brexit watch issue 1 - ey.comfile/ey-brexit... · the initial up-front sum the eu is expected to...

TRANSCRIPT

1

In this issue:

Negotiating

guidelines: EU takes

heed of Irish position

The hard realities of

a ‘soft’ border

Dublin Docks to

welcome more

financial services in

coming months

Issue 1, 5th May 2017

Brexit Watch

Fortnightly briefing on Brexit developments

DKM Commentary: Political developments in recent weeks have been predominantly positive from an Irish

perspective, demonstrating that the EU has taken on board issues of unique importance to

this country. References to Ireland in the negotiating priorities, Donald Tusk’s statement that

Ireland will be one of the first issues discussed and the ‘Kenny text’ are fruits of months of

diplomatic slog. That the Irish government will now shift its focus to economic issues is

welcome, and we await the Government’s forthcoming publication on how it plans to

mitigate the economic consequences of Brexit.

Some sources have claimed the UK general election will give more certainty and make a cliff-

edge Brexit less-likely. However, recent times have taught us to expect the unexpected and

initial engagements between the parties have not got off to an auspicious start. It is wise to

prepare for the worst case scenario – or at least assess what effect that scenario would have

on the daily operations of firms and Government. Impact assessments and contingency

planning are imperative: knowing what level of Brexit “hardness” a business can or cannot

manage, and in particular what kind of border is likely to emerge in the case of a no-deal

scenario, will help crystallise thinking.

Finally, news that financial services are due to announce relocations to Dublin in the coming

months is welcome, notwithstanding the added pressure it is likely to generate for housing

and other infrastructure. Indeed, the scope for such announcements is likely to add

momentum to infrastructure development initiatives in areas such as housing, office space

and public transport.

2

United Kingdom

Article 50: Notification of withdrawal

On 29 March Theresa May informed the European Council of the

UK’s decision to leave the European Union. The UK has two years

from this date to conclude a withdrawal agreement with the EU.

The agreement will set out how the UK will disentangle itself

from the Union, addressing matters such as border issues and

the rights of citizens and businesses.

The EU made clear that a separate agreement will address issues

such as the basis for future trade and cooperation, the outline of

which will be considered in the second phase of Article 50

negotiations.

Theresa May calls general election for 8 June

On 18 April, UK Prime Minister Theresa May called for an early

general election to be held on 8 June 2017. The motion for a

general election passed in the House of Commons by 522 to 13,

with Labour and the Liberal Democrats supporting the

government’s motion. The UK and EU have said that the general

election will not disrupt the Brexit negotiations timeline. YouGov

polls suggest the Conservatives will return a greater majority

than they currently hold, with the Conservatives estimated to

have a 16 point lead over Labour (as at 25-26 April ’17).

May and Juncker clash at dinner

Leaked reports published in a German newspaper of the dinner

between European Commission President Jean-Claude Juncker

and UK Prime Minister Theresa May ignited fears of Brexit talks

ending in failure. Jean-Claude Juncker was reported to have left

Downing Street stating that he was “ten times as sceptical as I

was before”. Mr Juncker reportedly informed the German

premier the next morning that Theresa May was deluding herself

and living “in another galaxy”.

Theresa May, however, dismissed the reports as “Brussels

gossip”, stressing the Commission’s official remarks that the

talks had been constructive.

The dinner took place on Wednesday 26 April, allowing Angela

Merkel to include in her Friday speech that some in Britain still

had “illusions” about obtaining concessions from the EU.

European Union

European Parliament adopts resolution on

negotiations with the United Kingdom

On 5 April, the European Parliament adopted a resolution on its

red lines for negotiations. The resolution, drafted by the

European People’s Party (EPP), is not binding but the European

Parliament must give its consent to both the withdrawal

agreement and any future framework agreement.

EU Brexit guidelines

The final European Council (Art. 50) guidelines were adopted on

29 April, less than fifteen minutes into the special meeting of the

EU27. German Chancellor Angela Merkel later commented that

she had never seen such unity of purpose at a Council meeting.

Prior to the event, Council President Donald Tusk had affirmed

that the UK government must settle the question of EU citizens,

the UK’s financial obligation to the EU and the question of a

border on the island of Ireland prior to any discussion on the EU-

UK future trade relationship.

The guidelines make reference to the “unique circumstances on

the island of Ireland” and called for “flexible and imaginative

solutions” to avoid a hard border, while respecting the integrity

of the EU’s legal order. Moreover, the acceptance of the ‘Kenny

text’, an EU declaration that allows for the reintegration of

Northern Ireland into the EU in the event of Irish unification, has

been hailed an Irish diplomatic success.

Brexit ‘bill’ increases

The initial up-front sum the EU is expected to demand from

Britain in financial liabilities has increased from €60bn to

€100bn, principally due to stricter demands from France and

Germany. According to an analysis conducted by the Financial

Times, the inclusion of post-Brexit farm payments, EU

administration fees in 2019 and 2020 and the refusal to grant

the UK a share of EU assets, will significantly increase the earlier

€60bn figure suggested by Jean-Claude Juncker. Over the long-

term, however, the net figure would reduce to approximately

€65bn as the UK received its share of EU spending and EU loan

repayments.

Ireland

Following the confirmation of the EU’s negotiating position on 29

April, the Irish Government published their approach to Brexit

negotiations, in which they detail the findings and outcomes of

the preparatory work on Brexit. In its statement on 2 May, the

Government announced that it would increase its focus on the

economic implications of Brexit, which would include focusing on

domestic policy measures to boost competitiveness and protect

the Irish economy from the potential negative impacts of Brexit.

The Government stated that it will prepare a further paper on

this issue.

Brexit Essentials The UK looks set to leave the single market and the customs

union when it leaves the EU in March 2019. This section explains

these two key elements of the EU acquis.

The Single Market

The Single Market, (also called the internal market) enables

workers, goods, capital and services to move freely within the

EU. To establish the Single Market, the EU Member States

eradicated numerous technical, legal and bureaucratic barriers

to free trade and free movement. The result is an area within

which businesses have access to all 500 million EU consumers

and where EU citizens are permitted to work, study, establish a

company and retire.

Economic Insight

Political Developments

3

Operating costs of 44-

tonne HGV [Freight

Transport Association]

£1 per minute Higher estimate of

increase in trade costs due

to border crossing [OECD]

24% No. of HGV movements

across the Irish border

per year [FTA]

2.12m

The internal market is central to the EU. Indeed, establishing a

common market in people, goods, services and capital was the

objective of the Treaty establishing the European Economic

Community (Treaty of Rome) in 1957. The EU has consistently

claimed that the ‘four freedoms’ (people, goods, capital and

services) are indivisible – a State may not ‘cherry pick’ the

freedoms it desires.

If, as seems likely, the UK will not accept the free movement of

workers post-Brexit, the UK cannot be part of the internal

market thus defined. This will particularly affect the UK financial

services sector, as they will lose the “passporting rights” that

allow financial services companies to do business in other EU

Member States based on their home State authorisation. It will

also affect the rights of EU citizens residing in the UK and of UK

citizens residing in the EU.

The Customs Union

The Customs Union is a single trading area, where all goods

circulate freely, without duty or customs control. It exists to

facilitate the removal of barriers to trade between countries as

per single market principles. The Customs Union involves a

uniform system of customs duties on imports from outside the

EU in the form of the Common Customs Tariff (CCT).

The Common Commercial Policy (CCP) is seen as a counterpart

to the CCT. The CCP requires that changes to tariff rates, the

conclusion of tariff and trade agreements and the commercial

aspects of intellectual property and foreign direct investment

must all be decided at an EU level based on uniform principles.

Notably, it prevents any EU Member State from conducting a

trade agreement with a third country.

‘Red, white and blue’ Brexit

Leaving both the Single Market and the EU Customs Union is not

an inevitable consequence of being outside the EU. For example,

the three EFTA EEA States (Iceland, Lichtenstein and Norway) are

part of the EU Single Market but not the Customs Union. And the

EU shares a customs union with Turkey, but Turkey is not part of

the Single Market.

However, the UK has ruled out remaining part of the EU’s Single

Market and the EU Customs Union by refusing to accept the

rights of EU workers to reside in the UK and by stating its

intention to not be bound by the Common Customs Tariff or

Common Commercial Policy.

Border Focus Following developments concerning the possible NI-ROI border

in the wake of Brexit

Hard realities of a ‘soft’ border

If the UK leaves the EU Customs Union in March 2019, there will

be a customs border on the island of Ireland. Advances in

technology could make the implementation of such a customs

border relatively ‘soft’ as borders go. However, even EU-

sanctioned “flexible and imaginative solutions” are not likely to

eliminate the need for customs posts, the possibility of delays or

the disadvantages of increased documentation.

Even at the Swedish-Norwegian border, often cited for its

efficient use of technology and as a potential model for Ireland

to follow, officials regularly conduct physical border checks on

freight carriers that can lead to hours of delay at busy times.

Moreover, this border is between an EU and an EEA EFTA State,

rather than an EU Member State and a third country as the NI-

ROI border would become.

As IBEC notes in its Economic Outlook, border controls and/ or

tariff barriers between Ireland and the UK would

“disproportionately impact” Irish businesses due to Irish reliance

on the UK market for raw materials, the high trade volume

between the UK and Ireland, UK-Irish trade in low margin goods

and closely intertwined supply chains.

Smuggler’s paradise

Much depends on how a border is implemented. An OECD Trade

Policy Paper estimates that border crossings can increase

transaction costs by between 2% and 24% of the value of the

traded goods. The Irish border would be difficult to control, not

only for politically sensitive reasons but also due to it passing

through villages, towns and private land. Were the cost of

crossing the Irish border to lie at the higher end of the OECD

range, there would be a large incentive to smuggle. As noted in a

Politico article on the topic of potential post-Brexit smuggling,

“the bigger the differences between the tax and regulatory

regimes on each side of the post-Brexit border, the greater the

opportunities for illicit profit.”

Potential solutions

Dedicated routes for customs, fast-track lanes for trusted traders

and number plate recognition technologies could mitigate many

of the potential negative effects of a border by keeping extra

costs to a minimum. Uncertainty for those involved in cross-

border trade (both on the island and with Great Britain) could

also be reduced with more information on how the authorities

intend to handle the increase in customs traffic and the customs

border itself. Contingency customs plans for the scenario where

the UK leaves with no deal would also facilitate internal

estimates of the worst case scenario.

4

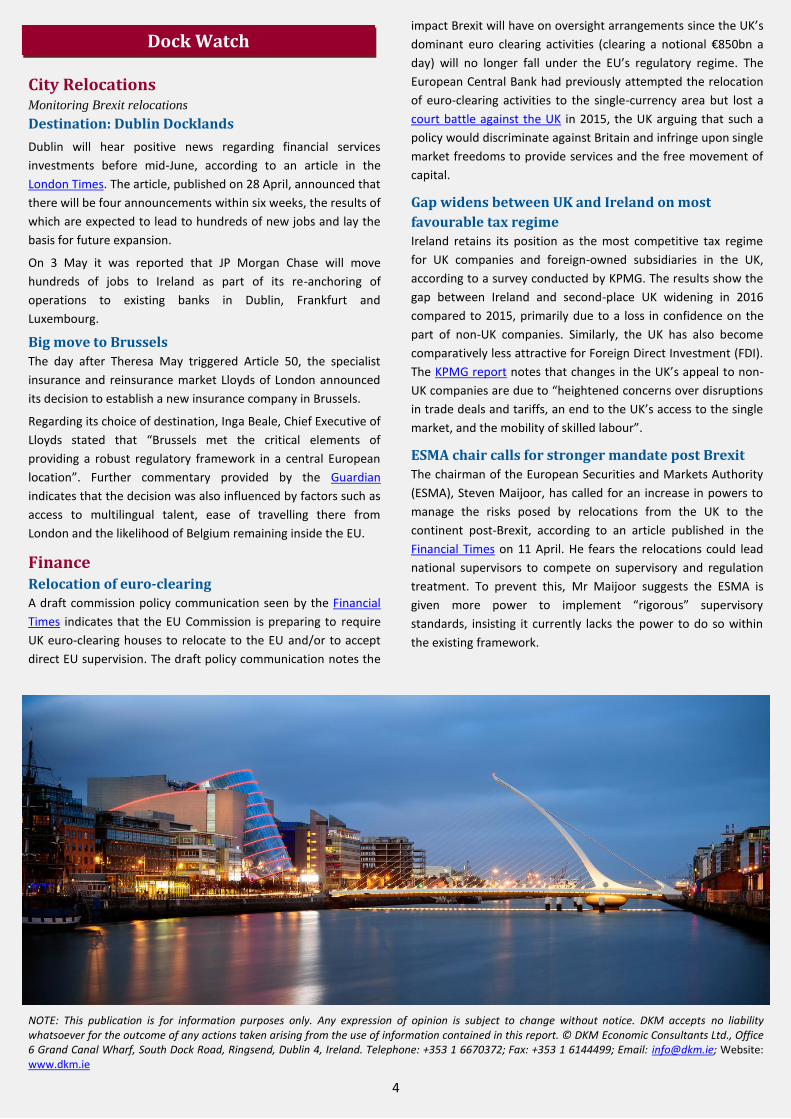

City Relocations Monitoring Brexit relocations

Destination: Dublin Docklands

Dublin will hear positive news regarding financial services

investments before mid-June, according to an article in the

London Times. The article, published on 28 April, announced that

there will be four announcements within six weeks, the results of

which are expected to lead to hundreds of new jobs and lay the

basis for future expansion.

On 3 May it was reported that JP Morgan Chase will move

hundreds of jobs to Ireland as part of its re-anchoring of

operations to existing banks in Dublin, Frankfurt and

Luxembourg.

Big move to Brussels

The day after Theresa May triggered Article 50, the specialist

insurance and reinsurance market Lloyds of London announced

its decision to establish a new insurance company in Brussels.

Regarding its choice of destination, Inga Beale, Chief Executive of

Lloyds stated that “Brussels met the critical elements of

providing a robust regulatory framework in a central European

location”. Further commentary provided by the Guardian

indicates that the decision was also influenced by factors such as

access to multilingual talent, ease of travelling there from

London and the likelihood of Belgium remaining inside the EU.

Finance Relocation of euro-clearing A draft commission policy communication seen by the Financial

Times indicates that the EU Commission is preparing to require

UK euro-clearing houses to relocate to the EU and/or to accept

direct EU supervision. The draft policy communication notes the

impact Brexit will have on oversight arrangements since the UK’s

dominant euro clearing activities (clearing a notional €850bn a

day) will no longer fall under the EU’s regulatory regime. The

European Central Bank had previously attempted the relocation

of euro-clearing activities to the single-currency area but lost a

court battle against the UK in 2015, the UK arguing that such a

policy would discriminate against Britain and infringe upon single

market freedoms to provide services and the free movement of

capital.

Gap widens between UK and Ireland on most

favourable tax regime Ireland retains its position as the most competitive tax regime

for UK companies and foreign-owned subsidiaries in the UK,

according to a survey conducted by KPMG. The results show the

gap between Ireland and second-place UK widening in 2016

compared to 2015, primarily due to a loss in confidence on the

part of non-UK companies. Similarly, the UK has also become

comparatively less attractive for Foreign Direct Investment (FDI).

The KPMG report notes that changes in the UK’s appeal to non-

UK companies are due to “heightened concerns over disruptions

in trade deals and tariffs, an end to the UK’s access to the single

market, and the mobility of skilled labour”.

ESMA chair calls for stronger mandate post Brexit

The chairman of the European Securities and Markets Authority

(ESMA), Steven Maijoor, has called for an increase in powers to

manage the risks posed by relocations from the UK to the

continent post-Brexit, according to an article published in the

Financial Times on 11 April. He fears the relocations could lead

national supervisors to compete on supervisory and regulation

treatment. To prevent this, Mr Maijoor suggests the ESMA is

given more power to implement “rigorous” supervisory

standards, insisting it currently lacks the power to do so within

the existing framework.

NOTE: This publication is for information purposes only. Any expression of opinion is subject to change without notice. DKM accepts no liability whatsoever for the outcome of any actions taken arising from the use of information contained in this report. © DKM Economic Consultants Ltd., Office 6 Grand Canal Wharf, South Dock Road, Ringsend, Dublin 4, Ireland. Telephone: +353 1 6670372; Fax: +353 1 6144499; Email: [email protected]; Website: www.dkm.ie

Dock Watch