bournemouth - essential 6-monthly finance directors' update - november 2017

TRANSCRIPT

James Robinson, Corporate

Partner

Chair’s welcome

Housekeeping

@pkfFrancisClark

#FDSeminar17

The Role of the FD

Finance

Custodian

Operational

Leadership

Execution

Insig

ht

ServiceChange Finance

Overs

ight

Friendly Food Ltd - background

• Niche luxury pet product business

• Makes and sells expensive treats for pets

• Historically UK only through pet shops

• Started as food treats but now also toys and accessories

• Rapid expansion through web sales

• Expanding overseas in US, China and Northern Europe

• Owned by Kat (85%) and Fred (15%) – they are unrelated

• Kat is looking to retire in the next 2 years, Fred within 5 years

• Second tier management are strong

• They may have some overseas employees in the near future

• Manufacturing and refrigerated storage is energy intensive

www.website.com

Fred the FD

Finance

Custodian

9/10

Operational

8/10

Leadership

7/10

Execution

6/10

Overs

ight

Insig

ht

ServiceChange

Friendly Food Ltd - financials

FY18

Budget

£’000

FY17

Actual

£’000

FY16

Actual

£’000

FY15

Actual

£’000

Sales 33,000 24,000 19,000 16,000

Gross profit 12,000 9,000 7,500 6,500

GPM 36% 37% 39% 41%

Net profit 1,900 1,400 1,100 1,000

Net margin 5.8% 5.8% 5.9% 6.3%

Cash 5,400 3,600 2,500 1,500

Net assets 7,900 6,100 5,000 4,000

P+L reserves 7,800 6,000 4,900 3,900

Programme

Topic Speaker FD role

Financial reporting

update

Tim Lannin Custodian

Cyber security Richard

Wilding

Custodian

Topical VAT issues Simon Anslow Operational

Brexit John Endacott Leadership

Business tax update Lisa

Whitbread

Leadership

Auto enrolment &

payroll update

Aimee

Raymond

Operational

Energy & sustainability Andrew Killick Execution

Management buy out Paul Stout Execution

8

Tim Lannin, Senior Manager

Financial reporting update

Programme

• FRS 102.2: what to expect from the

forthcoming update

• Keeping on top of intercompany

accounts

• Spotlight on share buybacks

• PSCs: are you making notifications on

time?

FRS 102.2: Where are we now?

FRS 102

• Current version

FRED 67

• Incremental improvements

FRS 102.2

• Periods beginning 1/1/19 onwards

Summary of expected changes

• Policy choice introduced: fair value or depreciated cost

• Option to use FV as deemed cost on transition rather than prior period reversal of value

Intra group property rental

• Removal as part of accounting policy process

• Example impact: must split mixed use property between investment and operating elements

Undue cost and effort

• Confirms exemption from discounting for loans TO small companies by director-shareholders and their close families

• No extension to non-small entities or intra group loans

Non-market rate loans

Summary of expected changes

• Relaxation of separate recognition of intangibles on acquisition

• Separation is policy decision on first acquisition –choose wisely

Goodwill and intangibles

• New description of “basic” (non FV) financial instrument to support detailed conditions

Financial instruments

• Reintroduction of Net Debt reconciliation

• No separate key management personnel compensation when only KMPs are directors

Disclosure changes

Forthcoming changes under IFRS

• Periods beginning on or after 1 January 2018

• Requires detailed analysis of contracts to determine when and how much turnover to recognise

• Restatement of prior year profit in some cases

IFRS 15: Revenue

• Periods beginning on or after 1 January 2019

• Requires lessees to bring all leases on balance sheet

• Restatement of prior year balance sheet and associated profit impact

IFRS 16:

Leases

Illustrative example: IFRS 16 impact

Current rules £000s IFRS 16 £000s

Property plant and

equipment

2,500 Includes future

lease obligations

4,250

Current assets 3,500 3,500

Current liabilities (3,000) Includes 12 months

lease rentals

(3,350)

Net current assets 500 150

Non- current

liabilities

(1,500) Includes 4 years

lease rentals

(2,900)

Net worth 1,500 1,500

Note to accounts

Operating lease

commitment

(5 years x £350k)

1,750

15

UK to IFRS convergence?

• Originally FRC proposed triennial reviews of

FRS 102 (2019,2022,2025 etc)

• Now awaiting practical implementation

experience of IFRS 15 and 16 before

reviewing

• FRS 102 not intended to mirror IFRS exactly

or automatically

• Watch this space….

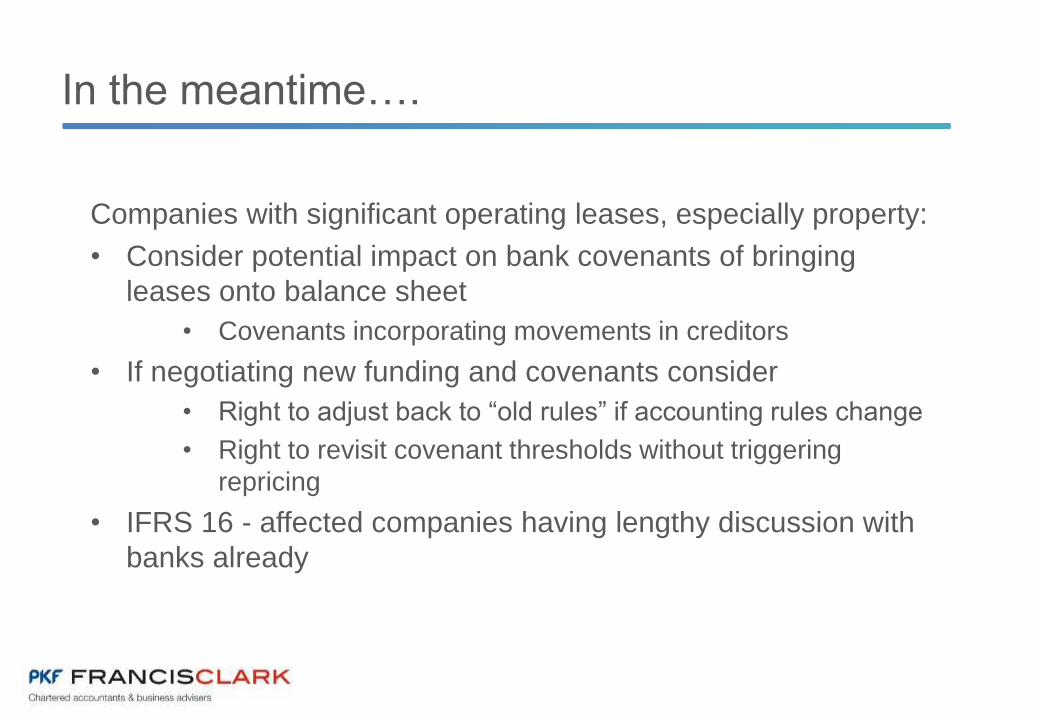

In the meantime….

Companies with significant operating leases, especially property:

• Consider potential impact on bank covenants of bringing

leases onto balance sheet

• Covenants incorporating movements in creditors

• If negotiating new funding and covenants consider

• Right to adjust back to “old rules” if accounting rules change

• Right to revisit covenant thresholds without triggering

repricing

• IFRS 16 - affected companies having lengthy discussion with

banks already

www.website.com

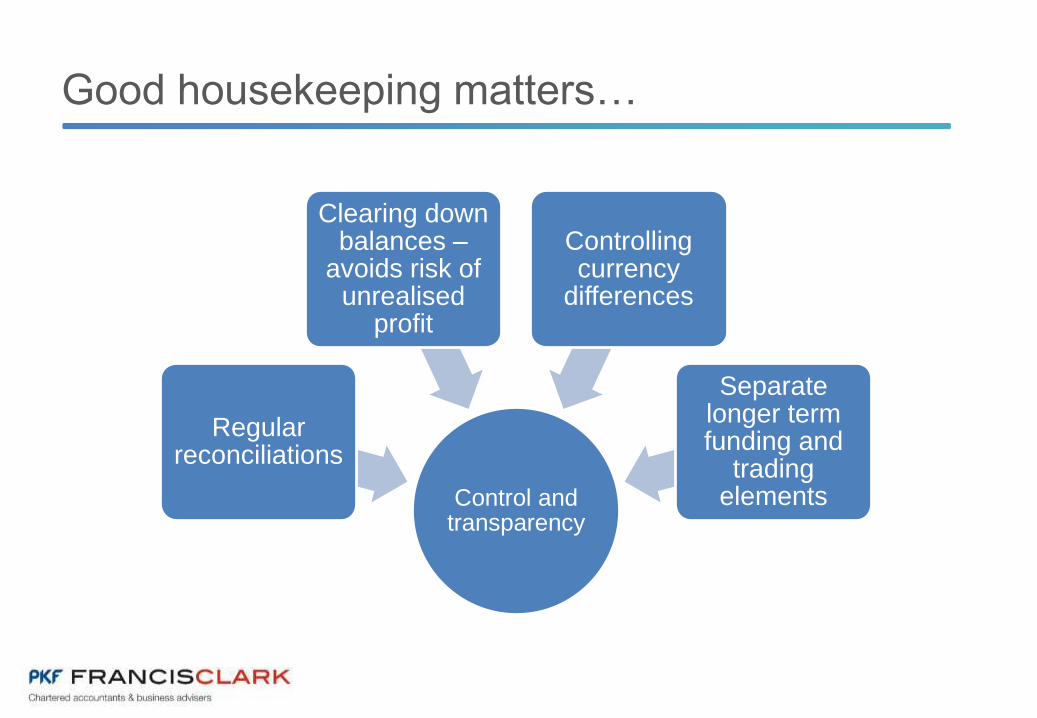

Keeping on top of intercompany accounts

• Interdependence of many group companies

• Efficient use of cash and resources

• Tax mitigation via management charges

• “Housekeeping” tips

• Intra group waivers – points to watch

Good housekeeping matters…

Control and transparency

Regular reconciliations

Clearing down balances –

avoids risk of unrealised

profit

Controlling currency

differences

Separate longer term funding and

trading elements

Intra-group waivers

• Formal release from liability, not provision for doubtful debt

• On reorganisation, before disposal of subsidiary

• To reflect reality of investment by parent

• Recognition in accounts when release occurs

• Plan in advance

• Documentation

Intra group waiver: parent to subsidiary

In parent’s books

• Dr Cost of investment

• Cr Intra group debtor

Note – may need to consider impairment of investment balance if NAV of subsidiary < cost of investment

In subsidiary’s books

• Dr Intra group creditor

• Cr Reserves

Note – generally accepted practice is that waiver of loan is form of capital contribution therefore cannot include in profit for the year

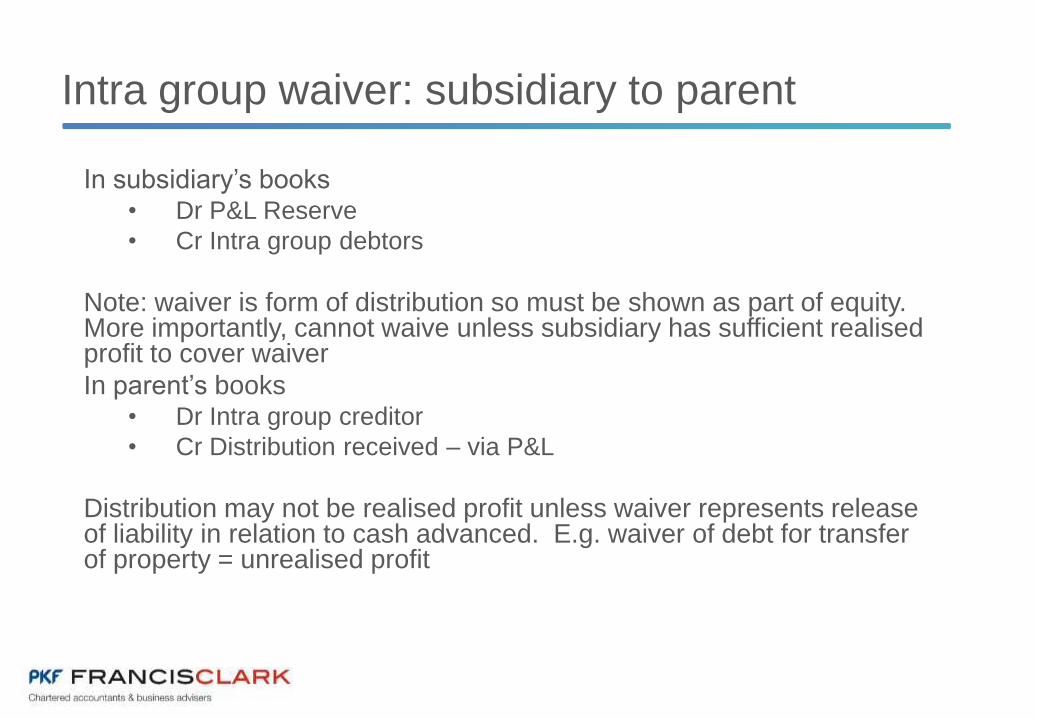

Intra group waiver: subsidiary to parent

In subsidiary’s books• Dr P&L Reserve

• Cr Intra group debtors

Note: waiver is form of distribution so must be shown as part of equity. More importantly, cannot waive unless subsidiary has sufficient realised profit to cover waiver

In parent’s books• Dr Intra group creditor

• Cr Distribution received – via P&L

Distribution may not be realised profit unless waiver represents release of liability in relation to cash advanced. E.g. waiver of debt for transfer of property = unrealised profit

www.website.com

Spotlight on share buybacks

• Mandatory redemption or ad hoc repurchase

• Contractual, take out minority shareholder, provide partial exit route for majority shareholder

• Key legal requirements

• Distributable (realised) profit

• Capital Redemption Reserve

• Consequences for failures in process

• Penalties for late filing

• Ineffective buyback – impact on disposal of company!

Sufficient distributable profit?

Last annual accounts £000s Distributable?

Share capital 50 No

Share premium 2,000 No

Revaluation reserve 2,700 Only if distribution

involves revalued asset

Profit and loss account

(includes £900k fair

value gains)

1,350 £450k – yes

£900k – probably not

Shareholders’ funds 6,100

Also consider:

1. performance since last annual accounts

2. Changes to accounting policy or adjustments affecting opening

reserves

Company wants to buy back 10,000 shares for £500,000

What if insufficient distributable profit?

Which is most

appropriate?

Dividend up from subsidiary

Capital reduction (share premium, CRR)

Bonus issue from revaluation

reserve, then capital reduction

Capital redemption reserve

• Potential consequence of buyback or repurchase

• Hold uncancelled shares in “treasury” – separate debit line

on balance sheet

• Cancel shares

• Nominal value of cancelled shares is transferred to Capital

Redemption Reserve

• Applies irrespective of where shares were classified on the

balance sheet i.e. as debt or equity

Illustrative example: buyback with capital

reduction

£000s Capital

reduction

Revised

balance sheet

Buyback £000s

Net assets 6,100 6,100 (500) 5,600

Share capital 50 50 (10) 40

Share premium 2,000 (1,000) 1,000 1,000

Revaluation reserve 2,700 2,700 2,700

Capital redemption

reserve

10 10

Profit and loss

account – realised

450 1,000 1,450 (500) 950

Profit and loss

account - unrealised

900 900 900

Shareholders’ funds 6,100 6,100 5,600

Company wants to buy back 10,000 shares for £500,000

27

PSC notifications

Persons with significant control

• From 26 June – “events driven” notification

• Update PSC register within 14 days of

change

• Notify registrar within further 14 days

(forms PSC01-09)

• Notification via Annual Confirmation

Statement has ceased

• Importance of updating share register

promptly for changes - prima facie evidence

of title to shares, dividend entitlement etc

www.website.com

Audit reports

• Revised format for periods beginning on or

after 17 June 2016

• Reordered and expanded wording

• Specific reference to going concern where

no issues….

• See example handout

29

Tim Lannin, Senior Manager

Financial reporting update

30

Richard Wilding, Head of cyber

security

Cyber Security

Cyber Crime is growing

• Cyber criminals have huge technical

know-how. Far superior to most

legitimate businesses.

• Businesses are often oblivious to the

threat that results from their lack of

cyber security.

• A company doesn’t have to have a

transactional website to be vulnerable.

• Many SME’s possess intellectual

property that has significant financial

value to cyber criminals

Current risks and threats

Current examples:

• AA, NHS, Deloitte hack, Equifax

• Ransomware, malware, fictitious e-

mails, requests for changes to master

files

www.website.com

Fred the FD as custodian

• Fred is concerned about cyber

security and its risk

• Fred feels he should do something

and would like some more comfort

• Awareness/training, policies/controls

and audit

Awareness and training

• Human error is often the weak link

• Establish a staff induction process (not a one

off exercise)

• Maintain user awareness of the security risks

faced by the organisation

• Monitor the effectiveness of security training

www.website.com

Controls/policies

Policies Controls

Produce a user security

policy

Include in employment

contracts

Online payments

Supplier detail changes

Passwords

Giving the company and FD comfort/assurance

• Cyber Essentials

• Cyber Essentials PLUS

• IASME accreditation

Cyber Essentials

• Self-assessment questionnaire for the company to complete

• Covers 5 key areas/71 questions

• We provide upfront assistance (1.5 days needed) to support how to complete and progress

• It is submitted via a secure portal for us to assess

• Basic vulnerability scan performed

• Assessor feedback provided

• Once successful can use the Cyber Essentials logo for 12m

• Limited insurance provided/can help reduce further cyber insurance

Cyber Essentials PLUS

• We audit and test the 5 key control areas

• Includes detailed vulnerability and limited penetration

testing

• A report is then issued

• Once successful can use the Cyber Essentials PLUS

logo for 12m

• Can help to reduce cyber insurance further

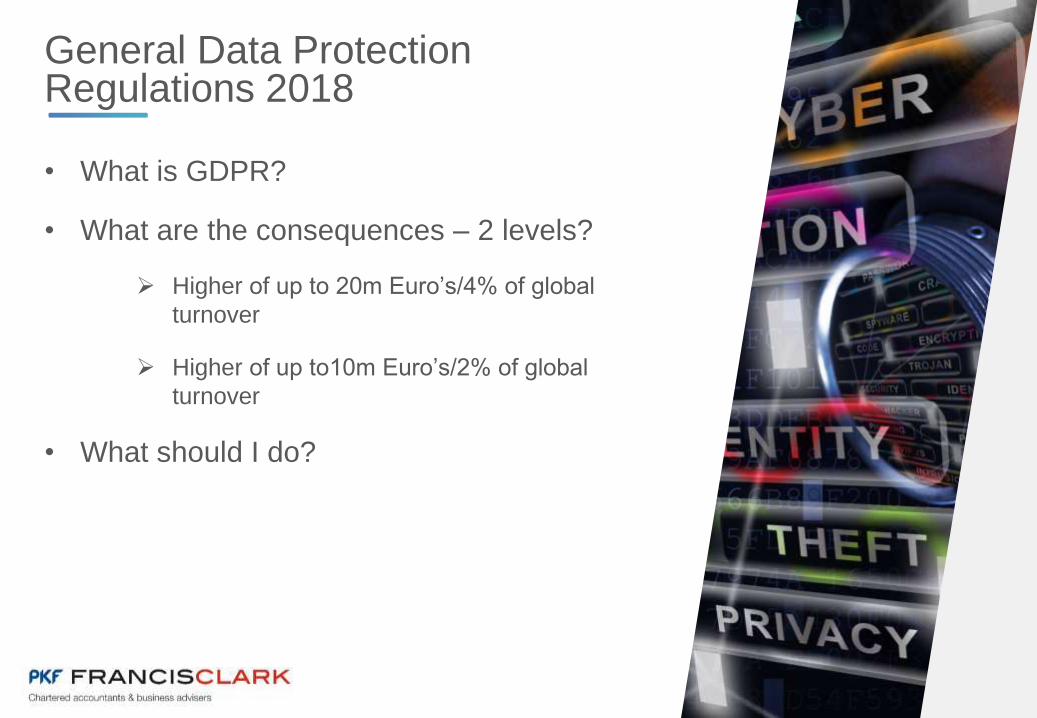

General Data Protection Regulations 2018

• What is GDPR?

• What are the consequences – 2 levels?

Higher of up to 20m Euro’s/4% of global

turnover

Higher of up to10m Euro’s/2% of global

turnover

• What should I do?

IASME (Information Assurance for Small and Medium Enterprises)

• IASME – two levels standard and gold

• 180 questions (including those in Cyber Essentials)

• Includes GDPR specific questions

• Akin to ISO27001

• A report is then issued

• Once successful can use the IASME logo for 12m

www.website.com

Next steps

• See brochure in pack

• Complete form

• 5 December cyber event

• Contact your PKF Francis Clark adviser or

e-mail: [email protected]

42

Richard Wilding, Head of cyber

security

Cyber Security

Simon Anslow, VAT Partner

VAT update

VAT

“It is a matter of life and death, a

road either to safety or to ruin.

Hence it is the subject of inquiry,

which can on no account be

neglected”

- Sun Tzu, The Art of War

VAT

“I think I got it wrong again…”

- Dick Emery, Actor, comedian,

philosopher

46

VAT - Agenda

• What’s new? What’s changed?

• Top 10 Tips, Tricks, Twists & Trips…in 20 mins!!

• Whisper it…Brexit

www.website.com

VAT – What’s New?

Disbursements

• Brabners case

• Re-charge of e-search fees

• No VAT on cost

• Re-charged to customer with no VAT

• HMRC view: component of taxable supply

• Tribunal agreed

• Assessment upheld £78k

• History relevant to legal firms, BUT…principles are generic

VAT – What’s New?

Disbursements (cont.)

So what is a disbursement?

• Agent is authorised & acting for client in paying 3rd party

• Client actually receives & uses the goods/services

• Client is responsible for paying the 3rd party

• Client aware that goods/services being provided by 3rd party

• Agent’s outlay must be separately itemised, and…

• Must recover only the exact amount paid to 3rd party

• Goods/services must be clearly additional to agent’s supplies

49

VAT – What’s New?

Disbursements (cont.)

How does this affect me?

• Be clear as to whether cost is

component or addition

• Where qualifies, either:

o Gross in/gross out; or

o Reclaim/recharge VAT

• Issues only when treatment changes: In

→ Out

www.website.com

VAT – What’s New?

Goods vs Services

• Mercedes Benz Financial Services CJEU case

• ‘Agility’ optional purchase scheme

• Agreement end – options:

o Purchase car (final payment)

o Return Car

o Commence new agreement

• Found:

o C. 40% final payment to purchase

o C. 50% customers opted to purchase

51

VAT – What’s New?

Goods vs Services (cont.)

• Historic treatment:

o Supply of goods

o FULL VAT due at outset

• Ruling:

o Supply of services

o VAT due on each payment

• Impact

o VAT cash-flow → Supplier

o VAT recovery (part) → Customer…?...NO!!

VAT – Top 10 Tips, Tricks, Twists & Trips

1. Business Mileage

• Pence Per Mile (PPM) Paid for business mileage

• HMRC accept proportion as ‘fuel’

• AA tables can be used…or

• Apply 1/3rd !*

• VAT recoverable @ 1/6th

• Fuel receipts should be retained…

• Can go back four years

*100% where company car

www.website.com

1. Business Mileage - Example

• Friendly Food Ltd:

o 40 sales staff

o Avge 15,000 business miles each pa.

o Mileage rate @ 45ppm

• VAT recovery:

VAT = 15,000 x 40 x £0.45 x 1/3rd x 1/6th

VAT = £15,000

VAT – Top 10 Tips, Tricks, Twists & Trips

VAT – Top 10 Tips, Tricks, Twists & Trips

2. EU Trade

Friendly Foods…now selling into Europe

• Distance Sellingo Non-VAT registered EU customers

o UK VAT; BUT

o Register & charge EU VAT if > threshold in calendar year

o Threshold varies per EU country €35k or €100k

• Distribution Depotso Move Own goods to EU warehouses/stock hotels

o Distribute from EU locations

o EU VAT registration required!!

VAT – Top 10 Tips, Tricks, Twists & Trips

3. Imports

Friendly Foods…importing from outside the EU

• Deferment Account

• Simplified Import VAT Accounting (SIVA)

• Inward Processing Relief (IPR)

• Customs Warehousing

• Binding Tariff Information (BTI)

VAT – Top 10 Tips, Tricks, Twists & Trips

4. Bad Debt Relief…and Creditors

Bad Debt Relief (BDR)

• VAT recoverable:

o Debtors > 6m old

o Write-off to a VAT BDR a/c

• BUT:

o VAT must have been originally accounted for

o Debt must not have been paid, sold or factored

o Adjust for any subsequent receipts

57

4. Bad Debt Relief…and Creditors

Creditors…the sting in the tail!

• VAT repayable:o Creditors > 6m old

o Irrespective of whether supplier has claimed BDR

• BUT:o VAT can be reclaimed if debt settled

WARNING HMRC are getting really hot on this one!!

VAT – Top 10 Tips, Tricks, Twists & Trips

VAT – Top 10 Tips, Tricks, Twists & Trips

5. Request For Payments

• Time of supply – services:

o Basic – when performed; or

o Issue of invoice; or

o Receipt of payment

• BUT NO ‘Basic’ Tax Point where:

o Ongoing/continuous services

o Long-term project/periodic payments

Consider: ‘Request For Payments’ (RFP)

www.website.com

5. Request For Payments

• RFPo Looks like an invoice…

o But omits key features (VAT # etc.)

Prompts payment

Initial significant VAT saving

Ongoing VAT cash-flow

BDR by default

X Increase administration

X Possible negative customer reception

VAT – Top 10 Tips, Tricks, Twists & Trips

VAT – Top 10 Tips, Tricks, Twists & Trips

6. Partial Exemption

• VAT Recovery

Taxable supplies √

Exempt supplies X

• Mixed supplies

o Attribute costs

o Apportion ‘mixed use’ costs

o De-minimis & NO restriction if Exempt Input VAT (pa):

< 7,500 and

< Total Input VAT

61

6. Partial Exemption

• Beware ‘non-standard’ Exempt Activity e.g.:o Finance/insurance income

o Property letting/sales

Friendly Foods…letting unused warehouse• Exempt income

• VAT on refurb./operational costs?

• De-minimis?

• If not, restriction!

• …or Opt To Tax?

VAT – Top 10 Tips, Tricks, Twists & Trips

VAT – Top 10 Tips, Tricks, Twists & Trips

7. Preregistration Input VAT

• Goods

o Up to 4 years < registration

o On hand at date of registration

o Purchased by the registered entity

o HMRC backed down on ‘depreciation’ argument

• Services

o Up to 6 months < registration

o Cannot have been ‘consumed’ < registration

Can be issues with partially exempt businesses

VAT – Top 10 Tips, Tricks, Twists & Trips

8. Z/R Certificates

• Charities

o Medical equipment

o Relevant goods

o Certain building adaptions

o Advertising services

• Buildings

o Relevant Residential Purpose

• Ships

o Qualifying vessels (supply/repair/maintenance)

VAT – Top 10 Tips, Tricks, Twists & Trips

9. Transfer Of Going Concern (TOGC)

• VAT-free sale of business, IF:

o Business or part of a business

o Capable of operating as such

o Similar business

o No immediately consecutive transfers

o No significant break in trading

o Must be registered or liable to be

www.website.com

9. Transfer Of Going Concern (TOGC)

Beware:

• A → B → C ≠ TOGC

• Land & Property

o Opted & new commercial properties

o Capital Goods Scheme

o Property letting

• VAT charged…OR NOT CHARGED

• Registration!

VAT – Top 10 Tips, Tricks, Twists & Trips

VAT – Top 10 Tips, Tricks, Twists & Trips

10. Reverse Charges

Services received ex-UK – no VAT but:

• VAT Registered Businesses:

o Reverse charge applies

o May not be entitled to full recovery

• Non-VAT Registered Businesses:

o If value exceeds threshold (currently £85k pa)…

o VAT registration required

o …and may not be entitled to recovery

VAT – Top 10 Tips, Tricks, Twists & Trips

+ VAT! Cars vs. Commercials

When is a car not a car?

When it’s a commercial…

‘Car’ ≠ Payload ≥1 Tonne

Consider twin-cab pick up AND reclaim the VAT!!

Friendly Foods…Fred & Kat both drive Porsches…

Bye-bye Porsche…hello Mitsubishi L200!!

VAT – Brexit

What happens post-March 2019?!

• VAT will still exist in the UK!

• Adoption of all current UK/EU law…

• …but with more flexibility

VAT

Remember, always

look beneath the

tip of the iceberg

What?

For whom?

When?

Where?

… and for how much?

Who?

Simon Anslow, VAT Partner

VAT update

71

John Endacott, Partner & Head of Tax

Brexit – what should you

be doing now?

PKF FC Brexit team leaders

Stuart Rogers, Head of International Tax

Liam Dushynsky, Customs Specialist

Change management –

contingency planning

• Brexit – known unknowns & unknown unknowns

• FDs need to show leadership, execute changes & consider operational impact

• How could Brexit impact your business?

• What are the possible options & opportunities for your business?

• Risk management

74

Brexit possibilities

• No Brexit

• Exit March 2019 - no deal with EU

• Exit March 2019 - same terms as now (WTO

approved free trade arrangement)

• Transitional period from March 2019 –

probably on same terms as now

www.website.com

Impact on business

• Impact on sales, direct costs &

overheads?

• Consider:

• Tariff impact – imports/exports

• Exchange & interest rates

• Subsidies

• Labour supply

• Border logistics

• Restrictive practices

• Likelihood of impact?

• Timescales for change?

Operations management

• Supply chain options

• Sales & costs – both in the EU or neither in the EU

• Does Inward Processing Relief help?

• Manage exchange rate risk?

• Contractual risks?

• Financial impact if outsourced arrangement fails?

• Transport, storage & ports - do you need AEO status?

(https://www.gov.uk/guidance/authorised-economic-operator-certification)

www.website.com

What should you be doing now?

• Have contingency plans & team in place

• Explore all options

• Have alternatives

• Watch long term commitments & legal

undertakings

• Get in early as HMRC may not be able to

cope

• Be prepared for opportunities

78

John Endacott, Partner & Head of Tax

Brexit – what should you

be doing now?

Coffee Break

Lisa Whitbread, Tax Consultant

Business tax update

Business tax

• The liberalisation of substantial shareholdings

exemption

• Group vs parallel company structuring

• Corporate loss changes and restriction

• Corporate interest restriction

Substantial shareholding exemption (SSE)

• Exemption of certain gains

• Major changes effective 1 April 2017

• Historically restricted to trading groups

• Extended to include investment groups

• No impact on other areas of tax law

• No change to the specific issue regarding FA2011 changes

Substantial shareholding exemption (SSE)

Key Criteria Pre 1 April 2017

Post 1 April 2017

10% ordinary share capital Yes Yes

Minimum twelve month holding period in two years prior to sale

Yes 2 yrs now 6

Target is a trading company before Yes Yes*

Target is a trading company after Yes No*

Disponor is a trading company or holding company of a trading group before

Yes No

Disponor is a trading company or a holding company of a trading group after

Yes No

Group vs Parallel?

• During growth – typically group structure

• Access to group relief

• Access to SSE – reinvest profits tax free

• Continued status as a trading group

• Commercial strength

• Banking requirements / cross guarantees

Group vs parallel company structuring

Hold co

(Friendly

Food Ltd)

Trade co1 Trade co2

Fred

Friendly Food Ltd disposes of Trade co2 and

claims SSE

Friendly Food Ltd pays

a dividend to Fred,

taxable at up to 38.1%

Friendly Food Ltd

reinvests proceeds tax

free into group

www.website.com

Group v parallel company

structuring

Trade co1 Trade co2

FredFred disposes of Trade co2

and are taxed at CGT rates

(20% / 10%)

Demerge?

• Transition from group to parallel?

• (Largely) tax free demergers

• Statutory demerger (a distribution in specie)

• Non statutory demerger

• Complex transactions

• Accounting implications

• Advance planning a must

Why Demerge?

• The sale of only part of the group is likely thus demerging

enables proceeds to be paid directly to the shareholders.

• Splitting of commercial risk and isolating high risk activity

from low risk – “protect the crown jewels”.

• Splitting ownership of the group into separate

entities/groups to resolve shareholder dispute

• To assist with family succession – different parts of the

business to be owned and operated by different family

members

• Preserving trade related tax reliefs on the trading arm of

the group by removing investment activity

Corporate tax losses -pre and post April 2017 losses

• Pre and post April 17 losses to be split

• Post April 17 losses – offset against profits on

group basis

• Pre April 17 losses – subject to old rules

• Choice on what to use in priority

• Transitional rules will create some complexity

• Increased compliance burden

www.website.com

Corporate tax losses £5m deduction allowance

• UK company's / groups entitled to £5m ‘deductions allowance’

• Exceed allowance – only 50% profits are reduced by b/f losses

• Large b/f losses & large profits –unexpected CT

• Transitional rules – review opening year positon

• Allocation of the £5m allowance

Corporation tax lossesExample – Friendly Food Limited

Loss memo

Brought forward loss £10m

Against CY profit (£5m)

Against CY profit (£1m)

Carry forward £4m

www.website.com

Corporate interest restriction

• OECD BEPS driven

• Applies if net interest expense of ≥ £2m

• Fixed ratio rule - 30% of Tax EBITDA

• Group ratio rule (by election)

• Interest not deducted is carried forward

Corporate interest restrictionWho will be affected?

• Highly leveraged groups

• Members of multinational groups

• Private equity owned companies / groups

• Property investment / capital intensive

• Companies expanding by acquisition

Autumn Budget 2017

• Government wants (needs) to raise more tax revenue

• Tax clampdown on freelancers using personal service

companies

• Patient Capital Review – announcements expected on

EIS/SEIS etc

• How long will favourable capital tax reliefs last?

• This and more will be picked up at our Spring Tax

Update.

Lisa Whitbread, Tax Consultant

Business tax update

96

Aimee Raymond, Financial

Planning Consultant

Auto Enrolment &

Payroll Update

Agenda

• Contribution Increases

• Cyclical Re-enrolment

• Developments

• Reviewing your existing scheme

• NOW:Pensions

• Payroll Outsourcing

• Questions

Contribution Increases

• Minimum contribution rates increase on 6 April 2018

• and again on 6 April 2019

• The minimum rates may differ slightly if an alternative salary definition has been adopted. The Pension Regulator website provides full details;

http://www.thepensionsregulator.gov.uk/en/employers/phasing-calculating-contributions-using-different-elements-of-pay.aspx

Date

From

Minimum

Employer

Contribution

Staff

Contribution

Minimum Total

Contribution

Current 1% 1% 2%

April 2018 2% 3% 5%

April 2019 3% 5% 8%

www.website.com

Cyclical Re-enrolment

• ‘Re-enrolment’ has to be carried out every 3 years

• flexibility on the date you select to complete the process

• ‘Eligible’ staff (between age 22 and state pension age and earning above £10,000p.a.) who opted out of pension scheme previously will have to be re-enrolled

• A re-declaration of compliance has to be made to the Pension Regulator

100

• October 2017 - 5th anniversary of Auto Enrolment

• All existing employers subject to duties by February 2018

• New employers must start duties as soon as they start paying staff

• ‘Master Trust Assurance Framework’ voluntary standard

• The Pension Schemes Act 2017 - stronger regulation of master trusts

• With experiences it is now possible to review;

investment performance

service levels

scheme governance/financial stability

charges

• Significant differences in scheme provider offerings –not all good

Developments

www.website.com

Reviewing your existing scheme

• An important employee benefit

• Staff recruitment and retention

• Review for continued suitability

• Scheme providers successes and failures -some Master Trusts have already closed

• Poor performance, or scheme closure detrimental to the employers affected

• Significant hassle to rectify closed scheme

• Unsettling for your employees

NOW:Pensions – a failing scheme?

• Historic poor service levels - to employers and employees

• Contributions not allocated correctly

• Member charges increasing to £1.50 per month from April 2018

• Removed from the Master Trust Assurance Framework

• Large financial losses – £16.6 million loss related to £1.3 million revenue in 2016

• NOW:Pensions suggest members with small preserved funds transfer to alternative scheme

• Francis Clark Financial Planning Ltd can review your existing AE scheme and recommend the best way forward

103

Outsourcing Payroll &

AE Administration

Risk Areas of Payroll Compliance

• Real Time Information, Auto

Enrolment, Gender Pay Gap

reporting and Apprenticeship

Levy – Government changes to

legislation

• GDPR– May 2018

• Fines imposed on the employer

• In-house costs

• Responsibility and anxiety of

providing this.

Outsourcing costs may pleasantly surprise you!

105

Fear of outsourcing

• Loss of control

• Concerns on data protection

• Incorrect or late payments

• Inadequate reports

• Errors not corrected

You authorise the payroll and payments

Personalised reports

Dedicated team of professionals providing

support

www.website.com

Benefits of outsourcing

• Skilled payroll professional processing your

payroll

• Ensure compliance with legislation

• Business Intelligent reports

• Employees paid on time and accurately

• Neutralising compliance risks

107

Health Check

• Review of internal processes and software

• Review of data processed to date

• Advice on correcting potential risk

• Advice on how to stay compliant with

legislation

• Implement contingency plan

• Guidance on completing the re-enrolment

process

• Skilled payroll professional contact

108

Aimee Raymond, Financial

Planning Consultant

Auto Enrolment &

Payroll Update

109

FD seminars - Market changes Q4 2017

Energy

Andrew Killick, Corporate Finance Partner

110

www.website.com

1. Manage costs: Corporate PPAs

2. Leverage estate: On site generation and storage

3. Create investment income

• Owning generation assets

• Demand side response

Combatting energy costsQ4 2017

Transforming a variable cost into an opportunity

111

Projects seeking fixed price power price agreements (“PPA”s)

• Large number of new projects seeking offtake agreements

• No requirement for physical relationship

Benefits of a corporate PPA to you

• Price stabilisation and potential cost savings

• Achieve sustainability and decarbonisation objectives

• Provide additionality

Recent UK examples

Corporate PPAsQ4 2017

112

www.website.com

New projects being constructed despite subsidy cuts

Proximity to the grid is key

Investment case is strengthened by co-location

On-site generationQ4 2017

Emergence of subsidy free generation

Relevance to Friendly Foods Ltd

Deliver attractive investment return

Enable private PPA with generating asset

Delivering significant reduction to annual energy cost

113

Energy storageQ4 2017

Need driven by increase in UK intermittent generation

Developers seeking sites with good access to grid

Units typically the size of a shipping container

Opportunity to generate additional revenue

Options for Friendly Foods Ltd

Rental income* Investment return*

Rental model £20k-£50k p.a Rent only

Self develop £400-£500k/MW >10%

* Numbers are for illustrative purposes only and will be site specific

114Demand side responseQ4 2017

Being smarter about how and when we use energy

By managing the timing your power demand you can receive payments for this flexibility

Example – Sainsbury’s smart refrigeration system

Relevance to Friendly Foods Ltd

Become part of a virtual power station

Responding to frequency response demands and earning income:

Managing refrigeration demand

Managing heating demand

115

Increased price of secondary assets due to limited supply

Index linked returns for up to 25 years

• Onshore wind and solar investment returns – 6-7%

• Higher for Biomass/EfW

Removal of subsidies requires the supply chain to adjust

Energy infrastructure investmentQ4 2017

Relevance to Friendly Foods Ltd

Utilise surplus cash to deliver >6-7% return

Scope to include within the pension plan

Assets qualify for Business Property Relief

116

FD seminars - Market changes Q4 2017

Energy

Andrew Killick, Corporate Finance Partner

MBO / alternative to a full

business sale

Paul Stout, Corporate Finance Director

Objectives of today

Exploring future plans of business owners in

order to allow business continuity

• Kat looking to retire in 2 years

• Fred within 5 years

Alternatives to sale:

- Share buyback

- MBO’s

1. What is an MBO?

2. Why an MBO maybe preferred over a full

sale?

3. How to fund an MBO?

What is a MBO?

• Purchase of a business by its management

• Allows management to participate in equity and

success

• Management are purchasing future cash flows

• Value is realised through exit, either trade sale…or

secondary MBO!

• Types - Vendor backed MBO, FAMBO

• Once in a lifetime opportunity

www.website.com

Why is a MBO preferred over a 100%

sale?

• Price – Trade does not always result in

higher value

• Flexibility on timing of exit (for Kat)

• Enables de-risking with possible upside

investment

• May allow for continued involvement

• Confidentiality maintained

• Allows for non-financial considerations

• Incentivises and rewards management

• Less Warranties and Indemnities

Friendly Food Limited

Friendly

Food Ltd

FredKat

15%

Valuation

2017 (Adjusted EBITDA) £2m

Profit Multiple 6

Enterprise Value £12m

Add Property £4m

Less Debt (£6m)

Equity Value £10m

Kat Selling 60% £6m

Kat roll over 25% £2.5m

Fred roll over 15% £1.5m

85%

Example Structure

NewCo

Kat FredA N

Other

Friendly

Food Ltd

Value - £10m

Kat

£6m

Funding

60%25%

Friendly Food

Ltd

FredKat

15%85%

A N

Other

A N

Other

5%5% 5%

Kat

www.website.com

How we can help

• Assisting owners and managers overcome

potential lack of awareness of options

• Team has undertaken >100 MBOs

• Assist with initial feasibility report

• Optimum structure for all (valuation, payment

terms, tax considerations)

• Favourable environment for MBOs

• Assist with business plan / projections

• Aware of active funders and terms

Making sure the right deal is secured for the

management team and owner in a timely manner

MBO / alternative to a full

business sale

Paul Stout, Corporate Finance Director

James Robinson, Corporate Partner

Chair’s close

Dates for the diary

FD seminars June 2018

• Plymouth – Monday 11 June, Boringdon Park Golf Club

• Exeter – Wednesday 13 June, Exeter Racecourse

• Bournemouth – Thursday 14 June, AFC Bournemouth

• Bodmin – Tuesday 19 June, Lanhydrock Golf & Country Club

• Taunton – Wednesday 20 June, Somerset County Cricket Club (tbc)

Disclaimer & copyright

c) copyright PKF Francis Clark, 2017

You shall not copy, make available, retransmit, reproduce, sell, disseminate, separate, licence, distribute, store electronically, publish, broadcast or otherwise circulate either within your business or for public or commercial purposes any of (or any part of) these materials and / or any services provided by PKF Francis Clark in any format whatsoever unless you have obtained prior written consent from PKF Francis Clark to do so and entered into a licence.To the maximum extent permitted by applicable law PKF Francis Clark excludes all representations, warranties and conditions (including, without limitation, the conditions implied by law) in respect of these materials and /or any services provided by PKF Francis Clark. These materials and /or any services provided by PKF Francis Clark are designed solely for the benefit of delegates of PKF Francis Clark. The content of these materials and / or any services provided by PKF Francis Clark does not constitute advice and whilst PKF Francis Clark endeavours to ensure that the materials and / or any services provided by PKF Francis Clark are correct, we do not warrant the completeness or accuracy of the materials and /or any services provided by PKF Francis Clark; nor do we commit to ensuring that these materials and / or any services provided by PKF Francis Clark are up-to-date or error or omission-free. Where indicated, these materials are subject to Crown copyright protection. Re-use of any such Crown copyright-protected material is subject to current law and related regulations on the re-use of Crown copyright extracts in England and Wales.These materials and / or any services provided by PKF Francis Clark are subject to our terms and conditions of business as amended from time to time, a copy of which is available on request.Our liability is limited and to the maximum extent permitted under applicable law PKF Francis Clark will not be liable for any direct, indirect or consequential loss or damage arising in connection with these materials and / or any services provided by PKF Francis Clark, whether arising in tort, contract, or otherwise, including, without limitation, any loss of profit, contracts, business, goodwill, data, income or revenue. Please note however, that our liability for fraud, for death or personal injury caused by our negligence, or for any other liability is not excluded or limited.

PKF Francis Clark is a trading name of Francis Clark LLP. Francis Clark LLP is a limited liability partnership, registered in England and Wales with registered number OC349116. The registered office is Sigma House, Oak View Close, Edginswell Park, Torquay TQ2 7FF where a list of members is available for inspection and at www.pkf-francisclark.co.uk. The term ‘Partner’ is used to refer to a member of Francis Clark LLP or to an employee. Registered to carry on audit work in the UK and Ireland, regulated for a range of investment business activities and licensed to carry out reserved legal activity of non-contentious probate in England and Wales by the Institute of Chartered Accountants in England and Wales. Partners acting as insolvency practitioners are licensed in the UK by the Institute of Chartered Accountants in England and Wales. A partner appointed as Administrator or Administrative Receiver acts only as agent of the insolvent entity and without personal liability. Francis Clark LLP is a member firm of the PKF International Limited network of legally independent firms and does not accept responsibility or liability for the actions or inactions on the part of any other individual member firm or firms.