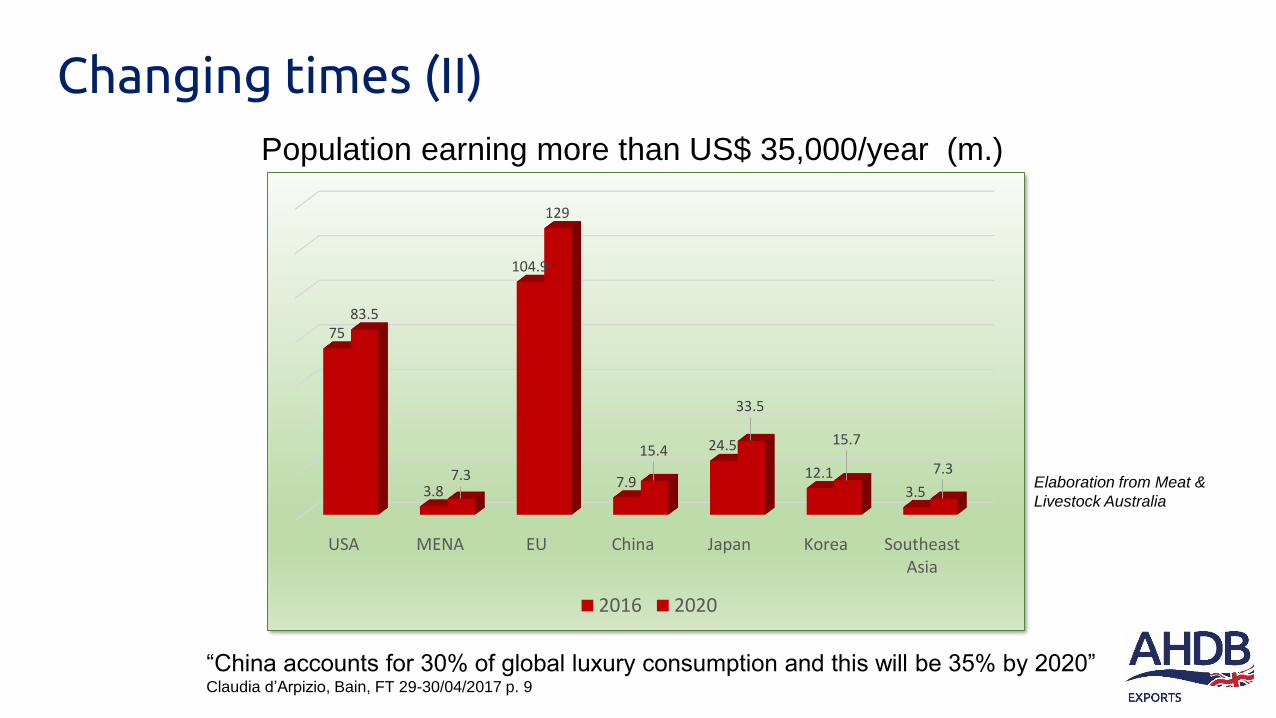

Changing times (I)

“China accounts for 30% of global luxury consumption and this will be 35% by 2020” Claudia d’Arpizio, Bain, FT 29-30/04/2017 p. 9

USA MENA EU China Japan Korea SoutheastAsia

75

3.8

104.9

7.9

24.5

12.13.5

83.5

7.3

129

15.4

33.5

15.7

7.3

2016 2020

Population earning more than US$ 35,000/year (m.)

Elaboration from Meat &

Livestock Australia

Changing times (II)

Salma Corp. Abu Dhabi

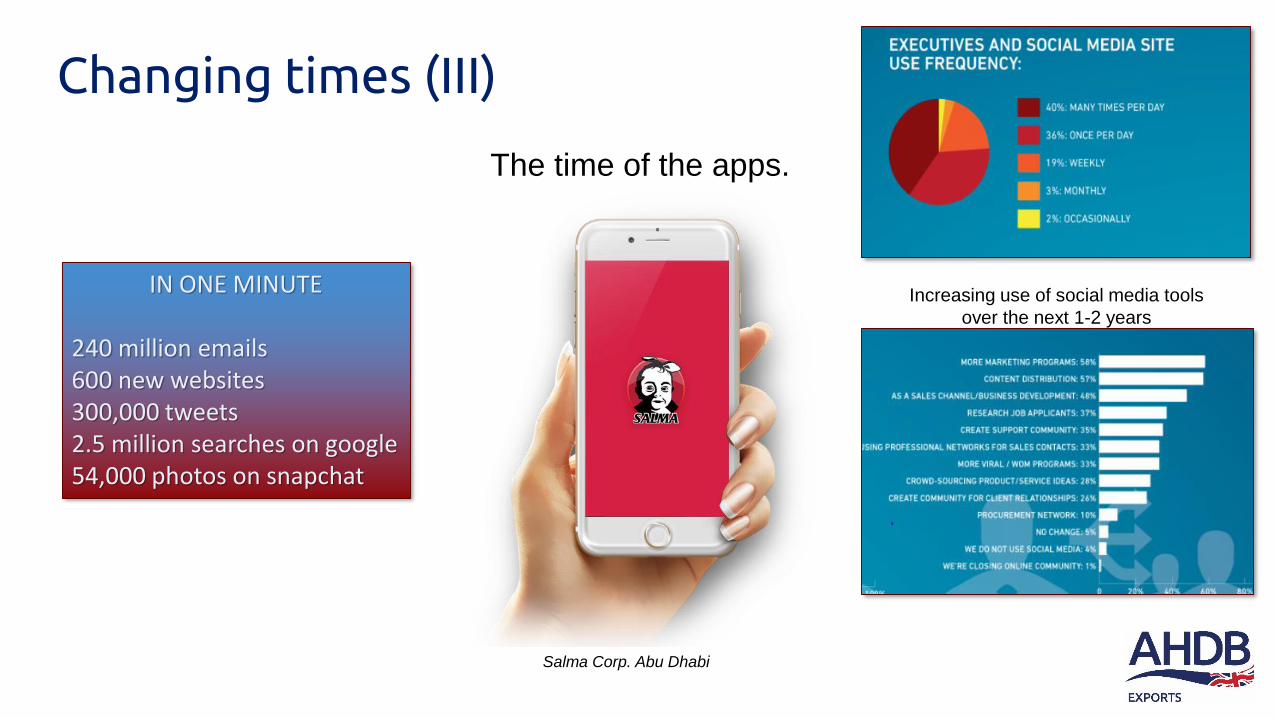

The time of the apps.

Socialnomics.com

Increasing use of social media tools

over the next 1-2 years

IN ONE MINUTE

240 million emails600 new websites300,000 tweets2.5 million searches on google54,000 photos on snapchat

Changing times (III)

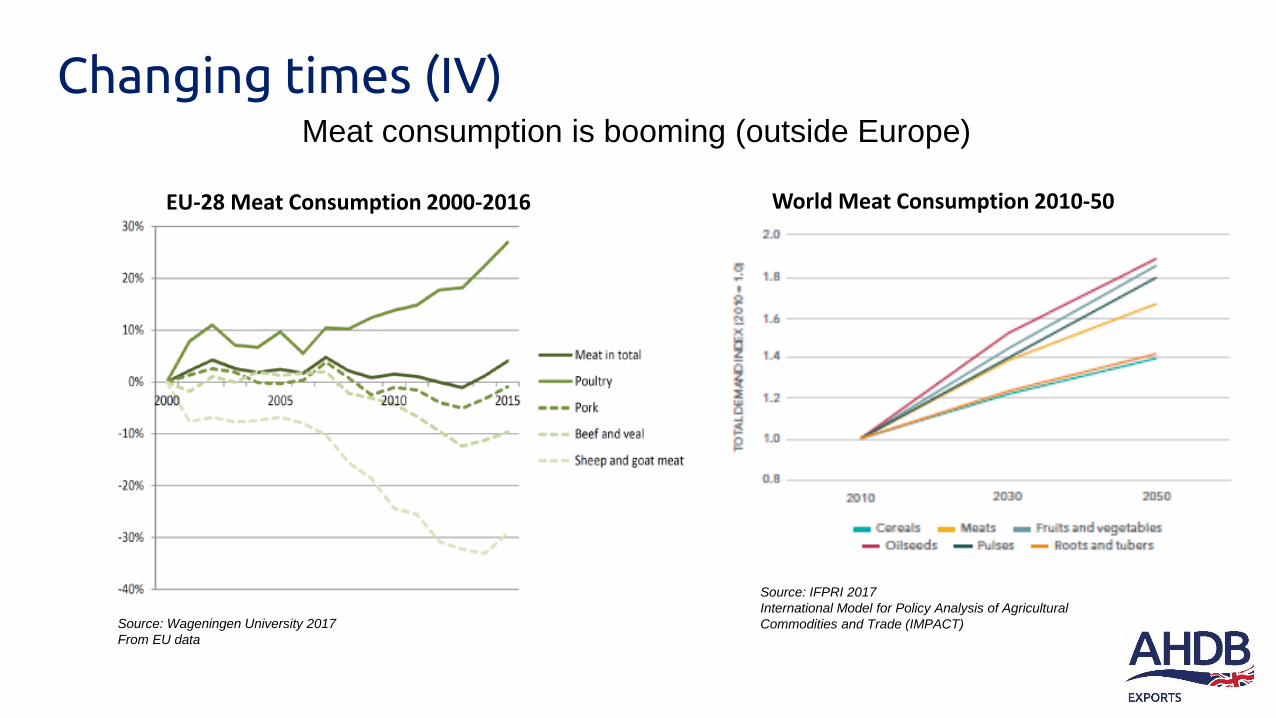

Source: Wageningen University 2017

From EU data

Source: IFPRI 2017

International Model for Policy Analysis of Agricultural

Commodities and Trade (IMPACT)

EU-28 Meat Consumption 2000-2016 World Meat Consumption 2010-50

Meat consumption is booming (outside Europe)

Changing times (IV)

We have a great story to tell!

Naturalness

Grass

Lifestyle Experience

TraditionOriginHistory

Great taste High welfare

Sustainability

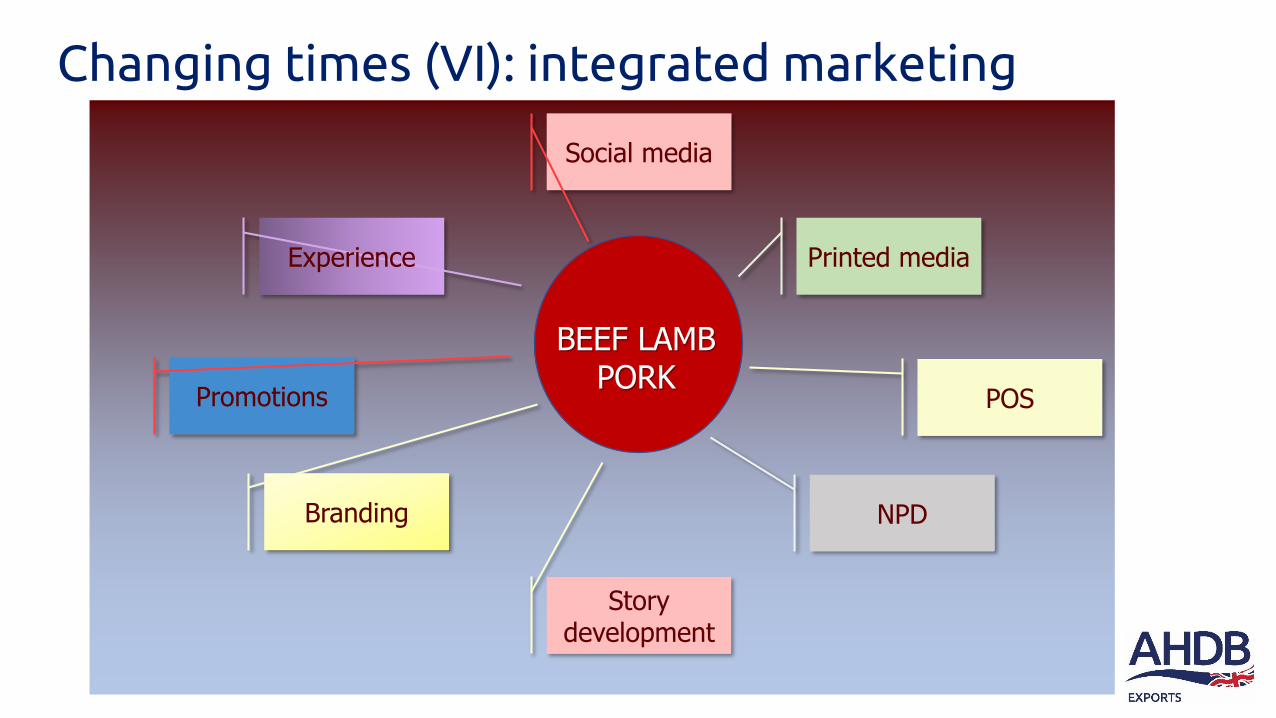

Changing times (V)

BEEF LAMB PORK

Social media

Printed media

POS

NPD

Story development

Branding

Promotions

Experience

Changing times (VI): integrated marketing

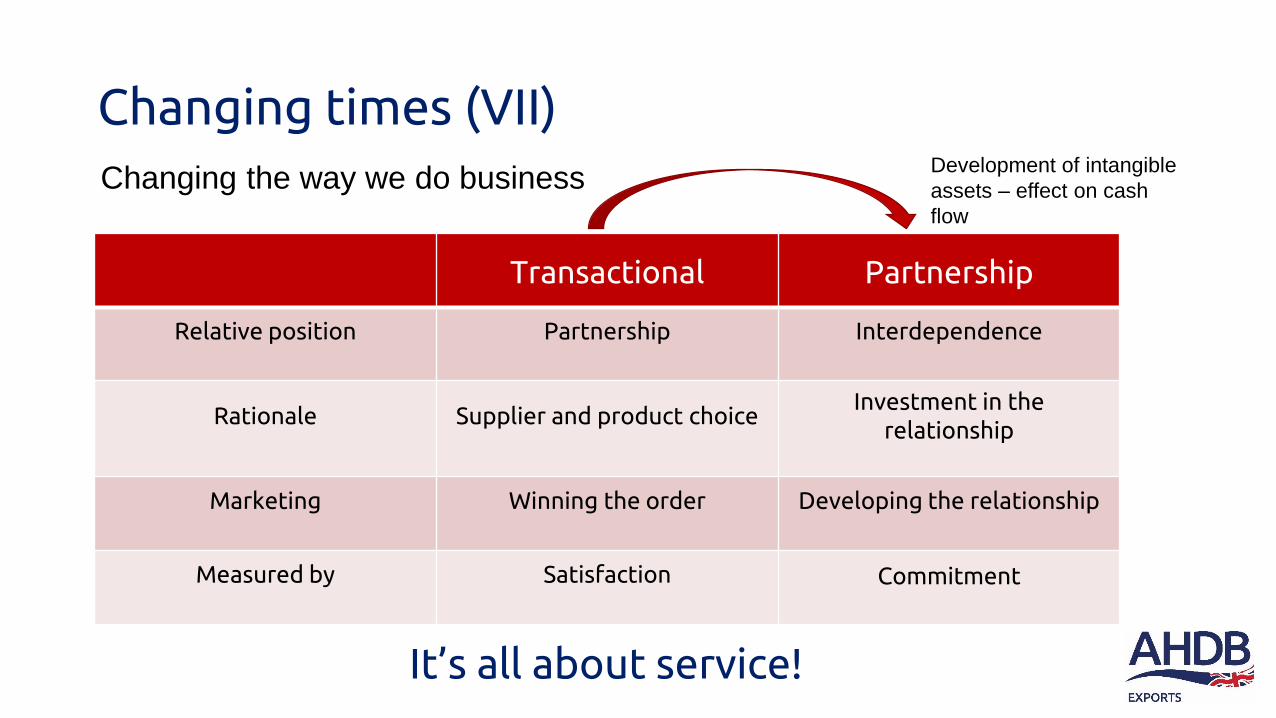

Transactional Partnership

Relative position Partnership Interdependence

Rationale Supplier and product choiceInvestment in the

relationship

Marketing Winning the order Developing the relationship

Measured by Satisfaction Commitment

Changing times (VII)

Changing the way we do businessDevelopment of intangible

assets – effect on cash

flow

It’s all about service!

Brexit (I)

ST 4 March 2016

“The only bad trade deal is the one

you are not part of.”

Geoffrey Wiggin (USDA)

Brexit (II): state of play

It will not be long before “we… all begin to find out the extent to which Brexit is a gentle stroll along a smooth path to a land of cake and consumption.”

Mark Carney, Governor of the Bank of England, June 2017

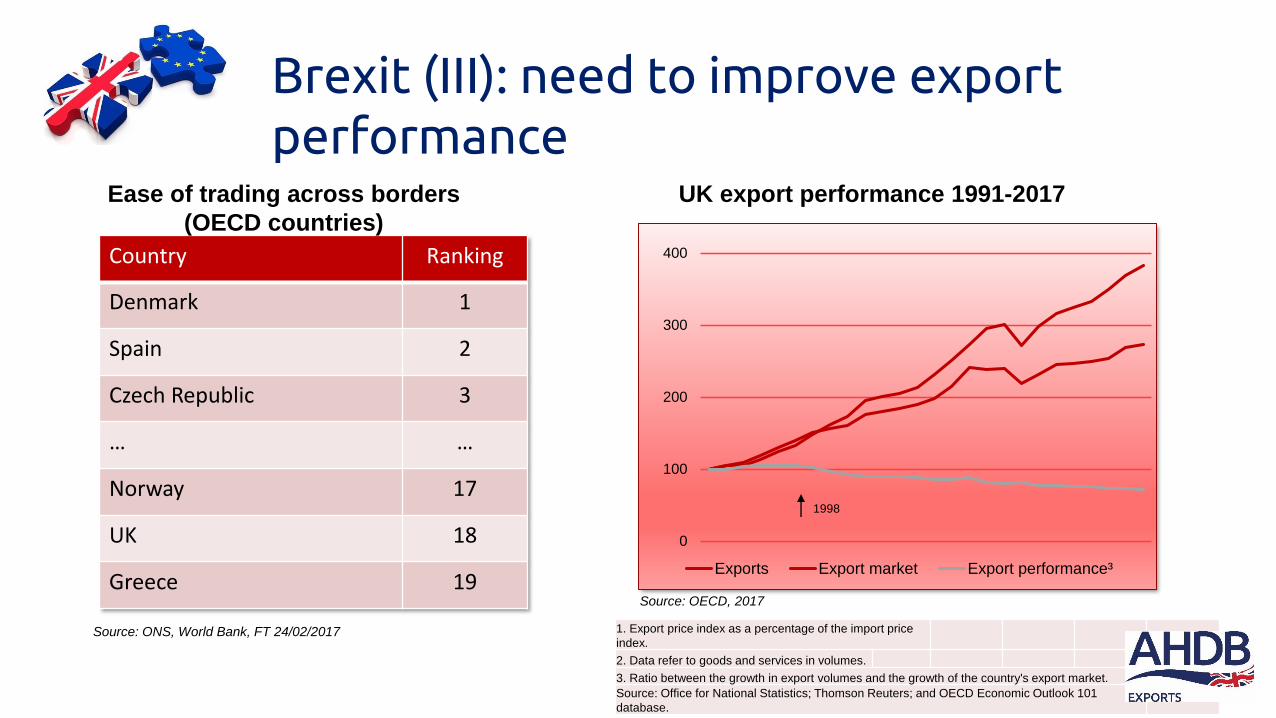

Brexit (III): need to improve export performance

Country Ranking

Denmark 1

Spain 2

Czech Republic 3

… …

Norway 17

UK 18

Greece 19

Ease of trading across borders

(OECD countries)

Source: ONS, World Bank, FT 24/02/2017

0

100

200

300

400

Exports Export market Export performance³

1998

UK export performance 1991-2017

Source: OECD, 2017

1. Export price index as a percentage of the import price

index.

2. Data refer to goods and services in volumes.

3. Ratio between the growth in export volumes and the growth of the country's export market.

Source: Office for National Statistics; Thomson Reuters; and OECD Economic Outlook 101

database.

Brexit (IV): EU exports in practice

The UK exports more than 6,000 trucks of chilled lamb yearly to the EU

• Registration of exporters with the

European Commission as Third Country

operator; regular controls

• Export documentation with proof of

origin

• Export Health Certificate is needed

• Border and veterinary control: document

control 100%, identity control 100%,

physical control 20%

• On the positive side, we already comply

with EU standards

• An additional 15,000 EHCs will be needed on top of the existing 10,000 EHCs,

meaning more than a doubling of activity in Carlisle

• As a consequence, electronic certification must be in place within approx. the next

two years

• The Government has looked into the electronic export health certification for pets,

horses, livestock and all types of livestock products for the last eight years

• We need to ensure a timely and ordered implementation of the system

Brexit (V): towards electronic health certification

• Most EHCs will need to be revised and agreed with countries and territories

• We are losing existing EU Trade Agreements which will need to be renegotiated.

(Will meat which is a time-consuming and sensitive / emotional product, be high on

the priority list?)

• This includes the negotiation of Tariff Rate Quotas or tariff-free access to some

markets

• We must not forget that the cost Non Tariff Barriers (the dreaded NTBs) is often

higher than tariffs.

• The increased cost of marketing UK produce in cost Third Countries will require

Government support

Brexit (VI): exports to Third Countries

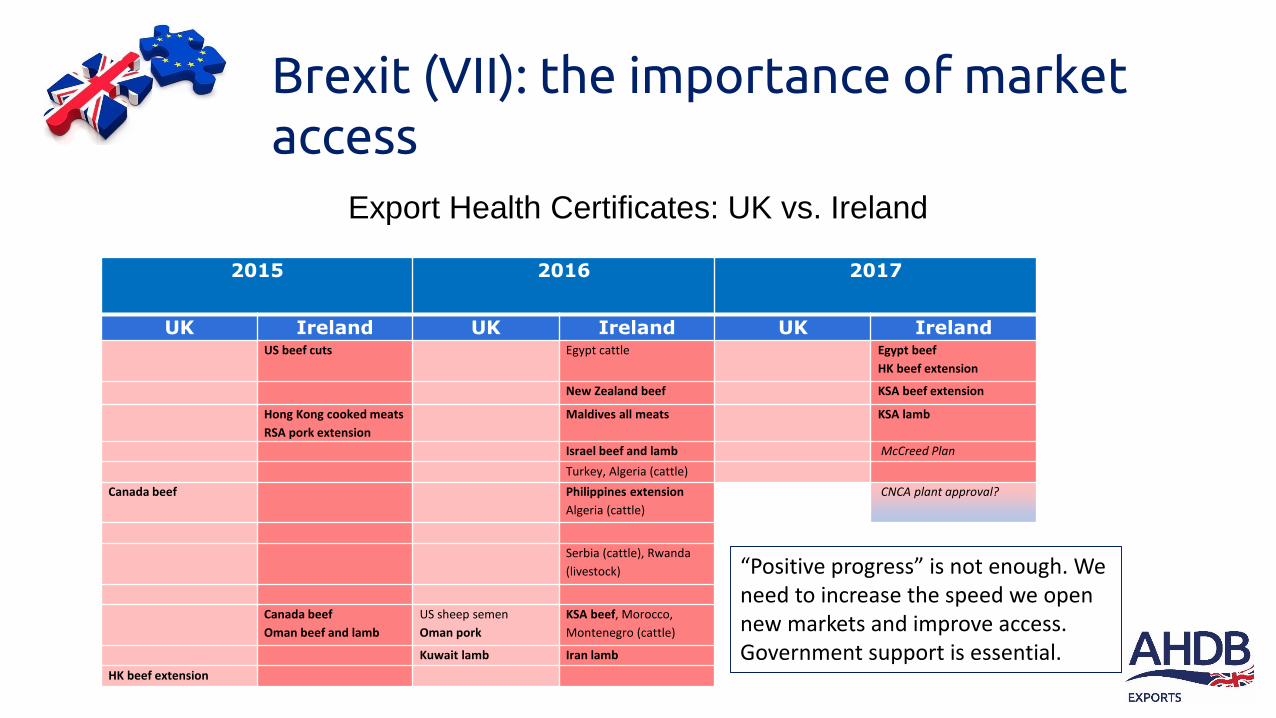

Brexit (VII): the importance of market access

2015 2016 2017

UK Ireland UK Ireland UK IrelandUS beef cuts Egypt cattle Egypt beef

HK beef extension

New Zealand beef KSA beef extension

Hong Kong cooked meats

RSA pork extension

Maldives all meats KSA lamb

Israel beef and lamb McCreed Plan

Turkey, Algeria (cattle)

Canada beef Philippines extension

Algeria (cattle)

CNCA plant approval?

Serbia (cattle), Rwanda

(livestock)

Canada beef

Oman beef and lamb

US sheep semen

Oman pork

KSA beef, Morocco,

Montenegro (cattle)

Kuwait lamb Iran lamb

HK beef extension

Export Health Certificates: UK vs. Ireland

“Positive progress” is not enough. We need to increase the speed we open new markets and improve access. Government support is essential.

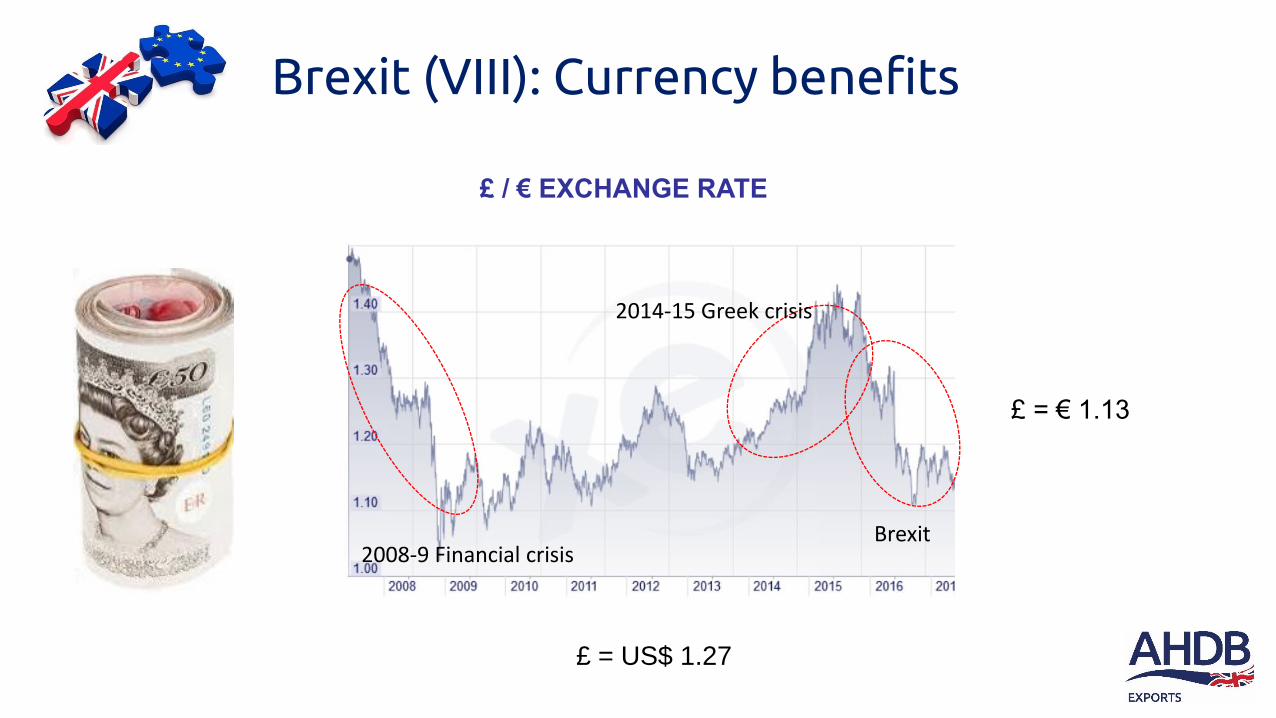

Brexit (VIII): Currency benefits

2008-9 Financial crisis

2014-15 Greek crisis

Brexit

£ = € 1.13

£ = US$ 1.27

£ / € EXCHANGE RATE

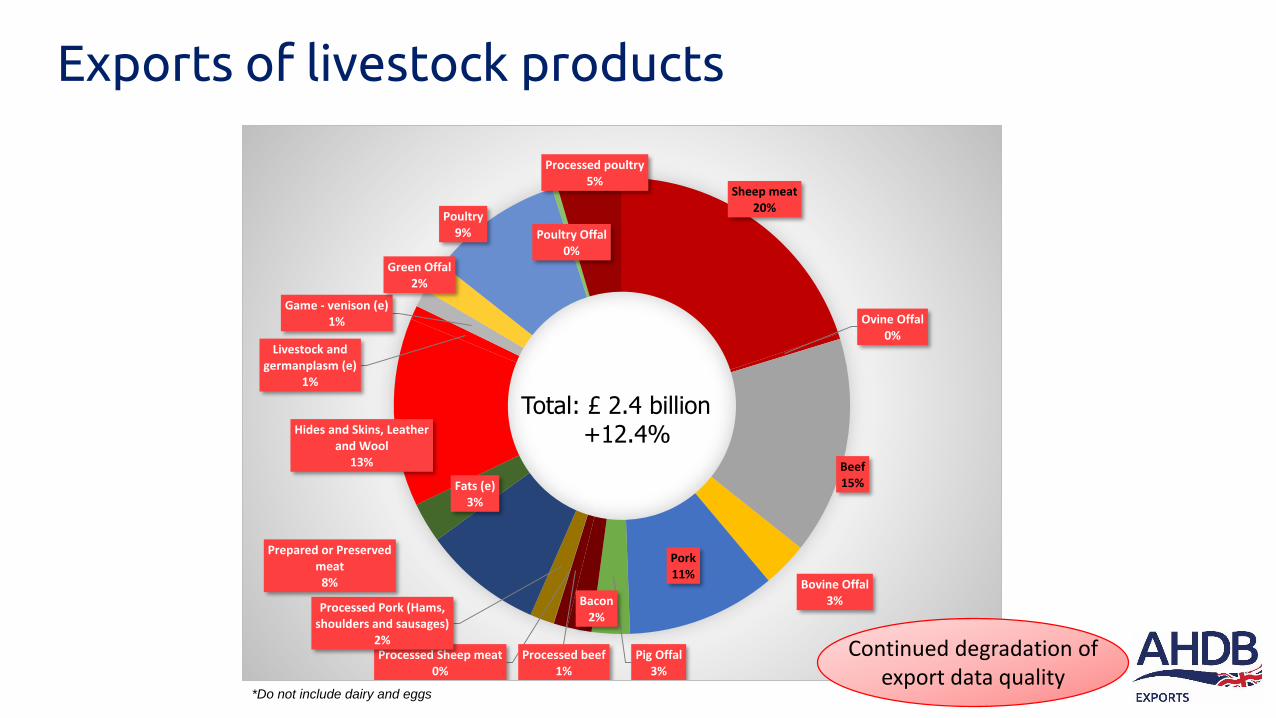

Sheep meat20%

Ovine Offal 0%

Beef15%

Bovine Offal 3%

Pork11%

Pig Offal 3%

Bacon2%

Processed beef1%

Processed Sheep meat0%

Processed Pork (Hams, shoulders and sausages)

2%

Prepared or Preserved meat

8%

Fats (e)3%

Hides and Skins, Leather and Wool

13%

Livestock and germanplasm (e)

1%

Game - venison (e)1%

Green Offal 2%

Poultry 9% Poultry Offal

0%

Processed poultry5%

*Do not include dairy and eggs

Total: £ 2.4 billion+12.4%

Continued degradation of export data quality

Exports of livestock products

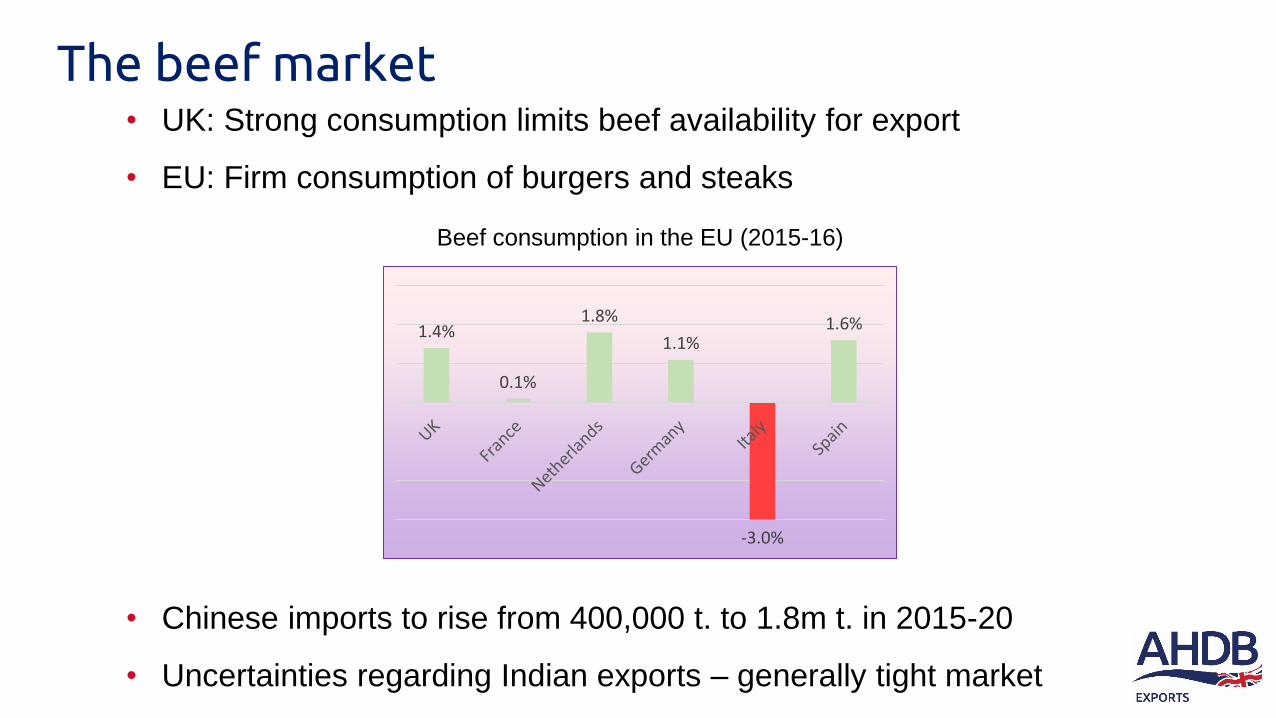

• UK: Strong consumption limits beef availability for export

• EU: Firm consumption of burgers and steaks

• Chinese imports to rise from 400,000 t. to 1.8m t. in 2015-20

• Uncertainties regarding Indian exports – generally tight market

The beef market

1.4%

0.1%

1.8%

1.1%

-3.0%

1.6%

Beef consumption in the EU (2015-16)

The beef market: great steaks and burgers

• Great development of premium steaks sales, matured on the

bone; beef is trendy

• Premium burgers are a major trend

• Organic beef

Ireland only exported 3% of its beef to Third Countries in 2016**2016, up from 2% in 2015

• We exported 110,000 tonnes of beef in 2016 (+10%) with a major

rise of frozen exports to 28,000 tonnes (+35%, +41% non-EU).

Very little carcase beef exports

• In the first months of 2017, beef exports to Third Countries are up

70% in value and 53% in volume against the same period of 2016.

They now represent 18% of the volume of beef exported from the

UK*

• Best performing markets: Hong Kong, Vietnam, Bulgaria, Spain,

French Polynesia

• Good prospects for 2017 but lack of product to export due to strong

domestic demand. Exports are down 12% in volume

UK beef exports

Hong Kong

Hong Kong

China

Hong Kong

Italy

Some interesting beef products

• Production is falling in New Zealand, Russia, USA, South America, South Africa but rising in Sudan, India… Altogether, supplies are scarce

• Chinese demand is recovering, leading to higher demand for sheep meat from Australia-NZ and higher imports from the UK

• Massive fall of New Zealand lamb exports to the EU. Higher exports to China and the USA

• Demand for organic lamb is rising in the EU.

• Sales potential in China, USA, KSA… as markets open

A great opportunity for the UK sheep meat

sector?

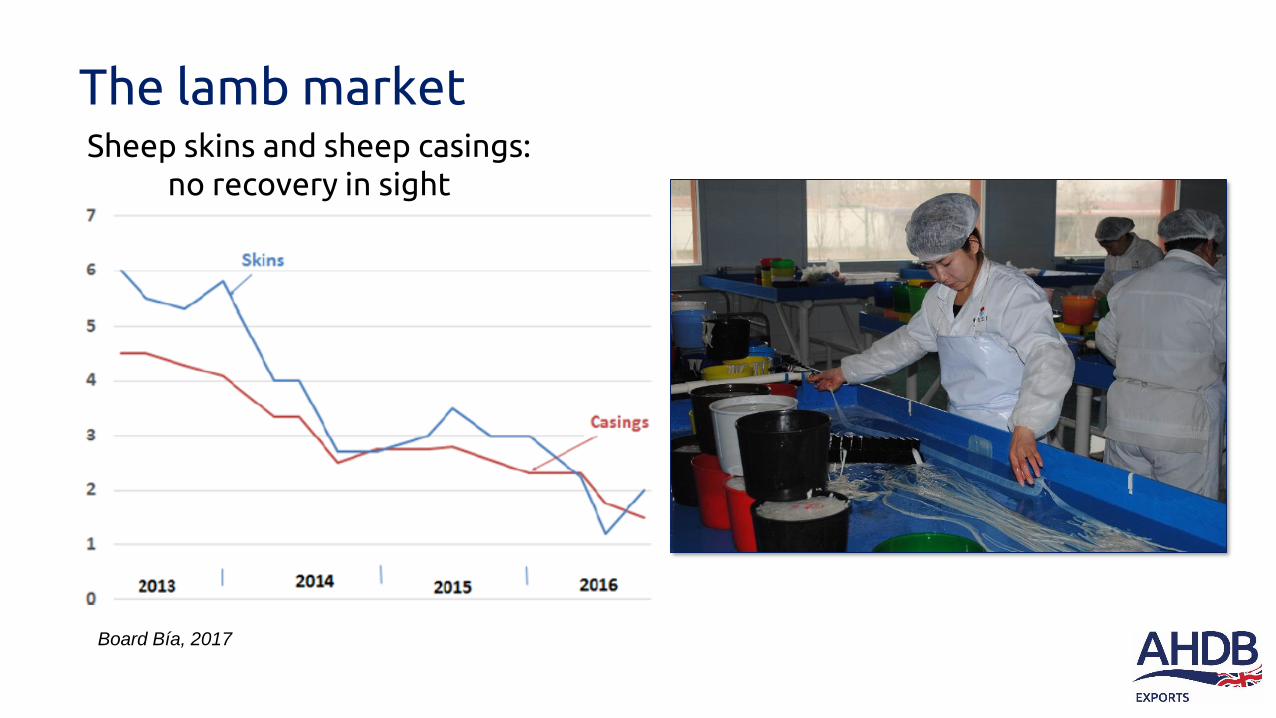

The lamb market

Sheep skins and sheep casings: no recovery in sight

Board Bía, 2017

The lamb market

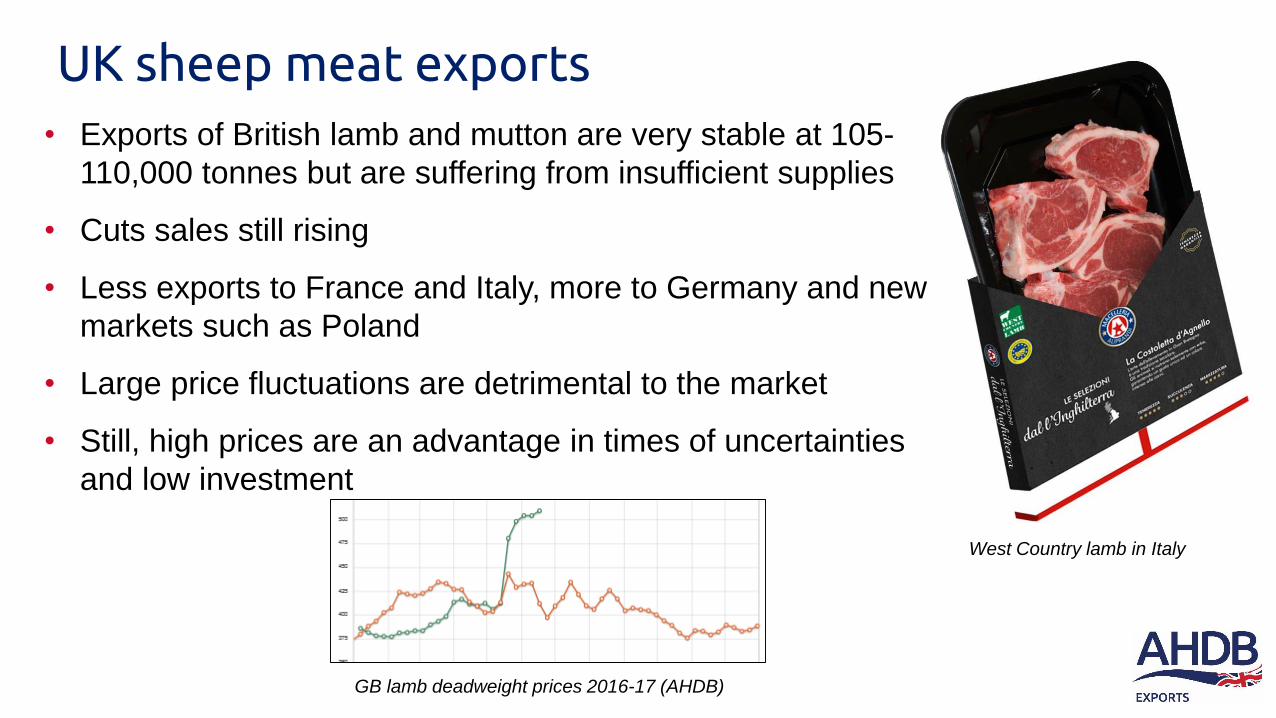

West Country lamb in Italy

GB lamb deadweight prices 2016-17 (AHDB)

UK sheep meat exports

• Exports of British lamb and mutton are very stable at 105-

110,000 tonnes but are suffering from insufficient supplies

• Cuts sales still rising

• Less exports to France and Italy, more to Germany and new

markets such as Poland

• Large price fluctuations are detrimental to the market

• Still, high prices are an advantage in times of uncertainties

and low investment

China

Ireland

Italy, Germany

China

Some interesting lamb products

Strong EU performance in Asia against stiff US and Brazilian competition

The international pork market

‘Pig World’ Qinglian Food, Shanghai

Positive outlook for Chinese imports

We exported £ 74m of pork and pig offal to China in 2016

Pork in China

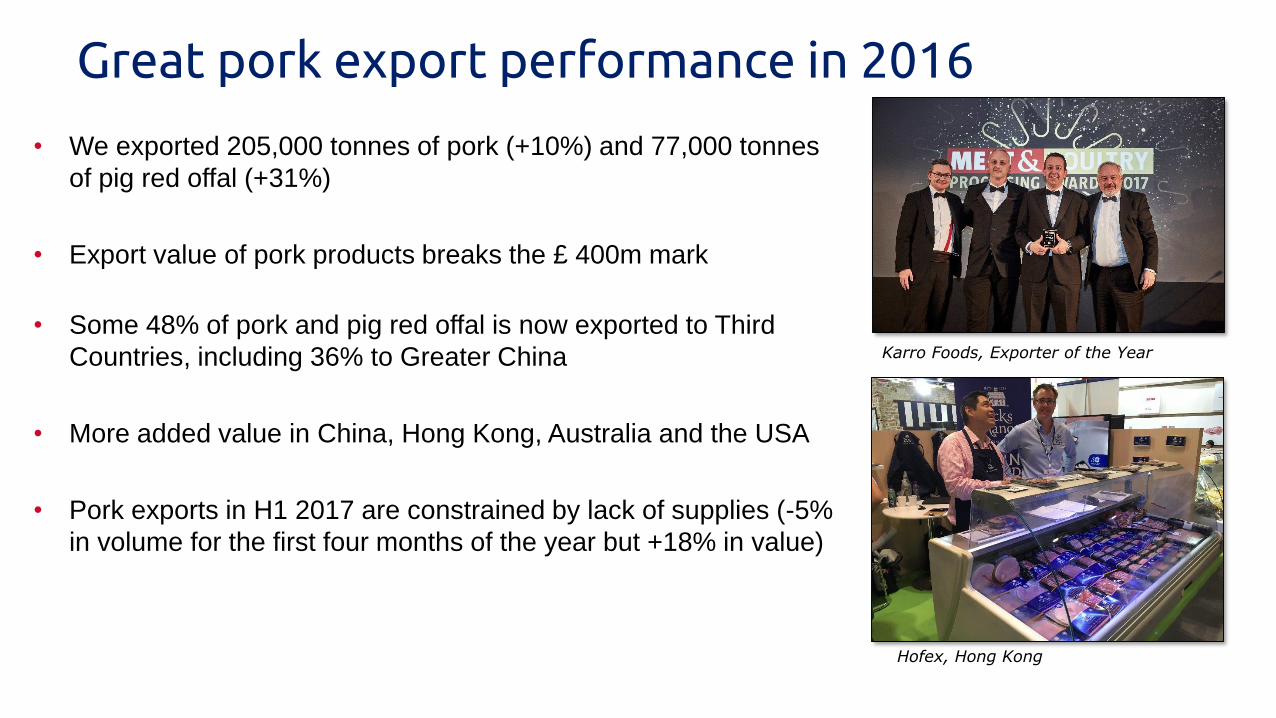

Karro Foods, Exporter of the Year

Hofex, Hong Kong

Great pork export performance in 2016

• We exported 205,000 tonnes of pork (+10%) and 77,000 tonnes

of pig red offal (+31%)

• Export value of pork products breaks the £ 400m mark

• Some 48% of pork and pig red offal is now exported to Third

Countries, including 36% to Greater China

• More added value in China, Hong Kong, Australia and the USA

• Pork exports in H1 2017 are constrained by lack of supplies (-5%

in volume for the first four months of the year but +18% in value)

Differentiated pork

Great pork export performance in 2016

• Stronger demand for organic, antibiotics-free, high welfare (…)

pork in USA, Australia, China

• Also high potential in Japan

• “Story” is particularly important in Asia. We benefits from a good

image

• Hong Kong is a particularly good market to test and sell premium

branded pork products

• At last we have made a good start with added value pork

products

Hong KongVietnam: frozen pork sausages

Germany: paprika-

marinated collar steak

Denmark

ItalyItaly

Spain

What’s new with pork?

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

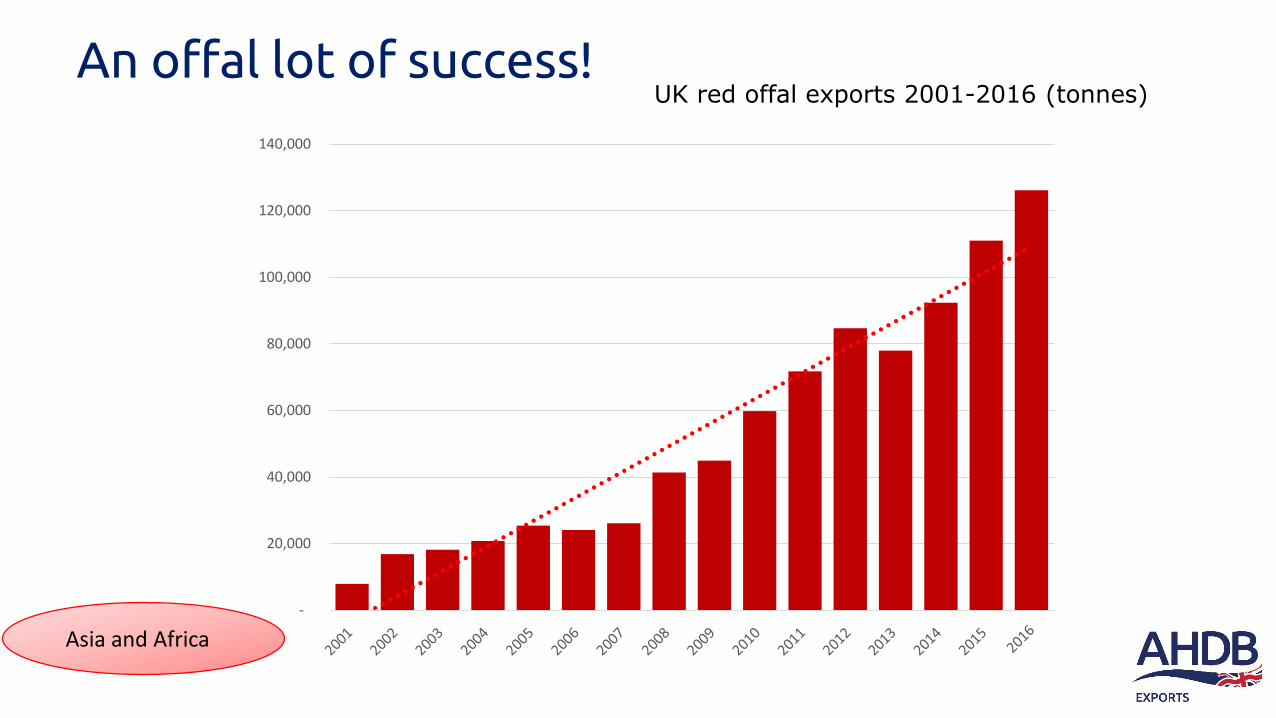

UK red offal exports 2001-2016 (tonnes)

Asia and Africa

An offal lot of success!

Germany -Switzerland

Dieter Müller at TIFA

• Main work involves development of lamb

sales in German retail: Edeka, Rewe, Real

• Halal lamb sales are booming

• Positive (but slow) developments in

Switzerland linked to the sustainability of

British lamb: no air miles

• Potential for major growth of lamb exports

Portugal

Lamb promotion in Auchan Cascais

• Good development of lamb sales 2016 to

date

• Working with Sonae, El Cortes Inglés,

Jerónimo Martins

• Growing supermarket beef sales

(picanhas)

• Also, beef for high-end food service

Spain

Salón de Gourmet, Madrid

• Following a tough time for Spanish

consumers in period 2008-14, sales of

premium meats are recovering

• Growing sales of premium English beef

in food service in Northern Spain

• British lamb is sold in food service and

retail

• Strong social media interaction on the

marketing of British lamb and beef

Italy

Metro lamb promotion

• Due to falling lamb and beef sales on the (tough)

Italian market, we are reviewing our Italian

operations

• Focus on West Country Lamb and Beef PGI

• Work with Auchan, Carrefour and other retailers

• Sales of premium English beef in food service

Greece - Cyprus

Chefs’ training in Cyprus

• Sales of manufacturing beef in Greece

remain at high levels

• We aim to deal directly with key Greek

food service accounts

• English beef sales to Cyprus are

progressing well

• Still, our main client is the premium

Alpha Mega supermarket in Cyprus

Inward mission of Dutch Chefs

• The Netherlands is now the fourth

largest market for British lamb

• Growth in the retail, high-end food

service and Halal segments

• Second largest market for UK beef –

forecast at 35,000 tonnes in 2017

• Large variety of boneless beef

products for retail and food service.

Fewer bone-in cows

The Netherlands

Poland - CEECs

Karol Okrasa in England

• Focus on the development of sales of English

lamb in economy with fast-rising incomes

• Product is present in retail and food service

with strong collaboration with some key

importers

• Co-operation with Poland’s top chef, Karol

Okrasa. Two major television cookery shows

have been dedicated to British lamb

• Next stop: the Czech Republic

• France: declining lamb sales while

maintaining market share. Some wins

with premium beef in food service

• Belgium: steady lamb sales and high

penetration. The Belgian market is the

third largest for UK lamb

• Scandinavia: slow development in

Denmark, Finland and Swededn

• Norway: little imports since 2014

• Slovenia: retail potential

SIRHA, Lyons

Other Europe

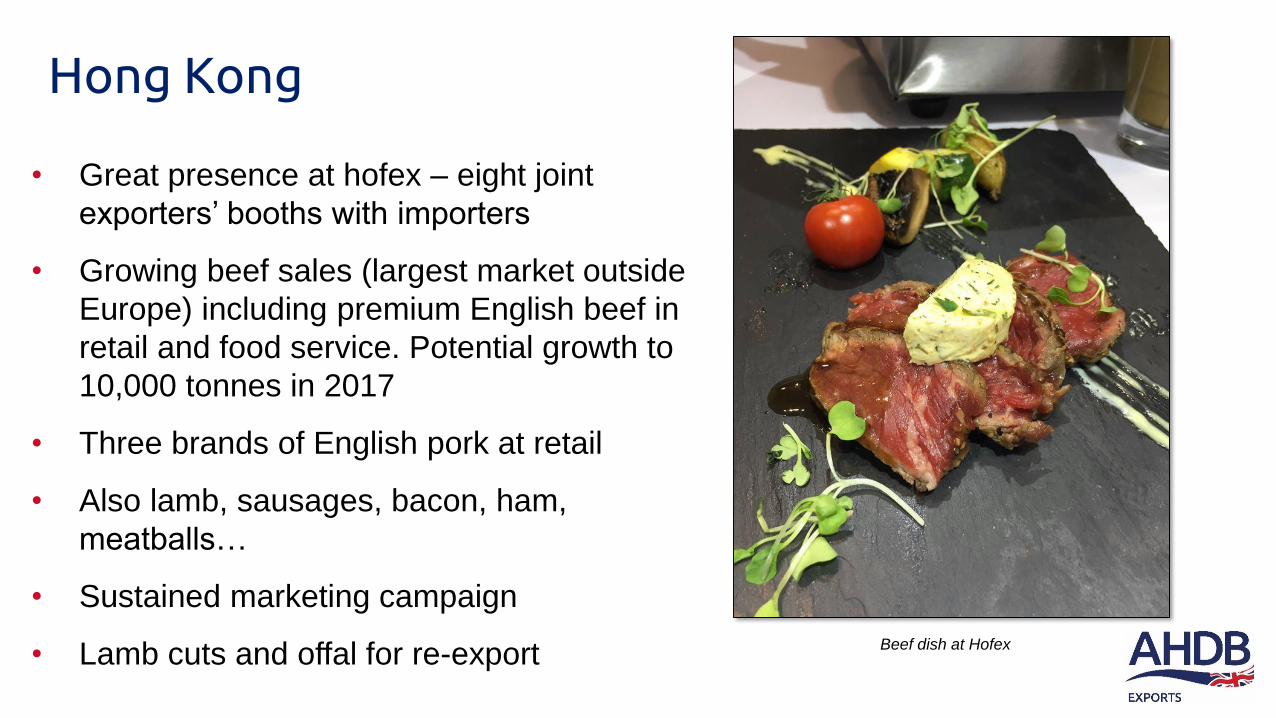

• Great presence at hofex – eight joint

exporters’ booths with importers

• Growing beef sales (largest market outside

Europe) including premium English beef in

retail and food service. Potential growth to

10,000 tonnes in 2017

• Three brands of English pork at retail

• Also lamb, sausages, bacon, ham,

meatballs…

• Sustained marketing campaign

• Lamb cuts and offal for re-export Beef dish at Hofex

Hong Kong

• Canada (CETA): beef potential, also

lamb development at retail

• Barbados: growing lamb sales at

retail, beef in food service

• Dominican Republic: pork

• Australia and New Zealand: added

value pork products

• Sub-Saharan Africa: offal and low

value cuts. Pork, beef livers to South

Africa

• USA: Differentiated pork

• South Korea, Japan, Philippines: pork

• GCC, Lebanon, Jordan: lamb

• Singapore: pork products, beef

NRA show, Chicago

Third Countries

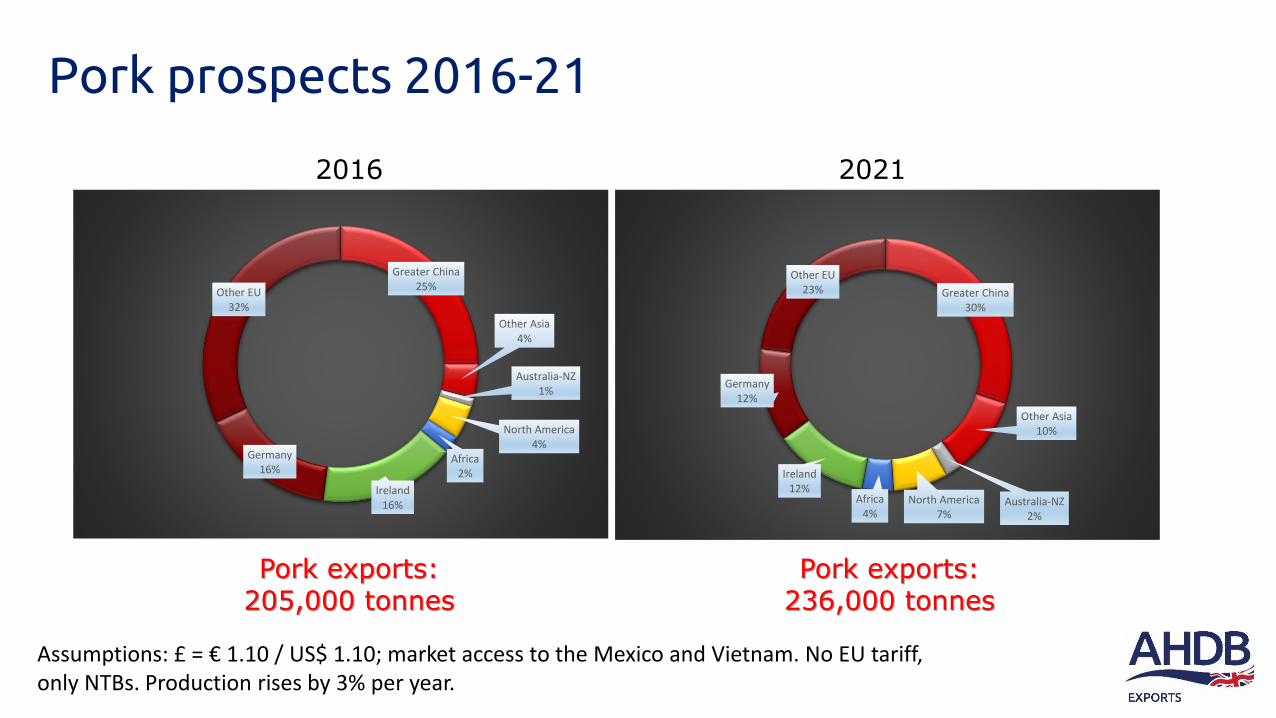

Pork prospects 2016-21

20212016

Pork exports: 205,000 tonnes

Pork exports: 236,000 tonnes

Assumptions: £ = € 1.10 / US$ 1.10; market access to the Mexico and Vietnam. No EU tariff, only NTBs. Production rises by 3% per year.

Greater China25%

Other Asia4%

Australia-NZ1%

North America4%

Africa2%

Ireland16%

Germany16%

Other EU32%

Greater China30%

Other Asia10%

Australia-NZ2%

North America7%

Africa4%

Ireland12%

Germany12%

Other EU23%

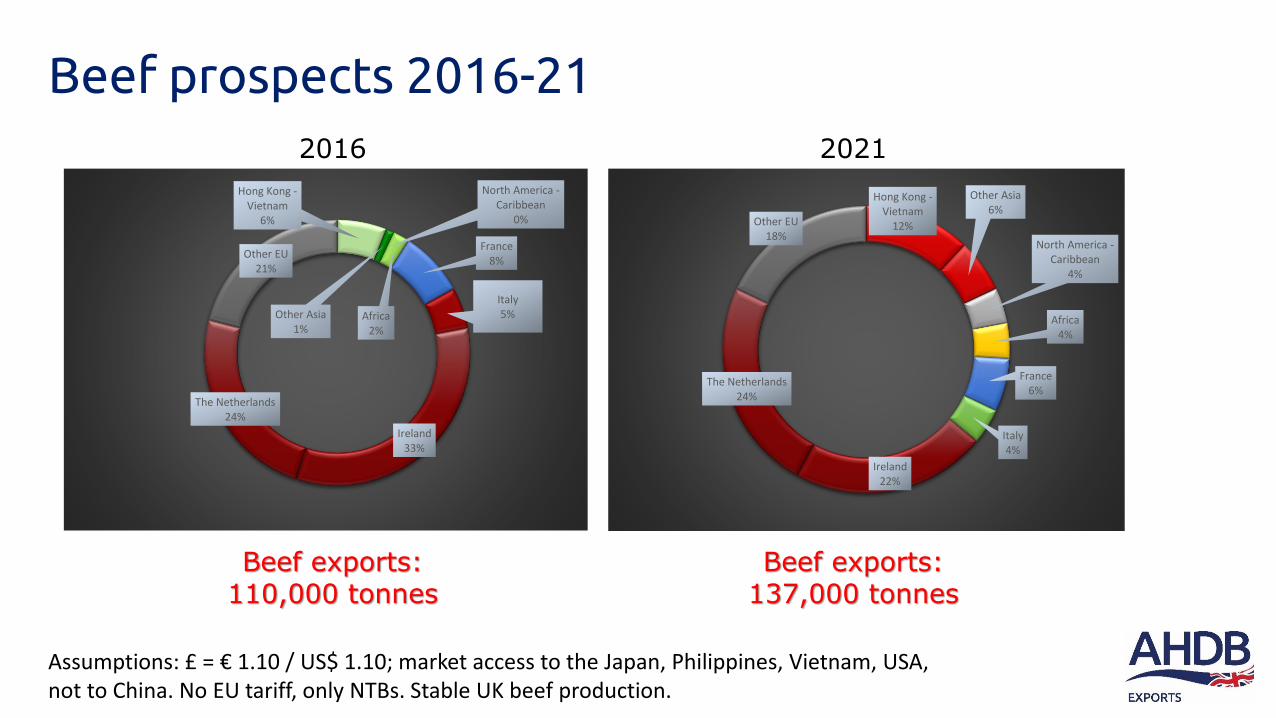

Hong Kong -Vietnam

6%

Other Asia1%

North America -Caribbean

0%

Africa2%

France8%

Italy5%

Ireland33%

The Netherlands24%

Other EU21%

Hong Kong -Vietnam

12%

Other Asia 6%

North America -Caribbean

4%

Africa4%

France6%

Italy4%

Ireland22%

The Netherlands24%

Other EU18%

20212016

Beef exports: 110,000 tonnes

Beef exports: 137,000 tonnes

Assumptions: £ = € 1.10 / US$ 1.10; market access to the Japan, Philippines, Vietnam, USA, not to China. No EU tariff, only NTBs. Stable UK beef production.

Beef prospects 2016-21

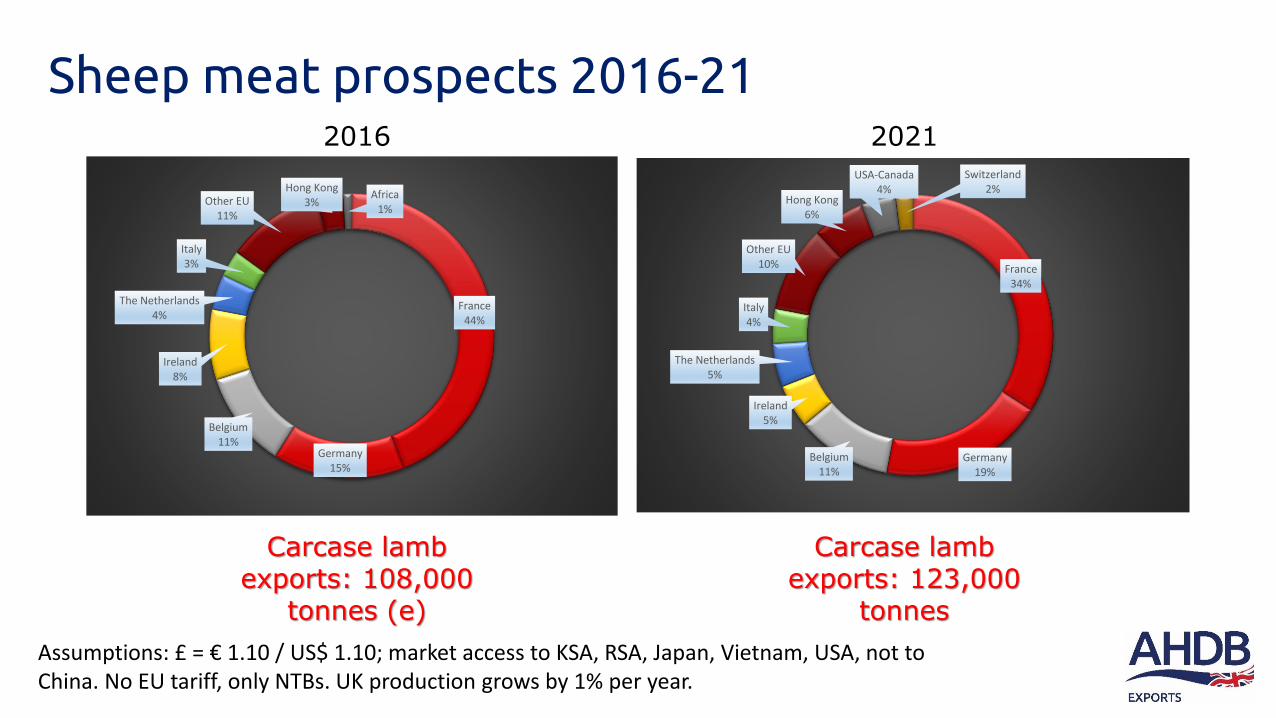

20212016

Carcase lamb exports: 108,000

tonnes (e)

Carcase lamb exports: 123,000

tonnes

Assumptions: £ = € 1.10 / US$ 1.10; market access to KSA, RSA, Japan, Vietnam, USA, not to China. No EU tariff, only NTBs. UK production grows by 1% per year.

France44%

Germany15%

Belgium11%

Ireland8%

The Netherlands4%

Italy3%

Other EU11%

Hong Kong3%

Africa1%

France34%

Germany19%

Belgium11%

Ireland5%

The Netherlands5%

Italy4%

Other EU10%

Hong Kong6%

USA-Canada4%

Switzerland2%

Sheep meat prospects 2016-21

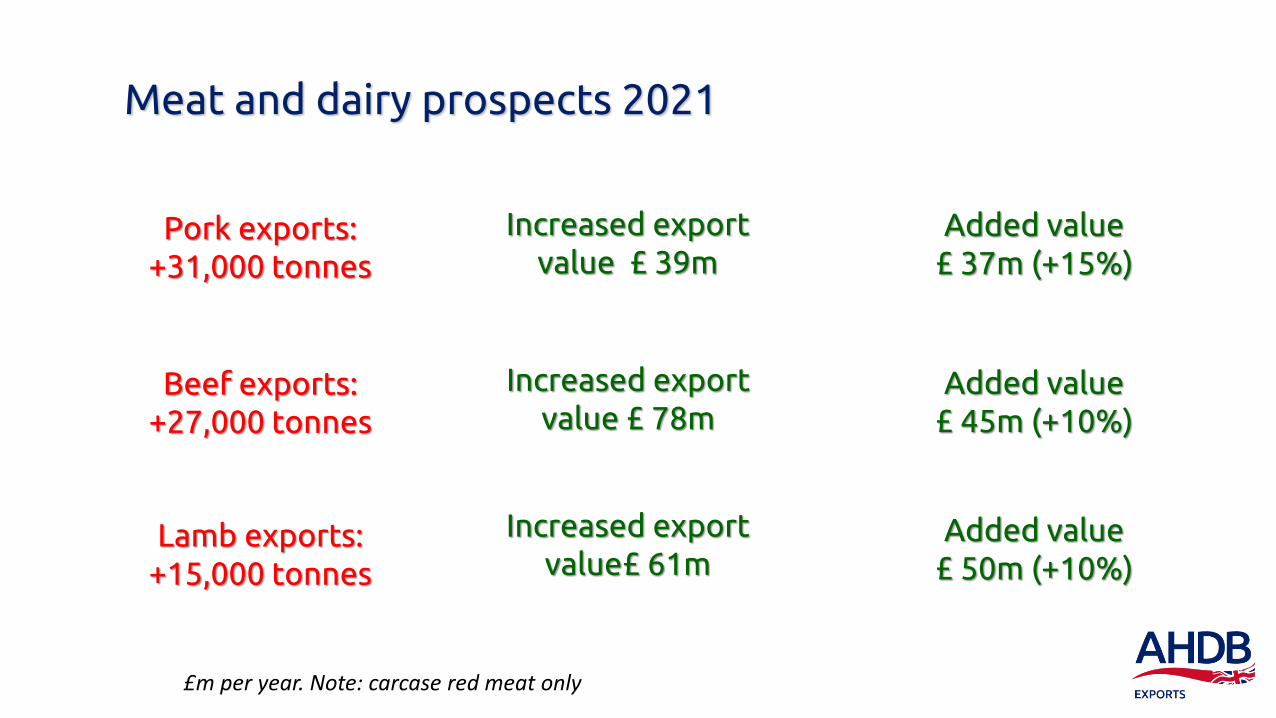

Meat and dairy prospects 2021

Pork exports: +31,000 tonnes

Beef exports: +27,000 tonnes

Lamb exports: +15,000 tonnes

Increased export value £ 39m

Increased export value £ 78m

Added value£ 45m (+10%)

Added value£ 37m (+15%)

Increased export value£ 61m

Added value£ 50m (+10%)

£m per year. Note: carcase red meat only

Restaurant & BarHong Kong, Sept

Africa missionSept

AnugaCologne, Oct

IndagraBucharest, Oct

FHCShanghai, Nov

Igeho

Basel, Nov.