bpm and insurance industry session 4 - ibm · bpm disciplines are just emerging, although many...

TRANSCRIPT

BPM and Insurance Industry

Srikanth VenkatesanPractice leader - Insurance

Agenda

BPM - In PrincipleBPM - In PracticeWhat effective BPM can do to your businessBPM and Insurance Industry in matured MarketsBPM adoption in Indian Insurance contextBPM adoption - Key questionsBPM adoption - Critical success factorsInsurance operations of the futureBPM Solutions and IBM

BPM

Automate

Integrate

Optimize

BPM - In Principle

BPM disciplines make process explicit (visible and independent of its implementation) using models. Models are increasingly executable, not just documentation.

BPM suites are the most complete set of integrated composition technologies for managing all aspects of process — people, machines, information, business rules and policies.

BPM disciplines are just emerging, although many BPM-enabling technologies are quite mature.

BPM is a technology-enabled set of disciplines to better address today's more-unpredictable market dynamics by applying explicit process management approaches. And if a process is transparent, effective and agile, it is likely to be perceived as innovative by internal employees, and external customers and partners

“Business Process Management, a software segment for end-to-end management of business processes,from modeling and design to deployment and execution,

to monitoring and optimization of business processes involving both people (workflow) and systems (automation). Some use BPM to mean Business Performance Management which related to business intelligence and BAM .”

Gartner Research

BPM - In Practice

Applied as a discipline combining software and business consulting expertise to accelerate process improvement and facilitate business innovation

Used as an approach that involves managing the entire lifecycle of a process

Applied to Govern an organization’s cross-functional, customer-focused, end-to-end core business processes

Used as a principle of continuous improvement, perpetually increasing value generation and sustaining market competitiveness (or dominance) of the organization.

Key Challenges Facing Insurer Leadership Worldwide

How do I comply with government regulationsand Industry standards (Solvency II, ACORD,

GDV, ...)

How do I comply with government regulationsand Industry standards (Solvency II, ACORD,

GDV, ...)

How do I continue to reduce costs and

consolidate operations?

How do improve innovation and agility while leveraging

past IT investments?

How do I respond quicker to my customers, agents,

and partners?

CxO Challenges

BPM solves common business challenges . . .

BPM governs organizational and operational activities

Models Process Knowledge Metrics

Expertise and AssetsPolicies Business Logic Methodology

Integration Modeling Events Monitoring

SoftwareForms Active Content Rules Engine Workflow

BPM includes

Empowers business users Identifies and Removes Bottlenecks

Provides Clear Visibility intoBusiness Processes

Streamlines complex integration across multiple processes

Enables Process change

Simulates / predicts outcomes

Business Process Management delivers immediate benefits and represents a longer-term business discipline

Empower business users

Provide actionable insights

Improve business agility

Reduce costs

Enhance collaboration

End-to-end process visibility

Boost worker productivity

Improve customer service

What Can BPM Do for Me?Companies are Using BPM to Provide a Variety of Benefits

BPM Aligns Business and IT to your Business Processes and your Changing Business Needs

BPM tools Empowers You To Embrace Change and Continuously Optimize Your Business

Model and Simulate

Monitor, Predict and Act

Rapidly Deploy and Change

End-to-End Processes

Continuously OptimizeSales FinanceOperations Partners

Businesses today must adapt to faster and more transformative change

Power Shift to Consumers

New Regulatory Requirements

Industry Consolidation

and M&A

Macro-Economic Changes

Global Competitors

Insurance Industry and BPM - Key Findings• BPM Use Within Insurance Is Limited – Used primarily in non core areas,

Insurers slow to adopt

• Not Integrated with core business systems – 10 out of 16 companies used BPM for stand alone functions

• Few BPM vendors had Industry experience – Basic BPM frameworks don’t do well in helping organizations realize business benefits

• Lack of clarity on usage of BPM – Lack of business case behind investments in BPM

• Perception of High cost - No view on TCO for a definitive period

Forrester research 2006

Insurance Industry and BPM - Key Findings

Lack of experience in using BPM tools – as ETL ?? As front end ?? As transaction systems ??

Business process complexity – Ever changing needs and lack of right combination of business and BPM skills lead to discontinuation of usage

Measurement of benefits – Not being able to calculate tangible benefits as the benefits span across functions / silos

Forrester research 2006

Market size of BPM solutions will grow at a rate of 21% CAGR and will be expected to be approximately at 3 billion USD

BPM adoption in India - so far

♦ Restricted to specific functionalities

♦ Restricted to Document centric process management

♦ Viewed as Imaging and workflow management only coupled with somecontent management

♦ Not Integrated with enterprise architecture

BPM adoption - Key Questions

What is the vendor’s installed base in terms of number of insurance companies and in the current geography ?

How many internal resources are dedicated to insurance?

How differentiated is the pre - built insurance-specific software that is included with the product?

How easily does this integrate with core Insurance solutions ?

How sophisticated is the product’s set of tools for monitoring and managing processes including change in rules and modifications in the processes?

Total cost of ownership

Key roles and Best Practices in BPM ImplementationRole Best Practice

Business process expert Focus on process first, then technology.Retain process intellectual property.Implement cross-departmental processes.Use collaboration for targeted business processes.Make the processes transparent

Enterprise architect View metadata broadly.Use process standards.Provide foundation for reusable tasks

IT operations professional Be sure underlying infrastructure is ready.Help select the right BPMS tool for your businessusers.

Application developmentprofessional

Help insulate process experts from underlyingtechnology.Support goals of the enterprise architect

BPM vendor Identify low-hanging fruit for initial applications.Standardize templates with ACORD businessprocess and data models.Provide business cases.Promulgate best practices

Critical Success factors

♦ Emphasis on the business process and overall objectives

♦ View process knowledge as a strategic asset

♦ Select cross system / functional processes for Implementation

♦ Use collaboration tools in the right context

♦ Measure results and improvise

Mailroom Process ApplicationPrep Route Output and StorageIndex

Workflow Enabled Operations (Content Centric)Workflow Enabled Operations (Content Centric)

Operations of the Future (Integration Centric)Operations of the Future (Integration Centric)

Traditional Paper Operations (Human Centric)Traditional Paper Operations (Human Centric) Data

Data

Data

Processes Services

TIFF XML

ProcessServer / Fabric

InputManagement

Automated

50 – 60%50 – 60%

15 - 30%15 - 30%

5 - 10%5 - 10%

Filenet

Operational efficiency limited by Knowledge worker being the “Integration” layer between Documents and Applications

Document recognition, work task automation maps, and exposed SOA Services enable “Lights Out” Automation and intelligent work task assignments

Insurance operation of the Future

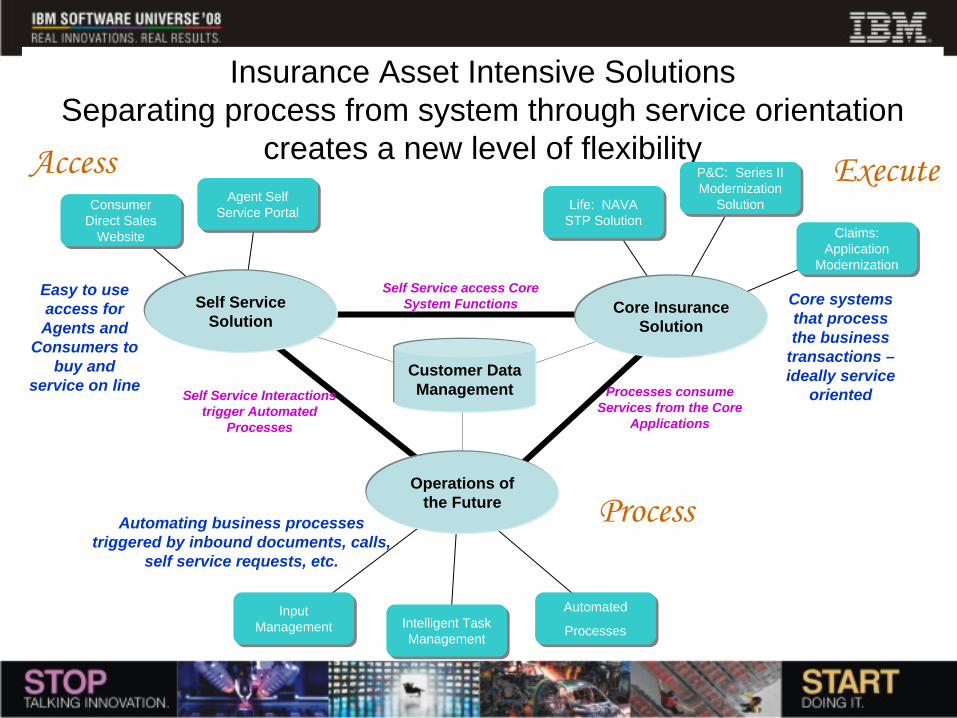

Insurance Asset Intensive Solutions Separating process from system through service orientation

creates a new level of flexibility

Self Service Solution

Consumer Direct Sales

Website

Consumer Direct Sales

Website

Customer Data Management

Operations of the Future

Core Insurance Solution

Processes consume Services from the Core

Applications

Self Service Interactions trigger Automated

Processes

Self Service access Core System Functions

Automating business processes triggered by inbound documents, calls,

self service requests, etc.

Core systems that process the business

transactions –ideally service

oriented

Easy to use access for Agents and

Consumers to buy and

service on line

Agent Self Service Portal

Agent Self Service Portal Life: NAVA

STP SolutionLife: NAVA

STP Solution

P&C: Series II Modernization

Solution

P&C: Series II Modernization

Solution

Claims: Application

Modernization

Claims: Application

Modernization

Input Management

Input Management Intelligent Task

ManagementIntelligent Task Management

Automated

Processes

Automated

Processes

Access

Process

Execute

Insurance Operations of the Future helps address new challengesInsurance Companies are facing a challenging time where Expenses are growing

while Revenues are shrinking

• Since the mid-50’s, the Insurance industry failed to turn an underwriting profit – profit earned by taking in more premium than it pays out in losses

• This changed in 2001 when the Industry began recording it’s most profitable years since the Depression

• However, the industry started trending backwards in 2007 when, expense growth outpaced premium growth as revenues started a decline due to softening rates

Industry trends and expense challengesExpense growth outpaced premium growth by 3.7%

SAN FRANCISCO Jan. 31, 2008

• Standard & Poor's Ratings Services has published a report that says U.S. property/casualty insurer expense ratios are expected to rise in the coming years. The report, titled, "How High Can U.S. Property/Casualty Insurer Expense Ratios Go?," notes that the average expense ratio of its rated P/C insurers is expected (once all data is in) to have risen in 2007 compared with 2006.

• "Insurers benefited from relatively low claims activity and robust earnings in 2006 and 2007, but are now finding themselves increasingly challenged by the double-edged sword of increasing expenses and the cyclical decline in premium growth," noted Standard & Poor's credit analyst Michael Gross.

• These pressures do not bode well for 2007 or 2008 expense ratios. For the five-year hardening premium rate environment of 2002-2006, expense growth among Standard & Poor's rated insurers outpaced premium growth by 3.7 percentage points.

• P/C insurers seeking to rein in expenses will face increasing challenges in 2008. Expense ratios at many insurers have room for improvement. "However, given the soft market's continuing headwind, we believe expense ratios are likely to increase before they start to decline," added Mr. Gross.

Changing demands from customers, regulators and agentsCarriers must invest in order to respond

• Consumers:– Expect rapid turn around via

multiple channels– Demand more innovation in

products and services

• Agents:– Will trade commission for

ease of doing business

• Regulators:– Regulation is increasing in

scope and complexity

• Employees– Skilled resources are

becoming scarce and expensive

• Carriers are still investing in new systems, channels, processes, and organizations to respond to a changed demographic

• Carriers are investing to either create – or respond to – new innovations…something new to this industry

• Carriers are having to compete for the agents customers on more than just price and commission – and also need to be easier to do business with as well

• National and Local regulations are on the rise – accounting for

ti bl t f

Success StoriesInsurance Carriers strive to better align their business initiatives with existing resources and

technology to achieve a higher level of operational efficiency

… while preparing for future growth and business models at the same time.

Source: Company Annual report, 2005

“The Zurich Way”: Focus on core markets Focus on core processes Increase operational efficiency Standardization of methodologies and processes

Source: Company Annual report, 2005

“The Zurich Way”: Focus on core markets Focus on core processes Increase operational efficiency Standardization of methodologies and processes

Further industry concentration: Individual Capital Adequacy Growing investment in technology and service

Critical success factors in the UK market: Flexibility in DistributionEfficiency in Capital ManagementBrand AwarenessDelivery Capabilities

Source: Company Annual report

Further industry concentration: Individual Capital Adequacy Growing investment in technology and service

Critical success factors in the UK market: Flexibility in DistributionEfficiency in Capital ManagementBrand AwarenessDelivery Capabilities

Source: Company Annual report

“Accelerating the pace of change” as the programme for 2006-2008: Operational improvement Growth & innovation, Capital optimization, Enhanced governance

Source: Company Annual report 2005

“Accelerating the pace of change” as the programme for 2006-2008: Operational improvement Growth & innovation, Capital optimization, Enhanced governance

Source: Company Annual report 2005

“3+One Strategy”: Protect and strengthen capital baseBoost operating profitReduce complexityIncrease competitive strength through customer focus and sustainability

Source: Company Annual report 2005

“3+One Strategy”: Protect and strengthen capital baseBoost operating profitReduce complexityIncrease competitive strength through customer focus and sustainability

Source: Company Annual report 2005

Company objectives: Provide more cost transparency to clients Reduce expenses and increase return on equityReduce claim processing timeProvide high quality customer service based on accessibility and professionalism in customer careWith one group-one system philosophy, use Danish Insurance system as a model for further development of its international activities

Source: Company Annual report 2005

Company objectives: Provide more cost transparency to clients Reduce expenses and increase return on equityReduce claim processing timeProvide high quality customer service based on accessibility and professionalism in customer careWith one group-one system philosophy, use Danish Insurance system as a model for further development of its international activities

Source: Company Annual report 2005

Operations of the Future Business ObjectivesIn moving to the Service Oriented Enterprise, Operations of the Future addresses 4

strategic imperatives while responding to changing market expectations

ReduceCycle Time

• Customers begin to expect instantaneous response to requests through policy life cycle

• Agents place business with carriers that deliver accurate results quicker – at times demonstrating a willingness to take lower commission

Mega-trend indicates processing efficiency becomes a competitive differentiator equal to and possibly more than commission to respond to changing demographic

OptimizeResources

• Skilled resources are graying and becoming harder to find – especially in the claims, underwriting, and agent skill classes

• At the same time, the market is demanding more complex and diversified programs to differentiate through product innovation

Mega-trend indicates that productivity of skilled resources will need to increase dramatically in order to respond to market demands and changing demographic

Reduce Expense

• Softening market and other competitive pressure require reduced cost of operations

• Once a new baseline is established on reduced labor from global sourcing – pressure will move to automation – removing labor costs entirely

Mega-trend indicates that operational innovations will be required to maintain bottom line competitiveness – especially in the face of outside entrants into market

IncreaseAgility

Technological advances are allowing for increasing innovations in product design and expectations

Mega-trend indicates that traditional claims operations will not be able to support “processing as usual” as carriers will have to rapidly change and modify their operations to support new and innovative products and product lines

Agents

Customers

Out

put M

anag

emen

t

Process Choreography and Management

Business logic, business specific functions, data, employeesIT-Infrastructure

Agents

Customers

@

Telephone

Internet

On-

site

Sup

port

Self

Serv

ice

Back Office

1st Level(CSR)

2nd Level(Specialist)

On-

site

Sup

port

Self

Serv

ice

Inpu

t Man

agem

ent

@

Telephone

Internet

Automation

Operations of the Future Solution ConceptService Orientation enables a transformation from document centric workflows – to completely automated processing of

inbound mail, e-mail, calls, and faxes

Core Insurance SolutionCore Insurance SolutionCore Insurance Solution

3rd Party

Filenet

ProviderAgentConsumer

PhoneWeb MailE-Mail

PhoneWeb MailE-Mail

Insurance Self

Service Solution

Insurance Insurance Self Self

Service Service SolutionSolution

Input Management

Scan and Interpret Inbound work

tasks

Dynamic Folder

Organize & Manage Work Folder Content

Output Mgmt

Process Work Task Output

Process Mgmt

Monitor processes and tasks

TeamLead

Lev 1 Emp.

Lev 2 Emp

Work Management

Assign and Route Work Tasks

Manager

Insurance Operations of the Future Solution – Asset View

Disability Claim Services

PLM Services

NAVAServices

Auto ClaimServices

NAVA ATP

“Lights Out”Automation of Documents

PLM ATP

“Lights Out”Automation of Documents

Disability Claim ATP

“Lights Out”Automation of Documents

Pers Auto Claim ATP

Automated Processing of Work Tasks

Traditional WF

Automated

Manual Work Tasks

IBM Asset

IBM Business Partner

In Development

SWG Offering

In POCIn POC

Available TodayAvailable Today

Solution OutlineSolution Outline

Available through Business PartnerAvailable through Business Partner

Available Through Business PartnerAvailable Through Business Partner

Insurance Operations of the Future: POC Operational View

The Benefits of a Strategic Transformation through Tactical Deployments

Today, the typical insurer may automate 10 to 15% of their tasks. By moving this to 70% - which appears reasonable by applying Service Orientation – this could result in as much as 66% operational

costs reduction

Type of Work

Fully Automated Tasks

Simple / CSR Tasks

Manual / Advanced Tasks

% of Work

15

40

45

100%

Cost

15

1000

2250

$3,265

% of Work

70

20

10

100%

Cost

70

500

500

$1,070

An example of a task is the work required to process an inbound piece of mail. It would also include tasks resulting from emails, Web interactions, and phone calls

Items are relative: Automated = $1; CSR Tasks = $25; Specialist Tasks = $50

Note: Numbers are not sourced to a commissioned study – they reflect observations and projections from customer experience but are not yet referenceable

Current State Future State

Solution Applications

• Mail Room Operations:– Streamline operations and automate sorting, indexing, and routing

• Mature File Net Operations:– Move from document handling automation to lights out processes– Automated indexing and routing

• Workforce Management– Automated / Optimized assignment of tasks from multiple channels (eMail, Phone, Web,

Mail, etc.)

• Straight Through Processing for:– Auto Claims and Claims Payments– Straight Through Policy Processing– Customer Service Requests

• Dynamic Folder:– Renewal processing– Claim processing – Complex commercial lines

• Output Management– Automated document generation (Thunderhead)

BPM Solutions & IBM

Wave chart from Forrester

Industry Domain Models

BPM and Industry Expertise

Leverage expertise and pre-built industry solution accelerators

Accelerate Your Success with BPM

Industry Content Packs

Optimize measurement management frameworkOptimize business processes in real time

Export first-level Business Process Execution Language (BPEL) Install/configure business process manage-ment system (BPMS) runtime environmentChoreograph processes across applica-tions and SOA services

Develop future business processesDevelop new organizationDevelop KPIsPerform process benchmarkingSimulate future business processesDevelop high-level service model

Assess and document current business processesAssess current IT and current organizationDocument current business rulesAnalyze process capability gaps

Evaluate current business strategyReview and evaluate strategic objectivesSelect opportunities/projects for improvement

Optimize measurement management frameworkOptimize business processes in real time

Export first-level Business Process Execution Language (BPEL) Install/configure business process manage-ment system (BPMS) runtime environmentChoreograph processes across applica-tions and SOA services

Develop future business processesDevelop new organizationDevelop KPIsPerform process benchmarkingSimulate future business processesDevelop high-level service model

Assess and document current business processesAssess current IT and current organizationDocument current business rulesAnalyze process capability gaps

Evaluate current business strategyReview and evaluate strategic objectivesSelect opportunities/projects for improvement

Process governance

ExecuteDefine OptimizeAssessEnvision

Processgovernance

Execute

Assess

Optim

ize Defin

e

Envision

CBMBusinessComponents

EnablingPlatform

SOA BusinessServices andApplications

DistributionDistribution

ProcessingProcessing

CampaignExecution

Correspondence

SmartRouting

Dialogue Handler

CaseHandling

Sales FinancialsConsolidation

MarketInformation

AdvertisingCampaigns

ApplicationsRelationshipManagement

In-boundCall Center

Service/Sales

Admin.

LocalBranchAdmin.

TellerServices

Channel/Distribution

Mgmt.

CustomerContactHandler

Self-serviceChannel

ProductDirectoryMarketing Inventory

Management

RewardsManagement

MerchantOperations

ProductManagement

FundManagement

RetailSecurities

PortfolioTrading

OTCServices

ProductDevelopment& Deployment

Production &Operations

Management

RetailLending

(Mortgages)

SecuritiesMarket

Analysis

ApplicationProcessing

CustomerProfile

Contact/Event History

Collections& Recovery

Recon-ciliations

OperationsAdministration

FinancialCapture

Payments CustomerAccount

Billing

Authorizations ProductProcessing

AllianceAdministration

Wireroom(S.W.I.F.T.)

DocumentManagement

Deposits(DDA)

Statements

AcquisitionAdministration

ConfirmationsContract Notes

ServicingManagement

PortfolioAdministration

ProductTracking

CustodyAdministration

Settlements

Valuations

CollateralHandling

Trading(Back Office)

Trading(Front Office)

MarketResearch

Alliance &Authority Mgmt

BusinessArchitecture

AcquisitionPlanning

BusinessUnit Tracking

Fixed AssetRegister

CustomerPortfolio &Analysis

CustomerBehavior& Models

BusinessAnd Resource

Planning

CustomerServicing &

Sales Planning

SegmentAnalysis &Planning

CreditManagement

Treasury

FinancialControl

Securitization

RiskManagement

Branch CashInventory

FinancePolicies

LoanSyndication

BusinessPolicies &

Procedures

Audit/Assurance/

Legal

AccountingGeneralLedger

CustomerAccounting

Policies

Asset &Liability Policy

& Planning

CustomerCreditAdmin.

ConsolidatedBook/PositionMaintenance

Insi

ght

Business Management

Risk and Financial

Managem

ent

Business Management

Manufacturing

CBMBusinessComponents

EnablingPlatform

SOA BusinessServices andApplications

DistributionDistribution

ProcessingProcessing

CampaignExecution

Correspondence

SmartRouting

Dialogue Handler

CaseHandling

Sales FinancialsConsolidation

MarketInformation

AdvertisingCampaigns

ApplicationsRelationshipManagement

In-boundCall Center

Service/Sales

Admin.

LocalBranchAdmin.

TellerServices

Channel/Distribution

Mgmt.

CustomerContactHandler

Self-serviceChannel

ProductDirectoryMarketing Inventory

Management

RewardsManagement

MerchantOperations

ProductManagement

FundManagement

RetailSecurities

PortfolioTrading

OTCServices

ProductDevelopment& Deployment

Production &Operations

Management

RetailLending

(Mortgages)

SecuritiesMarket

Analysis

ApplicationProcessing

CustomerProfile

Contact/Event History

Collections& Recovery

Recon-ciliations

OperationsAdministration

FinancialCapture

Payments CustomerAccount

Billing

Authorizations ProductProcessing

AllianceAdministration

Wireroom(S.W.I.F.T.)

DocumentManagement

Deposits(DDA)

Statements

AcquisitionAdministration

ConfirmationsContract Notes

ServicingManagement

PortfolioAdministration

ProductTracking

CustodyAdministration

Settlements

Valuations

CollateralHandling

Trading(Back Office)

Trading(Front Office)

MarketResearch

Alliance &Authority Mgmt

BusinessArchitecture

AcquisitionPlanning

BusinessUnit Tracking

Fixed AssetRegister

CustomerPortfolio &Analysis

CustomerBehavior& Models

BusinessAnd Resource

Planning

CustomerServicing &

Sales Planning

SegmentAnalysis &Planning

CreditManagement

Treasury

FinancialControl

Securitization

RiskManagement

Branch CashInventory

FinancePolicies

LoanSyndication

BusinessPolicies &

Procedures

Audit/Assurance/

Legal

AccountingGeneralLedger

CustomerAccounting

Policies

Asset &Liability Policy

& Planning

CustomerCreditAdmin.

ConsolidatedBook/PositionMaintenance

Insi

ght

Business Management

Risk and Financial

Managem

ent

Business Management

Manufacturing

Key Agility Indicators

BPM Methodologies

Industry Best Practices

Industry models and best practices

IBM Benchmark Wizard

People

Applications

Information

Agent

Customer

Loss Adjuster

CallCentre CSR People

Applications

Information

Agent

Customer

Loss Adjuster

CallCentre CSR

Over 2850 BPMcustomers in over 30 countries and growing

#1 in BPMS market shareMarket leading products

Deep industry knowledge and pre-built assets

Largest partner ecosystem

Global reach and scale

BPM from IBM Delivers Unrivaled Customer Value